Posts tagged ‘Larry Fink’

Fink & Capitalism: Need 4 Kitchens in Your House?

Do you need four kitchens in your house? Apparently financial industry titan Larry Fink does. If Mr. Fink were a designer for millionaire homeowners, he would advise them to use their millions to build more kitchens in their house (reinvest) rather than distribute those monies to family members (dividends) or use that money to pay back an equity loan from mom and dad for the down payment (share buybacks). Essentially that is exactly what is happening in the stock market. Companies that are generating record profits and margins (millionaires) are increasingly choosing to pay out larger percentages of profits to stockholders (family members) in the form of rising dividends and share buybacks. Contrary to Mr. Fink’s belief, corporate America is actually doing plenty with room additions, landscaping, and roof replacements – I will describe more later.

As a consequence of corporate America’s increasingly shareholder friendly practices of returning cash, Fink believes this trend will stifle innovation and long-term growth in American companies. Here’s a snapshot of the supposed dividend/buyback problem Mr. Fink describes:

Source: Financial Times

Fink Mails Letter from Soapbox

For those of you who do not know who Larry Fink is, he is the successful Chairman and CEO of BlackRock Inc. (BLK), an investment manager which oversees about $4.65 trillion in investment assets. Mr. Fink ignited this recent financial controversy when he jumped on his soapbox by mailing letters to 500 CEOs lecturing them on the importance of long-term investing. What is Mr. Fink’s beef? Fink’s issues revolve around his belief that CEOs and corporations are too short-term oriented.

In his letter, Mr. Fink had this to say:

“This pressure [to meet short-term financial goals] originates from a number of sources—the proliferation of activist shareholders seeking immediate returns, the ever-increasing velocity of capital, a media landscape defined by the 24/7 news cycle and a shrinking attention span, and public policy that fails to encourage truly long-term investment.”

He goes on to bolster his argument with the following:

“More and more corporate leaders have responded with actions that can deliver immediate returns to shareholders, such as buybacks or dividend increases, while underinvesting in innovation, skilled workforces or essential capital expenditures necessary to sustain long-term growth.”

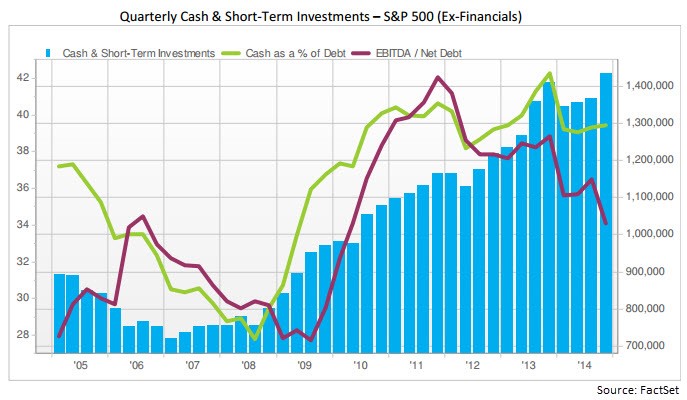

What Mr. Fink does not say in his letter is that large, multinational S&P 500 corporations driving this six-year bull run are sitting on a record hoard of cash, exceeding $1.4 trillion (see chart below). In this light, it should come as no surprise that CEOs are forking over more cash to investors in the forms of dividends and share repurchases.

What’s more, despite Fink’s assertion that share buybacks and dividends are killing innovation, he also fails to mention in his letter that 2014 capital expenditures of $730 billion are also at a record level. That’s right, CAPEX has not been cut to the bone as he implies, but rather risen to all-time highs.

It’s true that generationally low (and declining) interest rates have accelerated the pace of dividends/repurchases, however dividend payout ratios (the percentage of profits distributed to shareholders) of about 32% remain firmly below the long-term payout ratio of approximately 54% (see chart below) – see also Dividend Floodgates Widen. I find it difficult to fault many companies doing something with the gargantuan piles of inflation-losing cash anchoring their balance sheets. Don’t cash-rich companies have a fiduciary duty to borrow reasonable amounts of near-0% debt today (see Bunny Rabbit Market) in exchange for share buybacks currently providing returns of about 5.5% (inverse of 18x P/E ratio) and likely yielding 7%+ returns five years from now?

Source: Financial Times

The “Short-Term” Poster Child – Apple

There is no arguing that excessive debt eventually can catch up to a company. Our multi-year expanding economy is eventually due for another recession in the coming years, and there will be hell to pay for irresponsible, overleveraged companies. With that said, let’s take a look at the poster child of “short-termism” according to Mr. Fink …Apple Inc. (AAPL).

Of the roughly $500 billion in buybacks spent by S&P 500 companies in 2014, Apple accounted for approximately $45 billion of that figure. On top of that, CEO Tim Cook and his board generously decided to return another $11 billion to shareholders in the form of dividends. Has this “short-term” return of capital stifled innovation from the company that has launched iPhone version 6, iPad, Apple Watch, Apple Pay, and is investing into exciting areas like Apple Television, Apple Car, and who knows what else?

To put these Apple numbers into perspective, consider that last year Apple spent over $6 billion on research and development (R&D); $10 billion on capital expenditures; and hired over 12,000 new full-time employees. This doesn’t exactly sound like the death of innovation to me. Even after doling out roughly -$28 billion in expenditures and -$56 billion in dividends/share repurchases, Apple was amazingly able to keep their net cash position flat at an eye-popping +$141 billion!

Mr. Fink abhors “activist shareholders seeking immediate returns” but rather than deriding them perhaps he should send the greedy, capitalist Carl Icahn a personal thank you letter. Since Icahn’s vocal plea for a large Apple share buyback, the shares have skyrocketed about +85%, catapulting BlackRock’s ownership value in Apple to over $19 billion.

With respect to these increasing outlays, Mr. Fink also notes:

“Returning excessive amounts of capital to investors—who will enjoy comparatively meager benefits from it in this environment—sends a discouraging message.”

This would be true if investors took the dividends and stuffed them under their mattress, but an important message Mr. Fink neglects to address as it relates to dividends and share buybacks is demographics. There are 76 million Baby Boomers born between 1946 – 1964 and a Boomer is turning age 65 every 8 seconds. With many bonds trading at near 0% yields (even negative yields) it is no wonder many income starving retirees are demanding many of these cash-rich corporations to share more of the growing spoils via rising dividends.

Capitalism Works

After looking at a few centuries of our country’s history, one of the main lessons we can learn is that capitalism works – especially over the long-run. With about 200 countries across the globe, there is a reason the U.S. is #1…we’re good at capitalism. As our economy has matured over the decades, it is true our priorities and challenges have changed. It is also true that other countries may be narrowing the gap with the U.S., due to certain advantages (e.g., demographics, lower entitlements, easier regulations, etc), but the U.S. will continue to evolve.

In many respects, capitalism is very much like Darwinism – corporations either adapt with the competition…or they die. I repeatedly hear from pessimists that the U.S. is in a secular state of decline, but if that’s the case, how come the U.S. continues to dominate and innovate in major industries like biotechnology, mobile technology, networking, internet, aviation, energy, media, and transportation? Quite simply, we are the best and most experienced practitioners of capitalism.

Certainly, capitalism will continue to cultivate cyclical periods of excess investment/leverage and insufficient regulation. But guess what? Investors, including the public, eventually lose their shirts and behaviors/regulations adjust. At least for a little while, until the next period of excess takes hold. If Apple, and other balance sheet healthy companies allocate capital irresponsibly, capital will flow towards more aggressive and innovative companies. BlackBerry Limited (BBRY) knows a little bit about the consequences of cutthroat competition and suboptimal capital allocation.

While I emphatically share Mr. Fink’s focus on long-term investing values (including his self-serving tax reform ideas), I vigorously disagree with his attacks on shareholder friendly actions and his characterization of rising dividends/buybacks as short-term in nature. In fact, increasing dividends and share buybacks can very much coexist as a long-term investment and capital allocation strategy.

The question of proper capital allocation should have more to do with the age of a company. It only makes sense that younger companies on average should reinvest more of their profits into growth and innovation. On the other hand, more mature S&P 500-like companies will be in a better position to distribute higher percentages of profits to shareholders – especially as cash levels continue to rise to record levels and leverage remains in check.

BlackRock’s Larry Fink may continue to urge CEOs to reinvest their growing cash hoards into superfluous corporate kitchens, but Sidoxia and other prudent capitalist investors will continue to exhort CEOs to opportunistically take advantage of near-free borrowing rates and responsibly share the accretive gains with shareholders. That’s a message Mr. Fink should include in a letter to CEOs – he can use BlackRock’s lofty, above-average dividend to cover the cost of postage.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including AAPL and iShares ETFs, but at the time of publishing, SCM had no direct position in BLK, BBRY or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Retirement Epidemic: Poison Now or Later?

We live in an instant gratification society. The house, the car, and annual vacation take precedence over contributions to retirement and savings accounts. It therefore comes as no surprise to me that Americans spend more time on planning for vacation than they do on planning for retirement.

Given the choice of spending or saving, Americans in large part choose, “spend now, save later.” Or in other words, Americans choose to drink $10 margaritas now (spend) and swallow the more expensive poison (save) later. Spending now and saving later sounds good in theory until you reach your mid-60s and realize you’re going to have to work as a Wal-Mart Stores (WMT) greeter into your 80s while eating cat food in your tent.

To make matters worse, you don’t have to be a genius to see irresponsible government spending and globalization has compromised the health of our countries entitlements (Social Security and Medicare). Benefits are likely to be reduced over time and age eligibility requirements are likely to increase. If you fold in the dynamic of exploding healthcare costs and broad-based inflationary pressures, one can quickly realize savings habits need to change. The traditional model of working for 40 years and then relying on a pension and Social Security payments to cover a blissful multi-decade retirement just doesn’t apply to current reality. On top of the disappearance of plump pensions, life expectancy is rising (around 80 years in the U.S.), so the realistic risk of outliving your savings has a larger probability of occurring.

Surely I am overly dramatizing the situation by sounding the investing alarm bells out of self-interest…right? Wrong. As a geeky, financial numbers guy, I can objectively rely on numbers, and the statistics aren’t pretty.

Here’s a sampling:

- Empty Savings Cupboard: A 2013 study by the Employee Benefit Research Institute found that nearly half of workers had less than $10,000 saved, and according to Blackrock Inc (BLK), CEO, Larry Fink, the average American has saved only $25,000 for retirement

- Food Stamp Living: Almost half of middle-class workers, will be forced into a poor retirement lifestyle, living on a food budget of about $5 a day.

- 401(k) Will Not Save the Day: Compared to other forms of savings, the average 401(k) balance reached $89,300 at the end of 2013 – that’s the good news. The bad news is that only about half of all companies offer their employees 401(k) benefits, and for the approximately 60 million people that participate, about a fourth withdraw these 401(k) funds before retirement – out of necessity or for frivolous reasons. Even if you cheerily accept the size of the average balance, sadly this dollar amount is still massively deficient in meeting retirement needs. It’s believed that your savings should approximate 15-20 times your annual retirement expenses that aren’t covered by outside sources of income, such as social security or a pension.

If these figures aren’t scary enough to get you saving more, then just use common sense and understand the future is very uncertain. A 2012 New York Times article sarcastically captured how easy it is to plan for retirement:

First, figure out when you and your spouse will be laid off or be too sick to work. Second, figure out when you will die. Third, understand that you need to save 7 percent of every dollar you earn. (30 percent of every dollar [if you are 55 now].) Fourth, earn at least 3 percent above inflation on your investments, every year. (Easy. Just find the best funds for the lowest price and have them optimally allocated.) Fifth, do not withdraw any funds when you lose your job, have a health problem, get divorced, buy a house or send a kid to college. Sixth, time your retirement account withdrawals so the last cent is spent the day you die.

What to Do?

The short answer is save! Simplistically, this can be achieved in one of two ways: cut expenses or raise income. I won’t go into the infinite ways of doing this, but adjusting your mindset to live within your means is probably the first necessary step for most.

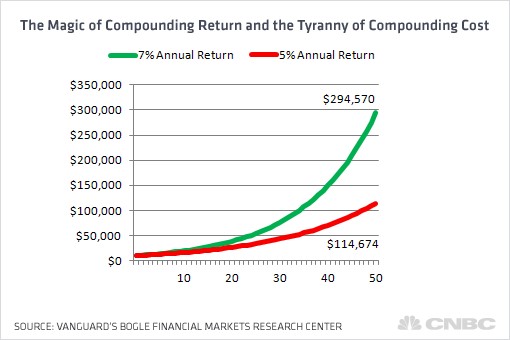

As it relates to your investments, fees should be your other major area of focus. The godfather of passive investing, Jack Bogle, highlighted the dramatic impact of fees on retirement savings. As you can see from the chart below, the difference between making 7% vs. 5% over an investing career by reducing fees can equate to hundreds of thousands of dollars, and prevent your nest egg from collapsing 2/3rd in value.

Source: CNBC

Lastly, if you are going to use an investment advisor, make sure to ask the advisor whether they are a “fiduciary” who legally is required to place your interests first. Sidoxia Capital Management is certainly not the only fiduciary firm in the industry, but less than 10% of advisors operate under this gold standard.

Investing and saving is a lot like dieting…easy to understand the concept but difficult to execute. The numbers speak for themselves. Rather than dealing with a crisis in your 70s and 80s, it’s better to take your poison now by investing, and reap the rewards of your hard work during your golden years.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), and WMT, but at the time of publishing SCM had no direct discretionary position in BLK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}