Posts tagged ‘John Mauldin’

Predictions – A Fool’s Errand

Making bold predictions is a fool’s errand. I think Yogi Berra summed it up best when he spoke about the challenges of making predictions:

“It’s tough to make predictions, especially about the future.”

While making predictions might seem like a pleasurable endeavor, the reality is nobody has been able to consistently predict the future (remember the 2012 Mayan Doomsday?), besides perhaps palm readers and Nostradamus. The typical observed pattern consists of a group of well-known forecasters bunched in a herd coupled with a few extreme outliers who try to make a big splash and draw attention to themselves. Due to the law of large numbers, a few of these extreme outlier forecasters eventually strike gold and become Wall Street darlings…until their next forecasts fail miserably.

Like a broken clock, these radical forecasters can be right twice per day but are wrong most of the time. Here are a few examples:

Peter Schiff: The former stockbroker and President of Euro Pacific Capital has been peddling doom for decades (see Emperor Schiff Has No Clothes). You can get a sense of his impartial perspective via Schiff’s reading list (The Real Crash: America’s Coming Bankruptcy, Financial Armageddon, Conquer the Crash, Crash Proof – America’s Great Depression, The Biggest Con: How the Government is Fleecing You, Manias Panics and Crashes, Meltdown, Greenspan’s Bubbles, The Dollar Crisis, America’s Bubble Economy, and other doom-instilled titles.

Meredith Whitney: She made an incredible bearish call on Citigroup Inc. (C) during the fall of 2007, alongside her accurate call of Citi’s dividend suspension. Unfortunately, her subsequent bearish calls on the municipal market and the stock market were completely wrong (see also Meredith Whitney’s Cloudy Crystal Ball).

John Mauldin: This former print shop professional turned perma-bear investment strategist has built a living incorrectly calling for a stock market crash. Like perma-bears before him, he will eventually be right when the next recession hits, but unfortunately, the massive appreciation will have been missed. Any eventual temporary setback will likely pale in comparison to the lost gains from being out of the market. I profiled the false forecaster in my article, The Man Who Cries Bear.

Nouriel Roubini: This renowned New York University economist and professor is better known as “Dr. Doom” and as one of the people who predicted the housing bubble and 2008-2009 financial crisis. Like most of the perma-bears who preceded him, Dr. Doom remained too doom-ful as the stock market more than tripled from the 2009 lows (see also Pinning Down Roubini).

Alan Greenspan: The graveyard of erroneous forecasters is so large that a proper summary would require multiple books. However, a few more of my favorites include Federal Reserve Chairman Alan Greenspan’s infamous “Irrational Exuberance” speech in 1996 when he warned of a technology bubble. Although directionally correct, the NASDAQ index proceeded to more than triple in value (from about 1,300 to over 5,000) over the next three years. – today the NASDAQ is hovering around 6,100.

Robert Merton & Myron Scholes: As I chronicled in Investing Caffeine (see When Genius Failed), another doozy is the story of the Long Term Capital Management hedge fund, which was run in tandem with Nobel Prize winning economists, Robert Merton and Myron Scholes. What started as $1.3 billion fund in early 1994 managed to peak at around $140 billion before eventually crumbling to a capital level of less than $1 billion. Regrettably, becoming a Nobel Prize winner doesn’t make you a great predictor.

Words From the Wise

Rather than paying attention to crazy predictions by academics, economists, and strategists who in many cases have never invested a penny of outside investor money, ordinary investors would be better served by listening to steely investment veterans or proven prediction practitioners like Billy Beane (minority owner of the Oakland Athletics and subject of Michael Lewis’s book, Moneyball), who stated the following:

“The crime is not being unable to predict something. The crime is thinking that you are able to predict something.”

Other great quotes regarding the art of predictions, include these ones:

“I can’t recall ever once having seen the name of a market timer on Forbes‘ annual list of the richest people in the world. If it were truly possible to predict corrections, you’d think somebody would have made billions by doing it.”

-Peter Lynch

“Many more investors claim the ability to foresee the market’s direction than actually possess the ability. (I myself have not met a single one.) Those of us who know that we cannot accurately forecast security prices are well advised to consider value investing, a safe and successful strategy in all investment environments.”

–Seth Klarman

“No matter how much research you do, you can neither predict nor control the future.”

–John Templeton

“Stop trying to predict the direction of the stock market, the economy or the elections.”

–Warren Buffett

“In the business world, the rearview mirror is always clearer than the windshield.”

–Warren Buffett

In the global financial markets, Wall Street is littered with strategists and economists who have flamed out after brief bouts of fame. Celebrated author Mark Twain captured the essence of speculation when he properly identified, “There are two times in a man’s life when he should not speculate: when he can’t afford it and when he can.” Instead of attempting to predict the future, investors will avoid a fool’s errand by simply seizing opportunities as they present themselves in an ever-changing world.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Dow 20,000 – Braking News or Breaking News?

Investors from around the globe excitedly witnessed the Dow Jones Industrial Average index break the much-anticipated 20,000 level and set a new all-time record high this week. The question now becomes, is this new threshold braking news (time to be concerned) or breaking news (time to be enthused)? The true answer is neither. While the record 20,000 achievement is a beautifully round number and is responsible for a bevy of headlines splashing around the world, the reality is this artificial 20,000 level is completely arbitrary.

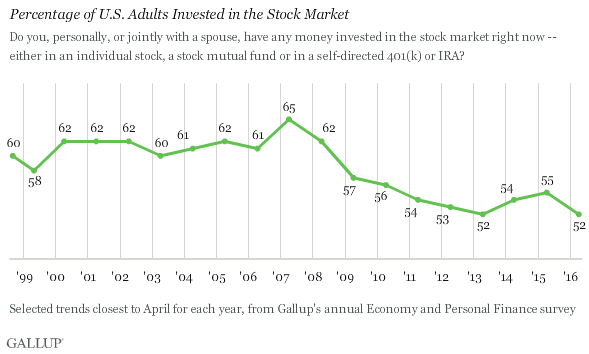

Time will tell whether this random numeric value will trigger the animal spirits of dispirited investors, but given all the attention, it is likely to jolt the attention span of distracted, ill-prepared savers. Unfortunately, the median family has only saved a meager $5,000 for retirement. For some years now, I have highlighted that this is the most hated bull market (see The Most Hated Bull Market Ever), and Gallup’s 2016 survey shows record low stock ownership, which also supports my view (chart below). Trillions of dollars coming out of stock funds is additional evidence of investors’ sour mood (see fund outflow data).

While investors have been selling stocks for years, record corporate profits, trillions in share buybacks, and trillions of mergers and acquisitions (in the face of a weak IPO market) have continually grinded stock prices to new record highs.

Pessimism Sells

The maligned press (deservedly so in many instances) has been quick to highlight a perpetual list of dread du jour. The daily panic-related topics do however actually change. Some days it’s geopolitical concerns in the Middle East, Russia, South China Sea, North Korea, and Iran and other days there are economic cries of demise in China, Brazil, Venezuela, or collapse in the Euro. And even when the economy is doing fine (unemployment rate chopped in half from 10%, near full employment), the media and talking heads often supply plenty of airtime to impending spikes of crippling inflation or Fed-induced string of choking interest rate increases.

I fondly look back on my articles from 2009, and 2010 when I profiled schlocks like Peter Schiff (see Emperor Schiff Has No Clothes) who recklessly peddled catastrophe to the masses. I guess Schiff didn’t do so well when he called for the NASDAQ to collapse to 500 (5,660 today) and the Dow to reach 2,000 (20,000 today).

Or how about the great forecaster John Mauldin who also piled onto death and destruction near the bottom in 2009 (see The Man Who Cries Wolf ). Here’s what Mauldin had to say:

“All in all, the next few years are going to be a very difficult environment for corporate earnings. To think we are headed back to the halcyon years of 2004-06 is not very realistic. And if you expect a major bull market to develop in this climate, you are not paying attention.” … “We are going to pay for that with a likely dip back into a recession.”

At S&P 856 (2,295 today) Mauldin added:

“This rally has all the earmarks of a major short squeeze…When the short squeeze is over, the buying will stop and the market will drop. Remember, it takes buying and lot of it to move a market up but only a lack of buying to create a bear market.”

Nouriel Roubini a.k.a. “Dr Doom” was another talking head who plastered the airwaves with negativity after the 2008-2009 financial crisis that I also profiled (see Pinning Down Roubini). For example, in early 2009, here’s what Roubini said:

“We are still only in the early stages of this crisis. My predictions for the coming year, unfortunately, are even more dire: The bubbles, and there were many, have only begun to burst.”

For long-term investors, they understand the never-ending doom and gloom headlines are meaningless noise. Legendary investor Peter Lynch pointed on on numerous occasions:

“If you spend more than 13 minutes analyzing economic and market forecasts, you’ve wasted 10 minutes.”

(see also Peter Lynch video)

The good news is all the media pessimism and investor skepticism creates opportunities for shrewd investors focusing on key drivers of stock price appreciation (corporate earnings, interest rates, valuations, and sentiment).

While the eternally, half-glass full media is quick to highlight the negatives, it’s interesting that it takes an irrelevant, arbitrary level to finally create a positive headline for a new all-time record high of Dow 20,000. Frustratingly, the new all-time record highs reached by the Dow in 2013, 2014, 2015, and 2016 were almost completely ignored (see chart below):

Source: Barchart.com

What happens next? Nobody knows for certain. What is certain however is that using the breaking news headlines of Dow 20,000 to make critical investment decisions is not an intelligent long-term strategy. If you, like many investors, have difficulty in sticking to a long-term strategy, then find a trusted professional to help you create a systematic, disciplined investment strategy. Now, that is some real breaking news.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Airbag Protection from Pundit Backseat Drivers

Giving advice to a driver from the backseat of a car is quite easy and enjoyable for some, but whether that individual is actually qualified to give advice is another subject. In the financial blogosphere and media there is an unending mass of backseat drivers recklessly directing investors off cliffs and into walls, but unfortunately there are no consequences for these blabbers. It’s the investors who are driving their personal portfolios that ultimately suffer from crashed financial dreams.

Unlike drivers who mandatorily require a license to drive to the local grocery store, bloggers, journalists, economists, analysts, strategists (aka “pundits”), and any other charismatic or articulate individual can emphatically counsel investors without any credentials, education, or licenses. More importantly than a piece of paper or letters on a business card, many of these self-proclaimed experts have little or no experience of investing real money…the exact topic the pundits are using to direct peoples’ precious and indispensable lifesavings.

It’s easy for bearish pundits like Peter Schiff, Nouriel Roubini, John Mauldin, and David Rosenberg (see also The Fed Ate My Homework) to throw economic hand grenades with their outlandishly gloomy predictions and fear mongering. However, more important than selling valuable advice, the pundit’s #1 priority is selling a convincing story, whether the story is grounded in reality or not. The pundit’s story is usually constructed by looking into the rearview mirror by creatively connecting current event dots in a way that may seem reasonable on the surface.

Crusty investors who have invested through various investment cycles know better than to pay attention to these opinions. As the saying goes, “Opinions are like ***holes. Everybody has one.” Stated differently, the great growth investor William O’Neil said the following:

“I would say 95% of all these people you hear on TV shows are giving you their personal opinion. And personal opinions are almost always worthless … facts and markets are far more reliable.”

Successful long-time investors like Warren Buffett rarely make predictions about the short-term directions of the market. Long-term investors know the only certainty in the market is uncertainty. At the core, investing is a game of probabilities. The objective of the game is to place your bets on those investments that establish the odds in your favor. As in many professions, however, the right process can have a negative outcome in the short-run. Those talented investors who have experience consistently applying a probabilistic approach generally do quite well in the long-run.

There is an endless multitude of investing advice, regardless of whether you choose to consume it over the TV, in newspapers, or through blogs. That’s why it’s so important to be discerning in your financial media consumption by focusing on experience…experience is the key. If you were to undergo a heart surgery, would you want a nurse or experienced doctor who had performed 2,000 successful heart surgeries? When you fly cross-country, do you want a flight attendant to fly the plane or a 20-year veteran pilot? I think you get the point.

The other factor to consider when comparing advice from a media pundit vs. experienced investor is skin in the game. Investment advisers who have their personal dollars at stake typically have spent a significantly larger amount of time formulating an investment thesis or strategy as compared to a loose-cannon TV journalist or inexperienced, maverick blogger.

There is a lot to consider as you maneuver your investment portfolio through volatile markets. With all the dangerous advice out there from backseat drivers, make sure you have experienced investment advice installed as protective airbags because listening to inexperienced air bags (pundits) could crash your portfolio into a wall.

Related Content: Financial Blogging Interview on Charlie Rose w/ Joe Weisenthal, Josh Brown, Felix Salmon, and Megan Murphy

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions in certain exchange traded fund positions, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Get Out of Stocks!*

Get out of stocks!* Why the asterisk mark (*)? The short answer is there is a certain population of people who are looking at alluring record equity prices, but are better off not touching stocks – I like to call these individuals the “sideliners”. The sideliners are a group of investors who may have owned stocks during the 2006-2008 timeframe, but due to the subsequent recession, capitulated out of stocks into gold, cash, and/or bonds.

The risk for the sideliners getting back into stocks now is straightforward. Sideliners have a history of being too emotional (see Controlling the Investment Lizard Brain), which leads to disastrous financial decisions. So, even if stocks outperform in the coming months and years, the sideliners will most likely be slow in getting back in, and wrongfully knee-jerk sell at the hint of an accelerated taper, rate-hike, or geopolitical sneeze. Rather than chase a stock market at all-time record highs, the sideliners would be better served by clipping coupons, saving, and/or finish that bunker digging project.

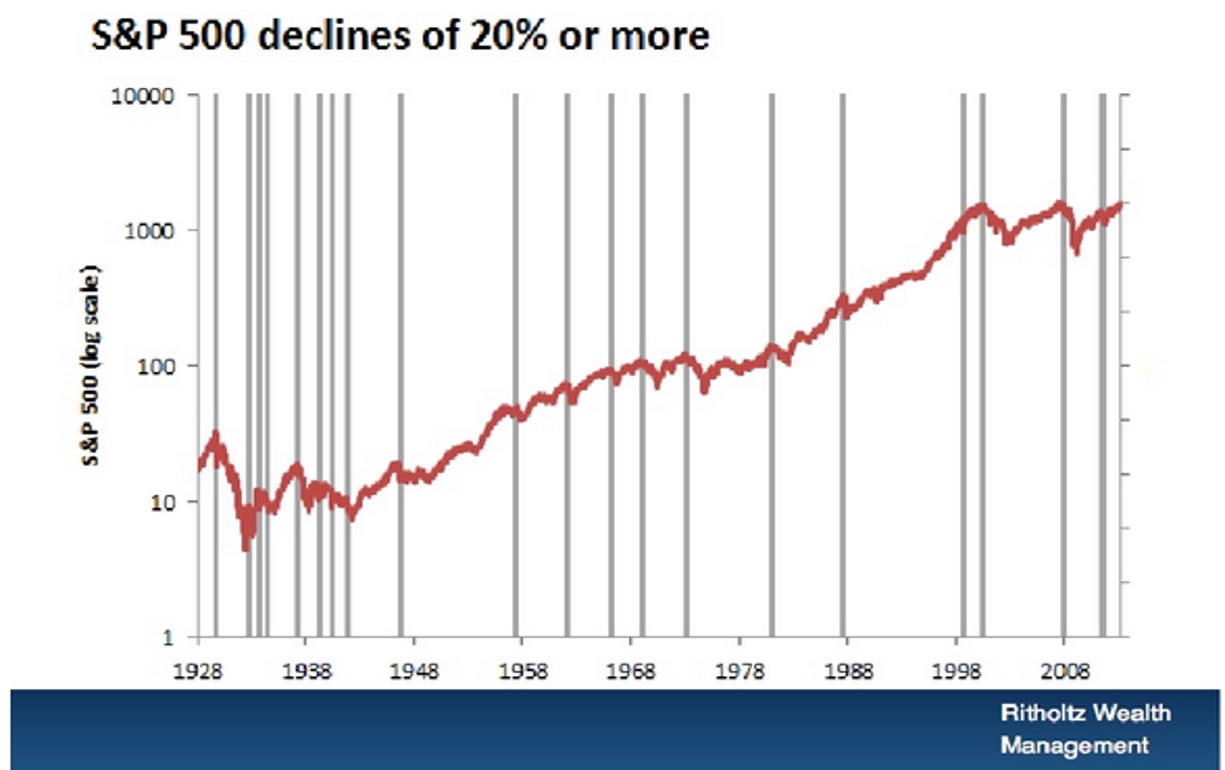

The fact is, if you can’t stomach a -20% decline in the stock market, you shouldn’t be investing in stocks. In a recent presentation, Barry Ritholtz, editor of The Big Picture and CIO of Ritholtz Wealth Management, beautifully displayed the 20 times over the last 85 years that the stocks have declined -20% or more (see chart below). This equates to a large decline every four or so years.

Strategist Dr. Ed Yardeni hammers home a similar point over a shorter duration (2008-2014) by also highlighting the inherent volatility of stocks (see chart below).

Stated differently, if you can’t handle the heat in the stock kitchen, it’s probably best to keep out.

It’s a Balancing Act

For the rest of us, the vast majority of investors, the question should not be whether to get out of stocks, it should revolve around what percentage of your portfolio allocation should remain in stocks. Despite record low yields and record high bond prices (see Bubblicious Bonds and Weak Competition, it is perfectly rational for a Baby-Boomer or retiree to periodically ring their stock-profit cash register, and reallocate more dollars toward bonds. Even if you forget about the 30%+ stock return achieved last year and the ~6% return this year, becoming more conservative in (or near) retirement with a larger bond allocation still makes sense. For some of our clients, buying and holding individual bonds until maturity reduces the risky outcome associated with a potential of interest rates spiking.

With all of that said, our current stance at Sidoxia doesn’t mean stocks don’t offer good value today (see Buy in May). For those readers who have followed Investing Caffeine for a while, they will understand I have been relatively sanguine about the prospects of equities for some time, even through a host of scary periods. Whether it was my attack of bears Peter Schiff, Nouriel Roubini, or John Mauldin in 2009-2010, or optimistic articles written during the summer crash of 2011 when the S&P 500 index declined -22% (see Stocks Get No Respect or Rubber Band Stretching), our positioning did not waver. However, as stock values have virtually tripled in value from the 2009 lows, more recently I have consistently stated the game has gotten a lot tougher with the low-hanging fruit having already been picked (earnings have recovered from the recession and P/E multiples have expanded). In other words, the trajectory of the last five years is unsustainable.

Fortunately for us, at Sidoxia we’re not hostage to the upward or downward direction of a narrow universe of large cap U.S. domestic stock market indices. We can scour the globe across geographies and capital structure. What does that mean? That means we are investing client assets (and my personal assets) into innovative companies covering various growth themes (robotics, alternative energy, mobile devices, nanotechnology, oil sands, electric cars, medical devices, e-commerce, 3-D printing, smart grid, obesity, globalization, and others) along with various other asset classes and capital structures, including real estate, MLPs, municipal bonds, commodities, emerging markets, high-yield, preferred securities, convertible bonds, private equity, floating rate bonds, and TIPs as well. Therefore, if various markets are imploding, we have the nimble ability to mitigate or avoid that volatility by identifying appropriate individual companies and alternative asset classes.

Irrespective of my shaky short-term forecasting abilities, I am confident people will continue to ask me my opinion about the direction of the stock market. My best advice remains to get out of stocks*…for the “sideliners”. However, the asterisk still signifies there are plenty of opportunities for attractive returns to be had for the rest of us investors, as long as you can stomach the inevitable volatility.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Central Bank Dog Ate My Homework

It’s been a painful four years for the bears, including Peter Schiff, Nouriel Roubini, John Mauldin, Jimmy Rogers, and let’s not forget David Rosenberg, among others. Rosenberg was recently on CNBC attempting to clarify his evolving bearish view by explaining how central banks around the globe have eaten his forecasting homework. In other words, Ben Bernanke is getting blamed for launching the stock market into the stratosphere thanks to his quantitative easing magic. According to Rosenberg, and the other world-enders, death and destruction would have prevailed without all the money printing.

In reality, the S&P 500 has climbed over +140% and is setting all-time record highs since the market bottomed in early 2009. Despite the large volume of erroneous predictions by Rosenberg and his bear buddies, that development has not slowed the pace of false forecasts. When you’re wrong, one could simply admit defeat, or one could get creative like Rosenberg and bend the truth. As you can tell from my David Rosenberg article from 2010 (Rams Butting Heads), he has been bearish for years calling for outcomes like a double-dip recession; a return to 11% unemployment; and a collapse in the market. So far, none of those predictions have come to fruition (in fact the S&P is up about +40% from that period, if you include dividends). After being incorrect for so long, Rosenberg has switched his mantra to be bullish on pullbacks on selective dividend-paying stocks. When pushed whether he has turned bullish, here’s what Rosenberg had to say,

“So it’s not about is somebody bearish or is somebody bullish or whether you’re agnostic, it’s really about understanding what the principle driver of this market is…it’s the mother of all liquidity-driven rallies that I’ve seen in my lifetime, and it’s continuing.”

Rosenberg isn’t the only bear blaming central banks for the unexpected rise in equity markets. As mentioned previously, fear and panic have virtually disappeared, but these emotions have matured into skepticism. Record profits, cash balances, and attractive valuations are dismissed as artificial byproducts of a Fed’s monetary Ponzi Scheme. The fact that Japan and other central banks are following Ben Bernanke’s money printing lead only serves to add more fuel to the bears’ proverbial fire.

Speculative bubbles are not easy to identify before-the-fact, however they typically involve a combination of excessive valuations and/or massive amounts of leverage. In hindsight we experienced these dynamics in the technology collapse of the late-1990s (tech companies traded at over 100x’s earnings) and the leverage-induced housing crisis of the mid-2000s ($100s of billions used to speculate on subprime mortgages and real estate).

I’m OK with the argument that there are trillions of dollars being used for speculative buying, but if I understand correctly, the trillions of dollars in global liquidity being injected by central banks across the world is not being used to buy securities in the stock market? Rather, all the artificial, pending-bubble discussions should migrate to the bond market…not the stock market. All credit markets, to some degree, are tied to the trillions of Treasuries and mortgage-backed securities purchased by central banks, yet many pundits (i.e., see El-Erian & Bill Gross) choose to focus on claims of speculative buying in stocks, and not bonds.

While bears point to the Shiller 10 Price-Earnings ratio as evidence of a richly priced stock market, more objective measurements through FactSet (below 10-year average) and Wall Street Journal indicate a forward P/E of around 14. A reasonable figure if you consider the multiples were twice as high in 2000, and interest rates are at a generational low (see also Shiller P/E critique).

The news hasn’t been great, volatility measurements (i.e., VIX) have been signaling complacency, and every man, woman, and child has been waiting for a “pullback” – myself included. The pace of the upward advance we have experienced over the last six months is not sustainable, but when we finally get a price retreat, do not listen to the bears like Rosenberg. Their credibility has been shot, ever since the central bank dog ate their homework.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Risk of “Double-Rip” on the Rise

Okay, you heard it here first. I’m officially anointing my first new 2013 economic term of the year: “Double-Rip!” No, the biggest risk of 2013 is not a “double-dip” (the risk of the economy falling back into recession), but instead, the larger risk is of a double-rip – a sustained expansion of GDP after multiple quarters of recovery. I know, this sounds like heresy, given we’ve had to listen to perma-bears like Nouriel Roubini, Peter Schiff, John Mauldin, Mohamed El-Erian, Bill Gross, et al shovel their consistently wrong pessimism for the last 14 quarters. However, those readers who have followed me for the last four years of this bull market know where I’ve stood relative to these unwavering doomsday-ers. Rather than endlessly rehash the erroneous gospel spewed by this cautious clan, you can decide for yourself how accurate they’ve been by reviewing the links below and named links above:

Roubini calling for double-dip in 2012

Roubini calling for double-dip in 2011

Roubini calling for double-dip in 2010

Roubini calling for double-dip in 2009

If we switch from past to present, Bill Gross has already dug himself into a deep hole just two weeks into the year by tweeting equity markets will return less than 5% in 2013. Hmmm, I wonder if he’d predict the same thing now that the market is up about +4.5% during the first 18 days of the year?

Why Double-Rip Over Double-Dip?

How can stocks rip if economic growth is so sluggish? If forced to equate our private sector to a car, opinions would vary widely. We could probably agree the U.S. economy is no Ferrari. Faster growing countries like China, which recently reported 4th quarter growth of +7.9% (up from +7.4% in 3rd quarter), have lapped us complacent, right-lane driving Americans in recent years. But speed alone should not be investors’ only key objective. If speed was the number one priority, the only places investors would be placing their money would be in countries like Rwanda, Turkmenistan, and Libya (see Business Insider article). However, freedom, rule of law, and entrepreneurial spirit are other important investment factors to be considered. The U.S. market is more like a Toyota Camry – not very flashy, but it will reliably get you from point A to point B in an efficient and safe manner.

Beyond lackluster economic growth, corporate profit growth has slowed remarkably. In fact, with about 10% of the S&P 500 index companies reporting 4th quarter earnings thus far, earnings growth is expected to rise a measly 2.5% from a year ago (from a previous estimate of 3.0% growth). With this being the case, how can stock prices go up? Shrewd investors understand the stock market is a discounting mechanism of future fundamentals, and therefore stocks will move in advance of future growth. It makes sense that before a turn in the economy, the brakes will often be activated before accelerating into another fast moving straight-away.

In addition, valuation acts like shock absorbers. With generational low interest rates and a below-average forward 12-month P/E (Price-Earnings) ratio of 13x’s, this stock market car can absorb a significant amount of fundamental challenges. The oft quoted message that “In the short run, the market is a voting machine but in the long run it is a weighing machine,” from value icon Benjamin Graham holds as true today as it did a century ago. The recent market advance may be attributed to the voters, but long-term movements are ultimately tied to the sustainable scales of sales, earnings, and cash flows.

If that’s the case, how can someone be optimistic in the face of the slowing growth challenges of this year? What 2013 will not have is the drag of election uncertainty, the fiscal cliff, Superstorm Sandy, and an end-of-the-world Mayan calendar concern. This is setting the stage for improved fundamentals as we progress deeper into the year. Certainly there will be other puts and takes, but the absence of these factors should provide some wind under the economy’s sails.

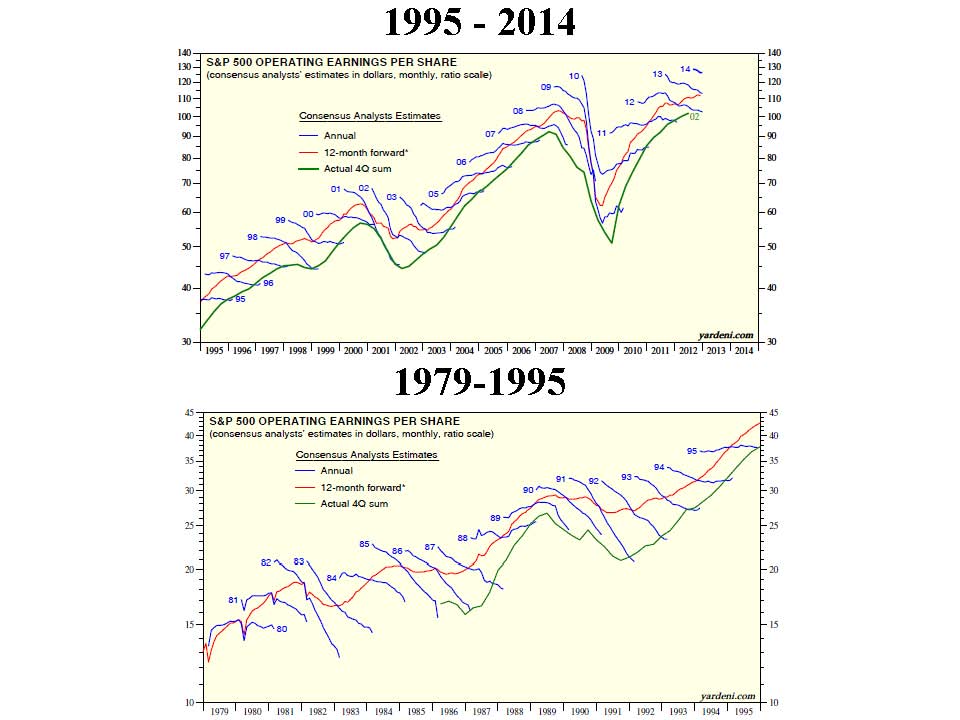

What’s more, history shows us that indeed stock prices can go up quite dramatically (more than +325% during the 1990s) when consensus earnings forecasts continually get trimmed. We have seen this same dynamic since mid-2012 – earnings forecasts have come down and stock prices have gone up. Strategist Ed Yardeni captures this point beautifully in a recent post on his Dr. Ed’s Blog (see charts below).

CLICK TO ENLARGE – Source: Dr. Ed’s Blog

What Will Make Me Bearish?

Am I a perma-bull, incessantly wearing rose-colored glasses that I refuse to take off? I’ll let you come to your own conclusion. When I see a combination of the following, I will become bearish:

#1. I see the trillions of dollars parked in near-0% cash start coming outside to play.

#2. See Pimco’s Bill Gross and Mohammed El-Erian on CNBC fewer than 10 times per week.

#3. See money flow stop flooding into sub-3% bonds (Scott Grannis) and actually reverse.

#4. Observe a sustained reversal in hemorrhaging of equity investments (Scott Grannis).

#5. Yield curve flattens dramatically or inverts.

#6. Nouriel and his bear buds become bullish and call for a “triple-rip” turn in the equity markets.

#7. Smarter, more-experienced investors than I, á la Warren Buffett, become more cautious. I arrogantly believe that will occur in conjunction with some of the previously listed items.

Despite my firm beliefs, it is evident the bears won’t go down without a fight. If you are getting tired of drinking the double-dip Kool-Aid, then perhaps it’s time to expand your bullish horizons. If not, just wait 12 months after a market rally, and buy yourself a fresh copy of the Merriam-Webster dictionary. There you can locate and learn about a new definition…double-rip!

Read Also: Double-Dip Guesses are “Probably Wrong”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in Fiat, Toyota, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Happy Birthday Bull Market!

Birthdays are always fun, but they are always more fun when more people come to the party. The birthday of the current bull market started on March 9, 2009, and as many bears point out, volume has been low, with a relatively small number of investors joining the party with hats and horns. This skepticism is not unusual in typical bull markets because the psychological scars from the previous bear market are still fresh in investors’ minds. How can investors get excited about investing when we are surrounded by record deficits, political gridlock, a crumbling European Union, slowing China, and peak corporate margins?

Bears Receive Party Invite but Stay Home

Perma-bears like Peter Schiff, Nouriel Roubini, John Mauldin, Mohamed El-Erian, and David Rosenberg have been consistently wrong over the last three years with their advice, but in some instances can sound smart shoveling it out to unassuming investors.

While nervous investors and bears have missed the 125%+ rally (see table below) over the last three years (mitigated by upward but underperforming gold prices), what many observers have not realized is that the so-called “Lost Decade” (see also Can the Lost Decade Strike Twice?) has actually been pretty spectacular for shrewd investors. Even if you purchased small and mid cap stocks at the peak of the market in March 2000, that large swath of stocks is up over +100%…yes, that’s right, more than doubled over the last 12 years. If you consider dividends, the numbers look significantly better.

Doubters of the equity market rally also ignore the three-year +135% advance in the NASDAQ (see also Ugly Stepchild) in part because the 11-year highs being registered still lag the peak levels reached in March 2000. Even though the NASDAQ increased 9-fold in the 1990s, if you bought the NASDAQ index in the first half of 1999, you would have still outperformed the S&P 500 index through the 2012 year-to-date period. Irrespective of how anyone looks at the performance of the NASDAQ index, it still has outperformed the S&P 500 index by more than +200% over the last 25 years, even if you include the bursting of the 2000 technology bubble.

CLICK TO ENLARGE

The point of all these statistics is to show that if you didn’t buy technology stocks at the climax of late 1999 or early 2000 prices, then the amount and type of available opportunities have been plentiful. The table above does not include emerging markets like Brazil, Mexico, and India (to name a few) that have also about doubled in price from the 2000 timeframe to 2012.

Heartburn can Accompany Sweet Treats

Being Pollyannaish after a doubling in market prices is never a wise decision. After three years of massive appreciation, those participating in the bull market run have eaten a lot of tasty cake. Now the question becomes, will investors also get some ice cream and a gift bag to go before the party ends? With the sweetness of the cake still being digested, there are still plenty of scenarios that can create investor heartburn. Obviously, the sovereign debt pig still needs to work its way through the European snake, and that could still take some time. In addition, although macroeconomic data (including employment data) generally have been improving, the trajectory of corporate profits has been decelerating – due in part to near record profit margins getting pressured by rising input costs. Domestically, structural debt and deficit issues have not gone away, and perpetual neglect will only exacerbate the current problems. On the psychology front, even though investors remain skittish, those still in the game are getting more complacent as evidenced by the VIX index now falling to the teens (a negative contrarian indicator).

Despite some of these cautionary signals, the good news is that many of these issues have been known for some time and have been reflected in valuations of the overall large cap indexes. Moreover, trillions of dollars remain idle in low yielding strategies as investors wait on the sidelines. Once prices move higher and there is more comfort surrounding the sustainability of an economic recovery, then capital will come pouring back into equity markets. In other words, investors will have to pay a premium cherry price if they wait for a comforting consensus to coalesce.

Limited Options

The other advantage working in investors’ favor is the lack of other attractive investment alternatives. Where are you going to invest these days when 10-year Treasuries and short-term CDs are yielding next to nothing? How about investing in risky, leveraged, illiquid real estate, just as banks unload massive numbers of foreclosures and process millions of short sales? If those investments don’t tickle your fancy, then how about pricey insurance and annuity products that nobody can understand? Cash was comforting in 2008-2009 and during volatility in recent summers, but with spiking food, energy, leisure, and medical costs, when does that cash comfort turn to cash pain?

Easy money and low interest rate policies being advocated by Federal Reserve Chairman Ben Bernanke and other global central bankers have sucked up available investment opportunities and compelled investors to look more closely at riskier assets like equities. With the large run in equities, I have been trimming back my winners and redeploying proceeds into higher dividend paying stocks and underperforming sectors of the market. Skepticism still abounds, and we may be ripe for a short-term pullback in the equity markets. For those rare birthday party attendees who are called long-term investors, opportunities still remain despite the large run in equities. The cake has been sweet so far, but if you are patient, some ice cream and a gift bag may be coming your way as well.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including emerging market, international, and bond/treasury ETFs), but at the time of publishing SCM had no direct position in VXX, MXY, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

John Mauldin: The Man Who Cries Wolf

We have all heard about the famous Aesop fable about The Boy Who Cried Wolf. In that story, a little boy amuses himself by tricking others into falsely believing a wolf is attacking his flock of sheep. After running to the boy’s rescue multiple times, the villagers became desensitized to the boy’s cries for help. The boy’s pleas ultimately get completely ignored by the villagers despite an eventual real wolf attack that kills the boy’s flock of sheep.

Mauldin: The Man Who Cries Bear

John Mauldin, former print shop professional and current perma-bear investment strategist, unfortunately seems to have taken a page from Aesop’s book by consistently crying for a market collapse. After spending many years wrongly forecasting a bear market, his dependable pessimism eventually paid dividends in 2008. Unfortunately for him, rather than reverse his downbeat outlook, he stepped on the pessimism pedal just as the equity markets have exploded upwards more than +80% from the March lows of last year. Mauldin is widely followed in part to his thoughtful pieces and intriguing contributing writers, but as some behavioral finance students have recognized, being bearish or cautious on the markets always sounds smarter than being bullish. I’m not so sure how smart Mauldin will sound if he’s wrong on the direction of the next 80% move?

The Challenged Predictor

I find it interesting that a man who freely admits to his challenged prediction capabilities continues to make bold assertive forecasts. Mauldin freely confesses in his writings about his inability to manage money and make correct market forecasts, but that hasn’t slowed down the pessimism express. Just two years ago as the financial crisis was unfolding, Mauldin admits to his poor fortune telling skills with regards to his annual forecast report each January:

“ I was wrong (as usual) about the stock markets.”

Here’s Mauldin explaining why he decided to switch from investing real money to the simulated version of investment strategy and economic analysis:

“I wanted to begin to manage money on my own… I found out as much about myself as I did about market timing. What I found out was that I did not have the emotional personality (the stomach?) to directly time the markets with someone else’s money… I simply worried too much over each move of the tape.”

Apparently timing the market is not so simple? Readers of Investing Caffeine understand my feelings about market timing (read Market Timing Treadmill piece) – it’s a waste of time. Market followers are much better off listening to investors who have successfully navigated a wide variety of market cycles (see Investing Caffeine Profiles), rather than strategists who are constantly changing positions like a flag in the wind. I wonder why you never hear Warren Buffett ever make a market prediction or throw out a price target on the Dow Jones or S&P 500 indexes? Maybe buying good businesses or investments at good prices, and owning them for longer than a nanosecond is a strategy that can actually work? Sure seems to work for him over the last few years.

When You’re Wrong

Typically a strategist utilizes two approaches when they are wrong:

1) Convert to Current Consensus: Most strategists change their opinion to match the current consensus thinking. Or as Mauldin described last year, “I expect that this year will bring a few surprises that will cause me to change my opinions yet again. When the facts change, I will try and change with them.” The only problem is…the facts change every day (see also Nouriel Roubini).

2) Push Prediction Out: The other technique is to ignore the forecasting mistake and merely push out the timing (see also Peter Schiff). A simple example would be of Mr. Mauldin extending his recession prediction made last April, “We are going to pay for that with a likely dip back into a recession in 2010,” to his current view made a few weeks ago, “I put the odds of a double-dip recession in 2011 at better than 50-50.”

More Mauldin Mistake Magic

Well maybe I’m just being overly critical, or distorting the facts? Let’s take a look at some excerpts from Mauldin’s writings:

A. January 10, 2009 (S&P @ 890):

Prediction: “I now think we will be in recession through at least 2009 before we begin a recovery….We could see a tradable rally in the next few months, but at the very least test the lows this summer, if not set new lows….It takes a lot of buying to make a bull market. It only takes an absence of buying to make a bear market.”

Outcome: S&P 500 today at 1,179, up +32%. Oops, maybe the timing of his recovery forecast was a little off?

B. February 14, 2009 (S&P @ 827):

Prediction/Advice: “Let me reiterate my continued warning: this is not a market you want to buy and hold from today’s level. This is just far too precarious an economic and earnings environment.”

Outcome: S&P 500 up +45%. You pay a cherry price for certainty and consensus.

C. April 10, 2009 (S&P @ 856):

Prediction: “All in all, the next few years are going to be a very difficult environment for corporate earnings. To think we are headed back to the halcyon years of 2004-06 is not very realistic. And if you expect a major bull market to develop in this climate, you are not paying attention.” On the economy he adds, “We are going to pay for that with a likely dip back into a recession in 2010.”

Outcome: S&P 500 up +38%, with the economy currently in recovery. Interestingly, his comments on corporate earnings in February 2009 referenced an estimate of $55 in S&P 2010. Now that we are 14 months closer to the end of 2010, not only is the consensus estimate much firmer, but the 2010 S&P estimate presently stands at approximately $75 today, about +36% higher than Mauldin was anticipating last year.

D. May 2, 2009 (S&P @ 878):

Prediction: “This rally has all the earmarks of a major short squeeze. ..When the short squeeze is over, the buying will stop and the market will drop. Remember, it takes buying and lot of it to move a market up but only a lack of buying to create a bear market.”

Outcome: S&P 500 up +36%.

Now that we have entered a new year and experienced an +80% move in the market, certainly Mauldin must feel a little more comfortable about the current environment? Apparently not.

E. April 2, 2010 (S&P @ 1178):

Prediction: “ I think it is very possible we’ll see another lost decade for stocks in the US. If we do have a recession next year, the world markets are likely to fall in sympathy with ours.”

Outcome: ????

Previous Mauldin Gems

Here are few more gloomy gems from Mauldin’s bearish toolbox of yester-year:

2005: “The market is a sideways to down market, with the risk to the downside as we get toward the end of the year and a possible recession on the horizon in 2006. And not to put too fine a point on it, I still think we are in a long term secular bear market.” Reality: S&P 500 up +5% for the year and up a few more years after that.

2006: “This year I think the market actually ends the year down, and by at least 10% or more during the year. Reality: S&P 500 up +14% (excluding dividends).

2007: Mauldin’s rhetoric was tamed in light of poor predictions, so rhetoric switches to a “Goldilocks recession” and a mere -10-20% range correction. He goes on to dismiss a deep bear market, “In future letters we will look at why a deep (the 40% plus that is typical in recession) stock market bear is not as likely.” Reality: S&P 500 up +5%. Looks like the writing on the wall for 2008 turned out a bit worse than he expected.

2008: Sticking to soft landing outlook Mauldin states, “I think this will be a mild recession … I don’t think we are looking at anything close to the bear market of 2000-2001.” Uggh. Ultimately, the bear market turned out to be the worst market since 1973-1974 – his prediction was just off by a few decades. Reality: S&P 500 down -37%.

Lessons Learned from Market Strategists

I certainly don’t mean to demonize John Mauldin because his writings are indeed very thoughtful, interesting and include provocative financial topics. But put in the wrong hands, his opinions (and dozens of other strategists’ views) can be extremely dangerous for the average investor trying to follow the ever-changing judgments of so-called expert strategists. To Mauldin’s credit, his writings are archived publicly for everyone to sift through – unfortunately the media and many average investors have short memories and do not take the time to hold strategists accountable for their false predictions. Although, Iike Warren Buffett, I do not make market timing predictions or forecast short-term market trends, I see no problem in strategists making bold or inaccurate forecasts, as long as they are held responsible. Every investor makes mistakes, unfortunately, strategist predictions are usually not readily available for analysis, unlike tangible investment manager performance numbers. When forecasting lightning strikes and extreme bets win, every newspaper, radio show, and media outlet has no problem of placing these soothsayers on a pedestal. Thanks to the law of large numbers and the constantly shifting markets, there will always be a few outliers making correct calls on bold predictions. Who knows, maybe Mauldin will be the next CNBC guru du jour in the future for predicting another lost decade of equity market performance (see Lost Decade article)?

Regardless of your views on the market, the next time you hear a financial strategist make a bold forecast, like John Mauldin crying wolf, I urge you to not go running with the motivation to alter your investment portfolio. I suppose the time to become frightened and drive the REAL wolf (bear market) away will occur when consistently pessimistic strategists like Mauldin turn more optimistic. Until then, tread lightly when it comes to acting on financial market forecasts and stick to listening to long-term, successful investors that have invested their own money through all types of market cycles.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}