Posts tagged ‘IPO’

Ignoring Economics and Vital Signs

As stock prices sit near all-time record highs, and as we enter year nine of the current bull market, I remain amazed and amused at the brazen disregard for important basic economic concepts like supply & demand, interest rates, and rising profits.

If the stock market was a doctor’s patient, over the last decade, bloggers, pundits, talking heads, and pontificators have been ignoring the improving, healthy patient’s vital signs, while endlessly predicting the death of the resilient stock market.

However, let’s be clear – it has not been all hearts and flowers for stocks – there have been numerous -10%, -15%, and -20% corrections since the Financial Crisis nine years ago. Those corrections included the Flash Crash, debt downgrade, Arab Spring, sequestration, Taper Tantrum, Iranian Nuclear Threat, Ukrainian-Crimea annexation, Ebola, Paris/San Bernardino Terrorist Attacks, multiple European & Chinese slowdowns and more.

Despite the avalanche of headlines and volatility, we all know the net result of these events – a more than tripling of stock prices (+259%) from March 2009 to new all-time record highs. With the incessant stream of negative news, how could prices appreciate so dramatically?

Over the years, the explanations by outside observers have changed. First, the recovery was explained as a “dead cat bounce” or a short-term cyclical bull market within a long-term secular bear market. Then, when stock prices broke to new records, the focus shifted to Quantitative Easing (QE1, QE2, QE3, and Operation Twist). The QE narrative implied the bull advance was temporary due to the non-stop, artificial printing presses of the Fed. Now that the Fed has not only ended QE but reversed it (the Fed is actually contracting its balance sheet) and hiked interest rates (no longer cutting), outsiders are once again at a loss. Now, the bears are left clinging to the flawed CAPE metric I wrote about three years ago (see CAPE Smells Like BS), and using political headlines as a theory for record prices (i.e., record stock prices stem from inflated tax cut and infrastructure spending expectations).

It’s unfortunate for the bears that all the conspiracy theory headlines and F.U.D. (fear, uncertainty, and doubt) over the last 10 years have failed miserably as predictors for stock prices. The truth is that stock prices don’t care about headlines – stock prices care about economics. More specifically, stock prices care about profits, interest rates, and supply & demand.

Profits

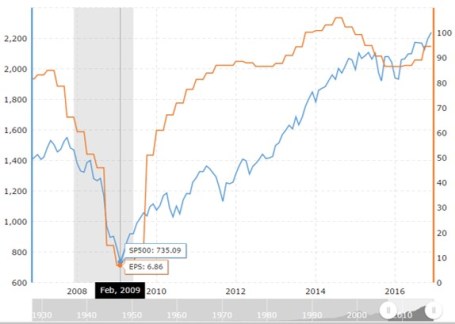

It’s quite simple. Stock prices have more than tripled since early 2009 because profits have more than tripled since 2009. As you can see from the Macrotrends chart below, 2009 – 2016 profits for the S&P 500 index rose from $6.86 to $94.54, or +1,287%. It’s no surprise either that stock prices stalled for 18 months from 2015 to mid-2016 when profits slowed. After profits returned to growth, stock price appreciation also resumed.

Source: Macrotrends

Interest Rates

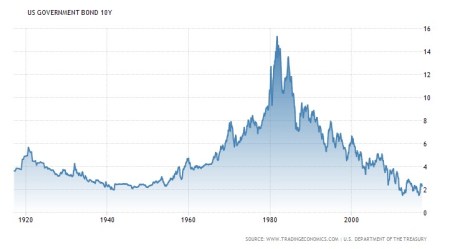

When you could earn a +16% on a guaranteed CD bank rate in the early 1980s, do you think stocks were a more or less attractive asset class? If you can sense the rhetorical nature of my question, then you can probably understand why stocks were about as attractive as rotten milk or moldy bread. Back then, stocks traded for about 8x’s earnings vs. the 18x-20x multiples today. The difference is, today interest rates are near generational lows (see chart below), and CDs pay near +0%, thereby making stocks much more attractive. If you think this type of talk is heresy, ignore me and listen to the greatest investor of all-time, Warren Buffett who recently stated:

“Measured against interest rates, stocks are actually on the cheap side.”

Source: Trading Economics

Supply & Demand

Another massively ignored area, as it relates to the health of stock prices, is the relationship of new stock supply entering the market (e.g., new dilutive shares via IPOs and follow-on offerings), versus stock exiting the market through corporate actions. While there has been some coverage placed on the corporate action of share buybacks – about a half trillion dollars of stock being sucked up like a vacuum cleaner by cash heavy companies like Apple Inc. (AAPL) – little attention has been paid to the trillions of dollars of stock vanishing from mergers and acquisition activities. Yes, Snap Inc. (SNAP) has garnered a disproportionate amount of attention for its $3 billion IPO (Initial Public Offering), this is a drop in the bucket compared to the exodus of stock from M&A activity. Consider the trivial amount of SNAP supply entering the market ($3 billion) vs. $100s of billions in major deals announced in 2016 – 2017:

- Time Warner Inc. merger offer by AT&T Inc. (T) for $85 billion

- Monsanto Co. merger offer by Bayer AG (BAYRY) for $66 billion

- Reynolds American Inc. merger offer by British American Tobacco (BTI) for $47 billion

- NXP Semiconductors merger offer by Qualcomm Inc. (QCOM) for $39 billion

- LinkedIn merger offer by Microsoft Corp. (MSFT) for $28 billion

- Jude Medical, Inc. merger offer by Abbott Laboratories (ABT) for $25 billion

- Mead Johnson Nutrition merger offer by Reckitt Benckiser Group for $18 billion

- Mobileye merger offer by Intel Corp. (INTC) for $15 billion

- Netsuite merger offer by Oracle Corp. (ORCL) for $9 billion

- Kate Spade & Co. merger offer by Coach Inc. (COH) for $2 billion

While these few handfuls of deals represent over $300 billion in disappearing stock, as long as corporate profits remain strong, interest rates low, and valuations reasonable, there will likely continue to be trillions of dollars in stocks being purchased by corporations. This continued vigorous M&A activity should provide further healthy support to stock prices.

Admittedly, there will come a time when profits will collapse, interest rates will spike, valuations will get stretched, sentiment will become euphoric, and/or supply of stock will flood the market (see Don’t be a Fool, Follow the Stool). When the balance of these factors turn negative, the risk profile for stock prices will obviously become less desirable. Until then, I will let the skeptics and bears ignore the healthy economic vital signs and call for the death of a healthy patient (stock market). In the meantime, I will continue focus on the basics of math and offer my economics textbook to the doubters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own AAPL, ABT, INTC, MSFT, T, and certain exchange traded funds, but at the time of publishing SCM had no direct position in SNAP, TWX, MON, KATE, N, MBLY, MJN, STJ, LNKD, NXPI, BAYRY, BTI, QCOM, ORCL, COH, RAI, Reckitt Benckiser Group, any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Growth Stocks – Cheaper by the Day

Are you a value investor? If you said “yes,” how would you feel about buying an $18 stock with a P/E (Price/Earnings) ratio of greater than 100x and a Price/Sales ratio of 14x for a company that three years earlier was started in a garage? This may not sound like a value stock, but had you bought this stock at the initial public offering (IPO), it would have been a screaming bargain – priced at less than 1x P/E ratio, based on this year’s earnings estimates.

You may be surprised to know, this company with a meager $18 IPO share price is now worth $9,192 per share today (if you adjust for three stock splits)! Yes, that’s correct, a +50,900% return. If you are wondering to which stock I’m referring, I am talking about Amazon.com Inc. (AMZN). Incredibly, ever since Amazon went public in 1997, the CEO Jeff Bezos has managed to command the start-up e-commerce company from $31 million in revenues to $121 billion (with a “b”) on an annual basis in 2016 (a +389,000% increase).

Discovering the next IPO that turns into a $363 billion behemoth is easier said than done, and unfortunately these types of companies are a rare breed. Even if you are lucky enough to identify these diamonds-in-the-rough, early in their growth cycle, very few investors have the fortitude and discipline to continually own the stocks through the perpetual volatility (i.e., peaks and valleys).

The good news is, although you may be unable to find every unicorn out there, you can still apply the same principles and characteristics to any growth stock you invest in. In order to prudently achieve outsized returns, one must identify innovative market leaders that have gained some type of sustainable competitive advantage, which will serve as the profit and cash flow growth engine for the stock over the long-term.

If a company does not have a unique advantage over industry competitors, they will likely be unable to compound earnings growth – the key to becoming a big winner. Albert Einstein, Nobel Prize winner is credited with identifying compounding as the “eighth wonder of the world,” and without compounding there will be no gigantic results.

Amazon may be a rare breed, but there are plenty of other examples of so-called “expensive” stocks that get dismissed or fall through the cracks as they explode in value to the stratosphere. Consider Starbucks Corp. (SBUX), which at the time of its IPO in 1992 was priced at a very rich P/E of 52x. Sound expensive? Actually, this was a greatest offer in a generation. Adjusted for stock splits, the IPO shares were valued at $0.27 – in the most recent trading session Starbucks shares closed at $55.90, a +20,600% increase. Similar to Amazon, had you purchased Starbucks shares at the IPO price, you would have been paying less than a measly, eye-popping 1x P/E ratio based on 2016 earnings.

Alphabet Inc. (GOOGL), formerly Google Inc., is another case of growth stock appearing pricey on the outside, but really a value of a lifetime on the inside. The hype surrounding the Google IPO was so palpable in 2004, the stock priced at a relatively nose-bleed level of 60x P/E level, approximately. The unconventional auction bidding method to buy the initial shares made investors even more skeptical. Suffice it to say, the greater than +1,600% gain has once again shown that investors can reap handsome rewards, if they do thorough enough due diligence and ignore the illusory big ticket IPO prices.

What most investors fail to realize is that P/E ratios are temporary. By purchasing a growth stock, the numerator of the P/E ratio (price) becomes static or fixed. As earnings of a growth company expand, the stock becomes cheaper by the day. More specifically, the numerator of the P/E (price) is flat, while the denominator (earnings) grows, thereby making the P/E ratio smaller (cheaper). And as you can see from the few previous examples I have provided, if you are able to identify winners, and hold them long enough, you will eventually realize the initial hefty price tag at purchase will be considered almost free after all the earnings compounding.

Legendary growth investor Peter Lynch summed it up concisely when he noted, “People concentrate too much on the P, but the E really makes the difference.” Lynch goes on to highlight the importance of patience in growth investing because stocks often go down or move sideways for long periods of time before dramatic increases occur:

“My best stocks performed in the 3rd year, 4th year, 5th year, not in the 3rd week or 4th week.”

I’ve illustrated a few successful examples of meteoric growth stocks, but more importantly the misconception many investors place on the current P/E ratio. There still is no substitute for hard-nosed, detailed fundamental research for finding big growth winners, because true growth stocks bought and held for a long enough period, will become cheaper by the day. If you don’t have the time, discipline, or patience to execute this winning strategy, find and hire an experienced investment manager who understands these concepts.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), AMZN, and GOOGL, but at the time of publishing had no direct position in SBUX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dying Unicorns

Historically, when people speak about unicorns they are referring to those magical white horses with long horns sprouting from their foreheads. Today, in Silicon Valley and on Wall Street, “unicorns” refer to those private companies valued at more than $1 billion. The current list of unicorns is extensive, including household names like money-losing Uber ($51.0 billion valuation), Airbnb ($25.5 billion), SnapChat ($15.3 billion), and about 150 other money-losing companies with a combined valuation of approximately a half trillion dollars (see list here). Just like the mythical unicorns we imagine and read about in fairy tales, Silicon Valley unicorns are at risk of dying off and becoming a myth as well.

Square at the Heart of the Problem

Following young technology start-ups with names like, Box, Dropbox, and Square can become quite confusing, but investors are becoming less confused about their desire for profits and fair valuations. The recent –33% discount in the planned pre-IPO offering price of Square shares to $11 – $13 ($4 billion) from the last private funding valuation of $15.46 ($6 billion) is signaling the deteriorating health of money-losing unicorns.

Adding insult to injury, money-losing Square provided recent private investors with a controversial “ratchet” clause, which essentially gives privileged investors additional shares, if the IPO (Initial Public Offering) price does not occur at a minimum set price. The net result is a fraction of advantaged investors receive a disproportionate percentage of the company’s value, while a majority of the other investors see their ownership value diluted. According to Forbes, approximately 30% of unicorns carry some contentious ratchet provisions, which may make IPO exits for these companies that much more difficult.

The recent Square news comes on the heels of other unicorns like Dropbox seeing its pre-IPO value being reduced by -24% from industry giant BlackRock Inc (BLK), an early Dropbox investor. According to the Wall Street Journal¸ bankers close to the company admitted achieving a pre-IPO valuation of $10 billion will be challenging. Subsequently, mutual fund behemoth Fidelity wrote down the value of social media, photo disappearing, mobile application company, Snapchat, by -25%.

Unfortunately, the problems for unicorn companies don’t stop after the IPO. Take for example, Fitbit Inc (FIT), the newly minted $6 billion IPO, which took place in June. Even though the wearable technology company may no longer be a unicorn, the -31% decline in its share price during the first half of November is evidence there are consequences to insiders dumping additional over-priced (or high-priced) shares on investors. Of the planned 17 million secondary share sale, the vast majority of the proceeds (14 million shares) are going to insiders who are taking the money and running, thereby leaving the company itself with a much smaller portion of the offering dollars.

Veteran investors have seen this movie before during the late 1990s tech bubble, and investors know that this type of movie ends very badly. As in any bubble, if you are able to participate early enough during the inflation process, it can be a spectacular ride before the bubble bursts. Unicorn companies can sell a dream for a while, but profitless prosperity cannot last forever. Eventually, profits and cash flows do become important for investors. And for some unicorn companies, the day of reckoning appears to have arrived now. It has been a fun, fairy tale ride for unicorn investors up until now, but with a half trillion dollars in unicorn investments beginning to die off, these early stage companies will need a steadier diet of profits to stay alive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in Uber, Airbnb, SnapChat, Box, Dropbox, Square, BLK, FIT and any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The $100 Billion Facebook Man

Source: Photobucket

If you don’t pay close enough attention, you may miss the Facebook initial public offering (IPO) in the blink of an eye. Since computer programming or Botox has frozen Facebook CEO Mark Zuckerberg’s face into a wide-eyed, blink-free state, you may have bought yourself a little more time to buy shares in this imminent IPO, which is estimated to value the company at upwards of $100 billion.

We don’t know a lot of details about the financial health of Facebook right now, but what we do know is that this snot-nosed, 27-year-old Mark Zuckerberg has created one of the most powerful companies on this planet and his estimated net worth is currently around $17 billion. Not bad for a college drop-out who started Facebook in 2004 as a freshman at Harvard University. Hmmm, maybe I should have dropped out of college like Mark Zuckerberg, Steve Jobs, and Bill Gates, and I too could have become a billionaire? OK, maybe not, but sometimes living in dreamland can be fun.

Speaking of dreams, Zuckerberg has a dream of connecting the whole world, and with more than 800 million-plus Facebook users, he is well on his way. If Facebook users made their own own country, it would be #3 behind only China and India – I’ll check back in a few years to see if Facebook can climb to the top position.

The Pre-IPO Interview

Charlie Rose recently ditched the tie and headed to Silicon Valley to conduct an interview at Facebook headquarters with Mark Zuckerberg and his Chief Operating Officer Sheryl Sandberg. If you fast forward to MINUTE 9:30 you can listen to the official Facebook IPO response:

Vodpod videos no longer available.

The Hype Machine

The hype surrounding the Facebook IPO is palpable and feels a lot like the Google Inc. (GOOG) IPO in 2004, but that capital raising event only resulted in proceeds of $1.9 billion for Google. The recent chatter surrounding the pending Facebook IPO places the value to be raised closer to $10 billion. Partial offerings seem to be the trend du jour in the social media IPO world, where companies like LinkedIn Corp. (LNKD), Groupon Inc. (GRPN), and Zillow Inc. (Z) all sold just a sliver of their shares to the public in order to create artificial scarcity, thereby pumping up short-term demand for their respective stocks. These companies trade at or above their initial offering price, but significantly below the early investor mouth-frothing spikes in share prices near the time of the IPOs. Facebook appears to be using the same playbook to build up hype for its eventual offering.

Even at an estimated value of $100 billion, Facebook still has some wood to chop if wants to pass Google (about $185 billion in value) and Apple Inc’s (AAPL) approximate $415 billion, but Zuckerberg is no stranger to ambition. When Facebook unveils its inevitable IPO prospectus in the not too distant future, we will have a better idea of whether Facebook and the 2010 Time magazine Person of the Year deserve all the mega-billion dollar accolades, or will an IPO feeding frenzy bring tears to those investors’ eyes that are not privileged enough to receive IPO allocated shares? Regardless of your faith or skepticism, we’re likely to find out the answer to these critical questions in a blink of an eye.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AGN, AAPL, GOOG but at the time of publishing SCM had no direct position in Facebook, MSFT, LNKD, GRPN, Z, TWX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Bove on Goldman-Facebook Deal: Hug the Public!

In a recent research report titled, Has Goldman Learned Anything?, esteemed Rochdale Research analyst Richard Bove chimed in about the recent controversy surrounding the failed U.S. private offering of Facebook shares by Goldman Sachs (GS) to the bank’s wealthiest clients. In the note, Bove states the following:

“The company is embroiled in a ‘headline’ controversy surrounding its handling of a Facebook offering which implies that Goldman does not understand the public’s interest at all.”

Bove goes onto add:

“I fear that this company may not yet understand that those actions that do not appear to be in the public’s interest can, in fact, harm the company.”

I’m having a real difficult time understanding how Goldman privately raising funds for a private company has anything to do with the public? Am I wrong, or don’t millions of private companies raise capital every year without getting approval from Mr. Joe and Mrs. Josephine Public? What exactly does Bove want Goldman CEO Lloyd Blankfein to say to Facebook chief Mark Zuckerberg?

“Oh hello Mr. Zuckerberg, this is Lloyd Blankfein calling from Goldman Sachs, and if I understand it correctly, you are interested in raising $1.5 billion for your company. I know you are arguably the greatest internet brand on this planet, but unfortunately I do not think we can help you because I believe the broader public may not be happy with their lack of ability to participate in the offering. If you don’t have Morgan Stanley’s or JP Morgan’s phone number, just let me know because perhaps they can assist you. Have a great day!”

Come on…Goldman Sachs is not a charitable organization with a mission to make the world a better place – they are one of thousands of publicly traded companies attempting to grow profits. Sure, could Goldman have more discreetly pursued this offering without attracting the massive media barrage? Absolutely. But let’s be fair, the buzz around Facebook is deafening and the paparazzi are following Mark Zuckerberg around as closely as Raj Rajaratnam chases insider trading tips. New York Times columnist and reporter Andrew Ross Sorkin (see Too Big to Fail book review) summed it up best when he said, “You take the words Facebook and Goldman Sachs and put them in the same sentence, it becomes a media sensation unto itself. So I think this was bound to happen one way or the other.”

So while I have no reason to cheerlead for Goldman Sachs, and I’m sure there are plenty of other reasons for the investment bank to be crucified, attempting to raise money for a private company is not a felony in my book. I commend Richard Bove’s altruistic intentions in protecting the public from Goldman Sachs’s evil capital raising activities, and I may even contribute to a group hug with the mass investing public. If he catches me on the right day, I may even give CEO Lloyd Blankfein a hug.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in GS, MS, JPM, Facebook, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Private Equity Sitting on Stuffed Wallet

The clock is ticking and private equity (PE) firms need to put some $445 billion in their wallets to work. Otherwise, the dreams of outsized returns and hefty fees will have to wait for another Golden Era of deal making. Why such a hurry to use the cash? According to Andrea Auerbach, a Managing Director at Cambridge Associates, “Most funds legally have five or six years to invest that capital…it’s use it or lose it.”

Shop ‘til Wallet Drops

As easy as it sounds, spending half a trillion dollars can be difficult. Here’s how IBD’s Norm Alster characterizes the challenge:

“To realize the outsize profits investors expect, private equity firms would have to borrow two or three times that amount. But for the most part, credit spigots for such deals are still dry. At the same time, pinning down buyout targets is not that easy. Many potential sellers are balking at parting with corporate assets in the midst of a serious downturn.”

The 2010 private equity environment is quite a bit different than the LBO boom era from a handful of years ago, as you can see from the chart below. Thanks to cheap, free-flowing funding from the banks, $1.4 trillion worth of deals were consummated in 2006 and 2007, including large deals like First Data Corp. ($27 billion deal – KKR); Alltel ($28 billion – Goldman Sachs/ Texas Pacific Group); and Harrah’s ($30 billion – Apollo Management/Texas Pacific Group). Unfortunately, deals done during this period were done when valuations and leverage were at extremely high historical levels.

Chart source: Thomson Reuters via IBD

Deal Timeout

What’s causing the current dearth of deals? In many instances, business owners have not calibrated valuation expectations downward enough to account for the bruising financial crisis. Given the 77 leveraged buyout defaults in 2009, investors have become more reticent in committing capital as well. Refinancing the mountains of debt associated with the troubled 2006-07 vintage of deals will require patience and creative financing skills from the banks.

Because of the logjam of deals created by the financial crisis, PE firms are actively looking for exit strategies relating to their portfolio companies. Since private equity inherently involves illiquid investments, typically the industry creates liquidity through initial public offerings (IPOs), merger & acquisitions, and/or recapitalization structures that partially or fully return investor capital.

If the economic malaise lingers and valuations remain depressed, I have no doubt owners will eventually return to the negotiating table while waving a white towel in hand. Until then, private equity firms will continue begging for capital from the banks (i.e., using “other peoples’ money”) and beating down sellers into submission with regards to price expectations. If PE firms are not successful in using that wad of cash by the end of the fund’s term, then investors will be free to walk away with their money without paying lucrative fees to the PE firms.

Don’t Forget Benefits

The PE field is facing its fair share of trials and tribulations, but PE’s diversification benefits should not be forgotten. The success of the “Yale Model,” implemented by David Swensen, has come under attack with the recent bursting of the credit bubble, but with the ever-swinging performance pendulum of various asset classes/styles moving in and out of favor, I am confident a consistent strategy integrating PE as a portion of a diversified portfolio will yield respectable risk-adjusted returns over the long-run. Like other areas in the financial services industry, fees are being scrutinized and transparency requests by investors (limited partners) have been on the rise. But first things first – before attractive PE profits can be made as part of a diversified portfolio, the wad of cash in the wallets of PE firms must find a home in portfolio companies.

Read Norm Alster’s full IBD article originally referenced on TRB

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including S&P 500-like positions), but at the time of publishing SCM had no direct positions in GS, Harrah’s or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Taking Facebook and Twitter Public

Facebook CEO Mark Zuckerberg

Valuing high growth companies is similar to answering a typical open-ended question posed to me during business school interviews: “Wade, how many ping pong balls can you fit in an empty 747 airplane?” Obviously, the estimation process is not an exact science, but rather an artistic exercise in which various techniques and strategies may be implemented to form a more educated guess. The same estimation principles apply to the tricky challenge of valuing high growth companies like Facebook and Twitter.

Cash is King

Where does one start? Conceptually, one method used to determine a company’s value is by taking the present value of all future cash flows. For growth companies, earnings and cash flows can vary dramatically and small changes in assumptions (i.e., revenue growth rates, profit margins, discount rates, taxes, etc.) can lead to drastically different valuations. As I have mentioned in the past, cash flow analysis is a great way to value companies across a broad array of industries – excluding financial companies (see previous article on cash flow investing).

Mature companies operating in stable industries may be piling up cash because of limited revenue growth opportunities. Such companies may choose to pay out dividends, buyback stock, or possibly make acquisitions of target competitors. However, for hyper-growth companies earlier in their business life-cycles, (e.g., Facebook and Twitter), discretionary cash flow may be directly reinvested back into the company, and/or allocated towards numerous growth projects. If these growth companies are not generating a lot of excess free cash flow (cash flow from operations minus capital expenditures), then how does one value such companies? Typically, under a traditional DCF (discounted cash flow model), modest early year cash flows are forecasted until more substantial cash flows are generated in the future, at which point all cash flows are discounted back to today. This process is philosophically pure, but very imprecise and subject to the manipulation and bias of many inputs.

To combat the multi-year wiggle room of a subjective DCF, I choose to calculate what I call “adjusted free cash flow” (cash flow from operations minus depreciation and amortization). The adjusted free cash flow approach provides a perspective on how much cash a growth company theoretically can generate if it decides to not pursue incremental growth projects in excess of maintenance capital expenditures. In other words, I use depreciation and amortization as a proxy for maintenance CAPEX. I believe cash flow figures are much more reliable in valuing growth companies because such cash-based metrics are less subject to manipulation compared to traditional measures like earnings per share (EPS) and net income from the income statement.

Rationalizing Ratios

Other valuation methods to consider for growth companies*:

- PE Ratio: The price-earnings ratio indicates how expensive a stock is by comparing its share price to the company’s earnings.

- PEG Ratio (PE-to-Growth): This metric compares the PE ratio to the earnings growth rate percentage. As a rule of thumb, PEG ratios less than one are considered attractive to some investors, regardless of the absolute PE level.

- Price-to-Sales: This ratio is less precise in my mind because companies can’t pay investors dividends, buy back stock, or make acquisitions with “sales” – discretionary capital comes from earnings and cash flows.

- Price-to-Book: Compares the market capitalization (price) of the company with the book value (or equity) component on the balance sheet.

- EV/EBITDA: Enterprise value (EV) is the total value of the market capitalization plus the value of the debt, divided by EBITDA (Earnings Before Interest Taxes Depreciation and Amortization). Some investors use EBITDA as an income-based surrogate of cash flow.

- FCF Yield: One of my personal favorites – you can think of this percentage as an inverted PE ratio that substitutes free cash flow for earnings. Rather than a yield on a bond, this ratio effectively provides investors with a discretionary cash yield on a stock.

*All The ratios above should be reviewed both on an absolute basis and relative basis in conjunction with comparable companies in an industry. Faster growing industries, in general, should carry higher ratio metrics.

Taking Facebook and Twitter Public

Before we can even take a stab at some of these growth company valuations, we need to look at the historical financial statements (income statement, balance sheet, and cash flow statement). In the case of Facebook and Twitter, since these companies are private, there are no publically available financial statements to peruse. Private investors are generally left in the dark, limited to public news related to what other early investors have paid for ownership stakes. For example, in July, a Russian internet company paid $100 million for a stake in Facebook, implying a $6.5 billion valuation for the total company. Twitter recently obtained a $100 million investment from T. Rowe Price and Insight Venture Partners thereby valuing the total company at $1 billion.

Valuing growth companies is quite different than assessing traditional value companies. Because of the earnings and cash flow volatility in growth companies, the short-term financial results can be distorted. I choose to find market leading franchises that can sustain above average growth for longer periods of time (i.e., companies with “long runways”). For a minority of companies that can grow earnings and cash flows sustainably at above-average rates, I will take advantage of the perception surrounding current short-term “expensive” metrics, because eventually growth will convert valuation perception to “cheap.” Google Inc. (GOOG) is a perfect example – what many investors thought was ridiculously expensive, at the $85 per share Initial Public Offering (IPO) price, ended up skyrocketing to over $700 per share and continues to trade near a very respectable level of $500 per share.

The IPO market is heating up and A123 Systems Inc (AONE) is a fresh example. Often these companies are volatile growth companies that require a deep dive into the financial statements. There is no silver bullet, so different valuation metrics and techniques need to be reviewed in order to come up with more reasonable valuation estimates. Valuation measuring is no cakewalk, but I’ll take this challenge over estimating the number of ping pong balls I can fit in an airplane, any day. Valuing growth companies just requires an understanding of how the essential earnings and cash flow metrics integrate with the fundamental dynamics surrounding a particular company and industry. Now that you have graduated with a degree in Growth Company Valuation 101, you are ready to open your boutique investment bank and advise Facebook and Twitter on their IPO price (the fees can be lucrative if you are not under TARP regulations).

DISCLOSURE: Sidoxia Capital Management and client accounts do not have direct long positions AONE, however some Sidoxia client accounts do hold GOOG securities at the time this article was published. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}