Posts tagged ‘Investment Strategy’

A Better Mousetrap

How do you earn better investment returns for your retirement? The short answer: You must find a better mousetrap.

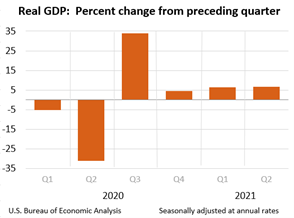

In the current economic environment, finding a better mousetrap to prevent infestations inside your investment portfolio can be a challenge. Concerns over the COVID delta variant, rising inflation, Federal Reserve policy (i.e., “tapering”), and geopolitical tensions (Afghanistan) remain looming in the background. However, the economy continues to expand at a healthy pace (+6.6% Q2 – Gross Domestic Product growth has soared to record heights (see charts below).

The rising economic tide has lifted various stock market indices to new record highs. For the month, the S&P 500 and Dow Jones Industrial Average powered ahead +2.9% and +1.2%, respectively. For the year, these hot results are even more singeing – the S&P 500 has surged +20.4% and the Dow +15.5%.

All good things eventually come to an end, so protecting your financial home against damaging economic rodents is paramount. How you will defend your savings against an inevitable correction and insidious inflation is essential.

Investing with a better mousetrap will allow you to catch better returns, accelerate your retirement, and help avoid the infestation of inflation eating away at your nest egg. If you turn on any financial channel or click on an investment advertisement, chances are someone will attempt to sell you some overpriced, whiz-bang strategy or investment mousetrap that claims to capture amazing, quick results. More often than not, those assertions are complete lies. As Granny Slome always used to tell me, “If it sounds too good to be true, then it probably is.”

Mousetrap Characteristics

What should you be looking for in your investing mousetrap? Here are five characteristics to build upon:

1) Have a long-term time horizon. There is no reliable get-rich-quick scheme that will consistently make you money. Whereas, investing over the long-term in a diversified portfolio generally affords you the luxury of “compounding”, the phenomenon that Einstein called the “eighth wonder of the world.” Chasing the meme stock du jour, crypto currency flavor of the month, and/or the daily day-trading strategy parroted on TV will only lead to a pool of financial tears.

2) Invest in low-cost investment vehicles and strategies. The less you pay in fees, taxes, and transaction costs means the more you can keep for yourself. Investing in low-fee ETFs (Exchange Traded Funds), liquid low-spread securities, and $0 commission trading platforms, along with maintaining long-term holdings to minimize taxes, are all approaches to keeping more money for your growing retirement nest egg.

3) Obtain a customizable strategy to fit your risk tolerance and financial situation. Everyone has a unique financial profile and risk appetite. What’s more, everybody’s situation does not remain static. Circumstances change and life has a way of throwing curveballs at you. Finding a competent investment professional, who is also a fiduciary, is easier said than done, but if you are able to work with an advisor like Sidoxia Capital Management (www.Sidoxia.com), this will afford you the benefit of making prudent adjustments to your situation as it changes.

4) Find an understandable and transparent investment strategy. If your advisor or investment manager cannot explain the strategy and outline the specific costs/fees, then you should look elsewhere. Understanding the objective and strategy of your investments is critical, otherwise volatility can lead to emotional, sub-optimal decision-making. Hidden costs compromise the integrity of the investment advisor, so do not associate yourself with these sketchy people.

5) Rely on proven results. Past results do not guarantee future returns, however, aligning your investment strategy with time-tested results can provide you peace of mind. At the end of the day, your investments need to perform, and having an experienced investment manager is a valuable asset for you.

There is never a shortage of concerns in the financial markets, in both good and bad times. Rather than lose sleep and nervously chew down your fingernails, relax and spend your time finding a better mousetrap.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (September 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Style Drift: Hail Mary Investing

The mutual fund investing game is extraordinarily competitive. According to The Financial Times, there were 69,032 global mutual funds at the end of 2008. With the extreme competitiveness comes lucrative compensation structures if you can win (outperform) – I should know since I was a fund manager for many years. However, the compensation incentive structures can create style drift and conflicts of interest. You can think of style drift as the risky “Hail Mary” pass in football – you are a hero if the play (style drift) works, but a goat if it fails. When managers typically drift from the investment fund objective and investment strategy, typically they do not get fired if they outperform, but the manager is in hot water if drifting results in underperformance. Occasionally a fund can be a victim of its own success. A successful small-cap fund can have positions that appreciate so much the fund eventually becomes defined as a mid-cap fund – nice problem to have.

Drifting Issues

Why would a fund drift? Take for example the outperformance of the growth strategy in 2009 versus the value strategy. The Russell 1000 Growth index rose about +28% through October 23rd (excluding dividends) relative to the Russell 1000 Value index which increased +14%. The same goes with the emerging markets with some markets like Brazil and Russia having climbed over +100% this year. Because of the wide divergence in performance, value managers and domestic equity managers could be incented to drift into these outperforming areas. In some instances, managers can possibly earn multiples of their salary as bonuses, if they outperform their peers and benchmarks.

The non-compliance aspect to stated strategies is most damaging for institutional clients (you can think of pensions, endowments, 401ks, etc.). Investment industry consultants specifically hire fund managers to stay within the boundaries of a style box. This way, not only can consultants judge the performance of multitudes of managers on an apples-to-apples basis, but this structure also allows the client or plan participant to make confident asset allocation decisions without fears of combining overlapping strategies.

For most individual investors however, a properly diversified asset allocation across various styles, geographies, sizes, and asset classes is not a top priority (even though it should be). Rather, absolute performance is the number one focus and Morningstar ratings drive a lot of the decision making process.

What is Growth and Value?

Unfortunately the style drift game is very subjective. Growth and value can be viewed as two sides of the same coin, whereby value investing can simply be viewed as purchasing growth for a discount. Or as Warren Buffet says, “Growth and value investing are joined at the hip.” The distinction becomes even tougher because stocks will often cycle in and out of style labels (value and growth). During periods of outperformance a stock may get categorized as growth, whereas in periods of underperformance the stock may change its stripes to value. Unfortunately, there are multiple third party data source providers that define these factors differently. The subjective nature of these style categorizations also can provide cover to managers, depending on how specific the investment strategy is laid out in the prospectus.

What Investors Can Do?

1) Read Prospectus: Read the fund objective and investment strategy in the prospectus obtained via mailed hardcopy or digital version on the website.

2) Review Fund Holdings: Compare the objective and strategy with the fund holdings. Not only look at the style profile, but also evaluate size, geography, asset classes and industry concentrations. Morningstar.com can be a great tool for you to conduct your fund research.

3) Determine Benchmark: Find the appropriate benchmark for the fund and compare fund performance to the index. If the fund is consistently underperforming (outperforming) on days the benchmark is outperforming (underperforming), then this dynamic could be indicating a performance yellow flag.

4) Rebalance: By periodically reviewing your fund exposures and potential style drift, rebalancing can bring your asset allocation back into equilibrium.

5) Seek Advice: If you are still confused, call the fund company or contact a financial advisor to clarify whether style drift is occurring in your fund(s) (read article on finding advisor).

Style drift can potentially create big problems in your portfolio. Misaligned incentives and conflicts of interest may lead to unwanted and hidden risk factors in your portfolio. Do yourself a favor and make sure the quarterback of your funds is not throwing “Hail Mary” passes – you deserve a higher probability of success in your investments.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Wade W. Slome, CFA, CFP is a contributing writer for Morningstar.com. Please read disclosure language on IC “Contact” page.

Building Your Financial Future – Mistakes Made in Investment Planning

Building Your Dream Future Requires a Plan

Building your retirement and financial future can be likened with the challenge of designing and building your dream home. The tools and strategies selected will determine the ultimate cost and outcome of the project.

I constantly get asked by investors, “Wade, is this the bottom – is now the right time to get in the markets?” First of all, if I precisely knew the answer, I would buy my own island and drink coconut-umbrella drinks all day. And secondarily, despite the desire for a simple, get-rich quick answer, the true solution often is more complex (surprise!). If building your financial future is like designing your dream home, then serious questions need to be explored before your wealth building journey begins:

1) Do I have enough money, and if not, how much money do I need to develop my financial future?

2) Can I build it myself, or do I need the help of professionals?

3) Do I have contingency plans in place, should my circumstances change?

4) What tools and supplies do I need to effectively bring my plans to life?

Most investors I run into have no investment plan in place, do not know the costs (fees) of the tools and strategies they are using, and if they are using an advisor (broker) they typically are in the dark with respect to the strategy implemented.

For the “Do-It-Yourselfers”, the largest problem I am witnessing right now is excessive conservatism. Certainly, for those who have already built their financial future, it does not make sense to take on unnecessary risk. However, for most, this is a losing strategy in a world laden with inflation and ever-growing entitlements like Medicare and Social Security. There’s clearly a difference between stuffing money under the mattress (short-term Treasuries, CDs, Money Market, etc.) and prudent conservatism. This is a credo I preach to my clients.

In many cases this conservative stance merely compounds a previous misstep. Many investors undertook excessive risk prior to the current financial crisis – for example piling 100% of investment portfolios into five emerging market commodity stocks.

What these examples prove is that the average investor is too emotional (buys too much near peaks, and capitulates near bottoms), while paying too much in fees. If you don’t believe me, then my conclusions are perfectly encapsulated in John Bogle’s (Vanguard) 1984-2002 study. The analysis shows the average investor dramatically underperforming both the professionally managed mutual fund (approximately by 7% annually) and the passive (“Do Nothing”) strategy by a whopping 10% per year.

Building your financial future, like building your dream home, requires objective and intensive planning. With the proper tools, strategies and advice, you can succeed in building your dream future, which may even include a coconut-umbrella drink.

Your Investment Car Needs Shocks

Smooth Out the Bumpy Ride

Investing can make for a bumpy ride. What can investors do to smooth out the rough financial journey? The simple answer: diversification. If you consider your investment portfolio as a car, then the process of diversification acts like shock absorbers. Those shocks make for a more comfortable ride while preventing potential disasters – like accidentally driving your investments off a cliff.

People generally understand the concept behind, “not putting all your eggs in one basket.” However, once introduced to financial theory terms such as correlation, covariance, and the efficient frontier, people’s eyes begin to glaze over…and rightfully so!

So what are some of the key points one should understand regarding diversification:

- Lunch CAN Be Free! There are very few free lunches in life, but with “diversification” you can indeed get something for nothing. For example, let’s assume you are approached with two investments, ski hats and sun visors, and each investment is expected to deliver a 5% annual return. Furthermore, let’s suppose that zero ski hats are sold in Spring and Summer (and zero sun visors in Fall and Winter). If you merely own one investment, that investment will be more risky (volatile) than a combo portfolio for half the year. Although any combination of two investments will create a 5% return, by diversifying (owning both investments), you can smooth out the ride. There’s your free lunch – the same return achieved for less risk (volatility)!

- Gravity Holds True For Investments Too! Nothing goes up forever, so do not concentrate your portfolio in sectors that have wildly outperformed other sectors/asset classes for long periods of time. Lessons learned over the last 10 years in the areas of technology and real estate highlight the dangers of over-exposure to any one sector in the economy.

- Vary Your Investment Diet! In the Oscar-nominated documentary Super Size Me, Morgan Spurlock decides to eat McDonald’s fast-food for breakfast, lunch, and dinner for thirty days. As a result, his cholesterol levels sky-rocket, he gains over 24 pounds, and his liver function deteriorates significantly. When it comes to your investment portfolio, you should balance it across a wide range of healthy options, including domestic and international stocks and bonds; large and small capitalization stocks; growth and value styles; cash and low-risk liquid investments; and alternative asset classes, such as real estate, commodities, and private investments.

The benefits of diversification will fluctuate under different economic climates. During our recent financial crisis, especially in late 2008, the correlation ratio (the degree that different asset classes move together) unfortunately was very high. However, those investors who were exposed to areas such as Treasury securities, gold, cash, and bonds generally fared better than those who did not. Subsequently, in the early part of 2009, the benefits of diversification shined through as outperformance in emerging markets, technology, consumer discretionary and growth stocks balanced the weakness suffered in banking, transportation, healthcare, bond and value segments.

Diversification helps on the rough roads of investing, so make sure to check those shocks!

{kind=link}