Posts tagged ‘invest’

Even Winning Teams Occasionally Lose

The stock market has been a winning team for years, generating outsized returns for investors. But so far this year, the winning streak appears to be coming to an end. For 2022, the S&P 500 index is down -21%, including -8% last month. However, since 2008, the stock market has generally been on a consistent tear racking up a record of 10 wins, 2 losses (2015 and 2018), and one tie (2011). In recent years, the U.S. stock market has been winning by a large margin (2019: +29%, 2020: +16%, 2021: +27%) and a significant contributor to the team’s win streak has been the Federal Reserve, or the designated hitter (DH).

Jerome Powell, the Fed Chair, has been a very effective clean-up hitter for the stock market, not only leading the stock market team to victories, but also appreciation in almost all global-risk asset classes. By keeping interest rates (the Federal Funds Rate target) essentially at 0% over the last few years, since the initial COVID pandemic outbreak, many investors are blaming Mr. Powell for elevated inflation rates. If that were truly the case, then we probably wouldn’t see the ubiquitous inflation globally, as we do now. Just as you would expect with any baseball team, any single player does not deserve all the credit for wins, nor should any single player receive all the blame for losses – the same principle applies to the Federal Reserve.

Regardless, the stock market’s best hitter is now injured. In addition to pushing interest rates higher, the Fed is hurting the team through its monetary policy of quantitative tightening or QT (i.e., selling bonds off the Fed’s balance sheet). Theoretically, QT should cause interest rates to move higher, all else equal, and thereby slow down growth in the economy, and help tame out-of-control inflation.

The stock market was also thrown a curve ball when Russia invaded Ukraine, which added gasoline to an already flaming inflation fire. Globally, consumers and businesses have witnessed exploding oil/gasoline prices, in addition to escalated food prices caused by a lack of grain and other commodity exports out of Ukraine.

Lastly, a wild pitch has been thrown at the U.S. stock market by China with its zero-COVID policy, which has essentially shut down the world’s 2nd largest economy and further delayed the full reopening of the global economic game. As a result of China’s hardline lockdown stance, global supply chain disruptions have intensified and import prices have mushroomed higher.

Although this all sounds like horrible news, in the game of investing, nobody wins all the time. As history teaches us, the stock market is generally up around 70% of the time. It just happens to be that we are in the middle of a 30% losing period.

Bad News Does Not Mean Bad Stock Market

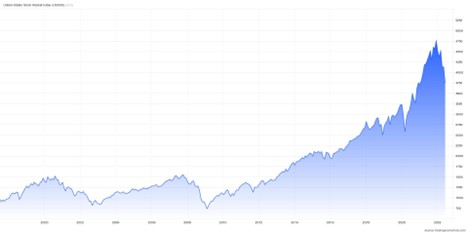

The majority of economists, strategists, and talking heads on television are forecasting a recession in our economy, either this year or next. This should come as no surprise to any experienced investor, as history teaches us that recessions occur on average about twice every decade. Long-term investors also understand that stock prices do not always just go up on good news and down on bad news. Stocks can go down on good news, and up on bad news. In fact, over the last 13 years, since the bottom of the 2008-2009 financial crisis, the stock market has increased about six-fold (even after this year’s -21% correction) in the face of some horrendously scary headlines (also see chart below):

· Ukraine-Russia

· COVID

· Elections / Capitol Insurrection

· Exit from Afghanistan

· Impeachment

· China Trade War & Tariffs

· Inverted Yield Curves

· N. Korea Missile Launches

· Brexit

· ISIS in Iraq

· Ebola

· Russia Takeover of Crimea

· Double Dip Recession Fears

· Eurozone Debt Crisis

S&P 500 Index (1997 – 2022)

Despite the recent headwinds in the stock market, not all the news is bad. Here are some tailwinds:

- PROFITS: Corporate profits remain at or near record levels.

- INFLATION: Inflation appears to be cooling as evidenced by declining commodity prices (TR Commodities CRB Index).

CRB Commodities Index (2022)

- PRICES: Valuations have come down significantly – Price/Earnings ratio of 15.9 (i.e., stock prices are on sale).

- SENTIMENT: Sentiment remains fearful – a contrarian buy indicator (an elevated VIX – Volatility Index can signal buying opportunities). As Warren Buffett says, “Be fearful when others are greedy, and greedy when others are fearful.”

VIX – Volatility Index (2021 – 2022)

Even though the U.S. stock market has been a long-term winner, investors have been betting against the winning team by selling stocks. As mentioned earlier, recessions, if we get one, are common and nothing new. The -21% correction in stock prices is already factoring in a mild recession, so we have already suffered near-maximum pain. Could prices go lower? Certainly. But should you quit a 26-mile marathon at mile 25 because the pain is too intense? In most instances, the answer should absolutely be “no” (see also No Pain, No Gain). Eventually, the Fed will stop raising interest rates, inflation will cool, the Russia-Ukraine war will be resolved, and solid growth will return. While many people are betting the stock market will lose this year, many long-term investors recognize betting on stock market success is a winning strategy over the long-run, especially when prices are on sale.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in BRKA/B or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Re-Questioning the Death of Buy & Hold Investing

Article originally posted September 17, 2010: At the time this original article was written, the Dow Jones Industrial Average was hovering around 11,500. Last week, the Dow closed at 20,624. Sure there have been plenty of ups and downs since 2010, but as I suggested seven years ago, perhaps “buy and hold” still is not dead today?

In the midst of the so-called “Lost Decade,” pundits continue to talk about the death of “buy and hold” (B&H) investing. I guess it probably makes sense to define B&H first before discussing it, but like most amorphous financial concepts, there is no clear cut definition. According to some strict B&H interpreters, B&H means buy and hold forever (i.e., buy today and carry to your grave). For other more forgiving Wall Street lexicon analysts, B&H could mean a multi-year timeframe. However, with the advent of high frequency trading (HFT) and supercomputers, the speed of trading has only accelerated further to milliseconds, microseconds, and even nanoseconds. Pretty soon B&H will be considered buying a stock and holding it for a day! Average mutual fund turnover (holding periods) has already declined from about 6 years in the 1950s to about 11 months in the 2000s according to John Bogle.

Technology and the lower costs associated with trading advancements arre obviously a key driver to shortened investment horizons, but even after these developments, professionals success in beating the market is less clear. Passive gurus Burton Malkiel and John Bogle have consistently asserted that 75% or more of professional money managers underperform benchmarks and passive investment vehicles (e.g., index funds and exchange traded funds).

This is not the first time that B&H has been held for dead. For example, BusinessWeek ran an article in August 1979 entitled The Death of Equities (see Magazine Cover article), which aimed to eradicate any stock market believers off the face of the planet. Sure enough, just a few years later, the market went on to advance on one of the greatest, if not the greatest, multi-decade bull market run in history. People repudiated themselves from B&H back then, and while B&H was in vogue during the 1980s and 1990s it is back to becoming the whipping boy today.

Excuse Me, But What About Bonds?

With all this talk about the demise of B&H and the rise of the HFT machines, I can’t help but wonder why B&H is dead in equities but alive and screaming in the bond market? Am I not mistaken, but has this not been the largest (or darn near largest) thirty-year bull market in bonds? The Federal Funds Rate has gone from 20% in 1981 to 0% thirty years later. Not a bad period to buy and hold, but I’m going to go out on a limb and say the Fed Funds won’t go from 0% to a negative -20% over the next thirty years.

Better Looking Corpse

There’s no denying the fact that equities have been a lousy place to be for the last ten years, and I have no clue what stocks will do for the next twelve months, but what I do know is that stocks offer a completely different value proposition today. At the beginning of the 2000, the market P/E (Price Earnings) valued earnings at a 29x multiple with the 10-year Treasury Note trading with a yield of about 6%. Today, the market trades at 13.5 x’s 2010 earnings estimates (12x’s 2011) and the 10-Year is trading at a level less than half the 2000 rate (2.75% today). Maybe stocks go nowhere for a while, but it’s difficult to dispute now that equities are at least much more attractive (less ugly) than the prices ten years ago. If B&H is dead, at least the corpse is looking a little better now.

As is usually the case, most generalizations are too simplistic in making a point. So in fully reviewing B&H, perhaps it’s not a bad idea of clarifying the two core beliefs underpinning the diehard buy and holders:

1) Buying and holding stocks is only wise if you are buying and holding good stocks.

2) Buying and holding stocks is not wise if you are buying and holding bad stocks.

Even in the face of a disastrous market environment, here are a few stocks that have met B&H rule #1:

Maybe buy and hold is not dead after all? Certainly, there have been plenty of stinking losing stocks to offset these winners. Regardless of the environment, if proper homework is completed, there is plenty of room to profitably resurrect stocks that are left for a buy and hold death by the so-called pundits.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: At the time the article was originally written, Sidoxia Capital Management (SCM) and some of its clients owned certain exchange traded funds and AAPL, AMZN, ARMH, and NFLX, but at the time of publishing SCM had no direct position in GGP, APKT, KRO, AKAM, FFIV, OPEN, RVBD, BIDU, PCLN, CRM, FLS, GMCR, HANS, BYI, SWN (*2,901% is correct %), CTSH, CMI, ISRG, ESRX, or any other security referenced in this article. As of 2/19/17 – Sidoxia owned AAPL, AMZN, and was short NFLX. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Questioning the Death of Buy & Hold Investing

In the midst of the so-called “Lost Decade,” pundits continue to talk about the death of “buy and hold” (B&H) investing. I guess it probably makes sense to define B&H first before discussing it, but like most amorphous financial concepts, there is no clear cut definition. According to some strict B&H interpreters, B&H means buy and hold forever (i.e., buy today and carry to your grave). For other more forgiving Wall Street lexicon analysts, B&H could mean a multi-year timeframe. However, with the advent of high frequency trading (HFT) and supercomputers, the speed of trading has only accelerated further to milliseconds, microseconds, and even nanoseconds. Pretty soon B&H will be considered buying a stock and holding it for a day! Average mutual fund turnover (holding periods) has already declined from about 6 years in the 1950s to about 11 months in the 2000s according to John Bogle.

Technology and the lower costs associated with trading advancements is obviously a key driver to shortened investment horizons, but even after these developments, professionals success in beating the market is less clear. Passive gurus Burton Malkiel and John Bogle have consistently asserted that 75% or more of professional money managers underperform benchmarks and passive investment vehicles (e.g., index funds and exchange traded funds).

This is not the first time that B&H has been held for dead. For example, BusinessWeek ran an article in August 1979 entitled The Death of Equities (see Magazine Cover article), which aimed to eradicate any stock market believers off the face of the planet. Sure enough, just a few years later, the market went on to advance on one of the greatest, if not the greatest, multi-decade bull market run in history. People repudiated themselves from B&H back then, and while B&H was in vogue during the 1980s and 1990s it is back to becoming the whipping boy today.

Excuse Me, But What About Bonds?

With all this talk about the demise of B&H and the rise of the HFT machines, I can’t help but wonder why B&H is dead in equities but alive and screaming in the bond market? Am I not mistaken, but has this not been the largest (or darn near largest) thirty year bull market in bonds? The Federal Funds Rate has gone from 20% in 1981 to 0% thirty years later. Not a bad period to buy and hold, but I’m going to go out on a limb and say the Fed Funds won’t go from 0% to a negative -20% over the next thirty years.

Better Looking Corpse

There’s no denying the fact that equities have been a lousy place to be for the last ten years, and I have no clue what stocks will do for the next twelve months, but what I do know is that stocks offer a completely different value proposition today. At the beginning of the 2000, the market P/E (Price Earnings) valued earnings at a 29x multiple with the 10-year Treasury Note trading with a yield of about 6%. Today, the market trades at 13.5 x’s 2010 earnings estimates (12x’s 2011) and the 10-Year is trading at a level less than half the 2000 rate (2.75% today). Maybe stocks go nowhere for a while, but it’s difficult to dispute now that equities are at least much more attractive (less ugly) than the prices ten years ago. If B&H is dead, at least the corpse is looking a little better now.

As is usually the case, most generalizations are too simplistic in making a point. So in fully reviewing B&H, perhaps it’s not a bad idea of clarifying the two core beliefs underpinning the diehard buy and holders:

1) Buying and holding stocks is only wise if you are buying and holding good stocks.

2) Buying and holding stocks is not wise if you are buying and holding bad stocks.

Even in the face of a disastrous market environment, here are a few stocks that have met B&H rule #1:

Maybe buy and hold is not dead after all? Certainly there have been plenty of stinking losing stocks to offset these winners. Regardless of the environment, if proper homework is completed, there is plenty of room to profitably resurrect stocks that are left for a buy and hold death by the so-called pundits.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, AMZN, ARMH, and NFLX, but at the time of publishing SCM had no direct position in GGP, APKT, KRO, AKAM, FFIV, OPEN, RVBD, BIDU, PCLN, CRM, FLS, GMCR, HANS, BYI, SWN (*2,901% is correct %), CTSH, CMI, ISRG, ESRX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

How to Make Money in Stocks Using Cash Flows

There you are in front of your computer screen, and lo and behold you notice one of your top 10 positions is down -11% (let’s call it ticker: ABC). With sweaty palms and blood rushing from your head, you manage to click with trembling hands on the ticker symbol that will imminently deliver the dreadful news. A competitor (ticker: XYZ) just pre-announced negative quarterly earnings results, and an investment bank, Silverman Sax, has decided to downgrade ABC on fears of a negative spill-over effect. What do you do now? Sell immediately on the cockroach theory – seeing one piece of bad news may mean there are many more dreadful pieces of information lurking behind the scenes? Or, should you back up the truck to take advantage of a massive buying opportunity?

There you are in front of your computer screen, and lo and behold you notice one of your top 10 positions is down -11% (let’s call it ticker: ABC). With sweaty palms and blood rushing from your head, you manage to click with trembling hands on the ticker symbol that will imminently deliver the dreadful news. A competitor (ticker: XYZ) just pre-announced negative quarterly earnings results, and an investment bank, Silverman Sax, has decided to downgrade ABC on fears of a negative spill-over effect. What do you do now? Sell immediately on the cockroach theory – seeing one piece of bad news may mean there are many more dreadful pieces of information lurking behind the scenes? Or, should you back up the truck to take advantage of a massive buying opportunity?

Thank goodness to our good friend, cash flow, which can help supply answers to these crucial questions. Without an ability to value the shares of stock, any decision to buy or sell will be purely based on gut-based emotions. Many Wall Street analysts follow this lemming based analysis when whipping around their ratings (see The Yuppie Bounce & the Lemming Leap). As I talk about in my book, How I Managed $20,000,000,000.00 by Age 32, I strongly believe successful investing requires a healthy balance between the art and the science. Using instinct to tap into critical experience acknowledges the importance of the artistic aspects of investing. Unfortunately, I know few (actually zero) investors that have successfully invested over the long-run by solely relying on their gut.

A winning investment strategy, I argue, includes a systematic, disciplined approach with objective quantitative measures to help guide decision making. For me, the science I depend on includes a substantial reliance on cash flow analysis (See Cash Flow Components Here). What I also like to call this tool is my cash register. Any business you look at will have cash coming into the register, and cash going out of it. Based on the capital needs, cash availability, and growth projects, money will furthermore be flowing in and out of the cash register. By studying these cash flow components, we gain a much clearer lens into the vitality of a business and can quickly identify the choke points.

ACCOUNTING GAMES

The other financial statements definitely shed additional light on the fitness of a company as well, but the income statement, in particular, is subject to a lot more potential manipulation. Since the management teams have more discretion in how GAAP (Generally Accepted Accounting Principles) is applied to the income statement, multiple levers can be pulled by the executives to make results look shinier than reality. For example, simply extending the useful life of an asset (e.g., a factory, building, computer, etc.) will have no impact on a company’s cash flow, yet it will instantaneously and magically raise a companies’ earnings out of thin air…voila!

“Stuffing the channel” is another manipulation strategy that can accelerate revenue recognition for a company. For example, let’s assume Company X ships goods to a distributor, Company Y, for the exclusive purpose of recognizing sales. Company X wins because they just increased their sales, Company Y wins because they have more inventory on hand (even if there is no immediate plan for the distributor to pay for that inventory), and the investor gets “hoodwinked” because they are presented artificially inflated sales and income results.

JOINT STRATEGY

These are but just a few examples of why it’s important to use the cash flow statement in conjunction with the income statement to get a truer picture of a company’s valuation and “quality of earnings.” If you don’t believe me, then check out the work done by reputable academics (Konan Chan, Narasimhan Jegadeesh, Louis Chan, and Josef Lakonishok) that show negative differentials between accounting earnings and cash flow are significantly predictive of future stock price performance (Read more).

So the next time a holding craters (or sky-rockets), take an accounting on the state of the company’s cash flows before making any rash decisions to buy or sell. By doing a thorough cash flow analysis, you’ll be well on your way to racking up gains into your cash register.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

The Hidden Train Wreck – Professional Athlete Portfolios

Need capital for a floating furniture venture? How about an oxygen absorbing skin procedure? Well, if you are having any difficulty, just call an NFL, NBA, or MLB rookie. Even wealthy professional athletes have been impacted by the financial crisis, not to mention the aggressive sales tactics of the investment industry and the players’ poor money management skills. Many players are too busy concentrating on winning games, while their portfolios are suffering losses. The statistics are staggering. Here are the findings, according to an article published in Sports Illustrated earlier this year:

- “By the time they have been retired for two years, 78% of former NFL players have gone bankrupt or are under financial stress because of joblessness or divorce.”

- “Within five years of retirement, an estimated 60% of former NBA players are broke.”

- The divorce rate for pro athletes ranges from 60% to 80%, based on estimates from athletes and agents.

- “According to the NFL Players Association, at least 78 players lost a total of more than $42 million between 1999 and 2002 because they trusted money to financial advisers with questionable backgrounds.”

These are not old, dementia-suffering widows living in Florida we are talking about, but rather professional athletes, many of which made multi-million fortunes during their playing careers. The article goes out of its way to demonstrate this is not a fringe issue affecting a minority of professional athletes. Numerous examples were provided, including the following:

- Ten current and former Major League Baseball players, including outfielder Jonny Damon of the New York Yankees, had some of their money tied up in the alleged $8 billion fraud perpetrated by Robert Allen Stanford.

- Raghib (Rocket) Ismail lost a fortune by investing in excessively risky ventures, including a movie about music label COZ Records; a cosmetics procedure company; a nationwide phone-card dispensing venture; and a framed calligraphy company opened in New Orleans two months before Hurricane Katrina hit.

- Drew Bledsoe, Rick Mirer and five other NFL retirees each invested a minimum of $100,000 in a failed start-up, which touted “biometric authentication” technology that potentially could replace credit cards with fingerprints. The players eventually sued UBS (the financial-services firm) for allegedly withholding information about the company founder’s criminal history and drug use.

- Torii Hunter, outfielder for the Los Angeles, invested almost $70,000 in living-room furniture that included inflatable rafts – perfect for those consumers living in flood zones. Suffice it to say, the results did not meet initial expectations.

- In addition to his legal problems, NFL quarterback Michael Vick filed for Chapter 11 bankruptcy last year partly because he could not repay about $6 million in bank loans that he directed toward a car-rental franchise in Indiana, wine shop in Georgia and real estate in Canada.

- Retired NBA forward Vin Baker’s seafood restaurant in Old Saybrook, Connecticut, was foreclosed on in February 2008 due to nearly $900,000 in unpaid loans.

- “NBA guard Kenny Anderson filed for bankruptcy in October 2005. He detailed how the estimated $60 million he earned in the league had dwindled to nothing. He bought eight cars and rang up monthly expenses of $41,000, including outlays for child support, his mother’s mortgage and his own five-bedroom house in Beverly Hills, Calif.—not to mention $10,000 in what he dubbed “hanging-out money.” He also regularly handed out $3,000 to $5,000 to friends and relatives.”

- “Former NBA forward Shawn Kemp (who has at least seven children by six women) and, more recently, Travis Henry (nine by nine) have seen their fortunes sapped by monthly child-support payments in the tens of thousands of dollars.”

Besides irresponsible spending, and greedy advisors, contributing factors to all the losses are the “boring” and “unintelligible” nature of securities investments. Professional athletes like to flaunt investments like night clubs and car dealerships – there is a “thrill of tangibility,” according to SI writer Pablo Torre.

Professional athletes are not the only ones suffering losses. Ordinary investors have lost also and are learning it’s not what you make – rather it’s what you preserve and grow. The majority of the athletes do not realize their peak earnings years cover a very brief period, and therefore need to be more prudent with their money management since the windfall moneys must be spread over many years.

Trust is an important but difficult trait to find for many of these athletes since many opportunistic friends, acquaintances, and family members in many cases put their self interests ahead of the professional athlete’s needs. There is no simple formula for intelligent money management, however there are ways for athletes to protect their financial blind spots:

1) Educate Themselves. Learn the basics of what you are investing in. You may not learn the ins and outs but you can get a basic understanding of the expected return and volatility of your investments. Athletes often forget about diversification as well, “Chronic over-allocation into real estate and bad private equity is the number one problem [for athletes] in terms of a financial meltdown,” Ed Butowsky of Chapwood Investments says.

2) Trust But Verify. Ronald Reagan famously made those statements decades ago and the principle applies to money too. Many athletes pay tens of thousands of dollars for investment advice, so asking questions is advisable. Specifically, ask how performance is trending versus comparable benchmarks and get a view over multiple time periods.

3) Avoid Friends and Family. If possible, separating business from friends and family is a wise idea. When emotions mix with money, harmful decisions can damage the athlete’s financial future.

4) Determine Fees & Commissions. When investing hundreds of thousands, if not millions of dollars, fees and commissions can be substantial; therefore it is imperative for the athletes to know what they are paying their advisors.

5) Experience Matters. Check out the background of your advisor and determine the licenses and credentials they hold. If you were flying a plane in a heavy storm, you would want an experienced pilot flying the plane, not a flight attendant.

6) Budget. Establish an investment plan with a sustainable lifestyle that accounts for inflation. As veteran agent Bill Duffy says, whose clients include Suns guard Steve Nash and Nuggets forward Carmelo Anthony, “A pro athlete’s money is supposed to outlive his career. Most players never get that.”

Athletes spend their whole lives trying to make the professional ranks in order to earn the big bucks. Due to their high profile status, financial advisors and trusted individuals prey on the sports figures’ wealth. Unfortunately a majority of the athletes lack the money management skills and discipline to preserve and grow their earned wealth. Perhaps repeatedly shining a light on the dirty under-belly of this tragic problem will prevent future financial train wrecks from occurring. Until then, I guess we’ll just have to sift though the bankrupt remains of inflatable sofa raft companies and liquidation proceeds from failed night clubs.

Read the Complete Sports Illustrated Article Here

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

Mountains of Cash Starting to Trickle Back

The month of July was an interesting month because investors opened their 401k and investment statements for the first time in a long while to notice an unfamiliar trend… account values were actually up. Like a child that has burnt their hand on a stove, the wounds and memories are still too fresh – more time must pass before investors decide to get back into the market in full force.

As you can see from the charts below, as investors globally panicked throughout 2008 and early 2009, money earning next to nothing in CDs and Money Market accounts was stuffed under the mattress in droves. The fear factor of last fall has caused current liquid assets to stand near 10 year highs at a level near 120% of the S&P 500 total market capitalization (Thomson Reuters) and at more extreme levels last fall if you just look at Money Market assets (bottom chart) . Now that the Armageddon scenario has been temporarily put to rest, we’re starting to see some of that cash to trickle back into the market. The silver lining is that there is still plenty of dry powder left to drive the market higher – not overnight, but once sustained confidence returns. If the earnings outlook continues to improve, come the beginning of October when 3rd quarter statements arrive in the mail, the pain of not being in the market will overwhelm the fear of burning another hand on the stove like in 2008.

It is funny how the sentiment pendulum can swing from the grips of despair a year ago. There is still headroom for the market to climb higher before the pendulum swings too far in the bullish direction – if you don’t believe me just look on the horizon at the mountain of cash.

Source: SentimenTrader.com (Fall 2008)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

{kind=link}

{kind=link}