Posts tagged ‘innovation’

Investors Slowly Waking to Technology Tailwinds

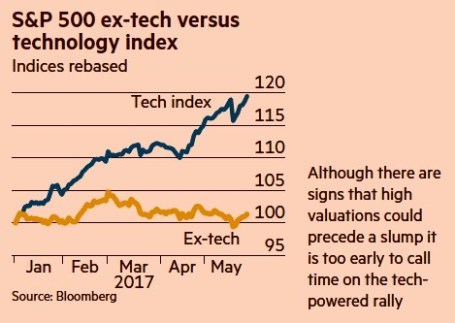

In recent years, investors have been overwhelmingly been distracted by geopolitical headlines and risk aversion caused by the worst financial crisis in a generation. In the background, the tailwinds of technological innovation have been silently gaining momentum. Although this topic is nothing new for Investing Caffeine followers, the outperformance of technology stocks has been pretty stunning in 2017 (see chart below), with the S&P 500 Technology sector rising almost +20% versus the Non-Tech sector eking out a little more than +1% return. Peered through the style lenses of Growth versus Value, technology’s contribution is also evident by the Russell 1000 Growth index’s 2017 outperformance over the Russell 1000 Value index by +11% (approximately +14% vs +3%, respectively).

Source: Bloomberg via The Financial Times

More specifically, what’s driving a significant portion of this outperformance? Robin Wigglesworth from The Financial Times highlighted a key contributing trend here:

“Facebook, Apple, Amazon and Netflix have all gained over 30 per cent this year, and Google is up 24 per cent. Their total market capitalisation now stands at $2.4 trillion. That makes them bigger than the French CAC 40 or Germany’s Dax, and nearly as large as the FTSE 100.”

Technology’s domination has been even more impressive since the cycle bottom of stock prices in 2009, if one contrasts the stark difference in the performance of the tech-heavy NASDAQ versus the more sector-balanced S&P 500. Over this timeframe, the NASDAQ has more than quadrupled in value and beaten the S&P 500 by more than +120%.

While the mass media likes to talk about technology bubbles, artificial money printing by global central banks, and imminent recessions, for years I have been highlighting the importance of the technology revolution and its beneficial impact on stock prices. Here are a few examples:

Technology Does Not Sleep in a Recession (2009)

Technology Revolution Raises Tide (2010)

NASDAQ and the R&D Tech Revolution (2014)

NASDAQ 5,000…Irrational Exuberance Déjà Vu? (2014)

The Traitorous 8 and Birth of Silicon Valley (2016)

As I have explained in many of my previous writings, the important factors of technology, globalization, and demographics have been the key driving forces behind the stock bull market and multi-decade decline in interest rates – not Quantitative Easing (QE) and/or rising debt levels.

Eventually, undoubtedly, euphoria and over-investment will lead to a cyclically-driven recession caused by excess capacity (supply exceeding demand). Regardless of the timing of future economic cycles, the continued multi-generational advance in new technological innovations will continue to drive economic growth, disinflation, improved standards of living, and higher stock prices. Until the animal spirits of the masses fully embrace this technological trend, Sidoxia and its clients will enjoy the tailwind of innovation as I continue to discover attractive investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FB, AAPL, AMZN, GOOG/L, certain exchange traded funds, and short position in NFLX, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Fink & Capitalism: Need 4 Kitchens in Your House?

Do you need four kitchens in your house? Apparently financial industry titan Larry Fink does. If Mr. Fink were a designer for millionaire homeowners, he would advise them to use their millions to build more kitchens in their house (reinvest) rather than distribute those monies to family members (dividends) or use that money to pay back an equity loan from mom and dad for the down payment (share buybacks). Essentially that is exactly what is happening in the stock market. Companies that are generating record profits and margins (millionaires) are increasingly choosing to pay out larger percentages of profits to stockholders (family members) in the form of rising dividends and share buybacks. Contrary to Mr. Fink’s belief, corporate America is actually doing plenty with room additions, landscaping, and roof replacements – I will describe more later.

As a consequence of corporate America’s increasingly shareholder friendly practices of returning cash, Fink believes this trend will stifle innovation and long-term growth in American companies. Here’s a snapshot of the supposed dividend/buyback problem Mr. Fink describes:

Source: Financial Times

Fink Mails Letter from Soapbox

For those of you who do not know who Larry Fink is, he is the successful Chairman and CEO of BlackRock Inc. (BLK), an investment manager which oversees about $4.65 trillion in investment assets. Mr. Fink ignited this recent financial controversy when he jumped on his soapbox by mailing letters to 500 CEOs lecturing them on the importance of long-term investing. What is Mr. Fink’s beef? Fink’s issues revolve around his belief that CEOs and corporations are too short-term oriented.

In his letter, Mr. Fink had this to say:

“This pressure [to meet short-term financial goals] originates from a number of sources—the proliferation of activist shareholders seeking immediate returns, the ever-increasing velocity of capital, a media landscape defined by the 24/7 news cycle and a shrinking attention span, and public policy that fails to encourage truly long-term investment.”

He goes on to bolster his argument with the following:

“More and more corporate leaders have responded with actions that can deliver immediate returns to shareholders, such as buybacks or dividend increases, while underinvesting in innovation, skilled workforces or essential capital expenditures necessary to sustain long-term growth.”

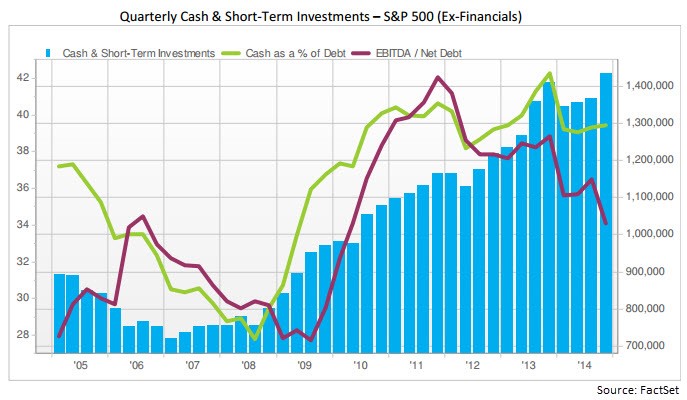

What Mr. Fink does not say in his letter is that large, multinational S&P 500 corporations driving this six-year bull run are sitting on a record hoard of cash, exceeding $1.4 trillion (see chart below). In this light, it should come as no surprise that CEOs are forking over more cash to investors in the forms of dividends and share repurchases.

What’s more, despite Fink’s assertion that share buybacks and dividends are killing innovation, he also fails to mention in his letter that 2014 capital expenditures of $730 billion are also at a record level. That’s right, CAPEX has not been cut to the bone as he implies, but rather risen to all-time highs.

It’s true that generationally low (and declining) interest rates have accelerated the pace of dividends/repurchases, however dividend payout ratios (the percentage of profits distributed to shareholders) of about 32% remain firmly below the long-term payout ratio of approximately 54% (see chart below) – see also Dividend Floodgates Widen. I find it difficult to fault many companies doing something with the gargantuan piles of inflation-losing cash anchoring their balance sheets. Don’t cash-rich companies have a fiduciary duty to borrow reasonable amounts of near-0% debt today (see Bunny Rabbit Market) in exchange for share buybacks currently providing returns of about 5.5% (inverse of 18x P/E ratio) and likely yielding 7%+ returns five years from now?

Source: Financial Times

The “Short-Term” Poster Child – Apple

There is no arguing that excessive debt eventually can catch up to a company. Our multi-year expanding economy is eventually due for another recession in the coming years, and there will be hell to pay for irresponsible, overleveraged companies. With that said, let’s take a look at the poster child of “short-termism” according to Mr. Fink …Apple Inc. (AAPL).

Of the roughly $500 billion in buybacks spent by S&P 500 companies in 2014, Apple accounted for approximately $45 billion of that figure. On top of that, CEO Tim Cook and his board generously decided to return another $11 billion to shareholders in the form of dividends. Has this “short-term” return of capital stifled innovation from the company that has launched iPhone version 6, iPad, Apple Watch, Apple Pay, and is investing into exciting areas like Apple Television, Apple Car, and who knows what else?

To put these Apple numbers into perspective, consider that last year Apple spent over $6 billion on research and development (R&D); $10 billion on capital expenditures; and hired over 12,000 new full-time employees. This doesn’t exactly sound like the death of innovation to me. Even after doling out roughly -$28 billion in expenditures and -$56 billion in dividends/share repurchases, Apple was amazingly able to keep their net cash position flat at an eye-popping +$141 billion!

Mr. Fink abhors “activist shareholders seeking immediate returns” but rather than deriding them perhaps he should send the greedy, capitalist Carl Icahn a personal thank you letter. Since Icahn’s vocal plea for a large Apple share buyback, the shares have skyrocketed about +85%, catapulting BlackRock’s ownership value in Apple to over $19 billion.

With respect to these increasing outlays, Mr. Fink also notes:

“Returning excessive amounts of capital to investors—who will enjoy comparatively meager benefits from it in this environment—sends a discouraging message.”

This would be true if investors took the dividends and stuffed them under their mattress, but an important message Mr. Fink neglects to address as it relates to dividends and share buybacks is demographics. There are 76 million Baby Boomers born between 1946 – 1964 and a Boomer is turning age 65 every 8 seconds. With many bonds trading at near 0% yields (even negative yields) it is no wonder many income starving retirees are demanding many of these cash-rich corporations to share more of the growing spoils via rising dividends.

Capitalism Works

After looking at a few centuries of our country’s history, one of the main lessons we can learn is that capitalism works – especially over the long-run. With about 200 countries across the globe, there is a reason the U.S. is #1…we’re good at capitalism. As our economy has matured over the decades, it is true our priorities and challenges have changed. It is also true that other countries may be narrowing the gap with the U.S., due to certain advantages (e.g., demographics, lower entitlements, easier regulations, etc), but the U.S. will continue to evolve.

In many respects, capitalism is very much like Darwinism – corporations either adapt with the competition…or they die. I repeatedly hear from pessimists that the U.S. is in a secular state of decline, but if that’s the case, how come the U.S. continues to dominate and innovate in major industries like biotechnology, mobile technology, networking, internet, aviation, energy, media, and transportation? Quite simply, we are the best and most experienced practitioners of capitalism.

Certainly, capitalism will continue to cultivate cyclical periods of excess investment/leverage and insufficient regulation. But guess what? Investors, including the public, eventually lose their shirts and behaviors/regulations adjust. At least for a little while, until the next period of excess takes hold. If Apple, and other balance sheet healthy companies allocate capital irresponsibly, capital will flow towards more aggressive and innovative companies. BlackBerry Limited (BBRY) knows a little bit about the consequences of cutthroat competition and suboptimal capital allocation.

While I emphatically share Mr. Fink’s focus on long-term investing values (including his self-serving tax reform ideas), I vigorously disagree with his attacks on shareholder friendly actions and his characterization of rising dividends/buybacks as short-term in nature. In fact, increasing dividends and share buybacks can very much coexist as a long-term investment and capital allocation strategy.

The question of proper capital allocation should have more to do with the age of a company. It only makes sense that younger companies on average should reinvest more of their profits into growth and innovation. On the other hand, more mature S&P 500-like companies will be in a better position to distribute higher percentages of profits to shareholders – especially as cash levels continue to rise to record levels and leverage remains in check.

BlackRock’s Larry Fink may continue to urge CEOs to reinvest their growing cash hoards into superfluous corporate kitchens, but Sidoxia and other prudent capitalist investors will continue to exhort CEOs to opportunistically take advantage of near-free borrowing rates and responsibly share the accretive gains with shareholders. That’s a message Mr. Fink should include in a letter to CEOs – he can use BlackRock’s lofty, above-average dividend to cover the cost of postage.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including AAPL and iShares ETFs, but at the time of publishing, SCM had no direct position in BLK, BBRY or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

NASDAQ Redux

The NASDAQ Composite index once again crossed the psychologically, all-important 5,000 threshold this week for the first time since the infamous tech-bubble burst in the year 2000. Of course, naturally, the media jumped on a non-stop, multi-day offensive comparing and contrasting today’s NASDAQ vs. the NASDAQ twin of yesteryear. Rather than rehash the discussion once again, I have decided to post three articles I published in recent years on the topic covering the outperformance of the spotlighted, tech-heavy index.

NASDAQ 5,000 Irrational Exuberance Déjà Vu?

Investors love round numbers and with the Dow Jones Industrial index recently piercing 17,000 and the S&P 500 index having broken 2,000 , even novice investors have something to talk about around the office water cooler. While new all-time records are being set for the major indices during September, the unsung, tech-laden NASDAQ index has yet to surpass its all-time high of 5,132 achieved 14 and ½ years ago during March of 2000.

Click Here to Read the Rest of the Article

NASDAQ and the R&D Tech Revolution

It’s been a bumpy start for stocks so far in 2014, but the fact of the matter is the NASDAQ Composite Index is up this year and hit a 14-year high in the latest trading session (highest level since 2000). The same cannot be said for the Dow Jones Industrial and S&P 500 indices, which are both lagging and down for the year. Not only did the NASDAQ outperform the Dow by almost +12% in 2013, but the NASDAQ has also trounced the Dow by over +70% over the last five years.

Click Here to Read the Rest of the Article

NASDAQ: The Ugly Stepchild

All the recent media focus has been fixated on whether the Dow Jones Industrial Average index (“The Dow”) will close above the 13,000 level. In the whole scheme of things, this specific value doesn’t mean a whole lot, but it does make for a great topic of conversation at a cocktail party. Today, the Dow is trading at 12,983, a level not achieved in more than three and a half years. Not a bad accomplishment, given the historic financial crisis on our shores and the debacle going on overseas, but I’m still not so convinced a miniscule +0.1% move in the Dow means much. While the Dow and the S&P 500 indexes garner the hearts and minds of journalists and TV reporters, the ugly stepchild index, the NASDAQ, gets about as much respect as Rodney Dangerfield (see also No Respect in the Investment World).

Click Here to Read the Rest of the Article

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

NASDAQ and the R&D-Tech Revolution

It’s been a bumpy start for stocks so far in 2014, but the fact of the matter is the NASDAQ Composite Index is up this year and hit a 14-year high in the latest trading session (highest level since 2000). The same cannot be said for the Dow Jones Industrial and S&P 500 indices, which are both lagging and down for the year. Not only did the NASDAQ outperform the Dow by almost +12% in 2013, but the NASDAQ has also trounced the Dow by over +70% over the last five years.

Is this outperformance a fluke or random coincidence? I’d beg to differ, and we will explore the reasons behind the NASDAQ being treated like the Rodney Dangerfield of indices. Or in other words, why the NASDAQ gets “no respect!” (see also NASDAQ Ugly Step Child).

Compared to the “bubble” days of the nineties, today’s discussions more rationally revolve around profits, cash flows, and valuations. Many of us old crusty veterans remember all the crazy talk of the “New Economy,” “clicks,” and “eyeballs” that took place in the mid-to-late 1990s. Those metrics and hyperbole are used less today, but if NASDAQ’s dominance extends significantly, I’m sure some new and old descriptive euphemisms will float to the conversational surface.

The technology bubble may have burst in 2000, and scarred memories of the -78% collapse in the NASDAQ (5,100 to 1,100) from 2000-2002 have not been forgotten. Despite that carnage, technology has relentlessly advanced through Moore’s Law, while internet connectivity has proliferated in concert with globalization. FedEx’s (FDX) Chief Information Officer Rob Carter summed it up nicely when he noted, “The sound we heard wasn’t the [tech] bubble bursting; it was the big bang.”

Even with the large advance in the NASDAQ index in recent years, valuations of the tech-heavy index remain within reasonable ranges. Accurate gauges of the NASDAQ Composite price-earnings ratio (P/E) are scarce, but just a few months ago, strategist Ned Davis pegged the index P/E at 21, well below the peak of 49 at the end of 1999. For now, the scars and painful memories of the 2000 crash have limited the amount of frothiness, although pockets of it certainly still exist (greed will never be fully eradicated).

Why NASDAQ & Technology Continue to Flourish

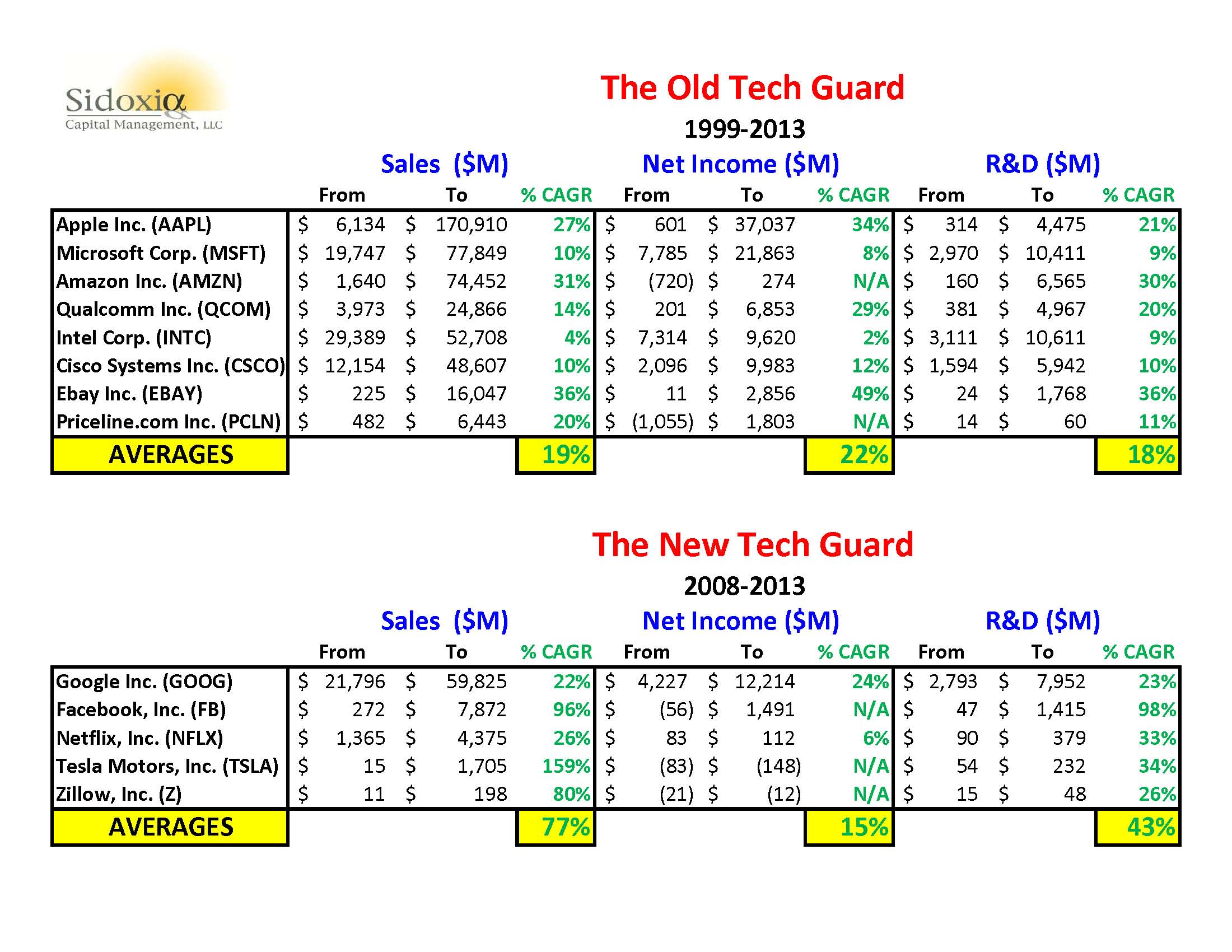

Regardless of how one analyzes the stock market, ultimately long-term stock prices follow the direction of profits and cash flows. Profits and cash flows don’t however grow out of thin air. Sustainable growth requires competitiveness. For most industries, a long-term competitive advantage requires a culture of innovation and technology adoption. As you can see from the NASDAQ listed companies BELOW, there is no shortage of innovation.

CLICK TO ENLARGE

Sources: ADVFN, SEC, Other

I’ve divided the largest technology companies in the NASDAQ 100 index that survived the bursting of the 2000 technology bubble into “The Old Tech Guard.” This group of eight stocks represents a total market value of about $1.5 trillion – equivalent to almost 10% of our country’s Gross Domestic Product (GDP). Incredibly, this select collection of companies achieved an average sales growth rate of +19%; income growth of +22%; and research & development growth of +18% over a 14-year period (1999-2013).

The second group of younger stocks (a.k.a., The New Tech Guard) that launched their IPOs post-2000 have accomplished equally impressive results. Together, these handful of companies have earned a market value of over $625 billion. There’s a reason investors are gobbling up these stocks. Over the last five years, The New Tech Guard companies have averaged an unbelievable +77% sales growth rate, coupled with a remarkable +43% expansion in average annual R&D expenditures.

Innovation Dead?

Who said innovation is dead? Not me. Combined, these 13 companies (Old Guard + New Guard) are spending about $55,000,000,000 on research and development…annually! If you consider the hundreds and thousands of other technology companies that are also investing aggressively for the future, it should come as no surprise that the pace of innovation is only accelerating.

While newscasters, bloggers, and newspapers will continue to myopically focus on the Dow and S&P 500 indices, do your investment portfolio a favor by not forgetting about the relentless R&D and tech revolution taking place within the innovative and often overlooked NASDAQ index.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), AAPL, GOOG, AMZN, FDX, QCOM, and a short position in NFLX, but at the time of publishing SCM had no direct discretionary position in MSFT, INTC, CSCO, EBAY, PCLN, FB, TSLA, Z, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Innovative Bird Keeps All the Worms

Source: Photobucket

As the old saying goes, “The early bird gets the worm,” but in the business world this principle doesn’t always apply. In many cases, the early bird ends up opening a can of worms while the innovative, patient bird is left with all the spoils. This concept has come to light with the recent announcement that social networking site MySpace is being sold for a pittance by News Corp. (NWS) to Specific Media Inc., an advertising network company. Although Myspace may have beat Facebook to the punch in establishing a social network footprint, Facebook steamrolled Myspace into irrelevance with a broader more novel approach. Rather than hitting a home run and converting a sleepy media company into something hip, Rupert Murdoch, CEO of News Corp. struck out and received crumbs for the Myspace sale (News Corp. sold it for $35 million after purchasing for $540 million in 2005, a -94% loss).

Other examples of “winner takes all” economics include:

Kindle vs. Book Stores: Why are Borders and Waldenbooks (BGPIQ.PK) bankrupt, and why is Barnes and Noble Inc. (BKS) hemorrhaging in losses? One explanation may be people are reading fewer books and reading more blogs (like Investing Caffeine), but the more credible explanation is that Amazon.com Inc. (AMZN) built an affordable, superior digital mousetrap than traditional books. I’ll go out on a limb and say it is no accident that Amazon is the largest bookseller in the world. Within three years of Kindle’s introduction, Amazon is incredibly selling more digital books than they are selling physical hard copies of books.

iPod vs. Walkman/MP3 Players: The digital revolution has shaped our lives in so many ways, and no more so than in the music world. It’s hard to forget how unbelievably difficult it was to fast-forward or rewind to a particular song on a Sony Walkman 30 years ago (or the hassle of switching cassette sides), but within a matter of a handful of years, mass adoption of Apple Inc.’s (AAPL) iPod overwhelmed the dinosaur Walkman player. Microsoft Corp.’s (MSFT) foray into the MP3 market with Zune, along with countless other failures, have still not been able to crack Apple’s overpowering music market positioning.

Google vs. Yahoo/Microsoft Search: Google Inc. (GOOG) is another company that wasn’t the early bird when it came to dominating a new growth industry, like search engines. As a matter of fact, Yahoo! Inc (YHOO) was an earlier search engine entrant that had the chance to purchase Google before its meteoric rise to $175 billion in value. Too bad the Yahoo management team chose to walk away…oooph. Some competitive headway has been made by the likes of Microsoft’s Bing, but Google still enjoys an enviable two-thirds share of the global search market.

Dominance Not Guaranteed

Dominant market share may result in hefty short-term profits (see Apple’s cash mountain), but early success does not guarantee long-term supremacy. Or in other words, obsolescence is a tangible risk in many technology and consumer related industries. Switching costs can make market shares sticky, but a little innovation mixed with a healthy dose of differentiation can always create new market leaders.

Consider the number one position American Online (AOL) held in internet access/web portal business during the late nineties before its walled gardens came tumbling down to competition from Yahoo, Google, and an explosion of other free, advertisement sponsored content. EBay Inc. (EBAY) is another competition casualty to the fixed price business model of Amazon and other online retailers, which has resulted in six and a half years of underperformance and a -44% decline in its stock price since the 2004 peak. Despite questionable execution, and an overpriced acquisition of Skype, eBay hasn’t been left for complete death, thanks to a defensible growth business in PayPal. More recently, Research in Motion Ltd. (RIMM) and its former gargantuan army of “CrackBerry” disciples have felt the squeeze from new smart phone clashes with Apple’s iPhone and Google’s Android operating system.

With the help of technology, globalization, and the internet, never in the history of the world have multi-billion industries been created at warp speed. Being first is not a prerequisite to become an industry winner, but evolutionary innovation, and persistently differentiated products and services are what lead to expanding market shares. So while the early bird might get the worm, don’t forget the patient and innovative second mouse gets all the cheese.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, AMZN, and GOOG, but at the time of publishing SCM had no direct position in BGPIQ.PK, NWS, YHOO, MSFT, SNE, AOL, EBAY, RIMM, Facebook, Skype, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Job Losses = Job Creation

Apple Inc. (AAPL) is considered the quintessential innovation company. After all, if you flip over an iPad or an iPhone it will clearly state, “Designed by Apple in California. Assembled in China.” Apple is just too busy innovating to worry about dirtying their hands by assembling products – they can simply outsource that work. Many people have a problem with the millions of manufacturing jobs moving offshore, but if I am the self anointed “Innovation Czar” for the United States, I definitely favor keeping the $120,000 Apple engineering jobs over the low-cost $2 per hour jobs being lost to China (or cheaper developing country). Oh sure, I would prefer keeping both workers, but if push comes to shove, I much rather keep the six-figure job. The bad news is the displaced American iPhone/iPad assembler must find an alternative lower-skilled employment opportunity. The good news is there are plenty of service-based jobs that will NOT get outsourced to the Chinese. If displaced workers are unhappy serving lattes at Starbucks or changing bedpans at the local hospital (or other unglamorous service-based job), then they can choose to retool their skills through education, in order to land higher-paying jobs not getting outsourced.

Bass Ackwards Job Assessment

While I may agree with many points made by Time Magazine’s Fareed Zakaria in his article, The Future of Innovation: Can America Keep Pace?, I think Zakaria is looking at the job trade-off a little backwards. Here is what says about Apple-created job losses in a CNN blog post:

“Apple has about $70 billion in revenues. The company that makes Apple’s products called Foxconn is in China. They have about the same revenue – $70 billion dollars. Apple employees 50,000 people. Foxconn employs 1,000,000 people. So you can have all the innovation you want and tens of thousands of engineers in California benefit, but hundreds of thousands of people benefit in China because the manufacturing has gone there. What does that mean? America needs to innovate even more to keep pace.”

Wow, that’s very altruistic of Apple to create thousands of jobs for Foxconn in Asia, but that $70 billion in Apple revenues likely generates close to 10 times the profits that Foxconn creates (Apple had 24% net profit margins last quarter versus probably a few percent at Foxconn). As Innovation Czar, I’ll gladly take the $20 billion in Apple profits added to the U.S. economy over the last 12 months versus the $2-3 billion profits at Foxconn (my estimate). Let’s be clear, profitable companies add jobs (Apple added over 12,000 employees in fiscal 2010, up +35%) – not weak or uncompetitive companies losing money.

Although the U.S. is losing low-skilled jobs to the likes of Foxconn, guess what those $120k engineering jobs at Apple are creating? Those positions are also generating lots of $12/hour service jobs. When you are paying your workers billions of dollars, like Apple, a lot of those dollars have a way of recirculating through our economy. For instance, if I am a six-figure employee at Apple, I am likely funding leisure jobs in Tahoe for family vacations; supporting jobs at Cheesecake Factory (CAKE) and Chipotle Mexican Grill (CMG) because my demanding schedule at Apple means more take-out meals; and creating jobs for auto workers at Ford (F) thanks to my new SUV purchase.

Margin Surplus Redux

The same arguments I make in the Apple vs. Foxconn comparison are very similar to the case I wrote about in Margin Surplus Retake, which compares the profit and trade deficit dynamics occurring in a $1,000 Toshiba laptop sale. Although Toshiba and its foreign component counterparts may recognize twice the revenues in a common laptop sale as American suppliers (contributing to our country’s massive trade deficit), Intel Corp. (INTC) and Microsoft Corp. (MSFT) generate six times the profits as Toshiba and company. The end result is a massive profit or margin surplus for the Americans – a better barometer to financial reality than stale government trade deficit statistics.

There are obviously no silver bullets or easy answers to resolve these ever-growing economic issues, but as political gridlock grinds innovation to a halt, globalization is accelerating. The rest of the world is racing to narrow the gap of our innovative supremacy, but our sense of entitlement will get us nowhere. Zakaria points out that by 2013, China is expected to overtake the U.S. as the leading scientific research publisher and after we held a three-fold increase in advanced engineering and technology masters degrees in 1995, China surpassed us in 2005 (63,514 in China vs. 53,349 in the U.S.). China may not be home to Facebook or Google Inc. (GOOG), but Baidu Inc. (BIDU) is headquartered in China with a market capitalization of $43 billion and Tencent Holdings is valued at more than $50 billion (not to mention Tencent has roughly the same number of users as Facebook – more than 600 million).

The jobless recovery has been painful for the 14 million unemployed, but there is hope for all, if innovation and education (see Keys to Success) can create more six-figure Apple jobs to offset less valuable jobs lost to outsourcing. In order to narrow the chasm between rich and poor in our country, Americans need to climb the labor ladder of innovation. Contrary to Fareed Zakaria’s assertion, swapping quality job gains with crappy job losses, is an economic trade I would make every day and twice on Sunday. If the country wants to return to the path of economic greatness and sustainable job creation, the country needs to embrace this idea of outsourced creative destruction.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, and GOOG, but at the time of publishing SCM had no direct position in Foxconn, Facebook, MSFT, INTC, CAKE, CMG, F, BIDU, Tencent, Toshiba, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Curing Our Ills with Innovation

Fareed Zakaria thoughts have blanketed both traditional and internet media outlets, spanning everything from Newsweek to Time, and the New York Times to CNN. With an undergraduate diploma from Yale and his PhD from Harvard, Dr. Zakaria has built up quite a following, especially when it comes to foreign affairs.

In his latest Time magazine article, Can America Keep Pace?, Zakaria addresses the role of innovation in the U.S., “Innovation is as American as apple pie.” The innovation lead the U.S. maintains over the rest of the world will not evaporate over night because this cultural instinct is bred into our DNA – innovation is not something you one can learn directly from a textbook, Wikipedia, or Google (GOOG). With that said, the innovation gap is narrowing between developed and developing countries. New York Times columnist Tom Friedman captured this sentiment when he stated the following:

“French voters are trying to preserve a 35-hour work week in a world where Indian engineers are ready to work a 35-hour day.”

The fungibility of labor has pressured industries by transferring jobs abroad to much lower-cost regions like China and India, and that trend is only expanding further into countries with even lower labor cost advantages. Zakaria agrees:

“America’s future growth will have to come from new industries that create new products and processes. Older industries are under tremendous pressure.”

The good news is the United States maintains a significant lead in certain industries. For instance, we Yankees have a tremendous lead in fields such as biotechnology, entertainment, internet technologies, and consumer electronics.

The poster child for innovation is Apple Inc. (AAPL), which arose from the ashes of death ten years ago with its then ground-breaking new product, the iPod. Since then, Apple has introduced many innovative products and upgrades as a result of its research and development efforts, including the recently launched iPad.

The Education Engine

Where we are falling short is in education, which is the foundation to innovation. In a country with a high school system that Microsoft Corp.’s (MSFT) founder Bill Gates calls “obsolete,” society is left with one-third of the students not graduating and nearly half of the remaining graduates unprepared for college. In this instant gratification society we live in, the long-term critical education issue has been pushed to the backburner. Other emerging countries like China and India are churning out more college graduates by the millions, and also dominating us in the key strategic count of engineering degrees.

Government’s Role

With the massive debt and deficits our country currently faces, an ongoing debate about the size and role of government persists. Zakaria makes the case that government must place a significant role when it comes to innovation. Unfortunately, the U.S. wastes billions on pork-barrel projects and suboptimal subsidies while dilly-dallying in political gridlock over critical investments in education, infrastructure spending, basic research, and energy policies. In the meantime, our fellow competing countries are catching up to us, and in certain cases passing us (e.g., alternative energy investments – see Electric Profits).

Zakaria makes this point on the subject:

“The fastest-growing economies are all busy using government policy to establish commanding leads in one industry after another. Google’s Eric Schmidt points out that ‘the fact of the matter is, other countries are putting a lot more money into nurturing new industries than we are, and we are not going to win unless we do something like what they’re doing.’”

As a matter of fact, an ITIF (Information Technology & Innovation Foundation) study measuring innovation improvement from 1999 to 2009, as it related to government funding for basic research, education and corporate-tax policies, ranked the U.S. dead last out of 40 countries.

Not All is Lost – Pie Slice Maintained

Source: Carpe Diem

Although the outlook may sounds bleak, not all is lost. In a recent Wall Street Journal interview with Bob Doll Chief Equity Strategist at the world’s largest money management company (BlackRock has $3.6 trillion in assets under management), he makes the case that the U.S. remains the leading source of technological innovation and home to the greatest universities and the most creative businesses in the world. He sees this trend persisting in part because of our country’s relative demographic advantages:

“Over the next 20 years, the U.S. work force is going to grow by 11%, Europe’s going to fall by five, and Japan’s going to fall by 17. This alone tells me the U.S. has a huge advantage over Europe and a bigger one over Japan for growth.”

So while emerging markets, like those in Asia, continue to gain a larger slice of the global GDP pie, Mark Perry at Carpe Diem shows how the U.S has maintained its proportional slice of a growing global economic pie, over the last four decades.

Growth is driven by innovation, and innovation is driven by education. If America wants to maintain its greatness, the focus needs to be placed on innovation-led growth. The world is moving at warp speed, and our neighbors are moving swiftly, whether we come along for the ride or not. The current, sour conversations regarding deficits, debt ceilings, entitlements, wars, and unemployment are all essential discussions, but more importantly, if these debates can be refocused on accelerating innovation, the country will be well on its way to curing its ills.

See also Our Nation’s Keys to Success

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and AAPL, but at the time of publishing SCM had no direct position in MSFT, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}