Posts tagged ‘imports’

Animal Spirits to Animal Hibernation

Investor mood or sentiment can change rather quickly. Immediately after the 2024 presidential elections, positive animal spirits catapulted the stock market higher due to hopes of stimulating tax cuts and deregulation legislation. However, those warm and fuzzy feelings soured last month, as investor focus shifted to on-again, off-again tariff talks, and stagflation concerns, which have converted animal spirits into gloomy feelings of hibernation.

As a result, the advancing bull market took a breather and transformed into a weary bear during March. For the month, the S&P 500 (-5.8%), NASDAQ (-8.2%), and the Dow Jones Industrial Average (-4.2%) all fell significantly in the wake of tariffs, inflation, and recession worries.

Lovely Liberation Day or Tariff Trouble?

Since the President took office in January, he has announced, reversed, and implemented tariffs across a wide range of countries and sectors, including China, Canada, Mexico, the EU, Colombia, Venezuela, steel, aluminum, oil, automobiles, digital services taxes, and more.

The day of reckoning begins on April 2nd, designated Liberation Day by the president. This is when the president and the White House officially announce global reciprocal tariffs on foreign countries in an attempt to reverse the nation’s large trade deficit (see chart below) and bring manufacturing back to the United States. For example, if Germany subsidizes BMW cars sold in the U.S. while simultaneously placing tariffs (i.e., additional taxes) on American Ford Explorers sold in Germany, the president wants to impose equivalent reciprocal tariffs on those same BMWs sold in the U.S. in an effort to level the trading playing field. On the surface, a $131 billion trade deficit sounds very significant, but when compared to a $30 trillion economy (Gross Domestic Product – GDP), this negative trade balance represents less than 0.5% of GDP – effectively a rounding error. I have previously written how tariffs represent more of a molehill than a mountain (see Tariff Sheriff), in part because consumer spending and services make up the vast majority of our country’s economic activity, whereas trade and manufacturing are relatively smaller segments.

Source: Trading Economics

Driving home the point that tariffs are more bark than bite, Senior White House trade and manufacturing counselor Peter Navarro recently stated the 2025 tariffs could add $700 billion annually to U.S. revenues, including $100 billion from the recently announced 25% auto tariffs. Many economists believe this collection estimate is too optimistic. However, even if this target is achievable, $700 billion only represents a measly 2% of overall GDP.

Tariffs = Recession or Stagflation?

With the recent stock market downdraft and growing concerns related to tariffs, some economists and pundits are raising the probability of a recession and the possibility of inflation accompanying an economic downturn (i.e., stagflation).

Economic data should clear some of the fog. Fresh employment numbers will be released this Friday, which should shine some light on the health of the economy. Irrespective of this month’s results, the most recent 4.1% unemployment rate (see chart below), though slightly higher over the last two years, does not strongly indicate a recession.

Source: Trading Economics

Other “hard” data, such as GDP, also suggest a slowing economy rather than a recession. For instance, a recent survey of 14 economists estimates the economy is growing at a paltry +0.3% rate in Q1 – 2025 versus +2.3% in Q4 – 2024. Data is continually changing, but if a looming recession were imminent, corporate earnings would likely be trending downward, not upwards, as evident in the chart below.

Source: Yardeni Research

Tariff Inflation Has Yet to Arrive

There is no doubt tariffs function as a tax hike on consumers because U.S. companies that pay the tariffs on imported goods are eventually forced to raise prices to maintain profit margins or limit margin degradation.

Nonetheless, inflation did not spike under President Trump’s first term. Even if the president’s new policies result in more aggressive tariff actions this go-around, inflation will likely remain in check due to the point mentioned earlier – imported goods represent a small percentage of overall consumer and business purchases.

Tariff implementation is just beginning, so only time will tell how pervasive inflation will become. However, what we do know now is that inflation has declined dramatically over the last couple of years and has not yet spiked (see Consumer Price Index chart below).

Source: Calafia Beach Pundit

Where Could I Be Wrong?

I have explained how some of the lagging “hard” data does not signal recession or stagflation, but what could I be missing? For starters, some of the leading “soft” data (e.g., surveys) indicate various cracks in the economic foundation are forming. Take the recent Consumer Confidence data (see chart below), which has weakened dramatically from pre-COVID and even post-COVID levels.

Source: Trading Economics

It’s not just consumers who are feeling uneasy about the economic environment; businesses are as well. Another soft data point flashing red is the NFIB Small Business Uncertainty index, which recently reported its second-highest reading in 48 years (see chart below). Even if my argument that tariffs are too small to materially impact the economy holds, if the psychological effects of tariff uncertainty paralyzes consumer and business economic activity to a standstill, then tariffs could indeed become a substantial factor.

Source: National Federation of Independent Business (NFIB)

What Comes Next After Liberation Day?

Liberation Day is unlikely to trigger an immediate and sustained V-shaped recovery in the stock market because international trading partners will be forced to announce retaliatory tariffs in response to President Trump’s reciprocal tariffs, potentially leading to additional reactionary tariffs by the U.S.

Additionally, the reciprocal tariffs announced on April 2nd will likely serve as a starting point for subsequent negotiations with trading partners. Without a comprehensive resolution, investor sentiment will likely remain somewhat unresolved and unsettled. Regardless of your views on the size and impact of tariffs, Liberation Day will at least bring some clarity and reduce the uncertainty surrounding the current murky and chaotic environment.

The multi-year bull market continued its charge after the presidential election, but investor sentiment has weakened the bull run due to tariff uncertainty. In response, the excited bull has temporarily turned into a sleepy bear. Depending on how these tariff events unfold, we will soon find out whether Liberation Day will awaken the bear to hunt for bulls or send it into deep hibernation.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in F or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

Par for the Course

Stocks have been in a multi-year bull market, but just as investors cannot earn positive returns every month, golfers also cannot achieve a hole-in-one or birdie on every hole, either. A challenging performance is exactly what happened last month when stocks recorded a bogey on the scorecard.

More specifically, this is how far out-of-bounds the major indexes were last month:

- S&P 500: -1.4%

- Dow Jones Industrial Average -1.6%

- NASDAQ: -4.0%

Technology stocks and the Magnificent 7 stocks felt the largest brunt of the force last month as tariffs and the impact of Chinese AI (Artificial Intelligence) competition gave investors heartburn as they digested the information (see New Year, New AI ERA & New Tariff Sheriff).

Tariffs – More Molehill Than Mountain

As mentioned, a large part of last month’s volatility can be explained by the policy uncertainty surrounding the impending tariffs on China, Canada, and Mexico. Despite the absence of new tariffs being implemented, in an attempt to lock in cheaper imported goods, U.S. corporations and consumers have been stockpiling foreign goods before prices move higher due to tariffs. The 25% proposed tariffs on Canadian and Mexican goods are set to be applied as soon as March 4th. A flat 25% tariff on imported steel and aluminum products is expected to begin on March 12th – these particular tariffs are expected to have a disproportionately negative impact on the automotive industry.

Regarding other proposed reciprocal trade agreements, the White House’s analysis on tariffs for all other countries (beyond China, Canada, and Mexico) is expected to arrive on the president’s desk on April 2nd.

All these proposed changes are having an immediate economic impact whether intended or not. Not only are consumers buying more overseas products now, as they brace for higher prices, but businesses are also shifting supply chains to countries outside of China, Canada, and Mexico, in hopes of finding temporary tariff loopholes.

The bottom-line is our country’s imports have been spiking up recently, especially in the first quarter. Imports by definition subtract from America’s economic activity, so if businesses and consumers are rationally stockpiling foreign goods before prices go up from tariffs, investors should not be surprised that GDP (Gross Domestic Product) growth is set to go negative in the first quarter (-1.5%), according to the Federal Reserve Bank of Atlanta.

This short-term spike in foreign product purchases should be temporary until the tariffs are officially put in place. Subsequently, demand for relatively cheaper U.S. goods should rise because foreign goods will be pricier. In other words, buyers may begin purchasing more American-made t-shirts on Amazon because those shirts could be cheaper than the Chinese-made t-shirts after the additional tariffs commence on China.

How large are these overall tariffs? When it comes to Mexico and Canada, the size of these countries’ imports is estimated at $918 billion (see the 2023 import breakdown below for the two countries). On the surface, this sounds like a very large number, and it is. However, if you consider the size of the U.S. GDP ($29.4 trillion), these tariffs will mathematically have less than a 1% impact on the direction of our country’s economic activity.

However, if demand for American products goes up after the tariffs begin, as mentioned above, then it is perfectly logical to expect the drag from imports can be diminished or possibly completely reversed, if consumers decide to buy more American goods.

Source: Visual Capitalist

Also worth noting, as I documented last month in my Investing Caffeine blog, imports only account for 13.9% of our country’s economic activity (see New Tariff Sheriff). So, while tariffs make for great scary headlines, the reality of the numbers paints a different picture. Overall, the uncertainty surrounding the discussion of tariffs is having a much larger economic impact than the actual tariffs themselves. In other words, what we are discussing is more molehill than mountain. We saw this same movie before during the administration’s first-term when tariffs did not crater the economy into recession or create disproportionately high inflation.

War at the White House

A geopolitical soap opera played out on global television last Friday during a meeting between Ukraine’s President Volodymyr Zelensky and President Trump in the Oval Office. The meeting was designed to be a celebratory signing of a minerals deal in which the U.S. would gain access to strategically important Ukrainian rare earth metals in exchange for continued U.S. aid and military support. A signed deal would increase the probability of a peace deal between Russia and Ukraine dramatically. What actually happened was a war of words at the White House, which resulted in Zelensky getting kicked out of the White House with no signed deal.

Both sides have economic and strategic incentives to reengage in peace and mineral deal negotiations, but if the U.S.-Ukraine relationship totally crumbles, Europe and the other NATO (North Atlantic Treaty Organization) countries will need to pick up the slack in their military and economic aid to Ukraine. Regardless, increased European support is required to stave off a broader incursion by Russia and Vladimir Putin into a wider portion of Europe.

Tariffs, the Russia-Ukraine war, and AI issues may have heightened investor anxiety last month, but long-term investors understand that annual -5% and -10% corrections in the equity markets are considered par for the course. In fact, over the last 12 months, the S&P 500 index has declined -5% five times, and -10% one time, yet the stock market is still up +16% on a trailing 12-month basis (see chart below).

Source: Trading Economics

Financial markets end up in the rough plenty of the time, which often results in performance scorecard bogeys. However, long-term investors and Sidoxia Capital Management clients have won more often than not because the benefits of American capitalism have created many more birdies and pars over time.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 3, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in META, NVDA, certain exchange traded funds (ETFs), but at the time of publishing had no direct position in BABA or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

Trade War Bark: Hold Tight or Nasty Bite?

In recent weeks, President Trump has come out viciously barking about potential trade wars, not only with China, but also with other allies, including key trade collaborators in Europe, Canada, and Mexico. What does this all mean? Should you brace for a nasty financial bite in your portfolio, or should you remain calm and hold tight?

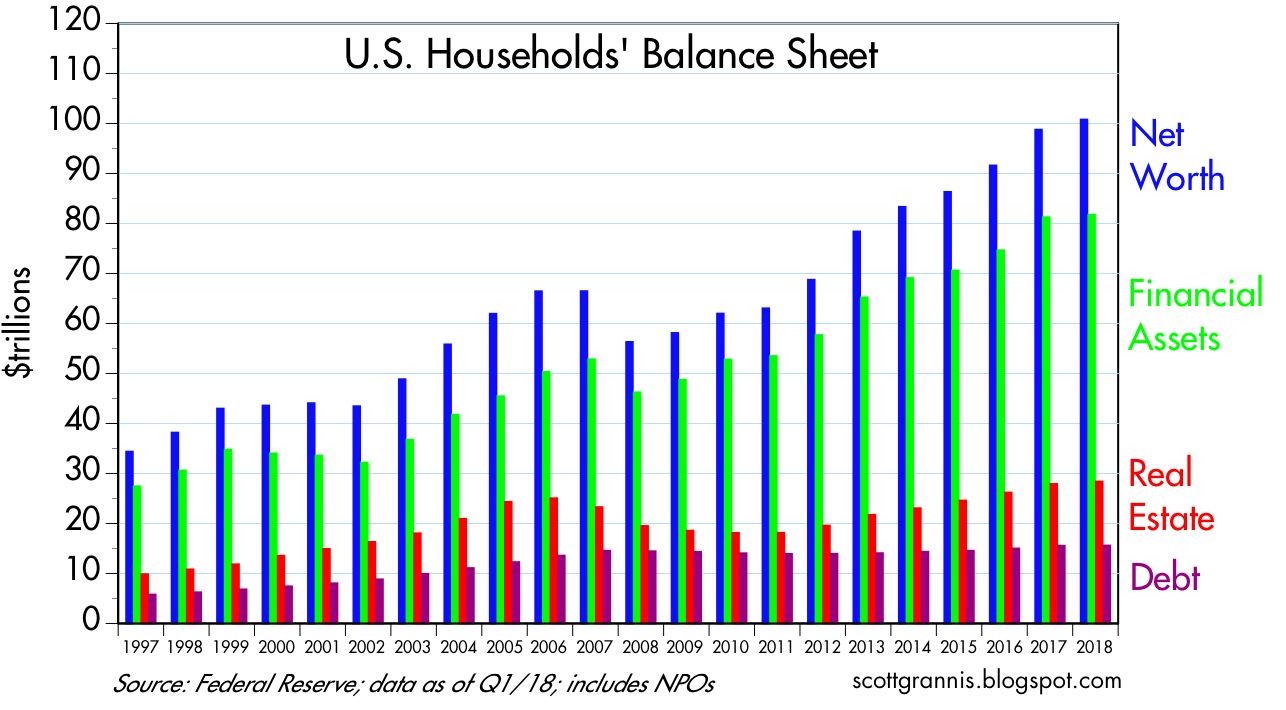

Let’s take a closer look. Recent talks of trade wars and tit-for-tat retaliations have produced mixed results for the stock market. For the month, the S&P 500 index advanced +0.5% (+1.7% year-to-date), while the Dow Jones Industrial Average modestly retreated -0.6% (-1.8% YTD). Despite trade war concerns and anxiety over a responsibly cautious Federal Reserve increasing interest rates, the economy remains strong. Not only is unemployment at an impressively low level of 3.8% (tying the lowest rate seen since 1969), but corporate profits are at record levels, thanks to a healthy economy and stimulative tax cuts. Consumers are feeling quite well regarding their financial situation too. For instance, household net worth has surpassed $100 trillion dollars, while debt ratios are declining (see chart below).

Source: Scott Grannis

Although trade is presently top-of-mind among many investors, a lot of the fiery rhetoric emanating from Washington should come as no surprise. The president heavily campaigned on the idea of reducing uniform unfair Chinese trade policies and leveling the trade playing field. It took about a year and a half before the president actually pulled out the tariff guns. The first $50 billion tariff salvo has been launched by the Trump administration against China, and an additional $200 billion in tariffs have been threatened. So far, Trump has enacted tariffs on imported steel, aluminum, solar panels, washing machines and other Chinese imports.

It’s important to understand, we are in the very early innings of tariff implementation and trade negotiations. Therefore, the scale and potential impact from tariffs and trade wars should be placed in the proper context relative to our $20 trillion U.S. economy (annual Gross Domestic Product) and the $16 trillion in annual global trade.

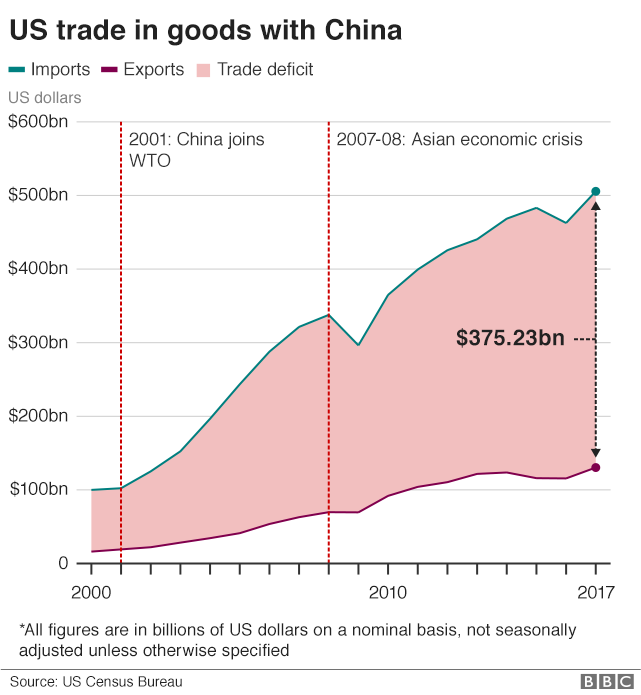

Stated differently, even if the president’s proposed $50 billion in Chinese tariffs quadruples in value to $200 billion, the impact on the overall economy will be minimal – less than 1% of the total. Even if you go further and consider our country’s $375 billion trade deficit with China for physical goods (see chart below), significant reductions in the Chinese trade deficit will still not dramatically change the trajectory of economic growth.

Source: BBC

The Tax Foundation adds support to the idea that current tariffs should have minimal influence:

“The tariffs enacted so far by the Trump administration would reduce long-run GDP by 0.06 percent ($15 billion) and wages by 0.04 percent and eliminate 48,585 full-time equivalent jobs.”

Of course, if the China trade skirmish explodes into an all-out global trade war into key regions like Europe, Mexico, Canada, and Japan, then all bets are off. Not only would inflationary pressures be a drag on the economy, but consumer and business confidence would dive and they would drastically cut back on spending and negatively pressure the economy.

Most investors, economists, and consumers recognize the significant benefits accrued from free trade in the form of lower-prices and a broadened selection. In the case of China, cheaper Chinese imports allow the American masses to buy bargain toys from Wal-Mart, big-screen televisions from Best Buy, and/or leading-edge iPhones from the Apple Store. Most reasonable people also understand these previously mentioned consumer benefits can be somewhat offset by the costs of intellectual property/trade secret theft and unfair business practices levied on current and future American businesses doing business in China.

Trump Playing Chicken

Right now, Trump is playing a game of chicken with our global trading partners, including our largest partner, China. If his threats of imposing stiffer tariffs and trade restrictions result in new and better bilateral trade agreements (see South Korean trade deal), then his tactics could prove beneficial. However, if the threat and imposition of new tariffs merely leads to retaliatory tariffs, higher prices (i.e., inflation), and no new deals, then this mutually destructive outcome will likely leave our economy worse off.

Critics of Trump’s tariff strategy point to the high profile announcement by Harley-Davidson to move manufacturing production from the United States to overseas plants. Harley made the decision because the tariffs are estimated to cost the company up to $100 million to move production overseas. As part of this strategy, Harley has also been forced to consider motorcycle price hikes of $2,200 each. On the other hand, proponents of Trump’s trade and economic policies (i.e., tariffs, reduced regulations, lower taxes) point to the recent announcement by Foxconn, China’s largest private employer. Foxconn works with technology companies like Apple, Amazon, and HP to help manufacture a wide array of products. Due to tax incentives, Foxconn is planning to build a $10 billion plant in Wisconsin that will create 13,000 – 15,000 high-paying jobs. Wherever you stand on the political or economic philosophy spectrum, ultimately Americans will vote for the candidates and policies that benefit their personal wallets/purses. So, if retaliatory measures by foreign countries introduces inflation and slowly grinds trade to a halt, voter backlash will likely result in politicians being voted out of office due to failed trade policies.

Source: Dr. Ed’s Blog

Time will tell whether the current trade policies and actions implemented by the current administration will lead to higher costs or greater benefits. Talk about China tariffs, NAFTA (North American Free Trade Agreement), TPP (Trans Pacific Partnership), and other reciprocal trade negotiations will persist, but these trading relationships are extremely complex and will take a long time to resolve. While I am explicitly against tariff policies in general, I am not an alarmist or doomsayer, at this point. Currently, the trade war bark is worse than the bite. If the situation worsens, the history of politics proves nothing is permanent. Circumstances and opinions are continually changing, which highlights why politics has a way of improving or changing policies through the power of the vote. While many news stories paint a picture of imminent, critical tariff pain, I believe it is way too early to come to that conclusion. The economy remains strong, corporate profits are at record levels (see chart above), interest rates remain low historically, and consumers overall are feeling better about their financial situation. It is by no means a certainty, but if improved trade agreements can be established with our key trading partners, fears of an undisciplined barking and biting trade dog could turn into a tame smooching puppy that loves trade.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 3, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, AMZN, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in WMT, HOG, HPQ, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Drought in Higher Rates May Be Over

The drought in higher interest rates may be nearing an end? Ever since the global financial crisis accelerated into full force in the fall of 2008, there were a constant flow of coordinated interest rate cuts triggered around the world with the aim of stimulating global GDP (Gross Domestic Product) and improving credit flow through the clogged financial pipes. Central banks across the world cut key benchmark interest rate levels and the impact of these reductions has a direct influence on what consumers pay for their financial products and services. More recently, we have begun to see the reversal of previous cuts with rate hikes witnessed in several international markets. Last week we saw Norway become the first western European country to raise rates, following an earlier October rate lift by Australia and another by Israel in August. For some countries, the sentiment has switched from global collapse fears to a stabilization posture coupled with future inflation concerns. In the U.S., the data has been more mixed (read article here) and the Federal Reserve has been clear on its intention to keep short-term rates at abnormally low levels for an extended period of time. That stance would likely change with evidence of inflationary pressures or improved job market conditions.

What Does This Mean for Consumers?

Prior to the financial crisis, credit availability flourished at affordably low rates. Now, with signs of a potential global recovery matched with regulatory overhauls, consumers may be impacted in several financial areas:

1) Credit Card Rates: Beyond regulatory changes in Washington (read more), the interest rate charged on unpaid credit card balances may be on the rise. When the Federal Reserve inevitably raises the targeted Federal Funds Rate (the interest rate for loans made between banks) from the current target rate range of 0.00% and 0.25%, this action will likely have direct upward pressure on consumer credit card rates. The associated increase in key benchmark rates such as the Prime Rate (the rate charged to a bank’s most creditworthy customers) and LIBOR (London Interbank Offer Rate) would result in higher monthly interest payments for consumers.

2) Other Consumer Loans: Many of the same forces impacting credit card rates will also impact other consumer loans, like home mortgages and auto loans. Pull out your loan documents – if you have floating or variable rate loans then you may be exposed to future hikes in interest rates.

3) Business Loans / Lines of Credit: Business owners -not just consumers – can also be impacted by rising rates. When the cost of funding goes up (.i.e., interest rates), the banks look to pass on those higher costs to the customer so the account profitability can be maintained.

4) Dollar & Import Prices: To the extent subsequent United States rate hikes lag other countries around the world, our dollar runs the risk of depreciating more in value (currency investors, all else equal, prefer currencies earning higher interest rates). A weaker dollar translates into foreign goods and services costing more. If international central banks continue to raise rates faster than the U.S., then imported good inflation could become a larger reality.

5) Hit to Bond Prices: Higher interest rates can also result in a negative hit to your bond portfolio. Higher duration bonds, those typically with longer maturities and lower relative coupon payments, are the most vulnerable to a rise in interest rates. Consider shortening the duration of your portfolio and even contemplate floating rate bonds.

Interest rates are the cost for borrowed money and even with the recent increase in consumers’ savings rate, consumers generally are still saddled with a lot of debt. Do yourself a favor and review any of your credit card agreements, loan documents, and bond portfolio so you will be prepared for any future interest rate increases. Shopping around for better rates and/or consolidating high interest rate debt into cheaper alternatives are good strategies as we face the inevitable end in the drought of higher global interest rates.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}