Posts tagged ‘hedge funds’

Market Drops as GameStop Pops

The stock market started with a bang this year with the S&P 500 index at first climbing +3% in January before ending with a whimper and a monthly decline of -1%. This performance followed a strong finish to a wild 2020 presidential election year (the S&P 500 rose +16%). There has been plenty of focus on the coronavirus health crisis and vaccine distribution (100 million doses in 100 days), along with debates over a $1.9 trillion proposed relief package by newly elected President Joe Biden, but there has been another story stealing attention in the financial market headlines…GameStop.

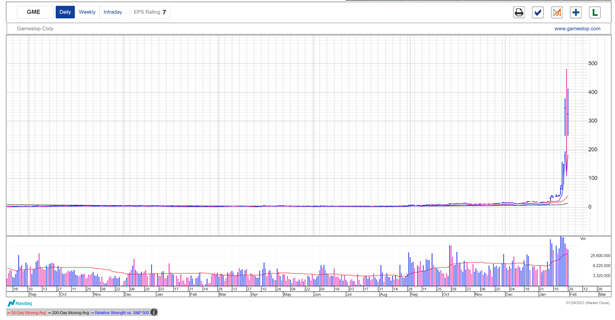

If a global pandemic and a populist attack on the Capitol were not enough for investors, the Reddit (WallStreetBets) and Robinhood revolution coordinated a mass attack on privileged hedge funds and short sellers by squeezing out-of-favor stocks like GameStop (Ticker: GME) to stratospheric levels (up +1,625% to $325/share in January alone) causing an estimated $20 billion of losses for many wealthy elites. To put the meteoric rise into perspective, before GameStop shares reached $325, the stock was valued below $20/share last month and has climbed more than 100x-fold from a low $2.57/share nine months ago (see chart below).

What Exactly Happened?

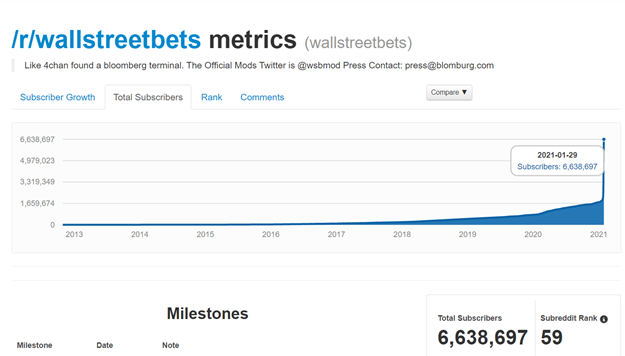

Well, millions of users on the social media platform Reddit banded together on a forum called “wallstreetbets” (see graphic below). WallStreetBets was established in 2012 and had approximately 1 million subscribers at the beginning of 2021 – today it has more than 7 million subscribers. Millions of these anti-establishment WallStreetBets followers effectively colluded together to inflate the share price of GameStop by ganging up on the many short sellers who were betting that GameStop share price would drop. In other words, Reddit-Robinhood buyer gains led to short seller losses. One hedge fund in particular, Melvin Capital, lost billions of dollars on its GameStop short bet and saw its fund performance decline by a whopping -53% in one month…ouch!

The Reddit WallStreetBets forum may have served as the match in this wildfire, but in order to trigger an inferno, a brokerage account is needed. A trading platform allows individual traders on Reddit to level the playing field against the hedge fund professionals and short sellers. The fuel for the GameStop detonation was Robinhood, a fintech (Financial Technology) brokerage firm founded in Silicon Valley in 2013 by two Stanford University graduates. The mission of the company is to “democratize finance for all.” But let’s not forget what Thomas Jefferson noted, “A democracy is nothing more than mob rule, where fifty-one percent of the people may take away the rights of the other forty-nine.” The Reddit-Robinhood mob certainly proved this point.

Although Robinhood was initially seen as a saint in the free trading revolution, eventually many of the brokerage company’s disciples became disenfranchised. Many users subsequently turned on the company and considered Robinhood a villain that was rigging the system when CEO Vlad Tenev halted the ability of its 13+ million users to buy GameStop shares.

Many traders came to the conclusion that Robinhood was working to save the perceived hedge fund bad guys by the firm temporarily terminating user purchases in GameStop stock. Mr. Tenev blamed regulatory capital requirements as a reason for disallowing Robinhood-ers to buy GameStop last week, which was a major contributing factor to why the stock price plummeted by -44% on January 28th. The following day, Robinhood partially reversed its stance and subsequently allowed minimal daily purchases of one share.

How Does Short Selling Work?

In the stock market, you can make gains by buying shares that go up in price, or you can make profits by short selling shares that go down in price. If you buy a stock, the most money you could lose is -100% of your original investment. For example, if you invest $1,000 into GameStop stock by buying 50 shares at $20 each, if the stock price goes to $0, the most the investor/trader could lose is 100% of their $1,000 original investment.

On the flip side, if you short a stock, the potential losses are limitless. For example, if you (or a hedge fund manager) shorts $1,000 of GameStop stock by selling 50 shares short at $20 each, if the stock price goes to $60, the short seller just loss -200% of their original investment [($20/shr – $60/shr) X 50 shares] = -$2,000. If GameStop goes to $100, the short seller loses -400%, and if GameStop price goes to $220, the short seller loses -1,000%. As you can see, the higher the price goes, there are infinite potential losses of the investor, trader, or hedge fund manager.

If a stock price continues to move higher, the only way for a short seller to stop the bleeding (i.e., close their short position or “bet”) is to buy shares. As a reminder, a buyer of stock closes their position by selling shares after they originally buy shares. A short seller closes their position by buying shares after they initially sell shares short. So again, if GameStop share price continues to move higher, the only way for GameStop short sellers to stop their losses is to buy more GameStop shares. This is the equivalent of pouring gasoline on a blazing fire because as millions of Reddit/Robinhood-ers are pushing GameStop’s share price higher almost every day, short selling hedge fund managers are left scrambling for the exits and forced to close their positions at even higher prices (i.e., larger losses).

What Does This All Mean?

Whether you are talking about speculation in Bitcoin, the rise of SPACs (Special Purpose Acquisition Companies), the increase in the number of IPOs (Initial Public Offerings), or the Reddit-Robinhood Revolution, risk appetite has been on the rise and long-term investors should proceed very cautiously. Just as many have experienced on trips to Las Vegas, big winnings can quickly turn to huge losses. Although it’s certainly fun to watch the individual Davids take down the hedge fund/short selling Goliaths, if the Reddit-Robinhood community gets too aggressive in its speculation, history shows us they will end up being the ones swimming in their tears or stoned to death.

If you need assistance navigating through all these land mines, please give us a call at Sidoxia Capital Management (949-258-4322) for a complimentary portfolio review.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME, AMC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Fine Tuning Your Stock Fishing Skills

If you are one of those fishing hobbyists crowded among a large group while hunting for a big fish, mathematics dictates your odds of reeling in a grand prize are significantly diminished. Expert fishermen are generally the first to arrive because they understand once the masses appear the opportunities will disappear. Like big fish, colossal stocks are rarely discovered by a large herd of investors. Financial bubbles occur in this manner, however these periods are usually short-lived and the investor pack often ends up losing more money on the way down relative to the profits earned on the way up. Successful investors are usually the ones following a disciplined systematic approach that is often contrarian in nature. In other words, not chasing performance requires patience, an elusive quality in these fast-paced, frenetic financial markets.

More prevalent in these markets are impulsive day-traders, unruly high frequency traders, and tempestuous hedge funds. Why own stocks, if you can rent them? Like a fisherman who constantly casts his/her bait in and out of the water, a short-sighted investor cannot realize outsized gains, unless the bait is given sufficient time to lure (find) the next winning idea.

Like many professions, experts often optimally mix the quantitative science and behavioral art of their craft. Whether it’s a teacher, doctor, accountant, attorney, or bus driver, the people who excel in their profession are the ones who move beyond the statistical and procedural basics of their trade. Practicing and understanding the nuts and bolts of your job is important, but developing those intangible, artistic skills only comes with experience. Unfortunately, many investing hobbyists don’t appreciate these artistic nuances and as a result go on destroying their portfolios, even though they act as if they were experts.

On the flip-side, decisions purely based on gut instincts will also lead to sub-par outcomes. The fisherman who does not account for the wind, temperature, geography, light, and seasonal differences will be at a distinct disadvantage to those who have studied these scientific factors.

In the fishing world, there is no miracle GPS device that will guide fish onto your hook, and the same is true for stocks. No software package or technical pattern will be a panacea for profits, however having some type of scientific tool to assist in the identification of investment opportunities should be exploited to its fullest. For us at Sidoxia Capital Management (www.Sidoxia.com), our tool is called SHGR (pronounced “SUGAR”), or Sidoxia Holy Grail Ranking. The name was created tongue-in-cheek; however its purpose is crucial. Following a quantitative system like SHGR ensures that a healthy dosage of discipline and objectivity is factored into our investment decisions, so inherent biases do not creep into our process and detract from performance. Specifically, our proprietary SHGR model incorporates multiple factors, including valuation, growth, sentiment indicators, profitability, and other qualitative measurements.

Although we use a “Holy Grail” ranking system, the fact of the matter is there are none in existence – for fishermen or investors. Experience teaches us the best opportunities are found where few are looking, and if proper quantitative tools are integrated into a multi-pronged process, then you will be uniquely positioned to catch a big fish.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and CMCSA, but at the time of publishing SCM had no direct position in BRKB, HNZ, HRL, UL, T, VZ, CAR, ZIP, AMR, LCC, ORCL, APKT, DELL, MSFT, RDSA, Repsol, ODP, OMX, HLF, BUD, STZ, GE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Opal Conference: Hedge Fund Heaven and Regulatory Rules

The recent Alternative Investment Summit held December 5-7 at the Ritz-Carlton in Laguna Niguel, California provided a little bit of everything for attendees – including a slice of hedge fund heaven and a less appetizing dollop of regulatory rules. If you are going to work hard, why not do it in an unrivaled, picturesque setting along the sandy shores of Dana Point? The well-attended conference, which was hosted by Opal Financial Group, was designed to address the interests of a broad set of constituents in the alternative investment food-chain, including representatives of hedge funds, fund of funds, endowments, consulting firms, private equity firms, venture capital firms, commodity trading advisors (CTAs), law firms, family offices, pension funds, along with various other vendors and service providers.

Although the topics and panel experts covered diverse areas, I found some interesting common themes emanating from the conference:

1) Waterboard Your Manager: In the wake of the Bernie Madoff Ponzi scheme and the recent sweeping insider trading investigations, institutional investors are having recurring nightmares. Consultants and other service-based intermediaries are feeling the heat in a fever-pitched litigation environment that is driving defensive behavior to avoid “headline risk” at any cost. As a result, institutional investors and fund of funds are demanding increased transparency and immediate liquidity in addition to conducting deeper, more thorough due diligence. One consultant jokingly said they will “waterboard” managers to obtain information, if necessary. In the hedge fund world, this risk averse stance is leading to a concentrated migration of funds to large established funds – even if those actions may potentially compromise return opportunities. In response to a question about insider trading investigations as they relate to client fund withdrawals, one nervous panel member advised clients to “shoot first, and ask questions later.”

2) Lurking Mountain of Maturity: Default rates in the overall bond markets have been fairly tame in the 2.0 – 2.5% range, however a mountain of previously issued debt is expected to mature over the next few years, meaning many of those corporate issuers will need to refinance the existing debt and issues longer term debt. For the most part, capital markets have been accommodating a large percentage of issuers, due to investors’ yield-hungry appetite. If the capital markets seize up and the banks continue lending like the Grinch, then the default rate could certainly creep up.

3) CLO Market Gaining Steam: The collateralized loan obligation market is still significantly below pre-crisis levels, however an estimated $3.5 billion 2010 new issue market is expected to gain even more momentum into 2011. New issuance levels are expected to register in at a more healthy $5.0 billion level next year.

4) Less Fruit in Debt Markets: The general sense among fund managers was that previously attractive bond prices have risen and bond yield spreads have narrowed. The low hanging fruit has been picked and earning similarly attractive returns will become even more challenging in the coming year, despite benign default rates. Even though bonds face a tough challenge of potential future interest rate increases, many managers believe selective opportunities can still be found in more illiquid, distressed debt markets.

5) Fund of Funds vs. Consultants: Playing in the sandbox is getting more crowded as some consultants are developing in-house investment solutions while fund of funds are advancing their own internal capabilities to target institutional investors directly. By doing so, the fund of funds are able to cut out the middle-man/woman consultant and keep more of the profit pie to themselves. From a plan sponsor perspective, institutional investors struggle with the trade-offs of investing in a diversified fund of funds vehicle versus aggregating the unique alpha generating capabilities of individual hedge fund managers.

6) Emerging Frontier Markets: There was plenty of debate about the dour state of global macroeconomic trends, but a healthy dose of optimism was injected into the discussion about emerging markets and the frontier markets. One panel member referred to the frontier markets as the Rodney Dangerfield (see Doug Kass) of the world (i.e., “get no respect”). The frontier markets are like the immature little brothers of the major emerging markets in China, India, Brazil, and Russia. Examples of frontier markets provided include Vietnam, Nigeria, Bangladesh, and Kenya. In general, these markets are heavily dependent on natural resources and will move in unison with supply-demand adjustments in larger markets like China. Of the approximately 80 frontier markets around the globe, 30 were described as uninvestable, with the remaining majority offering interesting prospects.

All in all the Opal Financial Group Alternative Investment Summit was a huge success. Besides becoming immersed in the many facets of alternative investments, I met leading thought leaders in the field, including an unexpected interaction with a world champion and living legend (read here for a hint). Many conferences are not worth the price of admission, but with global economic forces changing at breakneck speed and regulatory rules continually unfolding in response to the financial crisis, for those involved in the alternative investment field, this is one event you should not miss.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) is the General Partner of the Slome Sidoxia Fund, LP, a long-short hedge fund. SCM and some of its clients also own certain exchange traded funds (including emerging market ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Females in Finance – Coming Out of Hibernation

I’m not sure if you are like me, but the annual media ritual of myopically breaking down the sale of every shoe, belt, cell phone, television, and pair of underwear during the November/December holiday season can become very grating. What makes it a little easier for me to swallow is the stable of attractive female retail analysts who are finally unleashed from their long hibernation slumbers to review their mall traffic and parking satellite findings. I’m a happily married man, but I still cannot complain about seeing these multi-threat beauties dissect sales trends and fashion fads. However, in this day and age, I’m not so sure that females feel the same way about their under-representation in the finance field?

If there are 155.8 million females in the United States and 151.8 million males (Census Bureau: October 2009), then how come only 6% of hedge fund managers (BusinessWeek), 8% of venture capitalists, and 15% of investment bankers are female (Harvard Magazine)? Is the finance field just an ol’ boys network of chauvinist pig-headed males who only hire their own? Or do the severe time-demands of the field force females to opt-out of the industry due to family priorities?

Although I’m sure family choices and quality of life are factors that play into the decision of entering the demanding finance industry, from my experience I would argue women are notoriously underrepresented even at younger ages (well before family considerations would weigh into career decisions). Maybe cultural factors such as upbringing and education are other factors that make math-related jobs more appealing to men?

If underrepresentation in the finance field is not caused by female choice, then perhaps the male dominated industry is merely a function of more men opting into the field (i.e., men are better suited for the industry). More specifically, perhaps male brains are just wired differently? Some make the argument that all the testosterone permeating through male bodies leads them to positions involving more risk. If you look at other risk related fields like gambling, women too are dramatic minorities, making up about 1/3 of total compulsive gamblers.

Women Better than Men?

The funny part about the underrepresentation of females in finance is that one study actually shows female hedge fund managers outperforming their male counterparts. Here’s what a BusinessWeek article had to say about female hedge fund managers:

A new study by Hedge Fund Research found that, from January 2000 through May 31, 2009, hedge funds run by women delivered nearly double the investment performance of those managed by men. Female managers produced average annual returns of 9%, versus 5.82% for men and, in 2008, when financial markets were cratering, funds run by women were down 9.6%, compared with a 19% decline for men.

The article goes onto to theorize that women may not be afraid of risk, but actually are better able to manage risk. A UC Davis study found that male managers traded 45% more than female managers, thereby reducing returns by -2.65% (about 1% more than females).

Regardless of the theories or studies used to explain gender risk appetite, the relative underrepresentation of females in finance is a fact. I’ll let everyone else weigh in why that is the case, but in the meantime I will enjoy watching the female analysts explain the minute by minute account of UGG and iPad sales through the holiday shopping season.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

Related Articles:

BusinessWeek article on female fund managers

Bashful Path to Female Bankruptcies

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in DECK or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Shrewd Research or Bilking the System?

Information is power and some hedge funds, mutual funds, and investment managers will go to great lengths to obtain the lowdown.

Integrity of the financial markets is key and recently several hedge funds (Level Global Investors LP, Diamondback Capital Management LLC and Loch Capital Management LLC) have been raided by the Federal Bureau of Investigation (FBI). Other large investment players, including SAC Capital Advisors, Janus Capital Group Inc. (JNS) and Wellington Management Co. have also received inquiries as part of what some journalists are calling rampant industry insider trading activity. Even investment bank Goldman Sachs (GS) is allegedly being examined for potential unlawful leakage of merger information. Little is known about the allegations, so it is difficult to decipher whether this is the tip of the iceberg or standard investigative work?

Regardless of the scope of the investigation, there is a fine line between what scoop is considered fair versus illegal. The distinction becomes even more difficult to pinpoint with the evolution of faster and more voluminous trading (i.e., high frequency trading). The internet has accelerated the speed of information transfer faster than a politician’s promise to cut spending. Data is chewed up and spit out so quickly, meaning tradable information has a very short shelf life before it is profitably exploited by someone. In the old days of snail mail and private back-office meetings, security prices would require time for information to be completely reflected.

Expert Networks Questioned

Another ingredient introduced over the last decade is the advent of the “expert network,” which are firms that connect fund managers to industry specialists, in many cases as part of a “channel check” to gauge the health of a particular industry. About 10 years ago Regulation FD (Fair Disclosure) was introduced to prevent selective disclosure of “material non-public” information (tips that will likely cause security prices to go significantly up or down) by senior company officials and investor relation professionals to investor types. Greedy (and/or ingenious) institutional investors are Darwinian and as a result figured out a loophole around the system. Hedge funds and other investment managers figured out if the senior executives won’t cough up the good info, then why not target the junior executives and squeeze the inside story from them like informants? Expert networks (read thorough description here) serve as an informational channel to service this demand. Although I’m sure there have been a minority of cases where mid-level managers or junior executives have leaked material information (intentionally or unintentionally), I’m very confident that it is the exception more than the rule. In many instances when the beans were spilled, Regulation FD protects both the person disseminating the information and the investor receiving the information.

Rigged Game for Individuals?

OK sure…hedge funds and institutional managers may occasionally have privileged access to executive teams and can afford access to industry experts. I should know, since I managed a multi-billion fund and consistently had access to the upper rank of corporate executives. Hearing directly from the horse’s mouth and trying to interpret body language can provide insights and instill confidence in a trade, but these executives are not stupid enough to risk prison time by selectively disclosing material non-public information. This dynamic of privileged access will never change as long as CEOs and CFOs are allowed to communicate with investors. Corporate executives will naturally prioritize their limited investor communications towards the larger players.

So with the big-wig managers gaining access to the big-wig executives, has the game become rigged for the individual investors? The short answer is “no.” Over the last decade individual investors have experienced a tremendous leveling of the playing field versus institutional investors. While institutions have privileged access and have pushed to exploit HFT and expert networks, individual investors have gained access to institutional quality research (e.g., SEC filings, real-time conference calls, Wall Street reports, etc.) for free or affordable prices. With the ubiquity of technology and the internet, I only see that gap narrowing more over time.

There will always be cheaters who stretch themselves beyond legal boundaries and should be prosecuted to the full extent of the law. However, for the vast majority of institutional investors, they are using technology and other tools (i.e., expert networks) as shrewd resources to compete in a difficult game. I will reserve full judgment on the names pasted all over the press until the FBI and SEC reveal all their cards. So far there appears to be more noise than smoke coming from the barrel tip of the insider trading gun.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in GS, SAC Capital Advisors, Janus Capital Group Inc. (JNS), Wellington Management Co., or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

FX, the Carry Trade, and Arbitrage Vigilantes

What do you think of the Euro? How about the Japanese yen? Are you expecting the Thai baht to depreciate in value versus the Brazilian real? Speculators, central banks, corporations, governments, financial institutions, and other constituencies ask similar types of questions every day. The largely over-the-counter global foreign exchange markets (no central exchange) are ubiquitous, measuring in the trillions – the BIS (Bank for International Settlements) computed the value of traditional foreign exchange markets at $3.2 trillion in April 2007. Thanks to globalization, these numbers are poised to expand even further. Like other futures markets (think oil, gold, or pork bellies), traders can speculate on the direction of one currency versus another. Alternatively, investors and businesses around the world can use currency futures to hedge (protect) or facilitate international trade.

Without getting lost in the minutiae of foreign exchange currency trading, I think it’s helpful to step back and realize regardless of strategy, currency, interest rate, inflation, peg-ratio, deficits, sovereign debt, or other factor, money will eventually migrate to where it is treated best in the long-run. When it comes to currencies, it’s my fundamental belief that economies control their currency destinies based on the collective monetary, fiscal, and political decisions made by each country. If those decisions are determined imprudent by financial market participants, countries open themselves up to speculators and investors exploiting those decisions for profits.

Currency Trading Ice Cream Style

As mentioned previously, currency trading is predominantly conducted over-the-counter, outside an exchange, but there are almost more trading flavors than ice cream choices at Baskin-Robbins. For instance, one can trade currencies by using futures, options, swaps, exchange traded funds (ETFs), or trading on the spot or forward contract markets. Each flavor has its own unique trading aspects, including the all-important amount of leverage employed.

The Carry Trade

Similar to other investment strategies (for example real estate), if profit can be made by betting on the direction of currencies, then why not enhance those returns by adding leverage (debt). A simple example of a carry trade can illustrate how debt is capable of boosting returns. Suppose hedge fund XYZ wants to borrow (sell U.S. dollars) at 0.25% and buy the Swedish krona currency so they can invest that currency in 5.00% Swedish government bonds. Presumably, the hedge fund will eventually realize the spread of +4.75% (5.00% – 0.25%) and with 10x leverage (borrowings) the amplified return could reach +47.5%, assuming the relationship between the U.S. dollar and krona does not change (a significant assumption).

Positive absolute returns can draw large pools of capital and can amplify volatility when a specific trade is unwound. For example, in recent years, the carry trade from borrowing Japanese yen and investing in the Icelandic krona eventually led to a sharp unwinding in the krona currency positions when the Icelandic economy collapsed in 2008. High currency values make exports less competitive and more expensive, thereby dampening GDP (Gross Domestic Product) growth. On the flip side, higher currency values make imported goods and services that much more affordable – a positive factor for consumers. Adding complexity to foreign exchange markets are the countries, like China, that artificially inflate or depress currencies by “pegging” their currency value to a foreign currency (like the U.S. dollar).

Soros & Arbitrage Vigilantes

Hedge funds, proprietary trading desks, speculators and other foreign exchange participants continually comb the globe for dislocations and discrepancies to take advantage of. Traders are constantly on the look out for arbitraging opportunities (simultaneously selling the weakest and buying the strongest). Famous Quantum hedge fund manager, George Soros, took advantage of weak U.K. economy in 1992 when he spent $10 billion in bet against the British pound (see other Soros article). The Bank of England fought hard to defend the value of the pound in an attempt to maintain a pegged value against a basket of European currencies, but in the end, because of the weak financial condition of the British economy, Soros came out victorious with an estimated $1 billion in profits from his bold bet.

I’m not sure whether the debate over speculator involvement in currency collapses can be resolved? What I do know is the healthier economies making prudent monetary, fiscal, and political decisions will be more resilient in protecting themselves from arbitrage vigilantes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct position on any security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Getting Distressed can be a Beach

It was just another 65 degree winter day on the sunny shores of Huntington Beach at the 2nd Annual Distressed Investment Summit (March 1st through 3rd) when I entered the conference premises. Before digging into the minutiae of the distressed markets, a broad set of industry experts spoke to a diverse crowd including, pension fund managers, consultants, and hedge fund managers at the Hyatt Regency Huntington Beach Resort and Spa. The tone was somewhat restrained given the gargantuan price rebounds and tightening spreads (the premium paid on credit instruments above government securities) in the credit markets, nonetheless the tenor was fairly upbeat thanks to opportunities emanating from the still larger than average historical spreads.

Topics varied, but several speakers gave their views on the financial crisis, macroeconomic outlooks, general debt/credit trends, and areas of distressed credit opportunity. Like investors across all asset classes, many professionals tried to put the puzzle pieces together over the last few years, in order to provide a clearer outlook for the future of distressed markets. To put the addressable market in context, James Perry, Conference Chair and Investment Officer at the San Bernadino County Employees Retirement Association, described the opportunity set as a $2.5 trillion non-investment grade market, with $250-$400 billion in less liquid securities. Typically distressed securities consist of investments like bonds, bank debt, and/or CLOs (collateralized loan obligations), which frequently carry CCC or lower ratings from agencies such as Standard & Poors, Moodys, and Fitch.

As mentioned previously, since the audience came from a diverse set of constituencies, a broad set of topics and themes were presented:

- Beta Bounce is Gone: The collapse of debt prices and massive widening of debt spreads in 2008 and 2009 have improved dramatically over the last twelve months, meaning the low hanging fruit has already been picked for the most part. Last year was the finest hour for distressed investors because price dislocations caused by factors such as forced selling, technical idiosyncracies, and credit downgrades created a large host of compelling prospects. For many companies, long-term business fundamentals were little changed by the liquidity crunch. As anecdotal evidence for the death of the beta bounce, one speaker observed CLOs trading at 30-35 cents during the March 2009 lows. Those same CLOs are now trading at about 80 cents. Simple math tells us, by definition, there is less upside to par (the bond principal value = 100 cents on dollar).

- Distressed Defaults: Default rates are expected to rise in the coming months and years because of record credit issuance in the 2006-2007 timeframe. The glut of questionable buy-outs completed at the peak of the financial markets driven by private equity and other entities has created a sizeable inventory of debt that has a higher than average chance of becoming distressed. One panel member explained that CCC credit ratings experience a 40% default within 5 years, meaning the worst is ahead of us. The artificially depressed 4-7% current default rates are now expected to rise, but below the 12% default rate encountered in 2009.

- Wall of Maturities: Although the outlook for distressed investments look pretty attractive for the next few years, a majority of professionals speaking on the topic felt a wave of $1 trillion in maturities would roll through the market in the 2012-2014, leading to the escalating default rates mentioned above. CLOs related to many of the previously mentioned ill-timed buyouts will be a significant component of the pending debt wall. Whether the banks will bite the bullet and allow borrowers to extend maturities is still an open topic of debate.

- Mid Market Sweet Spot: Larger profitable companies are having little trouble tapping the financial markets to access capital at reasonable rates. With limited capital made available for middle market companies, there are plenty of opportunistic investments to sift through. With the banks generally hoarding capital and not lending, distressed debt investments are currently offering yields in the mid-to-high teens. Borrowers are effectively beggars, so they cannot be choosers. The investor, on the other hand, is currently in a much stronger position to negotiate first lien secured positions on the debt, which allows a “Plan B,” if the underlying company defaults. Theoretically, investors defaulting into an ownership position can potentially generate higher returns due forced restructuring and management of company operations. Of course, managing the day-to-day operations of many companies is much easier said than done.

- Is Diversification Dead? This question is relevant to all investors but was primarily directed at the fiduciaries responsible for managing and overseeing pension funds. The simultaneous collapse of prices across asset classes during the financial crisis has professionals in a tizzy. Several diversification attacks were directed at David Swensen’s strategy (see Super Swensen article) implemented at Yale’s endowment. Although Swensen’s approach covered a broad swath of alternative investments, the strategy was attacked as merely diversified across illiquid equity asset classes – not a good place to be at the beginning of 2008 and 2009. The basic rebuttal to the “diversification is dead mantra” came in the form of a rhetorical question: “What better alternative is there to diversification?” One other participant was quick to point out that asset allocation drives 85% of portfolio performance.

- Transparency & Regulation: In a post-Bernie Madoff world, even attending hedge fund managers conceded a certain amount of adequate transparency is necessary to make informed decisions. Understanding the strategy and where the returns are coming from is critical component of hiring and maintaining an investment manager.

- Distressed Real Estate Mixed Bag: Surprisingly, the prices and cap rates (see my article on real estate and stocks) on quality properties has not dramatically changed from a few years ago, meaning some areas of the real estate market appear to be less appealing . Better opportunities are generally more tenant specific and require a healthy dosage of creativity to make the deal economics work. Adjunct professor from Columbia University, Michael G. Clark, had a sobering view with respect to the residential real estate market home ownership rates, which he continues to see declining from a peak of 70% to 62% (currently 67%) over time. Clark sees a slow digestion process occurring in the housing market as banks use improved profits to shore up reserves and slowly bleed off toxic assets. He believes job security/mobility, financing, and immigration demographics are a few reasons we will witness a large increase in renters in coming periods. Also driving home ownership down is the increased density of youngsters living at home post-graduation. Clark pointed out the 20% of 26-year olds currently living at home with their parents, a marked increase from times past.

Overall, I found the 2nd Annual Distressed Investment Summit a very informative event, especially from an equity investor’s standpoint, since many stock jocks spend very little time exploring this part of the capital structure. Devoting a few days at the IMN sponsored event taught me that life does not have to be a beach if you mix some distress with a little sun, sand, and fun.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct position on any security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}