Posts tagged ‘Germany’

Rise of the Robots

We’re losing our jobs to robots, and they will destroy our economy. It makes for a great news soundbite, but has no factual basis in reality, if you look at the actual trajectory of automation and technology innovations throughout history. The global economy did not collapse when the steam engine replaced the oar; the automobile supplanted the horse; the computer became a substitute for the abacus; and the combine killed off the farmer. The same notion holds true today as robots become more ubiquitous in our daily commercial and personal lives.

From the early, post-revolutionary birth of our country in the 18th century, the agrarian economy accounted for upwards of 90% of jobs and financial activity…until farming technology evolved (see chart below). As new agricultural advancements were introduced, like the cotton gin, plow, scythe, chemical fertilizers, tractors, combine harvesters, and genetically engineered seeds, human capital (jobs) were redeployed into other growth sectors of the economy (e.g., factories, aerospace, semiconductors, medicine, etc.).

Source: Carpe Diem

Given that human labor accounts for about 2/3 of an average company’s expense structure, it should come as no surprise that corporations are looking to reduce costs by introducing more robotics and automation into their processes. The advantages to robotics adoption are numerous and I describe many of the reasons in my article, Chainsaw Replaces Paul Bunyan:

A robot won’t ask for a raise; it always shows up on time; you don’t have to pay for its healthcare; it can work 24/7/365 days per year; it doesn’t belong to a union; dependable quality consistency is a given; it produces products near your customers; and it won’t sue for discrimination or sexual harassment.

At Sidoxia Capital Management we opportunistically identified this growing trend quite early as evidenced by our initial 2012 investment in KUKA AG (Ticker: KUKAF), a German manufacturer of industrial robots. KUKA has recently made headlines due to a bid received from Chinese home-appliance company (Midea Group: Ticker – 000333.SZ) that values the dominant German robotics leader at $5 billion. Despite KUKA’s +273% share price appreciation from the end of 2012, not many people have heard of the company. While KUKA may not have caught the attention of many U.S. investors, the company has captured a bevy of blue-chip global customers, including Daimler, Airbus Group, Volkswagen, Fiat, Boeing, and Tesla.

Rather than sitting on its hands, KUKA has done its part to develop a higher profile. In fact, President Barack Obama and German Chancellor Angela Merkel recently received a robotics demonstration from KUKA’s CEO Till Reuter at the world’s largest industrial technology trade fair in Hannover, Germany this April (picture below)

Source: Bloomberg

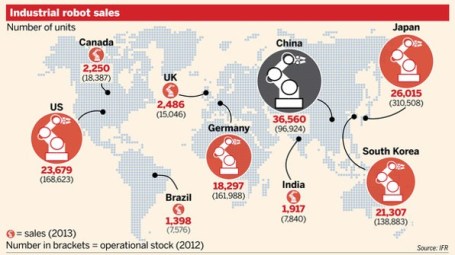

The recent multi-billion dollar bid by Midea Group has turned some onlookers’ heads, but what the potential deal really signals is the vast opportunity for robotics expansion in Asia. Rising labor costs in China, coupled with the enormous efficiency benefits of automation, have pushed China to become the largest purchasing country of robots in the world, ahead of the U.S., Japan, Korea and Germany (see chart below). However, according to the International Federation of Robotics (IFR), in 2015, Japan remained the country with the largest number of installed robots. IFR does not expect Japan to remain the “king” of the installed robotics hill forever. Actually, IFR estimates China will leapfrog Japan over the next few years to become both the largest purchaser of robots, along with maintaining the largest installed base of robots.

Source: Financial Times

In the coming months and years, there will be a steady stream of sensationalist headlines talking about the rise of the robots, and the destruction of jobs. We’ve repeatedly seen this movie before throughout history. Rather than a scary bloodbath ending, over the long-run we’ll likely see another happy ending. Any potential job losses will likely be outweighed by productivity gains, coupled with the benefits associated with more efficiently deployed labor to new growth sectors of the economy.

Even KUKA realizes the automation dynamics of the 21st century will serve as a net labor enhancer not detractor. If you don’t believe me, just ask Timo Boll, world champion table tennis player, who tested this theory vs. a KUKA robot (see video below). Ultimately, the rise of robots will lead to the rise of global growth and productivity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), KUKAF, BA, and TSLA, but at the time of publishing had no direct position in Daimler, Airbus Group, Volkswagen, Fiat Chrysler, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sports & Investing: Why Strong Earnings Can Hurt Stock Prices

With the World Cup in full swing and rabid fans rooting for their home teams, one may notice the many similarities between investing in stocks and handicapping in sports betting. For example, investors (bettors) have opposing views on whether a particular stock (team) will go up or down (win or lose), and determine if the valuation (point spread) is reflective of the proper equilibrium (supply & demand). And just like the stock market, virtually anybody off the street can place a sports bet – assuming one is of legal age and in a legal betting jurisdiction.

Soon investors will be poring over data as part of the critical, quarterly earnings ritual. With some unsteady GDP data as of late, all eyes will be focused on this earnings reporting season to reassure market observers the bull advance can maintain its momentum. However, even positive reports may lead to unexpected investor reactions.

So how and why can market prices go down on good news? There are many reasons that short-term price trends can diverge from short-run fundamentals. One major reason for the price-fundamental gap is this key factor: “expectations”. With such a large run-up in the equity markets (up approx. +195% from March 2009) come loftier expectations for both the economy and individual companies. For instance, just because corporate earnings unveiled from companies like Google (GOOG/GOOGL), J.P. Morgan (JPM), and Intel (INTC) exceed Wall Street analyst forecasts does not mean stock prices automatically go up. In many cases a stock price correction occurs due to a large group of investors who expected even stronger profit results (i.e., “good results, but not good enough”). In sports betting lingo, the sports team may have won the game this week, but they did not win by enough points (“cover the spread”).

Some other reasons stock prices move lower on good news:

- Market Direction: Regardless of the underlying trends, if the market is moving lower, in many instances the market dip can overwhelm any positive, stock- specific factors.

- Profit Taking: Many times investors holding a long position will have price targets or levels, if achieved, that will trigger selling whether positive elements are in place or not.

- Interest Rates: Certain valuation techniques (e.g. Discounted Cash Flow and Dividend Discount Model) integrate interest rates into the value calculation. Therefore, a climb in interest rates has the potential of lowering stock prices – even if the dynamics surrounding a particular security are excellent.

- Quality of Earnings: Sometimes producing winning results is not enough (see also Tricks of the Trade article). On occasion, items such as one-time gains, aggressive revenue recognition, and lower than average tax rates assist a company in getting over a profit hurdle. Investors value quality in addition to quantity.

- Outlook: Even if current period results may be strong, on some occasions a company’s outlook regarding future prospects may be worse than expected. A dark or worsening outlook can pressure security prices.

- Politics & Taxes: These factors may prove especially important to the market this year, since this is a mid-term election year. Political and tax policy changes today may have negative impacts on future profits, thereby impacting stock prices.

- Other Exogenous Items: Natural disasters and security attacks are examples of negative shocks that could damage price values, irrespective of fundamentals.

Certainly these previously mentioned issues do not cover the full gamut of explanations for temporary price-fundamental gaps. Moreover, many of these factors could be used in reverse to explain market price increases in the face of weaker than anticipated results.

If you’re traveling to Las Vegas to place a wager on the World Cup, betting on winning favorites like Germany and Argentina may not be enough. If expectations are not met and the hot team wins by less than the point spread, don’t be surprised to see a decline in the value of your bet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and GOOGL, but at the time of publishing had no direct positions in JPM and INTC. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Nuclear Knee-Jerk Reaction

It’s amazing how quickly the long-term secular growth winds can reverse themselves. Just a week ago, nuclear energy was thought of as a safe, clean, green technology that would assist the gasoline pump pain in our wallets and purses. Now, given the events occurring in Japan, “nuclear” has become a dirty word equated to a life-threatening game of Russian roulette.

Despite the spotty information filtering in from the Dai-Ichi plant in Japan, we are already absorbing knee-jerk responses out of industrial heavyweight countries like Germany and China. Germany has temporarily closed seven nuclear power centers generating about a quarter of its nuclear capacity, and China has instituted a moratorium on all new facilities being built. How big a deal is this? Well, China is one country, and it alone currently accounts for 44% of the 62 global nuclear reactor projects presently under construction (see chart below).

Source: World Nuclear Association (URRE Presentation)

As a result of the damaged Fukushima reactors, coupled with various governmental announcements around the globe, Uranium prices have dropped a whopping -30% within a month – plunging from about $70 per pound to around $50 per pound today.

Where does U.S. Nuclear Go from Here?

As you can see from the chart below, the U.S. is the largest producer of nuclear energy in the world, but since our small population is such power hogs, this relatively large nuclear capability only accounts for roughly 20% of our country’s total electricity needs. France, on the other hand, manages about half the reactors as we do, but the French derive a whopping 75% of their total electricity needs from nuclear power. According to the Nuclear Energy Institute, Japanese reliance on nuclear power falls somewhere in between – 29% of their electricity demand is filled by nuclear energy. Like Japan, the U.S. imports most of its energy needs, so if nuclear development slows, guess what, other resources will need to make up the difference. OPEC and various other oil-rich, dictators in the Middle East are licking their chops over the future prospects for oil prices, if a cost-effective alternative like nuclear ends up getting kicked to the curb.

Source: The Economist

As I alluded to above, there is, however, a silver lining. As long as oil prices remain elevated, any void created by a knee-jerk nuclear backlash will only create heightened demand for alternative energy sources, including natural gas, solar, wind, biomass, clean coal, and other creative substitutes. While we Americans may be addicted to oil, we also are inventive, greedy capitalists that will continually look for more cost-efficient alternatives to solve our energy problems (see also Electrifying Profits). Unlike other countries around the world, it looks like the private sector will have to do the heavy lifting to solve these resources on their own dime. Limited subsidies have been introduced, but overall our government has lacked a cohesive energy plan to kick-start some of these innovative energy alternatives.

Déjà Vu All Over Again

We saw what happened on our soil in March 1979 when the Three Mile Island nuclear accident in Pennsylvania consumed the hearts and minds of the country. Pure unadulterated panic set in and new nuclear production ground to a virtual halt. When the subsequent Chernobyl incident happened in April 1986 insult was added to injury. As you can see from the chart below, nuclear reactor capacity has plateaued for some twenty years now.

Source: Wikipedia

The driving force behind the plateauing nuclear facilities is the NIMBY (Not In My Back Yard) phenomenon. The Three Mile Island incident is still fresh in people’s minds, which explains why only one nuclear plant is currently under construction in our country, on top of a base of 104 U.S. reactors in 31 states. I point this out as an ambivalent NIMBY-er since I work 30 miles away from one of the riskiest, 30-year-old nuclear plants in the country (San Onofre).

Unintended Consequences

The Sendai disaster is home to the worst Japanese earthquake in 140 years, by some estimates, but history will prove once again what unintended consequences can occur when impulsive knee-jerk decisions are made. Just consider what has happened to oil prices since the moratorium on offshore drilling (post-BP disaster) was instituted. Sure we have witnessed a dictator or two topple in the Middle East, and there currently is adequate supply to meet demand, but I would make the case that we should be increasing domestic oil supplies (along with alternative energy sources), not decreasing supplies because it is politically safe.

Time will tell if the Japanese earthquake/tsunami-induced nuclear disaster will create additional unintended consequences, but I am hopeful the recent events will at a minimum create a serious dialogue about a comprehensive energy policy. If the comfortable, knee-jerk reaction of significantly diminishing nuclear production is broadly adopted around the world, then an urgent alternative supply response needs to occur. Otherwise, you may just need to enjoy that bike ride to work in the morning, along with that nice, romantic candle-lit dinner at night.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and alternative energy securities, but at the time of publishing SCM had no direct position in BP, URRE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}