Posts tagged ‘George Soros’

When Genius Failed

It has been a busy year between work, play, family, and of course the recent elections. My work responsibilities contain a wide-ranging number of facets, but in addition to research, client meetings, conference calls, conferences, trading, and other activities, I also attempt to squeeze in some leisure reading as well. While it’s sad but true that I find pleasure in reading SEC documents (10Ks and 10Qs), press releases, transcripts, corporate presentations, financial periodicals, and blogs, I finally did manage to also scratch When Genius Failed by Roger Lowenstein from my financial reading bucket list.

When Genius Failed chronicles the rise and fall of what was considered the best and largest global hedge fund, Long Term Capital Management (LTCM). The irony behind the collapse makes the story especially intriguing. Despite melding the brightest minds in finance, including two Nobel Prize winners, Robert Merton and Myron Scholes, the Greenwich, Connecticut hedge fund that started with $1.3 billion in early 1994 managed to peak at around $140 billion before eventually crumbling to ruin.

With the help of confidential internal memos, interviews with former partners and employees of LTCM, discussions with the Federal Reserve, and consultations with the six major banks involved in the rescue, Lowenstein provides the reader with a unique fly-on-the-wall perspective to this grand financial crisis.

There have certainly been plenty of well-written books recounting the 2008-2009 financial crisis (see my review on Too Big to Fail), but the sheer volume has burnt me out on the subject. With that in mind, I decided to go back in time to the period of 1993 – 1998, a point at the beginning of my professional career. Until LTCM’s walls began figuratively caving in and global markets declined by more than $1 trillion in value, LTCM was successful at maintaining a relatively low profile. The vast majority of Americans (99%) had never heard of the small group of bright individuals who started LTCM, until the fund’s ultimate collapse blanketed every newspaper headline and media outlet.

Key Characters

Meriwether: John W. Meriwether was a legendary trader at Salomon Brothers, where he started the Arbitrage Group in 1977 and built up a successful team during the 1980s. His illustrious career is profiled in Michael Lewis’s famed book, Liar’s Poker. Meriwether built his trading philosophy upon the idea that mispricings would eventually revert back to the mean or converge, and therefore shrewd opportunistic trading will result in gains, if patience is used. Another name for this strategy is called “arbitrage”. In sports terms, the traders of the LTCM fund were looking for inaccurate point spreads, which could then be exploited for profit opportunity. Prior to the launch of LTCM, in 1991 Meriwether was embroiled in the middle of a U.S. Treasury bid-rigging scheme when one of his traders Paul Mozer admitted to submitting false bids to gain unauthorized advantages in government-bond auctions. John Gutfreund, Salomon Brothers’ CEO was eventually forced to quit, and Salomon’s largest, famed shareholder Warren Buffett became interim CEO. Meriwether was slapped on the wrist with a suspension and fine, and although Buffett eventually took back Meriwether in a demoted role, ultimately the trader was viewed as tainted goods so he left to start LTCM in 1993.

LTCM Team: During 1993 Meriwether built his professional team at LTCM and he began this process by recruiting several key Salomon Brothers bond traders. Larry Hilibrand and Victor Haghani were two of the central players at the firm. Other important principals included Eric Rosenfeld, William Krasker, Greg Hawkins, Dick Leahy, Robert Shustak, James McEntee, and David W. Mullins Jr.

Nobel Prize Winners (Merton & Scholes): While Robert C. Merton was teaching at Harvard University and Myron S. Scholes at Stanford University, they decided to put their academic theory to the real-world test by instituting their financial equations with the other investing veterans at LTCM. Scholes and Merton were effectively godfathers of quantitative theory. If there ever were a Financial Engineering Hall of Fame, Merton and Scholes would be initial inductees. Author Lowenstein described the situation by saying, “Long-Term had the equivalent of Michael Jordan and Muhammad Ali on the same team.” Paradoxically, in 1997, right before the collapse of LTCM, Merton and Scholes would become Nobel Prize laureates in Economic Sciences for their work in developing the theory of how to price options.

The History:

Founded in 1993, Long-Term Management Capital was hailed as the most impressive hedge fund created in history. Near its peak, LTCM managed money for about 100 investors and employed 200 employees. LTCM’s primary strategy was to identify mispriced bonds and profit from a mean reversion strategy. In other words, as long as the overall security mispricings narrowed, rather than widened, then LTCM would stand to profit handsomely.

On an individual trade basis, profits from LTCM’s trades were relatively small, but the fund implemented thousands of trades and used vast amounts of leverage (borrowings) to expand the overall profits of the fund. Lowenstein ascribed the fund’s success to the following process:

“Leveraging its tiny margins like a high-volume grocer, sucking up nickel after nickel and multiplying the process a thousand times.”

Although LTCM implemented this strategy successfully in the early years of the fund, this premise finally collapsed like a house of falling cards in 1998. As is generally the case, hedge funds and other banking competitors came to understand and copy LTCM’s successful trading strategies. Towards the end of the fund’s life, Meriwether and the other fund partners were forced to experiment with less familiar strategies like merger arbitrage, pair trades, emerging markets, and equity investing. This diversification strategy was well intentioned, however by venturing into uncharted waters, the traders were taking on excessive risk (i.e., they were increasing the probability of permanent capital losses).

The Timeline

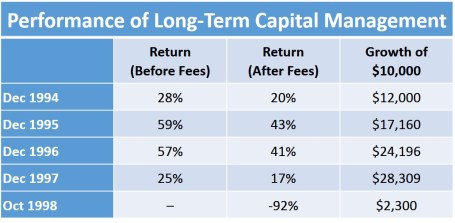

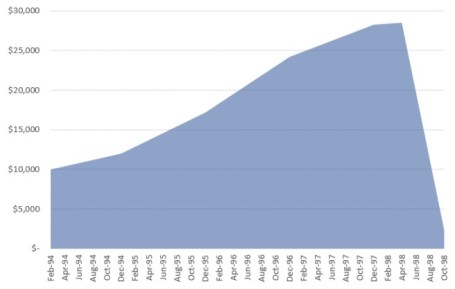

- 1994 (28% return, 20% after fees): After attempting to raise capital funding in 1993, LTCM opened its doors for business in February 1994 with $1.25 billion in equity. Financial markets were notably volatile during 1994 in part due to Federal Reserve Chairman Alan Greenspan leading the first interest rate hike in five years. The instability caused famed fund managers Michael Steinhardt and George Soros to lose -$800 million and $650 million, respectively, all within a timespan of less than a week. The so-called “Mexican Tequila Crisis” that occurred at the end of the year also resulted in a devaluation of the Mexican peso and crumbling of the Mexican stock market.

- 1995 (59% return, 43% after fees): By the end of 1995, the fund had tripled its equity capital and total assets had grown to $102 billion. Total leverage, or the ratio of debt to equity, stood around 28 to 1. LTCM’s derivative contract portfolio was like a powder keg, covering positions worth approximately $650 billion.

- 1996 (57% return, 41% after fees): By the spring of 1996, the fund was holding $140 billion in assets, making it two and a half times as big as Fidelity Magellan, the largest mutual fund on the planet. The fund also carried derivatives valued at more than $1 trillion, all financed off a relatively smaller $4 billion equity base. Investors were loving the returns and financial institutions were clamoring to gain some of LTCM’s business. During this period, as many as 55 banks were providing LTCM financing. The mega-returns earned in 1996 came in large part due to profitable leveraged spread trades on Japanese convertible bonds, Italian bonds, junk bonds, and interest rate swaps. Total profits for the year reached an extraordinary level of around $2.1 billion. To put that number in perspective, that figure was more money generated than the profits earned by McDonalds, Disney, American Express, Nike, Xerox, and many more Fortune 500 companies.

- 1997 (25% return, 17% after fees): The Asia Crisis came into full focus during October 1997. Thailand’s baht currency fell by -20% after the government decided to let the currency float freely. Currency weakness then spread to the Philippines, Malaysia, South Korea, and Singapore. As Russian bond spreads (prices) began to widen, massive trading losses for LTCM were beginning to compound. Returns remained positive for the year and the fund grew its equity capital to $5 billion. As the losses were mounting and the writing on the wall was revealing itself, professors Merton and Scholes were recognized with their Nobel Prize announcement. Ironically, LTCM was in the process of losing control. LTCM’s bloated number of 7,600 positions wasn’t making the fund any easier to manage. During 1997, the partners realized the fund’s foundation was shaky, so they returned $2.7 billion in capital to investors. Unfortunately, the risk profile of the fund worsened – not improved. More specifically, the fund’s leverage ratio skyrocketed from 18:1 to 28:1.

- 1998 (-92% return – loss): The Asian Crisis losses from the previous year began to bleed into added losses in 1998. In fact, losses during May and June alone ended up reducing LTCM’s capital by $461 million. As the losses racked up, LTCM was left in the unenviable position of unwinding a mind-boggling 60,000 individual positions. It goes almost without saying that selling is extraordinarily difficult during a panic. As Lowenstein put it, “Wall Street traders were running from Long-Term’s trades like rats from a sinking ship.” A few months later in September, LTCM’s capital shrunk to less than $1 billion, meaning about $100 billion in debt (leverage ratio greater than 100:1) was supporting the more than $100 billion in LTCM assets. It was just weeks later the fund collapsed abruptly. Russia defaulted on its ruble debt, and the collapsing currency contagion spread to global markets outside Russia, including Eastern Asia, and South America.

The End of LTCM

On September 23, 1998, after failed investment attempts by Warren Buffett and others to inject capital into LTCM, the heads of Bankers Trust, Bear Stearns, Chase Manhattan, Goldman Sachs, J.P. Morgan, Lehman Brothers, Merrill Lynch, Morgan Stanley Dean Witter, and Salomon Brothers all gathered at the Federal Reserve Bank of New York in the heart of Wall Street. Presiding over this historical get-together was Fed President, William J. McDonough. International markets were grinding to a halt during this period and the Fed was running out of time before an all-out meltdown was potentially about to occur. Ultimately, McDonough was able to get 14 banks to wire $3.65 billion in bailout funds to LTCM. While all LTCM partners were financially wiped out completely, initial investors managed to recoup a small portion of their original investment (23 cents on the dollar after factoring in fees), even though the tally of total losses reached approximately $4.6 billion. Once the bailout was complete, it took a few years for the fund to liquidate its gargantuan number of positions and for the banks to get their multi-billion dollar bailout paid back in full.

- 1999 – 2009 (Epilogue): Meriwether didn’t waste much time moping around after the LTCM collapse, so he started a new hedge fund, JWM Partners, with $250 million in seed capital primarily from legacy LTCM investors. Regrettably, the fund was hit with significant losses during the 2008-2009 Financial Crisis and was subsequently forced to close its doors in July 2009.

Source: The Personal Finance Engineer

Source: The Personal Finance Engineer

Lessons Learned:

- The Risks of Excessive Leverage: Although the fund grew to peak value of approximately $140 billion in assets, most of this growth was achieved with added debt. When all was said and done, LTCM borrowed more than 30 times the value of its equity. As Lowenstein put it, LTCM was “adding leverage to leverage, as if coating a flammable tinderbox with kerosene.” In home purchase terms, if LTCM wanted to buy a house using the same amount of debt as their fund, they would lose all of their investment, if the house value declined a mere 3-4%. The benefit of leverage is it multiplies gains. The downside to leverage is that it also multiplies losses. If you carry too much leverage in a declining market, the chance of bankruptcy rises…as the partners and investors of LTCM learned all too well. Adding fuel to the LTCM flames were the thousands of derivative contracts, valued at more than $1 trillion. Warren Buffett calls derivatives: “Weapons of Mass Destruction.”

- Past is Not Always Prologue for the Future: Just because a strategy works now or in the past, does not mean that same strategy will work in the future. As it relates to LTCM, Nobel Prize winning economist Merton Miller stated, “In a strict sense, there wasn’t any risk – if the world had behaved as it did in the past.” LTCM’s models worked for a while, then failed miserably. There is no Holy Grail investment strategy that works always. If an investment strategy sounds too good to be true, then it probably is too good to be true.

- Winning Strategies Eventually Get Competed Away: The spreads that LTCM looked to exploit became narrower over time. As the fund achieved significant excess returns, competitors copied the strategies. As spreads began to tighten even further, the only way LTCM could maintain their profits was by adding additional leverage (i.e., debt). High-frequency trading (HFT) is a modern example of this phenomenon, in which early players exploited a new technology-driven strategy, until copycats joined the fray to minimize the appeal by squeezing the pool of exploitable profits.

- Academics are Not Practitioners: Theory does not always translate into reality, and academics rarely perform as well as professional practitioners. Merton and Scholes figured this out the hard way. As Merton admitted after winning the Nobel Prize, “It’s a wrong perception to believe that you can eliminate risk just because you can measure it.”

- Size Matters: As new investors poured massive amounts of capital into the fund, the job of generating excess returns for LTCM managers became that much more difficult. I appreciate this lesson firsthand, given my professional experience in managing a $20 billion fund (see also Managing $20 Billion). Managing a massive fund is like maneuvering a supertanker – the larger a fund gets, the more difficult it becomes to react and anticipate market changes.

- Stick to Your Knitting: Because competitors caught onto their strategies, LTCM felt compelled to branch out. Meriwether and LTCM had an edge trading bonds but not in stocks. In the later innings of LTCM’s game, the firm became a big player in stocks. Not only did the firm place huge bets on merger arbitrage, but LTCM dabbled significantly in various long-short pair trades, including a $2.3 billion pair trade bet on Royal Dutch and Shell. Often the firm used derivative securities called equity swaps to make these trades without having to put up any significant capital. As LTCM experimented in the new world of equities, the firm was obviously playing in an area in which it had absolutely no expertise.

As philosopher George Santayana states, “Those who fail to learn from history are doomed to repeat it.” For those who take investing seriously, When Genius Failed is an important cautionary tale that provides many important lessons about financial markets and highlights the dangers of excessive leverage. You may not be a genius Nobel Prize winner in economics, but learning from Long-Term Capital Management’s failings will place you firmly on the path to becoming an investing genius.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), DIS, JPM, and MCD, but at the time of publishing had no direct position in AXP, NKE, XRX, RD, GS, MS, Shell, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

The Pain of Diversification

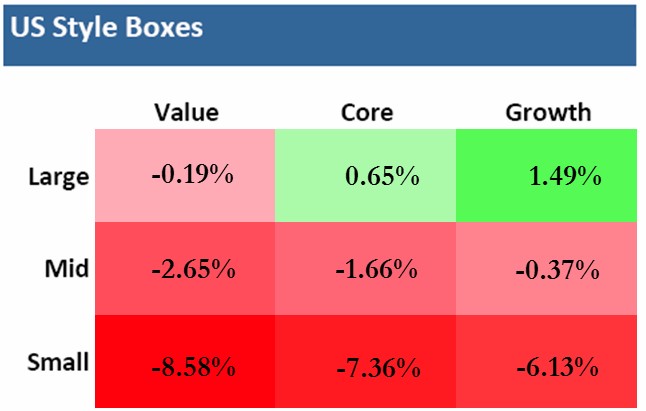

The oft-quoted tenet that diversification should be the cornerstone of any investment strategy has come under assault in the third quarter. As you can see from the chart below, investors could run, but they couldn’t hide. The Large Cap Growth category was the major exception, thanks in large part to Apple Inc.’s (AAPL) +8% appreciation. More specifically, seven out of the nine Russell Investments style boxes were in negative territory for the three month period. The benefits of diversification look even worse, if you consider other large asset classes and sectors such as the Gold/Gold Miners were down about -14% (GDX/GLD); Energy -9% (XLE); Europe-EAFE -6% (EFA); Utilities -5% (XLU); and Emerging Markets -4% (EEM).

*Results are for Q3 – 2014 (Source: Vanguard Group, Inc. & Russell Investments)

On the surface, everything looks peachy keen with all three major indices posting positive Q3 appreciation of +1.3% for the Dow, +0.6% for S&P 500, and +1.9% for the NASDAQ. It’s true that over the long-run diversification acts like shock absorbers for economic potholes and speed bumps, but in the short-run, all investors can hit a stretch of rough road in which shock absorbers may seem like they are missing. Over the long-run, you can’t live without diversification shocks because your financial car will eventually breakdown and the ride will become unbearable.

What has caused all this underlying underperformance over the last month and a half? The headlines and concerns change daily, but the -5% to -6% pullback in the market has catapulted the Volatility Index (VIX or “Fear Gauge”) by +85%. The surge can be attributed to any or all of the following: a slowing Chinese economy, stagnant eurozone, ISIS in Iraq, bombings in Syria, end of Quantitative Easing (QE), impending interest rate hikes, mid-term elections, Hong Kong protests, proposed tax inversion changes, security hacks, rising U.S. dollar, PIMCO’s Bill Gross departure, and a half dozen other concerns.

In general, pullbacks and corrections are healthy because shares get transferred out of weak hands into stronger hands. However, one risk associated with these 100 day floods (see also 100-Year Flood ≠ 100-Day Flood) is that a chain reaction of perceptions can eventually become reality. Or in other words, due to the ever-changing laundry list of concerns, confidence in the recovery can get shaken, which in turn impacts CEO’s confidence in spending, and ultimately trickles down to employees, consumers, and the broader economy. In that same vein, George Soros, the legendary arbitrageur and hedge fund manager, has famously written about his law of reflexivity (see also Reflexivity Tail Wags Dog). Reflexivity is based on the premise that financial markets continually trend towards disequilibrium, which is evidenced by repeated boom and bust cycles.

While, at Sidoxia, we’re still finding more equity opportunities amidst these volatile markets, what this environment shows us is conventional wisdom is rarely correct. Going into this year, the consensus view regarding interest rates was the economy is improving, and the tapering of QE would cause interest rates to go significantly higher. Instead, the yield on the 10-Year Treasury Note has gone down significantly from 3.0% to 2.3%. The performance contrast can be especially seen with small cap stocks being down-10% for the year and the overall Bond Market (BND) is up +3.1% (and closer to +5% if you include interest payments). Despite interest rates fluctuating near generational lows with paltry yields, the power of diversification has proved its value.

While there are multiple dynamics transpiring around the financial markets, the losses across most equity categories and asset classes during Q3 have been bloody. Nonetheless, investing across the broad bond market and certain large cap stock segments is evidence that diversification is a valuable time-tested principle. Times like these highlight the necessity of diversification gain to offset the current equity pain.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, BND, and certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in EEM, GDX, GLD, EFA, XLE, XLU, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Sidoxia’s Investor Hall of Fame

Investing Caffeine has profiled many great investors over the months and years, so I thought now would be a great time to compile a “Hall of Fame” summarizing some of the greatest of all-time. Nothing can replace experience, but learning from the greats can only improve your investing results – I’ve benefitted firsthand and so have Sidoxia’s clients. Here is a partial list from the Pantheon of investing greats along with links to the complete articles (special thanks to Kevin Weaver for helping compile):

Phillip Fisher – Author of the must-read classic Common Stocks and Uncommon Profits, he enrolled in college at age 15 and started graduate school at Stanford a few years later, before he dropped out and started his own investment firm in 1931. “If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never.” Not every investment idea made the cut, however he is known to have bought Motorola (MOT) stock in 1955 and held it until his death in 2004 for a massive gain. (READ COMPLETE ARTICLE)

Phillip Fisher – Author of the must-read classic Common Stocks and Uncommon Profits, he enrolled in college at age 15 and started graduate school at Stanford a few years later, before he dropped out and started his own investment firm in 1931. “If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never.” Not every investment idea made the cut, however he is known to have bought Motorola (MOT) stock in 1955 and held it until his death in 2004 for a massive gain. (READ COMPLETE ARTICLE)

Peter Lynch – Lynch graduated from Boston College in 1965 and earned a Master of Business Administration from the Wharton School of the University of Pennsylvania in 1968. Lynch’s Magellan fund averaged +29% per year from 1977 – 1990 (almost doubling the return of the S&P 500). In 1977, the obscure Magellan Fund started with about $20 million, and by his retirement the fund grew to approximately $14 billion (700x’s larger). Magellan outperformed 99.5% of all other funds, according to Barron’s. (READ COMPLETE ARTICLE)

Peter Lynch – Lynch graduated from Boston College in 1965 and earned a Master of Business Administration from the Wharton School of the University of Pennsylvania in 1968. Lynch’s Magellan fund averaged +29% per year from 1977 – 1990 (almost doubling the return of the S&P 500). In 1977, the obscure Magellan Fund started with about $20 million, and by his retirement the fund grew to approximately $14 billion (700x’s larger). Magellan outperformed 99.5% of all other funds, according to Barron’s. (READ COMPLETE ARTICLE)

William O’Neil – After graduating from Southern Methodist University, O’Neil started his career as a stock broker. Soon thereafter, at the ripe young age of 30, O’Neil purchased a seat on the New York Stock Exchange and started his own company, William O’Neil + Co. Incorporated. Following the creation of his firm, O’Neil went on to pioneer the field of computerized investment databases. He used his unique proprietary data as a foundation to unveil his next entrepreneurial baby, Investor’s Business Daily, in 1984. (READ COMPLETE ARTICLE)

Sir John Templeton – After Yale and Oxford, Templeton moved onto Wall Street, borrowed $10,000 to purchase more than 100 stocks trading at less than $1 per share (34 of the companies were in bankruptcy). Only four of the investments became worthless and Templeton made a boatload of money. Templeton bought an investment firm in 1940, leading to the Templeton Growth Fund in 1954. A $10,000 investment made at the fund’s 1954 inception would have compounded into $2 million in 1992 (translating into a +14.5% annual return). (READ COMPLETE ARTICLE)

Charles Ellis – He has authored 12 books, founded institutional consulting firm Greenwich Associates, a degree from Yale, an MBA from Harvard, and a PhD from New York University. A director at the Vanguard Group and Investment Committee chair at Yale, Ellis details that many more investors and speculators lose than win. Following his philosophy will not only help increase the odds of your portfolio winning, but will also limit your losses in sleep hours. (READ COMPLETE ARTICLE)

Charles Ellis – He has authored 12 books, founded institutional consulting firm Greenwich Associates, a degree from Yale, an MBA from Harvard, and a PhD from New York University. A director at the Vanguard Group and Investment Committee chair at Yale, Ellis details that many more investors and speculators lose than win. Following his philosophy will not only help increase the odds of your portfolio winning, but will also limit your losses in sleep hours. (READ COMPLETE ARTICLE)

Seth Klarman – President of The Baupost Group, which manages about $22 billion, he worked for famed value investors Max Heine and Michael Price of the Mutual Shares. Klarman published a classic book on investing, Margin of Safety, Risk Averse Investing Strategies for the Thoughtful Investor, which is now out of print and has fetched upwards of $1,000-2,000 per copy in used markets. From it’s 1983 inception through 2008 his Limited partnership averaged 16.5% net annually, vs. 10.1% for the S&P 500. During the “lost decade” he crushed the S&P, returning 14.8% and 15.9% for the 5 and 10-year periods vs. -2.2% and -1.4%. (READ COMPLETE ARTICLE)

Seth Klarman – President of The Baupost Group, which manages about $22 billion, he worked for famed value investors Max Heine and Michael Price of the Mutual Shares. Klarman published a classic book on investing, Margin of Safety, Risk Averse Investing Strategies for the Thoughtful Investor, which is now out of print and has fetched upwards of $1,000-2,000 per copy in used markets. From it’s 1983 inception through 2008 his Limited partnership averaged 16.5% net annually, vs. 10.1% for the S&P 500. During the “lost decade” he crushed the S&P, returning 14.8% and 15.9% for the 5 and 10-year periods vs. -2.2% and -1.4%. (READ COMPLETE ARTICLE)

George Soros – Escaping Hungary in 1947, Soros immigrated to the U.S. in 1956 and held analyst and management positions for the next 20 years. Known as the “The man who broke the Bank of England,” he risked $10 billion against the British pound in 1992 in a risky trade and won. Soros also gained notoriety for running the Quantum Fund, which generated an average annual return of more than 30%. (READ COMPLETE ARTICLE)

George Soros – Escaping Hungary in 1947, Soros immigrated to the U.S. in 1956 and held analyst and management positions for the next 20 years. Known as the “The man who broke the Bank of England,” he risked $10 billion against the British pound in 1992 in a risky trade and won. Soros also gained notoriety for running the Quantum Fund, which generated an average annual return of more than 30%. (READ COMPLETE ARTICLE)

Bruce Berkowitz -Bruce Berkowitz has not exactly been a household name. With his boyish looks, nasally voice, and slicked-back hair, one might mistake him for a grad student. However, his results are more than academic, which explains why this invisible giant was recently named the equity fund manager of the decade by Morningstar. The Fairholme Fund (FAIRX) fund earned a 13% annualized return over the ten-year period ending in 2009, beating the S&P 500 by an impressive 14%. (READ COMPLETE ARTICLE)

Thomas Rowe Price, Jr. – Known as the “Father of Growth Investing,” in 1937 he founded T. Rowe Price Associates (TROW) and successfully ramped up the company before the launch of the T. Rowe Price Growth Stock Fund in 1950. Expansion ensued until he made a timely sale of his company in the late 1960s. His Buy and Hold strategy proved successful. For example, in the early 1970s, Price had accumulated gains of +6,184% in Xerox (XRX), which he held for 12 years, and gains of +23,666% in Merck (MRK), which he held for 31 years. (READ COMPLETE ARTICLE)

There you have it. Keep investing and continue reading about investing legends at Investing Caffeine, and who knows, maybe you too can join Sidoxia’s Hall of Fame?!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in MOT, TROW, XRX, MRK, FAIRX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Shoot First and Ask Later?

The financial markets have been hit by a tsunami on the heels of idiotic debt negotiations, a head-scratching credit downgrade, and slowing economic data after a wallet-emptying spending binge by the government. These chain of events have forced many investors and speculators alike to shoot first, and ask questions later. Is this the right strategy? Well, if you think the world is going to end and we are in a global secular bear market stifled by a choking pile of sovereign debt, then the answer is a resounding “yes.” If however, you believe the blood curdling screams from an angered electorate will eventually influence existing or soon-to-be elected politicians in dealing with the obvious, then the answer is probably “no.”

Plug Your Ears

Anybody that says they confidently know what is really going to happen over the next six months is a moron. You can ask those same so-called talking head experts seen over the airwaves if they predicted the raging +35% upward surge last summer, right after the market tanked -17% on “double-dip” concerns and Fed Chairman Ben Bernanke gave his noted quantitative easing speech in Jackson Hole, Wyoming. I’m still flicking through the channels looking for the professionals who perfectly envisaged the panicked buying of the same downgraded Treasuries Standard and Poor’s pooped on. Oh sure, it makes perfect sense that trillions of dollars would flock to the warmth and coziness of sub-2% yielding debt in a country exploding with unsustainable obligations and deficits, fueled by a Congress that can barely blows its nose to a successful negotiation.

The moral of the story is that nobody knows the future with certainty – no matter how much CNBC producers would like you to believe the opposite is true. Some of the arguably smartest people in the world have single handedly triggered financial market implosions. Consider Robert Merton and Myron Scholes, both renowned Nobel Prize winners, who brought global financial markets to its knees in 1998 when Merton and Scholes’s firm (Long Term Capital Management) lost $500 million in one day and required a $3.6 billion bailout from a consortium of banks. Or ask yourself how well Fed Chairmen Alan Greenspan and Ben Bernanke did in predicting the credit crisis and housing bubble.

If the strategist or trader du jour squawking on the boob-tube was really honest, he or she would steal the sage words of wisdom from the television series secret agent Angus MacGyver who articulated, “Only a fool is sure of anything, a wise man keeps on guessing.”

Listen to the “E”-Word

If you can’t trust all the squawkers, then whom can you trust (besides me of course…cough, cough)? The answer is no different than the person you would look for in other life-important decisions. If you needed a serious heart by-pass surgery, would you get advice from a nurse or medical professor, or would you listen more closely to the top cardiologist at the Mayo Clinic who performed over 2,000 successful surgeries? If you were looking for a pilot to fly your plane, would you prefer a 25-year-old flight attendant, or a 55-year old steely veteran who has 10 million miles of flight experience? OK, I think you get the point…legitimate experience with a track record is key.

Unfortunately, most of the slick, articulate people we see on television may look experienced and have some gray hair, but the only thing they are experienced at is giving opinions. As my great, great grandmother once told me, “Opinions are a dime a dozen, but experience is much more valuable” (embellished for dramatic effect). You are better off listening to experienced professionals like Warren Buffett (listen to his recent Charlie Rose interview), who have lived through dozens of crises and profited from them – Buffett becoming the richest person on the planet doesn’t just come from dumb luck.

If you are having trouble sleeping, you either are taking too much risk, or do not understand the nature of the risk you are taking (see Sleeping like a Baby). Things can always get worse, and the risk of a self-fulfilling further decline is a possibility (read about Soros and Reflexivity). If you are determined to make changes to your portfolio, use a scalpel, and not an axe. The recent extreme volatility makes times like these ideal for reviewing your financial position, goals, and risk tolerance. But before you shoot your portfolio first, and ask questions later, prevent a prison sentence of panic, or your financial situation may end up behind bars.

[tweetmeme source=”WadeSlome” only_single=false https://investingcaffeine.com/2011/08/20/shoot-first-and-ask-later/%5D

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MHP, CMCSA, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Soros & Reflexivity: The Tail Wagging the Dog

Billionaire investor George Soros, who is also Chairman of Soros Fund Management and author of The Crash of 2008¸ is well known for his theory on reflexivity, which broadly covers political, social, financial, and economic systems. Soros built upon this concept (see also Soros Super Bubble), which was influenced by philosopher Karl Popper. With all the fear and greed rippling through global geographies as diverse as Iceland, California, Dubai, and Greece, now is an ideal time to visit Soros’s famous reflexivity theory, which may allow us to put the recent chaos in context. With the recent swoon in the market, despite domestic indicators trending positively, a fair question to ask is whether the dog is wagging the tail or the tail wagging the dog?

The Definition of Reflexivity

Simply stated, reflexivity can be explained as the circular relationship that exists between cause and effect. Modern financial theory teaches you these lessons: 1) Financial markets are efficient; 2) Information flows freely; 3) Investors make rational decisions; and 4) Markets eventually migrate towards equilibrium. Reflexivity challenges these premises with the claims that people make irrational and biased decisions with incomplete information, while the markets trend toward disequilibrium, evidenced by repeated boom and bust cycles.

Let’s use the housing market as an example of reflexivity. By looking at the housing bubble in the U.S., we can shed some light on the theory of reflexivity. Americans initial buying love affair with homes pushed prices of houses up, which led to higher valuations of loans on the books of banks, which allowed the banks to lend more money to buyers, which meant more home buying and pushed prices up even higher. To make matters worse, even the government joined the game by adding incentives for people who could not afford homes. As you can see, the actions and decisions of an observer can have a direct impact on other observers and the system itself, thereby creating a spiraling upward (or downward) effect.

Now What?

Now, the reflexivity tail that is wagging the dog is Europe…specifically Greece. The bear case goes as follows: the Greek financial crisis will brew into a stinky contagion, eventually spreading to Spain and Italy, thus hammering shut a U.S. export market. The double dip recession in the U.S. will not only exacerbate the pricking of the Chinese real estate bubble, but also topple all other global economies into ruin.

Certainly, the excessive sovereign debt levels across the globe have grown like cancer. Fortunately, we have identified the problem and politicians are being forced by voters to address the fiscal problems. More importantly, capital flows are an unbiased arbiter of economic policies. Over time – not in the short-run necessarily – capital will move to where it is treated best. Meaning those countries that harness responsible debt loads, institute pro-business growth policies, remove unsustainable and insolvent entitlements, and incentivize education and innovation will be the countries that earn the honor of holding their fair share of vital capital. If the politicians don’t make the correct decisions, the hemorrhaging of capital to foreigners and the painfully high unemployment levels will force Washington into making the tough but right decisions (usually in the middle of a crisis).

Reflexivity, as it pertains to financial markets, has been a concept the 79 year old George Soros has passionately espoused since his 1987 book, The Alchemy of Finance. Perhaps a better understanding of reflexivity will help us better take advantage of the tail wagging disequilibriums experienced in the current financial markets. Time will tell how long this disequilibrium will last.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

FX, the Carry Trade, and Arbitrage Vigilantes

What do you think of the Euro? How about the Japanese yen? Are you expecting the Thai baht to depreciate in value versus the Brazilian real? Speculators, central banks, corporations, governments, financial institutions, and other constituencies ask similar types of questions every day. The largely over-the-counter global foreign exchange markets (no central exchange) are ubiquitous, measuring in the trillions – the BIS (Bank for International Settlements) computed the value of traditional foreign exchange markets at $3.2 trillion in April 2007. Thanks to globalization, these numbers are poised to expand even further. Like other futures markets (think oil, gold, or pork bellies), traders can speculate on the direction of one currency versus another. Alternatively, investors and businesses around the world can use currency futures to hedge (protect) or facilitate international trade.

Without getting lost in the minutiae of foreign exchange currency trading, I think it’s helpful to step back and realize regardless of strategy, currency, interest rate, inflation, peg-ratio, deficits, sovereign debt, or other factor, money will eventually migrate to where it is treated best in the long-run. When it comes to currencies, it’s my fundamental belief that economies control their currency destinies based on the collective monetary, fiscal, and political decisions made by each country. If those decisions are determined imprudent by financial market participants, countries open themselves up to speculators and investors exploiting those decisions for profits.

Currency Trading Ice Cream Style

As mentioned previously, currency trading is predominantly conducted over-the-counter, outside an exchange, but there are almost more trading flavors than ice cream choices at Baskin-Robbins. For instance, one can trade currencies by using futures, options, swaps, exchange traded funds (ETFs), or trading on the spot or forward contract markets. Each flavor has its own unique trading aspects, including the all-important amount of leverage employed.

The Carry Trade

Similar to other investment strategies (for example real estate), if profit can be made by betting on the direction of currencies, then why not enhance those returns by adding leverage (debt). A simple example of a carry trade can illustrate how debt is capable of boosting returns. Suppose hedge fund XYZ wants to borrow (sell U.S. dollars) at 0.25% and buy the Swedish krona currency so they can invest that currency in 5.00% Swedish government bonds. Presumably, the hedge fund will eventually realize the spread of +4.75% (5.00% – 0.25%) and with 10x leverage (borrowings) the amplified return could reach +47.5%, assuming the relationship between the U.S. dollar and krona does not change (a significant assumption).

Positive absolute returns can draw large pools of capital and can amplify volatility when a specific trade is unwound. For example, in recent years, the carry trade from borrowing Japanese yen and investing in the Icelandic krona eventually led to a sharp unwinding in the krona currency positions when the Icelandic economy collapsed in 2008. High currency values make exports less competitive and more expensive, thereby dampening GDP (Gross Domestic Product) growth. On the flip side, higher currency values make imported goods and services that much more affordable – a positive factor for consumers. Adding complexity to foreign exchange markets are the countries, like China, that artificially inflate or depress currencies by “pegging” their currency value to a foreign currency (like the U.S. dollar).

Soros & Arbitrage Vigilantes

Hedge funds, proprietary trading desks, speculators and other foreign exchange participants continually comb the globe for dislocations and discrepancies to take advantage of. Traders are constantly on the look out for arbitraging opportunities (simultaneously selling the weakest and buying the strongest). Famous Quantum hedge fund manager, George Soros, took advantage of weak U.K. economy in 1992 when he spent $10 billion in bet against the British pound (see other Soros article). The Bank of England fought hard to defend the value of the pound in an attempt to maintain a pegged value against a basket of European currencies, but in the end, because of the weak financial condition of the British economy, Soros came out victorious with an estimated $1 billion in profits from his bold bet.

I’m not sure whether the debate over speculator involvement in currency collapses can be resolved? What I do know is the healthier economies making prudent monetary, fiscal, and political decisions will be more resilient in protecting themselves from arbitrage vigilantes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct position on any security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Soros on the Super Bubble

Like a bubble formed from chewing gum, the gradual expansion of the spherical formation occurs much slower than the immediacy of the pop. A minority of investors identified the treacherous, credit-induced bubble of 2008 before it burst, however not included in that group are financial regulators. Now we’re left with the task of cleaning up the sticky mess on our faces and establishing measures to prevent future blow-ups.

George Soros, Chairman of Soros Fund Management and author of The Crash of 2008, has been around the financial market block a few times, so I think it pays to heed the regulatory reform recommendations as it relates to the “Super bubble” of 2008. As you probably know, financial bubbles are not a new concept. Beyond the oft-mentioned technology and real estate bubbles of this decade, bubbles such as the “Tulip-mania” of the 1630s serve as a gentle reminder of the everlasting existence of irrational economic behavior. If the Dutch were willing to pay $76,000 for a tulip bulb (inflation-adjusted) almost 400 years ago, then virtually any mania is possible.

Bubbles and Efficiency

Efficient markets are somewhat like UFOs. Some people believe in them, but many do not. In order to believe in the existence of bubbles, one needs to question the validity of the pure form of efficient markets (read more about market efficiency). Here’s how Soros feels about market efficiency:

“I contend that financial markets always present a distorted picture of reality.”

I believe we will be in a hyper-sensitive period of bubble witch-hunting for a while, as the fresh wounds of 2008-09 heal themselves. If you get in early enough, bubbles can be profitable. Unfortunately, like a distracted teen fixated on the sunbathers at a nude beach, the excitement can lead to a painful burn if preventative sunscreen measures are not taken. Most bubble participants are too exhilarated to carry out a thoughtful exit strategy – the news can just be too tempting to jump off the top.

In his analysis of market regulation, Soros lays some of the “Great Recession” blame on the Federal Reserve and Alan Greenspan (Chairman of Fed):

“Instead of a tendency towards equilibrium, financial markets have a tendency to develop bubbles. Bubbles are not irrational: it pays to join the crowd, at least for a while. So regulators cannot count on the market to correct its excesses…The crash of 2008 was caused by the collapse of a super-bubble that has been growing since 1980. This was composed of smaller bubbles. Each time a financial crisis occurred the authorities intervened, took care of the failing institutions, and applied monetary and fiscal stimulus, inflating the super-bubble even further.”

Soros’ Recipe for Reform

What is Soros’ solution for the “Super bubble?” Here are some recommendations from his Op-Ed in the Financial Times:

- Regulator Accountability: First of all, financial authorities need to accept responsibility for preventing excesses – excuses are not an acceptable response.

- Control Credit: Rather than having static monetary targets such as margin requirements, capital reserve requirements, and loan-to-value ratios, Soros argues these metrics can be adjusted in accordance with the swinging moods of economic cycles. He punctuates the point by saying, “To control asset bubbles it is not enough to control the money supply; you must also control credit.”

- Limit Overheating in Specific Sectors: Had regulators limited lending during the real estate explosion or had the SEC limited technology IPOs in the late 1990s, perhaps our country would be in better financial health today.

- Manage Derivatives and Systemic Risk: Basically what Soros is saying here is that many market participants can become overwhelmed by certain exposures or exotic instruments, therefore it behooves regulators to proactively step in and regulate.

- Manage Too Big to Fail (read related Graham IC article): According to Soros a big reason we got into this trouble relates to the irresponsible proprietary trading departments at some of the larger banks. Responsibly separating these departments and limiting the amount of risk undertaken is an important element to the safety of our financial system.

- Reformulate Asset Holding Rules: Underestimating the risk profile of a certain security can lead to concentration issues, which can potentially generate systemic risk. Soros highlights the European Basel Accord rules as an area that can use some improvement.

Soros admits most, if not all, the measures he proposes will choke off the profitability of banks. For this reason, regulators must be very careful with the implementation and timing of these financial strategies. If employed too aggressively, the economy could find itself in a deflationary spiral. Move too slowly, and the loose monetary measures instituted by the Fed could fan the flames of inflation.

Bubbles will never go away. Eventually, the recent panic-induced fear will fade away and the entrepreneurial seeds of greed will germinate into new budding flowers of optimism. As investors nervously chomp away at their chewing gum, I will patiently await for the next financial bubble to form. I echo George Soros’s hope that regulators prick future “mini-bubbles” before they become “super-bubbles.”

Read Full George Soros Op-Ed on The Financial Times 10/25/09

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct positions in an security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Back to the Future: Mag Covers (Part III)

Congratulations to those who have graduated through my first two articles (Part I and Part II) regarding the use of media magazine covers as contrarian investment indicator tools. We’ve reviewed magazine’s horrendous ability of predicting market shifts during the 1970s and Tech Bubble of 2000, and now we will take a peek at the “Great Recession” of 2008 and 2009. If you have the stamina to complete this final article, your diploma and selfless glory will be waiting for you at the end.

This magazine cover series was not designed to be utilized as an exploitable investment strategy, but rather to increase awareness and raise skepticism surrounding investment content. Just because something is written or said by journalist or blogger does not mean it is a fact (although I fancy facts). In the field of investing, along with other behavioral disciplines, there are significant gray areas left open to interpretation. A more educated, critical eye exercised by the general public will perhaps release us from the repetitive boom-bust cycles we’ve become accustomed to. Perhaps my goal is naïve and idealistic, nonetheless I dare to dream.

The wounds from a year ago are still fresh, and we have not fully escaped from the problems that originally got us into this mess, but it is amazing what a 60%+ market move since March can do to the number of “Great Depression” references. Let’s walk down calamity memory lane over the last year:

Great Depression Redux?

Months ago we were in the midst of a severe recession, and the media was not shy about jumping on the “pessimism porn” bandwagon for the sake of ratings. Like a Friday the 13th sequel (nice tie in!), CNBC just weeks ago was plugging the crisis anniversary of the Lehman Brothers failure. Time magazine’s portrayal of the financial crisis as the next Great Depression, including the soup kitchen lines, mass unemployment, and collapse of thousands of banks, was used like chum to feed the frenzy of shocked investing onlookers. Unemployment rates are still creeping up, albeit at a slower rate, but we are nowhere near the 25% levels seen in the Great Depression.

American Disintegration

One of my favorite articles (read here) of the global crisis was written by The Wall Street Journal late last year about a Russian Professor, Igor Panarin (also a former KGB analyst). I find it absurdly amusing that the WSJ would even give credence to this story, but perhaps now I can look forward to an Op-Ed in their newspaper from Iranian President Mahmoud Ahmadinejad or North Korean Leader Kim Jong Ill. Not only did Professor Panarin pronounce the complete evaporation of the United States, but he also provided a specific timeframe. In late June or early July 2010, he expects the U.S. to fall into civil war and subsequently get carved up into six pieces by particular foreign regions, including China, Mexico, E.U., Japan, Canada, and Russia (which will control Alaska of course). I guess Sarah Palin will not be a happy camper?

Other Crisis Souvenirs

Hey Georgy, let me know when you turn bullish…so I can sell!

Market Mayhem

- Who’s that on the cover? Nancy Pelosi?!

Lessons Learned

Contrarianism for the sake of contrarianism is not necessarily a good thing. Trend can be your friend too. Bubbles take much longer to inflate than they burst, so it may be in your best interest to ride the wave of ecstasy for longer than the early alarm ringers. Take for example Alan Greenspan’s infamous irrational exuberance speech in 1996, when the NASDAQ index was trading around 1300. As we all know, the NASDAQ went on to pierce the 5000 mark, four years later. Sorry Al…right idea, but a tad early. Although he may have been correct directionally, his timing and degree were way off. Pundits like Nouriel Roubini and Peter Schiff are other examples of prognosticators who identified the financial crisis many years before the catastrophe actually hit. As I noted previously, trading based on magazine covers was not conceived as a legitimate investable strategy, but as I’ve shown they can be indicators of sentiment. And these sentiment indicators can be used as a valuable apparatus in your toolbox to prevent harmful decisions at the worst possible times.

Thanks for coming Back to the Future on this historical tour of cover stories. Now that you have graduated with honors, next time you are in line at the grocery store, feel free to flash your diploma to receive a discount on a magazine purchase.

Class dismissed.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}