Posts tagged ‘fiscal policy’

Choosing Your Favorite Dental Procedure: Recession or Inflation?

Going to the dentist can be a pleasurable or painful experience, depending on whether you have been properly brushing and flossing your teeth. If the stock market was a patient, its 2024 checkup would produce a large smile. Why so happy? Because the S&P 500 index is up a healthy +5.6% in the first four months of the year, thanks to a resilient economy, robust employment, and record corporate profits (see chart below). The smiles were even larger a month ago before the S&P 500’s five-month, almost +30% winning streak was broken from October to March.

Source: Yardeni.com

Driving the overall record profits of the stock market are the “Magnificent Seven” (see Fight the Fed or Risk Going Dead), which include mega-technology companies such as AI (Artificial Intelligence) stalwarts like NVIDIA Corp., Microsoft Corp., Alphabet Inc. (Google), and Meta Platforms Inc. As you can see in the chart below, these tech behemoths are generating gargantuan mounds of cash that are piling up at flabbergasting rate of over $300 billion per year.

Source: The Financial Times

How are these Silicon Valley titans achieving such colossal results? The short answer is: The AI Wave. As I pointed out in a previous post of mine, The World of AI, artificial intelligence projects are so large that Meta Platforms CEO Mark Zuckerberg committed to purchasing upwards of a jaw-dropping $10 billion in NVIDIA H100 chips by year-end. To put some of this AI craze into perspective, we learned over the last week that the combined 2024 capital expenditure plans of four companies (Microsoft, Alphabet, Meta and Amazon) are forecasted to exceed $200 billion – much of that driven by generative AI projects.

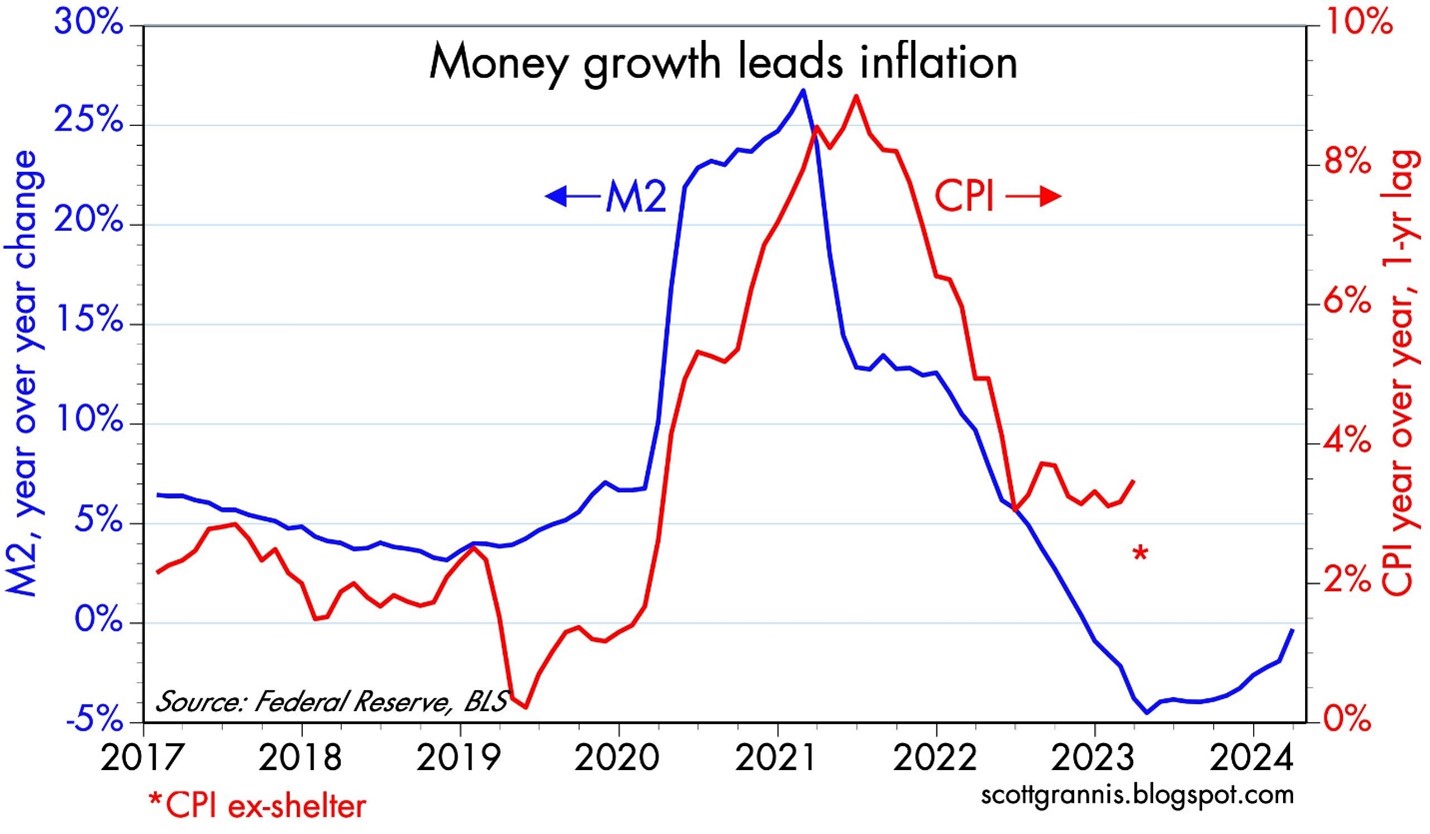

While many of these aforementioned companies are benefitting disproportionately from their exposure to AI, what has really been giving investors a toothache has been stubbornly high and sticky inflation (see red line on chart below), which has pushed up interest rates higher on the 10-Year Treasury Note yield by approximately +0.5% this month, near a 17-year high of 4.69%. Higher interest rates are bad for long-term bond prices (e.g., TLT down -6.8% last month) and generally troublesome for stocks as well. That’s why the S&P 500 took a breather last month with the S&P declining -4.2%, the Dow Jones Industrial Average falling -5.0%, and the technology-heavy NASDAQ index dropping -4.4%.

Source: Calafia Beach Pundit

Your Favorite Dental Procedure?

Investors definitely don’t want higher interest rates, but stock traders should be careful what they wish for. If low interest rates are really what investors want, this scenario could result in an undesirable package deal that includes a recession. So, if pain can come from different scenarios, what is your favorite economic dental procedure?

• A hot economy giving rise to high inflation/high interest rates?

• A cold economy triggering a recession with low interest rates?

I don’t know about you, but both these procedures sound painful to me.

Traders would certainly love to get some anesthesia in the form of Federal Reserve interest rate cuts to relieve the recent stock market pain. Nevertheless, Federal Reserve Chairman, Jerome Powell, has been hawkishly candid in his recent commentary, indicating he will be “data dependent” and let the forthcoming economic numbers guide the Fed’s monetary policy on future interest rate decisions.

Coming into 2024, most pundits were calling for a series of seven interest rate cuts by the end of the year. However, due to the hotter and more resilient economy, now the pendulum of investor sentiment has swung to an expectation of only one or two cuts. We will learn more today when the Fed concludes a two-day meeting with a published interest rate policy decision followed by a subsequent press conference with Jerome Powell.

Of course, not all financial scenarios necessarily have to lead to what feels like a painful root canal or tooth extraction. There is a legitimate path to a so-called “soft-landing.” This would be a goldilocks scenario in which our current elevated interest rates (i.e., Federal Funds target of 5.25% – 5.50%) gradually slow the economy to a level that continues the previous downward inflation trajectory towards the Fed’s long-term objective of 2.0%. If the “soft-landing” were achieved, the Fed could then begin cutting rates again to stimulate the economy.

Regardless of our country’s economic outcome, we can probably agree there is a lot of uncertainty out in the world. These unknowns include Russia-Ukraine, Israel-Hamas, our elections, inflation, Fed monetary policy, bond volatility, stock volatility, and a whole host of other variables. With this backdrop in mind, it’s more important than ever to ensure you have a diversified portfolio and detailed financial plan in place to achieve your long-term life goals. Do yourself a favor and get a financial check-up with an independent, experienced advisor like Sidoxia Capital Management (www.Sidoxia.com). That way, you can smile with a healthy set of pearly whites, rather than grimace in pain as you would from an undesirable dental procedure.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in individual stocks , certain exchange traded funds (ETFs), including NVDA, MSFT, META, and AMZN, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

April Flowers Have Investors Cheering Wow-sers!

Normally April showers bring May flowers, but last month the spring weather was dominated by sunshine that caused stock prices to blossom to new, all-time record highs across all major indexes. More specifically, the S&P 500 jumped +5.2% last month, the NASDAQ catapulted +5.4%, and the Dow Jones Industrial Average rose +2.7%. For the year, the Dow and S&P 500 index both up double-digit percentages (11%), while the NASDAQ is up a few percentage points less than that (8%).

What has led to such a bright and beaming outlook by investors? For starters, economic optimism has gained momentum as the global coronavirus pandemic appears to be improving after approximately 16 months. Not only are COVID-19 cases and hospitalizations rates declining, but COVID-19 related deaths are dropping as well. A large portion of the progress can be attributed to the 246 million vaccine doses administered so far in the United States.

Blossoming Economy

As a result of the improving COVID-19 health climate, economic activity, as measured by Gross Domestic Product (GDP), expanded by a healthy +6.4% rate during the first quarter. Economists are forecasting second quarter growth to accelerate to an even more brilliant rate of +10%.

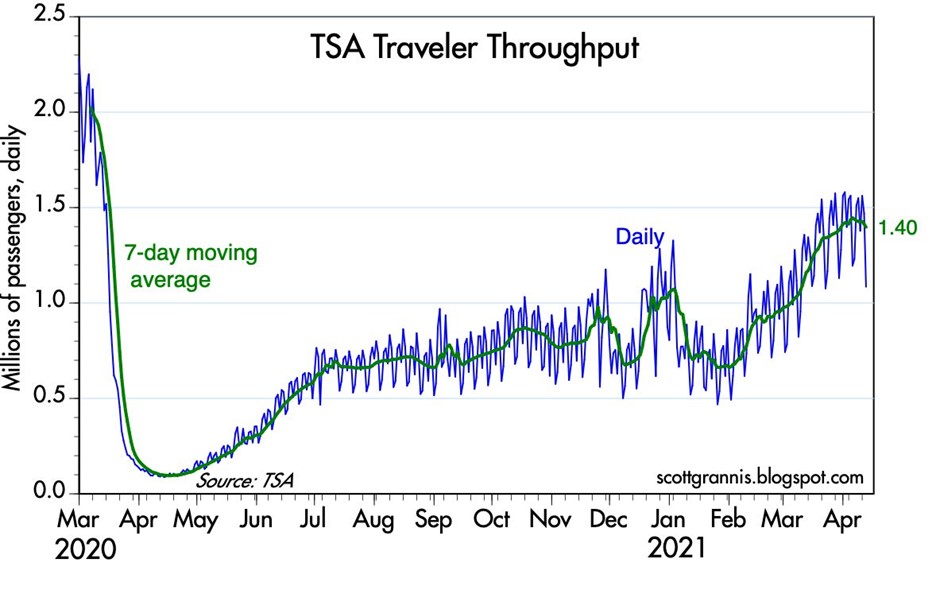

As the economy further re-opens and pent-up consumer demand is unleashed, activity is sprouting up in areas like airlines, hotels, restaurants, bars, movie theaters and gyms. An example of consumer demand climbing can be seen in the volume of passenger traffic in U.S. airports, which has increased substantially from the lows a year ago, as shown below in the TSA (Transportation Security Administration) data.

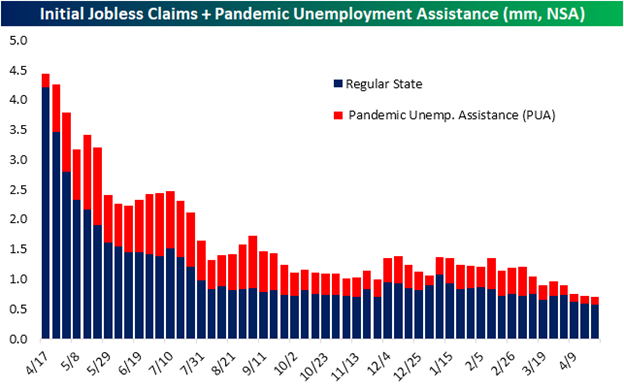

A germinating economy also means a healthier employment market and more jobs. The chart below shows the dramatic decline in the number of jobless receiving benefits and pandemic unemployment assistance.

Fed Fertilizer & Congressional Candy

Monetary and fiscal stimulus are creating fertile ground for the surge in growth as well. The Federal Reserve has been clear in their support for the economy by effectively maintaining its key interest rate target at 0%, while also maintaining its monthly bond buying program at $120 billion – designed to sustain low interest rates for the benefit of consumers and businesses.

From a fiscal perspective, Congress is serving up some sweet candy by doling out free money to Americans. So far, roughly $4 trillion of COVID-19 related stimulus and relief have passed Congress (see also Consumer Confidence Flies), and now President Biden is proposing roughly an additional $4 trillion of stimulus in the form of a $2 trillion jobs and infrastructure plan and a $1.8 trillion American Families Plan.

Candy and Spinach

While Congress is serving up trillions in candy, eventually, Americans are going to have to eat some less appetizing spinach in the form of higher taxes. Generally speaking, nobody likes higher taxes, so the question becomes, how does the government raise the most revenue (taxes) without upsetting a large number of voters? As 17th century French statesman Jean-Baptiste Colbert proclaimed, “The art of taxation consists in so plucking the goose as to get the most feathers with the least hissing.”

President Biden has stated he will only increase income taxes on people earning more than $400,000 annually and increase capital gains taxes for those earning more than $1,000,000 per year. According to CNBC, those earning more than $400,000 only represents 1.8% of total taxpayers.

Bitter tasting spinach for Americans may also come in the form of higher inflation (i.e., a general rise in a basket of goods and services), which silently eats away at everyone’s purchasing power, especially those retirees surviving on a fixed income. Federal Reserve Chairman Jerome Powell sees any increase in inflation as transitory, but if prices keep rising, the Federal Reserve will be forced to increase interest rates. Such a reversal in rates could choke off economic growth and potentially force the economy into a recession.

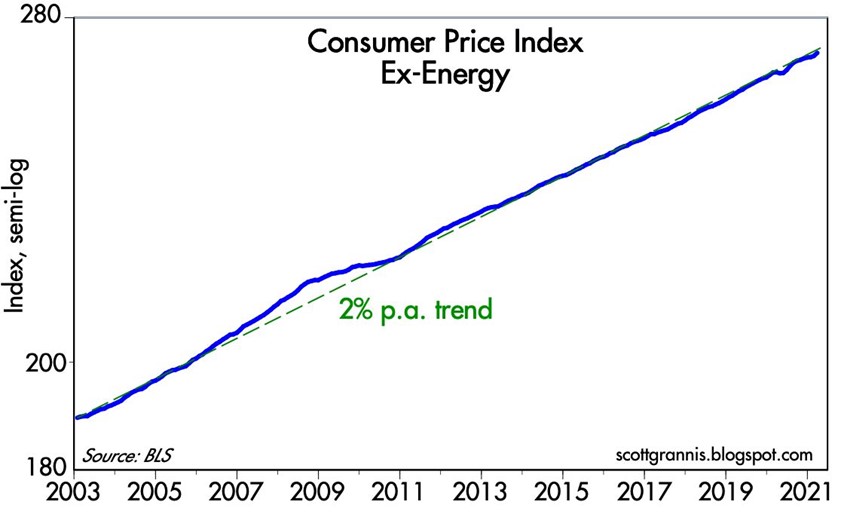

If you strip out volatile energy prices, the good news is that underlying inflation has not spiraled higher out of control, as you can see from the chart below.

In addition to the concerns of potential higher taxes, inflation, and rising interest rate policies from the Federal Reserve, for many months I have written about my apprehension about the speculation in SPACs (Special Purpose Acquisition Companies) and cryptocurrencies like Bitcoin. There are logical explanations to invest selectively into SPACs and purchase Bitcoin as a non-correlated asset for diversification purposes and a hedge against the dollar. But unfortunately, if history repeats itself, speculators will eventually end up in a pool of tears.

While there are certainly some storm clouds on the horizon (e.g., taxes, inflation, rising interest rates, speculative trading), April bloomed a lot of flowers, and the near-term forecast remains very sunny as the economy emerges from a global pandemic. As long as the government continues to provide candy to millions of Americans; the Federal Reserve remains accommodative in its policies; and the surge in pent-up demand persists to drive economic growth, we likely have some more time before we are forced to eat our spinach.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 3, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

GDP Figures & Election Jitters

Ever since the beginning of 2020, it’s been a tale of two cities. As renowned author Charles Dickens famously stated, “It was the best of times and worst of times.” The year started with unemployment at a “best of times” low level of 3.5% (see chart below) before coronavirus shutdown the economy during March when we transitioned to the “worst of times.”

|

With the recent release of record-high Gross Domestic Product (GDP) figures of +33.1% growth in Q3 (vs. -31.4% in Q2), and a +49% stock market rebound from the COVID-19 lows of March, a debate has been raging. Is the re-opening economic rebound that has occurred a V-shaped recovery that will continue expanding, or is the recovery that has occurred since March a temporary dead-cat bounce?

|

For many people, the ultimate answer depends on the outcome of the impending presidential election. Making matters worse are the polarized politics that are being warped, distorted, and amplified by social media (see Social Dilemma). Although the election jitters have many stock market participants on pins and needles, history reminds us that politics have little to do with the long-term direction of the stock market and financial markets. As the chart below shows, over the last century, stock prices have consistently gone up through both Democratic (BLUE) and Republican (RED) administrations.

|

Even if you have trouble digesting the chart above, I repeatedly remind investors that political influence and control are always temporary and constantly changing. There are various scenarios predicted for the outcome of the current 2020 elections, including a potential “Blue Wave” sweep of the Executive Branch (the president) and the Legislative Branch (the House of Representatives and Senate). Regardless of whether there is a Blue Wave, Red Wave, or gridlocked Congress, it’s worth noting that the previous two waves were fleeting. Unified control of government by President Obama (2008-2010) and President Trump (2016-2018) only lasted two years before the Democrats and Republicans each lost 100% control of Congress (the House of Representatives flipped to Republican in 2010 and Democrat in 2018).

Even though Halloween is behind us, many people are still spooked by the potential outcome of the elections (or lack thereof), depending on how narrow or wide the results turn out. Despite the +49% appreciation in stock prices, stock investors still experienced the heebie-jeebies last month. The S&P 500 index declined -2.8% for the month, while the Dow Jones Industrial Average and Nasdaq Composite index fell -4.6% and -2.3%, respectively. It is most likely true that a close election could delay an official concession, but with centuries of elections under our belt, I’m confident we’ll eventually obtain a peaceful continuation or transition of leadership.

Regardless of whomever wins the presidential election, roughly half the voters are going to be unhappy with the results. For example, even when President Ronald Reagan won in a landslide victory in 1980 (Reagan won 489 electoral votes vs. 49 for incumbent challenger President Jimmy Carter), Reagan only won 50.8% of the popular vote. In other words, even in a landslide victory, roughly 49% of voters were unhappy with the outcome. No matter the end result of the approaching 2020 election, suffice it to say, about half of the voting population will be displeased.

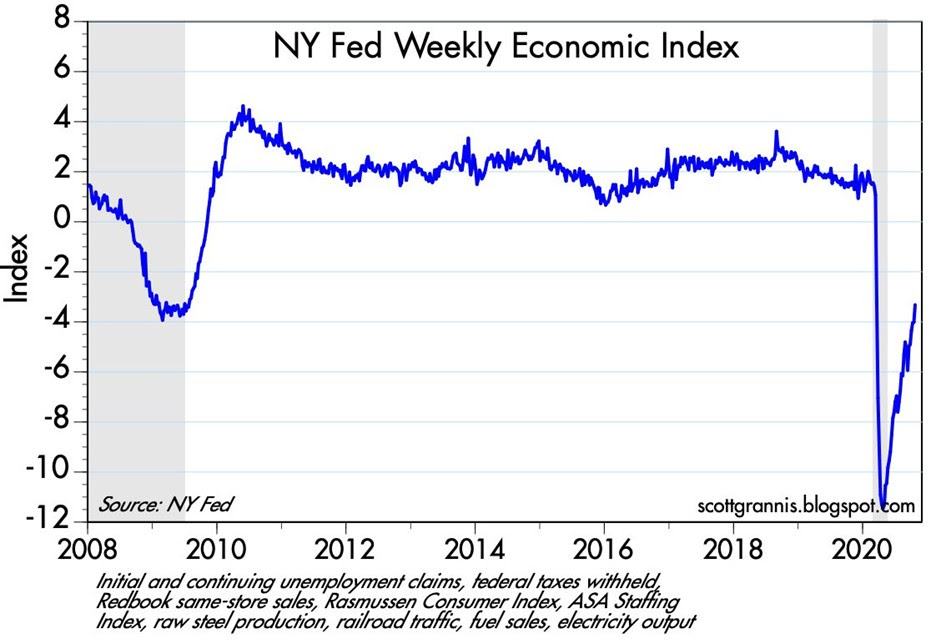

Despite the likely discontent, the upcoming winner will be working with (or inheriting) an economy firmly in recovery mode, whether you are referencing, jobs, automobile sales, home sales, travel, transportation traffic, consumer spending, or other statistics. The Weekly Economic Index from the New York Federal Reserve epitomizes the strength of the V-shaped recovery underway (see chart below).

It will come as no surprise to me if we continue to experience some volatility in financial markets shortly before and after the elections. However, history shows us that these election jitters will eventually fade, and the tale of two cities will become a tale of one city focused on the fundamentals of the current economic recovery.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (November 2, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFS), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}