Posts tagged ‘Financial Planning’

Time for Your Retirement Physical

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (October 1, 2014). Subscribe on the right side of the page for the complete text.

As a middle-aged man, I’ve learned the importance of getting my annual physical to improve my longevity. The same principle applies to the longevity of your retirement account. With the fourth quarter of the calendar year officially underway, there is no better time to probe your investment portfolio and prescribe some recommendations relating to your financial goals.

A physical is especially relevant given all the hypertension raising events transpiring in the financial markets during the third quarter. Although the large cap biased indexes (Dow Jones Industrials and S&P 500) were up modestly for the quarter (+1.3% and +0.6%, respectively), the small and mid-cap stock indexes underperformed significantly (-8.0% [IWM] and -4.2% [SPMIX], respectively). What’s more, all the daunting geopolitical headlines and uncertain macroeconomic data catapulted the Volatility Index (VIX – aka, “Fear Gauge”) higher by a whopping +40.0% over the same period.

- What caused all the recent heartburn? Pick your choice and/or combine the following:

- ISIS in Iraq

- Bombings in Syria

- End of Quantitative Easing (QE) – Impending Interest Rate Hikes

- Mid-Term Elections

- Hong Kong Protests

- Tax Inversions

- Security Hacks

- Rising U.S. Dollar

- PIMCO’s Bill Gross Departure

(See Hot News Bites in Newsletter for more details)

As I’ve pointed out on numerous occasions, there is never a shortage of issues to worry about (see Series of Unfortunate Events), and contrary to what you see on TV, not everything is destruction and despair. In fact, as I’ve discussed before, corporate profits are at record levels (see Retail Profits chart below), companies are sitting on trillions of dollars in cash, the employment picture is improving (albeit slowly), and companies are finally beginning to spend (see Capital Spending chart below):

Retail Profits

Source: Dr. Ed’s Blog

Capital Spending

Source: Calafia Beach Pundit

Even during prosperous times, you can’t escape the dooms-dayers because too much of a good thing can also be bad (i.e., inflation). Rather than getting caught up in the day-to-day headlines, like many of us investment nerds, it is better to focus on your long-term financial goals, diversification, and objective financial metrics. Even us professionals become challenged by sifting through the never-ending avalanche of news headlines. It’s better to stick with a disciplined, systematic approach that functions as shock absorbers for all the inevitable potholes and speed bumps. Investment guru Peter Lynch said it best, “Assume the market is going nowhere and invest accordingly.” Everyone’s situation and risk tolerance is different and changing, which is why it’s important to give your financial plan a recurring physical.

Vacation or Retirement?

Keeping up with the Joneses in our instant gratification society can be a taxing endeavor, but ultimately investors must decide between 1) Spend now, save later; or 2) Save now, spend later. Most people prefer the more enjoyable option (#1), however these individuals also want to retire at a young age. Often, these competing goals are in conflict. Unless, you are Oprah or Bill Gates (or have rich relatives), chances are you must get into the practice of saving, if you want a sizeable nest egg…before age 85. The problem is Americans typically spend more time planning their vacation than they do planning for retirement. Talking about finances with an advisor, spouse, or partner can feel about as comfortable as walking into a cold doctor’s office while naked under a thin gown. Vulnerability may be an undesirable emotion, but often it is a necessity to reach a desired goal.

Ignorance is Not Bliss – Avoid Procrastination

Many people believe “ignorance is bliss” when it comes to healthcare and finance, which we all know is the worst possible strategy. Normally, individuals have multiple IRA, 401(k), 529, savings, joint, trust, checking and other accounts scattered around with no rhyme or reason. As with healthcare, reviewing finances most often takes place whenever there is a serious problem or need, which is usually at a point when it’s too late. Unfortunately, procrastination typically wins out over proactiveness. Just because you may feel good, or just because you are contributing to your employer’s 401(k), doesn’t mean you shouldn’t get an annual physical for your health and finances. I’m the perfect example. While I feel great on the outside, ignoring my high cholesterol lab results would be a bad idea.

And even for the DIY-ers (Do-It-Yourself-ers), rebalancing your portfolio is critical. In the last fifteen years, overexposure to technology, real estate, financials, and emerging markets at the wrong times had the potential of creating financial ruin. Like a boat, your investment portfolio needs to remain balanced in conjunction with your goals and risk tolerance, or your savings might tip over and sink.

Financial markets go up and down, but your long-term financial well-being does not have to become hostage to the daily vicissitudes. With the fourth quarter now upon us, take control of your financial future and schedule your retirement physical.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in IWM, SPMIX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Only Thing to Fear is the Unknown Itself

Martin Luther King, Jr. famously stated, “The only thing we have to fear is fear itself,” but when it comes to the stock market, the only thing to fear is the “unknown.” As much as people like to say, “I saw that crisis coming,” or “I knew the bubble was going to burst,” the reality is these assertions are often embellished, overstated, and/or misplaced.

How many people saw these events coming?

- 1987 – Black Monday

- Iraqi War

- Thai Baht Currency Crisis

- Long-Term Capital Management Collapse & Bailout

- 9/11 Terrorist Attack

- Lehman Brothers Bankruptcy / Bear Stearns Bailout

- Flash Crash

- U.S. Debt Downgrade

- Arab Spring

- Sequestration Cuts

- Cyprus Financial Crisis

- Federal Reserve (QE1, QE2, QE3, Operation Twist, etc.)

Sure, there will always be a prescient few who may actually get it right and profit from their crystal balls, but to assume you are smart enough to predict these events with any consistent accuracy is likely reckless. Even for the smartest and brightest minds, uncertainty and doubt surrounding such mega-events leads to inaction or paralysis. If profiting in advance of these negative outcomes was so easy, you probably would be basking in the sun on your personal private island…and not reading this article.

Coming to grips with the existence of a never-ending series of future negative financial shocks is the price of doing business in the stock market, if you want to become a successful long-term investor. The fact of the matter is with 7 billion people living on a planet orbiting the sun at 67,000 mph, the law of large numbers tells us there will be many unpredictable events caused either by pure chance or poor human decisions. As the great financial crisis of 2008-2009 proved, there will always be populations of stupid or ignorant people who will purposely or inadvertently cause significant damage to economies around the world.

Fortunately, the power of democracy (see Spreading the Seeds of Democracy) and the benefits of capitalism have dramatically increased the standards of living for hundreds of millions of people. Despite horrific outcomes and unthinkable atrocities perpetrated throughout history, global GDP and living standards continue to positively march forward and upward. For example, consider in my limited lifespan, I have seen the introduction of VCRs, microwave ovens, mobile phones, and the internet, while experiencing amazing milestones like the eradication of smallpox, the sequencing of the human genome, and landing space exploration vehicles on Mars, among many other unimaginable achievements.

Despite amazing advancements, many investors are paralyzed into inaction out of fear of a harmful outcome. If I received a penny for every negative prediction I read or heard about over my 20+ years of investing, I would be happily retired. The stock market is never immune from adverse events, but chances are a geopolitical war in Ukraine/Iraq; accelerated Federal Reserve rate tightening; China real estate bubble; Argentinian debt default; or other current, worrisome headline is unlikely to be the cause of the next -20%+ bear market. History shows us that fear of the unknown is more rational than the fear of the known. If you can’t come to grips with fear itself, I fear your long-term results will lead to a scary retirement.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Rise of the Robo-Advisors: Paying to Do-It-Yourself

Robots and computers are taking over our lives. We see it in areas of our daily living, including the use of digitally driven cars, cell phones, automated vacuums, and electronic self-serve kiosks at the grocery store. And now robots have come into our investing and financial lives in the form of robo-advisors. With a few clicks of a computer mouse or taps on a smartphone, investors are hoping to find their way to financial nirvana.

What sites am I talking about? Here is a brief, albeit rapidly growing, list of popular robo-advisor sites:

Not all of these robo-sites invest individuals’ money, but nevertheless, there are several factors contributing to the upsurge in in these financial advice websites. For starters, there is a whole new, younger demographic pool of savers who have grown up with their iPhone and shop exclusively online for their goods and services. Many of these financial sites are trying to fill a void for this tech-savvy group looking for a new app to bring wealth and riches.

Another factor contributing to the rise of the robo-advisors is a function of the 2008-2009 financial crisis and the explosive growth of the multi-trillion dollar exchange traded fund (ETF) industry. Many baby boomers who were planning to retire were hit brutally hard by the financial crisis and subsequently asked themselves why they were paying such high fees to their advisors for losing money. With the stock market now increasing for five consecutive years, some investors are gaining confidence in pursuing other lower-cost solutions to their investments outside of the traditional human advisor channel.

Too Good to Be True? The Shortcomings

On the surface, the proposition of clicking a few buttons to create financial prosperity seems quite appealing, but if you look a little more closely under the hood, what you quickly realize is that most of these robo-advisor sites are glorifying the practice of doing-it-yourself (DIY). After conducting some due diligence on the various investment bells-and-whistles of these robo-sites, one quickly realizes individuals can replicate most of the kindergartener-esque ETF portfolios by merely calling 1-800-VANGUARD – without having to pay robo-advisor fees ranging from 0.15% – 0.95%. More specifically, Wealthfront and Betterment use 6-12 ETF security portfolios, integrating many Vanguard funds and other ETFs that can be purchased with a click of a mouse or phone call (without having to pay the robo-advisor middleman). A cynic may also point out these robo-investment sites are nothing more than expensive life-cycle funds that could be replicated at a fraction of the cost.

Despite the sites’ transparency preaching, filtering through robo fee and performance disclosure can be frustratingly tedious too – good luck to the novices. For example, Betterment claims to have created a superior performance track record, despite a hidden disclosure stating the results are manufactured from a computer back-test. The transparency pitch seems a little disingenuous, and I wonder how many of the new robo-site users are also aware of the extra underlying ETF fees? But when marketing a new high-cost start-up, I guess you need to fabricate a fancy chart and track record when you don’t have one. Underlying the robo investment sites is a disparate, hodge-podge of studies anointing Modern Portfolio Theory as the holy grail, but readers of this blog know there are many failings to pure quantitative strategies implemented by academics (see LTCM in Black Swans & Butter in Bangladesh).

The concept of DIY is nothing new. One can look no further than the impact Home Depot (HD) has had on the home improvement industry. In addition, there are plenty of individuals who choose to do their own income taxes with the help of software technology (i.e., Intuit), or those who forego hiring an estate planning attorney by using off-the-shelf legal documents (i.e., Legal Zoom). Many industries in our economy inherently have penny pinching DIY-ers, but despite current and future inroads made by the robo-advisors, there will always be individuals who do not have the capacity, patience, or interest to search out a DIY investment solution.

After watching the stock market rise for five consecutive years, taming investment portfolios may seem like a simple problem for internet software to solve, but experienced investors (not academics) understand successful long-term investing is never easy…with or without technology. The reality of the situation is that when volatility eventually spikes and we hit an inevitable bear market, these robo-sites will fail miserably in supplying the necessary human element to facilitate more prudent investment decisions.

While the rising robo-advisors may have many investment advisory shortcomings, I will acknowledge some appealing aggregating features that provide a helpful holistic view of an individual’s finances (see Mint). Also, these sites are forcing investors to ask their advisors the important and appropriate tough questions regarding fees, compensation, and conflicts of interest. However, in spite of the short-term, blossoming success of the robo-sites, investing has never been more difficult. Investors continue to get overwhelmed with the 24-7, 365 news cycles that proliferates an endless avalanche of global crises via TV, radio, Twitter, Facebook, and the blogosphere.

While a younger, less-affluent DIY demographic may flock to some of these robo-advisors, the millions of aging and retiring baby boomers ensures there will be plenty of demand for traditional advisors. Experienced independent RIA advisors and financial planners, like Sidoxia, who integrate low-cost ETFs into their investment management practices stand to benefit handsomely. Those advisors/sites offering simplistic, commoditized ETF offerings with no wealth planning services will be challenged. While I may not lose sleep over the rise of the robo-advisors, I will continue to dream of a robot that will lower my taxes and win me the lottery.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (including Vanguard ETFs), AAPL, but at the time of publishing SCM had no direct position in HD, TWTR, FB, Legal Zoom, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Buy in May and Tap Dance Away

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (May 1, 2014). Subscribe on the right side of the page for the complete text.

The proverbial Wall Street adage that urges investors to “Sell in May, and go away” in order to avoid a seasonally volatile period from May to October has driven speculative trading strategies for generations. The basic premise behind the plan revolves around the idea that people have better things to do during the spring and summer months, so they sell stocks. Once the weather cools off, the thought process reverses as investors renew their interest in stocks during November. If investing was as easy as selling stocks on May 1 st and then buying them back on November 1st, then we could all caravan in yachts to our private islands while drinking from umbrella-filled coconut drinks. Regrettably, successful investing is not that simple and following naïve strategies like these generally don’t work over the long-run.

Even if you believe in market timing and seasonal investing (see Getting Off the Market Timing Treadmill ), the prohibitive transaction costs and tax implications often strip away any potential statistical advantage.

Unfortunately for the bears, who often react to this type of voodoo investing, betting against the stock market from May – October during the last two years has been a money-losing strategy. Rather than going away, investors have been better served to “Buy in May, and tap dance away.” More specifically, the S&P 500 index has increased in each of the last two years, including a +10% surge during the May-October period last year.

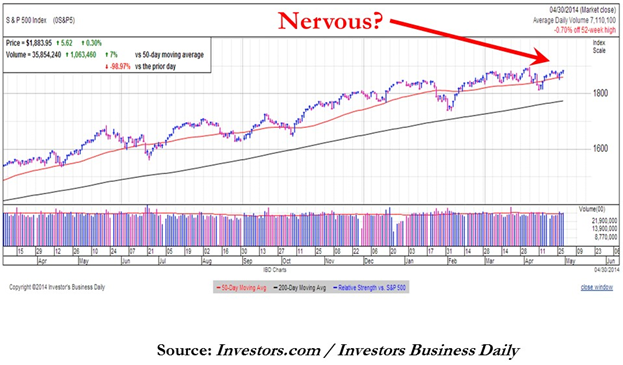

Nervous? Why Invest Now?

With the weak recent economic GDP figures and stock prices off by less than 1% from their all-time record highs, why in the world would investors consider investing now? Well, for starters, one must ask themselves, “What options do I have for my savings…cash?” Cash has been and will continue to be a poor place to hoard funds, especially when interest rates are near historic lows and inflation is eating away the value of your nest-egg like a hungry sumo wrestler. Anyone who has completed their income taxes last month knows how pathetic bank rates have been, and if you have pumped gas recently, you can appreciate the gnawing impact of escalating gasoline prices.

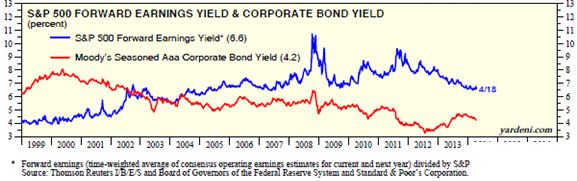

While there are selective opportunities to garner attractive yields in the bond market, as exploited in Sidoxia Fusion strategies, strategist and economist Dr. Ed Yardeni points out that equities have approximately +50% higher yields than corporate bonds. As you can see from the chart below, stocks (blue line) are yielding profits of about +6.6% vs +4.2% for corporate bonds (red line). In other words, for every $100 invested in stocks, companies are earning $6.60 in profits on average, which are then either paid out to investors as growing dividends and/or reinvested back into their companies for future growth.

Source: Dr. Ed’s Blog

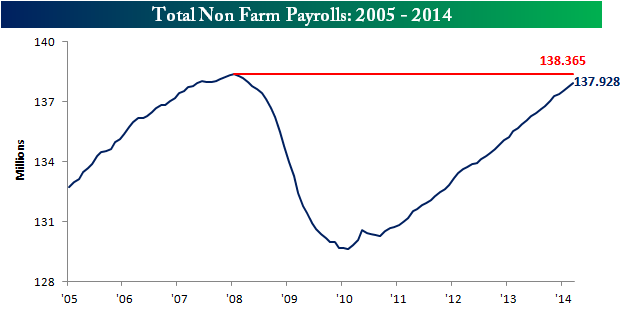

Hefty profit streams have resulted in healthy corporate balance sheets, which have served as ammunition for the improving jobs picture. At best, the economic recovery has moved from a snail’s pace to a tortoise’s pace, but nevertheless, the unemployment rate has returned to a more respectable 6.7% rate. The mended economy has virtually recovered all of the approximately 9 million private jobs lost during the financial crisis (see chart below) and expectations for Friday’s jobs report is for another +220,000 jobs added during the month of April.

Source: Bespoke

Wondrous Wing Woman

Investing can be scary for some individuals, but having an accommodative Fed Chair like Janet Yellen on your side makes the challenge more manageable. As I’ve pointed out in the past (with the help of Scott Grannis), the Fed’s stimulative ‘Quantitative Easing’ program counter intuitively raised interest rates during its implementation. What’s more, Yellen’s spearheading of the unprecedented $40 billion bond buying reduction program (a.k.a., ‘Taper’) has unexpectedly led to declining interest rates in recent months. If all goes well, Yellen will have completed the $85 billion monthly tapering by the end of this year, assuming the economy continues to expand.

In the meantime, investors and the broader financial markets have begun to digest the unwinding of the largest, most unprecedented monetary intervention in financial history. How can we tell this is the case? CEO confidence has improved to the point that $1 trillion of deals have been announced this year, including offers by Pfizer Inc. – PFE ($100 billion), Facebook Inc. – FB ($19 billion), and Comcast Corp. – CMCSA ($45 billion).

Source: Entrepreneur

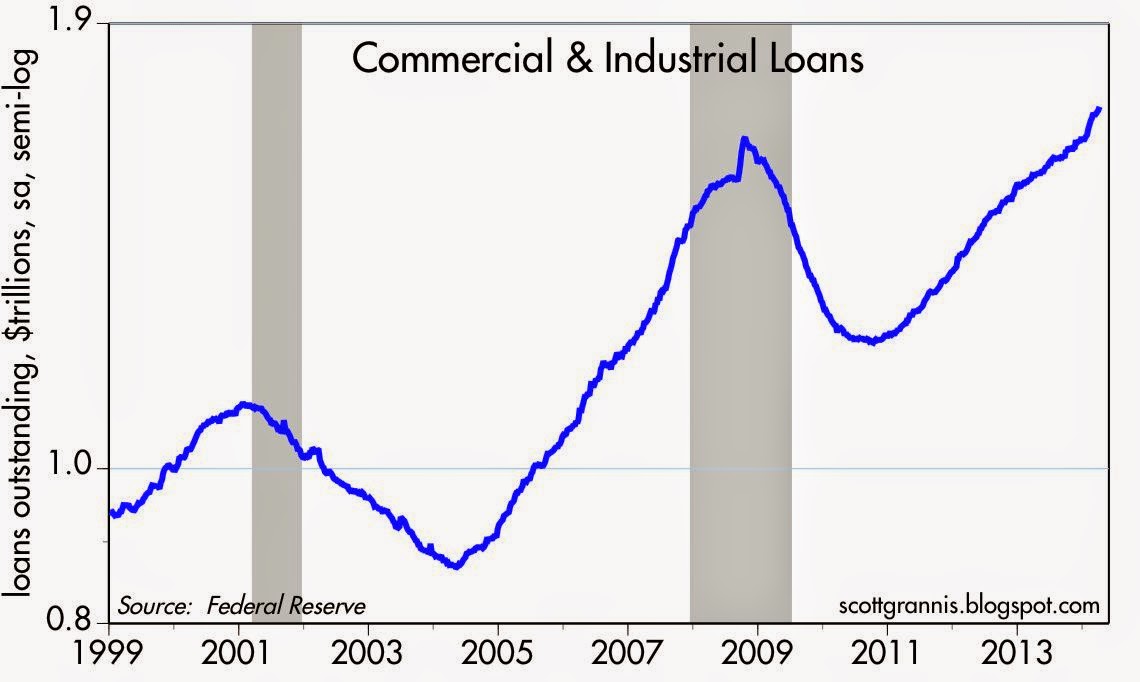

Banks are feeling more confident too, and this is evident by the acceleration seen in bank loans. After the financial crisis, gun-shy bank CEOs fortified their balance sheets, but with five years of economic expansion under their belts, the banks are beginning to loosen their loan purse strings further (see chart below).

The coast is never completely clear. As always, there are plenty of things to worry about. If it’s not Ukraine, it can be slowing growth in China, mid-term elections in the fall, and/or rising tensions in the Middle East. However, for the vast majority of investors, relying on calendar adages (i.e., selling in May) is a complete waste of time. You will be much better off investing in attractively priced, long-term opportunities, and then tap dance your way to financial prosperity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in PFE, CMCSA, and certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in FB or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Getting & Staying Rich 101

Fred J. Young worked 27 years as a professional money manager and investment counselor in the trust department at Harris Bank in Chicago. While working there he learned a few things about wealth accumulation and preservation, which he outlines in his book How to Get Rich and Stay Rich.

There is more than one way to skin a cat, and when it comes to getting rich, Young describes the only three ways of getting loaded:

1.) Inherit It: Using this method on the path to richness generally doesn’t take a lot of blood, sweat, and tears (perhaps a little brown-nosing wouldn’t hurt), but young freely admits you can skip his book if you are fortunate enough to garner boatloads of cash through your ancestry.

2.) Marry It: This approach to wealth accumulation can require a bit more effort than method number one. However, Young explains that if the Good Lord intended you to find your lifetime lover through destiny, then if your soul-mate has a lot of dough Young advises, “You [should] graciously accept the situation. Don’t fight it.”

3.) Spend < Earn: Normally this avenue to champagne and caviar requires the most effort. How does one execute option number three? “You spend less than you earn and invest the difference in something you think will increase in value and make you rich,” simply states Young. Sounds straightforward, but what does one invest their excess cash in? Young succinctly lists the customary investment tools of choice for wealth creation:

- Real estate

- Own their own business

- Common stocks

- Savings accounts (thanks to the magic of compound interest rates) – see also Penny Saved is Billions Earned

Rich Luck

If faced with choosing between good luck and good judgment, here is Fred Young’s response:

“You should take good luck. Good luck, by definition, denotes success. Good judgment can still go wrong.”

Like many endeavors, it’s good to have some of both (good luck and good judgment).

The Role of Courage

Courage is especially important when it comes to equity investing because buying stocks includes a very counterintuitive behavioral aspect that requires courage. Following the herd of average investors and buying stocks at new highs is easy and does not require a lot of courage. Young describes the various types of courage required for successful investing:

“The courage to buy when others are selling; the courage to buy when stocks are hitting new lows; the courage to buy when the economy looks bad; courage to buy at the bottom…The times when the gloom was the thickest invariably turned out to have been the best times to buy stocks.”

Keeping the Cash

Becoming rich is only half the challenge. In many cases staying rich can be just as difficult as accumulating the wealth. Young points out the intolerable pain caused by transitioning from wealth to poverty. What is Young’s solution to this tricky problem? Seek professional help. The risks undertaken to build wealth still exist when you are rich, and those same risks have the capability of tearing financial security away.

There are three paths to riches according to Fred Young (inheritance, marriage, and prudent investing). Some of these directions leading to mega-money require more effort than others, but if you are lucky enough to have deep pockets of riches, make sure you have the discipline and focus necessary to maintain that wealth – those deep pockets could have a hole.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investor Wake-Up Call

Source: Photobucket

The Pre Wake-Up Conversation

“Hey Milfred, did you see our brokerage statement? There must be a misprint. It says our portfolio of bonds is down.”

“Buford, how can that be, when our bond portfolio has been up for 30 consecutive years? I hear Jim Bernanke is trying to artificially inflate the economy by printing money and using it to buy bonds.”

![]() “Sweetheart, you got it wrong…it’s Ben Jernanke.”

“Sweetheart, you got it wrong…it’s Ben Jernanke.”

![]() “Ohhh, yeah honey, you’re right. I never expected prices to go down after government bond yields were up almost 50% in a few months.”

“Ohhh, yeah honey, you’re right. I never expected prices to go down after government bond yields were up almost 50% in a few months.”

![]() “Sweetie, maybe we should give our broker a call?”

“Sweetie, maybe we should give our broker a call?”

![]() “Oh you mean Skip? I think he wants us to call him a financial consultant or financial advisor now…not a broker.”

“Oh you mean Skip? I think he wants us to call him a financial consultant or financial advisor now…not a broker.”

![]() “Well anyway, I just read the largest fund manager in the world, Bill Gross, is trying to convert his bond fund into a stock fund (read article). I can’t imagine why Mr. Gross would want to do that (see PIMCO article), but maybe Skip knows? You know, after Skip sold us that high commission annuity and Class-A mutual fund with that 6.25% load, he decided to take his wife, kids, parents, and in-laws to Tahiti for the holidays.”

“Well anyway, I just read the largest fund manager in the world, Bill Gross, is trying to convert his bond fund into a stock fund (read article). I can’t imagine why Mr. Gross would want to do that (see PIMCO article), but maybe Skip knows? You know, after Skip sold us that high commission annuity and Class-A mutual fund with that 6.25% load, he decided to take his wife, kids, parents, and in-laws to Tahiti for the holidays.”

![]() “Oh I know, Skip is such a nice young man, and so thoughtful.”

“Oh I know, Skip is such a nice young man, and so thoughtful.”

![]() “You’re right Pumpkin, I just wish we could hear from him more than once every two years.”

“You’re right Pumpkin, I just wish we could hear from him more than once every two years.”

![]() “That’s right Snookum, but at least we get to talk to him when he drops off the paperwork, and his secretary is sure nice.”

“That’s right Snookum, but at least we get to talk to him when he drops off the paperwork, and his secretary is sure nice.”

![]() “What I really like about Skip is that he always makes so much common sense – he always tells us to buy investments that have already done really well like bonds and gold.”

“What I really like about Skip is that he always makes so much common sense – he always tells us to buy investments that have already done really well like bonds and gold.”

![]() “Exactly Buford. I just wonder how much longer it will take for stocks to become popular again, given the stock market is already up about 100% from the beginning of 2009? Perhaps with another +30% or so, maybe Skip will switch all our money out of bonds back into stocks?”

“Exactly Buford. I just wonder how much longer it will take for stocks to become popular again, given the stock market is already up about 100% from the beginning of 2009? Perhaps with another +30% or so, maybe Skip will switch all our money out of bonds back into stocks?”

![]() “What I love even more about Skip is that not only does he have us buy the popular investments, but he really protects us from buying the low-priced investments that are selling at bargain prices.”

“What I love even more about Skip is that not only does he have us buy the popular investments, but he really protects us from buying the low-priced investments that are selling at bargain prices.”

![]() “I hear you Muffin – come to think of it, maybe I should return that sweater I recently purchased at Marshall’s for 50% off – there may be an awful reason I do not know about.”

“I hear you Muffin – come to think of it, maybe I should return that sweater I recently purchased at Marshall’s for 50% off – there may be an awful reason I do not know about.”

![]() “Good idea Sweet Pea. The other thing I love about Skip is that he is so knowledgeable…he says the exact same thing I hear from those smart news people on TV. Good thing we have a reliable professional to protect our entire life savings.”

“Good idea Sweet Pea. The other thing I love about Skip is that he is so knowledgeable…he says the exact same thing I hear from those smart news people on TV. Good thing we have a reliable professional to protect our entire life savings.”

![]() “You’re right as usual dear. He may only have a high school GED, but we’re lucky he has these fancy letters behind his name that I never heard of like PFS, AFC, and RFC… those must be some important credentials.”

“You’re right as usual dear. He may only have a high school GED, but we’re lucky he has these fancy letters behind his name that I never heard of like PFS, AFC, and RFC… those must be some important credentials.”

![]() “I feel better after our conversation. Maybe we’ll hear from Skip, and if not, I’m sure he’ll drop-off some paperwork for a new investment, if our portfolio goes down by another 10%.”

“I feel better after our conversation. Maybe we’ll hear from Skip, and if not, I’m sure he’ll drop-off some paperwork for a new investment, if our portfolio goes down by another 10%.”

The Wake-Up Reality

I make some of these comments with tongue firmly in cheek, but the fact remains we live in a financial world with a structurally flawed system of loosely regulated, banks, brokerage firms, insurance companies, ratings agencies, hedge funds, mutual funds, and other financial institutions that continue to repeatedly place their interests ahead of clients. If the 2008-2009 financial crisis hasn’t taught you anything, then you should realize it behooves you to take control of your financial situation. At least ask tough questions that result in answers you can understand – not a lot of technical mumbo-jumbo that makes an advisor sound smart. Make life easier on yourself and have a blunt wake-up call conversation, otherwise grab a pen and get ready for Skip’s call – he’s about to come over with some more paperwork.

Related articles:

Beating off the Financial Sharks

Fees, Exploitation and Confusion Hammer Investors

Investment Credentials: The Letter Shell Game

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in TJX, or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

WEBINAR: 10 Ways to Protect & Grow Your Nest Egg

If analyzing quarterly reports, managing a hedge fund/client accounts, teaching a course, writing a second book, and squeezing in a vacation is not enough, then why not try to squeeze in a webinar too? That’s exactly what I decided to do, so please join us on Friday (7/23 @ 12:30 p.m. PST) to learn about the critical 10 Ways to Protect and Grow Your Nest Egg in Uncertain Times.

Webinar Details:

—July 23, 2010 (Friday) at 12:30 p.m. – 1:30 p.m. (Pacific Standard Time)

CLICK HERE TO CONNECT TO WEBINAR

Toll Free # (if not using PC): 1-877-669-3239

Access Code: 800 505 230

Managing your investments has never been more difficult in this volatile and uncertain world we live in. With life expectancies increasing, and ambiguity surrounding the reliability of future financial safety nets (Social Security & Medicare), prudently investing your hard earned money to protect and grow your nest egg has never been this critical.

Invest in yourself and block off some time at 12:30 p.m. PST on July 23rd to educate yourself on the “10 Ways to Protect and Grow Your Nest Egg” in a relaxed webinar setting in front of your own computer.

CLICK HERE TO CONNECT TO WEBINAR

Toll Free # (if not using PC): 1-877-669-3239

Access Code 800 505 230

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Hidden Train Wreck – Professional Athlete Portfolios

Need capital for a floating furniture venture? How about an oxygen absorbing skin procedure? Well, if you are having any difficulty, just call an NFL, NBA, or MLB rookie. Even wealthy professional athletes have been impacted by the financial crisis, not to mention the aggressive sales tactics of the investment industry and the players’ poor money management skills. Many players are too busy concentrating on winning games, while their portfolios are suffering losses. The statistics are staggering. Here are the findings, according to an article published in Sports Illustrated earlier this year:

- “By the time they have been retired for two years, 78% of former NFL players have gone bankrupt or are under financial stress because of joblessness or divorce.”

- “Within five years of retirement, an estimated 60% of former NBA players are broke.”

- The divorce rate for pro athletes ranges from 60% to 80%, based on estimates from athletes and agents.

- “According to the NFL Players Association, at least 78 players lost a total of more than $42 million between 1999 and 2002 because they trusted money to financial advisers with questionable backgrounds.”

These are not old, dementia-suffering widows living in Florida we are talking about, but rather professional athletes, many of which made multi-million fortunes during their playing careers. The article goes out of its way to demonstrate this is not a fringe issue affecting a minority of professional athletes. Numerous examples were provided, including the following:

- Ten current and former Major League Baseball players, including outfielder Jonny Damon of the New York Yankees, had some of their money tied up in the alleged $8 billion fraud perpetrated by Robert Allen Stanford.

- Raghib (Rocket) Ismail lost a fortune by investing in excessively risky ventures, including a movie about music label COZ Records; a cosmetics procedure company; a nationwide phone-card dispensing venture; and a framed calligraphy company opened in New Orleans two months before Hurricane Katrina hit.

- Drew Bledsoe, Rick Mirer and five other NFL retirees each invested a minimum of $100,000 in a failed start-up, which touted “biometric authentication” technology that potentially could replace credit cards with fingerprints. The players eventually sued UBS (the financial-services firm) for allegedly withholding information about the company founder’s criminal history and drug use.

- Torii Hunter, outfielder for the Los Angeles, invested almost $70,000 in living-room furniture that included inflatable rafts – perfect for those consumers living in flood zones. Suffice it to say, the results did not meet initial expectations.

- In addition to his legal problems, NFL quarterback Michael Vick filed for Chapter 11 bankruptcy last year partly because he could not repay about $6 million in bank loans that he directed toward a car-rental franchise in Indiana, wine shop in Georgia and real estate in Canada.

- Retired NBA forward Vin Baker’s seafood restaurant in Old Saybrook, Connecticut, was foreclosed on in February 2008 due to nearly $900,000 in unpaid loans.

- “NBA guard Kenny Anderson filed for bankruptcy in October 2005. He detailed how the estimated $60 million he earned in the league had dwindled to nothing. He bought eight cars and rang up monthly expenses of $41,000, including outlays for child support, his mother’s mortgage and his own five-bedroom house in Beverly Hills, Calif.—not to mention $10,000 in what he dubbed “hanging-out money.” He also regularly handed out $3,000 to $5,000 to friends and relatives.”

- “Former NBA forward Shawn Kemp (who has at least seven children by six women) and, more recently, Travis Henry (nine by nine) have seen their fortunes sapped by monthly child-support payments in the tens of thousands of dollars.”

Besides irresponsible spending, and greedy advisors, contributing factors to all the losses are the “boring” and “unintelligible” nature of securities investments. Professional athletes like to flaunt investments like night clubs and car dealerships – there is a “thrill of tangibility,” according to SI writer Pablo Torre.

Professional athletes are not the only ones suffering losses. Ordinary investors have lost also and are learning it’s not what you make – rather it’s what you preserve and grow. The majority of the athletes do not realize their peak earnings years cover a very brief period, and therefore need to be more prudent with their money management since the windfall moneys must be spread over many years.

Trust is an important but difficult trait to find for many of these athletes since many opportunistic friends, acquaintances, and family members in many cases put their self interests ahead of the professional athlete’s needs. There is no simple formula for intelligent money management, however there are ways for athletes to protect their financial blind spots:

1) Educate Themselves. Learn the basics of what you are investing in. You may not learn the ins and outs but you can get a basic understanding of the expected return and volatility of your investments. Athletes often forget about diversification as well, “Chronic over-allocation into real estate and bad private equity is the number one problem [for athletes] in terms of a financial meltdown,” Ed Butowsky of Chapwood Investments says.

2) Trust But Verify. Ronald Reagan famously made those statements decades ago and the principle applies to money too. Many athletes pay tens of thousands of dollars for investment advice, so asking questions is advisable. Specifically, ask how performance is trending versus comparable benchmarks and get a view over multiple time periods.

3) Avoid Friends and Family. If possible, separating business from friends and family is a wise idea. When emotions mix with money, harmful decisions can damage the athlete’s financial future.

4) Determine Fees & Commissions. When investing hundreds of thousands, if not millions of dollars, fees and commissions can be substantial; therefore it is imperative for the athletes to know what they are paying their advisors.

5) Experience Matters. Check out the background of your advisor and determine the licenses and credentials they hold. If you were flying a plane in a heavy storm, you would want an experienced pilot flying the plane, not a flight attendant.

6) Budget. Establish an investment plan with a sustainable lifestyle that accounts for inflation. As veteran agent Bill Duffy says, whose clients include Suns guard Steve Nash and Nuggets forward Carmelo Anthony, “A pro athlete’s money is supposed to outlive his career. Most players never get that.”

Athletes spend their whole lives trying to make the professional ranks in order to earn the big bucks. Due to their high profile status, financial advisors and trusted individuals prey on the sports figures’ wealth. Unfortunately a majority of the athletes lack the money management skills and discipline to preserve and grow their earned wealth. Perhaps repeatedly shining a light on the dirty under-belly of this tragic problem will prevent future financial train wrecks from occurring. Until then, I guess we’ll just have to sift though the bankrupt remains of inflatable sofa raft companies and liquidation proceeds from failed night clubs.

Read the Complete Sports Illustrated Article Here

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

{kind=link}