Posts tagged ‘financial crisis’

Turn Off TV – Emperor Media Has No Clothes!

Famous Danish author Hans Christian Andersen told a renowned fairy tale of an emperor who was conned into believing he is wearing an invisible suit. The crowd was too embarrassed to acknowledge his nakedness, so they pretend to not notice – until a young boy shouted, “The emperor has no clothes!”

Much like the fairy tale, when it comes to pointing out the many shortcomings of the financial media, I have no problem yelling, “The Emperor Media has no clothes!”

Media Spreads Fear and Misinformation

Mark Twain famously stated, “If you don’t read the newspaper, you’re uninformed. If you read the newspaper, you’re misinformed.” That sentiment rings especially true amid today’s swirl of alarming headlines. Here’s a sampling of recent media-induced worries:

- Global trade war caused by tariffs

- Declining value of the U.S. dollar

- Rising interest rates due to foreign debt sales

- Doubts over the U.S. dollar’s global reserve currency status

- Recession anxiety

- Stagflation fears

- Concerns about Executive Branch overreach

- Threats to remove the Federal Reserve Chairman

Is the sky falling? Is now the time to sell stocks, as the media often implies? Or are these risks being overstated and distorted by media outlets that chase monetary gains?

Issues are More Gray Than Black or White

Journalists – most of whom have little investing experience – like to authoritatively paint economic issues in black-or-white terms. But most reasonable people understand that these matters are complex, and the truth lies somewhere in the gray. To claim the media offers a balanced view of both the positives and negatives of complicated financial topics would be disingenuous.

I have been investing for over 30 years, and while I’ve never faced a global rebalancing of trade impacting trillions in economic activity, I’ve lived through far more uncertain times. Not only have my investments survived those volatile periods, but they have also thrived – repeatedly hitting new record highs.

F.U.D. Sells!

Does the media want you to believe the accurate, long-term stock market prosperity story? Hardly. As the saying goes, “If it bleeds, it leads.” Fear, uncertainty, and doubt (F.U.D.) sell more ads, subscriptions, newspapers, and magazines. The more blood, sweat, and anxiety in the headlines, the more money the media makes from distressed readers.

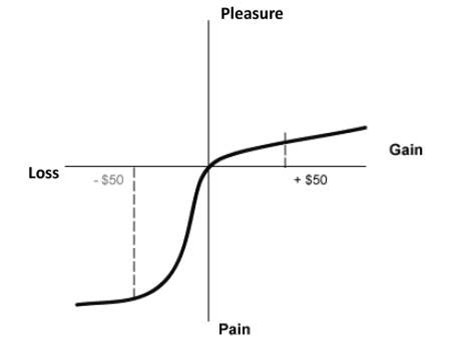

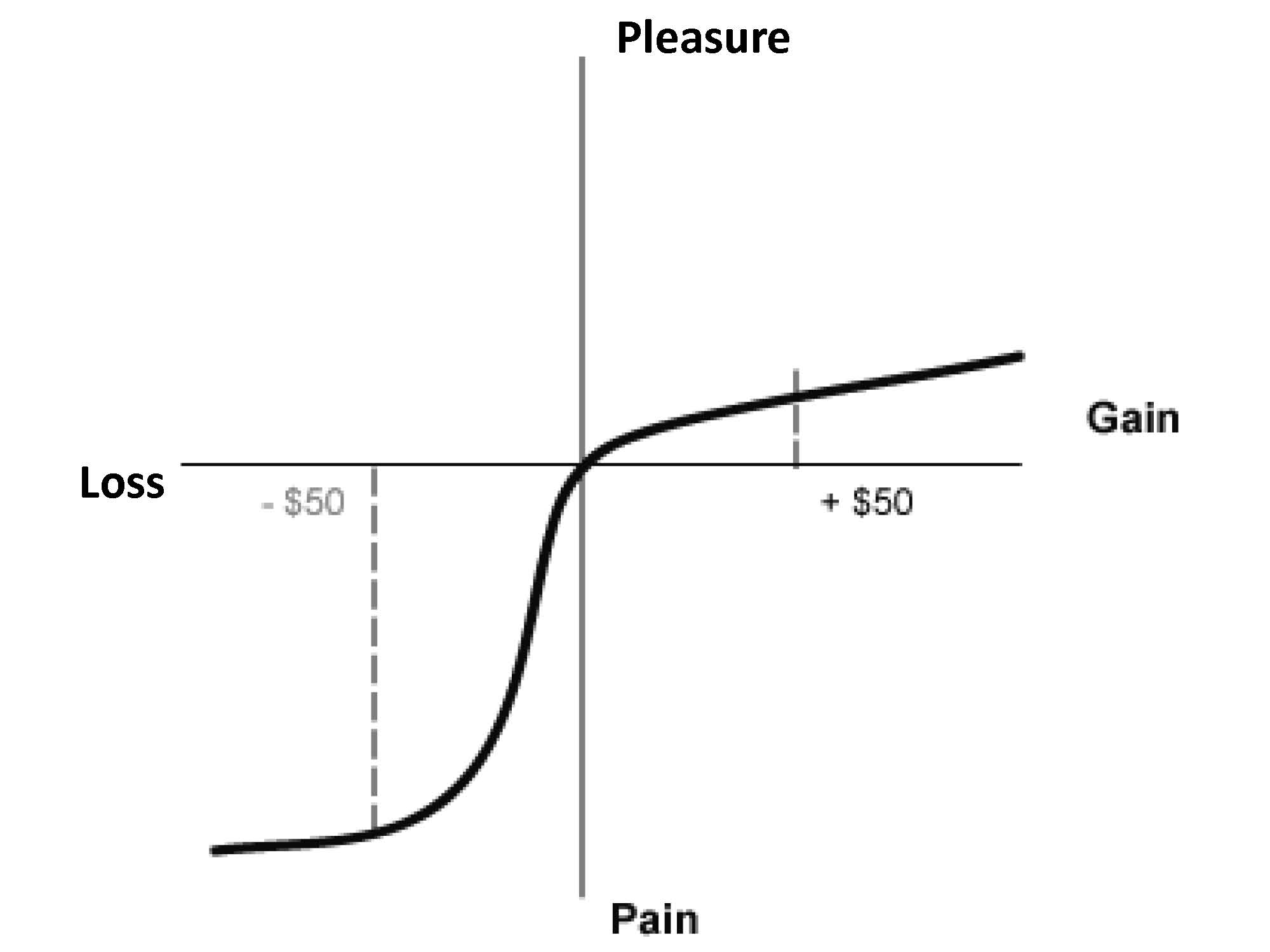

Behavioral finance pioneers, Nobel Prize winner Daniel Kahneman and Amos Tversky, showed that losses feel twice as painful as the pleasure of gains (see the Pleasure/Pain diagram below). Their Prospect Theory remains just as relevant today as when it was introduced in the late 1970s.

The greatest investor of all-time, Warren Buffett, once said, “Be fearful when others are greedy, and greedy when others are fearful.” Unfortunately, the media pushes the opposite mantra: “sell fear and buy greed.” When markets fall, they sell Armageddon. When markets soar, they sell nirvana. During periods of over-optimism, they also exploit FOMO (Fear of Missing Out) by feasting on investors’ emotional cycle of excitement.

Reassuring long-term investors that everything will be okay—or that dips are buying opportunities—doesn’t generate as much media profits and ad sales. Fear does.

History Doesn’t Repeat Itself, But It Often Rhymes

Too many investors suffer from short-term thinking and goldfish-like memory. But as Mark Twain wisely stated, “History doesn’t repeat itself, but It often rhymes.” And history has shown that listening to the media during times of extreme market volatility often leads to poor decisions.

Let’s take a look at some key examples where media-driven fear was more misleading than helpful over the decades:

The Nifty Fifty Collapse (1973-1974)

In the early 1970s, long before the “Magnificent 7” stocks came to the fore, we had the “Nifty Fifty” stocks. These large-cap blue chip stocks traded at lofty P/E (Price-Earnings) ratios and were seen as invincible before they came crashing down in 1973-1974. Suffice it to say, the media headlines were horrific during this period.

Here is some context for this period:

- The U.S. was exiting the Vietnam War

- Economy was undergoing a major recession

- Watergate scandal and presidential resignation

- 9% unemployment

- The Arab Oil Embargo

- Surging inflation

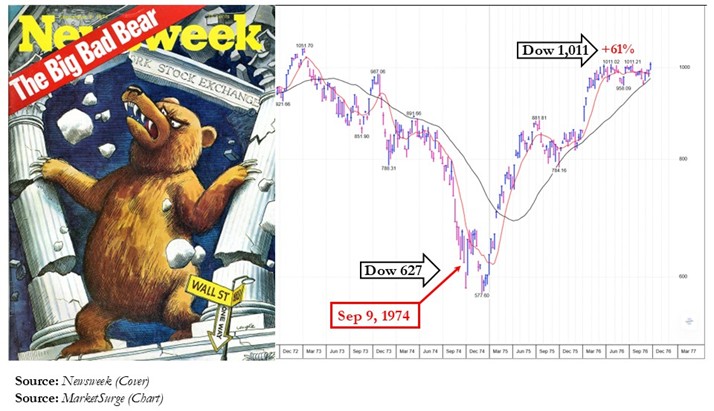

The media’s response? Doom and gloom. Here’s an example of this sentiment from the Newsweek cover, “The Big Bad Bear,” published on September 9, 1974.

For those who sold in fear, the results were disastrous. The Dow bottomed shortly after the magazine was released and the market rebounded +61% in less than two years. Panic was the wrong move.

“The Death of Equities” (1979)

Inflation plagued the 1970s, and just before one of the longest bull markets in history, BusinessWeek declared “The Death of Equities” on its now-infamous September 1979 cover. Once again, the media acted as a perfect contrarian indicator with the Dow quadrupling over the next decade.

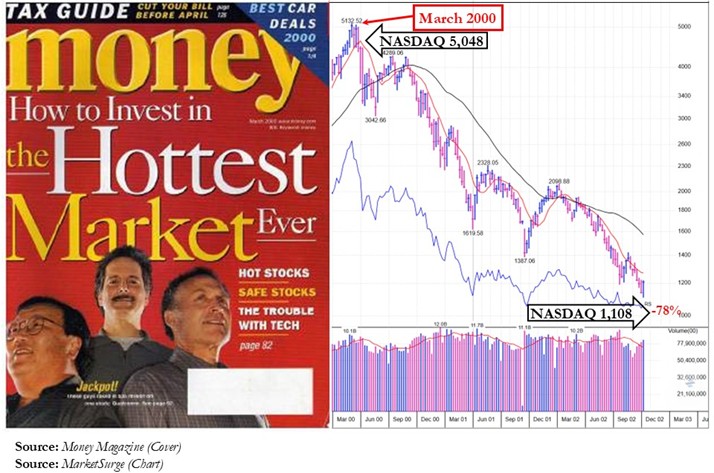

Dot-Com Bubble: “The Hottest Market Ever” (2000)

In March 2000, at the peak of the tech bubble, Money magazine ran a cover story: “How to Invest in the Hottest Market Ever.” Weeks later, the bubble burst. Suboptimal timing once again.

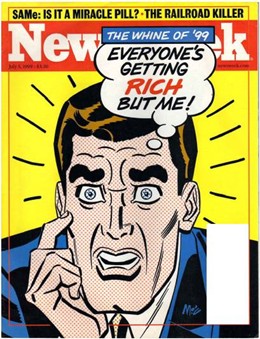

In that same timeframe, Newsweek captured the essence of FOMO with its July 5, 1999 cover: “Everyone Is Getting Rich but Me.” Right when risk was at its peak, most investors were blind to it and got sucked into the downdraft.

Source: NewsWeek

Financial Crisis – Depression 2.0 (2008)

In October 2008, the Time magazine cover encapsulated the zeitgeist of the period with a 1929 photo that included a line of desperate people waiting for food donations at a soup kitchen. Many feared a second Great Depression. Yet it was one of the best times in history to buy stocks with the Dow tripling over the next decade.

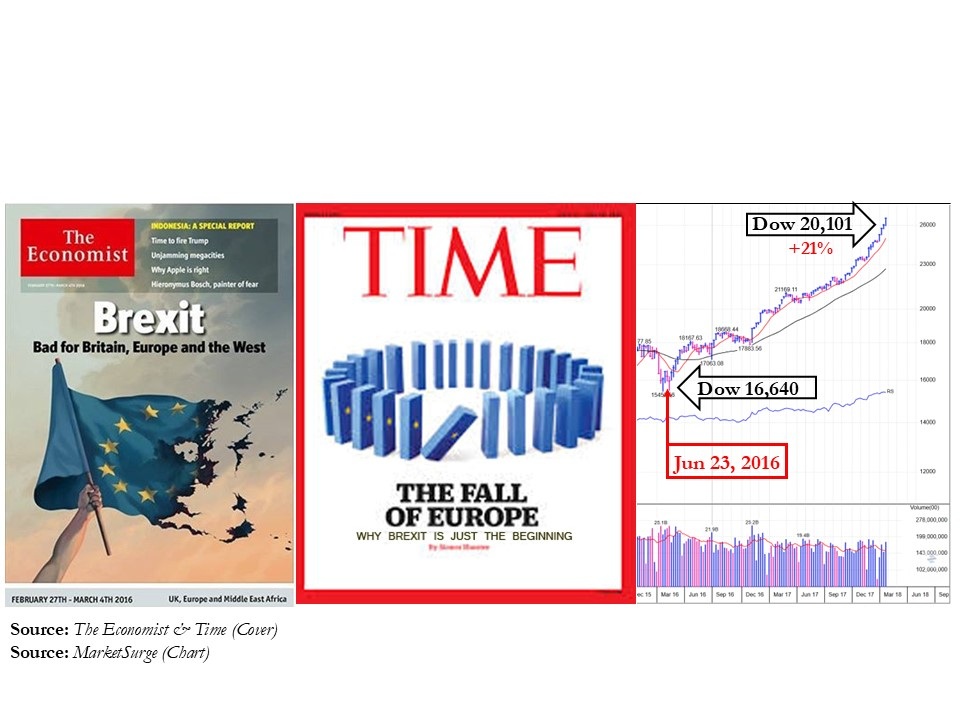

Brexit Panic (2016)

Media coverage around the U.K.’s Brexit vote to leave the EU (European Union) painted a picture of imminent recession and contagion. Instead, the media blitz surrounding Brexit turned out to be more molehill than mountain. Markets rebounded strongly and reached new highs in the subsequent months.

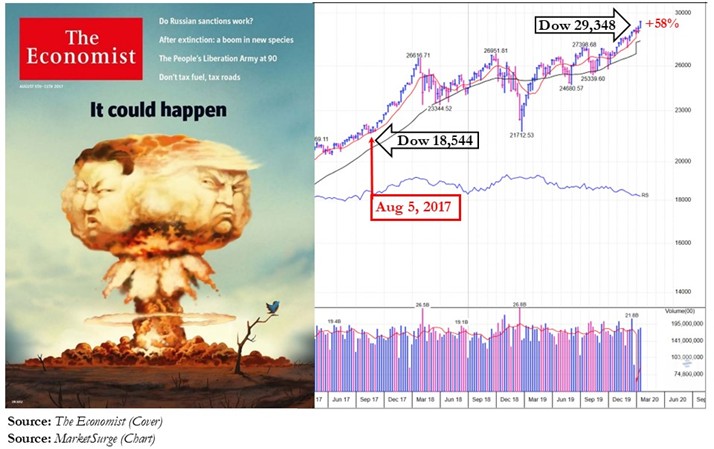

“Rocketman” and North Korea Missiles (2017)

Tensions flared in 2017 as North Korea tested missiles and President Trump threatened retaliation against dictator Kim Jong Un by bombing Pyongyang and “Rocket Man”. The media went into overdrive regarding the nuclear unease, but the market brushed it off and continued climbing +58% over the next few years.

COVID-19 Pandemic (2020)

With over 3 million deaths worldwide and a grinding halt to the global economy, markets initially fell roughly -35%. But as consumers stockpiled toilet paper, fast vaccine development and stimulus sparked a powerful rebound, with stocks finishing the year up +16%. Over the next two years, the Dow almost doubled.

Hostage to Our Lizard Brain

Why are we so susceptible to the sensationalist tendencies of the media? Evolution holds the answer. Humans’ DNA and brains are hard-wired to flee prey. The small almond-shaped tissue in our brain called the amygdala—or what author Seth Godin calls the “lizard brain”—evolved to respond instantly to danger. When headlines scream “crash” or “war,” our emotional brain overrides our logical one, which leads to poor long-term results. As Seth Godin explains, we’re wired to react, not reflect (Watch here). And the media knows it.

Headlines Change but the Long-Term Market Trend Doesn’t

Despite a barrage of negative headlines, stocks have remained resilient over the long run. The market has overcome wars, assassinations, currency crises, banking failures, terrorist attacks, pandemics, natural disasters, impeachments, tax hikes, recessions, restrictive Fed policies, debt downgrades, inflation, and yes, even tariffs (see chart below). Since WWII, we’ve had 12 recessions—each followed by a full recovery to new record highs. In baseball terms, the economy has batted a perfect 1.000 (12-for-12) with recession recoveries.

How to Survive the Avalanche of Media Headlines

Here are five key strategies:

- Turn off the TV: Don’t obsess over headlines. Emotional reactions result in poor decisions.

Buying high (greed) and selling low (fear) is not a recipe for long-term investment success.

- Diversify Your Investments: A well-balanced portfolio across asset classes helps reduce panic.

- Invest According to Time Horizon: Are you young? Assuming more risk and higher exposure to the stock market is generally fine. Are you near retirement? Don’t jeopardize your retirement goals – de-risk accordingly.

- Ignore Talking Heads: Most pundits don’t invest and their credibility is compromised by monetary conflicts of interest. It’s much more beneficial to follow seasoned professionals with real track records through multiple bull and bear markets.

- Avoid the Herd: Continually following the herd into the most popular investments often leads to underperformance. The grass is greener, and the food sources are more plentiful, off the beaten path trampled by the herd. Contrarian thinking works even though it can feel scary.

In the age of constant connectivity, headlines and the 24/7 news cycle are addictive. But if you’re tired of being a pawn in the media’s game, I invite you to join my fight by acknowledging that the Emperor Media has no clothes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (May 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

The Dirty Little Stock Market Secret

Shhhh…don’t tell anyone, I have a dirty little secret. Are you ready? Are you sure? The world is not going to end…really.

Despite lingering trade concerns (see Trump Hits China with Tariffs on $200 Billion in Goods), Elon Musk being sued by the Securities and Exchange Commission (SEC) for tweeting his controversial intentions to take Tesla Inc. (TSLA) private, and Supreme Court nominee, Brett Kavanaugh, facing scandalous sexual assault allegations when he was in high school, life goes on. In the face of these heated headlines, stocks still managed to rise to another record in September (see Another Month, Another Record). For the month, the Dow Jones Industrial Average climbed +1.9% (+7.0% for 2018), the S&P 500 notched a +0.4% gain (+9.0% for 2018), while the hot, tech-laden NASDAQ index cooled modestly by -0.8% after a scorching +17.5% gain for the year.

If the world were indeed in the process of ending and we were looking down into the abyss of another severe recession, we most likely would not see the following tangible and objective facts occurring in our economy.

- New Revamped NAFTA (North American Free Trade Agreement) 2.0 trade deal between the U.S., Mexico, and Canada was finalized (new deal is called United States-Mexico-Canada Agreement).

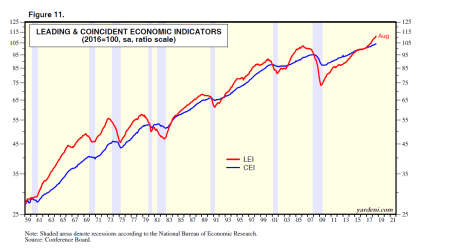

- Leading Economic Indicators are at a record high (a predictive statistic that historically falls before recessionary periods – in gray)

Source: Yardeni.com

- Unemployment Rate of 3.9% is near a record low

- Small Business Optimism is near record highs

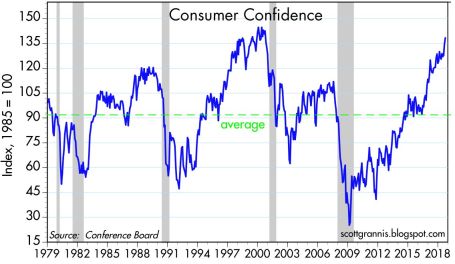

- Consumer Confidence is near record highs

Source: Scott Grannis

- Corporate Profits are at record highs

- Interest Rates remain at historically low levels despite the Federal Reserve’s actions to slowly migrate their interest rate target higher

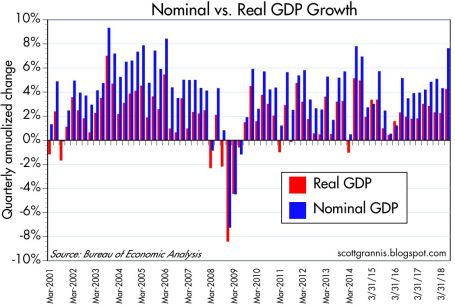

- Economic Growth (GDP) accelerating to +4.2% growth rate in the recent quarter

Source: Scott Grannis

Are we closer to a recession with the stock market potentially falling 20-30% in value? As I have written on numerous occasions, so-called pundits have been falsely forecasting recessions over the last decade, for as long as this bull market has been alive (see Professional Double-Dip Guesses are “Probably” Wrong).

Why so much investor angst as stock prices continue to chug along to record levels? One reason is investors are used to historically experiencing a recession approximately twice a decade on average, and we have yet to suffer one since the Great Recession around 10 years ago. While the mantra “we are due” for a recession might be a true statement, the fact also remains that this economic recovery has been the slowest since World War II, which logically could argue for a longer expansionary period.

What also holds true is that corporate profits already experienced a significant “profit recession” during this economic cycle, post the 2008-2009 financial crisis. More specifically, S&P 500 operating profits declined for seven consecutive quarters from December 2014 through June 2016. The largest contributors to the 2014-2016 profit recession were collapsing oil and commodity prices, coupled with a rapid appreciation in the value of the U.S. dollar, which made our exports more expensive and squeezed multinational corporation profits. The stock market eventually digested these profit-crimping headwinds and resumed its ascent to record levels, but not before the S&P 500 remained flat to down for about a year and a half (2014-2016).

Doom-and-gloom, in conjunction with toxic politics, continue to reign supreme over the airwaves. If you want in on a beneficial dirty little secret, you and your investments would be best served by ignoring all of the media noise and realizing the world is not going to end any time soon.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in TSLA or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Scary Blip

I hated it when my mom reminded me when I was a younger, but now that I’ve survived into middle-aged adulthood, I will give you the same medicine she gave me:

“I told you so.”

As I cautioned in last month’s newsletter, “It’s important for investors to remember this pace of gains cannot be sustainable forever.” I added that there were a whole bunch of scenarios for stock prices to go down or “stock prices could simply go down due to profit-taking.”

And that is exactly what we saw. From the peak achieved in late January, stock prices quickly dropped by -12% at the low in early February, with little-to-no explanation other than a vague blame-game on rising interest rates – the 2018 yield on the 10-Year Treasury Note rose from 2.4% to 2.9%. This explanation holds little water if you take into account interest rates on the 10-Year increased from roughly 1.5% to 3.0% in 2013 (“Taper Tantrum”), yet stock prices still rose +20%. The good news, at least for now, is the stock correction has been contained or mitigated. A significant chunk of the latest double-digit loss has been recovered, resulting in stock prices declining by a more manageable -3.9% for the month. Despite the monthly loss, the subsequent rebound in late February has still left investors with a gain of 1.5% for 2018. Not too shabby, especially considering this modest return comes on the heels of a heroic +19.4% gain in 2017.

As you can see at from the 22-year stock market chart below for the S&P 500, the brief but painful drop was merely a scary blip in the long-term scheme of things.

Whenever the market drops significantly over a short period of time, as it did this month, conspiracy theories usually come out of the woodwork in an attempt to explain the unexplainable. When human behavior is involved, rationalizing a true root cause can be very challenging, to say the least. It is certainly possible that technical factors contributed to the pace and scale of the recent decline, as has been the case in the past. Currently no smoking gun or fat finger has been discovered, however some pundits are arguing the popular usage of leveraged ETFs (Exchange Traded Funds) has contributed to the accelerated downdraft last month. Leveraged ETFs are special, extra-volatile trading funds that will move at amplified degrees – you can think of them as speculative trading vehicles on steroids. The low-cost nature, diversification benefits, and ability for traders to speculate on market swings and sector movements have led to an explosion in ETF assets to an estimated $4.6 trillion.

Regardless of the cause for the market drop, long-term investors have experienced these types of crashes in the past. Do you remember the 2010 Flash Crash (down -17%) or the October 1987 Crash (-23% one-day drop in the Dow Jones Industrial Average index)? Technology, or the lack thereof (circuit breakers), helped contribute to these past crashes. Since 1987, the networking and trading technologies have definitely become much more sophisticated, but so have the traders and their strategies.

Another risk I highlighted last month, which remains true today, is the potential for the new Federal Reserve chief, Jerome Powell, to institute a too aggressive monetary policy. During his recent testimony and answers to Congress, Powell dismissed the risks of an imminent recession. He blamed past recessions on previous Fed Chairmen who over enthusiastically increased interest rate targets too quickly. Powell’s comments should provide comfort to nervous investors. Regardless of short-term inflation fears, common sense dictates Powell will not want to crater the economy and his legacy by slamming the economic brakes via excessive rate hikes early during his Fed chief tenure.

Tax Cuts = Profit Gains

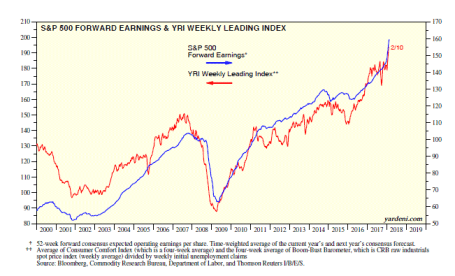

Despite the heightened volatility experienced in February, I remain fairly constructive on the equity investment outlook overall. The recently passed tax legislation (Tax Cuts and Job Act of 2017) has had an undeniably positive impact on corporate profits (see chart below of record profit forecasts – blue line). More specifically, approximately 75% of corporations (S&P 500 companies) have reported better-than-expected results for the past quarter ending December 31st. On an aggregate basis, quarterly profits have also risen an impressive +15% compared to last year. When you marry these stellar earnings results with the latest correction in stock prices, historically this combination of factors has proven to be a positive omen for investors.

Source: Dr. Ed’s Blog

Despite the rosy profit projections and recent economic strength, there is always an endless debate regarding the future direction of the economy and interest rates. This economic cycle is no different. When fundamentals are strong, stories of spiking inflation and overly aggressive interest rate hikes by the Fed rule the media airwaves. On the other hand, when fundamentals deteriorate or slow down, fears of a 2008-2009 financial crisis enter the zeitgeist. The same tug-of-war fundamental debate exists today. The stimulative impacts of tax cuts on corporate profits are undeniable, but investors remain anxious that the negative inflationary side-effects from a potential overheating economy could outweigh the positive economic momentum of a near full-employment economy gaining steam.

Rather than playing Goldilocks with your investment portfolio by trying to figure out whether the short-term stock market is too hot or too cold, you would be better served by focusing on your long-term asset allocation, and low-cost, tax-efficient investment strategy. If you don’t believe me, you should listen to the wealthiest, most successful investor of all-time, Warren Buffett (The Oracle of Omaha), who just published his annual shareholder letter. In his widely followed letter, Buffett stated, “Performance comes, performance goes. Fees never falter.” To emphasize his point, Buffett made a 10-year, $1 million bet for charity with a high-fee hedge fund manager (Protégé Partners). As part of the bet, Buffett claimed an investment in a low-fee S&P 500 index fund would outperform a selection of high-fee, hot-shot hedge fund managers. Unsurprisingly, the low-cost index fund trounced the hedge fund managers. From 2008-2017, Buffett’s index fund averaged +8.5% per year vs. +3.0% for the hedge fund managers.

During scary blips like the one experienced recently, lessons can be learned from successful, long-term billionaire investors like Warren Buffett, but lessons can also be learned from my mother. Do yourself a favor by getting your investment portfolio in order, so my mother won’t have to say, “I told you so.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Head Fakes Surprise as Stocks Hit Highs

In a world of seven billion people and over 200 countries, guess what…there are a plethora of crises, masses of bad people, and plenty of lurking issues to lose sleep over.

The fear du jour may change, but as the late-great investor Sir John Templeton correctly stated:

“Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.”

And for the last decade since the 2008-2009 Financial Crisis, it’s clear to me that the stock market has climbed a lot of worry, pessimism, and skepticism. Over the last decade, here is a small sampling of wories:

With over five billion cell phones spanning the globe, fear-inspiring news headlines travel from one end of the world to the other in a blink of an eye. Fortunately for investors, the endless laundry list of crises and concerns has not broken this significant, multi-year bull market. In fact, stock prices have more than tripled since early 2009. As famed hedge fund manager Leon Cooperman noted:

“Bull markets don’t die from old age, they die from excesses.”

On the contrary to excesses, corporations have been slow to hire and invest due to heightened risk aversion induced by the financial crisis. Consumers have saved more and lowered personal debt levels. The Federal Reserve took unprecedented measures to stimulate the economy, but these efforts have since been reversed. The Fed has even signaled its plan to reduce its balance sheet later this year. As the expansion has aged, corporations and consumer risk aversion has abated, but evidence of excesses remains paltry.

Investors may no longer be panicked, but they remain skeptical. With each subsequent new stock market high, screams of a market top and impending recession blanket headlines. As I pointed out in my March Madness article, stocks have made new highs every year for the last five years, but continually I get asked, “Wade, don’t you think the market is overheated and it’s time to sell?”

For years, I have documented the lack of stock buying evidenced by the continued weak fund flow sales. If I could summarize investor behavior in one picture, it would look something like this:

Corrections have happened, and will continue to occur, but a more significant decline will likely happen under specific circumstances. As I point out in Half Empty, Half Full?, the time to become more cautious will be when we see a combination of the following trends occur:

- Sharp increase in interest rates

- Signs of a significant decline in corporate profits

- Indications of an economic recession (e.g., an inverted yield curve)

- Spike in stock prices to a point where valuation (prices) are at extreme levels and skeptical investor sentiment becomes euphoric

Attempting to predict a market crash is a Fool’s Errand, but more important for investors is periodically reviewing your liquidity needs, time horizon, risk tolerance, and unique circumstances, so you can optimize your asset allocation. There will be plenty more head fake surprises, but if conditions remain the same, investors should not be surprised by new stock highs.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Marathon Market Gets a Cramp

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2015). Subscribe on the right side of the page for the complete text.

“Anyone can run a hundred meters, it’s the next forty-two thousand and two hundred that count.”

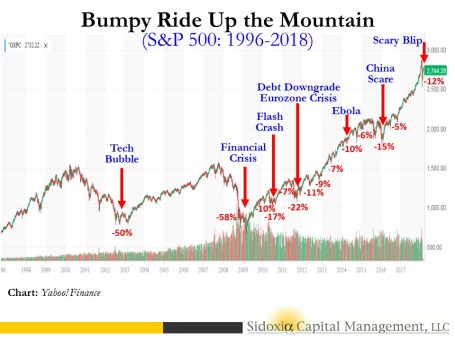

Investing is a lot like running a marathon…but it’s not a sprint to the retirement finish line. The satisfaction of achieving your long-term goal can be quite rewarding, but attaining ambitious objectives does not happen overnight. Along the hilly and winding course, there can be plenty of bumps and bruises mixed in with the elation of a runner’s high. While stocks have been running at a record pace in recent years, prices have cramped up recently as evidenced by the -2.6% decline of the S&P 500 stock index last month.

But the recent correction should be placed in the proper perspective as you approach and reach retirement. Since the end of the 2008 Financial Crisis the stock market has been racing ahead at a brisk rate, as you can see from the total return performance below (excluding 2015):

This performance is more indicative of a triumph than a catastrophe, but if you turned on the TV, listened to the radio, or surfed the web, you may come to a more frightening conclusion.

What’s behind the recent dip? These are some of the key concerns driving the recent price volatility:

- China: Slowing growth in China and collapse in Chinese stock market. China is suffering from a self-induced slowdown designed to mitigate corruption, prick the real estate bubble, and shift its export-driven economy to a more consumer-driven economy. These steps diminish short-term growth (albeit faster than U.S. growth), but nevertheless the measures should be constructive for longer-term growth.

- Interest Rates: Uncertainty surrounding the timing of a 0.25% target interest rate increase by the Federal Reserve. The move from 0% to 0.25% is like walking from the hardwood floor onto the rug…hardly noticeable. The inevitable move by the Fed has been widely communicated for months, and given where interest rates are today, the move will have a negligible impact on corporate borrowing costs. Like removing a Band-Aid, the initial action may cause some pain, but should be comfortably received shortly thereafter.

- Politics: Potential government shutdown / sequestration. The epic political saga will never end, however, as I highlighted in “Who Said Gridlock is Bad?,” political discourse in Washington has resulted in positive outcomes as it relates to our country’s fiscal situation (limited government spending and declining deficits). The government shutdown appears to have been averted for now, but it looks like we will be blanketed with brinkmanship nonsense again in a few months.

- Biotech/Pharmaceuticals: Politics over lofty drug prices and the potential impact of future regulation on the biotech sector. Given the current Congressional balance of power, any heavy-handed Democratic proposals is likely to face rigorous Republican opposition.

- Emerging Markets: Emerging market weakness, especially in Latin America (e.g., Brazil). These developments deserve close monitoring, but the growth in the three largest economic regions (U.S., Europe, and China) will have a much larger effect on the direction of global economic expansion.

- Middle East: Destabilized Middle East and Syria. Terrorist extremism and cultural animosity between various Middle East populations has existed for generations. There will be no silver bullet for a peaceful solution, so baby steps and containment are critical to maintain healthy global trade activity with minimal disruptions.

Worth noting, this current list of anxieties itemized above is completely different from six months ago (remember the Greece crisis?), and the list will change again six months into the future. Investing, like any competitive challenge, does not come easy…there is always something to worry about in the land of economics and geopolitics.

Here’s what the world’s top investor Warren Buffett said a few decades ago (1994) on the topic of politics and economics:

“We will continue to ignore political and economic forecasts which are an expensive distraction for investors and businessmen. Thirty years ago, no one could have foreseen the huge expansion of the Vietnam War, wage and price controls, two oil shocks, the resignation of a president, the dissolution of the Soviet Union, a one-day drop in the Dow of 508 points, or treasury bill yields fluctuating between 2.8% and 17.4%.”

In a world of 7.3 billion people and 196 countries there will never be a shortage of fear, uncertainty, and doubt (F.U.D.) – see events chart in The Bungee Market. In an ever-increasing, globally connected world, technology and the media continually amplify molehills into mountains, thereby making the next imagined Armageddon a simple click of a mouse or swipe of a smartphone away.

Today’s concerns are valid but in the vast majority of cases the issues are completely overblown, sensationalized and over-emphasized without context. Context is an integral part to investing, but unfortunately context usually cannot be explained in a short soundbite or headline. On the flip side, F.U.D. thrives in the realm of soundbites and headlines.

While investors may feel fatigued from a strong flow of headline headwinds, financial market race participants should take a break at the water stop to also replenish themselves with a steady tailwind of positive factors, including the following:

- Employment: The unemployment rate has been cut from a recession peak of 10.0% down to 5.1%, and the economy has been adding roughly +200,000 new monthly jobs on a fairly consistent basis. On top of that, there are a record 5.8 million job openings versus 3.7 million two years ago – a sign that the economy continues to hum along.

- Housing/Commercial Real Estate/Mortgage Rates: Housing prices have rebounded by about +30% from the 2012 lows; Housing starts have increased by +25% in the past year and 120% in the past four years; and 30-Year Fixed mortgage interest rates sit at 3.85% – a highly stimulative level within a spitting distance from record lows.

- Auto Sales: Surged to a post-recession record of 17.8 million units in August.

- Interest Rates: Massively stimulative and near generational lows, even if the Fed hikes its interest rate target by 0.25% in October, December or sometime in 2016.

- Capital Goods Orders: Up for three consecutive months.

- Rail Shipments/Truck Tonnage: Both these metrics are rising by about 3-4%.

- Retail Sales: Rising at a very respectable pace of 7% over the last six months.

- Low Energy & Commodity Prices: Inflation has remained largely in check thanks to plummeting commodity prices. Low oil and gas prices are benefiting consumers in numerous ways, including the contribution to car sales, home sales, and/or debt reduction.

While the -10% dip in stock prices from mid-August might feel like a torn knee ligament, long-term investors know -10% corrections historically occur about one-time per year, on average. So, even though you may be begging for a wheelchair, the best course of action is to take a deep breath, stick to your long-term investment plan, rebalance your portfolio if necessary, and continue staying on course towards your financial finish line.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

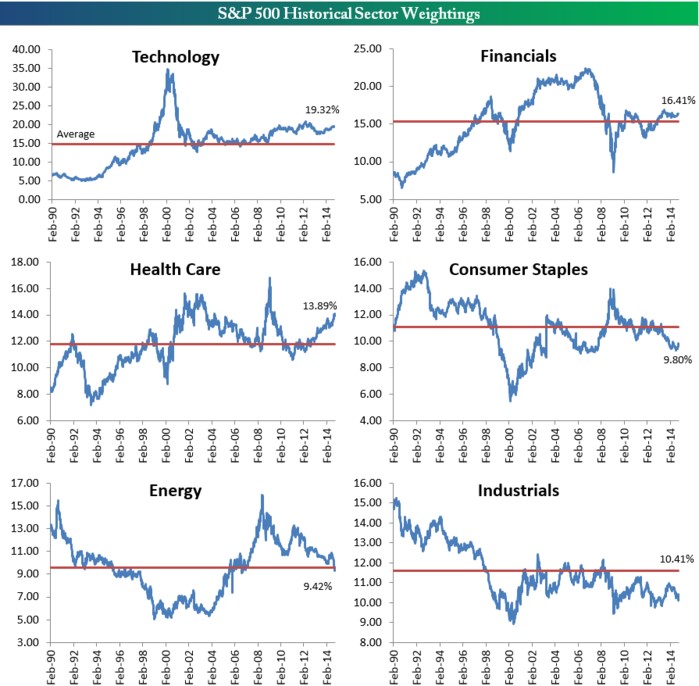

Sector Weightings: Another Financial Toolbox Gizmo

The ever-elusive $64,000 question of “Where does the stock market go from here?” is as popular a question today as it was a century ago. All you have to do is turn on CNBC to find an endless number of analysts, strategists, journalists, economists, and other talking heads guessing on the direction of stock prices. So many people are looking to make a quick buck or get a hot tip, but unfortunately investing is like dieting…it takes hard work and there are no simple solutions. As much as the pundits would like to make this investment game sound like a scientific certainty, in reality there is a lot of subjective art, experience, and luck that goes into successful investment outcomes. Consistent followers of Investing Caffeine understand there are a number of tools I use to guide me on the direction and level of stock prices, and three of my toolbox gizmos include the following:

- Earnings (Stock prices positively correlated)

- Interest Rates (Stock prices inversely correlated)

- Sentiment (Stock prices inversely correlated)

While these and other devices (see SHGR Holy Grail) are great for guesstimating the direction of longer-term stock prices, sector weightings are also great tools for identifying both overheated and unloved segments of the market. Take an extreme example, such as the S&P 500 Technology historical sector weighting in the year 2000. As you can see from the Bespoke Investment charts, the Technology sector went from about a 5% weighting of the overall market in the early 1990s to around 36% at the 2000 peak before dropping back down to 15% after the Tech Bubble burst. If you fast forward to the 2008-2009 Financial Crisis, we saw a similar “bubblicious” phenomenon rupture in the Financial sector. During 1980 the Financial segment accounted for approximately 5% of the total S&P 500 Index market capitalization in 1980 and skyrocketed to a peak of 23% in 2007, thanks in large part to a three decade bull-run in declining interest rates coupled with financial regulators asleep at the oversight switch.

Source: Bespoke Investment

While some segment weightings are currently above and below historical averages, the chart shows there is a tendency for mean reversion to occur over time. As I’ve written in the past, while I believe the broader market can be objectively be interpreted as reasonably priced in light of record earnings, record low interest rates, and a broader skeptical investing public ( see Markets Soar and Investors Snore), I’m still finding expensive, frothy sub-sectors in areas like money losing biotech and social media companies. The reverse can be said if you examined the 2000 period – the overall stock market was overpriced at its 3/24/00 peak (P/E ratio of about ~31x), but within the S&P 500 stocks there were bargains of a lifetime if you looked outside the Tech sector. Consider many of the unloved “Old Economy” stocks that got left behind in the 1990s. Had you invested in these forgotten stocks at the peak of the 2000 market (March 24, 2000), you would have earned an equal-weighted average return of +430% (and significantly higher than that if you included dividends):

Caterpillar Inc (CAT): +416%

Deere & Co (DE): +367%

FedEx Corp (FDX): +341%

Ingersoll-Rand Co (IR): +260%

Lockheed Martin Corp (LMT): +811%

Three M Company (MMM): +254%

Schlumberger Ltd (SLB): +158%

Union Pacific Corp (UNP): +1,114%

Exxon Mobil Corp (XOM): +148%

Average +430%

That +430% compares to a much more modest +36% return for the S&P 500 over the same period. What this data underscores are the perils of pure index investing and highlights the room for active investment managers like Sidoxia Capital Management to generate alpha.

There are many ways of analyzing “Where does the stock market go from here?,” but whatever methods you use, the power of examining sector weightings and mean reversion gizmos should be readily accessible in your investment toolbox.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FDX; non-discretionary positions in DE, LMT, MMM, SLB, XOM, and a range of positions in certain exchange traded fund positions, but at the time of publishing SCM had no direct position in CAT, IR, UNP, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Stock Talk: The Value of Media in Finance

I recently caught up with 50-year investment veteran Bill Kort to answer his questions regarding the media’s impact on the financial industry. After working for Kidder Peabody, A.G. Edwards, Wachovia, and Wells Fargo, Bill called it quits and decided to retire. Besides enjoying retirement with his wife, children, and grandchildren, Bill now also devotes considerable time to his blog Kort Sessions (www.KortSessions.com).

In a recent interview published on his Kort Sessions blog (KS), here’s what we discussed:

KS: Today, when you recommend a client take on, or increase equity exposure, what are the most common push-backs that you get? Have these changed in the past few years? If so, could you explain.

Wade Slome: “Given the events that have transpired over the last 15 years, I expect to receive a healthy dosage of pushback. Many investors have naturally been scarred from the 2008-2009 Financial Crisis, so convincing certain people that the 100-year flood will not occur every 100 days can be challenging. Regardless of the skepticism I receive, I feel it’s my duty to provide the best possible advice I can to existing clients and prospective clients. I can lead a horse to water, but I believe it’s not my job to force clients into a single investment option. At Sidoxia, we customize investment plans that meet clients’ risk tolerances, time horizons, and overall objectives.

With regard to sentiment changes in recent years, it is true that the tripling in equity market values since early 2009 has changed investor moods. Risk appetites have definitely increased. Nevertheless, cynicism is still rampant. Surveys done by Gallup show that stock ownership is near 15-year lows and despite stocks at or near record highs, ICI fund flow data shows money fleeing U.S. stock funds in 2014. With generational low interest rates, I see many long-term investors being too imprudently conservative. However, on the other hand, my responsibility is to also prevent other clients from taking on too much risk, especially if they have shorter investment time horizons or have limited funds in retirement.”

KS: When you speak with clients today, what are prominent worries do they have about their investments: The general level of the market, valuation, the economic backdrop, U.S. political issues or geopolitical concerns (all of the above)? Could you rank or tell me which concerns seem to be paramount.

Wade Slome: “In this 24-hour news cycle society we live in, an avalanche of real-time data gets crammed down our throats daily through our smartphones and Twitter-Facebook pages. As a result, the overwhelming barrage of news gets disseminated instantaneously, which in turn spreads fear like wildfire by word of mouth. In this type of environment it comes as no surprise to me that the general public is on edge. Every molehill is made into a mountain by media outlets for a simple reason…fear sells! Before the internet 20 years ago, virtually no one could find the location of Cyprus, Syria, Ukraine, or Gaza on a map – now we have Google and Wikipedia to show us or the Twitter feed scrolling at the bottom of our television sets reminds us. As far as concerns go, it’s tough to rank which ones are paramount. One day it’s the elections or Iran, and then the other day it’s the stock market crashing or the Ebola virus. Eventually the emotional pendulum will swing from fear and pessimism to optimism and euphoria, it always does. Like a lot of different professions, one of best strengths to have as an investment manager is the experience in knowing what noise to filter out and the ability to identify the relevant factors that drive outperformance.”

KS: Could you share the short-form responses that you might give to your clients when addressing the aforementioned issues.

Wade Slome: “The best advice I can give investors is to ignore the headlines. This principle is just as true today as it was a century or two ago. Mark Twain famously said, “If you don’t read the newspaper, you are uninformed. If you do read the newspaper, you are misinformed.” This is obviously presented a little tongue-in-cheek, but the main point being is headlines should not drive your investment decisions. It’s perfectly fine to be informed about the economy and politics, but people must realize the stock market often moves independently and in contrarian directions to prevailing media stories. Rather than emotionally react to news flow, it is much more important to create an objective, long-term investment plan that takes advantage of market noise, hype, and volatility.”

KS: Finally, this is a little bit of a leading question that I hope you might run with. Do you find any useful purpose being served by the financial, general or political media that might aid an individual’s investment process?

Wade Slome: “In my view of the financial markets, there are a few underlying principles that drive stock prices over the long-term, and they include such basic factors as earnings, valuations, interest rates, and market psychology. What I would objectively try to argue is that the financial, general, or political media have little to no impact on the first three factors and only modest influence on the last one (market psychology). Part of the reason I have been so constructive on the markets on my Investing Caffeine blog over the last five years is because all these factors have generally pointed in the right direction. I will become nervous when earnings decline, valuations get stretched, interest rates spike, and/or psychology turns euphoric. Right now, I don’t think we are seeing any of that occurring.

With that said, I do believe there are exceptions to the rule that the “media is evil.” If you have the time, interest, and patience to stagger through the endless desert of financial media, you can find a few rare flowers. Although I do consume mass amounts of media, 99% of it ends up in the trash or ignored. I do my best to reserve my media consumption to those successful investors who have lived through multiple market cycles and have a winning track record to back it up. It is possible to find sage investment bloggers; Warren Buffett interviews on CNBC; or newspaper interviews of thriving venture capitalists, if you properly dine on a healthy media diet. Unfortunately there is a lot of junk food financial content out in media land. What should generally be avoided at all costs are rants from economists, journalists, analysts, commentators, and talking heads. No matter how eloquent or articulate they may sound, the vast majority of the people you see on television have not invested a professional dime in their careers, so all you are getting from them are worthless, vacillating opinions. I choose to stick to commentary from the tried and true investment veterans.”

Bill, thanks again for the thoughtful interview questions, and continued success with your Kort Sessions blog!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own GOOG/GOOGL, and a range of positions in certain exchange traded fund positions, but at the time of publishing SCM had no direct position in TWTR, FB, WFC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Floating Hedge Fund on Ice Thawing Out

These days, pundits continue to talk about how the same financial crisis plaguing Greece and its fellow PIIGS partners (Portugal, Ireland, Italy & Spain) is about to plow through the eurozone and then ultimately the remaining global economy with no mercy. If all the focus is being placed on a diminutive, calamari-eating, Ouzo-drinking society like Greece, whose economy matches the size of Maryland, then why not evaluate an even more miniscule, PIIGS prequel country…Iceland.

That’s right, the same Iceland that just four years ago people were calling a “hedge fund on ice.” You know, that frozen island that had more foreign depositors investing in their banks than people living in the country. Before Icelandic banks became more than 75% of the overall stock market, and Gordon Gekko became the country’s patron saint, Iceland was more known for fishing. The fishing industry accounted for about half of Iceland’s exports, and the next largest money maker may have been Bjork, the country’s famed and quirky female singer.

In looking back at the financial crisis of 2008-2009, as it turned out, Iceland served as a canary in the global debt binging coal mine. In order to attract the masses of depositors to Icelandic banks, these financial institutions offered outrageous, unsustainable interest rates to yield-starved customers. How did the Icelandic bankers offer such high rates? Well of course, it was those can’t-lose American subprime mortgages that were offering what seemed like irresistibly high yields. Of course, what seemed like a dream at the time, eventually turned into a nightmare once the scheme unraveled. Ultimately, it became crystal clear that the subprime borrowers could not pay the outrageous rates, especially after rates unknowingly reset to untenable levels for many borrowers.

At the peak of the crisis, the Icelandic banks were holding amounts of debt exceeding six times the Icelandic GDP (Gross Domestic Product) and these lenders suffered more than $100 billion in losses. One of the Icelandic banks was even funding a large condominium project in my neighboring Southern California city of Beverly Hills. When the excrement hit the fan after Lehman Brothers went bankrupt, it didn’t take long for Iceland’s stock market to collapse by more than -95%; Iceland’s Krona to crumple; and eventually the trigger of Iceland’s multi-billion bailout by numerous constituents, including the IMF (International Monetary Fund).

Bitter Medicine First, Improvement Next

Today, four years after the subprime implosion and Lehman debacle, the hedge fund on ice known as Iceland is beginning to thaw, and their economic picture is looking much brighter (see charts below). GDP growth is the highest it has been in four years (4.5% recently); the stock market has catapulted upwards (almost doubling from the lows); and the Iceland unemployment rate has declined from over 9% a few years ago to about 7% today.

Source: Trading Economics

Source: Trading Economics

Re-jiggering a phony economy with a faulty facade cannot be repaired overnight. However, now that the banking system has been allowed to clear out its excesses, Iceland can move forward. One tailwind behind the economy has been Iceland’s weaker currency, which has led to a +17% increase in foreign tourist nights at Icelandic hotels through April this year. What’s more, tourist traffic at Iceland’s airport hit a record in May. Iceland has taken its bitter medicine, adjusted, and is currently reaping some of the rewards.

Although the detrimental effects of austerity experienced by the economies and banks of Greece, Spain, and Italy crowd out most of today’s headlines, Iceland is not the only country to make painful changes to its fiscal ways and then taste the sweetness of progress. Let’s not forget the Guinness drinking Irish. Ireland, like Greece, Portugal, and Spain received a bailout, but Ireland’s banking system was arguably worse off than Spain’s, yet Ireland has seen its borrowing costs on its 10-year bond decrease dramatically from 9.2% at the beginning of 2011 to about 7.4% this month (still high, but moving in the right direction). The same can be said for the United States. Our banks were up against the ropes, but after some recapitalization, tighter oversight, and stricter lending standards, our banks have gotten back on track and have helped assist our economy grow for 11 consecutive quarters (albeit at uninspiring growth rates).

The austerity versus growth debate will no doubt continue to circulate through media circles. In my view, these arguments are too simplistic and one dimensional. Every country has its unique culture and distinct challenges, but even countries with massive financial excesses can steer themselves back to a path of growth. A floating hedge fund on ice to the north of us has proven that fact to us, as we witness brighter days beginning to thaw Iceland’s chilly economy to expansion again.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in Lehman Brothers, Guinness, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Broken Record Repeats Itself

Article is an excerpt from previously released Sidoxia Capital Management’s complementary June 2012 newsletter. Subscribe on right side of page.

Traditional music records have been replaced with CDs (compact discs) and digital downloads. Although the problem of a broken record repeating itself is no longer an issue, our financial markets have not conquered the problem of repetition. More specifically, the timing of the -6.3% stock market decline during May (as measured by the S&P 500 index), coincides with the same broken sell-offs we have temporarily experienced over the last two summers. First, we had the “Flash Crash” in the summer of 2010, and then the debt ceiling debate and credit downgrade of 2011.

So far, the “Sell in May and go away” mantra has followed the textbook lessons over the last few years, but as you can see from the chart below, the short-lived seasonal sell-offs have been followed by significant advances (up +33% from 2010 lows and up +29% from the 2011 lows). Given the global challenges, a two-steps forward, one-step back pattern in equity markets should not be seen as overly surprising by investors.

Source: Yahoo Finance

Although the late-spring and summer doldrums have not been a joy-ride in recent years, these overly simplistic seasonal trading rules of thumb have not been exceedingly reliable either. For example, even though the months of May in 2010-2012 produced negative returns, the previous 25 Mays going back to 1985 produced positive returns more than 2/3 of the time. Rather than fiddle with these unreliable, unscientific trading rules, individuals would be better served by listening to famous Jedi Master Yoda from Star Wars, who so astutely noted, “Uncertain, the future is.”

Voting Machines and Scales

Given the spread of globalization and technology, the speed of news dissemination has never been faster. With the 2008-2009 financial crisis still burned into investors’ minds, the default response to any scary news item is to shoot first and ask questions later. Renowned long-term investing legend Ben Graham famously highlighted, “In the short run the market is a voting machine. In the long run it’s a weighing machine.”

As it relates to short-run current events, here are some of the items that investors were voting on (no pun intended) this month:

Europe, Europe, Europe: This problem has been with us for some time now, and there are no signs it will disappear anytime soon. In a game of chicken between the EU (European Union) and Greek legislators, fresh elections are taking place on June 17th, which will ultimately determine if Greece will exit the Euro monetary union or stick to the bitter medicine of austerity prescribed by the key European decision-makers in Germany. As Greece attempts to clean up its own mess, European politicians and G-20 leaders around the globe are scrambling to create plans that ring-fence countries like Spain and Italy from succumbing to a Greek-born contagion.

Presidential Politics: If you haven’t been living in a cave for the last six months, you probably know that 2012 is a presidential election year. Regardless of your politics, there are big questions surrounding the economy, jobs, deficits, debt, taxes, entitlements, defense, gay marriage, and other important issues. Answers to many of these questions will remain unclear until we get closer to the elections. The financial markets do not like uncertainty, so probabilities would indicate volatility will remain par for the course for the foreseeable future.

Facebook Folly: Despite my warnings, Facebook’s initial public offering (IPO) failed to live up to the social media giant’s hype – the share price has fallen -22% since the shares originally priced. Great companies do not always make great stocks, especially when a relatively new kid on the block has his company’s stock initially valued at a hefty price-tag of more than a $100 billion. Finger pointing is being spread liberally on the botched Facebook deal (e.g., Morgan Stanley, NASDAQ, Facebook), but no need to shed a tear for 28-year-old founder Mark Zuckerberg since his ownership stake in the company is still valued at around $15 billion – enough to cover a European trip to McDonald’s with his newlywed wife.

Dimon in a Rough Spot: Jamie Dimon, the poster child of the banking industry (and CEO of JP Morgan Chase – JPM), dropped a bomb on the investment community earlier in the month by explaining how a rogue “whale” trader racked up $2 billion in initial losses (and growing) by taking excessive risk and throwing controls into the wind.

Chinese Dragon Losing Steam: The #2 global economy has been losing some steam as witnessed by slowing industrial production and GDP growth (Gross Domestic Product). In turn, the self correcting economic forces of supply and demand have provided relief to consumers and corporations in the form of lower fuel, energy, and commodity prices. Chinese leaders are not sitting still – there are plans of accelerating infrastructure spending and assisting banks in the form of capital injections and lower reserve requirements.

As I discussed in a previous Investing Caffeine article (see The European Dog Ate My Homework), although the current headlines remain gloomy, that will always be the case. Just a few years ago, Bear Stearns, Lehman Brothers, AIG, CDS (credit default swaps), and subprime mortgages were the boogeymen. In the 1980s, we had the Savings & Loan financial crisis and the infamous 1987 Crash. During the 1970s, the Vietnam War, Nixon’s impeachment proceedings, and rising inflation were the dominating issues. Since then, the equity markets are up over 20x-fold – time will always reward those patient long-term investors. Despite all the doom and gloom, stock markets have roughly doubled over the last three years and all the major indexes remain solidly in the black for the year. Choppy waters are likely to remain as we approach this year’s elections, but for those who understand broken records often repeat themselves, there’s a good chance the music will eventually sound much better.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including commodities, inflation protection, floating rate bonds, real estate, dividend, and alternative investment ETFs), but at the time of publishing SCM had no direct position in FB, MCD, JPM, MS, NDAQ, AIG, Lehman Brothers, Bear Stearns, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investing with the Sentiment Pendulum

Article is an excerpt from Sidoxia Capital Management’s complementary May 2012 newsletter. Subscribe on right side of page.

The last five years have been historic in many respects. Not only have governments and central banks around the world undertaken unprecedented actions in response to the global financial crisis, but investors have ridden an emotional rollercoaster in response to historically unparalleled uncertainties.

While the nature of this past crisis has been unique, experienced investors know these fears continually manifest themselves in different forms over various cycles in time. Despite the more than doubling in equity market values over the last few years, as measured by the S&P 500 index, the emotional pendulum of investor sentiment has only partially corrected. Investor temperament has thankfully swung away from “Panic,” but has only moved closer to “Fear” and “Skepticism.” Here are some of the issues contributing to investors’ current sour mood:

The Next European Domino: The fear of the Greek domino toppling the larger Spanish and Italian economies has investors nervously chewing their finger-nails, and political turmoil in France and the Netherlands isn’t creating any additional warm and fuzzies.

Job Additions Losing Steam: New job creation here in the U.S. weakened to a lethargic monthly rate of +120,000 new jobs in March, while the unemployment rate remains stubbornly high at an 8.2% level.

Domestic Growth Losing Mojo: GDP (Gross Domestic Product) growth of +2.2% during the first quarter of 2012 also opened the door for the pessimists. Consumers are still spending (+2.9% growth), but government spending, business investment, and housing are taking wind out of the economy’s sails.

Emerging Markets Submerging: Unspectacular growth in the U.S. is not receiving any favors from slowing emerging markets like China and Brazil, which took fiscal and monetary actions to slow inflation and housing speculation in 2011.

Humpty Dumpty Politics: Presidential elections, tax policy, and deficit reduction are all concerns that carry the possibility of pushing the economic Humpty Dumpty off the wall, and as a result potentially lead to a great fall. The determination of Humpty Dumpty’s fate will likely have to wait until year-end or 2013.

Any student of history knows these fears and other concerns never go away – they simply change. But like supply and demand, gravitational forces eventually swing the emotional pendulum in the opposite direction. As Sir John Templeton so aptly stated, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” Or in other words, escalating bull markets must climb the proverbial “Wall of Worry” in order to sustain upward momentum. If there was nothing to worry about, then all the buyers would already be in the markets. We are nowhere close to experiencing “Euphoria” like we saw in stocks during the late-1990s or in the housing market around 2005.

Positively Climbing the “Wall of Worry”

With all this bad news out there, surprisingly there are some glimmers of hope chipping away at the “Wall of Worry.” Here are some of the positive factors helping turn pessimist frowns upside down:

Slow & Steady Wins the Race: The economic recovery has been weaker than hoped, but I can think of worse scenarios than 11 consecutive quarters of GDP growth and 25 straight months of private job creation, which has reduced the unemployment rate from 10.0% in October 2009 to 8.2% last month.

Earnings Machine Keeps Chugging Along: With the majority of S&P 500 companies having reported their quarterly results for the first quarter, three-fourths of the companies are beating forecasted earnings, which are currently registering in at a respectable +7.1% rate (Thomson Reuters). One company epitomizing this trend is Apple Inc. (AAPL). The near doubling in Apple’s profits during the quarter, thanks to explosive iPhone sales, pushed Apple’s shares over $600 and helped drive the NASDAQ index to its best day of the year.

Super Ben to the Rescue: The Federal Reserve has already stated their intention of keeping interest rates near 0% until 2014. The potential of additional monetary stimulus spearheaded by Federal Reserve Chairman Ben Bernanke, in the form of QE3 (Quantitative Easing Part III), may provide further needed support to the stock market (a.k.a., the “Bernanke Put”).

Return of the IPO: Initial Public Offerings (IPOs) have gained steam versus last year with more than 53 already coming to market in the first four months of 2012. This is no 1999, but a good number of deals have done quite well over the last month. For example, data analysis company Splunk Inc. (SPLK) share price is already up around 100% and the value of leisure luggage company TUMI Holdings (TUMI) has climbed over +40%. In a few weeks, the highly anticipated blockbuster Facebook (FB) IPO is expected to begin trading its shares, so we can see if the chronicled deal can live up to all the hype.

Dividends Galore: Dividend payments to stockholders are flowing at an extraordinary rate so far in 2012. Companies like IBM (increased its dividend by +13%), Exxon Mobil – (XOM +21%); Goldman Sachs – (GS +31%) are but just a few of the dividend raisers this year. Through the first three months of the year, the number of companies increasing their dividend payments was up +45% as compared to the comparable number for all of 2011.

Emerging Growth Not Dead: While worriers fret over slowing growth in China, companies like Apple grew by more than +100% in this region and collected nearly 20% of its revenues from this Asian country (~$8 billion). Coincidentally, China is expected to surpass an incredible one billion mobile connections in May – many of those iPhones. In other related news, Starbucks Corp. (SBUX) plans to triple its workforce and number of stores in China over the next three years. China has also helped fuel a backlog of Caterpillar Inc. (CAT) that is more than triple the level of 2009. Emerging markets may have slowed down in 2011, but with inflation beginning to stabilize, emerging market central banks and governments are now beginning to ease policies and reduce red-tape. For example, Brazil and India have started to lower key benchmark interest rates, and China has started to reverse capital flow restrictions.

Stay Off the Trampled Path

The mantra of “Sell in May and go away” always gets a lot of playtime around this period of the year. Over the last few years, the temporary spring/summer sell-offs have only been followed by stronger price appreciation. Individuals attempting to time the market (see also Getting Off the Treadmill) generally end up in tears. And for those traders who boast about their excellent timing (like those suspicious friends who brag about always winning in Las Vegas), we all know the truth – nobody buys at the lows and sells at the highs…except for liars.

With all the noise and cross-currents flooding the airwaves, investing for individuals without assistance has never been so difficult. But before hiding in your cave or reacting to the next scary headline about Europe, the economy, or politics, do yourself a favor by reminding yourself these chilling news items are nothing new and are often great contrarian indicators (see also Back to the Future). The emotional pendulum is constantly swinging from fear to greed and investors stand to prosper by adjusting sentiment and actions in the opposite direction. To survive in the investing wild, it is best to realize that the grass is greener and the eating more abundant when you stay off the trampled path of the herd.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in SPLK, TUMI, IBM, XOM, GS, SBUX, CAT, FB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}