Posts tagged ‘fees’

10 Ways to Destroy Your Portfolio

![]()

With the increased frequency of heightened volatility, investing has never been as challenging as it is today. However, the importance of investing has never been more crucial either, due to rising life expectancies, corrosive effects of inflation, and the uncertainty surrounding the sustainability of government programs like Social Security, Medicare, and pensions.

If you are not wasting enough money from our structurally flawed and loosely regulated investment industry that is inundated with conflicts of interest, here are 10 additional ways to destroy your investment portfolio:

#1. Watch and React to Sensationalist News Stories: Typically, strategists and pundits do a wonderful job of parroting the consensus du jour. With the advent of the internet, and 24/7 news cycles, it is difficult to not get caught up in the daily vicissitudes. However, the accuracy of the so-called media experts is no better than weather forecasters’ accuracy in predicting the weather three Saturdays from now at 10:23 a.m. Investors would be better served by listening to and learning from successful, seasoned veterans (see Investing Caffeine Profiles).

#2. Invest for the Short-Term and Attempt Market Timing: Investing is a marathon, and not a sprint, yet countless investors have the arrogance to believe they can time the market. A few get lucky and time the proper entry point, but the same investors often fail to time the appropriate exit point. The process works similarly in reverse, which hammers home the idea that you can be 200% wrong when you are constantly switching your portfolio positions.

#3. Blindly Invest Without Knowing Fees: Like a dripping faucet, fees, transaction costs, taxes, and other charges may not be noticeable in the short-run, but combined, these portfolio expenses can be devastating in the long-run. Whether you or your broker/advisor knowingly or unknowingly is churning your account, the practice should be immediately halted. Passive investment products and strategies like ETFs (Exchange Traded Funds), index funds, and low turnover (long time horizon / tax-efficient) investing strategies are the way to go for investors.

#4. Use Technical Analysis as a Primary Strategy: Warren Buffett openly recognizes the problem with technical analysis as evidenced by his statement, “I realized technical analysis didn’t work when I turned the charts upside down and didn’t get a different answer.” Legendary fund manager Peter Lynch adds, “Charts are great for predicting the past.” Most indicators are about as helpful as astrology, but in rare instances some facets can serve as a useful device (like a Lob Wedge in golf).

#5. Panic-Sell out of Fear & Panic-Buy out of Greed: Emotions can devastate portfolio returns when investors’ trading activity follows the herd in good times and bad. As the old saying goes, “The herd is lead to the slaughterhouse.” Gary Helms rightly identifies the role that overconfidence plays when ininvesting when he states,”If you have a great thought and write it down, it will look stupid 10 hours later.” The best investment returns are earned by traveling down the less followed path. Or as Rob Arnott describes, “In investing, what is comfortable is rarely profitable.” Get a broad range of opinions and continually test your investment thesis to make sure peer pressure is not driving key investment decisions.

#6. Ignore Valuation and Yield: Valuation is like good pitching in baseball…very important. Valuation may not cause all of your investments to win, but this factor should be an integral part of your investment process. Successful investors think about valuation similarly to skilled sports handicappers. Steven Crist summed it up beautifully when he said, “There are no ‘good’ or ‘bad’ horses, just correctly or incorrectly priced ones.” The same principle applies to investments. Dividends and yields should not be overlooked – these elements are an essential part of an investor’s long-run total return.

#7. Buy and Forget: “Buy-and-hold” is good for stocks that go up in price, and bad for stocks that go flat or decline in value. Wow, how deeply profound. As I have written in the past, there are always reasons of why you should not invest for the long-term and instead sell your position, such as: 1) new competition; 2) cost pressures; 3) slowing growth; 4) management change; 5) excessive valuation; 6) change in industry regulation; 7) slowing economy; 8 ) loss of market share; 9) product obsolescence; 10) etc, etc, etc. You get the idea.

#8. Over-Concentrate Your Portfolio: If you own a top-heavy portfolio with large weightings, sleeping at night can be challenging, and also force average investors to make bad decisions at the wrong times (i.e., buy high and sell low). While over-concentration can be risky, over-diversification can eat away at performance as well – owning a 100 different mutual funds is costly and inefficient.

#9. Stuff Money Under Your Mattress: With interest rates at the lowest levels in a generation, stuffing money under the mattress in the form of CDs (Certificates of Deposit), money market accounts, and low-yielding Treasuries that are earning next to nothing is counter-productive for many investors. Compounding this problem is inflation, a silent killer that will quietly disintegrate your hard earned investment portfolio. In other words, a penny saved inefficiently will lead to a penny depreciating rapidly.

#10. Forget Your Mistakes: Investing is difficult enough without naively repeating the same mistakes. As Albert Einstein said, “Insanity is doing the same thing, over and over again, but expecting different results.” Mistakes will be made and it behooves investors to document them and learn from them. Brushing your mistakes under the carpet may make you temporarily feel better emotionally, but will not help your financial returns.

As the year approaches a close, do yourself a favor and evaluate whether you are committing any of these damaging habits. Investing is tough enough already, without adding further ways of destroying your portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Building Your All-Star NBA Portfolio

Image by © Royalty-Free/Corbis

You may or may not care, but the NBA (National Basketball Association) playoffs are in full swing. If you were an owner/manager of an NBA team, you probably wouldn’t pick me as a starting player on your roster – and if you did, we would need to sit down and talk. I played high school basketball (“played” is a loose term) in my youth, and even played in my early 40s against other over-aged veterans with knee braces, goggles, and headbands. Once my injuries began to pile up and my playing time was minimized by the spry, millennial team members, I knew it was time to retire and hang up my jockstrap.

The great thing about your investments is that you can create an All-Star NBA portfolio without the necessity of a salary market cap or billions of dollars like Mark Cuban. You can actually put the greatest professional players in the world (stocks/bonds) into your portfolio whether you invest $1,000 or $10,000,000. Sure, transactions costs can eat away at the smaller portfolios, but if investors are correctly managing their funds over years, and not months, then virtually everyone can create a cost-efficient elite team of stocks, bonds, and alternatives.

Now that we’ve established that anyone can create a championship caliber portfolio, the question then becomes, how does an owner go about selecting his/her team’s players? It may sound like a cliché, but diversification is paramount. Although centers Tim Duncan, Dwight Howard, Chris Bosh, Marc Gasol, and DeAndre Jordan may get a lot of rebounds for your team, it wouldn’t make sense to have those five starting centers on your team. The same principle applies to your investment portfolio.

Generally speaking, the best policy for investors is to establish exposure to a broad set of asset classes customized to your time horizon, risk tolerance, objectives, and constraints. In other words, it is prudent to have exposure to not only stocks and bonds, but other areas like real estate, commodities, alternatives, and emerging markets. Everybody has their own unique situation, and with interest rates and valuations continually changing, it makes sense that asset allocations across all individuals will be very diverse.

In basketball terms, the sizes and types of guards, forwards, and centers will be dependent on the objectives of the team’s owners/managers. For example, it is very logical to have Stephen Curry (see great video) as the starting guard for the fast-paced, highest scoring NBA team, Golden State Warriors but Curry would not be ideally suited for the slow, grind-em-up offense of the Utah Jazz (one of the lowest scoring teams in the NBA).

In order to build a consistent winning percentage for your portfolio, you need to have a systematic, disciplined process of choosing your all-star-team, which can’t just consist of picking the hottest player of the day. Not only could it be too expensive, the consequences of over-concentrating your portfolio with an expensive position can be painful….just ask Los Angeles Laker fans how they feel about overpaying for Kobe Bryant’s $23.5 million 2014-2015 salary. Investors who chased the overpriced tech sector in the late 1990s, with stock prices trading at over 100 times trailing 12-month earnings, understand how painful losses can be in the subsequent “bubble” burst.

Having a strong bench of players is crucial as well. This requires a research process that can prioritize opportunities based on quantitative and fundamental processes (at Sidoxia we use our SHGR model). Sometimes your starters get injured, fatigued, or bought out by a competitor. Interest rates, valuations, exchange rates, earnings growth rates and other economic factors are continually fluctuating, so having a bench of suitable investment ideas is critical for different financial environments.

Beating the market is a challenging endeavor, not only for individuals, but also for professionals. If you don’t believe me, then check out what Dalbar had to say about this subject in its annual report entitled, Quantitative Analysis of Investor Behavior:

Dalbar found that in 2014, the average investor in a stock mutual fund underperformed the S&P 500 by a margin of 8.19 percent. Fixed-income investors underperformed the Barclays Aggregate Bond Index by a margin of 4.81 percent.

Ouch! If you want to generate winning returns matching the likes of the 1,000-win club, which includes Gregg Popovich, Phil Jackson, and Pat Riley then you need to avoid some of the most common investor mistakes (see also 10 Ways to Destroy Your Portfolio). Chasing performance, ignoring diversification, emotionally reacting to news headlines, paying high fees, and over-trading are sure fire ways to get technical fouls and ejected from the investment game. Avoiding these mistakes and following a systematic, objective process will make you and your investment portfolio a successful all-star.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Retirement Epidemic: Poison Now or Later?

We live in an instant gratification society. The house, the car, and annual vacation take precedence over contributions to retirement and savings accounts. It therefore comes as no surprise to me that Americans spend more time on planning for vacation than they do on planning for retirement.

Given the choice of spending or saving, Americans in large part choose, “spend now, save later.” Or in other words, Americans choose to drink $10 margaritas now (spend) and swallow the more expensive poison (save) later. Spending now and saving later sounds good in theory until you reach your mid-60s and realize you’re going to have to work as a Wal-Mart Stores (WMT) greeter into your 80s while eating cat food in your tent.

To make matters worse, you don’t have to be a genius to see irresponsible government spending and globalization has compromised the health of our countries entitlements (Social Security and Medicare). Benefits are likely to be reduced over time and age eligibility requirements are likely to increase. If you fold in the dynamic of exploding healthcare costs and broad-based inflationary pressures, one can quickly realize savings habits need to change. The traditional model of working for 40 years and then relying on a pension and Social Security payments to cover a blissful multi-decade retirement just doesn’t apply to current reality. On top of the disappearance of plump pensions, life expectancy is rising (around 80 years in the U.S.), so the realistic risk of outliving your savings has a larger probability of occurring.

Surely I am overly dramatizing the situation by sounding the investing alarm bells out of self-interest…right? Wrong. As a geeky, financial numbers guy, I can objectively rely on numbers, and the statistics aren’t pretty.

Here’s a sampling:

- Empty Savings Cupboard: A 2013 study by the Employee Benefit Research Institute found that nearly half of workers had less than $10,000 saved, and according to Blackrock Inc (BLK), CEO, Larry Fink, the average American has saved only $25,000 for retirement

- Food Stamp Living: Almost half of middle-class workers, will be forced into a poor retirement lifestyle, living on a food budget of about $5 a day.

- 401(k) Will Not Save the Day: Compared to other forms of savings, the average 401(k) balance reached $89,300 at the end of 2013 – that’s the good news. The bad news is that only about half of all companies offer their employees 401(k) benefits, and for the approximately 60 million people that participate, about a fourth withdraw these 401(k) funds before retirement – out of necessity or for frivolous reasons. Even if you cheerily accept the size of the average balance, sadly this dollar amount is still massively deficient in meeting retirement needs. It’s believed that your savings should approximate 15-20 times your annual retirement expenses that aren’t covered by outside sources of income, such as social security or a pension.

If these figures aren’t scary enough to get you saving more, then just use common sense and understand the future is very uncertain. A 2012 New York Times article sarcastically captured how easy it is to plan for retirement:

First, figure out when you and your spouse will be laid off or be too sick to work. Second, figure out when you will die. Third, understand that you need to save 7 percent of every dollar you earn. (30 percent of every dollar [if you are 55 now].) Fourth, earn at least 3 percent above inflation on your investments, every year. (Easy. Just find the best funds for the lowest price and have them optimally allocated.) Fifth, do not withdraw any funds when you lose your job, have a health problem, get divorced, buy a house or send a kid to college. Sixth, time your retirement account withdrawals so the last cent is spent the day you die.

What to Do?

The short answer is save! Simplistically, this can be achieved in one of two ways: cut expenses or raise income. I won’t go into the infinite ways of doing this, but adjusting your mindset to live within your means is probably the first necessary step for most.

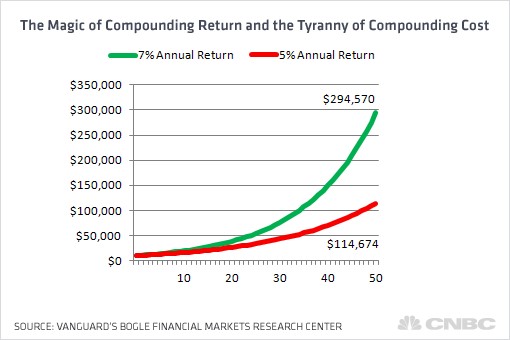

As it relates to your investments, fees should be your other major area of focus. The godfather of passive investing, Jack Bogle, highlighted the dramatic impact of fees on retirement savings. As you can see from the chart below, the difference between making 7% vs. 5% over an investing career by reducing fees can equate to hundreds of thousands of dollars, and prevent your nest egg from collapsing 2/3rd in value.

Source: CNBC

Lastly, if you are going to use an investment advisor, make sure to ask the advisor whether they are a “fiduciary” who legally is required to place your interests first. Sidoxia Capital Management is certainly not the only fiduciary firm in the industry, but less than 10% of advisors operate under this gold standard.

Investing and saving is a lot like dieting…easy to understand the concept but difficult to execute. The numbers speak for themselves. Rather than dealing with a crisis in your 70s and 80s, it’s better to take your poison now by investing, and reap the rewards of your hard work during your golden years.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), and WMT, but at the time of publishing SCM had no direct discretionary position in BLK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Performance Beauty in Eye of Beholder

The average person may be a good judge in picking the winner of a beauty contest, but unfortunately your average investor is ill-equipped to sift through the thousands of mutual funds and hedge funds and thoughtfully discern the relevant performance metrics for investment purposes.

Investment firms however, are well-equipped with smoke, mirrors, and a tool-chest filled with numerous tricks. Here are a few of the investment firms’ gimmicks:

- Cherry Picking: Fund firms are notorious with cutting out the bad performance numbers and cherry picking the good periods. As investment guru Charles Ellis reminds us, the wow factor results of “investment performance become quite ordinary by simply adding or subtracting one or two years at the start or the end of the period shown. Investors should always get the whole record – not just selected excerpts.”

- Limited Time Period: Often the period highlighted by investment firms is insufficient to make a proper conclusion regarding a manager’s outperformance capabilities. Ellis acknowledges that gathering enough yearly performance information can be practically challenging:

“By the time you had gathered enough data to determine whether your fund manager really was skillful or just lucky, at least one of you would probably have died of old age.”

- Fee Disclosure: Some managers’ performance figures look stupendous until one realizes once hefty fees are subtracted from the reported figures, what previously looked top-notch is now average or below-average. It is important to read the small print or ask tough questions of the broker peddling a fund.

- Audited Figures: Legitimacy of performance is key, and there are different levels of audited figures. Global Investment Performance Standards (GIPS) compliance is an industry accepted standard. For pooled investment vehicles, audited results from regional or national accounting firms can be important too.

- Misused Rating Systems: Morningstar is the 800 pound gorilla in the mutual fund world and provides some useful data. Unfortunately, most Morningstar investors use the data incorrectly. A 2000 study by the Journal of Financial and Quantitative Analysis discovered, “There is little statistical evidence that Morningstar’s highest-rated funds outperform the medium-rated funds.” On this subject, Charles Ellis points out the following:

“While Morningstar candidly admits that its star ratings have little or no predictive power, 100 percent of net new investment money going into mutual funds goes to funds that were recently awarded five stars and four stars…Indeed, in the months after the ratings are handed out each year, the five-star funds generally earn less than half as much as the broad market index!…Morningstar ratings are misleading investors into buying high and selling low.”

Investors need to be careful in how they use the ratings – simply buying 4-5 star funds and selling star-losing funds can be a heartburning recipe for bad results. Buying high and selling low usually doesn’t turn out very well.

Find Winners…Then What?

Even if you are successful in identifying the winning funds, those same funds tend to underperform in subsequent periods. Ellis, a believer in passive index investing, noticed only 10% of active managers outperformed over 25 years, and the odds of sustaining outperformance in subsequent periods diminished even further.

Charles Ellis also noticed a fat-tail syndrome of losers versus winners. For example, Ellis found 2% of active managers outperformed over a set time period, but a whopping 16% underperformed the market over a similar timeframe. Consistent with these findings, Ellis stresses that past performance does not predict future results, with one exception: “The worst losers do tend to keep losing. If you do decide to select active investment managers, promise yourself you will stay with your chosen manager for many years…changing managers is not only expensive, but it usually doesn’t work.”

Professionals to the Rescue

Well, if individuals are not in a position to pick future winning fund managers, then thank heavens the professional consultants can help out…not exactly. Ellis was blunt about the capabilities of those professionals selecting active investment managers:

“Pension executives and investment consultants who specialize in selecting the best managers have, as a group, been unsuccessful at selecting managers who can beat the market.”

Ellis uses a respected firm as an example to prove his point:

“Cambridge Associates reports candidly, ‘There is no sound basis for hiring or firing managers solely on the basis of recent performance.’”

At the end of the day, finding current winners is not a problem, but sifting through the massive quantity of funds and selecting future winners is very challenging for individuals and professionals alike. The financial industry would like you to believe picking the future performance beauty winner is a simple task – the data seems to indicate otherwise. Rather than wasting your money attempting to pick the beauty winner, perhaps your money would be better spent on purchasing a tiara for yourself.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MORN, Cambridge Associates, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investor Wake-Up Call

Source: Photobucket

The Pre Wake-Up Conversation

“Hey Milfred, did you see our brokerage statement? There must be a misprint. It says our portfolio of bonds is down.”

“Buford, how can that be, when our bond portfolio has been up for 30 consecutive years? I hear Jim Bernanke is trying to artificially inflate the economy by printing money and using it to buy bonds.”

![]() “Sweetheart, you got it wrong…it’s Ben Jernanke.”

“Sweetheart, you got it wrong…it’s Ben Jernanke.”

![]() “Ohhh, yeah honey, you’re right. I never expected prices to go down after government bond yields were up almost 50% in a few months.”

“Ohhh, yeah honey, you’re right. I never expected prices to go down after government bond yields were up almost 50% in a few months.”

![]() “Sweetie, maybe we should give our broker a call?”

“Sweetie, maybe we should give our broker a call?”

![]() “Oh you mean Skip? I think he wants us to call him a financial consultant or financial advisor now…not a broker.”

“Oh you mean Skip? I think he wants us to call him a financial consultant or financial advisor now…not a broker.”

![]() “Well anyway, I just read the largest fund manager in the world, Bill Gross, is trying to convert his bond fund into a stock fund (read article). I can’t imagine why Mr. Gross would want to do that (see PIMCO article), but maybe Skip knows? You know, after Skip sold us that high commission annuity and Class-A mutual fund with that 6.25% load, he decided to take his wife, kids, parents, and in-laws to Tahiti for the holidays.”

“Well anyway, I just read the largest fund manager in the world, Bill Gross, is trying to convert his bond fund into a stock fund (read article). I can’t imagine why Mr. Gross would want to do that (see PIMCO article), but maybe Skip knows? You know, after Skip sold us that high commission annuity and Class-A mutual fund with that 6.25% load, he decided to take his wife, kids, parents, and in-laws to Tahiti for the holidays.”

![]() “Oh I know, Skip is such a nice young man, and so thoughtful.”

“Oh I know, Skip is such a nice young man, and so thoughtful.”

![]() “You’re right Pumpkin, I just wish we could hear from him more than once every two years.”

“You’re right Pumpkin, I just wish we could hear from him more than once every two years.”

![]() “That’s right Snookum, but at least we get to talk to him when he drops off the paperwork, and his secretary is sure nice.”

“That’s right Snookum, but at least we get to talk to him when he drops off the paperwork, and his secretary is sure nice.”

![]() “What I really like about Skip is that he always makes so much common sense – he always tells us to buy investments that have already done really well like bonds and gold.”

“What I really like about Skip is that he always makes so much common sense – he always tells us to buy investments that have already done really well like bonds and gold.”

![]() “Exactly Buford. I just wonder how much longer it will take for stocks to become popular again, given the stock market is already up about 100% from the beginning of 2009? Perhaps with another +30% or so, maybe Skip will switch all our money out of bonds back into stocks?”

“Exactly Buford. I just wonder how much longer it will take for stocks to become popular again, given the stock market is already up about 100% from the beginning of 2009? Perhaps with another +30% or so, maybe Skip will switch all our money out of bonds back into stocks?”

![]() “What I love even more about Skip is that not only does he have us buy the popular investments, but he really protects us from buying the low-priced investments that are selling at bargain prices.”

“What I love even more about Skip is that not only does he have us buy the popular investments, but he really protects us from buying the low-priced investments that are selling at bargain prices.”

![]() “I hear you Muffin – come to think of it, maybe I should return that sweater I recently purchased at Marshall’s for 50% off – there may be an awful reason I do not know about.”

“I hear you Muffin – come to think of it, maybe I should return that sweater I recently purchased at Marshall’s for 50% off – there may be an awful reason I do not know about.”

![]() “Good idea Sweet Pea. The other thing I love about Skip is that he is so knowledgeable…he says the exact same thing I hear from those smart news people on TV. Good thing we have a reliable professional to protect our entire life savings.”

“Good idea Sweet Pea. The other thing I love about Skip is that he is so knowledgeable…he says the exact same thing I hear from those smart news people on TV. Good thing we have a reliable professional to protect our entire life savings.”

![]() “You’re right as usual dear. He may only have a high school GED, but we’re lucky he has these fancy letters behind his name that I never heard of like PFS, AFC, and RFC… those must be some important credentials.”

“You’re right as usual dear. He may only have a high school GED, but we’re lucky he has these fancy letters behind his name that I never heard of like PFS, AFC, and RFC… those must be some important credentials.”

![]() “I feel better after our conversation. Maybe we’ll hear from Skip, and if not, I’m sure he’ll drop-off some paperwork for a new investment, if our portfolio goes down by another 10%.”

“I feel better after our conversation. Maybe we’ll hear from Skip, and if not, I’m sure he’ll drop-off some paperwork for a new investment, if our portfolio goes down by another 10%.”

The Wake-Up Reality

I make some of these comments with tongue firmly in cheek, but the fact remains we live in a financial world with a structurally flawed system of loosely regulated, banks, brokerage firms, insurance companies, ratings agencies, hedge funds, mutual funds, and other financial institutions that continue to repeatedly place their interests ahead of clients. If the 2008-2009 financial crisis hasn’t taught you anything, then you should realize it behooves you to take control of your financial situation. At least ask tough questions that result in answers you can understand – not a lot of technical mumbo-jumbo that makes an advisor sound smart. Make life easier on yourself and have a blunt wake-up call conversation, otherwise grab a pen and get ready for Skip’s call – he’s about to come over with some more paperwork.

Related articles:

Beating off the Financial Sharks

Fees, Exploitation and Confusion Hammer Investors

Investment Credentials: The Letter Shell Game

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in TJX, or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

ETF Slam Dunk: Mixing Jordan & Rodman

Players in the same game may use different strategies in the hunt for success. Take five-time NBA champ Dennis “The Worm” Rodman vs. Hall of Famer and fourteen-time All-Star Michael Jordan. Rodman’s bad-boy antics, tattoos, and loud hair colors more closely resemble the characteristics of a brash trader or quick-trigger hedge fund manager, which explains why Rodman played for five different NBA teams. Jordan on the other-hand was less impulsive, and like a long-term investor, held a longer term horizon with respect to team loyalty – he spent 13 seasons with one team (Chicago Bulls), excluding a brief, half-hearted return to the Washington Wizards. Despite their differences, they shared one common goal…the ambition to win.

In the investment world, traders and long-term investors in many cases could be even more different than Rodman and Jordan…just think Jim Cramer and Warren Buffett. But when it comes to the exploding trend of Exchange Traded Funds (ETFs) expansion, traders and investors of all types share the common appreciation for lower costs (management fees and trading commissions). Beyond the lower costs, ETFs also offer a wide and growing range of liquid exposures, regardless of whether a trader wants to hold the ETF for five hours or an investor wants to own it for five years. The benefits of low cost and liquidity, relative to traditional actively managed mutual funds, are two key reasons why this market has blossomed to $822 billion in size and is still strengthening at a healthy clip.

Source: SPDR

The flight to bonds and out of equities has been well documented (see chart below), but underneath the surface is a migrating investor trend out of active managers, and into lower cost vehicles for equity exposure (ETFs and Index Funds). The poster child beneficiary of this movement is the Vanguard Group (based in Valley Forge, Pennsylvania), which manages $1.4 trillion in fund assets, including $112 billion in ETFs (Bloomberg). Equity heavy fund management companies like Janus Capital Group Inc. (JNS) and T. Rowe Price Group Inc. (TROW) have felt the brunt of the pain from the disinterested investing public.

Source: Iacono Research

The migration away from expensive actively managed funds has created a cut-throat dog-fight for ETF market share. Competition has gotten so bad that discount brokerage firms like Fidelity Investments ($1.25 trillion in mutual fund assets) and Charles Schwab Corp. (SCHW) have begun offering free ETF trading. Just two days ago Schwab also purchased Windward Investment Management, Inc. (~$3.9 billion in assets under management), for $150 million in stock and cash.

At the end of the day, money goes where it is treated best. Irrespective of differences between long-term investors and short-term traders, the lower costs and improved liquidity associated with ETFs have shifted money away from more costly, actively traded mutual funds. At my firm, Sidoxia Capital Management, I choose to use a diversified hybrid approach via my Fusion investment products (Conservative, Moderate, and Aggressive). Fusion integrates low-cost, tax-efficient investment vehicles and strategies, including fixed income securities (including funds & ETFs), individual stocks, and equity ETFs. Regardless of the differing preferences of hair colors and tattoos, my bet is that Dennis Rodman and Michael Jordan could agree on the importance of two things…winning games and using ETFs.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in JNS, TROW, SCHW or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investment Credentials: The Letter Shell Game

Photo Source: Imetco.com

In most professional industries – whether you are talking about a doctor, lawyer, dentist, accountant, or other respected field – a comprehensive and rigorous multi-year schooling and examination process is required to gain entrance into the club. Unfortunately for those working with professionals (I use the term loosely) in the investment and insurance fields, all that most advisors need to do is have a pulse and spend a few hours or days studying for an exam. Our structurally flawed and loosely cobbled together financial regulatory system is like a shell game that is constantly moving and hiding different conflicts of interest.

Left in the wake of the financial crisis, the public has been left picking up the pieces from the rating agency conflicts, Madoff scandal, Lehman Brothers bankruptcy, AIG collapse, Goldman Sachs hearings, golden parachute bonuses, billions in fees, commissions, and investor losses. Rather than watch the backs of investors, the system has favored financial institutions and penalized investors with fees, commissions, transactions costs, fine print, and layers of conflicts of interests. Andy Warhol described the amassing of fees like the prices of art – under both circumstances you collect “anything you can get away with.” So unless investors do their own thorough homework, there’s a good chance they will end up with a failing grade.

One of the major deception components is the creation of many worthless, pathetic lettered credentials that in many cases are worth less than the paper or business cards they are written on. Now, I’m sure some of these multi-letter credentials are worth more than others, but as a practicing professional in the industry for more than 15 years, it feels like I come across some new three letter designation every week. I know I am not alone with my sentiments, because respected professionals and colleagues I work with chuckle at many of these lettered credentials, and like me, have no clue what they stand for. When receiving a new business card with some of these strange letters, I often don’t know if I should cover my mouth while I burst out laughing, or if I’m supposed to be genuinely impressed?

Perhaps for hardworking parents, like a Joe and Mary Smith, it may mean something, but unless a multi-year curriculum (for example, the CFA Chartered Financial Analyst or CFP® – Certified Financial Planning programs) is put behind the alphabet of letters on a business card, please do not be offended if I yawn. Investors deserve better and fairer representation from someone managing their life savings, much like they get from a MD performing a surgery, a JD protecting a proprietor’s business, a CPA shielding a tax return from the IRS, or a DDS performing a root canal.

While it may sound like I am demonizing the broker/salesmen/advisors that are swimming around in the investment waters looking for commission opportunities (see Financial Sharks article), I understand some of them have genuine intentions and do not purposely misrepresent their credentials. As a matter of fact, many of the brokerage firms that hire these individuals require them to add funny letters to their business card for marketing purposes.

Here is a list of finance-related credentials other than the aforementioned:

- AAMS (Accredited Asset Management Specialist)

- AFC (Accredited Financial Counselor)

- AWMA (Accredited Wealth Management Advisor)

- CAIA (Chartered Alternative Investment Analyst)

- CASL (Chartered Advisor for Senior Living)

- CCFC (Certified Cash Flow Consultant)

- CFS (Certified Fund Specialist)

- CIMA (Certified Investment Management Analyst)

- CIMC (Certified Investment Management Consultant)

- CMA (Certified Management Accountant)

- CMFC (Chartered Mutual Fund Counselor)

- CMT (Chartered Market Technician)

- ChFC (Chartered Financial Consultant)

- CCFC (Certified Cash Flow Consultant)

- CDFA (Certified Divorce Financial Analyst)

- CEBS (Certified Employee Benefit Specialist)

- CDP (Certified Divorce Planner)

- CLTC (Certified in Long Term Care)

- CLU (Chartered Life Underwriter)

- CPCU (Chartered Property Casualty Underwriter)

- CRPC (Chartered Retirement Planning Counselor)

- CTFA (Certified Trust and Financial Adviser)

- FRM (Financial Risk Manager)

- MSFS (Master of Science in Financial Services)

- PFS (Personal Financial Specialist – awarded by the American Institute of Certified Public Accountants (AICPA))

- QPFC (Qualified Plan Financial Consultant)

- REBC (Registered Employee Benefits Consultant)

- RFC (Registered Financial Consultant)

When it comes to these and other industry credentials I am open to being enlightened on the relative merits…I’m all ears. And even if you trust the CFP® and CFA designations as the gold standards in the investing field, holding those credentials alone are not sufficient to make someone a good adviser. However, until I gain a better understanding of the dozens of other confusing credentials, I will continue to scratch my head and wonder which ones are worth more than the others, and which ones are not worth squat.

Healing the Wounds

It will take a long time for the financial industry to gain back the trust of investors, but it will require a multi-prong effort from regulators, financial industry executives, and investors themselves (who need to do better homework). If we want to more specifically dissect the professional service industry, then why not form one certification for each segment –not dozens.

What’s more, rather than pulling the wool over the public’s eyes with meaningless titles and credentials, let’s establish a fiduciary duty and designation that is demanded of all investment professionals. Moreover, let’s make the filtering process more rigorous in weeding out the dead-weight before handing the precious keys over to a professional. Unless changes are made, the corrupt system will remain structurally flawed, ripe with conflicts of interest, and aggressive salesmen calling themselves professionals –even if meaningless credentials are flaunted around to garner fees and commissions from the unsuspecting public.

Not everyone in the industry is a crook, but make sure you follow the ball very closely, so you do not lose in the investment shell game.

Read the Partial List of Financial Service Credentials on the CFP® Website

Wade W. Slome, CFA, CFP® <— Don’t worry if you are not impressed by these letters…my wife and friends are not either!

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in Lehman/Barclays, GS, or AIG (but do own derivative position in subsidiary) or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Buy-Out Firms Shooting Blanks

Photo source: Photobucket

During the golden age of the mega-buyouts in the mid-2000s, when banks were lending like drunken sailors, and private equity firms were taking the practically free funding to shoot at almost every company in sight, it’s no wonder managers of these funds were “high-fiving” each other. Unfortunately for the participants, the music ended in 2007, and the heavy debt-loaded guns that previously were killing large elephant deals got replaced with harmless toy guns shooting blanks at phantom transactions.

Peter Morris, a former Morgan Stanley (MS) banker and author of the scornful report, “Private Equity, Public Loss,” took a critical eye at the industry pointing to the reasons these high risk-taking private equity firms are underperforming the S&P 500 significantly. Bolstering his underperformance assertions, Morris points to 542 deals in the Yale endowment that underperformed by -40% once fees were subtracted. The Center for the Study of Financial Innovation, which is affiliated with Morris, cites a 2005 paper by Steven Kaplan (University of Chicago), and Antoinette Schoar (Massachusetts Institute of Technology). The paper shows the average buy-out fund underperformed the S&P 500 index from 1980 – 2001.

Another factor that Morris feels should not be ignored relates to risk. Morris feels the excessive risk profiles associated with these private equity funds have not been adequately considered by many unknowing investors and public taxpayers. Pensioners are vulnerable to these underperforming, risk-adjusted returns, while unassuming taxpayers could also be on the hook if risky private equity bets go bad. Under certain scenarios these potentially rocky private equity investments could bring a financial institution to its knees and force governments to use taxpayer bailout money. The Financial Times features a $6.5 billion investment made by Terra Firma, which was subsequently written down to zero, to make its point about the inherent risk private equity plays in the overall financial system.

Heads We Win, Tails You Lose

What makes the purported underperformance more scathing is the fact that these funds should bear higher returns to compensate investors for the additional liquidity risk and leverage that is undertaken. Like hedge funds, most private equity funds charge a 2% management fee, and a 20% performance fee for results achieved above a certain hurdle rate. The problem, that many outside observers highlight, is that the private equity firms have very little skin in the game, for example as little as 2%. With not a lot of their own dough in the game, the fund managers have a built in incentive to swing for the fences, because a profit windfall will filter to them should they hit it big. Morris characterizes this conflict of interest as “heads we win, tails you lose.” Another knock against investors revolves around return calculations. The opacity surrounding returns makes private equity less attractive, since valuations are only truly accurately reflected upon sale, which often takes many years.

Have all these shortcomings scared off investors? Apparently not. Just recently Blackstone Group (BX) raised a new $13.5 billion fund, the firm’s 6th fund, fresh off of its 5th fund that raised a total of $20 billion. The focus of the new fund will be on Asia and North America. In the short-run, Europe will occupy less of the fund’s attention until the region’s economy recovers.

To the extent more of these studies garner traction, I’m sure the private equity industry will react with a forceful response, especially with billions in potential fees at stake. One thing is for sure, investors have become more demanding and shrewd post the financial crisis, so if private equity managers want to earn the rich fees of yesteryear, they will need to do better than shoot blanks.

Read The Financial Times Buy-Out Study Article

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MS, BX, Terra Firma or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Annuity Trap

Like the infamous Roach Motel, annuities allow investors to check-in while making it very difficult to check out. In many instances, getting out of annuities can be cost prohibitive (fees, charges, commissions, expenses, etc.), even if escaping these fee-laden products is in the investors’ best financial interest.

In an article dated April 13th, 2010, Jay Peroni warned others by outlining a typical annuity fee structure as follows:

- Mortality and Expense Charge 1.50%

- Sub Account Management Fees 1.00%

- Unreported trading costs 0.78%

- Annual Administrative Expenses 0.15%

TOTAL ANNUAL EXPENSES 3.43%

What aren’t included in these numbers above are the surrender charges, which effectively can lock you into the annuity if you are averse to paying hefty surrender charges. Normally, the surrender charges vary from up to a 10% charge for large withdrawals in year one, decreasing to something like 1% in year 10. Worth noting, steep sales commissions can be layered on top of the previous charges or mysteriously embedded in the fee structure categories above.

The Big Sell

Driving the push for these 3%+ annual fees are lucrative financial institutions hiring aggressive salespeople. Typically annuities are sold under the guise of safe tax shelter investments. What the broker won’t tell you is that only a fraction (“exclusion ratio”) of the annuity payments is shielded from taxes, and the rest of the payments are taxed at the higher, unfavorable ordinary income tax rate (relative to qualified dividends and capital gains from other securities). Much of the time, many of the salespeople, who call themselves “financial advisors,” know little about these complex annuity products (see Financial Sharks article). What these brokers do understand are the big, fat commissions they stand to collect upon fleecing unsuspecting investors.

Scores of these so-called advisors are actually “registered representatives” who do not carry a fiduciary duty (meaning they are NOT required to make investment decisions in the best interest of their clients). Certainly, there are some situations where annuities might be appropriate, but from my experience there are very few cases where the egregious charges and expenses outweigh the benefits. I believe the vast majority of brokers/registered reps/salespeople are more concerned about padding their wallets than building and protecting client portfolios.

The Alternatives

If safety and tax advantages are features you are looking for then I encourage you to look at more efficient options such as the following:

- 401k Defined Contribution Retirement Plan (or other “Qualified Plan”): Allows you to achieve tax deferral often with free money given to you in the form of a match to your contributions.

- IRA (Individual Retirement Account): Whether you consider a traditional or Roth IRA, there are tax deferral advantages with lower fees.

- Low Turnover, High Dividend Portfolios: Using a tax efficient management strategy with better tax treatment of income is another approach that I firmly believe will outperform most annuities.

- Tax-Exempt Muni Bonds or Corporates: The tax-exempt status of municipal bonds affords investors a tax advantaged status. The after-tax yield on corporate bonds can be compared to the returns promised on annuities (AFTER all fees, charges, and commissions). Holding individual bonds until maturity can help avoid interest rate risk.

- Ladder Zero Coupon Bonds: If safe fixed payments are what you are looking for, then staggered purchases of zero coupon bonds can be purchased as well.

These are only a few options that could and should be considered when reviewing your personal objectives and circumstances. With regard to the insurance component of an annuity contract, there are more cost effective ways of paying for insurance – most notably, term insurance.

At the end of the day, no matter the financial product, it is important you understand the underlying fees charged on any strategy, along with how the person selling you stuff is compensated. If you don’t do your homework on these extremely complex products (many not regulated by the NASD or SEC), then you may find yourself checking into the annuity hotel, but unable to check out.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Membership Privileges: Cheese Tubs & Space Travel

With Senate proposals pushing to cap debit card fees earned by the credit card companies (Visa Inc. [V] and MasterCard Inc. [MA]), you better hurry up and take advantage of underappreciated membership privileges while you still can. The card companies are not too happy, but maybe they deserve some legitimate sympathy. I mean, supporting banks that gouge customers at rates reaching upwards of 20% can be challenging for any card network oligopoly to handle. So before Congress strips away the card companies’ God-given right to siphon away fees from millions of Americans, you have the obligation to utilize the membership privileges of your credit card – even if those benefits include using Visa’s concierge services for purchasing a giant tub of nacho cheese or booking a space travel trip. Unfortunately, many cardholders are unaware they carry the power of a personal servant in their wallet or purse. Tim Ferriss, creator of Experiments in Life Design, on the other hand chose to repeatedly use his personal servant to handle some of the most mission critical responsibilities you could imagine…for example:

1) Punch Bowl Tub of Cheese: Ferriss didn’t make his request for a tub of cheese completely uncompromising, but rather he was flexible in his demands. When the Visa concierge, David, asked Ferris what size cheese container he wanted, Ferriss reasonably responded, “Can, jar, tub, I don’t care. I just want liquid cheese, and a lot of it.”

2) Crossword Magicians: Why get flustered with a USA Today crossword clue (“Blue Grotto Locale”) when you can simply ring Maurice, your trusty Visa crossword concierge to solve the puzzle? Ferris used this approach and found the method much classier than using a computer or phone to find the answer. The answer to 62 across: ISLE OF CAPRI.

3) Feeling Blue? No problem, daily affirmations are just a few keypad strokes away from your fingertips. Getting told he was “good enough” by Jamie the concierge was a little ambitious, but Ferriss was satisfied by receiving a third party affirmation service along with a gratuitous note from Jamie letting him know what a good person he was.

4) Going Galactic: Now that he was getting warmed up, Ferriss had loftier goals (no pun intended). Specifically he requested the concierge to “book a trip to space.” Ferriss was not let down – the Visa Signature concierge came through with a $200,000 price quote from Virgin Galactic.

5) Looking at Limitations: Overall, the concierge service delivered on its mission of fielding random requests and answering questions. Nonetheless, Visa Signature needed a little more time to complete a self assessment of the services Visa could NOT perform (e.g., plan a wedding, call a friend, or write an article). Eventually Ferriss received an adequate response and went on to complete his prank-a-thon.

Believe it or not, some financial institutions provide services to you without charging you an arm and a leg. Maybe the card companies already have enough arms and legs to keep themselves content, but given political pressure on Visa and MasterCard, you better book that space flight and place that cheese tub order ASAP.

Read Full Tim Ferriss Article on Concierge Services (post was originally published on Credit Card Chaser)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in V, MA, Virgin, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}