Posts tagged ‘fee-only advisor’

Inflating Dollars & Deflating Footballs

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (February 2, 2015). Subscribe on the right side of the page for the complete text.

In the weeks building up to Super Bowl XLIX (New England Patriots vs. Seattle Seahawks) much of the media hype was focused on the controversial alleged “Deflategate”, or the discovery of deflated Patriot footballs, which theoretically could have been used for an unfair advantage by New England’s quarterback Tom Brady. While Brady ended up winning his record-tying 4th Super Bowl ring for the Patriots by defeating the Seahawks 28-24, the stock market deflated during the first month of 2015 as well. Similar to last year, the stock market has temporarily declined last January before surging ahead +11.4% for the full year of 2014. It’s early in 2015, and investors chose to lock-in a small portion of the hefty, multi-year bull market gains. The S&P 500 was sacked for a loss of -3.1% and the Dow Jones Industrial index by -3.7%.

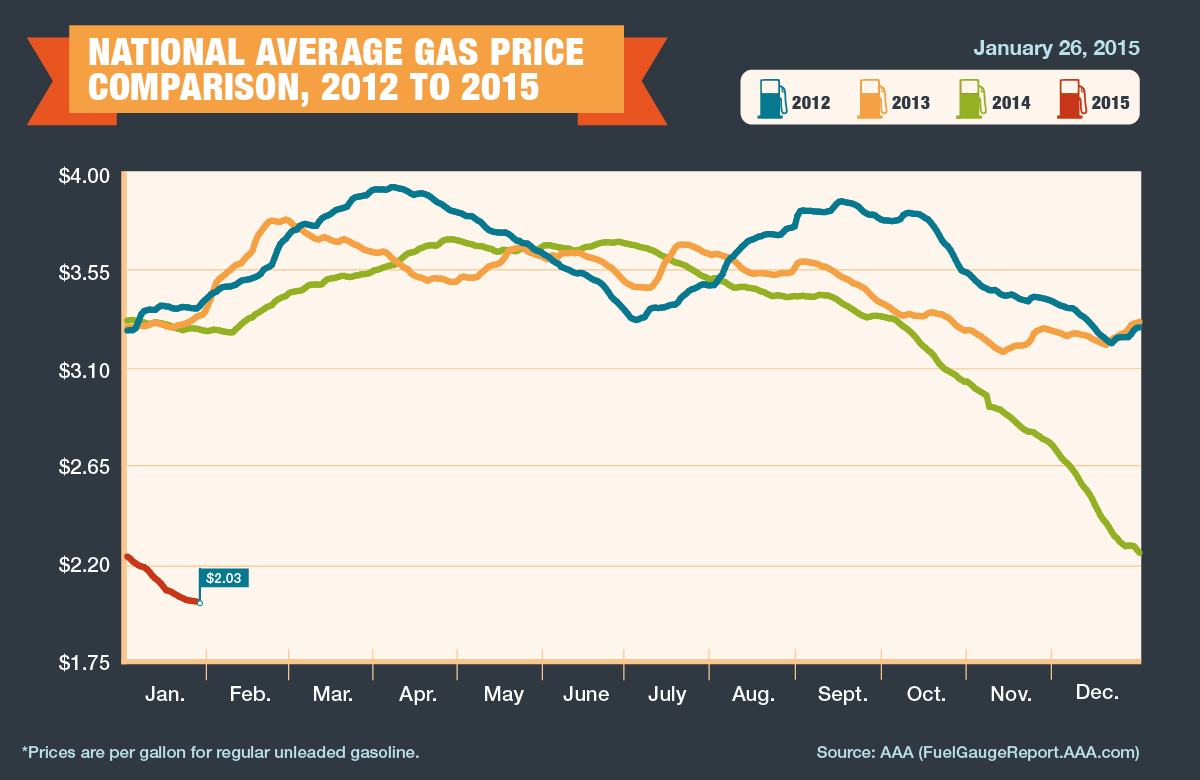

Despite some early performance headwinds, the U.S. economy kicked off the year with the wind behind its back in the form of deflating oil prices. Specifically, West Texas Intermediate (WTI) crude oil prices declined -9.4% last month to $48.24, and over -51.0% over the last six months. Like a fresh set of substitute legs coming off the bench to support the team, the oil price decline represents an effective $125 billion tax cut for consumers in the form of lower gasoline prices (average $2.03 per gallon nationally) – see chart below. The gasoline relief will allow consumers more discretionary spending money, so football fans, for example, can buy more hot dogs, beer, and souvenirs at the Super Bowl. The cause for the recent price bust? The primary reasons are three-fold: 1) Sluggish oil demand from developed markets like Europe and Japan coupled with slowing consumption growth in some emerging markets like China; 2) Growing supply in various U.S. fracking regions has created a temporary global oil glut; and 3) Uncertainty surrounding OPEC (Organization of Petroleum Exporting Countries) supply/production policies, which became even more unclear with the recent announced death of Saudi Arabia’s King Abdullah.

Source: AAA

More deflating than the NFL football’s “Deflategate” is the approximate -17% collapse in the value of the euro currency (see chart below). Euro currency matters were made worse in response to European Central Bank’s (ECB) President Mario Draghi’s announcement that the eurozone would commence its own $67 billion monthly Quantitative Easing (QE) program (very similar to the QE program that Federal Reserve Chairwoman Janet Yellen halted last year). In total, if carried out to its full design, the euro QE version should amount to about $1.3 trillion. The depreciating effect on the euro (and appreciating value of the euro) should help stimulate European exports, while lowering the cost of U.S. imports – you may now be able to afford that new Rolls-Royce purchase you’ve been putting off. What’s more, the rising dollar is beneficial for Americans who are planning to vacation abroad…Paris here we come!

Source: XE.com

Another fumble suffered by the global currency markets was introduced with the unexpected announcement by the Swiss National Bank (SNB) that decided to remove its artificial currency peg to the euro. Effectively, the SNB had been purchased and accumulated a $490 billion war-chest reserve (Supply & Demand Lessons) to artificially depress the value of the Swiss franc, thereby allowing the country to sell more Swiss army knives and watches abroad. When the SNB could no longer afford to prop up the value of the franc, the currency value spiked +20% against the euro in a single day…ouch! In addition to making its exports more expensive for foreigners, the central bank’s move also pushed long-term Swiss Treasury bond yields negative. No, you don’t need to check your vision – investors are indeed paying Switzerland to hold investor money (i.e., interest rates are at an unprecedented negative level).

In addition to some of the previously mentioned setbacks, financial markets suffered another penalty flag. Last month, multiple deadly terrorist acts were carried out at a satirical magazine headquarters and a Jewish supermarket – both in Paris. Combined, there were 16 people who lost their lives in these senseless acts of violence. Unfortunately, we don’t live in a Utopian world, so with seven billion people in this world there will continue to be pointless incidences like these. However, the good news is the economic game always goes on in spite of terrorism.

As is always the case, there will always be concerns in the marketplace, whether it is worries about inflation, geopolitics, the economy, Federal Reserve policy, or other factors like a potential exit of Greece out of the eurozone. These concerns have remained in place over the last six years and the stock market has about tripled. The fact remains that interest rates are at a generational low (see also Stretching the High Yield Rubber Band), thereby supplying a scarcity of opportunities in the fixed income space. Diversification remains important, but regardless of your time horizon and risk tolerance, attractively valued equities, including high-quality, dividend-paying stocks should account for a certain portion of your portfolio. Any winning retirement playbook understands a low-cost, globally diversified portfolio, integrating a broad set of asset classes is the best way of preventing a “deflating” outcome in your long-term finances.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

One Size Does Not Fit All

When you go shopping for a pair of shoes or clothing what is the first thing you do? Do you put on a blindfold and feel for the right size? Probably not. Most people either get measured for their personal size or try on several different outfits or shoes. When it comes to investments, the average investor makes uninformed decisions and in many instances relies more on what other advisors recommend. Sometimes this advice is not in the best interest of the client. For example, some broker recommendations are designed to line their personal pockets with fees and/or commissions. In some cases the broker may try to unload unpopular product inventory that does not match the objectives and constraints of the client. Because of the structure of the industry, there can be some inherent conflicts of interest. As the famous adage goes, “You don’t ask a barber if you need a haircut.”

Tabulate Inventory

A more appropriate way of managing your investment portfolio is to first create a balance sheet (itemizing all your major assets and liabilities) individually or with the assistance of an advisor (see “What to Do” article) – I recommend a fee-only Registered Investment Advisor (RIA)* who has a fiduciary duty towards the client (i.e., legally obligated to work for the best interest of the client). Some of the other major factors to consider are your short-term and long-term income needs (liquidity important as well) and your risk tolerance.

Risk Appetites

The risk issue is especially thorny because the average investor appetite for risk changes over time. Typically there is also a significant difference between perceived risk and actual risk.

For many investors in the late 1990s, technology stocks seemed like a low risk investment and everyone from cab drivers to retired teachers wanted into the game at the exact worst (riskiest) time. Now, as we have just suffered through the so-called Great Recession, the risk pendulum has swung back in the opposite direction and many investors have piled into what historically has been perceived as low-risk investments (e.g., Treasuries, corporate bonds, CDs, and money market accounts). The problem with these apparently safe bets is that some of these securities have higher duration characteristics (higher price volatility due to interest rate changes) and other fixed income assets have higher long-term inflation risk.

Source (6/30/09): Morningstar Encorr Analyzer (Ibbotson Associates) via State Street SPDR Presentation

A more objective way of looking at risk is by looking at the historical risk as measured by the standard deviation (volatility) of different asset classes over several time periods. Many investors forget risk measurements like standard deviation, duration, and beta are not static metrics and actually change over time.

Diversification Across Asset Classes Key

Source: State Street Global Advisors (June 30, 2009)

Correlation, which measures the price relationship between different asset classes, increased dramatically across asset classes in 2008, as the global recession intensified. However, over longer periods of time important diversification benefits can be achieved with a proper mixture of risky and risk-free assets, as measured by the Efficient Frontier (above). Conceptually, an investor’s main goal should be to find an optimal portfolio on the edge of the frontier that coincides with their risk tolerance.

Tailor Portfolio to Changing Circumstances

In my practice, I continually run across clients or prospects that initially find themselves at the extreme ends of the risk spectrum. For example, I was confronted by an 80 year old retiree needing adequate income for living expenses, but improperly forced by their broker into 100% equities. On the flip side, I ran into a 40 year old who decided to allocate 100% of their retirement assets to fixed income securities because they are unsure of stocks. Both examples are inefficient in achieving their different investment objectives, yet there are even larger masses of the population suffering from similar issues.

In my practice, I continually run across clients or prospects that initially find themselves at the extreme ends of the risk spectrum. For example, I was confronted by an 80 year old retiree needing adequate income for living expenses, but improperly forced by their broker into 100% equities. On the flip side, I ran into a 40 year old who decided to allocate 100% of their retirement assets to fixed income securities because they are unsure of stocks. Both examples are inefficient in achieving their different investment objectives, yet there are even larger masses of the population suffering from similar issues.

Financial markets and client circumstances are constantly changing, so the objectives of the portfolio should be periodically revisited. One size does not fit all, so it’s important to construct the most efficient customized portfolio of assets that meets the objectives and constraints of the investor. Take it from me, I’m constantly re-tailoring my wardrobe (like my investments) to meet the needs of my ever-changing waistline.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: For disclosure purposes, Sidoxia Capital Management, LLC is a Registered Investment Advisor (RIA) certified in the State of California. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}