Posts tagged ‘farming’

Rise of the Robots

We’re losing our jobs to robots, and they will destroy our economy. It makes for a great news soundbite, but has no factual basis in reality, if you look at the actual trajectory of automation and technology innovations throughout history. The global economy did not collapse when the steam engine replaced the oar; the automobile supplanted the horse; the computer became a substitute for the abacus; and the combine killed off the farmer. The same notion holds true today as robots become more ubiquitous in our daily commercial and personal lives.

From the early, post-revolutionary birth of our country in the 18th century, the agrarian economy accounted for upwards of 90% of jobs and financial activity…until farming technology evolved (see chart below). As new agricultural advancements were introduced, like the cotton gin, plow, scythe, chemical fertilizers, tractors, combine harvesters, and genetically engineered seeds, human capital (jobs) were redeployed into other growth sectors of the economy (e.g., factories, aerospace, semiconductors, medicine, etc.).

Source: Carpe Diem

Given that human labor accounts for about 2/3 of an average company’s expense structure, it should come as no surprise that corporations are looking to reduce costs by introducing more robotics and automation into their processes. The advantages to robotics adoption are numerous and I describe many of the reasons in my article, Chainsaw Replaces Paul Bunyan:

A robot won’t ask for a raise; it always shows up on time; you don’t have to pay for its healthcare; it can work 24/7/365 days per year; it doesn’t belong to a union; dependable quality consistency is a given; it produces products near your customers; and it won’t sue for discrimination or sexual harassment.

At Sidoxia Capital Management we opportunistically identified this growing trend quite early as evidenced by our initial 2012 investment in KUKA AG (Ticker: KUKAF), a German manufacturer of industrial robots. KUKA has recently made headlines due to a bid received from Chinese home-appliance company (Midea Group: Ticker – 000333.SZ) that values the dominant German robotics leader at $5 billion. Despite KUKA’s +273% share price appreciation from the end of 2012, not many people have heard of the company. While KUKA may not have caught the attention of many U.S. investors, the company has captured a bevy of blue-chip global customers, including Daimler, Airbus Group, Volkswagen, Fiat, Boeing, and Tesla.

Rather than sitting on its hands, KUKA has done its part to develop a higher profile. In fact, President Barack Obama and German Chancellor Angela Merkel recently received a robotics demonstration from KUKA’s CEO Till Reuter at the world’s largest industrial technology trade fair in Hannover, Germany this April (picture below)

Source: Bloomberg

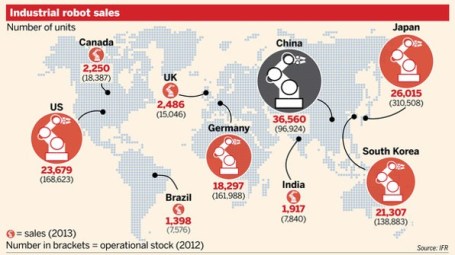

The recent multi-billion dollar bid by Midea Group has turned some onlookers’ heads, but what the potential deal really signals is the vast opportunity for robotics expansion in Asia. Rising labor costs in China, coupled with the enormous efficiency benefits of automation, have pushed China to become the largest purchasing country of robots in the world, ahead of the U.S., Japan, Korea and Germany (see chart below). However, according to the International Federation of Robotics (IFR), in 2015, Japan remained the country with the largest number of installed robots. IFR does not expect Japan to remain the “king” of the installed robotics hill forever. Actually, IFR estimates China will leapfrog Japan over the next few years to become both the largest purchaser of robots, along with maintaining the largest installed base of robots.

Source: Financial Times

In the coming months and years, there will be a steady stream of sensationalist headlines talking about the rise of the robots, and the destruction of jobs. We’ve repeatedly seen this movie before throughout history. Rather than a scary bloodbath ending, over the long-run we’ll likely see another happy ending. Any potential job losses will likely be outweighed by productivity gains, coupled with the benefits associated with more efficiently deployed labor to new growth sectors of the economy.

Even KUKA realizes the automation dynamics of the 21st century will serve as a net labor enhancer not detractor. If you don’t believe me, just ask Timo Boll, world champion table tennis player, who tested this theory vs. a KUKA robot (see video below). Ultimately, the rise of robots will lead to the rise of global growth and productivity.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), KUKAF, BA, and TSLA, but at the time of publishing had no direct position in Daimler, Airbus Group, Volkswagen, Fiat Chrysler, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Magical Growth through Manufacturing Decline

In a data driven world, we can never get enough numbers. The market magicians and the media machines have no problem overhyping or overselling the importance of each pending data-point. With a quick economic sleight of hand, the industry pundits have converted the average investor into a frothing Pavlovian dog, begging for another market shaking statistic. One of the supposed earth-rattling data points is the monthly ISM Manufacturing Index figure, but the release of the ISM number alone isn’t enough for the audience. The real fun comes in determining whether the monthly number registers above or below a schizophrenic 50 level – a number above 50 indicates the manufacturing economy is generally expanding (August came in at 50.6).

The trick can often be surprising, but more surprising to me is the importance placed on this relatively small, disappearing segment of our economy. With the manufacturing sector now accounting for just 11-13% of GDP (see also Manufacturing – Losing Out?), shouldn’t we be focusing more on the “Services” sector of the economy, which accounts for roughly 75% of our country’s output, up from 62% in 1971 (source: Earthtrends). I believe economist Mark Perry at Carpe Diem captured this phenomenon best in his post from earlier this year (Decline of Manufacturing – The World is Much Better Off ):

The fact of the matter is that manufacturing has been declining as a percentage of GDP over the decades just as the broader economy has seen massive growth. While manufacturing got chopped in half, as a percentage of GDP, from 1970 to 2011 we have seen GDP balloon from about $1 trillion to $15 trillion. If manufacturing declined by another 50% of GDP, I’d do cartwheels to see another 15x increase in economic expansion. I acknowledge the existence of certain synergies between product development and product manufacturing, but these benefits must be weighed against higher domestic costs that could make sales potentially unviable.

The fact of the matter is that manufacturing has been declining as a percentage of GDP over the decades just as the broader economy has seen massive growth. While manufacturing got chopped in half, as a percentage of GDP, from 1970 to 2011 we have seen GDP balloon from about $1 trillion to $15 trillion. If manufacturing declined by another 50% of GDP, I’d do cartwheels to see another 15x increase in economic expansion. I acknowledge the existence of certain synergies between product development and product manufacturing, but these benefits must be weighed against higher domestic costs that could make sales potentially unviable.

Déjà Vu All Over Again

This isn’t the first time in our country’s history that we’ve experienced explosive economic growth as legacy segments of the economy decline in relative importance. Consider the share of jobs agriculture controlled in the early 1800s – a whopping 90% of jobs were tied to farms (see chart below). Today, that percentage is less than 2% in the wake of the U.S. becoming the 20th Century global superpower. History has taught us that technology can be a bitch on employment, as robots, machinery, processes, and chemistry replace the demand for human labor. As Perry points out, there is no doubt that “tractors, electricity, combines, the cotton gin, automatic milking machinery, computers, GPS, hybrid seeds, irrigation systems, herbicides, pesticides” replaced millions of farming jobs, but guess what…American ingenuity ruled the day. As it turns out, those economic resources freed up by technology and productivity were redeployed into new, expanding, job-fertile areas of the economy like, “manufacturing, health care, education, business, retail, computers, transportation, etc.”

Source: Carpe Diem

More Apples or More GMs?

The farming lobby still cries for its inefficient, growth-muffling subsidies today, but many unproductive, unionized domestic manufacturing industries are also screaming for government assistance because cheap foreign labor and new technologies are stealing manufacturing jobs by the boatloads. So at the core, the real question is do we want government and investments supporting more companies like Apple Inc. (AAPL) or more companies like General Motors Company (GM)?

As you may know, by flipping over an iPhone, any observer can clearly notice the product is “designed by Apple in California – assembled in China.” It is clear that Apple and its customers value brains over manufacturing brawn. At $371 billion and the most valuable publicly traded stock in the universe, Apple is dominating the electronics world, all the while hiring employees by the thousands. These facts beg the question of whether Apple should revamp their manufacturing supply-chain back to the U.S. to save more domestic jobs? Of course the result of a manufacturing strategy shift to a higher cost region would make Apple less competitive, force them to charge consumers higher prices for Apple products, and open the door for competitors to freely steal market share? Would this strategy create more incremental jobs, or fewer jobs? I think I’ll side with the Steve Jobs philosophy of business, which says “more profitable businesses must fill more job openings.”

If this Apple case study isn’t illustrative enough for you, maybe you should take a look at companies like GM. The U.S. automobile industry has historically been notoriously mismanaged, thanks to a horrific manufacturing cost structure, anchored by unsustainable pension and healthcare costs. Should investors be surprised that an uncompetitive, bloated cost structure leaves companies like GM less money to invest in new products and innovation? This irrational cost management contributed to decades of market share losses to foreigners. If I’m the job creation czar in the U.S., I think I’ll choose the Apple path to job creation over GM’s route.

Global Competitiveness = Jobs

With a 9.1% unemployment rate and the recent introduction of the American Jobs Act, there has been plenty of emphasis and focus on job creation. At the end of the day, what will create durable, long-term job creation is innovative, competitively priced products and services that can be sold domestically and abroad. How do we achieve this goal? We need an education system that can teach and train a workforce sufficiently to meet the discerning tastes of a global marketplace. Government, on the other hand, needs to support (not direct) the private sector by investing in strategic areas to help global competitiveness (i.e., education, energy independence, basic research, infrastructure, entrepreneurial capital for business formation, etc.), while facilitating a business environment that incentivizes growth.

Regardless of the policy mixtures, the common denominator needs to be focused on improving global competitiveness. Excessive focus on a declining manufacturing sector and the monthly ISM data will only distract decision makers from the core issues. If the economic magician’s sleight of hand diverts investor attention for too long, we may see more jobs disappear.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and AAPL, but at the time of publishing SCM had no direct position in GM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page

{kind=link}