Posts tagged ‘Facebook’

Investors Slowly Waking to Technology Tailwinds

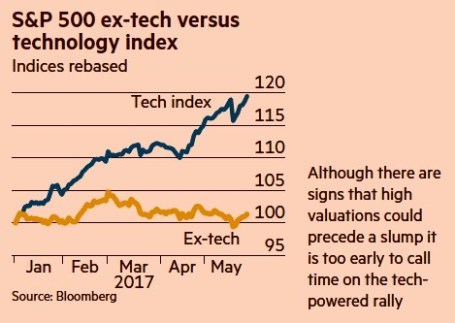

In recent years, investors have been overwhelmingly been distracted by geopolitical headlines and risk aversion caused by the worst financial crisis in a generation. In the background, the tailwinds of technological innovation have been silently gaining momentum. Although this topic is nothing new for Investing Caffeine followers, the outperformance of technology stocks has been pretty stunning in 2017 (see chart below), with the S&P 500 Technology sector rising almost +20% versus the Non-Tech sector eking out a little more than +1% return. Peered through the style lenses of Growth versus Value, technology’s contribution is also evident by the Russell 1000 Growth index’s 2017 outperformance over the Russell 1000 Value index by +11% (approximately +14% vs +3%, respectively).

Source: Bloomberg via The Financial Times

More specifically, what’s driving a significant portion of this outperformance? Robin Wigglesworth from The Financial Times highlighted a key contributing trend here:

“Facebook, Apple, Amazon and Netflix have all gained over 30 per cent this year, and Google is up 24 per cent. Their total market capitalisation now stands at $2.4 trillion. That makes them bigger than the French CAC 40 or Germany’s Dax, and nearly as large as the FTSE 100.”

Technology’s domination has been even more impressive since the cycle bottom of stock prices in 2009, if one contrasts the stark difference in the performance of the tech-heavy NASDAQ versus the more sector-balanced S&P 500. Over this timeframe, the NASDAQ has more than quadrupled in value and beaten the S&P 500 by more than +120%.

While the mass media likes to talk about technology bubbles, artificial money printing by global central banks, and imminent recessions, for years I have been highlighting the importance of the technology revolution and its beneficial impact on stock prices. Here are a few examples:

Technology Does Not Sleep in a Recession (2009)

Technology Revolution Raises Tide (2010)

NASDAQ and the R&D Tech Revolution (2014)

NASDAQ 5,000…Irrational Exuberance Déjà Vu? (2014)

The Traitorous 8 and Birth of Silicon Valley (2016)

As I have explained in many of my previous writings, the important factors of technology, globalization, and demographics have been the key driving forces behind the stock bull market and multi-decade decline in interest rates – not Quantitative Easing (QE) and/or rising debt levels.

Eventually, undoubtedly, euphoria and over-investment will lead to a cyclically-driven recession caused by excess capacity (supply exceeding demand). Regardless of the timing of future economic cycles, the continued multi-generational advance in new technological innovations will continue to drive economic growth, disinflation, improved standards of living, and higher stock prices. Until the animal spirits of the masses fully embrace this technological trend, Sidoxia and its clients will enjoy the tailwind of innovation as I continue to discover attractive investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FB, AAPL, AMZN, GOOG/L, certain exchange traded funds, and short position in NFLX, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Investing, Housing, and Speculating

We all know there was a lot of speculation going on in the housing market during 2005-2007 as risk-loving adventurists loaded up on NINJA loans (No Income, No Job, and No Assets) and subprime CDS (Credit Default Swap) securities. But there is a different kind of speculation going on now, and it isn’t tied directly to housing. Instead of buying a house with no down payment and a no interest loan, speculators are leaping into other hazardous areas of danger. Like a frog jumping from lily pad to lily pad, speculators are now hopping around onto money-chasing industries, including biotech, social media, Bitcoin, and alternative energy.

As French novelist Jean-Baptise Alphonse Karr noted, “The more things change, the more they stay the same.” Irrespective of the painful consequences of the bubble-bursting aftermaths, human behavior and psychology addictively succumb to the ever-seductive emotion of greed. Over the last 15 years, massive fortunes have been gained and lost while chasing frothy financial dreams in areas like technology, housing, and gold.

Most get-rich-quick dream chasers have no idea of how to invest in or value a stock, but they sure know a good story when they hear one. Chasing top performing stocks is lot like jumping off a bridge – anyone can do it, and it feels exhilarating until you hit the ground. However, there is a better way to create wealth. Despite rampant speculation, most individuals understand the principles behind buying a house, which if applied to stocks, can make you a superior investor, and assist you in avoiding dangerous, speculative investments.

Here are some valuable housing insights to improve your stock buying:

#1.) Price is the Almighty Variable: Successful real estate investors don’t make their fortunes by chasing properties that double or triple in value. Buying a rusty tool shed for $1 million makes about as much sense as Facebook paying $19 billion (1,000 x’s the estimated 2013 annual revenues) for a money-losing company, WhatsApp. Better to buy real estate when there is blood in the street. Like the stock market, housing is cyclical. Many traders believe that price patterns are more important than the actual price. If squiggly, technical price moving averages (see Technical Analysis article) make so much money for stock-renting speculators, then how come day traders haven’t used their same crossing-lines and Point & Figure software in the housing market? Yes, it’s true that the real estate transactions costs and illiquidity can be costly for real estate buyers, but 6% load fees, lockup periods, 20% hedge fund fees, and 9% margin rates haven’t stopped stock speculators either.

#2). Cash is King: It doesn’t take a genius to purchase a rental property – I know because practically half the people I know in Southern California own rental properties. For example, if I buy a rental property for $1 million cash, is it a good purchase? Well, it depends on how much after-tax cash I can collect by renting it out? If I can only net $3,000 per month (3.6% annualized return), and be responsible for replacing roofs, fixing toilets, and evicting tenants, then perhaps I would be better off by collecting 6.5% from a low-cost, tax-efficient exchange traded real estate fund, without having to suffer from all the headaches that physical real estate investing brings. Forecasting future asset price appreciation is tougher, but the point is, understanding the underlying cash flow dynamics of a company is just as important as it is for housing purchases.

#3). Debt/Leverage Cuts in Both Directions: Adding debt (or leverage) to a housing or stock investment can be fantastic if prices go up, and disastrous if prices go down. Putting a 20% down payment on a $1 million house works out wonderfully, if the price of the house increases to $1.2 million. My $200,000 down payment is now worth $400,000, or up +100%. The same math works in reverse. If the price of the home drops to $800,000, then my $200,000 down payment is now worth $0, or down -100% (ouch). Margin debt on an equity brokerage account works in a similar fashion, but usually a 50% down payment is needed (less risky than real estate). That’s why I always chuckle when many real estate investors tell me they steer clear of stocks because they are “too risky”.

#4). Growth Matters: If you buy a home for $1 million, is it likely to be worth more if you add a kitchen, tennis court, swimming pull, third floor, and putting green? In short, the answer is yes. The same principle applies to stocks. All else equal, if a company based in Los Angeles, establishes new offices in New York, London, Beijing, and Rio de Janeiro, and then acquires a profitable competitor at a discounted price, chances are the company will be much more valuable after the additions. The key concept here is that asset values are not static. Asset valuations are impacted in both directions, whether we are talking about positive growth opportunities or negative disruptions.

Overall, speculatively chasing performance is tempting, but if you don’t want your financial foundation to crumble, then build your successful investment future by sticking to the fundamentals and financial basics.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct discretionary position in FB, Bitcoin, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Market Expands and So Does Sidoxia’s Team

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (March 3, 2014). Subscribe on the right side of the page for the complete text.

After a brief pause at the beginning of the year, the stock market built on the tremendous gains of 2013 (S&P 500 up +30%) by reaching record highs again in February by expanding another +4.3% for the month. My investment management and financial planning firm, Sidoxia Capital Mangement, LLC, has been expanding as well. Just this last month, we added a key investment and financial planning professional (Keith C. Bong, CFA, CPA Press Release) with more than 25 years of experience in the fields.

The Record Setting Advance Continues

Now entering the sixth year of this record setting bull market, many investors and pundits have been surprised by the strength and duration of the advance. At the nadir of the financial crisis, the stock market reached a multi-year low of 666 on March 9, 2009. For comparison purposes, the S&P 500 recently closed at 1,845, almost tripling in value since the crisis lows. Pessimists and skeptics, who locked in losses during the crisis plunge, have watched the explosive gains while sitting on their hands. While I freely admit, the low-hanging fruit has been picked, many of the doubters are still calling for a collapse as “troubling news continues to pour in from all over the planet.” However, what the naysayers neglect to acknowledge is the fact that S&P 500 reported profits, the lifeblood of bull markets, have also tripled in value. Despite what the bears say, not everything is a speculative house of cards.

Late to the Party Because of Uncertainty

Although the stock party has lasted five years thus far, individuals have only begun buying for about one year (see ICI fund flows data in Here Comes the Dumb Money) – about +$28 billion of new money in 2013 and another +$12 billion so far this year (ICI data through February 19th). After approximately six years and -$600 billion in stock sales (2007-2012), it’s no wonder investors have been slow to reverse course. Adding to the angst, investors have been bombarded with an endless stream of political and economic concerns on a daily basis, leading to the late arrival of most individuals to the stock investing party. While it’s true that more people have joined the party in recent months, floods of investors are still waiting outside in the cold. Here are a few reasons for the tardiness:

- Geopolitical Concerns: Most recently it was Syria, Iran, and Argentina that got short-term traders chewing their fingernails…now it’s the Ukraine. Just yesterday, I had to spend about 10 minutes locating the Ukranian province of Crimea on a map. For those who have not been keeping track, after days of civil unrest that left some 75 protesters dead, Ukrainian President Viktor Yanukovych fled the capital city of Kiev and agreed with opposition leaders to reduce his powers and hold early presidential elections later this year. For context, in 1954, the former Soviet Union leader Nikita Khrushchev transferred Crimea from the Russian Soviet republic to Ukraine on the basis of economic ties that were closer with Kiev than with Moscow. Prior to that transfer, Russia seized Crimea from the declining Ottoman Empire in the 18th century. Fast forward to today, and fresh off a successful Olympics in Sochi, Russia, Russian President Vladimir Putin hasn’t been happy about the citizen uprising in neighboring Ukraine, so he has decided to flex his muscles and move Russian troops into Crimea. The situation is very fluid and the U.S., along with other global leaders, are crying foul. Time will tell if this situation escalates into a military conflict like the 2008 Georgia-Russia crisis, or if cooler heads prevail.

- Fed Policy Concerns: Federal Reserve Chair Janet Yellen gave her inaugural address last month before Congress, where she signaled continuity in policy with former Fed Chair Ben Bernanke. Indications remain strong that the reduction of bond buying stimulus (i.e., “tapering”) will continue in the months ahead, despite mixed economic results. The “Polar Vortex” occurring on the East Coast, coupled with a record draught on the West Coast contributed to the recent reduction of Q4-2013 GDP growth figures, which were revised lower to +2.4% growth (from +3.2%).

- Domestic Politics: In a sharply politically divided country like the U.S., is there ever a complete hugs & kisses consensus? In short, “no”. How can there be 100% agreement when sharply divisive issues like Obamacare, immigration, tax reform, entitlements, budgets, and foreign affairs are always in flux? Layer on a Congressional midterm election this November and you have a recipe for uncertainty.

Because of all this uncertainty, there are still literally trillions of dollars in cash sitting on the sidelines, waiting to come join the fun. But uncertainty is a relative term because there is always doubt surrounding geopolitics, economics, and Washington D.C. Sentiment moves like a pendulum from fear to greed. Eventually panic/fear sways back the other direction as business/consumer confidence overshadow the deep scarred emotions of 2008-09. As the stock markets have grinded to record highs, fear and skepticism have slowly begun to erode.

Sidoxia Uncertainty

Speaking of uncertainty, I too encountered many doubters and skeptics when I started my firm, Sidoxia Capital Management, LLC in early 2008. Great timing, I thought at the time, as our economy entered the worst recession and financial crisis in a generation and the walls of our nation’s financial system were caving in.

With virtually no company assets or revenues at the time, this was the backdrop as I embarked on my entrepreneurial journey. Seemingly secure investment banking pillars like Bear Stearns and Lehman Brothers, which each had been around for more than a century, crumbled within the blink of an eye. As bailouts were occurring left and right, in conjunction with recurring multi-hundred point collapses in the Dow Jones Industrial index, cynics would repeatedly ask me, “Wade it’s great that you have a lot of experience, but how are you going to gain clients?” It was a fair and reasonable question at the time, but perseverance and hard work have allowed Sidoxia to beat the odds. Publishing several books, conducting numerous media appearances, and gaining thousands of social media followers (InvestingCaffeine.com) hasn’t hurt in building Sidoxia’s brand either.

After achieving record growth in the first five years of the firm, Sidoxia more than doubled its assets under management again in 2013. More important than all of the previously mentioned achievements has been our ability to service our clients with a disciplined, customized process that has demonstrated strong long-term results and helped solidify our valued relationships.

A Few Party Animals Getting Reckless at the Stock Party

Success for Sidoxia or any investor has not come easy over the last six years. As I wrote in a Series of Unfortunate Events, we’ve had to navigate our clients’ investment assets through the following events and more:

- Flash Crash

- Debt Ceiling Debates-Brinksmanship

- U.S. Debt Downgrade

- European Recession

- Arab Spring – Tunisia, Libya, Egypt

- Greek Crisis and Potential Exit from EU

- Uncertain U.S. Presidential Elections

- Sequestration

- Cyprus Financial Crisis

- Income Tax Hikes

- Federal Reserve Tapering

- Syrian Civil War / Military Threat

- Government Shutdown

- Obamacare & Its Glitches

- Iranian Nuclear Threat

- Argentinian Currency Collapse

- Polar Vortex

- Ukrainian Instability

It is no small feat that stock markets have made new records in the face of these daunting concerns. But simply ignoring scary headlines won’t earn you an investing trophy. Successful investing also requires controlling temptation and greed. At a celebratory bash, there are always irresponsible party animals, just like there are always reckless speculators gambling in the financial markets. It certainly is possible to party responsibly without getting crazy during festivities and still have fun. Even though the majority of investors currently are behaving well, as substantiated by the reasonable P/E ratio being paid (15x’s estimated 2014 profits) there are a few foolish players. Pockets of speculative fervor can be found in several areas of the financial markets. Here are a few:

- Bitcoin Breakdown: The world’s largest Bitcoin exchanged filed for bankruptcy after it lost 750,000 Bitcoin units, worth about $477,000,000, based on current exchange rates. The popularity of this speculative virtual currency seems eerily similar to the great Dutch Tulip-Mania of the 1630s.

- Biotech Bliss: Ignorance is a bliss, and apparently so is buying biotech stocks. There’s no need to speculate on gold or Bitcoins when you can invest in the Biotechnology Index (BTK), which has already advanced +21% this year on top of a 51% gain in 2013. Over the last 5+ years, the index has more than quadrupled.

- Facebook Folly: WhatsApp with Facebook Inc’s (FB) $19 billion acquisition of the cellphone texting company? CEO Mark Zuckerberg is claiming he got a bargain by paying almost 1,000x’s the estimated annual revenue of WhatsApp ($20 million). When only a fraction of the 450 million users are paying for the service, I’m OK going out on a limb and calling this deal kooky.

- High Ticket Tesla: Tesla Motors Inc (TSLA) has become a cult stock. The company has a price tag of $30 billion despite burning $7 million in cash last year. The announcement of a $4-5 billion battery “Gigafactory” added to the company’s recent hype. To put things into perspective, General Motors (GM) has revenues 75x’s larger than Tesla and GM generated over $5 billion in 2013 free cash flow. Nevertheless, GM is only valued at 1.9x’s the market value of Tesla…head scratch.

- Social Media Silliness: Maybe not quite as wacky as the $19 billion price tag paid for WhatsApp, but the $30 billion value placed on Twitter Inc (TWTR) for a company that burned $30 million of cash in their most recent financial report is silly too. Yelp Inc (YELP) is another multi-billion valued company that is losing money. I love all these services, but great services don’t always make great stocks. Investors from the dot-com era vividly remember what happened to those overvalued stocks once the bubble burst.

Fear and greed are omnipresent, and some of these speculative areas may continue to appreciate in value. However, controlling or ignoring the powerful emotions of fear and greed will help you in achieving your financial goals. As the markets (and Sidoxia’s team) expand, our disciplined investment process should allow us to objectively identify attractive investment opportunities without succumbing to the pitfalls of panic-selling or performance-chasing.

Other Recent Investing Caffeine Articles:

Retirement Epidemic: Poison Now or Later?

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in FB, TWTR, YELP, TSLA, BTK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Broken Record Repeats Itself

Article is an excerpt from previously released Sidoxia Capital Management’s complementary June 2012 newsletter. Subscribe on right side of page.

Traditional music records have been replaced with CDs (compact discs) and digital downloads. Although the problem of a broken record repeating itself is no longer an issue, our financial markets have not conquered the problem of repetition. More specifically, the timing of the -6.3% stock market decline during May (as measured by the S&P 500 index), coincides with the same broken sell-offs we have temporarily experienced over the last two summers. First, we had the “Flash Crash” in the summer of 2010, and then the debt ceiling debate and credit downgrade of 2011.

So far, the “Sell in May and go away” mantra has followed the textbook lessons over the last few years, but as you can see from the chart below, the short-lived seasonal sell-offs have been followed by significant advances (up +33% from 2010 lows and up +29% from the 2011 lows). Given the global challenges, a two-steps forward, one-step back pattern in equity markets should not be seen as overly surprising by investors.

Source: Yahoo Finance

Although the late-spring and summer doldrums have not been a joy-ride in recent years, these overly simplistic seasonal trading rules of thumb have not been exceedingly reliable either. For example, even though the months of May in 2010-2012 produced negative returns, the previous 25 Mays going back to 1985 produced positive returns more than 2/3 of the time. Rather than fiddle with these unreliable, unscientific trading rules, individuals would be better served by listening to famous Jedi Master Yoda from Star Wars, who so astutely noted, “Uncertain, the future is.”

Voting Machines and Scales

Given the spread of globalization and technology, the speed of news dissemination has never been faster. With the 2008-2009 financial crisis still burned into investors’ minds, the default response to any scary news item is to shoot first and ask questions later. Renowned long-term investing legend Ben Graham famously highlighted, “In the short run the market is a voting machine. In the long run it’s a weighing machine.”

As it relates to short-run current events, here are some of the items that investors were voting on (no pun intended) this month:

Europe, Europe, Europe: This problem has been with us for some time now, and there are no signs it will disappear anytime soon. In a game of chicken between the EU (European Union) and Greek legislators, fresh elections are taking place on June 17th, which will ultimately determine if Greece will exit the Euro monetary union or stick to the bitter medicine of austerity prescribed by the key European decision-makers in Germany. As Greece attempts to clean up its own mess, European politicians and G-20 leaders around the globe are scrambling to create plans that ring-fence countries like Spain and Italy from succumbing to a Greek-born contagion.

Presidential Politics: If you haven’t been living in a cave for the last six months, you probably know that 2012 is a presidential election year. Regardless of your politics, there are big questions surrounding the economy, jobs, deficits, debt, taxes, entitlements, defense, gay marriage, and other important issues. Answers to many of these questions will remain unclear until we get closer to the elections. The financial markets do not like uncertainty, so probabilities would indicate volatility will remain par for the course for the foreseeable future.

Facebook Folly: Despite my warnings, Facebook’s initial public offering (IPO) failed to live up to the social media giant’s hype – the share price has fallen -22% since the shares originally priced. Great companies do not always make great stocks, especially when a relatively new kid on the block has his company’s stock initially valued at a hefty price-tag of more than a $100 billion. Finger pointing is being spread liberally on the botched Facebook deal (e.g., Morgan Stanley, NASDAQ, Facebook), but no need to shed a tear for 28-year-old founder Mark Zuckerberg since his ownership stake in the company is still valued at around $15 billion – enough to cover a European trip to McDonald’s with his newlywed wife.

Dimon in a Rough Spot: Jamie Dimon, the poster child of the banking industry (and CEO of JP Morgan Chase – JPM), dropped a bomb on the investment community earlier in the month by explaining how a rogue “whale” trader racked up $2 billion in initial losses (and growing) by taking excessive risk and throwing controls into the wind.

Chinese Dragon Losing Steam: The #2 global economy has been losing some steam as witnessed by slowing industrial production and GDP growth (Gross Domestic Product). In turn, the self correcting economic forces of supply and demand have provided relief to consumers and corporations in the form of lower fuel, energy, and commodity prices. Chinese leaders are not sitting still – there are plans of accelerating infrastructure spending and assisting banks in the form of capital injections and lower reserve requirements.

As I discussed in a previous Investing Caffeine article (see The European Dog Ate My Homework), although the current headlines remain gloomy, that will always be the case. Just a few years ago, Bear Stearns, Lehman Brothers, AIG, CDS (credit default swaps), and subprime mortgages were the boogeymen. In the 1980s, we had the Savings & Loan financial crisis and the infamous 1987 Crash. During the 1970s, the Vietnam War, Nixon’s impeachment proceedings, and rising inflation were the dominating issues. Since then, the equity markets are up over 20x-fold – time will always reward those patient long-term investors. Despite all the doom and gloom, stock markets have roughly doubled over the last three years and all the major indexes remain solidly in the black for the year. Choppy waters are likely to remain as we approach this year’s elections, but for those who understand broken records often repeat themselves, there’s a good chance the music will eventually sound much better.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including commodities, inflation protection, floating rate bonds, real estate, dividend, and alternative investment ETFs), but at the time of publishing SCM had no direct position in FB, MCD, JPM, MS, NDAQ, AIG, Lehman Brothers, Bear Stearns, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Box Wine, Facebook and PEG Ratios

I’m no wine connoisseur, but I do know I would pay more for a bottle of Dom Pérignon champagne than I would pay for a container of Franzia box wine. In the world of stocks, the quality disparity is massive too. In order to navigate the virtually infinite number of stocks, we need to have an instrument in our toolbox that can assist us in accurately comparing stocks across the quality spectrum. Thank goodness we have the handy PEG ratio (Price/Earnings to Growth) that elegantly marries the price paid for a stock (as measured by the P/E ratio) with the relative quality of the stock (as measured by its future earnings growth rate).

Famed investor Peter Lynch (see Inside the Brain of an Investing Genius) understood the PEG concept all too well as he used this tool religiously in valuing and analyzing different companies. Given that Lynch earned a +29% annual return from 1977-1990, I’ll take his word for it that the PEG ratio is a useful tool. As highlighted by Lynch (and others), the key factor in using the PEG ratio is to identify companies that trade with a PEG ratio of less than 1. All else equal, the lower the ratio, the better potential for future price appreciation. Facebook Vs. Eastman Kodak

To illustrate the concept of how a PEG ratio can be used to compare stocks with two completely different profiles, let’s start by answering a few questions. Would a rational investor pay the same price (i.e., Price-Earnings [P/E] ratio) for a company with skyrocketing profits as they would for a company going into bankruptcy? Look no further than the lofty expected P/E multiple to be afforded to the shares of the widely anticipated Facebook (FB) initial public offering (IPO). That same rational investor is unlikely to pay the same P/E multiple for a money losing company like Eastman Kodak Co. (EKDKQ.PK) that faces product obsolescence. The contrasting values for these two companies are stark. Some pundits are projecting that Facebook shares could fetch upwards of a 100x P/E ratio, while not too long ago, Kodak was trading at a P/E ratio of 4x. Plenty of low priced stocks have outperformed expensive ones, but remember, just because a “value” stock may have a lower absolute P/E ratio in the recent past, does not mean it will be a better investment than a “growth” stock sporting a higher P/E ratio (see Fallacy of High P/Es).

Price, Earnings, and Dividends

As I’ve written in the past, a key determinant of future stock prices is future earnings growth (see It’s the Earnings Stupid). The higher the P/E multiple, the more important future earnings growth becomes. The lower the future growth, the more important valuation and dividends become.

We can look at various money-making scenarios that incorporate these factors. If my goal were to double my money in 5 years (i.e., earn a 100% return), there are numerous ways to skin the profit-making cat. Here are four examples:

1) Buy a non-dividend paying stock of a company that achieves earnings growth of 15%/year and maintains its current P/E ratio over time.

2) Buy a stock of a company that has a 5% dividend and achieves earnings growth of 11%/year and maintains its current P/E ratio over time.

3) Buy a value stock with a 5% dividend that achieves earnings growth of 5%/year and increase its P/E ratio by 10% each year.

4) Buy a non-dividend paying growth stock that achieves earnings growth of 20%/year and decreases its P/E ratio by about 5% each year.

I think you get the idea, but as you can see, in addition to earnings growth, dividends and valuation do play a significant role in how an investor can earn excess returns.

Lynch’s Adjusted PEG

Peter Lynch added a slight twist to the traditional PEG analysis by accounting for the role of dividends in the denominator of the PEG equation:

PEG (adjusted by Lynch) = PE Ratio/(Earnings Growth Rate + Dividend Yield)

This “adjusted PEG” ratio makes intuitive sense under various perspectives. For starters, if two different companies both had a PEG ratio of 0.8, but one of the two stocks paid a 3% dividend, Lynch’s adjusted PEG would register in at a more attractive level of 0.6 for the dividend paying stock.

Looked at under a different lens, let’s suppose there are two lemonade stands that IPO their stocks at the same time, and both companies use the exact same business model. Moreover, let us assume the following:

• Lemonade stand #1 has a P/E of 14x and growth rate of 15%.

• Lemonade stand #2 has a P/E of 12x and growth rate of 8%, but it also pays a dividend of 3%.

Given this information, which one of the two lemonade stands would you invest in? Many investors see the lower P/E of Lemonade stand #2, coupled with a nice dividend, as the more attractive opportunity of the two. But as we can see from Lynch’s “adjusted PEG” ratio, Lemonade stand #1 actually has the lower, more attractive value (.9 or 14/15 vs 1.1 or 12/(8+3)).

This analysis may be delving into the weeds a bit, but this framework is critical nonetheless. Valuation and earnings projections should be essential components of any investment decision, and with record low interest rates, dividend yields are playing a much more important role in the investment selection process. Regardless of your purchase decision thought process, whether deciding between Dom Perignon and box wine, or Facebook and Kodak shares, having the PEG ratio at your disposal should help you make wise and lucrative decisions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in FB, EKDKQ.PK, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The $100 Billion Facebook Man

Source: Photobucket

If you don’t pay close enough attention, you may miss the Facebook initial public offering (IPO) in the blink of an eye. Since computer programming or Botox has frozen Facebook CEO Mark Zuckerberg’s face into a wide-eyed, blink-free state, you may have bought yourself a little more time to buy shares in this imminent IPO, which is estimated to value the company at upwards of $100 billion.

We don’t know a lot of details about the financial health of Facebook right now, but what we do know is that this snot-nosed, 27-year-old Mark Zuckerberg has created one of the most powerful companies on this planet and his estimated net worth is currently around $17 billion. Not bad for a college drop-out who started Facebook in 2004 as a freshman at Harvard University. Hmmm, maybe I should have dropped out of college like Mark Zuckerberg, Steve Jobs, and Bill Gates, and I too could have become a billionaire? OK, maybe not, but sometimes living in dreamland can be fun.

Speaking of dreams, Zuckerberg has a dream of connecting the whole world, and with more than 800 million-plus Facebook users, he is well on his way. If Facebook users made their own own country, it would be #3 behind only China and India – I’ll check back in a few years to see if Facebook can climb to the top position.

The Pre-IPO Interview

Charlie Rose recently ditched the tie and headed to Silicon Valley to conduct an interview at Facebook headquarters with Mark Zuckerberg and his Chief Operating Officer Sheryl Sandberg. If you fast forward to MINUTE 9:30 you can listen to the official Facebook IPO response:

Vodpod videos no longer available.

The Hype Machine

The hype surrounding the Facebook IPO is palpable and feels a lot like the Google Inc. (GOOG) IPO in 2004, but that capital raising event only resulted in proceeds of $1.9 billion for Google. The recent chatter surrounding the pending Facebook IPO places the value to be raised closer to $10 billion. Partial offerings seem to be the trend du jour in the social media IPO world, where companies like LinkedIn Corp. (LNKD), Groupon Inc. (GRPN), and Zillow Inc. (Z) all sold just a sliver of their shares to the public in order to create artificial scarcity, thereby pumping up short-term demand for their respective stocks. These companies trade at or above their initial offering price, but significantly below the early investor mouth-frothing spikes in share prices near the time of the IPOs. Facebook appears to be using the same playbook to build up hype for its eventual offering.

Even at an estimated value of $100 billion, Facebook still has some wood to chop if wants to pass Google (about $185 billion in value) and Apple Inc’s (AAPL) approximate $415 billion, but Zuckerberg is no stranger to ambition. When Facebook unveils its inevitable IPO prospectus in the not too distant future, we will have a better idea of whether Facebook and the 2010 Time magazine Person of the Year deserve all the mega-billion dollar accolades, or will an IPO feeding frenzy bring tears to those investors’ eyes that are not privileged enough to receive IPO allocated shares? Regardless of your faith or skepticism, we’re likely to find out the answer to these critical questions in a blink of an eye.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AGN, AAPL, GOOG but at the time of publishing SCM had no direct position in Facebook, MSFT, LNKD, GRPN, Z, TWX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Microsoft Enters Garbage Recycling Business

Microsoft Inc. (MSFT) is going green in more ways than one. Not only is Microsoft shelling out a lot of green ($8.5 billion) to acquire internet communication company Skype, but Microsoft is also going green by recycling Skype – an asset previously tossed away as garbage by eBay Inc. (EBAY). While I’m certain Microsoft executives did their due diligence and a large cadre of savvy bankers provided their stamp of approval on the deal, recycling a previously disposed item successfully poses some unique challenges.

The Problems

What could possibly go wrong in a sexy, strategic deal that plans to leverage Skype’s power of internet communication across Microsoft’s various businesses including mobile, business software, gaming, and advertising platforms?

- Sticker Shock: The Microsoft-Skype deal is still in its early phases, but the multi-billion price tag has already elicited heartburn from some investors (heart attacks among others). In Microsoft’s defense, what’s a mere $8.5 billion among friends, especially if your wallet is stuffed with over $60 billion in cash like Microsoft? With the 3-month Treasury bill currently yielding 0.02%, the massive wads of cash that Microsoft (and other tech giants) is sitting on appear to be burning a hole in buyers’ pockets. In a kooky internet world where IPO valuations of $70 billion for Facebook, $25 billion for Groupon, and $3 billion for LinkedIn are freely tossed around, an $8.5 billion Skype offer may seem like par for the course (or even a bargain). Sadly, however, I am having difficulty reconciling how Microsoft will take 663 million money-losing customers at Skype and balance the laws of economics by adding further volumes of money-losing customers. Apple Inc. (AAPL) spends about $2 billion per year in research & development, and is expected to produce more than $100 billion in revenues in fiscal 2011, while the $8.5 billion that Microsoft spent on Skype produced less than $1 billion in revenues last year. I presume Microsoft has some aggressive assumptions built into their Skype forecasts to rationalize the price paid for Skype.

- Failure Déjà Vu: Does the desire to integrate wiz-bang technology into existing product platforms sound familiar? It should – eBay Inc. (EBAY) already attempted and failed at integrating Skype before it threw in the white towel at the end of 2009 and sold a majority $1.9 billion stake of Skype shares back to a group of investors, including the Skype founders. Back in 2005, when eBay paid a then bargain of $3.1 billion for Skype (including earnouts), former CEO Meg Whitman evangelized the “Power of 3” (Skype + eBay’s Marketplace + PayPal) – I suppose new CEO John Donahoe must now promote the “Power of 2.” In Skype merger sequel of 2011, Microsoft’s CEO Steve Ballmer is espousing the benefits of Skype across Microsoft properties such as Outlook, Windows Live Messenger, Xbox, Kinect, and its newly created Nokia Corp. (NOK) relationship. Gaudy priced mergers in the internet/social media space have a way of eventually ending up in the deal graveyard. Consider AOL Inc.’s (AOL) 2008 deal with social network Bebo for $850 million – two years later AOL sold it for $10 million. News Corp’s (NWS) high profile purchase of MySpace for $580 million is reportedly looking for a new home at a fraction of the original price ($50 million). Hewlett-Packard Co.’s (HPQ) ostentatious $2.4 billion value (~125 x’s forward earnings) paid for 3Par Inc. during a bidding war with Dell Inc. (DELL) in 2010 is another recent example of a risky high-priced deal.

- Telco Carrier Skepticism: Although Microsoft has ambitions of taking over the world with Skype, the telecom service carrier companies that facilitate Skype traffic may feel differently. As the telcos spend billions to expand the global internet superhighway, if Skype is clogging traffic on their networks then the carriers will likely require additional compensation – no freeloaders allowed.

- Rocky Past Marriages: When it comes to acquisitions, Microsoft historically hasn’t fooled around as much as some other large Fortune 100 companies, nonetheless some important past relationships have gone sour. Take for instance Microsoft’s previous largest $6 billion cash acquisition of aQuantive Inc. in 2007. As Microsoft continues to chase Google Inc. (GOOG) at their heels, Microsoft has little to show for the aQuantive deal, except for a lot of employee turnover. The sizable but smaller $1.1 billion acquisition of Great Plains in 2001 has its critics too. Like Skype, the Great Plains business software deal made strategic sense, but six years after the units were fully integrated founder and owner Doug Burgum packed his bags and left Microsoft.

Consequences

What happens next for Microsoft? I know it’s difficult to imagine that Microsoft’s colossal underperformance since the beginning of 2010 could worsen – Microsoft has underperformed the market by a whopping -38% over that period – but by massively overpaying for Skype’s losses, Microsoft is not making their own job any easier. Although Microsoft has missed many key technology trends over the last few years (e.g., search, mobile, tablets, social media, etc.) and its stock has been in the dumps, the PC behemoth is looking to salvage a previously failed merger into a successful one. Time will tell if Microsoft can recycle a trashed, money losing operation into hefty green profits. If not, investors will be out for blood wondering why $8.5 billion was thrown away like garbage.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, and GOOG, but at the time of publishing SCM had no direct position in MSFT, Skype, EBAY, AOL, HPQ, DELL, NOK, Facebook, MySpace, LinkedIn, Groupon, Bebo, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Rebuilding after the Political & Economic Tsunami

Excerpt from Free April Sidoxia Monthly Newsletter (Subscribe on right-side of page)

The Start of the Arab Uprising

The Arab uprising grew its roots from an isolated and disgraced Tunisian fruit vendor (26- year-old Mohammed Bouazizi) who burned himself to death in protest of the persistent, deep-seeded corruption prevalent throughout the government (view excellent 60 Minutes story on Tunisia uprising). The horrific death ultimately led to the swift removal of Egypt’s 30-year President Hosni Mubarak, whose ejection was spurred by massive Facebook-organized protests. Technology has flattened the world and accelerated the sharing of powerful ideas, which has awoken Arab citizens to see the greener grass across other global democratic nations. Facebook, Twitter, and LinkedIn can be incredible black-holes of productivity destroyers (I know firsthand), but as recent events have proven, these social networking services, which handle about 1 billion users globally, can also serve valuable purposes.

As the flames of unrest have been fanned across the Middle East and Northern Africa, autocratic dictators haven’t had the luxury of idly sitting on their hands. Instead, these leaders have been pushed to relent to the citizens’ wishes by addressing previously taboo issues, such as human rights, corruption, and economic opportunity. These fresh events feel like new-found changes, but these major social tectonic shifts have been occurring throughout history, including our lifetimes (e.g., Tiananmen Square massacre and the fall of the Berlin Wall).

Good News or Bad News?

Recent headlines have created angst among the masses, and the uncertainty has investors asking a lot of questions. Besides radioactive concerns in both Japan and the Middle East (one actual, one figurative), the “worry list” of items continues to stack higher. Oil prices, inflation, the collapsing dollar, exploding deficits, a China bubble, foreclosures, unemployment, quantitative easing (QE2), mountainous debt, 2012 elections, and the end of the world among others, are worries crowding people’s brains. Incredibly, somehow the market still manages to grind higher. More specifically, the Dow Jones Industrial Average has climbed a very respectable +6.4% for 2011.

With the endless number of worries, how on earth could the major market indexes still advance, especially after a doubling in value from 24 months ago? For one, these political and economic shocks are nothing new. History has shown us that democratic, capitalistic markets ultimately move higher in the face of wars, assassinations, banking crises, currency crises, and various other stock market frauds and scandals. I’m willing to go out on a limb and say these worrisome events will continue this year, next year, and even over the next decade.

Most baby boomers living in the early 1980s remember when 30-year mortgage rates on homes reached 18.5%, inflation hit 14.8%, and the Federal Funds interest rate peaked near 20%. Boomers also survived Vietnam, Watergate, the Middle East oil embargo, Iranian hostage crisis, 1987 Black Monday, collapse of the S&L banks, the rise and fall of the Cold War, Gulf War I/II, yada, yada, yada. Despite all these cataclysmic events, from the last birth of the Baby Boomers (1964), the Dow Jones Industrial catapulted from about 890 to 12,320. This is no April Fool’s joke! The market has increased a whopping 14-fold (without dividends) in the face of all this gruesome news. You won’t find that story on the front-page of The Wall Street Journal.

Lost Decade Goes on Sale

The gains over the last four and half decades have been substantial, but much more is said about the recent “Lost Decade.” Although it has generally been a lousy decade for most investors in the stock market, eventually the stock market follows the direction of profits. What the popular press negates to mention is that S&P 500 operating earnings have more than doubled from about $47 in 1999 to an estimated $97 in 2011. Over the same period, the price of the market has been chopped by more than half (i.e., the Price – Earnings multiple has been cut from 29x to 13.5x). With stocks selling at greater than -50% off from 1999, no wonder smart investors like Warren Buffett are buying America – Buffett just spent $9 billion in cash on buying Lubrizol Corp (LZ). Retail investors absolutely loved stocks in 2000 at the peak, believing there was virtually no risk. Now the tables have been turned and while stock prices are trading at a -50% discount, retail investors are intensely skeptical and nervous about the prospects for stocks. Shoppers don’t usually wait for prices to go up 30% and then say, “Oh goody, prices are much higher now, so I think I will buy!” but that is what they are saying now.

I don’t want to oversell my enthusiasm, because the deals were dramatically better in March of 2009. Hindsight is 20-20, but at the nadir of the stock market, stock prices traded at bargain basement levels of 7x times 2011 earnings. We may not see opportunities like that again in our lifetime, so sitting in cash may not be the most advisable positioning.

Although I would argue every investor should have some exposure to equities, an investor’s time horizon, objectives, constraints and risk tolerance should be the key determinants of whether your investment portfolio should have 5% equity exposure or 95% exposure.

So while the economic and political dominoes may appear to be tumbling based on the news du jour, don’t let the headlines and the so-called media pundits scare you into paralysis. Bad news and tragedy will continue, but fortunately when it comes to prosperity, history is on our side. As you attempt to organize and pickup the financial pieces of the last few years, make sure you have a disciplined, long-term investment plan that adapts to changing market and personal conditions.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in LZ, Facebook, Twitter, LinkedIn, BRKA/B, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Bove on Goldman-Facebook Deal: Hug the Public!

In a recent research report titled, Has Goldman Learned Anything?, esteemed Rochdale Research analyst Richard Bove chimed in about the recent controversy surrounding the failed U.S. private offering of Facebook shares by Goldman Sachs (GS) to the bank’s wealthiest clients. In the note, Bove states the following:

“The company is embroiled in a ‘headline’ controversy surrounding its handling of a Facebook offering which implies that Goldman does not understand the public’s interest at all.”

Bove goes onto add:

“I fear that this company may not yet understand that those actions that do not appear to be in the public’s interest can, in fact, harm the company.”

I’m having a real difficult time understanding how Goldman privately raising funds for a private company has anything to do with the public? Am I wrong, or don’t millions of private companies raise capital every year without getting approval from Mr. Joe and Mrs. Josephine Public? What exactly does Bove want Goldman CEO Lloyd Blankfein to say to Facebook chief Mark Zuckerberg?

“Oh hello Mr. Zuckerberg, this is Lloyd Blankfein calling from Goldman Sachs, and if I understand it correctly, you are interested in raising $1.5 billion for your company. I know you are arguably the greatest internet brand on this planet, but unfortunately I do not think we can help you because I believe the broader public may not be happy with their lack of ability to participate in the offering. If you don’t have Morgan Stanley’s or JP Morgan’s phone number, just let me know because perhaps they can assist you. Have a great day!”

Come on…Goldman Sachs is not a charitable organization with a mission to make the world a better place – they are one of thousands of publicly traded companies attempting to grow profits. Sure, could Goldman have more discreetly pursued this offering without attracting the massive media barrage? Absolutely. But let’s be fair, the buzz around Facebook is deafening and the paparazzi are following Mark Zuckerberg around as closely as Raj Rajaratnam chases insider trading tips. New York Times columnist and reporter Andrew Ross Sorkin (see Too Big to Fail book review) summed it up best when he said, “You take the words Facebook and Goldman Sachs and put them in the same sentence, it becomes a media sensation unto itself. So I think this was bound to happen one way or the other.”

So while I have no reason to cheerlead for Goldman Sachs, and I’m sure there are plenty of other reasons for the investment bank to be crucified, attempting to raise money for a private company is not a felony in my book. I commend Richard Bove’s altruistic intentions in protecting the public from Goldman Sachs’s evil capital raising activities, and I may even contribute to a group hug with the mass investing public. If he catches me on the right day, I may even give CEO Lloyd Blankfein a hug.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in GS, MS, JPM, Facebook, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Internet: The Fourth Necessity

The basic necessities for human life are food, water, shelter and most importantly…the internet. Imagine a world where you cannot: access your email; text your spouse or significant other in the same house; Twitter the contents of your lunch; or Facebook a YouTube video of a dancing meringue dog (see video). Scary thought.

Many people take the internet for granted, just like the air we breathe, but how important a role does the internet play in people’s lives? Mary Meeker, internet analyst from Morgan Stanley, takes a look at this question in a recently released presentation she completed. Earlier in the decade, Meeker was raked over the coals during the deflation of the internet bubble, but in many respects she has been redeemed in the subsequent years as hundreds of millions of people continue to plug into the internet.

According to the broad base of expert strategists, we apparently are living in an overvalued, “New Normal ” market with subdued growth for as far as the eye can see (check out New Abnormal). In the mean time Meeker shows how the top 15 global internet franchises have nearly quadrupled revenue from $33 billion in 2004 to $126 billion today. Perhaps abnormally outsized opportunities in the corporate internet universe will be the “New Normal” over the coming years?

Internet Ubiquity

Source: Morgan Stanley

How ubiquitous is the internet becoming? Last year 1.8 billion people accessed this invisible global flattening medium we like to call the internet, and users spent 18.8 trillion minutes online, up +21% over the previous year. Many people are very familiar with the home-bred internet franchises of Facebook (620 million users), Google (940 million users), and Apple (120 million internet device users), but many investors under-appreciate the global scale of international internet franchises like Tencent (637 million users…more than Facebook by the way), Baidu ($40 billion market value), or Alibaba.com ($10 billion market value).

Source: Morgan Stanley

Mobile ubiquity is on the rise too. Connecting through a desktop or laptop is not enough these days, so internet addicts are increasingly attaching a mobile phone umbilical cord for such useful bathroom applications such as this (click here). Lugging a laptop around all over the place can be an inconvenience. So primal is the mobile instinct among internet users, Morgan Stanley expects mobile phone shipments to surpass PC and laptop shipments over the next 24 months.

What’s Next?

The party is just getting started. If you just consider eCommerce (purchases online), which only accounts for 4% of total commerce conducted in the U.S., then there is a lot of headroom for internet purchases to expand. The incredible potential rings true especially if you contemplate old traditional catalog, which peaked at more than 10% of overall commerce according to some industry executives. The rich feature functionality afforded to users through the internet, coupled with the increased convenience of mobility, augur well for future ecommerce sales growth.

The internet has been around for 15 years, but in the whole scheme of things this transformative medium is just a baby – especially if you consider the amount of time it took other revolutions like electricity, the rail network, and automobile proliferation to spread. That is why it is not too late to join the internet party. Food, water, and shelter are human necessities of life, just like exposure to the internet revolution is a necessity for your investment portfolio.

Read the Morgan Stanley Internet Presentation by Mary Meeker

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL and GOOG, but at the time of publishing SCM had no direct position in MS, BIDU, Tencent, Alibaba.com, Facebook, Twitter, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}