Posts tagged ‘Europe’

End of the World or Status Quo?

If you were the chief executive of a newspaper, television, or magazine company, what headline stories would you run to generate the most viewers and readers? Which subjects will you choose to make me impulsively grab a magazine in the grocery line, keep me glued to the television news, or suck me in to click-bait advertisements on the web? For example, what topics below would you select to grab the most attention?

· Hurricane or Sunshine?

· High Speed Car Chase or Cat Saved from Tree?

· Bloody Murder or Baby’s Birthday?

· Messy Divorce or Wedding Celebration?

· Impeachment or Bipartisan Legislation

· End of the World or Status Quo?

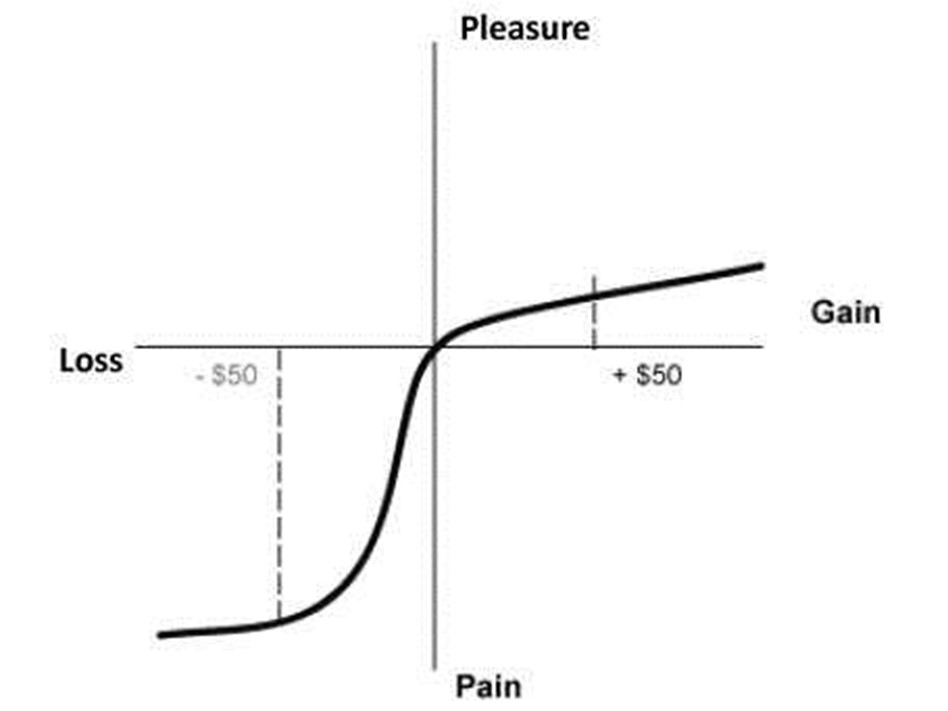

If you selected the first subject in each pair above, you would likely gain much more initial interest. In choosing a winning topic, the saying goes, “what bleeds, leads.” In other words, scary or controversial stories always grab more attention than feel-good or status quo narratives. And that is why the vast majority of media outlets are drawn to negativity, just as mosquitos are attracted to bug zappers. This phenomenon can be explained in part with the help of Nobel Prize winner Daniel Kahneman and his partner Amos Tversky, who conducted research showing the pain from losses is more than twice as painful as are the pleasures experienced from gains (see chart below).

The significant volatility seen in the stock market recently from the Russian war/invasion of Ukraine is further evidence of how this fear dynamic can create short-term panics.

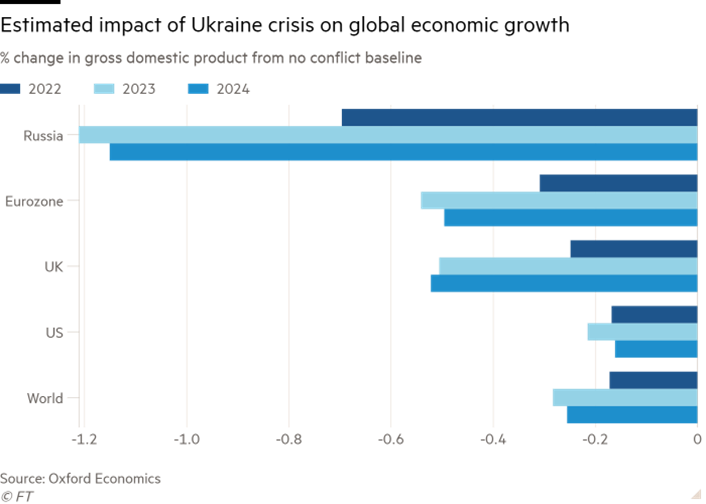

Although the stock market as measured by the S&P 500 index has gone gangbusters over the last three years, almost doubling in value (2019: +29%, 2020: +16%, 2021: +27%), the S&P 500 has hit an air pocket during the first couple months of 2022 (-8%), including down -3% in February. The year started with turbulence as investors became fearful of a Federal Reserve that is entering the beginning stages of interest rate hikes while cutting stimulative bond purchases. And then last month, the Russian-Ukrainian incursion made investors even more skittish. Like always, these geopolitical events tend to be short-lived once investors realize the impact turns out to be less meaningful than initially feared. As you can see below, the worst economic impact is forecasted to be felt by Russia (consensus on 2/24/22 of approximately a -1.0% hit to economic growth), more than twice as bad as the -0.2% to -0.4% knock to growth for the U.S., Europe, and the world (see chart below). The Russian hit will likely be worse after accelerated sanctions.

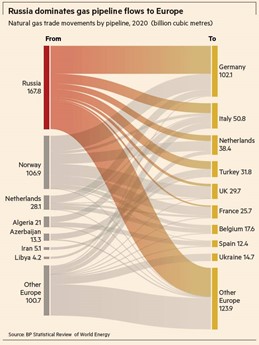

As it relates to Ukraine, many Americans don’t even know where the country is located on a map. Ukraine accounts for about only 0.14% of total global GDP (i.e., a rounding error and less than 1% of total global economic activity). Russia, although larger than Ukraine, is still a relative small-fry and represents only about 3% of total global economic activity. If you live in Europe during the winter, you might be a little more concerned about Vladimir Putin’s recent activities because a lot of Europe’s energy (natural gas) is supplied by Russia through Ukraine. For example, Germany receives about half of its natural gas from Russia (see chart below).

Russia, on the other hand, is larger than Ukraine, but the red country is still a relative small-fry representing only about 3% of total global economic activity. When it comes to energy production however, Russia is more than a rounding error because the country accounts for about 11% of global energy production (#3 country globally behind the United States and Saudi Arabia). By taking all these factors into account, we can confidently state that Russia and Ukraine have a very low probability of solely pulling the global economy into recession.

If history repeats itself, this conflict will turn out to be another garden variety decline in the stock market and an opportunity to buy at a discount. It’s virtually impossible to predict a short-term bottom in stock prices has been reached, but over the long-run, stock investors have been handsomely rewarded for not panicking and staying invested (see chart below).

At the end of the day, the daily headlines will continually attempt to sell the negative story that the world is coming to an end. If you have the fortitude and discipline to ignore the irrelevant noise, the status quo of normal volatility can create more exciting opportunities and better returns for long-term investors.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2022). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

S.T.I.N.K. – Deja Vu All Over Again

Yogi Berra is a Baseball Hall of Fame catcher and manager who played 18 out of 19 seasons with the New York Yankees. Besides his incredible baseball skills, Berra was also known for his humorous and witty quotes, which were called “Yogi-isms.” Reportedly, one of Berra’s most famous Yogi-isms occurred after he observed fellow teammates, Mickey Mantle and Roger Maris, continually hitting back-to-back home runs:

“It’s déjà vu all over again.”

The Merriam-Webster dictionary defines déjà vu as “a feeling that one has seen or heard something before.” I experienced the same sense last month as I was bombarded with ominous news headlines. Some of you may recall the panic attack over the PIIGS regions during the 2010 – 2012 timeframe (Solving Europe & Deadbeat Cousin). I’m obviously not referring to the pork product, but rather Portugal, Italy, Ireland, Greece, and Spain, which rocked financial markets due to investor fears that Greece’s fiscal irresponsibility may force the country to leave the eurozone and drag the rest of Europe into financial ruin.

Suffice it to say, the imploding Greece/Europe disaster scenario did not happen. If you fast forward to today, the fear has returned again, however with a different acronym spin. Rather than speak about PIIGS, today the talking heads are fretting over S.T.I.N.K. – Spain, Tariffs, Italy, and North Korea.

*Worth noting, the letter “I” in S.T.I.N.K. could also be sustained or replaced by the word Iran, given the Trump administration’s desire to exit the Iran Nuclear Deal. The move comes despite support by our country’s tight NATO (North Atlantic Treaty Organization) allies who want the U.S. to remain in the agreement.

An overview of S.T.I.N.K. unease is summarized here:

Spain: After a reign of six years, Spain’s Prime Minister Mariano Rajoy is on the verge of being ousted to socialist opposition leader, Pedro Sanchez. Corruption convictions involving former members in Rajoy’s conservative Popular Party only increases the probability that the imminent no-confidence vote in the Spanish parliament will lead to Rajoy’s exit.

Tariffs: President Trump is lifting the temporary steel and aluminum tariff exemptions provided to many of our allies, including Canada, Mexico, and the European Union. Recent breakdowns in trade discussions with allies like Mexico and Canada are likely to make the renegotiation of NAFTA (North American Free Trade Agreement) even more challenging. Handicapping President Trump’s global trade rhetoric can be difficult, especially given the periodic inconsistency in Trump’s actions relative to his words. Time will tell whether Trump’s tough trade talk is merely a negotiating tool designed to gain better trade terms for the U.S., or whether this strategy backfires, and trading partner allies choose to retaliate with tariffs of their own. For example, the EU has threatened to impose import taxes on bourbon; Mexico has warned about levying taxes on American farm products; and Canada is focused on the same steel and aluminum tariffs that Trump has been referencing.

Italy: Pandemonium temporarily set in when Italy’s President Sergio Mattarella essentially vetoed the finance minister selection by Italian Prime Minister Giuseppe Conte. Initially, Italian bond prices plummeted and interest rates spiked as fears of an Italian exit from the euro currency, but after the rejection of the original finance chief, the populist Five Star and League coalition parties agreed to institute a more moderate finance minister and bond prices/rates stabilized.

North Korea: The on-again-off-again denuclearization summit between the U.S. and North Korea may actually take place in Singapore on June 12th. In recent days, Secretary of State Mike Pompeo has held face-to-face meetings with North Korean General Kim Yong Chol in New York. The senior North Korean leader is also planning to hand deliver a letter from Korean leader Kim Jong Un to President Trump in preparation for the nuclear summit. The U.S. is attempting to incentivize North Korea with economic relief in return for North Korea giving up their nuclear capabilities.

Thanks to S.T.I.N.K., volatility has risen, but the downdrafts have been relatively muted as evidenced by the moves in the stock averages this month. More specifically, the S&P 500 index rose +2.2% last month, while the technology-heavy Nasdaq index catapulted +5.3%. Nevertheless, not all indexes are created equally as witnessed by the Dow Jones Industrial Index, which climbed a more muted +1.1% for the month. For the year, the Dow is down -1.2%, while the S&P and Nasdaq indexes are higher by +1.2% and +7.8%, respectively.

Ever since the 2008-2009 financial crisis, observers have incessantly and anxiously waited for the return of a “stinky” economic and/or geopolitical catastrophe that will wreck the American economy. Unfortunately for the pessimists, stock prices have more than quadrupled in value since early-2009. Yogi Berra may have been correct when he said, “It’s déjà vu all over again,” but just like PIIGS concerns failed to cause global economic contagion, STINK concerns are unlikely to cause significant economic damage either. Over the last year, the only “stink” occurring has been the stink of cool, hard cash.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2018). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Hot Dogs, Political Fireworks, and Our Nation’s Birthday

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 3, 2017). Subscribe on the right side of the page for the complete text.

The 4th of July has arrived once again as we celebrate our country’s 241st birthday of independence. Besides being a time to binge on hot dogs, apple pie, fireworks, and baseball, this national holiday allows Americans to also reflect on the greatness created by our nation’s separation from the British Empire.

As our Founding Fathers fought for freedom and believed in a more prosperous future, I’m not sure if the signers of our Declaration of Independence (Below [left to right]: Roger Sherman, Benjamin Franklin, Thomas Jefferson, John Adams, and Robert Livingston) envisioned a world with tweeting Presidents, driverless Uber taxis, internet dating, biotechnology medical breakthroughs, cloud storage, and countless other innovations that have raised the standard of living for billions of people around the world.

(These Founding Fathers may use different pictures for their Facebook profile, if they were alive today.)

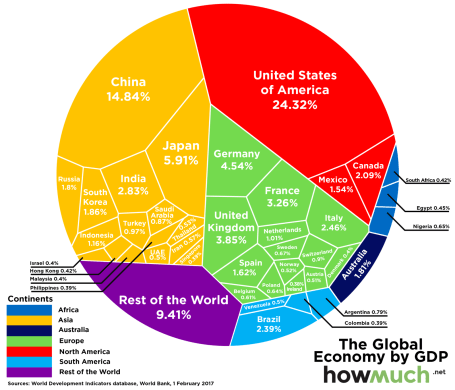

I tend to agree with the wealthiest billionaire investor on the planet, Warren Buffett, that being born in the United States is the equivalent of winning the “Ovarian Lottery.” The opportunities for finding success are exponentially higher, if you were born in America vs. Bangladesh, for example. Surprisingly, the U.S. only accounts for about 4% of the global population (325 million out of 7.5 billion world total). However, even though we Americans make up such a small portion of the of the people on the planet, we still manage to generate over $18 trillion in goods and services, which makes us the world’s largest economy. As the #1 economy, we account for almost 25% of the world’s total economic output (see table & graphic below).

| Rank | Country | GDP (Nominal, 2015) | Share of Global Economy (%) |

| #1 | United States | $18.0 trillion | 24.3% |

| #2 | China | $11.0 trillion | 14.8% |

| #3 | Japan | $4.4 trillion | 5.9% |

| #4 | Germany | $3.4 trillion | 4.5% |

| #5 | United Kingdom | $2.9 trillion | 3.9% |

Source: Visual Capitalist

How do we create six times the output of our population (i.e., 4% of world’s population producing 25% of the world’s output)? Despite the nasty, imperfect, mudslinging politics we live through daily, the U.S. has perfected the art of capitalism, which has landed us on top of the economic Mt. Everest. Although, there is always room for improvement, culturally, the winning “entrepreneurial” strain is born into our American DNA. The recent merger announcement between Amazon.com Inc. (AMZN) and Whole Foods (WFM), the leading natural and organic foods supermarket, is evidence of this entrepreneurial strain. Amazon has come a long way and gained significant steam since its founding in July 1994 by CEO Jeff Bezos. Consequently, the momentum of this internet giant has it steamrolling the entire retail industry, which has led to a flood of store closings, including department store chains, Macy’s, J.C. Penney, Sears and Kmart. The Amazon-Whole Foods merger announcement was not a huge surprise to my family because we actually order more than half of our groceries from AmazonFresh (Amazon’s food delivery program). What’s more, since I despise shopping, I continually find myself taking advantage of Amazon’s “Prime Now” 2-hour delivery option to my office, which is free to all Prime subscribers. It won’t be long before Amazon’s multi-channel strategy will allow me to make same-day orders for groceries, electronics, and general merchandise from my office, then pick up those items on my way home from work at the local Whole Foods store.

Leading the Pack

Replicating this competitive advantage around the world is a challenge for competing countries, and our nation remains leap years ahead of others, regardless of their efforts. However, the United States does not have a monopoly on capitalism. We are slowly exporting our entrepreneurial secret sauce abroad with the help of technology and globalization. Just consider these three Chinese companies alone are valued at almost $1 trillion (Alibaba Group $360B [BABA]; Tencent Holdings $340B [TCEHY]; and China Mobile $220B [CHL]), and the largest expected IPO (Initial Public Offering) in the world could be a Saudi Arabian company valued at $2 trillion (Saudi Aramco). When 96% of the world’s population lies outside of the U.S., this reality helps explain why exporting our advancements should not be considered a bad thing. In fact, a growing international pie means more American jobs and more dollars will flow back to the U.S., as we export more value-added products and services abroad.

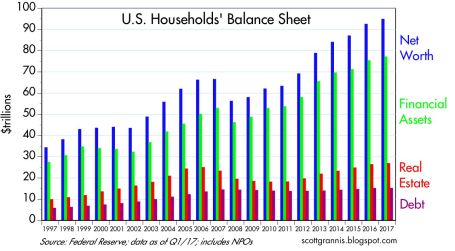

Even if other countries are narrowing the entrepreneurial competitive gap with the United States, we still remain a beacon of light for others to follow. Despite what you may read in the newspaper or hear on the TV, Americans are dramatically better off financially over the last 20 years. Not only has net worth increased spectacularly, but consumers have also responsibly reduced debt leverage ratios (see chart below).

Source: Calafia Beach Pundit

If you were a bright CEO working for an innovative new start-up company, would you choose to launch your company in a closed, censored society like China? How about a fractured Britain that is pushing to break away from the European Union? Better yet, how about Japan with its exploding debt levels, a declining population, and a stock market that is about half the level it peaked at 28 years ago? Do emerging markets like Brazil with widespread corruption scandals blanketing a new president (after a recently impeached president) seem like the best location for a hot new venture? The answer to all these questions is a resounding “no”, even when compared to the warts and flaws that come with our durable democracy.

Political Pyrotechnics

Besides the bombs bursting in air during the 4th of July celebration, there were plenty of political fireworks blasting in our nation’s capital last month. No matter what side of the political fence you stand on, last month was explosive. Consider ousted FBI Director Jim Comey’s impassioned testimony relating to his firing by President Donald Trump; the contentious Attorney General Jeff Sessions Senate Intelligence Committee interview; the politically driven Republican baseball shooting; and the Special Counsel leader Robert Mueller’s investigation into Russian interference and potential Trump administration collusion into the 2016 elections.

Despite the combative atmosphere in Washington D.C., the stock market managed to notch another record high last month, with the Dow Jones Industrial Average index advancing another 340.98 points (+1.6%) for the month, and +8.0% for the first half of 2017. As I have written numerous times, the scary headlines accumulating since 2009 have prevented investors, strategists, economists, and even professionals from adequately participating in the almost quadrupling in stock prices since early 2009. Unfortunately, to the detriment of many, large swaths of investors who were burned by the 2008-2009 Financial Crisis have been scarred to almost permanent risk aversion. The fact of the matter is stock prices care more about economic factors than political / news headlines (see Moving on Beyond Politics).

The bitter, vitriolic political discourse is unlikely to disappear anytime soon, so do yourself a favor, and focus on the more important factors driving financial markets to new record highs – mainly corporate profits, interest rates, valuations, and sentiment (see Don’t Be a Fool). During this year’s 4th of July, partaking in hot dogs, apple pie, fireworks, and baseball are wholly encouraged, but please also take the time to celebrate and acknowledge the magnitude of our country’s greatness. That’s a birthday wish, I think we can all agree upon.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AMZN and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in WFM, BABA, TCEHY, CHL, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Head Fakes Surprise as Stocks Hit Highs

In a world of seven billion people and over 200 countries, guess what…there are a plethora of crises, masses of bad people, and plenty of lurking issues to lose sleep over.

The fear du jour may change, but as the late-great investor Sir John Templeton correctly stated:

“Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.”

And for the last decade since the 2008-2009 Financial Crisis, it’s clear to me that the stock market has climbed a lot of worry, pessimism, and skepticism. Over the last decade, here is a small sampling of wories:

With over five billion cell phones spanning the globe, fear-inspiring news headlines travel from one end of the world to the other in a blink of an eye. Fortunately for investors, the endless laundry list of crises and concerns has not broken this significant, multi-year bull market. In fact, stock prices have more than tripled since early 2009. As famed hedge fund manager Leon Cooperman noted:

“Bull markets don’t die from old age, they die from excesses.”

On the contrary to excesses, corporations have been slow to hire and invest due to heightened risk aversion induced by the financial crisis. Consumers have saved more and lowered personal debt levels. The Federal Reserve took unprecedented measures to stimulate the economy, but these efforts have since been reversed. The Fed has even signaled its plan to reduce its balance sheet later this year. As the expansion has aged, corporations and consumer risk aversion has abated, but evidence of excesses remains paltry.

Investors may no longer be panicked, but they remain skeptical. With each subsequent new stock market high, screams of a market top and impending recession blanket headlines. As I pointed out in my March Madness article, stocks have made new highs every year for the last five years, but continually I get asked, “Wade, don’t you think the market is overheated and it’s time to sell?”

For years, I have documented the lack of stock buying evidenced by the continued weak fund flow sales. If I could summarize investor behavior in one picture, it would look something like this:

Corrections have happened, and will continue to occur, but a more significant decline will likely happen under specific circumstances. As I point out in Half Empty, Half Full?, the time to become more cautious will be when we see a combination of the following trends occur:

- Sharp increase in interest rates

- Signs of a significant decline in corporate profits

- Indications of an economic recession (e.g., an inverted yield curve)

- Spike in stock prices to a point where valuation (prices) are at extreme levels and skeptical investor sentiment becomes euphoric

Attempting to predict a market crash is a Fool’s Errand, but more important for investors is periodically reviewing your liquidity needs, time horizon, risk tolerance, and unique circumstances, so you can optimize your asset allocation. There will be plenty more head fake surprises, but if conditions remain the same, investors should not be surprised by new stock highs.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Sweating Your Way to Investment Success

There are many ways to make money in the financial markets, but if this was such an easy endeavor, then everybody would be trading while drinking umbrella drinks on their private islands. I mean with all the bright blinking lights, talking baby day traders, and software bells and whistles, how difficult could it actually be?

Unfortunately, financial markets have a way of driving grown men (and women) to tears, usually when confidence is at or near a peak. The best investors leave their emotions at the door and follow a systematic disciplined process. Investing can be a meat grinder, but the good news is one does not need to have a 90% success rate to make it lucrative. Take it from Peter Lynch, who averaged a +29% return per year while managing the Magellan Fund at Fidelity Investments from 1977-1990. “If you’re terrific in this business you’re right six times out of 10,” says Lynch.

Sweating Way to Success

If investing is so tough, then what is the recipe for investment success? As the saying goes, money management requires 10% inspiration and 90% perspiration. Or as strategist and long-time investor Don Hays notes, “You are only right on your stock purchases and sales when you are sweating.” Buying what’s working and selling what’s not, doesn’t require a lot of thinking or sweating (see Riding the Wave), just basic pattern recognition. Universally loved stocks may enjoy the inertia of upward momentum, but when the music stops for the Wall Street darlings, investors rarely can hit the escape button fast enough. Cutting corners and taking short-cuts may work in the short-run, but usually ends badly.

Real profits are made through unique insights that have not been fully discovered by market participants, or in other words, distancing oneself from the herd. Typically this means investing in reasonably priced companies with significant growth prospects, or cheap out-of-favor investments. Like dieting, this is easy to understand, but difficult to execute. Pulling the trigger on unanimously hated investments or purchasing seemingly expensive growth stocks requires a lot of blood, sweat, and tears. Eating doughnuts won’t generate the conviction necessary to justify the valuation and excess expected return for analyzed securities.

Times Have Changed

Investing in stocks is difficult enough with equity fund flows hemorrhaging out of investor accounts like the asset class is going out of style. Stocks’ popularity haven’t been helped by the heightened volatility, as evidenced by the multi-year trend in the schizophrenic volatility index (VIX) – escalated by the international geopolitics and presidential elections. Globalization, which has been accelerated by technology, has only increased correlations between domestic market and international markets. In decades past, concerns over economic activity in Iceland, Dubai, and Greece may not even make the back pages of The Wall Street Journal. Today, news travels at the speed of a “Tweet” and eventually results in a sprawling front page headline.

The equity investing game may be more difficult today, but investing for retirement has never been more important. Stuffing money under the mattress in Treasuries, money market accounts, CDs, or other conservative investments may feel good in the short run, but will likely not cover inflation associated with rising fuel, food, healthcare, and leisure costs. Regardless of your investment strategy, if your goal is to earn excess returns, you may want to check the moistness of your armpits – successful long-term investing requires a lot of sweat.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in ETFC, VXX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

U.S. Takes Breather in Windy Economic Race

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (May 1, 2015). Subscribe on the right side of the page for the complete text.

Looking back, in the race for financial dominance, the U.S. economy sprinted out to a relatively quick recovery from the 2008-2009 financial crisis injury compared to its other global competitors. The ultra-loose monetary policies implemented by the Federal Reserve (i.e., zero percent Fed Funds rate, quantitative easing – QE, Operation Twist, etc.) and the associated weakening in the value of the U.S. dollar served as tailwinds for growth. The low interest rate byproduct created cheaper borrowing costs for consumers and businesses alike for things like mortgages, refinancings, stock buybacks, and infrastructure investments. The cheaper U.S. dollar also helped domestically based, multinational companies sell their goods abroad at more attractive prices.

However, those positive dynamics have now changed. With the end of stimulative bond buying (QE) and threats of imminent interest rate hikes coming from the Federal Reserve and its Chairwoman Janet Yellen, the tailwinds for the U.S. economy have now transitioned into headwinds. The measly +0.2% growth recently reported in the 1st quarter – Gross Domestic Product (GDP) results are evidence of an economy currently sucking wind (see chart below).

As it relates to the stock market, the Dow Jones crept up +0.4% for the month of April to 17,841, and is essentially flat for all of 2015. Small Cap stocks in the Russell 2000® Index (companies with an average value of $2 billion – IWM), pulled a muscle in April as shown by the index’s -2.6% tumble. A slight increase in the yield of the 10-Year Treasury to 2.05% caused bond prices to contract a modest -0.5% for the month.

Beyond a strengthening dollar and threats of rising interest rates, debilitating port strikes on the West Coast and abnormally cold weather especially back east also contributed to weak trade data and sub par economic performance. Although a drop in oil and gasoline prices should ultimately be stimulative for broader consumer and industrial activity, the immediate negative impacts of job losses and declining drilling in the energy sector added to the drag on 1st quarter GDP results.

Source: Scott Grannis (Calafia Beach Pundit)

The good news is that many of the previously mentioned negative factors are temporary in nature and should self-correct themselves as we enter the 2nd quarter. One positive aspect to our country’s strong currency is cheaper imports. So, as the U.S. recovers from its temporary currency cramps, foreigners will continue pumping out cheap exports to Americans for purchase. If this import phenomenon lasts, these lower priced goods, coupled with discounted oil prices, should keep a lid on broader inflation. The benefit of lower inflation means the Federal Reserve is more likely to postpone slamming the brakes on the economy with interest rate hikes. The decision of when to lift interest rates will ultimately be data-dependent. Due to the lousy 1st quarter numbers, it will probably take some time for economic momentum to reemerge, and therefore the Fed is unlikely to raise interest rates until September, at the earliest.

The great thing about financial markets and economics is many of these swirling monetary winds eventually self-correct themselves. And during April, we saw these self-correcting mechanisms up close and in person. For example, from March 2014 to March 2015 the U.S. dollar appreciated in value by about +25% versus the euro currency (FXE). However, from the peak exchange rate seen this March, the value of the U.S. dollar declined by about -7%. The same self-correcting principle applies to the oil market. From the highs reached in mid-2014 at about $108 per barrel, crude oil prices plunged by about -60% to a low of $42 per barrel in March. Since then, oil prices have recovered significantly by spiking over +40% to about $60 per barrel today.

Competitors Narrow the Gap with the U.S.

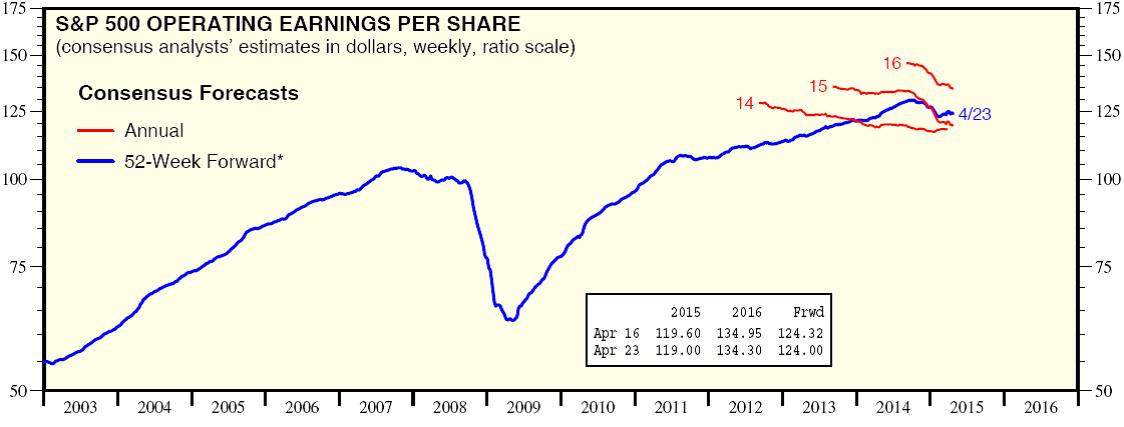

Source: Dr. Ed Yardeni

As I’ve written many times in the past, one of the ultimate arbiters of stock price performance is the long-term direction of corporate profits. And as you can see from the chart above, profits have hit a bump in the road after a fairly uninterrupted progression over the last six years. The decline is nowhere near the collapse of 2008-2009, but given the rise in stock prices, investors should be prepared for the bears and skeptics to become more vocal.

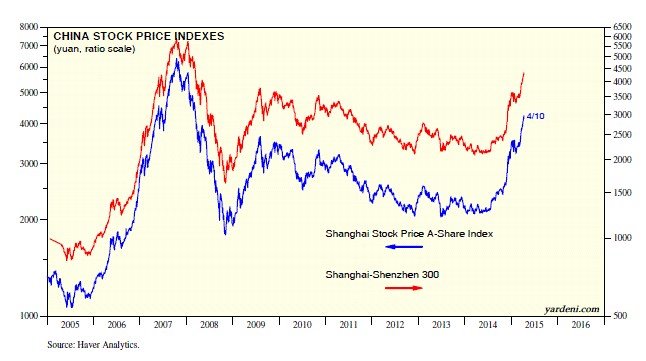

And while the U.S. has struggled a bit, European and Asian shares have advanced significantly. To that point, Asian equities (FXI) spiked an impressive +16% in April (see chart below) and European stocks jumped a respectable +4% (VGK) over the same timeframe.

Source: Dr. Ed’s Blog

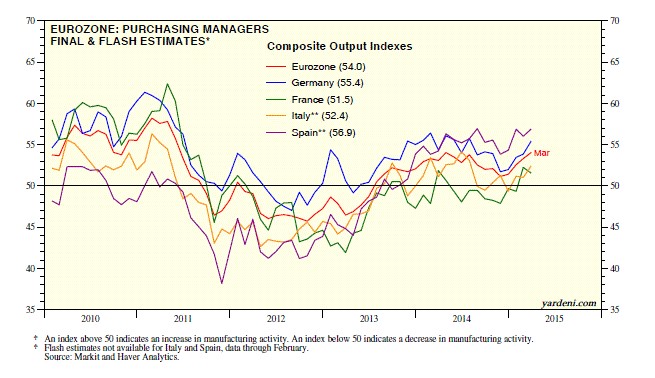

Bolstering the advance in China’s shares has been the Chinese central bank’s move to cut the amount of cash that banks must hold as reserves (“reserve requirements”). The action by the central bank is designed to spur bank lending and combat slowing growth in the world’s second largest economy. The Europeans are not sitting idly on their hands either. European central bankers have taken a cheat sheet page from the U.S. playbook and have introduced their own form of trillion dollar+ quantitative easing (see Draghi Provides Beer Goggles) in hopes of jump starting the European economy. Given the moves, how is the European business activity picture looking? Well, based on the Eurozone Purchasing Managers’ Index (PMI), you can see from the chart below that the region is finally growing (readings > 50 indicate expansion).

Source: Dr. Ed’s Blog

The economic winds in the global race for growth have been swirling in all directions, and due to temporary headwinds, the dominating lead of the U.S. has narrowed. Fortunately for long-term investors, they understand investing is a marathon and not a sprint. Holding a globally balanced and diversified portfolio will help you maintain the stamina required for these volatile and windy economic times.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), FXI, VGK, and a short position in FXE, but at the time of publishing, SCM had no direct position in IWM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Earnings Coma: Digesting the Gains

Over the last five years, the stock market has been an all-you-can-eat buffet of gains for investors. It has been almost two years since the spring of 2012 when the Arab Spring and potential exit of Greece from the EU caused a -10% correction in the S&P 500 index (see Series of Unfortunate Events). Indigestion of this 10% variety is typically on the menu and ordered at least once per year. With stocks up about +50% over the last two years, performance has tasted sweet. But even binging on your favorite entrée or dessert will eventually lead to a food coma. At that bloated point, a digestion phase is required before another meal of gains can be consumed.

So far investors haven’t been compelled to expel their meals quite yet, but it’s clear to me the rate of appreciation is not sustainable over the long-term. Could the incredible returns continue in the short-run during 2014? Certainly. As I’ve written before, the masses remain skeptical of the recovery/rally and any definitive acceleration in economic growth could spark the powder-keg of skeptics to come join the party (see Here Comes the Dumb Money). If and when that happens, I will be gladly there to systematically ring the register of profits I’ve consumed, by locking in gains and reallocating to less loved areas (i.e., go on a stock diet).

Q4 Appetizers Here, Main Course Not Yet

The 4th quarter earnings appetizers have been served, evidenced by the 50-odd S&P 500 corporations that have reported their financial results, and thus far some Tums may be needed to relieve some heartburn. Although about half of those companies reporting have beat Wall Street estimates, 37% of the group have missed expectations, according to Thomson Reuters. It’s still early in the earnings season, but as of now, the ratio of companies beating Wall Street forecasts is below historical averages.

We can put a little meat on the earnings bone by highlighting the disappointing profit warnings and lackluster results from bellwether companies like United Parcel Service (UPS), Intel Corp (INTC), General Electric (GE), CSX Corp (CSX), and Royal Dutch Shell (RDSA), to name a few. Is it time to panic and run for the restroom (or exits)? Probably not. About 90% of the S&P 500 companies still need to give their Q4 profitability state of the union. What’s more, another reason to not throw in the white towel yet is the global economic environment looks significantly better in areas like Europe, China, and other emerging markets.

Worth remembering, the stock market is a discounting mechanism. The market pays much more attention to the future versus the past. So, even if the early earnings read doesn’t look so great now, the fact that the S&P 500 is down less than -1% off of its all-time, record highs may be an indication of better things ahead.

Recipe for a Pullback?

If earnings continue to drag on in a disappointing fashion, and political brinkmanship materializes surrounding the debt ceiling, it could easily be enough to spark some profit-taking in stocks. While Sidoxia is finding no shortage of opportunities, it has become apparent some speculative pockets of euphoria have developed. Areas like social media and biotech are ripe for corrections.

While the gains over the last few years have been tantalizing, investors must be reminded to not overindulge. Carefully selecting stocks to chew and digest is a better strategy than recklessly binging on everything in the buffet line. There are plenty of healthy areas of the market to choose from, so it’s important to be discriminating…or your portfolio could end up in a coma.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in UPS, INTC, GE, CSX, RDSA, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Ski Slope Market: What’s Next in 2014?

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (January 2, 2014). Subscribe on the right side of the page for the complete text.

Skiing, or snowboarding in my case, is a lot like investing in the stock market…a bumpy ride. Snow, wind, ice, and moguls are common for seasoned skiers, and interest rate fluctuations, commodity price spikes, geopolitical turmoil, and -10% corrections are ordinary occurrences for veteran equity investors. However, in 2013 stock investors enjoyed pristine conditions, resulting in the best year for the Dow Jones Industrial Average since 1996. Individuals owning stocks witnessed their portfolios smoothly race to sunny, powder-like returns. More specifically, a December Santa Claus rally (S&P +2.4% for the month) capped off a spectacular year, which resulted in the S&P 500 Index soaring +30%, the NASDAQ Composite Index +38%, and the Dow +26%.

Despite the meteoric move in stocks this year, many observers missed the excitement of the equity ski slopes in exchange for lounging in the comfort of the deceivingly risky but warm lodge. In the lodge, these stock-frightened individuals sipped hot cocoa with wads of inflation-losing cash, bonds, and gold. As a result, these perceived safe assets have now become symbolic relics of the 2008-2009 financial crisis. In the short-run, the risk-averse coziness of the lodge may feel wonderful, but before the lounging observers can say “bull market,” the overpriced cocoas and holiday drinks will eat holes through retirement wallets and purses.

As you can see from the chart below, it is easy for the nervous lodge loungers to vividly remember the scary collapse of 2008-09 (point A to B). Surprisingly, many of these same skeptics are able to ignore or discount the explosive move of 2009-13 (point B to C). There’s another way of looking at this volatile time period. Had an investor fallen into a coma six years ago and then awakened today, an S&P portfolio would still have risen a respectable +26% (point A to C), plus more than +10% or so from dividends.

Turbulent Times on Back-Country Bond & Gold Trails

While stockholders have thoroughly enjoyed the recent climate, the 2013 weather conditions haven’t been as ideal for gold and bond investors. Gold investors felt less-than-precious in 2013 as they went flying off a cliff and broke a leg. In fact, the shiny metal suffered its worst performance in 30 years and underperformed stocks by a whopping -58%. With this year’s -28% loss (GLD), gold has underperformed stocks over the last six years, after including the impact of dividends.

Like gold traders, most bondholders were wounded in 2013 as well, but they did not get completely buried in an avalanche. Nevertheless, 2013 was a rocky ride overall for the bond haven hunters, as evidenced by the iShares Barclays Aggregate Bond composite (AGG), which fell -4%. As I’ve discussed previously, in Confessions of a Bond Hater, not all bonds are created equally, and actually many Sidoxia client portfolios include shorter-duration bonds, inflation protection bonds, convertible bonds, floating rate bonds, and high-yield bonds. Structured correctly, a thoughtfully constructed bond portfolio can outperform in a rising rate environment like we experienced in 2013.

Although bonds as a broad category may not currently offer great risk-reward characteristics, individuals in the mid-to-latter part of retirement need less volatility and more income – attributes bonds (not stocks) can offer. In other words, certain people are better served by snow-shoeing, or going on sleigh rides rather than risking a wipeout or tree collision on a downhill ski adventure. By owning the right types of bonds, your portfolio can avoid a severe investment crash.

Positive 2014 Outlook but Helmet Advised

With the NASDAQ index having more than tripled to over 4,176 from the 2009 lows, napping spectators are beginning to wake up and take notice. After money hemorrhaged out of the stock market for years (despite positive total returns in 2009, 2010, 2011, 2012), the fear trend began to reverse itself in 2013 and investment capital began returning to stock funds (see Here Comes the Dumb Money).

Adding fuel to the bull market fire, the International Monetary Fund (IMF) head Christine Lagarde recently signaled an increase in economic growth forecasts for the U.S. in 2014, thanks to an improving employment picture, successful Congressional budget negotiations, and actions by the Federal Reserve to unwind unprecedented monetary stimulus. If you consider the added factors of rising corporate profits, improving CEO confidence (e.g., Ford expansion), the shale energy boom, an expanding housing market, and our technology leadership position, one can paint a reasonably optimistic picture for the upcoming years.

Nonetheless, I am quick to remind investors and clients that the pace of the +30% appreciation in 2013 is unsustainable, and we are still overdue for a -10% correction in the major stock indexes.

The fundamental outlook for the economy may be improving, but there are still plenty of clouds on the horizon that could create a short-term market snowstorm. Domestically, we have the upcoming 2014 mid-term elections; debt ceiling negotiations; and a likely continuation of the Federal Reserve tapering program. Abroad, there are Iranian nuclear program talks; instability in Syria; meager and uncertain growth in Europe; and volatile economic climates in emerging markets like China, Brazil and India. After such a large advance this year, any one of these concerns (or some other unforeseen event) could provide an ample excuse to sell stocks and take some profits.

Since wipeouts are common, a protective helmet in the form of a valuation-oriented, globally diversified portfolio is strongly advised. For seasoned skiers and long-term investors, experiencing the never-ending ups and downs of skiing (investing) is a necessity to reach a desired destination. If you have trouble controlling your skis (money/emotions), it’s wise to seek the assistance of an experienced instructor (investment advisor) so your investment portfolio doesn’t crash.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in AGG, GLD, F, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Nail Not in Emerging Market Coffin Yet

I wouldn’t say the nail is in the emerging market coffin quite yet. During the financial crisis, the EMSCI Emerging Market Index (EEM) was left for dead (down -50% in 2008) before resurrection in 2009 and 2010 (up +74% and +16%, respectively). For the last two years however, the EMSCI index has underperformed the S&P 500 Index massively by more than -30%. Included in this international index are holdings from China, Russia, India, Brazil, South Korea, and South Africa, among others.

The question now becomes, can the emerging markets resurrect themselves from the dead again? Recent signs are flashing “yes”. Over the last three months, the emerging markets have outperformed the S&P 500 by more than +8%, but these stocks still have a lot of ground to make up before reaching the peak levels of 2007. Last year’s slowing growth in China and a European recession, coupled with talks of the Federal Reserve’s “tapering” of monetary stimulus, didn’t provide the EMSCI index any help over the last few years.

With all the distracting drama currently taking place in Washington D.C., it’s a relief to see some other indications of improvement. For starters, China’s most recent PMI manufacturing index results showed continued improvement, reaching a level of 51.1 – up from August and signaling a reversal from contraction earlier this year (levels above 50 point to expansion). Chinese government leaders are continuing their migration from an externally export-driven economy to an internally consumer-driven economy. Despite the shift, China is still targeting a respectable +7.5% GDP economic growth target, albeit a slower level than achieved in the past.

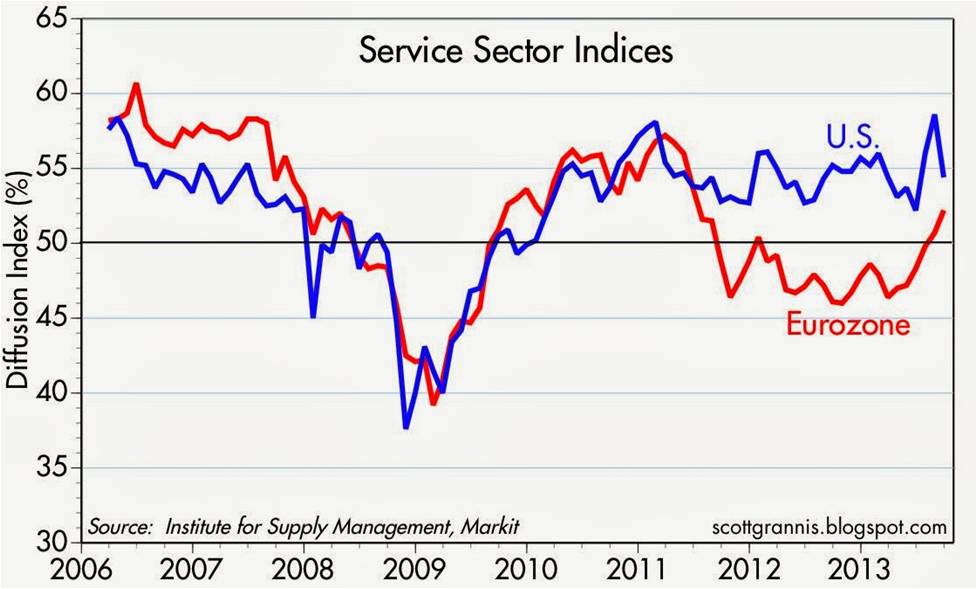

Adding to emerging market optimism is Europe’s apparent economic turnaround (or stabilization). As you can see from the chart below, the European Institute for Supply Management (ISM) service sector index has lately shown marked improvement. If the European and Chinese markets can sustain these recovering trends, these factors bode well for emerging market financial returns.

Source: Calafia Beach Pundit

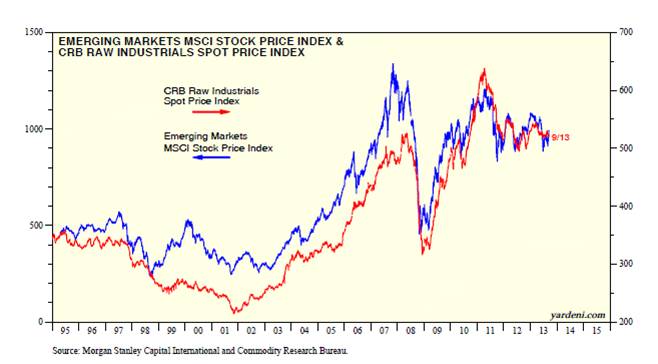

While it is clear these developments are helping the rebound in emerging market indices, it is also clear the supply-demand relationship in commodities will coincide with the next big up or down move in developing markets. Ed Yardeni, strategist and editor of Dr. Ed’s Blog, recently wrote a piece showing the tight correlation between emerging market stock prices and commodity prices (CRB Index). His conclusions come as no surprise to me given these resource-rich markets and their dependence on Chinese demand along with commodity needs from other developed countries. Expanding populations and rising standards of living in emerging market countries have and will likely continue to position these countries well for long-term commodity price appreciation. The development of new, higher-value service and manufacturing sectors should also lead to sustainably improved growth in these emerging markets relative to developed economies.

Source: Dr. Ed’s Blog

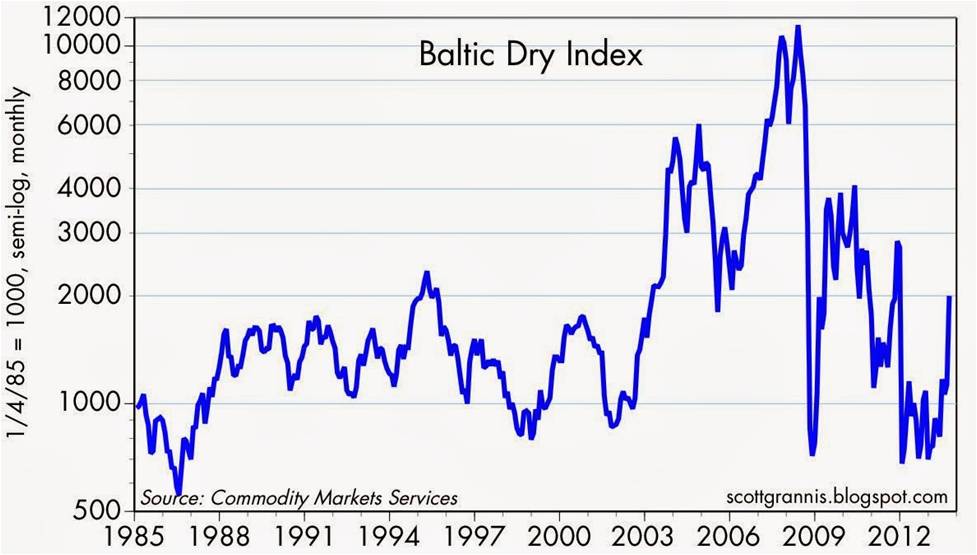

Adding fuel to the improving emerging market case is the advancement in the Baltic Dry Index (see chart below). The recent upward trajectory of the index is an indication that the price for moving major raw materials like coal, iron ore, and grains by sea is rising. This statistical movement is encouraging, but as you can see it is also very volatile.

Source: Calafia Beach Pundit

While the emerging markets are quite unpredictable and have been out-of-favor over the last few years, a truly diversified portfolio needs a healthy dosage of this international exposure. You better check a pulse before you put a nail in the coffin – the emerging markets are not dead yet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including emerging market ETFs, but at the time of publishing, SCM had no direct position in EEM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Vice Tightens for Those Who Missed the Pre-Party

The stock market pre-party has come to an end. Yes, this is the part of the bash in which an exclusive group is invited to enjoy the fruits of the festivities before the mobs arrive. That’s right, unabated access to the nachos; no lines to the bathroom; and direct access to the keg. For those of us who were invited to the stock market pre-party (or crashed it on their own volition), the spoils have been quite enjoyable – about a +128% rebound for the S&P 500 index from the bottom of 2009, and a +147% increase in the NASDAQ Composite index over the same period (excluding dividends paid on both indexes).

Although readers of Investing Caffeine have received a personal invitation to the stock market pre-party since I launched my blog in early 2009, many have shied away, out of fear the financial market cops may come and break-up the party.

Rather than partake in stock celebration over the last four years, many have chosen to go down the street to the bond market party. Unlike the stock market party, the fixed-income fiesta has been a “major-rager” for more than three decades. However, there are a few signs that this party has gotten out-of-control. For example, crowds of investors are lined up waiting to squeeze their way into some bond indulgence; after endless noise, neighbors are complaining and the cops are on their way to shut the party down; and PIMCO’s Bill Gross has just jumped off the roof to do a cannon-ball into the pool.

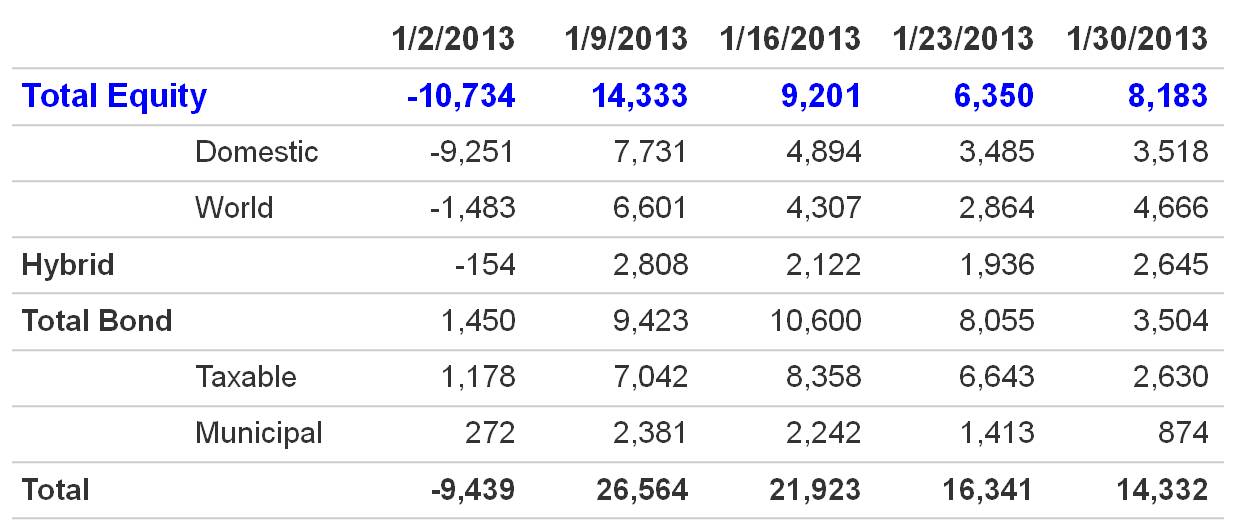

Even though the stock-market pre-party has been a blast, stock prices are still relatively cheap based on historical valuation measurements, meaning there is still plenty of time for the party to roll on. How do we know the party has just started? After five years and about a half a trillion dollars hemorrhaging out of domestic funds (see Calafia Beach Pundit), there are encouraging signs that a significant number of party-goers are beginning to arrive to the party. More specifically, as it relates to stocks, a fresh $10 billion has flowed into domestic equity mutual funds during this January (see ICI chart below). This data is notoriously volatile, and can change dramatically from month-to-month, but if this month’s activity is any indication of a changing mood, then you better hurry to the stock party before the bouncer stops letting people in.

Source: Investment Company Institute (ICI)

Vice Begins to Tighten on Party Outsiders

Many stock market outsiders have either been squeezed into the bond market, hidden in cash, or hunkered down in a bunker with piles of gold. While some of these asset classes have done okay since early 2009, all have underperformed stocks, but none have performed worse than cash. For those doubters sitting on the equity market sidelines, the pain of the vice squeezing their portfolios has only intensified, especially as the economy and employment picture slowly improves (see chart below) and stock prices persist directionally upward. For years, fear-mongering stock skeptics have warned of an imploding dollar, exploding inflation, a run-away deficit/debt, a reckless money-printing Federal Reserve, and political gridlock. Nevertheless, none of these issues have been able to kill this equity bull market.

Source: Calafia Beach Pundit

But for those willing and able investors to enter the stock party today, one must realize this party will only get riskier over time. As we exit the pre-party and enter into the main event, you never know who may join the party, including some uninvited guests who may steal money, get sick on the carpet, participate in illegal activities, and/or ruin the fun by clashing with guests. We have already been forced to deal with some of these uninvited guests in recent years, including the “flash crash,” debt ceiling debate, European financial crisis, fiscal cliff, and lastly, sequestration is about to arrive as well (right after parking his car).

New investors can still objectively join the current equity party, but it is necessary to still be cognizant of not over-staying your welcome. However, for those party-pooping doubters who already missed the pre-party, the vice will continue to tighten, leaving stock cynics paralyzed as they watch additional missed opportunities enjoyed by the rest of us.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, Japanese ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}

{kind=link}