Posts tagged ‘equity’

Stocks: Be My Long-Term Valentine

With Valentine’s Day just around the corner, stock bulls remain in love as the major indexes once again hit another new, all-time record high this week (Dow 20,269). Unfortunately, however, there are many other investors afraid of going through another 2008-2009-like break-up, so they remain single as they watch from the sidelines. In a recent post, I point out, as repeated record highs continue to be broken, the skeptics remain fearful of divorcing their cash. While it is indeed true that since the end of the 2016 presidential election, some investors are beginning to date stocks again, there are still wide swaths of conflicted observers very afraid of potential rejection.

As I’ve documented on numerous occasions, the skepticism is evident in the depressing long-term trends found in the weekly fund flows data and the disheartening record-low stock ownership statistics.

Long-Term Relationships

For some, casually dating can be fun and exciting. The same principle applies to short-term traders and speculators. In the short-run, the freedom to make free-wheeling, non-committal stock purchases can be exhilarating. Unfortunately, the fiscal and emotional costs of short-term dating/trading often outweigh the fleeting benefits.

How can you avoid the relationship blues? In short…focus on the long-term. Like any relationship, investing takes work, and there will always be highs, lows, and bumps in the road. It is better to think in terms of a marathon, rather than a sprint. The important lesson is to maintain a systematic, disciplined approach that you can apply irrespective of the changing investment environment. In other words, that means not loosely reacting (buying or selling) to presidential tweets of the day.

Famed investor Peter Lynch spoke about long-term stock fund investing in this manner

“If you invest in mutual funds and make mutual funds investment changes in less than 10 years…you’re really just ‘dating.’ Investing in mutual funds should be marital – for richer, for poorer, and so on; mutual fund decisions should be entered into soberly and advisedly and for the truly long term.”

No relationship survives without experiencing wild swings, and stocks are no exception. Establishing deep roots to your investments via intensive fundamental analysis provides stability, especially if you are managing your portfolio personally. Even if you are outsourcing your investment management to an advisor like Sidoxia Capital Management, it is still important to understand your advisor’s investment process and philosophy. That way, when the economic and political winds are blowing fiercely, you won’t overreact emotionally and see your gains fly away.

Investing legend Warren Buffett has discussed the importance of intensive research on long-term investment performance through his “20-Hole Punch Card” rule:

“I could improve your ultimate financial welfare by giving you a ticket with only twenty slots in it so that you had twenty punches – representing all the investments that you got to make in a lifetime. And once you’d punched through the card, you couldn’t make any more investments at all. Under those rules, you’d really think carefully about what you did, and you’d be forced to load up on what you’d really thought about. So you’d do so much better.”

Patience is a Virtue

In the instant gratification society we live in, patience is difficult to come by, and for many people ignoring the constant chatter of fear is challenging. Pundits spend every waking hour trying to explain each blip in the market, but in the short-run, prices often move up or down regardless of the daily headlines.

Explaining this randomness, Peter Lynch said the following:

“Often, there is no correlation between the success of a company’s operations and the success of its stock over a few months or even a few years. In the long term, there is a 100% correlation between the success of a company and the success of its stock. It pays to be patient, and to own successful companies.”

Long-term investing, like long-term relationships, is not a new concept. Investment time horizons have been shortening for decades, so talking about the long-term is generally considered heresy. Rather than casually dating your investments, perhaps you should commit to a long-term relationship and divorce your bad short-term centric habits. Now that sounds like a sweet Valentine’s Day kiss your investment portfolio would enjoy.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, T, FB and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

PIMCO and Stocks: The Slow Motion Train Wreck

I believe it was Bill Clinton who said, “If you don’t toot your horn, it usually stays untooted.” Good advice, but keeping his horn concealed may have helped his political and personal career in a few instances too.

In sticking with the horn metaphor, I will toot my own horn as it relates to my skepticism about bond behemoth PIMCO’s long failed attempt to enter the equity fund market. Since 2009, watching PIMCO’s efforts of gaining credibility in stock investing has been like observing a slow motion train wreck.

Although, PIMCO may continue its flailing struggles in its so-called equity offerings, the proverbial nail in the coffin was announced last week when PIMCO’s chief investment officer of global equities, Virginie Maisonneuve, left the bond giant after only a year. This departure adds to the list of high profile departures, including Bill Gross, Mohamed El-Erian, Paul McCulley, Neel Kashkari, and others.

The Wall Street Journal states PIMCO only has $3 billion (0.2%) of the firms $1.6 trillion of assets remaining in actively traded stock funds. PIMCO claims to have more assets in equity funds managed by Research Affiliates but good luck finding any stocks in these portfolios – for example, Morningstar lists 0 Stock Holdings and 698 Bond Holdings in its PIMCO RAE Fundamental Plus EMG Stock Fund. And please explain to me how this is a stock fund?

Regardless, any way you look at it PIMCO continues to flounder in its stock fund efforts. If you would like to read more about my victory lap, please reference my previous February 2013 PIMCO article, Beware: El-Erian & Gross Selling Buicks…Not Chevys.

Here is a partial excerpt:

PIMCO Smoke & Mirrors: Stock Funds with NO Stocks

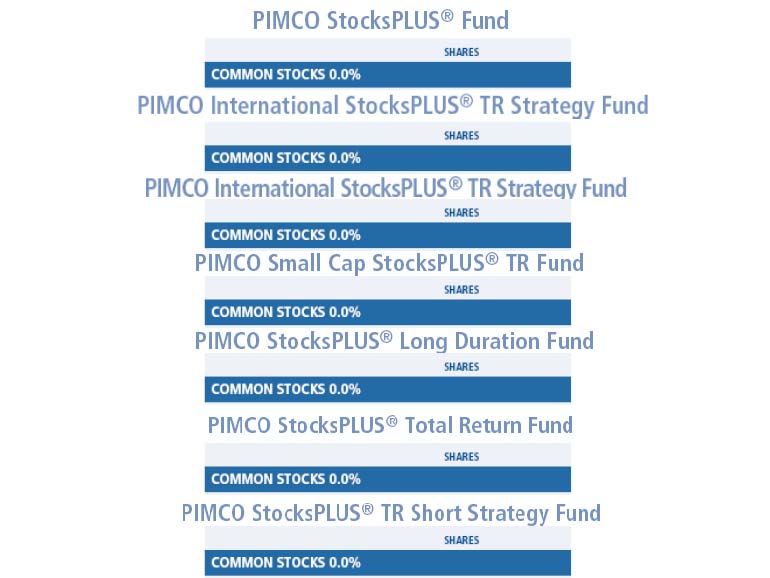

Just when I thought I had seen it all, I came across PIMCO’s Equity-Related funds. Never in my career have I seen “equity” mutual funds that invest solely in “bonds.” Well, apparently PIMCO has somehow creatively figured out how to create stock funds without investing in stocks. I guess that is one strategy for a bond-centric company of getting into the equity fund market? This is either ingenious or bordering on the line of criminal. I fall into the latter camp. How the SEC allows the world’s largest bond company to deceivingly market billions in bond-filled stock funds to individual investors is beyond me. After innocent people got fleeced by unscrupulous mortgage brokers and greedy lenders, in this Dodd-Frank day and age, I can’t help but wonder how PIMCO is able to solicit a StockPlus Fund that has 0% invested in common stocks. You can judge for yourself by reviewing their equity-related funds on their website (see also chart below):

PIMCO Equity-Related Funds with No Equity

PIMCO Active Equity Funds Struggle

With more than 99% of PIMCO’s $2 trillion in assets under management locked into bonds, company executives have made a half-hearted effort of getting into the equity markets, even though they’ve enjoyed high-fiving each other during the three-decade-long bond bull market (see Downhill Marathon Machine). In hopes of diversifying their bond-heavy revenue stream, in 2009 they hired the head of the high-profile $700 billion, government TARP program (Neil Kashkari). Subsequently, PIMCO opened its first set of actively managed funds in 2010. Regrettably for PIMCO, the sledding has been quite tough. In 2012, all six actively managed equity funds lagged their benchmarks. Moreover, just a few weeks ago, Kashkari their rock star hire decided to quit and pursue a return to politics.

Mohamed El-Erian and Bill Gross have never been camera shy or bashful about bashing stocks. PIMCO has virtually all their bond eggs in one basket and their leaderless equity division is struggling. What’s more, like some car salesmen, they have had a creative way of describing the facts. If it’s a Chevy or unbiased advice you’re looking for, I recommend you steer clear from Buick salesmen and PIMCO headquarters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in PEFAX or any other PIMCO security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Dividends: From Sapling to Abundant Fruit Tree

Dividends are like fruit and an investment in stock is much like purchasing a sapling. When purchasing a stock (sapling) the goal is two-fold: 1) Buy a sapling (tree) that is expected to bear a lot of fruit; and 2) Pay a cheap or fair price. If the right saplings are purchased at the right prices, then investors can enjoy a steady diet of fruit that has the potential of producing more fruit each year. Fruit can come in the form of future profits, but as we will see, the sweetness of a profitable company also paying dividends can prove much more fruitful over the long-term.

Investing in growth equities at reasonable prices seems like a pretty intelligent strategy, but of late the vast majority of fresh investor capital has been piling into bonds. This is not a flawed plan for retirees (and certain wealthy individuals) and should be a staple in all investment portfolios, to a degree (some of my client portfolios contain more than 80%+ in fixed income-like securities), but for many investors this overly narrow bond focus can lead to suboptimal outcomes. Right now, I like to think of bonds like a reliable bag of dried fruit, selling for a costly price. However, unlike stocks, bonds do not have the potential of raising periodic payments like a sapling with strong growth prospects. “Double-dippers” who are expecting the economy to spiral into a tailspin, along with nervous snakebit equity investors, prefer the reliability of the bagged dry fruit (bonds)… no matter how high the price.

How Sweet is the Fruit? How Does a +2,300% Yield Sound?

Not only do equities offer the potential of capital appreciation, but they also present the prospect of dividend hikes in the future – important characteristics, especially in inflationary environments. Bonds, on the other hand, offer static fixed payments (no hope of interest rate hikes) with declining purchasing power during periods of escalating general prices.

Given the possibility of a “double-dip” recession, one would expect corporate executives to be guarding their cash with extreme stinginess. On the contrary, so far in 2010, companies have shown their confidence in the recovery by increasing or initiating dividends at a +55% higher clip versus the same period last year. Underpinning these announcements, beyond a belief in an economic recovery, are large piles of cash growing on the balance sheets of nonfinancial companies. According to Standard & Poor’s (S&P), cash hit a record $837 billion at the end of March, up from $665 billion last year.

The S&P 500 dividend yield at 2.06% may not sound overwhelmingly high, but with CDs and money markets paying next to nothing, the Federal Funds rate at effectively 0%, and the 10-Year Treasury Note yielding an uninspiring 3.11%, the S&P yield looks a little more respectable in that light.

If the stock market yield doesn’t enthuse you, how does a +2,300% yield sound to you? That’s roughly what a $.05 (split adjusted) purchase of Wal-Mart (WMT) stock in 1972 would be earning you today based on the current $1.21 dividend per share paid today. That return alone is mind-blowing, but this analysis doesn’t even account for the near 1,000-fold increase in the stock price over the similar timeframe. That’s what happens if you can find a company that increases its dividend for 37 consecutive years.

Procter & Gamble (PG) is another example. After PG increased its dividend for 54 consecutive years, from a split-adjusted $.01 per share in 1970 to a $1.93 payout today, original shareholders are earning an approximate 245% yield on their initial investment (excluding again the massive capital appreciation over 40 years). There’s a reason investment greats like Warren Buffett have invested in great dividend franchises like WMT, PG, KO, BUD, WFC, and AXP.

Bad Apples do Exist

Dividend payment is not guaranteed by any means, as evidenced by the dividend cuts by financial institutions during the 2008-2009 crisis (e.g., BAC, WFC, C) or the discontinuation of BP PLC’s (BP) dividend after the Gulf of Mexico oil spill disaster. Bonds are not immune either. Although bonds are perceived as “safe” investments, the interest and principal payment streams are not fully insured – just ask bondholders of bankrupt companies like Lehman Brothers, Visteon, Tribune, or the countless other companies that have defaulted on their debt promises.

This is where doing your homework by analyzing a company’s competitive positioning, financial wherewithal, and corporate management team can lead you to those companies that have a durable competitive advantage with a corporate culture of returning excess capital to shareholders (see Investing Caffeine’s “Education” section). Certainly finding a WMT and/or PG that will increase dividends consistently for decades is no easy chore, but there are dozens of budding possibilities that S&P has identified as “Dividend Aristocrats” – companies with a multi-year track record of increasing dividends. And although there is uncertainty revolving around dividend taxation going into 2011, I believe it is fair to assume dividend payment treatment will be more favorable than bond income.

Apple Allocation

Growth companies that reinvest profits into new value-expanding projects and/or hoard cash on the balance sheet may make sense conceptually, but dividend paying cultures instill a self-disciplining credo that can better ensure proper capital stewardship by corporate boards. All too often excess capital is treated as funny money, only to be flushed away by overpaying for some high-profile acquisition, or meaningless share buybacks that merely offset generous equity grants to employees.

So, when looking at new and existing investments, consider the importance of dividend payments and dividend growth potential. Investing in an attractively priced sapling with appealing growth prospects can lead to incredibly fruitful returns.

Read the Whole WSJ Article on Dividends

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct positions in BAC, WFC, C, BP, PG, KO, BUD, WFC, AXP, Lehman Brothers, Visteon, Tribune, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}