Posts tagged ‘equity risk premium’

Waiting for the Fat Pitch

Fall is here and the leaves are beginning to change, which means it’s baseball playoffs time and the World Series is quickly approaching. Investing in some respects is similar to baseball because they both require discipline and patience. One investing legend who embodies those characteristics is Warren Buffett, and he has repeatedly spoken about Ted Williams and waiting for the “fat pitch.”

John Huber, over at BHI, did a great job summarizing Ted Williams’ hitting philosophy here:

“Ted Williams was famous for “waiting for the fat pitch”. He would only look to swing at pitches in the part of the strike zone where he knew he had a higher probability of getting a hit. There were parts of his strike zone where he batted .230 and there were other parts of the strike zone where he batted .400. He knew that if he waited for a pitch over the heart of the plate and didn’t swing at pitches in the .230 part of the strike zone—even though they were strikes—he would improve his odds of getting a hit and increase his overall batting average.”

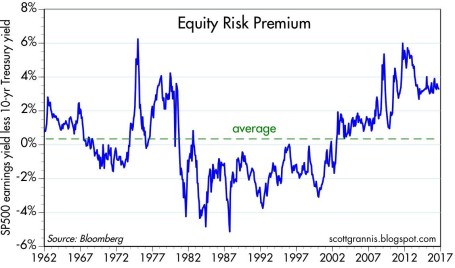

This lesson of patience and discipline is critical for your investment portfolio. Too many people speculate by chasing a hot tip or good stock story, or on the flip side, panic by selling based upon transitory negative news headlines. Today, we see risk aversion happening on steroids. Consider there is over $8 trillion sitting in savings accounts earning effectively nothing – the equivalent of stuffing money under the mattress (see also Invest or Die). In other words, investors are paying extremely high prices (chasing) for safer (less volatile) securities – bonds and cash, while equities are yielding a much higher rate as measured by the earnings yield of the S&P 500 (S&P operating profits / index value). Scott Grannis at Calafia Beach Pundit calls this dynamic the equity risk premium (chart below).

Source: Scott Grannis

As you can see from the chart, ever since the financial crisis occurred, stocks have been compensating investors at significantly higher levels (almost 4% currently) than the yields on 10-Year Treasury Notes, a phenomenon not experienced for the previous three decades.

When will this equity premium revert back towards the mean? There are number of factors that could correct this disparity.

1). The economy enters recession and profits decline to a point at which bonds offer a more compelling risk-reward ratio than stocks.

2). Interest rates rise (bond prices decline) to a point at which bonds offer a more compelling risk-reward ratio than stocks.

3). Investors bid stocks significantly higher to a point at which bonds offer a more compelling risk-reward ratio than stocks.

Most people are worried about scenario #1, but there is plenty objective data that splashes cold water on that view. Consider the unemployment rate has been chopped in half since 2009 with about 15 million jobs added; corporate profits are at/near record highs; auto sales are at/near record highs; home sales continue on an improving trajectory; and the yield curve remains positive, among other factors. If you absorb that information, it clearly doesn’t resemble a recessionary environment, but that doesn’t prevent people from worrying.

Regarding scenario #2, rising rates are an eventuality, but an absence of meaningful inflation, coupled with sluggish global growth are likely to keep a lid on interest rates for some time. Any casual observer would realize that interest rates have been on a downward trend for more than 35 years (see also Fall is Here: Change is Near). Even with a potential second rate increase in a decade initiated by the Fed this upcoming December, the long-term downward trend in rates will likely remain intact.

While the media likes to focus on the half-glass full scenarios (#1 & #2), very little time has been expended on the possibility of scenario #3, which contemplates a rise in stock prices to erase the discount in stock prices relative to bond prices (i.e., elevated equity risk premium).

While many people are ignoring the probability of scenario #3 occurring, like a disciplined hitter in baseball, successful investing requires patience while you wait for your fat investment pitch.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

Chicken or Beef? Time for a Stock Diet?

The stock market has been gorging on gains over the last six years and the big question is are we ready for a crash diet? In other words, have we consumed too much, too fast? Since the lows of 2009 the S&P 500 index has more than tripled (or +209% without dividends).

In our daily food diets our proteins of choice are primarily chicken and beef. When it comes to finances, our investment choices are primarily stocks and bonds. There are many factors that can play into a meat-eaters purchase decision, including the all-important factor of price. When the price of beef spikes, guess what? Consumers rationally vote with their wallets and start substituting beef for relatively lower priced chicken options.

The same principle applies to stocks and bonds. And right now, the price of bonds in general have gone through the roof. In fact bond prices are so high, in Europe we are seeing more than $2 trillion in negative yielding sovereign bonds getting sucked up by investors.

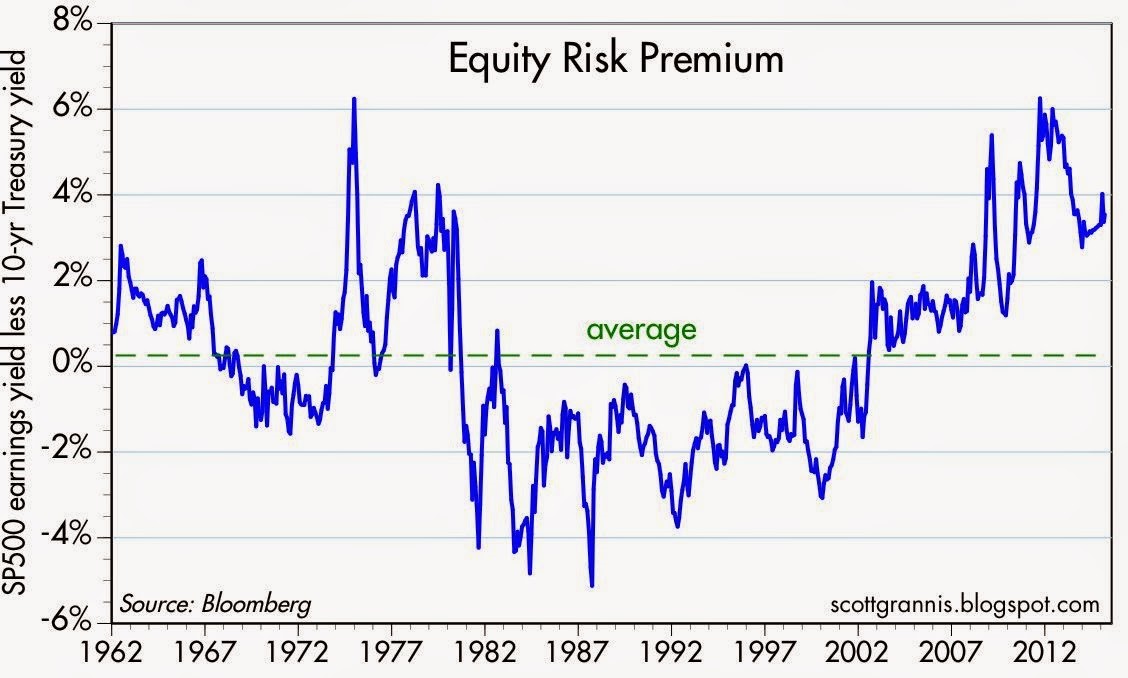

Another area where we see evidence of pricey bonds can be found in the value of current equity risk premiums. Scott Grannis of Calafia Beach Pundit posted a great 50-year history of this metric (chart below), which shows the premium paid to stockholders over bondholders is near the highest levels last seen during the Great Recession and the early 1980s. To clarify, the equity risk premium is defined as the roughly 5.5% yield currently earned on stocks (i.e., inverse of the approx. 18x P/E ratio) minus the 2.0% yield earned on 10-Year Treasury Notes.

Source: Scott Grannis

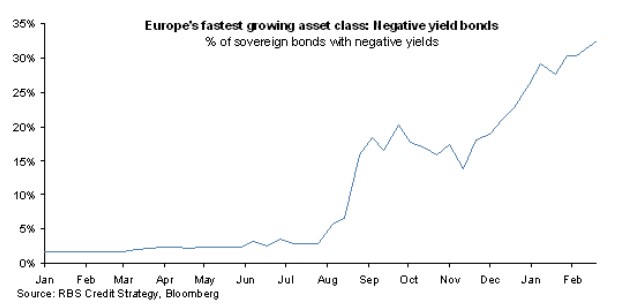

The equity risk premium even looks more favorable if you consider the negative interest rate European environment mentioned earlier. The 60 billion euros of monthly debt in ECB (European Central Bank) quantitative easing purchases has accelerated the percentage of negative yield bond issuance, as you can see from the chart below.

Source: FT Alphaville

Hibernating Bond Vigilantes

Dr. Ed Yardeni coined the famous phrase “bond vigilantes” to describe the group of hedge funds and institutional investors who act as the bond market sheriffs, ready to discipline any over leveraged debt-issuing entity by deliberately cratering prices via bond sales. For now, the bond vigilantes have in large part been hibernating. As long as the vigilantes remain asleep at the switch, stock investors will likely continue earning these outsized premiums.

How long will these fat equity premiums and gains stick around? A simple diet of sharp interest rate increases or P/E expansion would do the trick. An increase in the P/E ratio could come in one of two ways: 1) sustained stock price appreciation at a rate faster than earnings growth; or 2) a sharp earnings decline caused by a recessionary environment. On the bright side for the bulls, there are no imminent signs of interest rate spikes or recessions. If anything, dovish commentary coming from Fed Chairwoman Janet Yellen and the FOMC would indicate the economy remains in solid recovery mode. What’s more, a return to normalized monetary policy will likely involve a very gradual increase in interest rates – not a piercing rise as feared by many.

Regardless of whether it’s beef prices or bond prices spiking, rather than going on a crash diet, prudently allocating your money to the best relative value will serve your portfolio and stomach best over the long run.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Can the Lost Decade Strike Twice?

There is an old saying that lightning does not strike twice in the same place. I firmly believe this principle will apply to stock returns over the next decade. Josh Brown, investor and writer for The Reformed Broker highlighted a chart published by Bloomberg showing the 10-year return for various asset classes. Statisticians and market commentators have been quick to point out that stocks, as measured by various benchmarks, have not only underperformed bonds for the last 10 years, but stock performance has actually also been negative for the trailing decade.

Source: Bloomberg via The Reformed Broker

Will this trend persist during the next decade? Will the lost decade in stocks be repeated again, similar to the deflation death spiral experienced by the Japanese? (Read more regarding Japanese market on IC). With the Fed Funds rate at effectively zero, is it possible bonds can pull off a miracle over the next 10 years? I suppose anything is possible, but I seriously doubt it.

Let’s not forget that the P/E ratio (Price-Earnings) pegged by some to be at about 14-15x’s 2010 expected earnings – nestled comfortably within historical bands. Granted, financials and some other sectors were overheated (e.g. certain Consumer industries), but based on next year’s estimates, some industries are already expected to exceed the peak earnings achieved during 2007 (e.g., Technology).

History on Our Side

Source: Crestmont Research. Dated graph over the last century showing stock returns rarely result in negative returns over a rolling 10 year period.

For the trailing decade using December 20, 2009 as an end point, I arrive at a marginally negative return for the S&P 500 index assuming an average dividend yield of 2.5% for the period. Certainly the negative return would be pronounced by any fees, commissions or taxes related to a 10-year buy-and-hold strategy of the broad market index. This chart gets chopped off in 2005, nonetheless history is on our side, lending support that stock returns have a good chance of improving on the results over the last 10 years.

Equity Risk Premium

The bubbles and scandals that have blanketed corporate America over the last 10 years have made the average investor extremely skeptical. What does this mean for the pricing of risk? Well, if you rewind to the year 2000 when technology exceeded 50% of some indexes, and many investors thought technology was a low risk endeavor, there was virtually no equity risk premium discounted into many stock prices. If you fast forward to today, the reverse is occurring. Investors despise market volatility and arguably demand a much higher risk premium for taking on the instability of stocks. This is the exact environment investors should desire – lots of skepticism and money piled into bonds (See IC article on investor queasiness). As Warren Buffett says, “Be fearful when others are greedy and greedy when others are fearful.” I believe the next 10 years will be a time to be greedy.

The analysis above is obviously very narrow in scope, since we are only discussing domestic stock markets. In my client portfolios I advocate a broadly diversified portfolio across asset classes (including bonds), geographies, and styles. However, in managing bonds across portfolios, I am forced to tactfully include strategies such as inflation protection and shorter duration techniques. With the year-end fast approaching, now is a good time to review your financial goals and asset allocation.

Lightning definitely negatively impacted stocks this decade, but betting for lightning to strike twice this decade could very well turn out to be a losing wager.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct positions in BRKA. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}