Posts tagged ‘emotions’

Cutting Losses with Fisher’s 3 Golden Sell Rules

Returning readers to Investing Caffeine understand this is a location to cover a wide assortment of investing topics, ranging from electric cars and professional poker to taxes and globalization. Investing Caffeine is also a location that profiles great investors and their associated investment lessons.

Today we are going to revisit investing giant Phil Fisher, but rather than rehashing his accomplishments and overall philosophy, we will dig deeper into his selling discipline. For most investors, selling securities is much more difficult than buying them. The average investor often lacks emotional self-control and is unable to be honest with himself. Since most investors hate being wrong, their egos prevent taking losses on positions, even if it is the proper, rational decision. Often the end result is an inability to sell deteriorating stocks until capitulating near price bottoms.

Selling may be more difficult for most, but Fisher actually has a simpler and crisper number of sell rules as compared to his buy rules (3 vs. 15). Here are Fisher’s three sell rules:

1) Wrong Facts: There are times after a security is purchased that the investor realizes the facts do not support the supposed rosy reasons of the original purchase. If the purchase thesis was initially built on a shaky foundation, then the shares should be sold.

2) Changing Facts: The facts of the original purchase may have been deemed correct, but facts can change negatively over the passage of time. Management deterioration and/or the exhaustion of growth opportunities are a few reasons why a security should be sold according to Fisher.

3) Scarcity of Cash: If there is a shortage of cash available, and if a unique opportunity presents itself, then Fisher advises the sale of other securities to fund the purchase.

Reasons Not to Sell

Prognostications or gut feelings about a potential market decline are not reasons to sell in Fisher’s eyes. Selling out of fear generally is a poor and costly idea. Fisher explains:

“When a bear market has come, I have not seen one time in ten when the investor actually got back into the same shares before they had gone up above his selling price.”

In Fisher’s mind, another reason not to sell stocks is solely based on valuation. Longer-term earnings power and comparable company ratios should be considered before spontaneous sales. What appears expensive today may look cheap tomorrow.

There are many reasons to buy and sell a stock, but like most good long –term investors, Fisher has managed to explain his three-point sale plan in simplistic terms the masses can understand. If you are committed to cutting investment losses, I advise you to follow investment legend Phil Fisher – cutting losses will actually help prevent your portfolio from splitting apart.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Searching for the Market Boogeyman

With the stock market reaching all-time record highs (S&P 500: 1900), you would think there would be a lot of cheers, high-fiving, and back slapping. Instead, investors are ignoring the sunny, blue skies and taking off their rose-colored glasses. Rather than securely sleeping like a baby (or relaxing during a three-day weekend) with their investment accounts, people are biting their fingernails with clenched teeth, while searching for a market boogeyman in their closets or under their beds.

If you don’t believe me, all you have to do is pick up the paper, turn on the TV, or walk over to the office water cooler. An avalanche of scary headlines that are spooking investors include geopolitical concerns in Ukraine & Thailand, slowing housing statistics, bearish hedge fund managers (i.e., Tepper Einhorn, Cooperman), declining interest rates, and collapsing internet stocks. In other words, investors are looking for things to worry about, despite record corporate profits and stock prices. Peter Lynch, the manager of the Magellan Fund that posted +2,700% in gains from 1977-1990, put short-term stock price volatility into perspective:

“You shouldn’t worry about it. You should worry what are stocks going to be 10 years from now, 20 years from now, 30 years from now.”

Rather than focusing on immediate stock market volatility and other factors out of your control, why not prioritize your time on things you can control. What investors can control is their asset allocation and spending levels (budget), subject to their personal time horizons and risk tolerances. Circumstances always change, but if people spent half the time on investing that they devoted to planning holiday vacations, purchasing a car, or choosing a school for their child, then retirement would be a lot less stressful. After realizing 99% of all the short-term news is nonsensical noise, the next important realization is stocks are volatile securities, which frequently go down -10 to -20%. As much as amateurs and professionals say or think they can profitably predict these corrections, they very rarely can. If your stomach can’t handle the roller-coaster swings, then you shouldn’t be investing in the stock market.

Bear-markets generally coincide with recessions, and since World War II, Americans experience about two economic contractions every decade. And as I pointed out earlier in A Series of Unfortunate Events, even during the current massive bull market, a recession has not been required to suffer significant short-term losses (e.g., Flash Crash, Greece, Arab Spring, Obamacare, Cyprus, etc.). Seasoned veterans understand these volatile periods provide incredible investment opportunities. As Warren Buffett states, “Be fearful when others are greedy, and be greedy when others are fearful.” Fear and panic may be behind us, but skepticism is still firmly in place. Buying during current skepticism is still not a bad thing, as long as greed hasn’t permeated the masses, which remains the case today.

Overly emotional people that make investment decisions with their gut do more damage to their savings accounts than conservative, emotional investors who understand their emotional shortcomings. On the other hand, the problem with investing too conservatively, for those that have longer-term time horizons (10+ years), is multi-pronged. For starters, overly conservative investments made while interest rate levels hover near historical lows lead to inflationary pressures gobbling up savings accounts. Secondly, the low total returns associated with excessively conservative investments will result in a later retirement (e.g., part-time Wal-Mart greeter in your 80s), or lower quality standard of living (e.g., macaroni & cheese dinners vs. filet mignon).

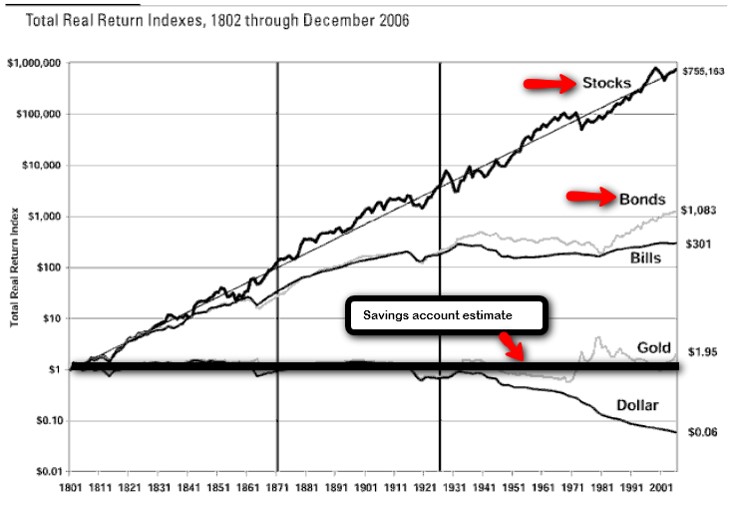

Most people say they understand the trade-offs of risk and return. Over the long-run, low-risk investments result in lower returns than high risk investments (i.e., bonds vs. stocks). If you look at the following chart and ask anyone what their preferred path would be over the long-run, almost everyone would select the steep, upward-sloping equity return line.

Source: Betterment.com / Stocks for the Long Run

Yet, stock ownership and attitudes towards stocks remain at relatively low and skeptical levels (see Gallup survey in Markets Soar and Investors Snore). It’s true that attitudes are changing at a glacial pace and bond outflows accelerated in 2013, but more recently stock inflows remain sporadic and scared money is returning to bonds. Even though it has been over five years, the emotional scars from 2008-2009 apparently still need some time to heal.

Investing in stocks can be very scary and hazardous to your health. For those millions of investors who realize they do not hold the emotional fortitude to withstand the ups and downs, leave the worrying responsibilities to the experienced advisors and investment managers like me. That way you can focus on your job and retirement, while the pros can remain responsible for hunting and slaying the boogeyman.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing with the Sentiment Pendulum

Article is an excerpt from Sidoxia Capital Management’s complementary May 2012 newsletter. Subscribe on right side of page.

The last five years have been historic in many respects. Not only have governments and central banks around the world undertaken unprecedented actions in response to the global financial crisis, but investors have ridden an emotional rollercoaster in response to historically unparalleled uncertainties.

While the nature of this past crisis has been unique, experienced investors know these fears continually manifest themselves in different forms over various cycles in time. Despite the more than doubling in equity market values over the last few years, as measured by the S&P 500 index, the emotional pendulum of investor sentiment has only partially corrected. Investor temperament has thankfully swung away from “Panic,” but has only moved closer to “Fear” and “Skepticism.” Here are some of the issues contributing to investors’ current sour mood:

The Next European Domino: The fear of the Greek domino toppling the larger Spanish and Italian economies has investors nervously chewing their finger-nails, and political turmoil in France and the Netherlands isn’t creating any additional warm and fuzzies.

Job Additions Losing Steam: New job creation here in the U.S. weakened to a lethargic monthly rate of +120,000 new jobs in March, while the unemployment rate remains stubbornly high at an 8.2% level.

Domestic Growth Losing Mojo: GDP (Gross Domestic Product) growth of +2.2% during the first quarter of 2012 also opened the door for the pessimists. Consumers are still spending (+2.9% growth), but government spending, business investment, and housing are taking wind out of the economy’s sails.

Emerging Markets Submerging: Unspectacular growth in the U.S. is not receiving any favors from slowing emerging markets like China and Brazil, which took fiscal and monetary actions to slow inflation and housing speculation in 2011.

Humpty Dumpty Politics: Presidential elections, tax policy, and deficit reduction are all concerns that carry the possibility of pushing the economic Humpty Dumpty off the wall, and as a result potentially lead to a great fall. The determination of Humpty Dumpty’s fate will likely have to wait until year-end or 2013.

Any student of history knows these fears and other concerns never go away – they simply change. But like supply and demand, gravitational forces eventually swing the emotional pendulum in the opposite direction. As Sir John Templeton so aptly stated, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” Or in other words, escalating bull markets must climb the proverbial “Wall of Worry” in order to sustain upward momentum. If there was nothing to worry about, then all the buyers would already be in the markets. We are nowhere close to experiencing “Euphoria” like we saw in stocks during the late-1990s or in the housing market around 2005.

Positively Climbing the “Wall of Worry”

With all this bad news out there, surprisingly there are some glimmers of hope chipping away at the “Wall of Worry.” Here are some of the positive factors helping turn pessimist frowns upside down:

Slow & Steady Wins the Race: The economic recovery has been weaker than hoped, but I can think of worse scenarios than 11 consecutive quarters of GDP growth and 25 straight months of private job creation, which has reduced the unemployment rate from 10.0% in October 2009 to 8.2% last month.

Earnings Machine Keeps Chugging Along: With the majority of S&P 500 companies having reported their quarterly results for the first quarter, three-fourths of the companies are beating forecasted earnings, which are currently registering in at a respectable +7.1% rate (Thomson Reuters). One company epitomizing this trend is Apple Inc. (AAPL). The near doubling in Apple’s profits during the quarter, thanks to explosive iPhone sales, pushed Apple’s shares over $600 and helped drive the NASDAQ index to its best day of the year.

Super Ben to the Rescue: The Federal Reserve has already stated their intention of keeping interest rates near 0% until 2014. The potential of additional monetary stimulus spearheaded by Federal Reserve Chairman Ben Bernanke, in the form of QE3 (Quantitative Easing Part III), may provide further needed support to the stock market (a.k.a., the “Bernanke Put”).

Return of the IPO: Initial Public Offerings (IPOs) have gained steam versus last year with more than 53 already coming to market in the first four months of 2012. This is no 1999, but a good number of deals have done quite well over the last month. For example, data analysis company Splunk Inc. (SPLK) share price is already up around 100% and the value of leisure luggage company TUMI Holdings (TUMI) has climbed over +40%. In a few weeks, the highly anticipated blockbuster Facebook (FB) IPO is expected to begin trading its shares, so we can see if the chronicled deal can live up to all the hype.

Dividends Galore: Dividend payments to stockholders are flowing at an extraordinary rate so far in 2012. Companies like IBM (increased its dividend by +13%), Exxon Mobil – (XOM +21%); Goldman Sachs – (GS +31%) are but just a few of the dividend raisers this year. Through the first three months of the year, the number of companies increasing their dividend payments was up +45% as compared to the comparable number for all of 2011.

Emerging Growth Not Dead: While worriers fret over slowing growth in China, companies like Apple grew by more than +100% in this region and collected nearly 20% of its revenues from this Asian country (~$8 billion). Coincidentally, China is expected to surpass an incredible one billion mobile connections in May – many of those iPhones. In other related news, Starbucks Corp. (SBUX) plans to triple its workforce and number of stores in China over the next three years. China has also helped fuel a backlog of Caterpillar Inc. (CAT) that is more than triple the level of 2009. Emerging markets may have slowed down in 2011, but with inflation beginning to stabilize, emerging market central banks and governments are now beginning to ease policies and reduce red-tape. For example, Brazil and India have started to lower key benchmark interest rates, and China has started to reverse capital flow restrictions.

Stay Off the Trampled Path

The mantra of “Sell in May and go away” always gets a lot of playtime around this period of the year. Over the last few years, the temporary spring/summer sell-offs have only been followed by stronger price appreciation. Individuals attempting to time the market (see also Getting Off the Treadmill) generally end up in tears. And for those traders who boast about their excellent timing (like those suspicious friends who brag about always winning in Las Vegas), we all know the truth – nobody buys at the lows and sells at the highs…except for liars.

With all the noise and cross-currents flooding the airwaves, investing for individuals without assistance has never been so difficult. But before hiding in your cave or reacting to the next scary headline about Europe, the economy, or politics, do yourself a favor by reminding yourself these chilling news items are nothing new and are often great contrarian indicators (see also Back to the Future). The emotional pendulum is constantly swinging from fear to greed and investors stand to prosper by adjusting sentiment and actions in the opposite direction. To survive in the investing wild, it is best to realize that the grass is greener and the eating more abundant when you stay off the trampled path of the herd.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in SPLK, TUMI, IBM, XOM, GS, SBUX, CAT, FB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Cutting Losses with Fisher’s 3 Golden Sell Rules

Returning readers to Investing Caffeine understand this is a location to cover a wide assortment of investing topics, ranging from electric cars and professional poker to taxes and globalization. Investing Caffeine is also a location that profiles great investors and their associated investment lessons.

Today we are going to revisit investing giant Phil Fisher, but rather than rehashing his accomplishments and overall philosophy, we will dig deeper into his selling discipline. For most investors, selling securities is much more difficult than buying them. The average investor often lacks emotional self-control and is unable to be honest with himself. Since most investors hate being wrong, their egos prevent taking losses on positions, even if it is the proper, rational decision. Often the end result is an inability to sell deteriorating stocks until capitulating near price bottoms.

Selling may be more difficult for most, but Fisher actually has a simpler and crisper number of sell rules as compared to his buy rules (3 vs. 15). Here are Fisher’s three sell rules:

1) Wrong Facts: There are times after a security is purchased that the investor realizes the facts do not support the supposed rosy reasons of the original purchase. If the purchase thesis was initially built on a shaky foundation, then the shares should be sold.

2) Changing Facts: The facts of the original purchase may have been deemed correct, but facts can change negatively over the passage of time. Management deterioration and/or the exhaustion of growth opportunities are a few reasons why a security should be sold according to Fisher.

3) Scarcity of Cash: If there is a shortage of cash available, and if a unique opportunity presents itself, then Fisher advises the sale of other securities to fund the purchase.

Reasons Not to Sell

Prognostications or gut feelings about a potential market decline are not reasons to sell in Fisher’s eyes. Selling out of fear generally is a poor and costly idea. Fisher explains:

“When a bear market has come, I have not seen one time in ten when the investor actually got back into the same shares before they had gone up above his selling price.”

In Fisher’s mind, another reason not to sell stocks is solely based on valuation. Longer-term earnings power and comparable company ratios should be considered before spontaneous sales. What appears expensive today may look cheap tomorrow.

There are many reasons to buy and sell a stock, but like most good long –term investors, Fisher has managed to explain his three-point sale plan in simplistic terms the masses can understand. If you are committed to cutting investment losses, I advise you to follow investment legend Phil Fisher – cutting losses will actually help prevent your portfolio from splitting apart.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Alligators, Airplane Crashes, and the Investment Brain

“Neither a man nor a crowd nor a nation can be trusted to act humanely or think sanely under the influence of a great fear…To conquer fear is the beginning of wisdom.” – Bertrand Russell

Fear is a powerful force, and if not harnessed appropriately can prove ruinous and destructive to the performance of your investment portfolios. The preceding three years have shown the poisonous impacts fear can play on the average investor results, and Jason Zweig, financial columnist at The Wall Street Journal presciently wrote about this subject aptly titled “Fear,” just before the 2008 collapse.

Fear affects us all to differing degrees, and as Zweig points out, often this fear is misguided – even for professional investors. Zweig uses the advancements in neuroscience and behavioral finance to help explain how irrational decisions can often be made. To illustrate the folly in human’s thought process, Zweig offers up a multiple examples. Here is part of a questionnaire he highlights in his article:

“Which animal is responsible for the greatest number of human deaths in the U.S.?

A.) Alligator; B.) Bear; C.) Deer; D.) Shark; and E.) Snake

The ANSWER: C) Deer.

The seemingly most docile creature of the bunch turns out to cause the most deaths. Deer don’t attack with their teeth, but as it turns out, deer prance in front of speeding cars relatively frequently, thereby causing deadly collisions. In fact, deer collisions trigger seven times more deaths than alligators, bears, sharks, and snakes combined, according to Zweig.

Another factoid Zweig uses to explain cloudy human thought processes is the fear-filled topic of plane crashes versus car crashes. People feel very confident driving in a car, yet Zweig points out, you are 65 times more likely to get killed in your own car versus a plane, if you adjust for distance traveled. Hall of Fame NFL football coach John Madden hasn’t flown on an airplane since 1979 due to his fear of flying – investors make equally, if not more, irrational judgments in the investment world.

Professor Dr. Paul Slovic believes controllability and “knowability” contribute to the level of fear or perception of risk. Handguns are believed to be riskier than smoking, in large part because people do not have control over someone going on a gun rampage (i.e., Jared Loughner Tuscon, Arizona murders), while smokers have the power to just stop. The reality is smoking is much riskier than guns. On the “knowability” front, Zweig uses the tornadoes versus asthma comparison. Even though asthma kills more people, since it is silent and slow progressing, people generally believe tornadoes are riskier.

The Tangible Cause

Deep within the brain are two tiny, almond-shaped tissue formations called the amygdala. These parts of the brain, which have been in existence since the period of early-man, serve as an alarm system, which effectively functions as a fear reflex. For instance, the amygdala may elicit an instinctual body response if you encounter a bear, snake, or knife thrown at you.

Money fears set off the amygdala too. Zweig explains the linkage between fiscal and physical fears by stating, “Losing money can ignite the same fundamental fears you would feel if you encountered a charging tiger, got caught in a burning forest, or stood on the crumbling edge of a cliff.” Money plays such a large role in our society and can influence people’s psyches dramatically. Neuroscientist Antonio Damasio observed, “Money represents the means of maintaining life and sustaining us as organisms in our world.”

The Solutions

So as we deal with events such as the Lehman bankruptcy, flash crashes, Greek civil unrest, and Middle East political instability, how should investors cope with these intimidating fears? Zweig has a few recommended techniques to deal with this paramount problem:

1) Create a Distraction: When feeling stressed or overwhelmed by risk, Zweig urges investors to create a distraction or moment of brevity. He adds, “To break your anxiety, go for a walk, hit the gym, call a friend, play with your kids.”

2) Use Your Words: Objectively talking your way through a fearful investment situation can help prevent knee-jerk reactions and suboptimal outcomes. Zweig advises to the investor to answer a list of unbiased questions that forces the individual to focus on the facts – not the emotions.

3) Track Your Feelings: Many investors tend to become overenthusiastic near market tops and show despair near market bottoms. Long-term successful investors realize good investments usually make you sweat. Fidelity fund manager Brian Posner rightly stated, “If it makes me feel like I want to throw up, I can be pretty sure it’s a great investment.” Accomplished value fund manager Chris Davis echoed similar sentiments when he said, “We like the prices that pessimism produces.”

4) Get Away from the Herd: The best investment returns are not achieved by following the crowd. Get a broad range of opinions and continually test your investment thesis to make sure peer pressure is not driving key investment decisions.

Investors can become their worst enemies. Often these fears are created in our minds, whether self-inflicted or indirectly through the media or other source. Do yourself a favor and remove as much emotion from the investment decision-making process, so you do not become hostage to the fear du jour. Worrying too much about alligators and plane crashes will do more harm than good, when making critical decisions.

Read Other Jason Zweig Article from IC

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Historical Trampoline Cycles of Fear & Greed

What goes up, eventually comes down, and what goes down, eventually comes up. Like an adolescent jumping on a trampoline, emotions in the financial markets jump sky high before crashing down to earth…and then the process repeats itself. The underlying reasons behind every market gyration are different, but the emotions of fear and greed are similar. Since 1919, there have been 29 recessions, and 29 recoveries (pretty good recovery batting average). Over that 92 year period we have also witnessed the Dow Jones Industrial Average go from around 100 in 1919 to over 12,300 today – not too shabby.

The blood curdling panic experienced in 2008 and early 2009 has turned to ordinary fear among retail investors – although the doubling of the equity markets from two years ago has instilled a good dosage of animal spirits into professional traders and speculators. When trillions of low yielding cash and Treasuries ultimately come barreling into equity markets, thereby extending equity valuations, then I will become extra nervous. Until then, plenty of opportunities still exist – there just is not nearly as much low-hanging fruit as two years ago.

More of the Same

To make the point that “the more things change, the more things stay the same,” you can go all the way back to 1932 and read the words of Dean Witter – I also wrote about the history of panic in the 1970s (see Rhyming History).

Even some 80 years ago, Witter was keenly aware of the doomsday bears:

“People are deterred from buying good stocks and bonds now only because of an unwarranted terror…All sorts of bugaboos are paraded to destroy the last vestige of confidence. Stories of disaster which are incredible and untrue are told to foolish and credulous listeners, who appear willing to believe the worst.”

The bugaboo purveyors I called out in 2009 included Peter Schiff, Nouriel Roubini, Meredith Whitney, and Jimmy Rogers. I’m not sure who the next genius du jour(s) will be, but I am confident they will be prominently paraded over the media airwaves.

Cherry Price for Consensus

As firmer signs of an economic recovery finally take hold, investors slowly regain confidence about investing in risky assets. The only problem is that prices have skyrocketed! Witter captures this dynamic beautifully back in 1932:

“Some people say that they wish to await a clearer view of the future. When the future is again clear the present bargains will no longer be available. Does anyone think that present prices will continue when confidence has been fully restored? Such bargains exist only because of terror and distress.”

Herd Gets Slaughtered

History proves over and over again…the general investing public suffers the consequences of following the herd of fear and greed. Or as Witter states:

“It is easy to run with the crowd. The path of least resistance is to join in the wailings that are now so popular. The constructive policy, however, is to maintain your courage and your optimism, to have faith in the ultimate future of your country and to proclaim your faith and to recommend the purchase of good bonds and good stocks, which are inordinately depreciated.”

In the short-run, markets move up and down in an unpredictable fashion, like an irresponsible teenager jumping on a trampoline. In the long-run, investors can do themselves a favor by ignoring the masses, and sticking to a disciplined, systematic investment approach that includes controlled valuation metrics and contrarian sentiment factors. That way, you won’t fall off the investment trampoline and permanently break your portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Ellis on Battling Demons and Mr. Market

A lot of ground was covered in the first cut of my review on Charles Ellis’s book, Winning the Loser’s Game (“WTLG”). His book covers a broad spectrum of issues and reasons that help explain why so many amateurs and professional investors dramatically underperform broad market indexes and other forms of passive investing (such as index funds).

A major component of investor underperformance is tied to the internal or emotional aspects to investing. As I have written in the past, successful investing requires as much emotional art as it does mathematical science. Investing solely based on numbers is like a tennis player only able to compete with a backhand – you may hit a few good shots, but will end up losing in the long-run to the well-rounded players.

Ellis recognizes these core internal shortcomings and makes insightful observations throughout his book on how emotions can lead investors to lose. As George J.W. Goodman noted, “If you don’t know who you are, the stock market is an expensive place to find out.” Hopefully by examining more of Ellis’s investment nuggets, we can all become better investors, so let’s take a deeper dive.

Mischievous Mr. Market

Why is winning in the financial markets so difficult? Ellis devotes a considerable amount of time in WTLG talking about the crafty guy called “Mr. Market.” Here’s how Ellis describes the unique individual:

“Mr. Market is a mischievous but captivating fellow who persistently teases investors with gimmicks and tricks such as surprising earnings reports, startling dividend announcements, sudden surges of inflation, inspiring presidential announcements, grim reports of commodities prices, announcements of amazing new technologies, ugly bankruptcies, and even threats of war.”

Investors can easily get distracted by Mr. Market, and Ellis makes the point of why we are simple targets:

“Our internal demons and enemies are pride, fear, greed, exuberance, and anxiety. These are the buttons that Mr. Market most likes to push. If you have them, that rascal will find them. No wonder we are such easy prey for Mr. Market with all his attention-getting tricks.”

The market also has a way of lulling investors into complacency. Somehow, bull markets manage to make geniuses not only out of professionals and amateur investors, but also cab drivers and hair-dressers. Here is Ellis’s observation of how we tend to look at ourselves:

“We also think we are ‘above average’ as car drivers, as dancers, at telling jokes, at evaluating other people, as friends, as parents, and as investors. On average, we also believe our children are above average.”

This overconfidence and elevated self-assessment generally leads to excessive risk-taking and eventually hits arrogant investors over the head like a sledgehammer. Michael Mauboussin, Legg Mason Chief Investment Strategist and author of Think Twice, is a current thought leader in the field of behavioral finance that tackles many of these behavioral finance issues (read my earlier piece).

The Collateral Damage

As mentioned by Ellis in the previous WTLG article I wrote, “Eighty-five percent of investment managers have and will continue over the long term to underperform the overall market.” When emotions take over our actions, Mr. Market has a way of making investors make the worst decisions at the worst times. Ellis describes this phenomenon in more detail:

“The great risk to individual investors is not that the market can plummet, but that the investor may be frightened into liquidating his or her investments at or near the bottom and miss all the recovery, making the loss permanent. This happens to all too many investors in every terrible market drop.”

With the market about doubling from the early 2009 equity market lows, this devastating problem has become more evident. With volatility rearing its ugly head throughout 2008 and early 2009, investors bailed into low-yielding cash and Treasuries at the nastiest time. Now the stock market has catapulted upwards and those same investors now face significant interest rate risk and still are experiencing meager yields.

The Winning Formula

Ellis acknowledges the difficulty of winning at the investing game, but experience has shown him ways to combat the emotional demons. Number one…know thyself.

“’Know thyself’ is the cardinal rule in investing. The hardest work in investing is not intellectual; it’s emotional.”

Knowing thyself is easier said than done, but experience and mistakes are tremendous aids in becoming a better investor – especially if you are an investor who spends time studying the missteps and learns from them.

From a practical portfolio construction standpoint, how can investors combat their pesky emotions? Probably the best idea is to follow Ellis’s sage advice, which is to “sell down to the sleeping point. Don’t go outside your zone of competence because outside that zone you may get emotional, and being emotional is never good for your investing.”

Finding good investment ideas is just half the battle – fending off the demons and Mr. Market can be just as, if not more, challenging. Fortunately, Mr. Ellis has been kind enough to share his insights, allowing investors of all types to take this valuable investment advice to help win at a losing game.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Sentiment Cycle of Fear and Greed

Investing can be like a cross-country emotional roller-coaster ride to retirement. There are plenty of ups and downs, and plenty of unexpected twist and turns, but as long as investors stay the course, they will eventually reach their retirement objective. If not properly kept in check, however, emotions have the potential of sabotaging and/or delaying retirement objectives.

Barry Ritholtz at The Big Picture revisited the topic of sentiment cycles to hammer home the counterintuitive nature of successful investing (see also Doing the Opposite). As Ritholtz correctly points out in his chart, “euphoria” is actually the emotional “point of maximum financial risk,” and “despondency” is the “point of maximum financial opportunity.”

Source: The Big Picture with RED Sidoxia comments

In other words when the housing market was “euphoric” with demand in 2006, the financial risk was the highest, as millions of leveraged borrowers and homeowners painfully realized. Average investors suffered the reverse problem in early 2009 when “despondency” ruled the day and equity markets have marched upwards approximately +80% to +100%. Millions of investors bought real estate near the peak of the market and sold equities near the bottom of the market. Buying high and selling low is not a recipe for a retirement investment plan.

A more comedic representation of the sentiment cycle is provided below (CLICK TO ENLARGE). Laughable but spot on.

If investing was so simple, Jim Cramer would be among Forbes wealthiest top 10 and Lenny Dyskstra would have his private jet back (see story).

Where we are exactly on the sentiment cycle curve is debatable (my opinion is in RED on top chart), but if investors want to accelerate their path to financial success, they need to play the equity markets a lot more like a game of chess – anticipating future events not reacting to current ones. Too often, what appears as the obvious investment choice generates the worst long-term results. While on the investment rollercoaster, the choices that create the sweatiest palms are usually the best long-term decisions.

Read more about “Sentiment Cycles” from The Big Picture

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

“Pessimism Porn” Takes a Hit – Emotions of Investing

“Every dark cloud has a silver lining, but lightning kills hundreds of people each year who are trying to find it.”

–Tongue-in-cheek quote from motivational poster.

There’s nothing like a little destructive global financial crisis to boost viewership ratings. CNBC benefitted last fall from all the gloom and doom permeating the media outlets, but unfortunately for the cable business channel, a more constructive market environment over the last six months doesn’t sell as well as what New York Magazine called, “pessimism porn.” Tyler Durden at Zero Hedge recently provided statistics showing the impact of more optimistic financial markets. CNBC experienced total viewer year-over-year declines of -37% as measured in mid-September – worse than Mr. Durden’s late July statistics that illustrated a -28% decline.

Small wonder that we now see discussions developing between Comcast Corp. (CMCSA) and General Electric (GE) over a potential partnership with the NBC-Universal assets. Other potential parties may enter the fray, but GE’s shopping of the traditional media unit is evidence ofthe station’s pessimism over a secularly declining business.

Businesses are not the only ones influenced by pessimism – so are individuals. Behavioral economists Daniel Kahneman and Amos Tversky have provided support to the impact pessimism has on peoples’ psyches. Emotional fears of loss can have a crippling effect in the decision making process. Through their research, Kahneman and Tversky showed the pain of loss is more than twice as painful as the pleasure from gain. How do they prove this? Through various hypothetical gambling scenarios, they highlight how irrational decisions are made. For example, more people choose the scenario of an initial $600 nest egg that grows by $200, rather than starting with $1,000 and losing $200 (despite ending up at the same exact point under either scenario).

Of course investors have short memories from a historical perspective. Whether it’s the 17th century tulip mania (people paying tens of thousands for tulips – inflation adjusted), the technology bubble of the late 1990s, or the more recent real estate/credit craze, eventually a new bubble forms.

If you are one of those people that get sucked into “pessimism porn” or big bubbles, then I suggest you grab the remote control, turn off CNBC, and then switch over to The History Channel. You may just learn from the repeated emotional mistakes made by those of our past.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in CMCSA, GE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}