Posts tagged ‘emerging markets’

Nail Not in Emerging Market Coffin Yet

I wouldn’t say the nail is in the emerging market coffin quite yet. During the financial crisis, the EMSCI Emerging Market Index (EEM) was left for dead (down -50% in 2008) before resurrection in 2009 and 2010 (up +74% and +16%, respectively). For the last two years however, the EMSCI index has underperformed the S&P 500 Index massively by more than -30%. Included in this international index are holdings from China, Russia, India, Brazil, South Korea, and South Africa, among others.

The question now becomes, can the emerging markets resurrect themselves from the dead again? Recent signs are flashing “yes”. Over the last three months, the emerging markets have outperformed the S&P 500 by more than +8%, but these stocks still have a lot of ground to make up before reaching the peak levels of 2007. Last year’s slowing growth in China and a European recession, coupled with talks of the Federal Reserve’s “tapering” of monetary stimulus, didn’t provide the EMSCI index any help over the last few years.

With all the distracting drama currently taking place in Washington D.C., it’s a relief to see some other indications of improvement. For starters, China’s most recent PMI manufacturing index results showed continued improvement, reaching a level of 51.1 – up from August and signaling a reversal from contraction earlier this year (levels above 50 point to expansion). Chinese government leaders are continuing their migration from an externally export-driven economy to an internally consumer-driven economy. Despite the shift, China is still targeting a respectable +7.5% GDP economic growth target, albeit a slower level than achieved in the past.

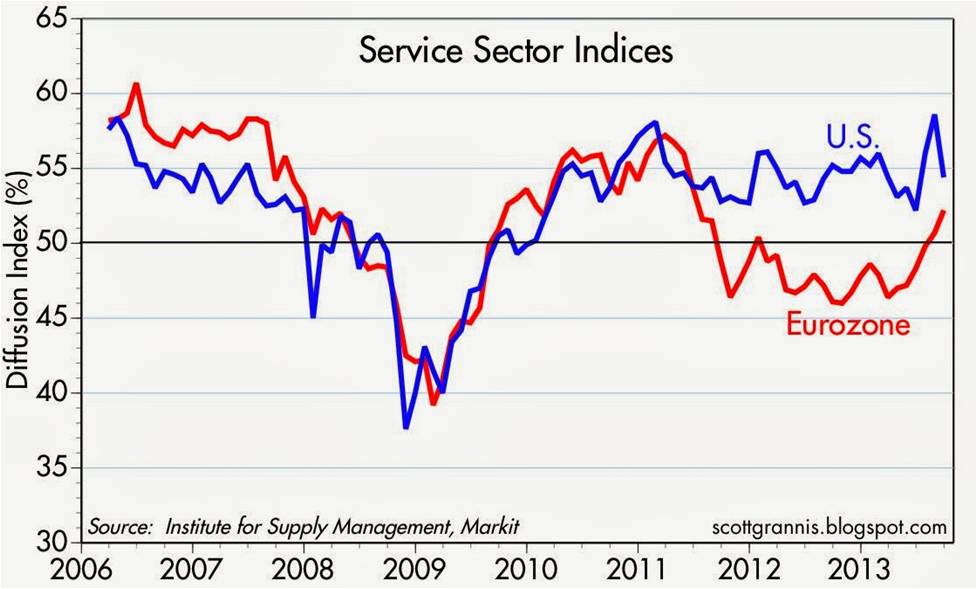

Adding to emerging market optimism is Europe’s apparent economic turnaround (or stabilization). As you can see from the chart below, the European Institute for Supply Management (ISM) service sector index has lately shown marked improvement. If the European and Chinese markets can sustain these recovering trends, these factors bode well for emerging market financial returns.

Source: Calafia Beach Pundit

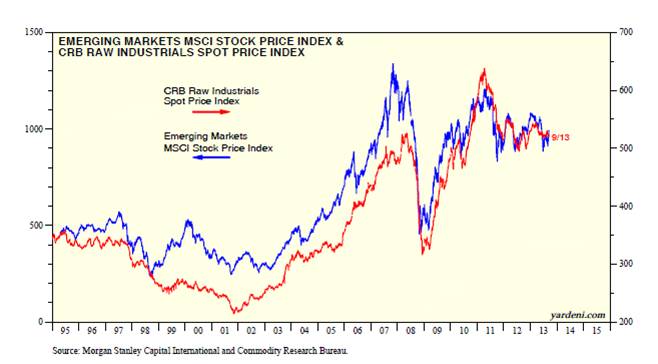

While it is clear these developments are helping the rebound in emerging market indices, it is also clear the supply-demand relationship in commodities will coincide with the next big up or down move in developing markets. Ed Yardeni, strategist and editor of Dr. Ed’s Blog, recently wrote a piece showing the tight correlation between emerging market stock prices and commodity prices (CRB Index). His conclusions come as no surprise to me given these resource-rich markets and their dependence on Chinese demand along with commodity needs from other developed countries. Expanding populations and rising standards of living in emerging market countries have and will likely continue to position these countries well for long-term commodity price appreciation. The development of new, higher-value service and manufacturing sectors should also lead to sustainably improved growth in these emerging markets relative to developed economies.

Source: Dr. Ed’s Blog

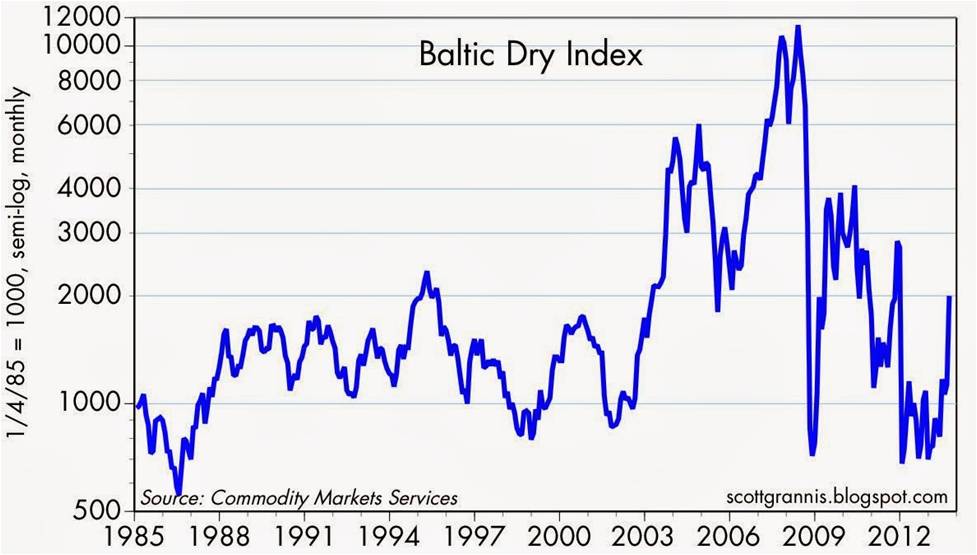

Adding fuel to the improving emerging market case is the advancement in the Baltic Dry Index (see chart below). The recent upward trajectory of the index is an indication that the price for moving major raw materials like coal, iron ore, and grains by sea is rising. This statistical movement is encouraging, but as you can see it is also very volatile.

Source: Calafia Beach Pundit

While the emerging markets are quite unpredictable and have been out-of-favor over the last few years, a truly diversified portfolio needs a healthy dosage of this international exposure. You better check a pulse before you put a nail in the coffin – the emerging markets are not dead yet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including emerging market ETFs, but at the time of publishing, SCM had no direct position in EEM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

M&A Bankers Away as Elephant Hunters Play

With trillions in cash sitting in CEO and private equity wallets, investment bankers have been chasing mergers & acquisitions with a vengeance. Unfortunately for the bankers, investor skittishness has slowed merger activity in the boardroom. Rather than aggressively stalk corporate prey, bidders look more like deer in headlights. However, animal spirits are not completely dead. Some board members have seen the light and realize the value-destroying characteristics of idle cash in a near-zero interest rate environment, so they have decided to go elephant hunting. During a nine day period alone in the first quarter of 2013, a total of $87.7 billion in elephant deals were announced:

- HJ Heinz Company (HNZ – $27.4 billion) – February 14, 2013 – Bidder: Berkshire Hathaway (BRKA)/ 3G Capital Partners.

- Virgin Media Inc. (VMED – $21.9 billion) – February 6, 2013 – Bidder: Liberty Global Inc. (LBTYA).

- Dell Inc. (DELL – $21.8 billion) – February 5, 2013 – Bidder: Silver Lake Partners LP, Michael Dell, Carl Icahn.

- NBCUniversal Media LLC 49% Stake (GE- $17.6 billion) – February 12, 2013 – Bidder: Comcast Corp. (CMCSA).

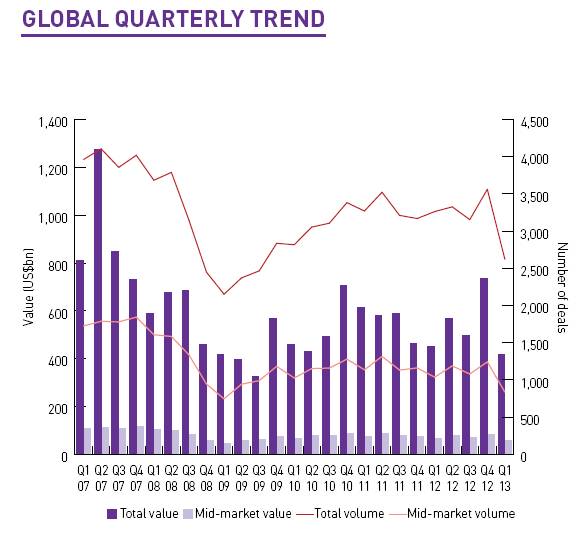

These elephant deals helped the overall M&A deal values in the United States increase by +34% in Q1 from a year ago to $167 billion (see Mergermarket report). Unfortunately, the picture doesn’t look so good on a global basis. The overall value for global M&A deals in Q1 registered $418 billion, down -7% from the first quarter of 2012. On a transaction basis, there were a total of 2,621 deals during the first three months of the year, down -20% from 3,262 deals in the comparable period last year.

Source: Mergermarket

With central banks across the globe pumping liquidity into the financial system and the U.S. stock market near record highs, one would think buyers would be writing big M&A checks as they wrote poems about rainbows, puppy dogs, and flowers. This is obviously not the case, so why such the sour mood?

The biggest scapegoat right now is Europe. While the U.S. economy appears to be slowly-but-surely plodding along on its economic recovery, Europe continues to dig a deeper recessionary hole. Austerity-driven fiscal policies are hindering growth, and concerns surrounding a Cypriot contagion continue to grab headlines. Although the U.S. dollar value of deals was up substantially in Q1, the number of transactions was down significantly to 703 deals from 925 in Q1-2012 (-24%). Besides buyer nervousness, unfriendly tax policy could have accelerated deals into 2012, and stole business from 2013.

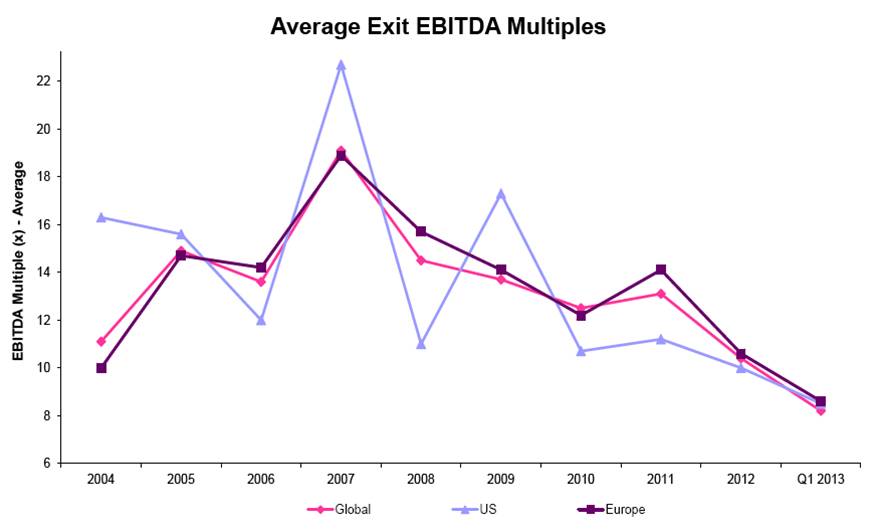

Besides lackluster global M&A volume, the record low EBITDA multiples on private equity exit prices is proof that skepticism on the sustainability of the economic recovery remains uninspired. With exit multiples at a meager level of 8.2x globally, many investors are holding onto their companies longer than they would like.

Source: Mergermarket

While merger activity has been a mixed bag, a bright spot in the M&A world has been the action in emerging markets. In 2012, the value of global transactions was essentially flat, yet emerging market deal values were up approximately +9% to $524 billion. This value exceeded the pre-crisis M&A activity level in 2007 by $73 billion, a feat not achieved in the other regions around the globe. Although emerging markets also pulled back in Q1, this region now account for 23% of total global M&A deal values.

Elephant buyout deals in the private equity space (skewed heavily by the Heinz & Dell deals) caused results to surge in this segment during the first quarter. Private equity related buyouts accounted for the highest share of global M&A activity (~21%) since 2007. However, like the overall U.S. M&A market, the number of Q1 transactions in the buyout space (372 transactions) declined to the lowest count in about four years.

Until skepticism turns into confidence, elephant deals will continue to distort results in the M&A sector (Echostar’s [DISH] play for Sprint [S] is further evidence). However, the existence of these giant transactions could be a leading indicator for more activity in the coming quarters. If bankers want to generate more fees, they may consider giving Warren Buffett a call. Here’s what he had to say after the announcement of the Heinz deal:

“I’m ready for another elephant. Please, if you see any walking by, just call me.”

Despite the weak overall M&A activity, the hunters are out there and they have plenty of ammunition (cash).

See also: Mergermarket Monthly M&A Insider Report (April 2013)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and CMCSA, but at the time of publishing SCM had no direct position in HNZ, BRKA, VMED, LBTYA, DELL, GE, DISH, S or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Organizing Your Investment Basket

With the Easter bunny relaxing after a busy holiday, kids from all over are given the task of organizing the candy and money collected during their hunts. Investors are also constantly reminded that their portfolio eggs should not be solely placed in one basket either. Instead, investors are told to diversify their investments across a whole host of asset classes, geographies, styles, and sizes. In other words, this means investors should be spreading their money across commodity, real estate, international, emerging market, value, growth, small-cap, and large-cap investments. As Jason Zweig, journalist from a the Wall Street Journal points out, much of the diversification benefits can be achieved with relatively small change in the position count of a portfolio:

“As many studies have shown, at least 40% of the variability in returns can be reduced by moving from a single company to 20. Once a portfolio contains 20 or 30 stocks, adding more does little to damp the fluctuations in wealth over time.”

But wait. Going from one banking stock to 20 banking stocks is not going to provide you with the proper diversification you want or need. Rather, what is as important as investing across asset class, geography, style, and size, is to follow the individual stock strategies of guru Peter Lynch. In order to put his performance into perspective, Lynch’s Fidelity Magellan fund averaged +29% per year from 1977 – 1990 – almost doubling the return of the S&P 500 index for that period.

More specifically, to achieve these heroic returns, Lynch divided the stocks in his fund into the following categories:

Slow Growers: This group of stocks wasn’t Lynch’s favorite because these companies typically operate in mature industries with limited expansion opportunities. For these single-digit EPS growers, Lynch focused more on identifying high dividend-paying stocks that were trading at attractive valuations. In particular, he paid attention to a dividend-adjusted PEG ratio (Price-to-Earnings Growth). A utility company would be an example of a “Slow Grower.”

Stalwarts: These are large established companies that still have the ability to achieve +10% to +12% annual earnings growth regardless of the economic cycle. Lynch liked these stocks especially during recessions and downturns. Valuations are still very important for Stalwarts, and many of them pay dividends. An investor may not realize a “home run” with respect to returns, but a +30% to 50% return over a few years is not out of the question, if selected correctly. Former examples of “Stalwarts” include Coca Cola (KO) and Procter & Gamble (PG).

Fast Growers: This categorization applies to small aggressive firms averaging about +20% to +25% annual earnings growth. While “Fast Growers” offer the most price appreciation potential, these stocks also offer the most risk, especially once growth/momentum slows. If timed correctly, as Lynch adeptly achieved, these stocks can increase multi-fold in value. The great thing about these “Fast Growers” is they don’t have to reside in fast growth industries. Lynch actually preferred market share gainers in legacy industries.

Cyclicals: These companies tend to see their sales and profits rise and fall with the overall economic cycle. The hyper-sensitivity to economic fluctuations makes the timing on these stocks extremely tricky, leading to losses and tears – especially if you get in too late or get out too late. To emphasize his point, Lynch states, “Cyclicals are like blackjack: stay in the game too long and it’s bound to take all your profit.” The other mistake inexperienced investors make is mistaking a “Cyclical” company as a “Stalwart” at the peak of a cycle. Examples of cyclical industries include airline, auto, steel, travel, and chemical industries.

Turnarounds: Lynch calls these stocks, “No Growers,” and they primarily of consist of situations like bail-outs, spin-offs, and restructurings. Unlike cyclical stocks, “Turnarounds” are usually least sensitive to the overall market. Even though these stocks are beaten down or depressed, they are enormously risky. Chyrysler, during the 1980s, was an example of a favorable Lynch turnaround.

Asset Plays: Overlooked or underappreciated assets such as real estate, oil reserves, patented drugs, and/or cash on the balance sheet are all examples of “Asset Plays” that Lynch would consider. Patience is paramount with these types of investments because it may take considerable time for the market to recognize such concealed assets.

Worth noting is that not all stocks remain in the same Lynch category. Apple Inc. (AAPL) is an example of a “Fast Grower” that has migrated to “Stalwart” or “Slow Grower” status, therefore items such as valuation and capital deployment (dividends and share buyback) become more important.

Peter Lynch’s heroic track record speaks for itself. Traditional diversification methods of spreading your eggs across various asset class baskets is useful, but this approach can be enhanced by identifying worthy candidates across Lynch’s six specific stock categories. Hunting for these winners is something Lynch and the Easter bunny could both agree upon.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and AAPL, but at the time of publishing SCM had no direct position in KO, PG, Chrysler, Fidelity Magellan, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Robotic Chain Saw Replaces Paul Bunyan

The world is rapidly changing and so is the profile of jobs. Technology is advancing at an accelerating pace, and this is having enormous impacts on the look, feel, and shape of global workforce dynamics. If lumberjack Paul Bunyan and his blue ox Babe were alive today, the giant would not be chopping down trees with a plain old steel axe, but more likely Mr. Bunyan would be using a 20 inch, 8 horse-power chain saw with side-mounted tensioner purchased from ChainSawsDirect.com.

But productivity in logging is not the only industry in which output has dramatically increased over the last generation. A recent New York Times article published by John Markoff explores how robots and automation are displacing humans across many different companies and industries around the world.

In China, manufacturers have exploited the value of cheap labor in the name of low-priced exports, but with millions of workers now moving to job-filled cities, workers are now demanding higher wages and better working conditions. Besides rising wages, higher transportation costs have eaten away labor expense advantages too. One way of getting around the issues of labor costs, labor relations, and transportations costs is to integrate robots into your workplace. A robot won’t ask for a raise; it always shows up on time; you don’t have to pay for its healthcare; it can work 24/7/365 days per year; it doesn’t belong to a union; dependable quality consistency is a given; it produces products near your customers; and it won’t sue you for discrimination or sexual harassment. The initial costs of a robot may be costlier than hiring a human being by a factor of five times an annual salary, but that hasn’t stopped companies everywhere from integrating robots into their operations.

The Orange Box on Wheels

One incredible example of robot usage (not covered by Markoff) is epitomized through Amazon.com Inc.’s (AMZN) $750 million acquisition of Kiva Systems Inc. last year. In some cases, Kiva uses hundreds of autonomous mobile robots in a warehouse to create a freeway-like effect of ecommerce fulfillment that can increase worker productivity four-fold. Amazon is a true believer of the technology as evidenced by the use of Kiva robots in two of its major websites, shoe-retailer Zappos.com and baby-products site Diapers.com, but Kiva’s robots have also been used by other major retailers including Crate & Barrel, Staples Inc (SPLS), and Gap Inc (GPS). The orange square robots on wheels, which can cost in the range of $2 – $20 million per system, travel around a warehouse tracking the desired items and bring them back to a warehouse worker, ready to then be packed and shipped to a customer. Larger warehouses can use up to 1,000 of the Kiva robots. To see how this organized chaos works, check out the video below to see the swarm of orange machines dancing around the warehouse floor.

The Next Chapter

The auto and electronics industry have historically been the heaviest users of robots and automation, but those dynamics are changing. Healthcare, food, aviation, and other general industries are jumping on the bandwagon. And these trends are not just happening in developed markets, but rather emerging markets are leading the charge – even if penetration rates are lower there than in the richer countries. The robotic usage growth is rapid in emerging markets, but the penetration of robotic density per 10,000 workers in China, Brazil and India is less than 10% of that in Japan and Germany (< 20% penetration of the U.S.), according to IFR World Robotics. As a matter of fact, IFR is forecasting that China will be the top robot market by 2014.

What does this mean for jobs? Not great news if you are a low-skilled worker. Take Foxconn, the company that manufactures and assembles those nifty Apple iPhones (AAPL) that are selling by the millions and generating billions in profits. The harsh working conditions in these so-called massive sweatshops have resulted in suicides and high profile worker backlashes. Related to these issues, Foxconn dealt with at least 17 suicides over a five year period. What is Foxconn’s response? Well, besides attempting to respond to worker grievances, Foxconn chairman Terry Gou announced plans to produce 1 million robots in three years , which will replace about 500,000 jobs….ouch!

As the New York Times points out, the “Rise of Machines” is not about to result in Terminator-like robots taking over the world anytime soon:

“Even though blue-collar jobs will be lost, more efficient manufacturing will create skilled jobs in designing, operating and servicing the assembly lines, as well as significant numbers of other kinds of jobs in the communities where factories are.”

Many companies see this trend accelerating and are investing aggressively to profit from the robotic automation and productivity benefits. In today’s day and age, Paul Bunyan would have surely taken advantage of these trends, just as I plan to through Sidoxia Capital Management’s opportunistic investments in the robotic sector.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), AMZN, and AAPL, but at the time of publishing SCM had no direct positions in Foxconn/Hon Hai, Crate & Barrel, SPLS, GPS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing with the Sentiment Pendulum

Article is an excerpt from Sidoxia Capital Management’s complementary May 2012 newsletter. Subscribe on right side of page.

The last five years have been historic in many respects. Not only have governments and central banks around the world undertaken unprecedented actions in response to the global financial crisis, but investors have ridden an emotional rollercoaster in response to historically unparalleled uncertainties.

While the nature of this past crisis has been unique, experienced investors know these fears continually manifest themselves in different forms over various cycles in time. Despite the more than doubling in equity market values over the last few years, as measured by the S&P 500 index, the emotional pendulum of investor sentiment has only partially corrected. Investor temperament has thankfully swung away from “Panic,” but has only moved closer to “Fear” and “Skepticism.” Here are some of the issues contributing to investors’ current sour mood:

The Next European Domino: The fear of the Greek domino toppling the larger Spanish and Italian economies has investors nervously chewing their finger-nails, and political turmoil in France and the Netherlands isn’t creating any additional warm and fuzzies.

Job Additions Losing Steam: New job creation here in the U.S. weakened to a lethargic monthly rate of +120,000 new jobs in March, while the unemployment rate remains stubbornly high at an 8.2% level.

Domestic Growth Losing Mojo: GDP (Gross Domestic Product) growth of +2.2% during the first quarter of 2012 also opened the door for the pessimists. Consumers are still spending (+2.9% growth), but government spending, business investment, and housing are taking wind out of the economy’s sails.

Emerging Markets Submerging: Unspectacular growth in the U.S. is not receiving any favors from slowing emerging markets like China and Brazil, which took fiscal and monetary actions to slow inflation and housing speculation in 2011.

Humpty Dumpty Politics: Presidential elections, tax policy, and deficit reduction are all concerns that carry the possibility of pushing the economic Humpty Dumpty off the wall, and as a result potentially lead to a great fall. The determination of Humpty Dumpty’s fate will likely have to wait until year-end or 2013.

Any student of history knows these fears and other concerns never go away – they simply change. But like supply and demand, gravitational forces eventually swing the emotional pendulum in the opposite direction. As Sir John Templeton so aptly stated, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” Or in other words, escalating bull markets must climb the proverbial “Wall of Worry” in order to sustain upward momentum. If there was nothing to worry about, then all the buyers would already be in the markets. We are nowhere close to experiencing “Euphoria” like we saw in stocks during the late-1990s or in the housing market around 2005.

Positively Climbing the “Wall of Worry”

With all this bad news out there, surprisingly there are some glimmers of hope chipping away at the “Wall of Worry.” Here are some of the positive factors helping turn pessimist frowns upside down:

Slow & Steady Wins the Race: The economic recovery has been weaker than hoped, but I can think of worse scenarios than 11 consecutive quarters of GDP growth and 25 straight months of private job creation, which has reduced the unemployment rate from 10.0% in October 2009 to 8.2% last month.

Earnings Machine Keeps Chugging Along: With the majority of S&P 500 companies having reported their quarterly results for the first quarter, three-fourths of the companies are beating forecasted earnings, which are currently registering in at a respectable +7.1% rate (Thomson Reuters). One company epitomizing this trend is Apple Inc. (AAPL). The near doubling in Apple’s profits during the quarter, thanks to explosive iPhone sales, pushed Apple’s shares over $600 and helped drive the NASDAQ index to its best day of the year.

Super Ben to the Rescue: The Federal Reserve has already stated their intention of keeping interest rates near 0% until 2014. The potential of additional monetary stimulus spearheaded by Federal Reserve Chairman Ben Bernanke, in the form of QE3 (Quantitative Easing Part III), may provide further needed support to the stock market (a.k.a., the “Bernanke Put”).

Return of the IPO: Initial Public Offerings (IPOs) have gained steam versus last year with more than 53 already coming to market in the first four months of 2012. This is no 1999, but a good number of deals have done quite well over the last month. For example, data analysis company Splunk Inc. (SPLK) share price is already up around 100% and the value of leisure luggage company TUMI Holdings (TUMI) has climbed over +40%. In a few weeks, the highly anticipated blockbuster Facebook (FB) IPO is expected to begin trading its shares, so we can see if the chronicled deal can live up to all the hype.

Dividends Galore: Dividend payments to stockholders are flowing at an extraordinary rate so far in 2012. Companies like IBM (increased its dividend by +13%), Exxon Mobil – (XOM +21%); Goldman Sachs – (GS +31%) are but just a few of the dividend raisers this year. Through the first three months of the year, the number of companies increasing their dividend payments was up +45% as compared to the comparable number for all of 2011.

Emerging Growth Not Dead: While worriers fret over slowing growth in China, companies like Apple grew by more than +100% in this region and collected nearly 20% of its revenues from this Asian country (~$8 billion). Coincidentally, China is expected to surpass an incredible one billion mobile connections in May – many of those iPhones. In other related news, Starbucks Corp. (SBUX) plans to triple its workforce and number of stores in China over the next three years. China has also helped fuel a backlog of Caterpillar Inc. (CAT) that is more than triple the level of 2009. Emerging markets may have slowed down in 2011, but with inflation beginning to stabilize, emerging market central banks and governments are now beginning to ease policies and reduce red-tape. For example, Brazil and India have started to lower key benchmark interest rates, and China has started to reverse capital flow restrictions.

Stay Off the Trampled Path

The mantra of “Sell in May and go away” always gets a lot of playtime around this period of the year. Over the last few years, the temporary spring/summer sell-offs have only been followed by stronger price appreciation. Individuals attempting to time the market (see also Getting Off the Treadmill) generally end up in tears. And for those traders who boast about their excellent timing (like those suspicious friends who brag about always winning in Las Vegas), we all know the truth – nobody buys at the lows and sells at the highs…except for liars.

With all the noise and cross-currents flooding the airwaves, investing for individuals without assistance has never been so difficult. But before hiding in your cave or reacting to the next scary headline about Europe, the economy, or politics, do yourself a favor by reminding yourself these chilling news items are nothing new and are often great contrarian indicators (see also Back to the Future). The emotional pendulum is constantly swinging from fear to greed and investors stand to prosper by adjusting sentiment and actions in the opposite direction. To survive in the investing wild, it is best to realize that the grass is greener and the eating more abundant when you stay off the trampled path of the herd.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in SPLK, TUMI, IBM, XOM, GS, SBUX, CAT, FB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Happy Birthday Bull Market!

Birthdays are always fun, but they are always more fun when more people come to the party. The birthday of the current bull market started on March 9, 2009, and as many bears point out, volume has been low, with a relatively small number of investors joining the party with hats and horns. This skepticism is not unusual in typical bull markets because the psychological scars from the previous bear market are still fresh in investors’ minds. How can investors get excited about investing when we are surrounded by record deficits, political gridlock, a crumbling European Union, slowing China, and peak corporate margins?

Bears Receive Party Invite but Stay Home

Perma-bears like Peter Schiff, Nouriel Roubini, John Mauldin, Mohamed El-Erian, and David Rosenberg have been consistently wrong over the last three years with their advice, but in some instances can sound smart shoveling it out to unassuming investors.

While nervous investors and bears have missed the 125%+ rally (see table below) over the last three years (mitigated by upward but underperforming gold prices), what many observers have not realized is that the so-called “Lost Decade” (see also Can the Lost Decade Strike Twice?) has actually been pretty spectacular for shrewd investors. Even if you purchased small and mid cap stocks at the peak of the market in March 2000, that large swath of stocks is up over +100%…yes, that’s right, more than doubled over the last 12 years. If you consider dividends, the numbers look significantly better.

Doubters of the equity market rally also ignore the three-year +135% advance in the NASDAQ (see also Ugly Stepchild) in part because the 11-year highs being registered still lag the peak levels reached in March 2000. Even though the NASDAQ increased 9-fold in the 1990s, if you bought the NASDAQ index in the first half of 1999, you would have still outperformed the S&P 500 index through the 2012 year-to-date period. Irrespective of how anyone looks at the performance of the NASDAQ index, it still has outperformed the S&P 500 index by more than +200% over the last 25 years, even if you include the bursting of the 2000 technology bubble.

CLICK TO ENLARGE

The point of all these statistics is to show that if you didn’t buy technology stocks at the climax of late 1999 or early 2000 prices, then the amount and type of available opportunities have been plentiful. The table above does not include emerging markets like Brazil, Mexico, and India (to name a few) that have also about doubled in price from the 2000 timeframe to 2012.

Heartburn can Accompany Sweet Treats

Being Pollyannaish after a doubling in market prices is never a wise decision. After three years of massive appreciation, those participating in the bull market run have eaten a lot of tasty cake. Now the question becomes, will investors also get some ice cream and a gift bag to go before the party ends? With the sweetness of the cake still being digested, there are still plenty of scenarios that can create investor heartburn. Obviously, the sovereign debt pig still needs to work its way through the European snake, and that could still take some time. In addition, although macroeconomic data (including employment data) generally have been improving, the trajectory of corporate profits has been decelerating – due in part to near record profit margins getting pressured by rising input costs. Domestically, structural debt and deficit issues have not gone away, and perpetual neglect will only exacerbate the current problems. On the psychology front, even though investors remain skittish, those still in the game are getting more complacent as evidenced by the VIX index now falling to the teens (a negative contrarian indicator).

Despite some of these cautionary signals, the good news is that many of these issues have been known for some time and have been reflected in valuations of the overall large cap indexes. Moreover, trillions of dollars remain idle in low yielding strategies as investors wait on the sidelines. Once prices move higher and there is more comfort surrounding the sustainability of an economic recovery, then capital will come pouring back into equity markets. In other words, investors will have to pay a premium cherry price if they wait for a comforting consensus to coalesce.

Limited Options

The other advantage working in investors’ favor is the lack of other attractive investment alternatives. Where are you going to invest these days when 10-year Treasuries and short-term CDs are yielding next to nothing? How about investing in risky, leveraged, illiquid real estate, just as banks unload massive numbers of foreclosures and process millions of short sales? If those investments don’t tickle your fancy, then how about pricey insurance and annuity products that nobody can understand? Cash was comforting in 2008-2009 and during volatility in recent summers, but with spiking food, energy, leisure, and medical costs, when does that cash comfort turn to cash pain?

Easy money and low interest rate policies being advocated by Federal Reserve Chairman Ben Bernanke and other global central bankers have sucked up available investment opportunities and compelled investors to look more closely at riskier assets like equities. With the large run in equities, I have been trimming back my winners and redeploying proceeds into higher dividend paying stocks and underperforming sectors of the market. Skepticism still abounds, and we may be ripe for a short-term pullback in the equity markets. For those rare birthday party attendees who are called long-term investors, opportunities still remain despite the large run in equities. The cake has been sweet so far, but if you are patient, some ice cream and a gift bag may be coming your way as well.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including emerging market, international, and bond/treasury ETFs), but at the time of publishing SCM had no direct position in VXX, MXY, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Curing Our Ills with Innovation

Fareed Zakaria thoughts have blanketed both traditional and internet media outlets, spanning everything from Newsweek to Time, and the New York Times to CNN. With an undergraduate diploma from Yale and his PhD from Harvard, Dr. Zakaria has built up quite a following, especially when it comes to foreign affairs.

In his latest Time magazine article, Can America Keep Pace?, Zakaria addresses the role of innovation in the U.S., “Innovation is as American as apple pie.” The innovation lead the U.S. maintains over the rest of the world will not evaporate over night because this cultural instinct is bred into our DNA – innovation is not something you one can learn directly from a textbook, Wikipedia, or Google (GOOG). With that said, the innovation gap is narrowing between developed and developing countries. New York Times columnist Tom Friedman captured this sentiment when he stated the following:

“French voters are trying to preserve a 35-hour work week in a world where Indian engineers are ready to work a 35-hour day.”

The fungibility of labor has pressured industries by transferring jobs abroad to much lower-cost regions like China and India, and that trend is only expanding further into countries with even lower labor cost advantages. Zakaria agrees:

“America’s future growth will have to come from new industries that create new products and processes. Older industries are under tremendous pressure.”

The good news is the United States maintains a significant lead in certain industries. For instance, we Yankees have a tremendous lead in fields such as biotechnology, entertainment, internet technologies, and consumer electronics.

The poster child for innovation is Apple Inc. (AAPL), which arose from the ashes of death ten years ago with its then ground-breaking new product, the iPod. Since then, Apple has introduced many innovative products and upgrades as a result of its research and development efforts, including the recently launched iPad.

The Education Engine

Where we are falling short is in education, which is the foundation to innovation. In a country with a high school system that Microsoft Corp.’s (MSFT) founder Bill Gates calls “obsolete,” society is left with one-third of the students not graduating and nearly half of the remaining graduates unprepared for college. In this instant gratification society we live in, the long-term critical education issue has been pushed to the backburner. Other emerging countries like China and India are churning out more college graduates by the millions, and also dominating us in the key strategic count of engineering degrees.

Government’s Role

With the massive debt and deficits our country currently faces, an ongoing debate about the size and role of government persists. Zakaria makes the case that government must place a significant role when it comes to innovation. Unfortunately, the U.S. wastes billions on pork-barrel projects and suboptimal subsidies while dilly-dallying in political gridlock over critical investments in education, infrastructure spending, basic research, and energy policies. In the meantime, our fellow competing countries are catching up to us, and in certain cases passing us (e.g., alternative energy investments – see Electric Profits).

Zakaria makes this point on the subject:

“The fastest-growing economies are all busy using government policy to establish commanding leads in one industry after another. Google’s Eric Schmidt points out that ‘the fact of the matter is, other countries are putting a lot more money into nurturing new industries than we are, and we are not going to win unless we do something like what they’re doing.’”

As a matter of fact, an ITIF (Information Technology & Innovation Foundation) study measuring innovation improvement from 1999 to 2009, as it related to government funding for basic research, education and corporate-tax policies, ranked the U.S. dead last out of 40 countries.

Not All is Lost – Pie Slice Maintained

Source: Carpe Diem

Although the outlook may sounds bleak, not all is lost. In a recent Wall Street Journal interview with Bob Doll Chief Equity Strategist at the world’s largest money management company (BlackRock has $3.6 trillion in assets under management), he makes the case that the U.S. remains the leading source of technological innovation and home to the greatest universities and the most creative businesses in the world. He sees this trend persisting in part because of our country’s relative demographic advantages:

“Over the next 20 years, the U.S. work force is going to grow by 11%, Europe’s going to fall by five, and Japan’s going to fall by 17. This alone tells me the U.S. has a huge advantage over Europe and a bigger one over Japan for growth.”

So while emerging markets, like those in Asia, continue to gain a larger slice of the global GDP pie, Mark Perry at Carpe Diem shows how the U.S has maintained its proportional slice of a growing global economic pie, over the last four decades.

Growth is driven by innovation, and innovation is driven by education. If America wants to maintain its greatness, the focus needs to be placed on innovation-led growth. The world is moving at warp speed, and our neighbors are moving swiftly, whether we come along for the ride or not. The current, sour conversations regarding deficits, debt ceilings, entitlements, wars, and unemployment are all essential discussions, but more importantly, if these debates can be refocused on accelerating innovation, the country will be well on its way to curing its ills.

See also Our Nation’s Keys to Success

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, GOOG, and AAPL, but at the time of publishing SCM had no direct position in MSFT, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Dow Déjà Vu – Shining Rainbow or Bad Nightmare?

Excerpt from Free January Sidoxia Monthly Newsletter (Subscribe on right-side of page)

The Dow Jones Industrial Average is sitting at 11,577 points. Dick Fuld is still CEO of Lehman Brothers, AIG is still trading toxic CDS derivative contracts, and the $700 billion TARP bailout is a pre-idea about to be invented in the brain of Treasury Secretary Hank Paulson. Oops, wait a second, this isn’t the Dow 11,577of September 2008, but rather this is the Dow 11,577 of December 2010 (+11% for the year, excluding dividends). Was the -50% drop we experienced in the equity markets during 2008-2009 all just a bad dream? If not, how in the heck has the stock market climbed spectacularly? Most people don’t realize that stocks have about doubled over the last 21 months (and up roughly +20%-25% in the last 6 months) – all in the face of horrendously depressing news swirling around the media (i.e., jobs, debt, deficits, N. Korea, Iran, “New Normal,” etc.). Market volatility often does not make intuitive sense, and as a result, many market observers have been caught flat-footed.

Here are a few basic factors that average investors have not adequately appreciated:

1) Headlines are in Rearview Mirror: News that everyone reads in newspapers and magazines and hears on the television and radio is all backward looking. It’s always best to drive while looking forward through the windshield and try to anticipate what’s around the corner – not obsess with backward looking activity in the rearview mirror. That’s how the stock market works – tomorrow’s news (not yesterday’s or today’s) is what drives prices up or down. As the economy teetered on the verge of a “Great Depression-like” scenario in 2008-2009, investors became overly pessimistic and stocks became dramatically oversold. More recently, news has been perking up. Previous recessions have seen doubters slowly convert to believers and push prices higher – eventually stocks become overbought and euphoria slows the bull market. I believe we are in phase II of this three-part economic recovery.

2) Ignore Emerging Markets at Own Peril: We Americans tend to wear blinders when it comes to focusing on domestic issues. We focus more on healthcare reform and political issues, such as “Don’t Ask, Don’t Tell,” rather than the billions of foreigners chasing us as they climb the global economic ladder. Citizens in emerging markets are more concerned about out-competing and out-innovating us through educated workforces, so they can steal our jobs and buy more toasters, iPods, and cars – things we Americans have already taken for granted. The insatiable appetite of the expanding global middle class for a better standard of living is also driving ballooning commodity prices – everything from coal to copper and corn to cotton (the 4 Cs). This universal sandbox that we play in offers tremendous opportunities to grasp and tremendous threats to avoid, if investors open their eyes to these emerging market trends.

3) Capital Goes Where it’s Treated Best: Many voters are fed-up with the political climate in Washington and the sad state of economic affairs. The great thing about the global capitalistic marketplace we live in is that it does not discriminate – capital flows to where it is treated best. On a macro basis, money flows to countries that are fiscally responsible, support pro-growth initiatives, harbor educated work forces, control valuable natural resources, and honor the rule of law. On a micro basis, money flows to companies that are attractively priced and/or capable of sustainably growing earnings and cash flow. Voters and politicians will ultimately figure it out, or capital will go where it’s treated best.

Today’s Dow 11,577 is no bad dream, but rather resembles the emergence of a bright shining rainbow after a long, cold, and dark storm. The rainbow won’t stick around forever, but if investors choose to ignore the previously mentioned factors, like so many investors have overlooked, portfolio performance may turn into an ugly nightmare.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, and an AIG derivative security, but at the time of publishing SCM had no direct position in GS, any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Opal Conference: Hedge Fund Heaven and Regulatory Rules

The recent Alternative Investment Summit held December 5-7 at the Ritz-Carlton in Laguna Niguel, California provided a little bit of everything for attendees – including a slice of hedge fund heaven and a less appetizing dollop of regulatory rules. If you are going to work hard, why not do it in an unrivaled, picturesque setting along the sandy shores of Dana Point? The well-attended conference, which was hosted by Opal Financial Group, was designed to address the interests of a broad set of constituents in the alternative investment food-chain, including representatives of hedge funds, fund of funds, endowments, consulting firms, private equity firms, venture capital firms, commodity trading advisors (CTAs), law firms, family offices, pension funds, along with various other vendors and service providers.

Although the topics and panel experts covered diverse areas, I found some interesting common themes emanating from the conference:

1) Waterboard Your Manager: In the wake of the Bernie Madoff Ponzi scheme and the recent sweeping insider trading investigations, institutional investors are having recurring nightmares. Consultants and other service-based intermediaries are feeling the heat in a fever-pitched litigation environment that is driving defensive behavior to avoid “headline risk” at any cost. As a result, institutional investors and fund of funds are demanding increased transparency and immediate liquidity in addition to conducting deeper, more thorough due diligence. One consultant jokingly said they will “waterboard” managers to obtain information, if necessary. In the hedge fund world, this risk averse stance is leading to a concentrated migration of funds to large established funds – even if those actions may potentially compromise return opportunities. In response to a question about insider trading investigations as they relate to client fund withdrawals, one nervous panel member advised clients to “shoot first, and ask questions later.”

2) Lurking Mountain of Maturity: Default rates in the overall bond markets have been fairly tame in the 2.0 – 2.5% range, however a mountain of previously issued debt is expected to mature over the next few years, meaning many of those corporate issuers will need to refinance the existing debt and issues longer term debt. For the most part, capital markets have been accommodating a large percentage of issuers, due to investors’ yield-hungry appetite. If the capital markets seize up and the banks continue lending like the Grinch, then the default rate could certainly creep up.

3) CLO Market Gaining Steam: The collateralized loan obligation market is still significantly below pre-crisis levels, however an estimated $3.5 billion 2010 new issue market is expected to gain even more momentum into 2011. New issuance levels are expected to register in at a more healthy $5.0 billion level next year.

4) Less Fruit in Debt Markets: The general sense among fund managers was that previously attractive bond prices have risen and bond yield spreads have narrowed. The low hanging fruit has been picked and earning similarly attractive returns will become even more challenging in the coming year, despite benign default rates. Even though bonds face a tough challenge of potential future interest rate increases, many managers believe selective opportunities can still be found in more illiquid, distressed debt markets.

5) Fund of Funds vs. Consultants: Playing in the sandbox is getting more crowded as some consultants are developing in-house investment solutions while fund of funds are advancing their own internal capabilities to target institutional investors directly. By doing so, the fund of funds are able to cut out the middle-man/woman consultant and keep more of the profit pie to themselves. From a plan sponsor perspective, institutional investors struggle with the trade-offs of investing in a diversified fund of funds vehicle versus aggregating the unique alpha generating capabilities of individual hedge fund managers.

6) Emerging Frontier Markets: There was plenty of debate about the dour state of global macroeconomic trends, but a healthy dose of optimism was injected into the discussion about emerging markets and the frontier markets. One panel member referred to the frontier markets as the Rodney Dangerfield (see Doug Kass) of the world (i.e., “get no respect”). The frontier markets are like the immature little brothers of the major emerging markets in China, India, Brazil, and Russia. Examples of frontier markets provided include Vietnam, Nigeria, Bangladesh, and Kenya. In general, these markets are heavily dependent on natural resources and will move in unison with supply-demand adjustments in larger markets like China. Of the approximately 80 frontier markets around the globe, 30 were described as uninvestable, with the remaining majority offering interesting prospects.

All in all the Opal Financial Group Alternative Investment Summit was a huge success. Besides becoming immersed in the many facets of alternative investments, I met leading thought leaders in the field, including an unexpected interaction with a world champion and living legend (read here for a hint). Many conferences are not worth the price of admission, but with global economic forces changing at breakneck speed and regulatory rules continually unfolding in response to the financial crisis, for those involved in the alternative investment field, this is one event you should not miss.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) is the General Partner of the Slome Sidoxia Fund, LP, a long-short hedge fund. SCM and some of its clients also own certain exchange traded funds (including emerging market ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Blowing the Perfect Investment Game

Photo source: Boston.com

Armando Galarraga, pitcher from the Detroit Tigers baseball team, became a victim of a blown call by umpire Jim Joyce, resulting in a lifetime opportunity being ripped from his clutches. Not only did the error in judgment cost Galarraga a perfect game – a feat only achieved by 20 pitchers over the last 130 years – but the blunder also cost him a no-hitter. Perfect games are difficult to come by in the investment world too, but for those ambitious investors reaching for the finance Hall of Fame, I strongly believe a healthy dosage of international and emerging markets is required to achieve perfection (or significant outperformance).

The Fab Five

The oft quoted view that the U.S. was the dominant economic powerhouse in the 20th century (after Britain controlled the 19th century) led me to analyze five emerging growth markets outside of the U.S. There are some clear leaders in pursuit of 21st century economic supremacy, however nothing in the global pecking order is guaranteed. What I do know is that me and my clients will be relying on the financial tailwinds of growth coming from these international markets to provide excess return potential to my portfolios (albeit at the cost of shorter-term volatility). Even retired individuals, or those with shorter time horizons, should consider small bite sizes of these emerging markets in their portfolios, if merely for some of the diversification benefits (see diversification article).

Pundits and media types endlessly write and talk about the “lost decade,” the demise of “buy and hold,” and/or the “death of equities.” Well, as you can see, the lost decade through the first half of 2010 turned out to be a significantly lucrative period for investors with the stomach and courage to invest outside the familiar comfort zone of the United States (see chart below).

Specifically, here is the international outperformance achieved in the sample of international markets as compared to the United States (S&P 500 Index):

- Brazil +266.22% (EWZ tracking Bovespa Index)

- India +266.16% (Bombay Stock Exchange – BSE)

- Australia +68.16% (ASX 200 Index)

- China +68.06% (Shanghai Index)

- Hong Kong +39.74% (Hang Seng Index)

- United States -128.19% Average Underperformance versus five other geographic indexes.

An added kicker for investment consideration is valuation. According to The Financial Times market data section, all these international markets, with the exception of India, trade at a discount to the S&P 500 on a Price/Earnings ratio basis (P/E).

Victim of Our Own Success

Graph source: The New York Times

In many respects, our country has continued to thrive in spite of some of our political and economic shortcomings. As you can see from the chart below (NY Times article) our country’s market share of the world’s Gross Domestic Product (GDP) has been steadily been declining since World War II (and we’ve still done OK). With U.S. GDP exceeding $14 trillion, our sheer size makes it much more difficult to grow relative to our smaller, more nimble international brethren. Given our top economic position in the world, Warren Buffett succinctly identified the force working against size when he said, “Gravity always wins.” I would expect gravitational influences to continue to weigh us down in the future, but our declining share should not be considered a detrimental trend. Globalization needs to be embraced by policymakers so we can take advantage of these faster growing countries as opportunistic export markets. We Americans can improve our standard of living while riding the coattails of our speedy neighbors. Do yourself a favor and include a healthy chunk of higher growth markets into your portfolio – it’s important you do not blow your own investment game.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including BKF, FXI, EWZ), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}