Posts tagged ‘elections’

Fed Ripping Off the Inflation Band-Aid

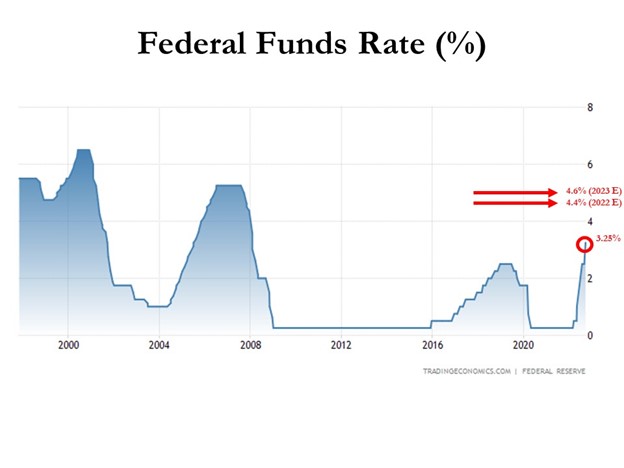

Inflation rates have been running near 40-year highs, and as a result, the Federal Reserve is doing everything in its power to rip off the Band-Aid of insidious high price levels in a swift manner. The Fed’s goal is to inflict quick, near-term pain on the economy in exchange for long-term price stability and future economic gains. How quickly has the Fed been hiking interest rates? The short answer is the rate of increases has been the fastest in decades (see chart below). Essentially, the Federal Reserve has pushed the targeted benchmark Federal Funds target rate from 0% at the beginning of this year to 3.25% today. Going forward, the goal is to lift rates to 4.4% by year-end, and then to 4.6% by next year (see Fed’s “dot plot” chart).

How should one interpret all of this? Well, if the Fed is right about their interest rate forecasts, the Band-Aid is being ripped off very quickly, and 95% of the pain should be felt by December. In other words, there should be a light at the end of the tunnel, soon.

The Good News on Inflation

When it comes to inflation, the good news is that it appears to be peaking (see chart below), and many economists see the declining inflation trend continuing in the coming months. Why do pundits see inflation peaking? For starters, a broad list of commodity prices have declined significantly in recent months, including gasoline, crude oil, steel, copper, and gold, among many others.

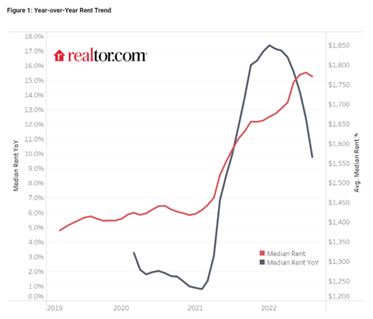

Outside of commodities, investors have seen prices drop in other areas of the economy as well, including housing prices, which recently experienced the fastest monthly price drop in 11 years, and rent prices as well (see chart below).

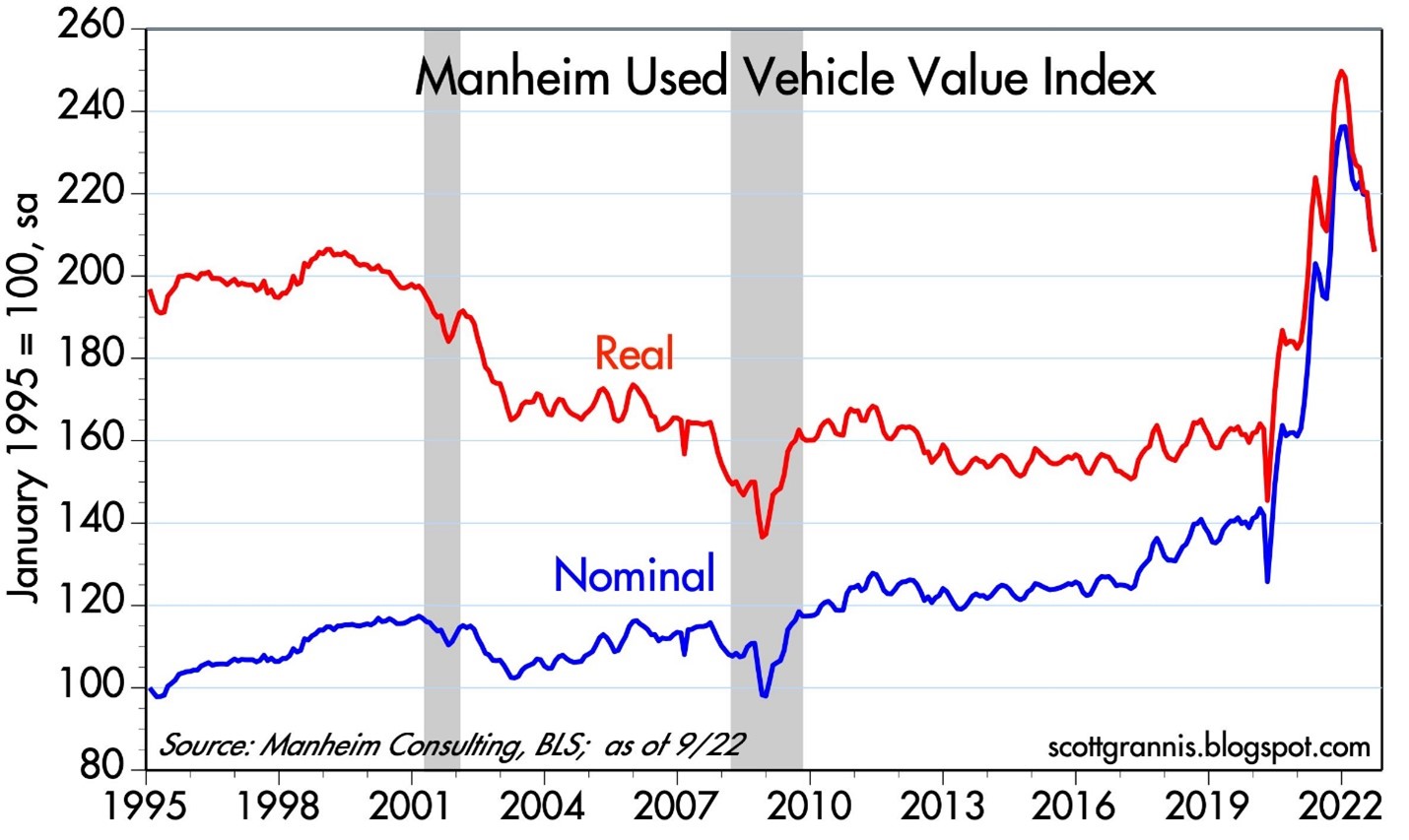

Anybody who was shopping for a car during the pandemic knows what happened to pricing – it exploded higher. But even in this area, we are seeing prices coming down (see chart below), and CarMax Inc. (KMX), the national used car retail chain confirmed the softening price trend last week.

Pain Spread Broadly

When interest rates increase at the fastest pace in 40 years, pain is felt across almost all asset classes. It’s not just U.S. stocks, which declined -9.3% last month (S&P 500), but it’s also housing -8.5% (XHB), real estate investment trusts -13.8% (VNQ), bonds -4.4% (BND), Bitcoin -3.1%, European stocks -10.1% (VGK), Chinese stocks -14.4% (FXI), and Agriculture -3.0% (DBA). The +17% increase in the value of the U.S. dollar this year against a basket of foreign currencies is substantially pressuring cross-border business for larger multi-national companies too – Microsoft Corp. (MSFT), for example, blamed U.S. dollar strength as the primary reason to cut earnings several months ago. Like Hurricane Ian, large interest rate increases have caused significant damage across a wide swath of areas.

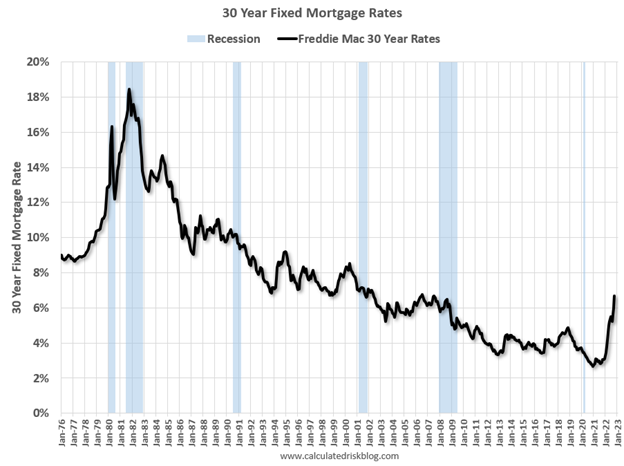

But for those following the communication of Federal Reserve Chairman, Jerome Powell, in recent months, they should not be surprised. Chairman Powell has signaled on numerous occasions, including last month at a key economic conference in Jackson Hole, Wyoming, that the Fed’s war path to curb inflation by increasing interest rates will inflict wide-ranging “pain” on Americans. Some of that pain can be seen in mortgage rates, which have more than doubled in 2022 and last week eclipsed 7.0% (see chart below), the highest level in 20 years.

Now is Not the Time to Panic

There is a lot of uncertainty out in the world currently (i.e., inflation, the Fed, Russia-Ukraine, strong dollar, elections, recession fears, etc.), but that is always the case. There is never a period when there is nothing to be concerned about. With the S&P 500 down more than -25% from its peak (and the NASDAQ down approximately -35%), now is not the right time to panic. Knee-jerk emotional decisions during stressful times are very rarely the right response. With these kind of drops, a mild-to-moderate recession is already baked into the cake, even though the economy is expected to grow for the next four quarters and for all of 2023 (see GDP forecasts below). Stated differently, it’s quite possible that even if the economy deteriorates into a recession, stock prices could rebound smartly higher because any potential future bad news has already been anticipated in the current price drops.

Worth noting, as I have pointed out previously, numerous data points are indicating inflation is peaking, if not already coming down. Inflation expectations have already dropped to about 2%, if you consider the spread between the yield on the 5-Year Note (4%) and the yield on the 5-Year TIP-Treasury Inflation Protected Note (2%). If the economy continues to slow down, and inflation has stabilized or declined, the Federal Reserve will likely pivot to decreasing interest rates, which should act like a tailwind for financial markets, unlike the headwind of rising rates this year.

Ripping off the Band-Aid can be painful in the short-run, but the long-term gains achieved during the healing process can be much more pleasurable.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in MSFT, BND and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in KMX, XHB, VNQ, VGK, FXI, DBA or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Head Fakes Surprise as Stocks Hit Highs

In a world of seven billion people and over 200 countries, guess what…there are a plethora of crises, masses of bad people, and plenty of lurking issues to lose sleep over.

The fear du jour may change, but as the late-great investor Sir John Templeton correctly stated:

“Bull markets are born on pessimism and they grow on skepticism, mature on optimism, and die on euphoria.”

And for the last decade since the 2008-2009 Financial Crisis, it’s clear to me that the stock market has climbed a lot of worry, pessimism, and skepticism. Over the last decade, here is a small sampling of wories:

With over five billion cell phones spanning the globe, fear-inspiring news headlines travel from one end of the world to the other in a blink of an eye. Fortunately for investors, the endless laundry list of crises and concerns has not broken this significant, multi-year bull market. In fact, stock prices have more than tripled since early 2009. As famed hedge fund manager Leon Cooperman noted:

“Bull markets don’t die from old age, they die from excesses.”

On the contrary to excesses, corporations have been slow to hire and invest due to heightened risk aversion induced by the financial crisis. Consumers have saved more and lowered personal debt levels. The Federal Reserve took unprecedented measures to stimulate the economy, but these efforts have since been reversed. The Fed has even signaled its plan to reduce its balance sheet later this year. As the expansion has aged, corporations and consumer risk aversion has abated, but evidence of excesses remains paltry.

Investors may no longer be panicked, but they remain skeptical. With each subsequent new stock market high, screams of a market top and impending recession blanket headlines. As I pointed out in my March Madness article, stocks have made new highs every year for the last five years, but continually I get asked, “Wade, don’t you think the market is overheated and it’s time to sell?”

For years, I have documented the lack of stock buying evidenced by the continued weak fund flow sales. If I could summarize investor behavior in one picture, it would look something like this:

Corrections have happened, and will continue to occur, but a more significant decline will likely happen under specific circumstances. As I point out in Half Empty, Half Full?, the time to become more cautious will be when we see a combination of the following trends occur:

- Sharp increase in interest rates

- Signs of a significant decline in corporate profits

- Indications of an economic recession (e.g., an inverted yield curve)

- Spike in stock prices to a point where valuation (prices) are at extreme levels and skeptical investor sentiment becomes euphoric

Attempting to predict a market crash is a Fool’s Errand, but more important for investors is periodically reviewing your liquidity needs, time horizon, risk tolerance, and unique circumstances, so you can optimize your asset allocation. There will be plenty more head fake surprises, but if conditions remain the same, investors should not be surprised by new stock highs.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Huh… Stocks Reach a Record High?

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (September 1, 2016). Subscribe on the right side of the page for the complete text.

The stock market hit all-time record highs again in August, but despite the +6.2% move in 2016 S&P 500 stock prices (and +225% since early 2009), investors continue to scratch their heads in confusion. Individuals continue to ask, “Huh, how can stocks be trading at or near record levels (+6% for the year) when Brexit remains a looming overhang, uncertainty surrounds the U.S. presidential election, global terrorist attacks are on the rise, negative interest rates are ruling the day, and central banks around the globe are artificially propping up financial markets (see also Fed Myths vs. Reality)? Does this laundry list of concerns stress you out? If you said “yes”, you are not alone.

As I’ve pointed out in the past, we live in a different world today. In the olden days, terrorist attacks, natural disasters, currency crises, car chases, bank failures, celebrity DUIs, and wars happened all the time. However, before the internet existed, people either never heard about these worries, or they just didn’t care (or both). Today, we live in a Twitter, Facebook, Instagram, Snapchat, society with 500+ cable channels, and supercomputers in the palm of our hands (i.e., smartphones) with more computing power than existed on the Apollo mission to the moon. In short, doom-and-gloom captures human attention and sells advertising, the status quo does not.

- Record corporate profits are on the rise

- Stabilizing value of the dollar

- Stabilizing energy and commodity prices

- Record low interest rates

- Skeptical investing public

Fortunately, the stock market pays more attention to these important dynamics, rather than the F.U.D. (Fear, Uncertainty, Doubt) peddled by the pundits, bloggers, and TV talking heads. Certainly, any or all of the previously mentioned positive factors could change or deteriorate over time, but for the time being, the bulls are winning.

Let’s take a closer look at the influencing components that are driving stock prices higher:

Record Corporate Profits

Source: Yardeni.com

Profits are the mother’s milk that feeds the stock market. During recessions, profits are starved and stock prices decline. On the flip side, economic expansions feed profits and cause share prices to rise. As you can see from the chart above, there was a meteoric rise in corporate income from 2009 – 2014 before a leveling off occurred from 2015 going into 2016. The major headwinds causing profits to flatten was a spike of 25% in the value of the U.S. dollar relative to the value of other global currencies, all within a relatively short time span of about nine months (see chart below).

Why is this large currency shift important? The answer is that approximately 40% of multinational profits derived by S&P 500 companies come from international markets. Therefore, when the value of the dollar rose 25%, the cost to purchase U.S. products and services by foreign buyers became 25% costlier. Selling dramatically higher cost goods abroad squeezed exports, which in turn led to a flattening of profits. Time will tell, but as I showed in the first chart, the slope of the profit line has resumed its upwards trajectory, which helps explain why stock prices have been advancing in recent months.

Besides a strong dollar, another negative factor that temporarily weakened earnings was the dramatic decline in oil prices (see chart below) Two years ago, WTI oil prices were above $100 per barrel. Today, prices are hovering around $45 per barrel. As you can imagine, this tremendous price decline has had a destructive impact on the profits of the energy sector in general. The good news is that after watching prices plummet below $30 earlier this year, prices have since stabilized at higher levels. In other words, the profits headwind has been neutralized, and if global economic growth recovers further, the energy headwind could turn into an energy tailwind.

Record Low Interest Rates

Stocks were not popular during the early 1980s. In fact, the Dow Jones Industrial Average traded at 2,600 in 1980 vs 18,400 today. The economy was much smaller back then, but another significant overhang to lower stock prices was higher interest rates (and inflation). Back in 1980, the Federal Funds target rate set by the Federal Reserve reached a whopping 20.0% versus today the same rate sits at < 0.5%.

Why is this data important? When you can earn a 16.99% yield in a one-year bank CD (see advertisement below), generally there is a much smaller appetite to invest in riskier, more volatile stocks. Another way to think about rates is to equate interest rates to the cost of owning stocks. When interest rates were high, the relative cost to own stocks was also high, so many investors liquidated stocks. It makes perfect sense that stocks in that high interest rate environment of 1980 would be a lot less attractive compared to a relatively safe CD that paid 17% over a 12-month period.

On the other hand, when interest rates are low, the relative cost of owning stocks is low, so it makes sense that stock prices are rising in this environment. Just like profits, interest rates are not static, and they too can change rapidly. But as long as rates remain near record lows, and profits remain healthy, stocks should remain an appealing asset class, especially given the scarcity of strong alternatives.

Skeptical Investing Public

The last piece of the puzzle to examine in order to help explain the head-scratching record stock prices is the pervasive skepticism present in the current stock market. How can Brexit, presidential election, terrorism, negative interest rates, and uncertain Federal Reserve policies be good for stock prices? Investing in many respects can be like navigating through traffic. When everyone wants to drive on the freeway, it becomes congested and a bad option, therefore taking side-streets or detours is a better strategy. The same principle applies to the stock market. When everyone wants to invest in the stock market (like during the late 1990s) or buy housing (mid-2000s), prices are usually too inflated, and shrewd investors decide to choose a different route by selling.

The same holds true in reverse. When nobody is interested in investing (see also, 18-year low in stock ownership and two trillion of stocks sold), then generally that is a strong sign that it is a good time to buy. Currently, skepticism is plentiful, for all the reasons cited above, which is a healthy investment indicator. Many individuals continue reading the ominous headlines and scratching their heads in confusion over today’s record stock prices. In contrast, at Sidoxia, we have opportunistically benefited from investors’ skepticism by discovering plenty of attractive opportunities for our clients. There’s no confusion about that.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and FB, but at the time of publishing had no direct position in TWTR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Autumn, Elections and Replacement Refs

Article is an excerpt from previously released Sidoxia Capital Management’s complementary October 1, 2012 newsletter. Subscribe on right side of page.

As September has come to a close, the grand finale of our annual seasons has commenced… autumn. How do we know autumn is here? Well, for starters, the leaves are changing colors; the weather is about to cool; and the NFL replacement referees are watching Sunday football games from their couches.

While 2012 is split into quarters, football games and investment seasons are also divided into four quarters. Right now, the economic fourth quarter has just started and the home team is winning. As we can see from the stock market scoreboard, the S&P 500 index is up +15% this year (+6% in Q3) and the NASDAQ index has catapulted +20% through September (+6% also in Q3). The U.S. home team is winning, but a fumble, blocked kick, or interception could mean the difference between an exciting win and a devastating loss.

Another game divided into four parts is the game of presidential politics. However, presidential elections are divided into four years – not four quarters. Five weeks from now, we’ll find out if our Commander in Chief Obama will get to lead our team for another game lasting four years, or whether backup quarterback Mit Romney will be called into the game. The fans are getting restless due to anemic growth and lingering joblessness, but for now, the coach is keeping the president in the starting lineup. Both President Obama and Governor Romney will take some head-to-head practice snaps against each other in the first of three scheduled presidential debates beginning this week.

Bernanke Changes Rules

The New York Jets have Tim Tebow for their secret weapon (1 for 1 yesterday!), and the United States economy has Ben Bernanke. Although our home team may be winning, it has required some monetary rule-changing policies to be instituted by Federal Reserve Chairman Ben Bernanke to keep our team in the lead. Just a few weeks ago, Mr. Bernake instituted QE3 (3rd round of quantitative easing), which is an open-ended mortgage buying program designed to lower home buying interest rates and stimulate the economy (see Helicopter Ben to QE3 Rescue). The short-term benefits of the $40 billion monthly bond buying binge are relatively clear (lower borrowing costs for homebuyers), but the longer-term costs of inflation are stewing patiently on the backburner.

Source: Calafia Beach Pundit (Scott Grannis)

As you can see from the chart above, August median home prices are up +10% for existing single-family homes over the last year. Housing affordability is at extremely attractive levels, and although the bank loan purse strings are tight, a modest loosening is beginning to unfold.

Economy Playing Injured

Our starters may still be playing, but many are injured, just like the jobless are limping through the employment market. Encouragingly, although unemployment remains stubbornly high, the number of people collecting unemployment checks is a lot lower (-1.25 million fewer than a year ago). Not great news, but at least we are hobbling in the right direction (see chart below).

Source: Calafia Beach Pundit (Scott Grannis)

Time for Fiscal Cliff Hail Mary?

If a team is losing at the end of a game, a “Hail Mary” pass might be necessary. We are quickly nearing this fiscal Armageddon situation as the approximately $700 billion “fiscal cliff” (a painful combo of spending cuts and tax hikes) kicks in at the end of the year (see PIMCO chart below via The Reformed Broker).

Running trillion dollar deficits in perpetuity is not a sustainable strategy, so for most people, a combination of spending cuts and/or tax hikes makes sense to narrow the gap (see chart below). Last year’s recommendations from the bipartisan Simpson-Bowles commission, which were ignored, are not a bad place to start. What happens in the lame-duck session of Congress (after the elections) will dramatically impact the score of the current economic game, and decide who wins and who loses.

Source: Calafia Beach Pundit (Scott Grannis)

Heated debates continue on how the gap between expenses and revenues will be narrowed, but regardless, Democrats will continue to push for capital gains tax hikes on the rich (see tax chart below); and the Republicans will push to cut spending on entitlements, including untenable programs like Medicare and Social Security.

Source: The Wall Street Journal

The game is not quite over, but the fourth quarter promises to be a bloody battle. So while the replacement refs may be back at home, the experienced returning refs have been known to blow calls too. Let’s just hope that autumn, the season of bounteous fecundity, ends up being a continued trend of sweet market success, rather than a political period of botched opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Private Equity: Parasite or Pollinator?

In the wild, there exist both parasitic and symbiotic relationships. In the case of blood thirsty ticks that feed off deer, this parasitic relationship differs from the symbiotic association of nectar-sucking bees and pollen-hungry flowers. These are merely a few examples, but suffice it to say, these same intricate interactions occur in the business world as well.

Our economy is a complex jungle of relationships, spanning governments, businesses, consumers, investors, and many intermediaries, including private equity (PE) firms. With the November election rapidly approaching, more attention is being placed on how private equity firms fit into the economic food chain. Figuring out whether PE firms are more like profit-sucking parasites or constructive job creating mechanisms has moved to the forefront, especially given presidential candidate Mitt Romney’s past ties to Bain Capital, a successful private equity firm he founded in 1984.

Currently it is politically advantageous to portray PE professionals as greedy, job-cutting outsourcers – I’m still waiting for the political ad showing a PE worker clubbing a baby seal or plucking the legs off of a Daddy Long Legs spider. While I’d freely admit a PE pro can be just as gluttonous as an investment banker, hedge fund manager, or venture capitalist, simplistic characterizations like these miss the beneficial effects these firms provide to the overall economy. Capitalism is the spine that holds our economy together and has allowed us to grow into the greatest superpower on the planet. Private equity is but a small part of our capitalistic ecosystem, but plays a valuable role nonetheless.

While there are many perspectives on the role of private equity in our economy, here are my views on a few of the hot button issues:

Job Creation: Although I believe PE firms are valuable to our economy, I think it is a little disingenuous of Romney and his supporters to say Bain was a net “job creator” to the tune of 100,000+ jobs during his tenure. The fact of the matter is PE firms’ priority is to create profitable returns for its investors, and if that requires axing heads, then so be it – most PE firms have no qualms doing precisely that. Romney et al point to successes like Staples Inc. (SPLS), Dominos Pizza Inc. (DPZ) and Sports Authority, Inc., where profitability and success ultimately led to job expansion. From my viewpoint, I believe these examples are more the exception than the rule. Not surprisingly, any job losses executed in the early years of a PE deal will eventually require job additions if the company survives and thrives. Let’s face it, no company can cut its way to prosperity in perpetuity.

Competitveness: Weak, deteriorating, or bankrupt companies cannot and will not hire. Frail or mismanaged companies will sooner or later be forced to cut jobs on their own –the same protocol applied by opportunistic PE vultures swarming around. While PE firms typically focus on bloated or ineffective companies, I think the media outlets overemphasize the cost-cutting aspects of these deals. Sure, PE companies cut jobs, outsource functions, and cut benefits in the name of profits, but that alone is not a sustainable strategy. Trimming fat, by replacing complacent management teams, investing in modern software/equipment, expanding markets, and implementing accountability are all paramount factors in making these target companies more efficient and competitive in the long-run.

Financial Markets-Arbiter: At the end of the day, I think the IPO/financial markets are the final arbiters of how much value PE firms create, not only for investors, but also for the economy overall. If greedy PE firms’ sole functions were to saddle companies with massive debts, cut heads off, and then pay themselves enormous dividends, then there would never be a credible exit strategy for investors to cash out. If PE firms are correctly performing their jobs, then they will profitably create leaner more efficient durable companies that will be able to grow earnings and create jobs over the long-term. If they are unsuccessful in this broad goal, then the PE firm will never be able to profitably exit their investment via a corporate sale or public offering.

Bain Banter: Whether you agree with PE business practices or not, it is difficult to argue with the financial success of Bain Capital. According to a Wall Street Journal article, Bain Capital deals between 1984 – 1999 produced the following results:

“Bain produced about $2.5 billion in gains for its investors in the 77 deals, on about $1.1 billion invested. Overall, Bain recorded roughly 50% to 80% annual gains in this period, which experts said was among the best track records for buyout firms in that era.”

Critics are quick to point out the profits sucked up by PE firms, but they neglect to acknowledge the financial benefits that accrue to the large number of pension fund, charity, and university investors. Millions of middle-class American workers, retirees, community members, teachers, and students are participating in those same blood sucking profits that PE executives are slurping down.

Even though I believe private equity is a net-positive contributor to competiveness and economic growth in recent decades, there is no question in my mind that these firms participated in a massive bubble in the 2005-2007 timeframe. Capital was so cheap and abundant, prices on these deals escalated through the roof. What’s more, the excessive amounts of leverage used in those transactions set these deals up for imminent failure. PE firms and their investors have lost their shirts on many of those deals, and the typical 20%+ historical returns earned by this asset class have become long lost memories. Attractive returns do not come without risk.

With the presidential election rhetoric heating up, the media will continue to politicize, demonize and oversimplify the challenges surrounding this asset class. Despite its shortcomings, private equity will continue to have a positive symbiotic relationship with the economy…rather than a parasitic one.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in SPLS, DPZ, Sports authority, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Trading Obama, Romney and Extraterrestrials

Source: Photobucket

Investors vote on stocks every day by buying shares in favored positions and selling shares in those out-of-favor. But shouldn’t voting on stocks be different from voting for politicians? Actually, no! Now, politicians can be traded just like traditional stocks or other liquid securities. If you don’t believe me, then you should check out www.Intrade.com. Intrade is an online trading platform that is home to various prediction markets that forecast the probability of outcomes of various real-world events, including who will win the 2012 U.S. Presidential election. Just like investors can trade IBM on the New York Stock Exchange (NYSE) or Apple Inc. (AAPL) on the NASDAQ exchange, so too can individuals trade election shares in Barack Obama (ticker: OBMA) and Mitt Romney (ticker: RMNY) on the Intrade platform (see chart below).

Source: Intrade.com

By definition, the trading mechanics of Intrade involve a resolution of a particular event structured as a binary “Yes” or “No” result. Similar to a sports bet, Intrade eventually declares a winning or losing outcome – but there are no ties. For example, by November 6, 2012, we will know whether Obama’s shares will be trading either at $10 per share, if he becomes re-elected, or $0 per share if he loses to Romney. Just like a stock, traders can go long Obama shares, if they think he will win, or short Obama shares, if they think he will lose. Analogous to stocks, holding periods may vary too. Traders can either hold their position until the event expiration, and realize a gain or loss, or instead traders can lock in shorter-term profits/losses by closing a position before the official outcome ends.

Another great thing about Intrade’s prediction markets is that each event share price can be quickly converted to an outcome probability. So as you can see from Obama’s Intrade chart above, the current $5.28 share price signifies a 52.8% probability of Obama winning the 2012 Presidential election. No need to worry about distracting stock-splits, share offerings, or stock buybacks that could distort the true underlying dynamics of the Intrade event fundamentals.

Bizarre Bets and Over-the-Top Trades

Crazy Super Bowl “prop” bets have been around for ages, and the senseless nature of the bets did not disappoint this year, if you consider the following ridiculous Super Bowl XLVI prop bets:

• Will it take Kelly Clarkson longer or shorter than 1 minute 34 seconds to sing the National Anthem?

• Will Madonna’s hair color be blonde when she begins the Super Bowl Halftime show?

• How many times will model Giselle Bundchen be shown on TV during the game?

• What Color will the Gatorade be that is dumped on the Head Coach of the Winning Super Bowl Team?

I think you get the idea from these examples, and I believe Intrade figured out the quirky benefits as well. Betting on unusual or strange outcomes can be a lucrative endeavor.

Here are just a few of the bizarre and remarkable events you can trade on Intrade:

• NASA to announce discovery of extraterrestrial life before midnight Dec. 31, 2012

• Arctic sea ice area for Sep. 2012 to be less than 4.3 million square kilometers?

• Magnitude 9.0 (or higher) earthquake to occur anywhere before midnight Dec. 31, 2012

• The Dark Knight Rises to break the all-time opening weekend box-office record

• The US debt limit to be raised before midnight Dec. 31, 2012

• Bashar al-Assad to no longer be President of Syria before midnight Dec. 31, 2012

• The US Supreme Court to rule individual mandate unconstitutional before midnight Dec. 31, 2012

• Higgs Boson Particle to be observed on/before Dec. 31, 2013

Rules of the Game

You may be asking yourself, “All this betting/trading sounds like fun, but isn’t this Intrade thing illegal gambling?” If your thought process went in this direction, you are not alone – I asked myself the same question. I’m no attorney, but the apparent loophole for Intrade’s business operation appears to be tied to its foreign incorporation in Ireland. Less apparent is how American law applies to Intrade as referenced in a recent New York Times article that states, “It is unclear whether American law applies to Intrade.”

Although U.S. residents may not be able to trade legally on Intrade, roaming the site may provide some quirky entertainment and provide profound answers to critical questions like, “Do extraterrestrials exist?; How much money will the new Batman movie make at the box office?; And which President are we going to get stuck with for the next four years?” Surfing around on Intrade can be a blast, but if it gets too boring, you can always go back to trading regular stocks.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and Wade Slome have no affiliation with Intrade. SCM and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in NYX, IBM any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Broken Record Repeats Itself

Article is an excerpt from previously released Sidoxia Capital Management’s complementary June 2012 newsletter. Subscribe on right side of page.

Traditional music records have been replaced with CDs (compact discs) and digital downloads. Although the problem of a broken record repeating itself is no longer an issue, our financial markets have not conquered the problem of repetition. More specifically, the timing of the -6.3% stock market decline during May (as measured by the S&P 500 index), coincides with the same broken sell-offs we have temporarily experienced over the last two summers. First, we had the “Flash Crash” in the summer of 2010, and then the debt ceiling debate and credit downgrade of 2011.

So far, the “Sell in May and go away” mantra has followed the textbook lessons over the last few years, but as you can see from the chart below, the short-lived seasonal sell-offs have been followed by significant advances (up +33% from 2010 lows and up +29% from the 2011 lows). Given the global challenges, a two-steps forward, one-step back pattern in equity markets should not be seen as overly surprising by investors.

Source: Yahoo Finance

Although the late-spring and summer doldrums have not been a joy-ride in recent years, these overly simplistic seasonal trading rules of thumb have not been exceedingly reliable either. For example, even though the months of May in 2010-2012 produced negative returns, the previous 25 Mays going back to 1985 produced positive returns more than 2/3 of the time. Rather than fiddle with these unreliable, unscientific trading rules, individuals would be better served by listening to famous Jedi Master Yoda from Star Wars, who so astutely noted, “Uncertain, the future is.”

Voting Machines and Scales

Given the spread of globalization and technology, the speed of news dissemination has never been faster. With the 2008-2009 financial crisis still burned into investors’ minds, the default response to any scary news item is to shoot first and ask questions later. Renowned long-term investing legend Ben Graham famously highlighted, “In the short run the market is a voting machine. In the long run it’s a weighing machine.”

As it relates to short-run current events, here are some of the items that investors were voting on (no pun intended) this month:

Europe, Europe, Europe: This problem has been with us for some time now, and there are no signs it will disappear anytime soon. In a game of chicken between the EU (European Union) and Greek legislators, fresh elections are taking place on June 17th, which will ultimately determine if Greece will exit the Euro monetary union or stick to the bitter medicine of austerity prescribed by the key European decision-makers in Germany. As Greece attempts to clean up its own mess, European politicians and G-20 leaders around the globe are scrambling to create plans that ring-fence countries like Spain and Italy from succumbing to a Greek-born contagion.

Presidential Politics: If you haven’t been living in a cave for the last six months, you probably know that 2012 is a presidential election year. Regardless of your politics, there are big questions surrounding the economy, jobs, deficits, debt, taxes, entitlements, defense, gay marriage, and other important issues. Answers to many of these questions will remain unclear until we get closer to the elections. The financial markets do not like uncertainty, so probabilities would indicate volatility will remain par for the course for the foreseeable future.

Facebook Folly: Despite my warnings, Facebook’s initial public offering (IPO) failed to live up to the social media giant’s hype – the share price has fallen -22% since the shares originally priced. Great companies do not always make great stocks, especially when a relatively new kid on the block has his company’s stock initially valued at a hefty price-tag of more than a $100 billion. Finger pointing is being spread liberally on the botched Facebook deal (e.g., Morgan Stanley, NASDAQ, Facebook), but no need to shed a tear for 28-year-old founder Mark Zuckerberg since his ownership stake in the company is still valued at around $15 billion – enough to cover a European trip to McDonald’s with his newlywed wife.

Dimon in a Rough Spot: Jamie Dimon, the poster child of the banking industry (and CEO of JP Morgan Chase – JPM), dropped a bomb on the investment community earlier in the month by explaining how a rogue “whale” trader racked up $2 billion in initial losses (and growing) by taking excessive risk and throwing controls into the wind.

Chinese Dragon Losing Steam: The #2 global economy has been losing some steam as witnessed by slowing industrial production and GDP growth (Gross Domestic Product). In turn, the self correcting economic forces of supply and demand have provided relief to consumers and corporations in the form of lower fuel, energy, and commodity prices. Chinese leaders are not sitting still – there are plans of accelerating infrastructure spending and assisting banks in the form of capital injections and lower reserve requirements.

As I discussed in a previous Investing Caffeine article (see The European Dog Ate My Homework), although the current headlines remain gloomy, that will always be the case. Just a few years ago, Bear Stearns, Lehman Brothers, AIG, CDS (credit default swaps), and subprime mortgages were the boogeymen. In the 1980s, we had the Savings & Loan financial crisis and the infamous 1987 Crash. During the 1970s, the Vietnam War, Nixon’s impeachment proceedings, and rising inflation were the dominating issues. Since then, the equity markets are up over 20x-fold – time will always reward those patient long-term investors. Despite all the doom and gloom, stock markets have roughly doubled over the last three years and all the major indexes remain solidly in the black for the year. Choppy waters are likely to remain as we approach this year’s elections, but for those who understand broken records often repeat themselves, there’s a good chance the music will eventually sound much better.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including commodities, inflation protection, floating rate bonds, real estate, dividend, and alternative investment ETFs), but at the time of publishing SCM had no direct position in FB, MCD, JPM, MS, NDAQ, AIG, Lehman Brothers, Bear Stearns, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Listening for Dinner Bell or Penalty Whistle?

Excerpt from my monthly newsletter (sign-up on the right of page)…

Investors are eagerly waiting on the sidelines wondering whether to listen for a dinner bell signaling the time to sink their teeth into traditional equity investments, or respond to a penalty whistle by nervously maintaining money in depleted, inflation-losing CDs. A large swath of investors are still scarred from the losses experienced from the 2008-2009 financial crisis and are trying to rationalize the recent +80% move in equity markets (S&P 500 index) over the last 18 months. Eating saltine crackers and drinking water in CDs and money market accounts yielding < 1% feels OK when the world is collapsing around you, but eventually people realize retirement goals are tough to achieve with the money stuffed under the mattress.

Here are some recent bells and whistles we are listening to:

Mid-Term Elections: Regardless of your politics, Republicans are forecasted to regain control of the House of Representatives, while expectations for a narrow Democrat Senate majority remains the consensus. Currently, Democrat Jerry Brown is a handful of points in the lead over Meg Whitman for the California governor’s race. Another issue voters are closely monitoring is the likelihood of Bush tax-cut extensions.

Printing Press Part II: The Federal Reserve has strongly hinted of another round at the printing press in an effort to stimulate the economy by keeping interest rates low (e.g., record low 30-year fixed mortgage rates around 4.2%). The Fed accomplishes this so-called Quantitative Easing (or QE2) by purchasing Treasuries and mortgage backed securities – pumping more dollars into the financial system to expand credit and loans. In addition, QE2 is structured to stimulate the meager 0.8% core inflation experienced over the last 12 months (Bloomberg) to a Goldilocks level – not too hot and not too cold. QE2 asset purchase estimates are all over the map, but estimates generally stand at the low end of the original $200 billion to $2 trillion range.

Growth Continues: Although companies are sitting on record piles of cash ($1.8 trillion for all non-financial companies), chief executive officers continue to have short arms with their deep pockets when it comes to spending on new hires. Persistent growth for five consecutive quarters (2% GDP expansion in Q2), coupled with tight cost controls, is resulting in 46% estimated growth in 2010 corporate profits as measured by the average of S&P 500 companies. For the time being, “double dip” worries have been put on hold for this jobless recovery.

Unemployment Hypochondria: As I wrote in an earlier Investing Caffeine article (READ HERE), there is an almost obsessive focus on the unemployment rate, which although moving in the right direction, remains at a stubbornly high 9.6% rate nationally. Fresh new employment data will be released this Friday.

Foreclosure-gate: As foreclosures have increased and the decline in the housing market has matured, investors have grown more impatient with collections from mortgage backed securities originators. Banks and other mortgage lenders could face more than $100 billion in losses (CNBC) in mortgage “putbacks” related to improper packaging and terms disclosed to investors. Lawyers are salivating at the opportunity of litigating the thousands of potential cases across the country.

Create Your Own Blueprint – Block Noise

In reality, there is no dinner bell or penalty whistle when it comes to investing. Sure, we hear dinner bells and whistles every day on TV from strategists and economists, but in this sordid, cacophony of daily noise, the long line-up of soothsayers are constantly switching back and forth between optimistic bells and pessimistic whistles. The consistent onslaught of this indiscernible noise serves no constructive purpose for the average investor. I strongly believe the correct plan of attack is to create a customized investment plan that meets your long-term objectives, constraints, and risk tolerance. By creating a diversified portfolio of low-cost tax-efficient products and strategies, I believe investors will be more securely positioned for a more comfortable and less stressful retirement.

I have my own opinions on the economic environment, which I detail in excruciating detail through my InvestingCaffeine.com writings. These macro-economic opinions are stimulating but have little to no bearing on the construction of my investment portfolios. More important is focusing on the investment areas with the best fundamental prospects, while balancing risk and return for each client.

Despite what I just said, if you are still determined to know my opinions on the market direction, then follow me to the dinner table; I just heard the dinner bell ring.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in GE, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}

{kind=link}