Posts tagged ‘Ed Yardeni’

Political Showers Bring Record May Stock Flowers

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2017). Subscribe on the right side of the page for the complete text.

There has been a massive storm of political rain that has blanketed the media airwaves and internet last month, however, the stock market ignored the deluge of headlines and focused on more important factors, as prices once again pushed to new record highs. Over the eight-year bull market, the old adage to “sell in May, and go away,” once again was not a very successful strategy. Had investors heeded this advice, they would have missed out on a +1.2% gain in the S&P 500 index during May (up +7.7% for 2017) and a +2.5% surge in the technology-driven NASDAQ index (+15.1% in 2017).

Keeping track of the relentless political storm of new headlines and tweets almost requires a full-time staff person, but nevertheless we have summarized some of the political downpour here:

French Elections: In the wake of last year’s U.K. “Brexit”, fears of an imminent “Frexit” (French Exit) resurfaced ahead of the French presidential. Emmanuel Macron, a 39-year-old former investment banker, swept to a decisive victory over National Front candidate Marine Le Pen by a margin of 66% to 34%.

Firing of FBI Director: President Trump fired FBI Director James Comey based on the recommendation of deputy attorney general Rod Rosenstein, who cited Comey’s mishandling of Hillary Clinton’s private email server investigation. The president’s critics claim Trump was frustrated with the FBI’s investigation into the administration’s potential ties with Russian officials in relation to the 2016 presidential elections. Comey is expected to testify next week to Congress, where he will likely address reports that President Trump asked him to drop the FBI’s investigation into former National Security Advisor Michael Flynn during a February meeting.

Trump Classified Leak to Russians: Reports show that President Trump revealed classified information regarding the Islamic State (ISIS) to the Russian foreign minister during an Oval Office meeting. The ISIS related information emanating from Syria reportedly had been passed to the U.S. from Israel, with the provision that it not be shared.

Impeachment Talk and Appointment of Independent Special Prosecutor: Heightened reports of Russian intervention coupled with impeachment cries from the Democratic opposition coincided with Deputy Attorney General Rod Rosenstein’s announcement that former FBI director Robert Mueller III would take on the role as an independent special counsel in the investigation of Russian interference in the 2016 election. Rosenstein had the authority to make the appointment after Attorney General Jeff Sessions recused himself after admitting contacts with Russian officials. The White House, which has denied colluding with the Russians, issued a statement from President Donald Trump looking forward “to this matter concluding quickly.”

Kushner Under Back Channel Investigation: President Trump’s son-in-law and senior advisor, Jared Kushner, is under investigation over discussions to set up a back channel of communication with Russian officials. At the heart of the probe is a December meeting Kushner held with Sergey Gorkov, an associate of Russian President Vladimir Putin and the head of the state-owned Vnesheconombank, a Russian bank subject to sanctions imposed by President Obama. Back channels have been legally implemented by other administrations, but the timing and nature of the discussions could make the legal interpretation more difficult.

Trump’s First Foreign Trip: A whirlwind trip by President Trump through the Middle East and Europe, resulted in commitments to Middle East peace, multi-billion contract signings with the Saudis, pledges to fight Muslims extremism, calls for NATO members to pay their “fair share,” and demands for German President Angela Merkel to address the elevated trade deficit with the U.S.

Subpoenas Issued to Trump Advisors: The House Intelligence Committee issued subpoenas to ousted National Security Adviser Michael Flynn and President Trump’s personal attorney, Michael Cohen, as it relates to potential Russian interference in the presidential campaign. Flynn reportedly plans to invoke his Fifth Amendment rights in response to a separate subpoena issued by the Senate Intelligence Committee.

Repeal and Replace Healthcare: The Republican-controlled House of Representatives narrowly passed a vote to repeal and replace the Affordable Care Act after prior failed attempts. The bill, which allows states to apply for a waiver on certain aspects of coverage, including pre-existing conditions, received no Democratic votes. While the House passage represents a legislative victory for President Trump, Senate Republicans must now take up the legislation that addresses conclusions by the nonpartisan Congressional Budget Office (CBO). More specifically, the CBO found the revised House health care bill could leave 23 million more Americans uninsured while reducing the federal deficit by $119 billion in the next decade.

North Korea Missile Tests: If domestic political turmoil wasn’t enough, North Korea conducted an unprecedented number of medium-to-long-range missile tests in an effort to develop an intercontinental ballistic missile (ICBM) capable of hitting the mainland United States. Due to the rising tensions, the U.S. and South Korea have been planning nuclear carrier drills off the coast of the Korean peninsula.

Wow, that was a mouthful. While all these politics may be provocative and stimulating, long-time followers of mine understand my position…politics are meaningless (see Politics-Schmolitics). While a terrorist or military attack on U.S. soil would undoubtedly have an immediate and negative impact, 99% of daily politics should be ignored by investors. If you don’t believe me, just take a look at the stock market, which continues to make new record highs in the face of a hurricane of negative political headlines. What the stock market really cares most about are profits, interest rates, and valuations:

- Record Profits: Stock prices follow the direction of earnings over the long-run. As you can see below, profits vacillate year-to-year. However, profits are currently surging, and therefore, so are stock prices – despite the negative political headlines.

Source: Dr. Ed’s Blog

- Near Generationally Low Interest Rates: Generally speaking, most asset classes, including real estate, commodities, and stock prices are worth more when interest rates are low. When you could earn 15% on a bank CD in the early 1980s, stocks were much less attractive. Currently, bank CDs almost pay nothing, and as you can see from the chart below, interest rates are near a generational low – this makes stock prices more attractive.

- Attractive Valuations: The price you pay for an asset is always an important factor, and the same principle applies to your investments. If you can buy a $1.00 for $0.90, you want to take advantage of that opportunity. Unfortunately, the value of stocks is not measured by a simple explicit price, like you see at a grocery store. Rather, stock values are measured by a ratio (comparing an investment’s price relative to profits/cash flows generated). Even though the stock market has surged this year, stock values have gotten cheaper. How is that possible? Stock prices have risen about +8% in the first quarter, while profits have jumped +15%. When profits rise faster than prices appreciate, that means stocks have gotten cheaper. From a multi-year standpoint, I agree with Warren Buffett that prices remain attractive given the current interest rate environment. To read more about valuations, check out Ed Yardeni’s recent article on valuations.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

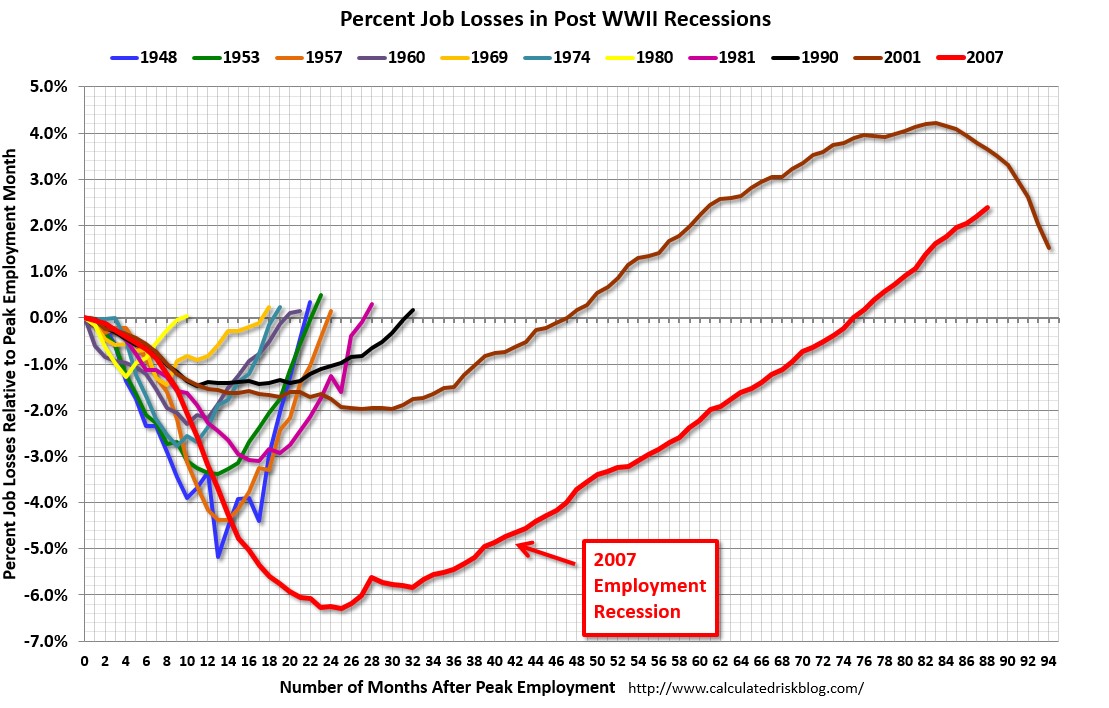

Coast is Clear Until 2019

The economic recovery since the Great Financial Crisis of 2008-09 has been widely interpreted as the slowest recovery since World War II. Bill McBride of Calculated Risk captures this phenomenon incredibly well in his historical job loss chart (see red line in chart below):

Source: Calculated Risk

History tells us that the economy traditionally suffers from an economic recession twice per decade, but we are closing in on seven years since the last recession with little evidence of impending economic doom.

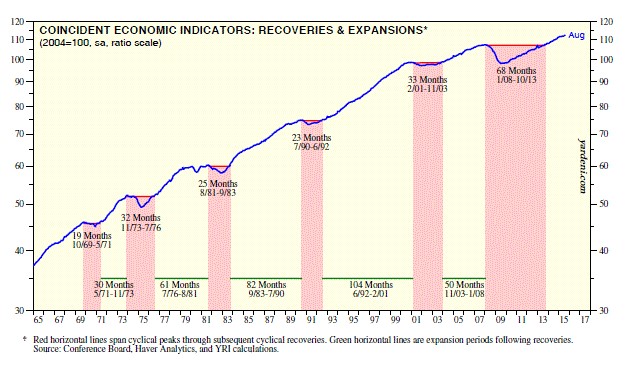

So, are we due for another recession? Logic would dictate that since this recovery has been the slowest in a generation, the duration of this recovery should also be the longest. Strategist Ed Yardeni of Dr. Ed’s Blog uses data from historical economic cycles and CEI statistics (Coincident Economic Indicators) to make the same case. Based on his analysis, Yardeni does not see the next recession arriving until March 2019 (see chart below). If you take a look at the last five previous cycle peaks, recoveries generally last for an additional five and a half years (roughly 65 months). Since the last rebound to a cyclical peak occurred in October 2013, 65 months from then would imply the next downturn would begin in March 2019.

Source: Dr. Ed’s Blog

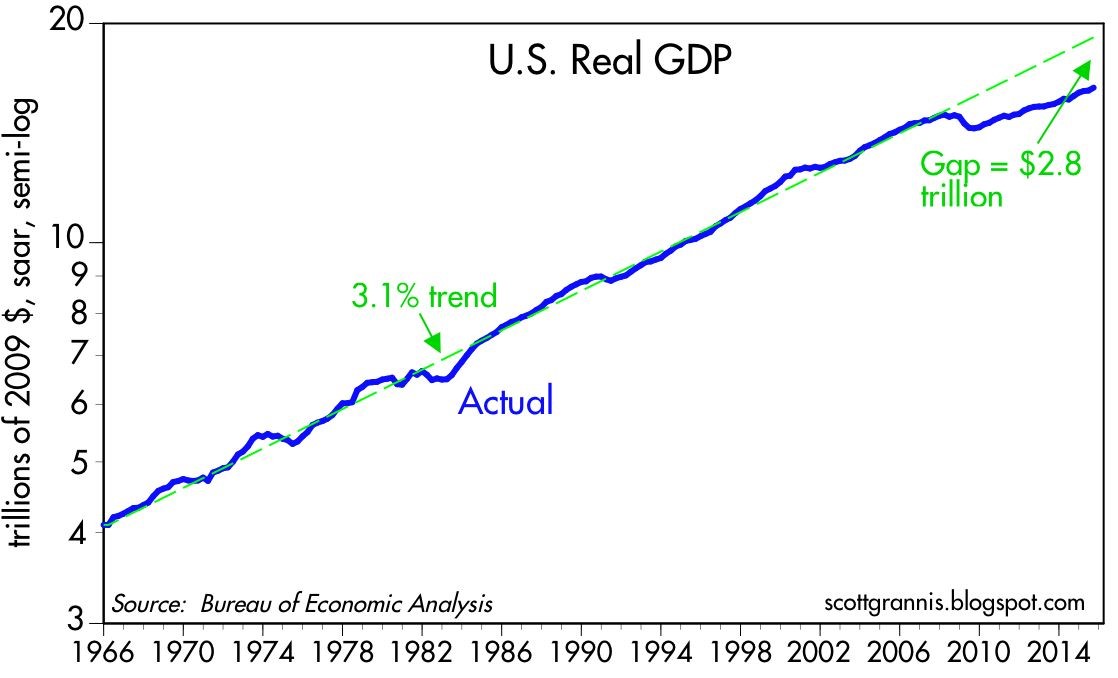

Typically, an economy loses steam and enters a recession after a phase of over-investment, tight labor conditions, and an extended period of tight central bank monetary policies. Over the last seven years, we have experienced quite the opposite. Corporations have been very slow to invest or hire new employees. For those employees hired, many of them are “under-employed” (i.e., working part-time), or in other words, these workers want more work hours. Our country’s slower-than-expected growth has created an output gap. Scott Grannis at Calafia Beach Pundit estimates this gap to approximate $2.8 trillion (see chart below). The CBO expects a smaller gap estimate of about $580 billion to narrow over the next few years. By Grannis’s calculations, there is a reservoir of 5 – 10 million jobs that could be tapped if the economy was operating more efficiently.

Source: Calafia Beach Pundit

Bolstering his argument, Grannis points out that the risk of a recession rises when there are significant capacity constraints and tight money. He sees the opposite happening – an enormous supply of unused capacity remains underutilized as he describes here:

“Today, money is abundant and resources are abundant. Even energy is abundant, because its price has fallen by over 50% in the past year or so. Corporate profits are near record highs, the supply of labor is virtually unconstrained, energy is suddenly cheap, and productive capacity is relatively abundant.”

While new uncertainties have been introduced (e.g., slowing China, potential government shutdown/sequestration, emerging market weakness), the reality remains there is always uncertainty. Even if you truly believe there is more uncertainty today relative to yesterday, the economy has some relatively strong shock absorbers to ride out the volatility.

There are plenty of potentially bad things to worry about, but if it’s a cyclical recession that you are worried about, then why don’t you grab a seat, order a coconut drink with an umbrella, and wait another three and a half years until you reach the circled date of March 2019 on your calendar.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Chicken or Beef? Time for a Stock Diet?

The stock market has been gorging on gains over the last six years and the big question is are we ready for a crash diet? In other words, have we consumed too much, too fast? Since the lows of 2009 the S&P 500 index has more than tripled (or +209% without dividends).

In our daily food diets our proteins of choice are primarily chicken and beef. When it comes to finances, our investment choices are primarily stocks and bonds. There are many factors that can play into a meat-eaters purchase decision, including the all-important factor of price. When the price of beef spikes, guess what? Consumers rationally vote with their wallets and start substituting beef for relatively lower priced chicken options.

The same principle applies to stocks and bonds. And right now, the price of bonds in general have gone through the roof. In fact bond prices are so high, in Europe we are seeing more than $2 trillion in negative yielding sovereign bonds getting sucked up by investors.

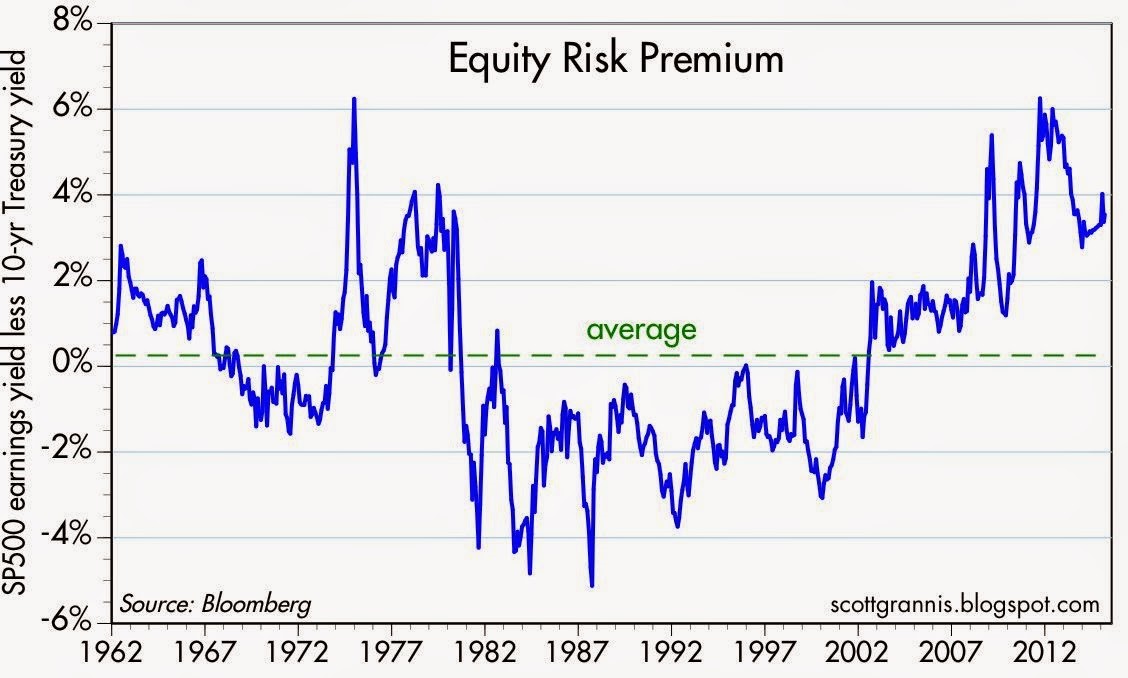

Another area where we see evidence of pricey bonds can be found in the value of current equity risk premiums. Scott Grannis of Calafia Beach Pundit posted a great 50-year history of this metric (chart below), which shows the premium paid to stockholders over bondholders is near the highest levels last seen during the Great Recession and the early 1980s. To clarify, the equity risk premium is defined as the roughly 5.5% yield currently earned on stocks (i.e., inverse of the approx. 18x P/E ratio) minus the 2.0% yield earned on 10-Year Treasury Notes.

Source: Scott Grannis

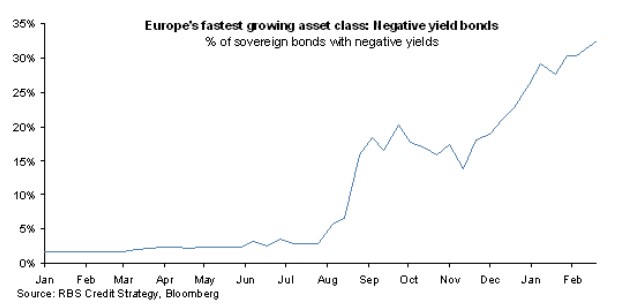

The equity risk premium even looks more favorable if you consider the negative interest rate European environment mentioned earlier. The 60 billion euros of monthly debt in ECB (European Central Bank) quantitative easing purchases has accelerated the percentage of negative yield bond issuance, as you can see from the chart below.

Source: FT Alphaville

Hibernating Bond Vigilantes

Dr. Ed Yardeni coined the famous phrase “bond vigilantes” to describe the group of hedge funds and institutional investors who act as the bond market sheriffs, ready to discipline any over leveraged debt-issuing entity by deliberately cratering prices via bond sales. For now, the bond vigilantes have in large part been hibernating. As long as the vigilantes remain asleep at the switch, stock investors will likely continue earning these outsized premiums.

How long will these fat equity premiums and gains stick around? A simple diet of sharp interest rate increases or P/E expansion would do the trick. An increase in the P/E ratio could come in one of two ways: 1) sustained stock price appreciation at a rate faster than earnings growth; or 2) a sharp earnings decline caused by a recessionary environment. On the bright side for the bulls, there are no imminent signs of interest rate spikes or recessions. If anything, dovish commentary coming from Fed Chairwoman Janet Yellen and the FOMC would indicate the economy remains in solid recovery mode. What’s more, a return to normalized monetary policy will likely involve a very gradual increase in interest rates – not a piercing rise as feared by many.

Regardless of whether it’s beef prices or bond prices spiking, rather than going on a crash diet, prudently allocating your money to the best relative value will serve your portfolio and stomach best over the long run.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Stock Market: Shrewd Bet or Stupid Gamble?

Trillions of dollars have been lost and gained over the last five years. The extreme volatility strangled investment portfolios, and as a result millions of investors capitulated by throwing in the towel and locking in losses. Melted 401ks, shrunken IRAs, and beat-up retirement accounts bruised the overarching psyche of Americans to the point they questioned whether the stock market is a shrewd bet or stupid gamble?

The warmth and safety of bonds provided some temporary relief in subsequent years, but the explosive rebound in stock prices to new record highs in 2013 coupled with the worst year in a decade for bonds still have many on the sidelines asking whether they should get back in?

As I’ve written many times in the past (see Timing Treadmill), timing the market is a fruitless effort. Elementary statistics, including the “Law of Large Numbers” will demonstrate that blind squirrels can and will beat the market on occasion, but very few can consistently beat the stock market indices for sustained periods (see Dart-Throwing Chimps).

However, there have been some gun-slinging hedge fund managers who have accumulated some impressive track records. Because of insanely high management fees, many overpaid hedge fund managers will swing for the fences by using a combination of excessive leverage and/or concentration. If the hedge funds connect with lucky returns, the managers can take the money and run. If they swing and miss…no problem. Close shop, hang out a shingle across the street, change the hedge fund’s name, and try again. Of course there are those successful hedge fund managers who have learned how to manipulate the system and exploit information to their advantage, but many of those managers like Raj Rajaratnam and Steven Cohen are either behind bars or dealing with the Feds (see fantastic Frontline piece on Cohen).

But not everyone cheats. There actually are a minority of managers who consistently beat the market by taking a long-term approach like Warren Buffett. Long-term outperforming managers are like lifetime .300 hitters in Major League Baseball – the outperformers exist, but they are rare. In 2007, AssociatedContent.com did a study that showed there were only 12 active career .300 hitters in Major League Baseball.

Another legend in the investment industry is John Bogle, the founder of the Vanguard Group, a firm primarily focused on passive, index-based investment strategies. Although it is counter-intuitive to most, just matching the market (or index) will put you in the top-quartile over the long-run (see Darts, Monkeys & Pros). There’s a reason Vanguard manages more than $2,000,000,000,000+ (yes…trillion) of investors’ money. Even at this gargantuan size, Vanguard remains a fraction of the overall industry. Regardless, the gospel of low-cost, tax-efficient, long-term horizons is slowly leaking out to the masses (Disclosure: Sidoxia is a devoted user of Vanguard and other providers’ low-cost Exchange Traded Funds [ETFs]).

Rolling the Dice?

Unlike Las Vegas, where the odds are stacked against you, in the stock market the odds are stacked in your favor if you stay in the game long enough and don’t chase performance. Dr. Ed Yardeni has a great chart (below) summarizing stock market returns over the last 85 years, and what the data highlights is that the market is up (or flat) 69% of the time (59/86 years). The probabilities are so favorable that if I got comparable odds in Vegas, I’d probably live there!

Source: Dr. Ed’s Blog

Unfortunately, rather than using this time arbitrage in conjunction with the incredible power of compounding (see A Penny Saved is Billions Earned), many individuals look at the stock market like a casino – similarly to betting on black or red at a roulette wheel. Speculating about the direction of the market can be fun, and I’ve been known to guess on occasion, but it’s a complete waste of time. Creating a long-term plan of reaching or maintaining your retirement goals through a diversified portfolio is the way to go – not bobbing in out of the market with cash and bonds.

At Sidoxia, we don’t actively trade and time individual stocks either. For the majority of our client portfolios, we follow a growth philosophy similar to the late T. Rowe Price:

“The growth stock theory of investing requires patience, but is less stressful than trading, generally has less risk, and reduces brokerage commissions and income taxes.”

Nobody knows the direction of the stocks with certainty, and irrespective of whether the market goes down this year or not, history has proven the stock market has been a shrewd, long-term bet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Aaaaaaaah: Turbulence or Nosedive?

We’ve all been there on that rocky plane ride…clammy hands, heart beating rapidly, teeth clenched, body frozen, while firmly bracing the armrests with both appendages. The sky outside is dark and the interior fuselage rattles incessantly until….whhhhhssssshhh. Another quick jerking moment of turbulence has once again sucked the air out of your lungs and the blood from your heart. The rational part of your brain tries to assure you that this is normal choppy weather and will shortly transition to calm blue skies. The irrational and emotional, part of our brains (see Lizard Brain) tells us the treacherous plane ride is on the cusp of plummeting into a nosedive with passengers’ last gasps saved for blood curdling screams before the inevitable fireball crash.

Well, we’re now beginning to experience some small turbulence in the financial markets, and at the center of the storm is a collapsing Argentinean peso and a perceived slowing in China. In the case of Argentina, there has been a century-long history of financial defaults and mismanagement (see great Scott Grannis overview). Currently, the Argentinean government has been painted into a corner due to the depletion of its foreign currency reserves and financial mismanagement, as evidenced by an inflation rate hitting a whopping 25% rate.

On the other hand, China has created its own set of worries in investors’ minds. The flash Markit/HSBC Purchasing Managers’ Index (PMI) dropped to a level of 49.6 in January from 50.50 in December, which has investors concerned of a market crash. Adding fuel to the fear fire, Chinese government officials and banks have been trying to reverse excesses encountered in the country’s risky shadow banking system. While the size of Argentina’s economy may not be a drop in the bucket, the ultimate direction of the Chinese economy, which is almost 20x’s the size of Argentina’s, should be much more important to global investors.

At the end of the day, most of these mini-panics or crises (turbulence) are healthy for the overall financial system, as they create discipline and will eventually change irresponsible government behaviors. While Argentinean and Chinese issues dominate today’s headlines, these matters are not a whole lot different than what we have read about Greece, Ireland, Italy, Spain, Portugal, Cyprus, Turkey, and other negligent countries. As I’ve stated before, money goes where it’s treated best, and the stock, bond, and currency vigilantes ensure that this is the case by selling the assets associated with deadbeat countries. Price declines eventually catch the attention of politicians (remember the TARP vote failure of 2008?).

Is This the Beginning of the Crash?!

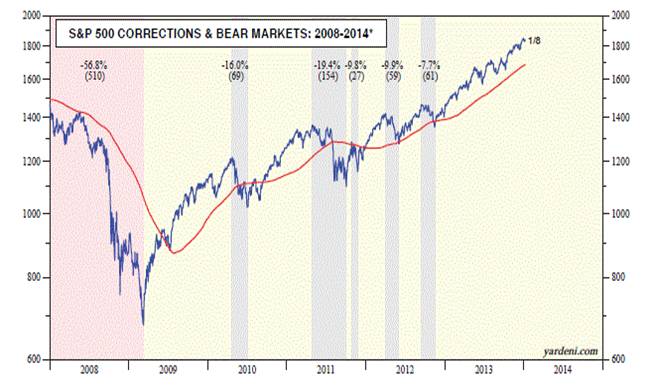

What goes up, must come down…right? That is the pervading sentiment I continually bump into when I speak to people on the street. Strategist Ed Yardeni did a great job of visually capturing the last six years of the stock market (below), which highlights the most recent bear market and subsequent major corrections. Noticeably absent in 2013 is any major decline. So, while many investors have been bracing for a major crash over the last five years, that scenario hasn’t happened yet. The S&P chart shows we appear to be due for a more painful blue (or red) period of decline in the not-too-distant future, but that is not necessarily the case. One would need only to thumb through the history books from 1990-1997 to see that investors lived through massive gains while avoiding any -10% correction – stocks skyrocketed +233% in 2,553 days. I’m not calling for that scenario, but I am just pointing out we don’t necessarily always live through -10% corrections annually.

Source: Dr. Ed’s Blog

Even though we’ve begun to experience some turbulence after flying high in 2013, one should not panic. You may be better off watching the end of the airline movie before putting your head in between your legs in preparation for a nosedive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Risk of “Double-Rip” on the Rise

Okay, you heard it here first. I’m officially anointing my first new 2013 economic term of the year: “Double-Rip!” No, the biggest risk of 2013 is not a “double-dip” (the risk of the economy falling back into recession), but instead, the larger risk is of a double-rip – a sustained expansion of GDP after multiple quarters of recovery. I know, this sounds like heresy, given we’ve had to listen to perma-bears like Nouriel Roubini, Peter Schiff, John Mauldin, Mohamed El-Erian, Bill Gross, et al shovel their consistently wrong pessimism for the last 14 quarters. However, those readers who have followed me for the last four years of this bull market know where I’ve stood relative to these unwavering doomsday-ers. Rather than endlessly rehash the erroneous gospel spewed by this cautious clan, you can decide for yourself how accurate they’ve been by reviewing the links below and named links above:

Roubini calling for double-dip in 2012

Roubini calling for double-dip in 2011

Roubini calling for double-dip in 2010

Roubini calling for double-dip in 2009

If we switch from past to present, Bill Gross has already dug himself into a deep hole just two weeks into the year by tweeting equity markets will return less than 5% in 2013. Hmmm, I wonder if he’d predict the same thing now that the market is up about +4.5% during the first 18 days of the year?

Why Double-Rip Over Double-Dip?

How can stocks rip if economic growth is so sluggish? If forced to equate our private sector to a car, opinions would vary widely. We could probably agree the U.S. economy is no Ferrari. Faster growing countries like China, which recently reported 4th quarter growth of +7.9% (up from +7.4% in 3rd quarter), have lapped us complacent, right-lane driving Americans in recent years. But speed alone should not be investors’ only key objective. If speed was the number one priority, the only places investors would be placing their money would be in countries like Rwanda, Turkmenistan, and Libya (see Business Insider article). However, freedom, rule of law, and entrepreneurial spirit are other important investment factors to be considered. The U.S. market is more like a Toyota Camry – not very flashy, but it will reliably get you from point A to point B in an efficient and safe manner.

Beyond lackluster economic growth, corporate profit growth has slowed remarkably. In fact, with about 10% of the S&P 500 index companies reporting 4th quarter earnings thus far, earnings growth is expected to rise a measly 2.5% from a year ago (from a previous estimate of 3.0% growth). With this being the case, how can stock prices go up? Shrewd investors understand the stock market is a discounting mechanism of future fundamentals, and therefore stocks will move in advance of future growth. It makes sense that before a turn in the economy, the brakes will often be activated before accelerating into another fast moving straight-away.

In addition, valuation acts like shock absorbers. With generational low interest rates and a below-average forward 12-month P/E (Price-Earnings) ratio of 13x’s, this stock market car can absorb a significant amount of fundamental challenges. The oft quoted message that “In the short run, the market is a voting machine but in the long run it is a weighing machine,” from value icon Benjamin Graham holds as true today as it did a century ago. The recent market advance may be attributed to the voters, but long-term movements are ultimately tied to the sustainable scales of sales, earnings, and cash flows.

If that’s the case, how can someone be optimistic in the face of the slowing growth challenges of this year? What 2013 will not have is the drag of election uncertainty, the fiscal cliff, Superstorm Sandy, and an end-of-the-world Mayan calendar concern. This is setting the stage for improved fundamentals as we progress deeper into the year. Certainly there will be other puts and takes, but the absence of these factors should provide some wind under the economy’s sails.

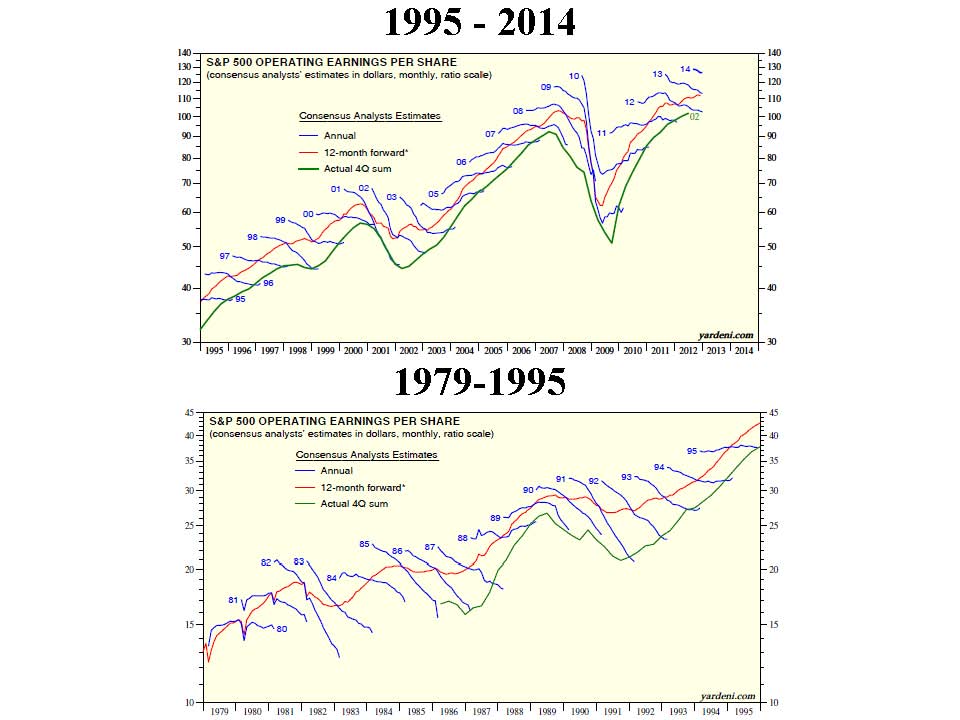

What’s more, history shows us that indeed stock prices can go up quite dramatically (more than +325% during the 1990s) when consensus earnings forecasts continually get trimmed. We have seen this same dynamic since mid-2012 – earnings forecasts have come down and stock prices have gone up. Strategist Ed Yardeni captures this point beautifully in a recent post on his Dr. Ed’s Blog (see charts below).

CLICK TO ENLARGE – Source: Dr. Ed’s Blog

What Will Make Me Bearish?

Am I a perma-bull, incessantly wearing rose-colored glasses that I refuse to take off? I’ll let you come to your own conclusion. When I see a combination of the following, I will become bearish:

#1. I see the trillions of dollars parked in near-0% cash start coming outside to play.

#2. See Pimco’s Bill Gross and Mohammed El-Erian on CNBC fewer than 10 times per week.

#3. See money flow stop flooding into sub-3% bonds (Scott Grannis) and actually reverse.

#4. Observe a sustained reversal in hemorrhaging of equity investments (Scott Grannis).

#5. Yield curve flattens dramatically or inverts.

#6. Nouriel and his bear buds become bullish and call for a “triple-rip” turn in the equity markets.

#7. Smarter, more-experienced investors than I, á la Warren Buffett, become more cautious. I arrogantly believe that will occur in conjunction with some of the previously listed items.

Despite my firm beliefs, it is evident the bears won’t go down without a fight. If you are getting tired of drinking the double-dip Kool-Aid, then perhaps it’s time to expand your bullish horizons. If not, just wait 12 months after a market rally, and buy yourself a fresh copy of the Merriam-Webster dictionary. There you can locate and learn about a new definition…double-rip!

Read Also: Double-Dip Guesses are “Probably Wrong”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in Fiat, Toyota, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Plumbers & Cops: Can the Debt Ceiling be Fixed?

The ceiling is leaking, but it’s unclear whether it will be repaired? Rather than fix the seeping fiscal problem, Democrats and Republicans have stared at the leaky ceiling and periodically applied debt ceiling patches every year or two by raising the limit. Nanosecond debt ceiling coverage has reached a nauseating level, but this issue has been escalating for many months. Last fall, politicians feared their long-term disregard of fiscally responsible policies could lead to a massive collapse in the financial ceiling protecting us, so the President called in the bipartisan plumbers of Alan Simpson & Erskine Bowles to fix the leak. The commission swiftly identified the problems and came up with a deep, thoughtful plan of action. Unfortunately, their recommendations were abruptly dismissed and Washington fell back into neglect mode, choosing instead to bicker like immature teenagers. The result: poisonous name calling and finger pointing that has placed Washington politicians one notch above Cuba’s Fidel Castro, Venezuela’s Hugo Chavez, and Iran’s Mahmoud Ahmadinejad on the list of the world’s most hated leaders. Strategist Ed Yardeni captured the disappointment of American voters when he mockingly states, “The clowns in Washington are making people cry rather than laugh.”

Although despair is in the air and the outlook is dour, our government can redeem itself with the simple passage of a debt ceiling increase, coupled with credible spending reduction legislation (and possibly “revenue enhancers” – you gotta love the tax euphimism).

The Elephant in the Room

Our country’s spending problems is nothing new, but the 2008-2009 financial crisis merely amplified and highlighted the severity of the problem. The evidence is indisputable – we are spending beyond our means:

Source: scottgrannis.blogspot.com

If the federal spending to GDP chart is not convincing enough, then review the following graph:

- Source: blog.yardeni.com – A graph a first grader could understand.

You don’t need to be a brain surgeon or rocket scientist to realize government expenditures are massively outpacing revenues (tax receipts). Expenditures need to be dramatically reduced, revenues increased, and/or a combination thereof. Applying for a new credit card with a limit to spend more isn’t going to work anymore – the lenders reviewing those upcoming credit applications will straightforwardly deny the applications or laugh at us as they gouge us with prohibitively high borrowing costs. The end result will be the evaporation of entitlement programs as we know them today (including Medicare and Social Security). For reference of exploding borrowing costs, please see Greek interest rate chart below. The mathematical equation for the Greek financial crisis (and potentially the U.S.) is amazingly straightforward…Loony Spending + Looney Politicians = Loony Interest Rates.

Source: Bloomberg.com via Wikipedia.com

To illustrate my point further, imagine the government owning a home with a mortgage payment tied to a 2.5% interest rate (a tremendously low, average borrowing cost for the U.S. today). Now visualize the U.S. going bankrupt, which would then force foreign and domestic lenders to double or triple the rates charged on the mortgage payment (in order to compensate the lenders for heightened U.S. default risk). Global investors, including the Chinese, are pointing a gun at our head, and if a political blind eye on spending continues, our foreign brethren who have provided us with extremely generous low priced loans will not be bashful about pulling the high borrowing cost trigger. The ballooning mortgage payments resulting from a default would then break an already unsustainably crippling budget, and the government would therefore be placed in a position of painfully slashing spending. Too extreme a shift towards austerity could spin a presently wobbling economy into chaos. That’s precisely the situation we face under a no-action Congressional default (i.e., no fix by August 2nd or shortly thereafter). To date, the Chinese have collected their payments from us with a nervous smile, but if the U.S. can’t make some fiscally responsible choices, our Asian Pacific pals will be back soon with a baseball bat to collect.

The Cops to the Rescue

Any parent knows disciplining teenagers doesn’t always work out as planned. With fiscally irresponsible spending habits and debt load piling up to the ceiling, politicians are stealing the prospects of a brighter future from upcoming generations. The good news is that if the politicians do not listen to the parental voter cries for fiscal sanity, the capital market cops will enforce justice for the criminal negligence and financial thievery going on in Washington. Ed Yardeni calls these capital market enforcers the “bond vigilantes.” If you want proof of lackadaisical and stubborn politicians responding expeditiously to capital market cops, please hearken back to September 2008 when Congress caved into the $700 billion TARP legislation, right after the Dow Jones Industrial average plummeted 777 points in a single day.

Who exactly are these cops? These cops come in the shape of hedge funds, sovereign wealth funds, pension funds, endowments, mutual funds, and other institutional investors that shift their dollars to the geographies where their money is treated best. If there is a perceived, heightened risk of the United States defaulting on promised debt payments, then global investors will simply take their dollar-denominated investments, sell them, and then convert them into currencies/investments of more conscientious countries like Australia or Switzerland.

Assisting the capital market cops in disciplining the unruly teenagers are the credit rating agencies. S&P (Standard and Poor’s) and Moody’s (MCO) have been watching the slow-motion train wreck develop and they are threatening to downgrade the U.S.’ AAA credit rating. Republicans and Democrats may not speak the same language, but the common word in both of their vocabularies is “reelection,” which at some point will effect a reaction due to voter and investor anxiety.

Nobody wants to see our nation’s pipes burst from excessive debt and spending, and if the political plumbers can repair the very obvious and fixable fiscal problems, we can move on to more important challenges. It’s best we fix our problems by ourselves…before the cops arrive and arrest the culprits for gross negligence.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MCO, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}