Posts tagged ‘economic growth’

Green Lights Everywhere… But Is It Time to Tap the Brakes?

The economic and market fundamentals appear to be flashing green lights everywhere. Growth is strong, inflation has cooled, and financial conditions have eased. Yet even with clear skies and open roads, experienced drivers know conditions can change quickly. It may not be time to slam on the brakes—but it could be time to keep a foot hovering nearby.

After the Federal Reserve aggressively applied the brakes in 2022 with seven rate hikes—taking the federal funds rate from 0.25% to 4.50%—the stock market declined nearly 19%. Since rates peaked at 5.50% in 2023, the Fed has cut rates six times, lowering them by a cumulative 1.75% to approximately 3.75%. Those cuts have helped pave the way for a smoother ride, providing a meaningful tailwind to equity markets.

That said, the most recent quarter-point cut produced mixed results. Last month, the Dow Jones Industrial Average rose +0.7%, the S&P 500 was essentially flat at –0.1%, and the NASDAQ lagged with a –0.5% decline.

Navigating the Winning Streak

We have encountered a few economic speed bumps along the way—tariffs and geopolitical events earlier in 2025, for example—but once investors realized those tariffs were more bark than bite (as I discussed previously in Tariff Sheriff), stocks resumed their impressive run. The market has now delivered three consecutive years of strong returns: 2023 (+24%), 2024 (+23%), and 2025 (+16%).

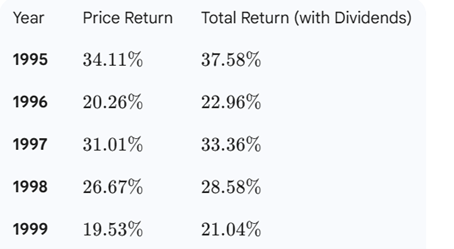

With these strong gains, today’s environment can feel like cruising on a national highway—clear roads, sunny skies, cruise control engaged, and little traffic in sight. The momentum could continue. Three strong years in a row do not rule out a fourth or fifth. In fact, the late 1990s offer a powerful reminder: from 1995 through 2000, the stock market averaged approximately 29% annual returns through the March 2000 peak (see table below). However, once the technology bubble burst, it took more than 13 years for the market to reclaim new year-end highs.

Source: Gemini

After more than three decades of investing, one lesson remains clear: trees can grow for years—but they do not grow to the sky forever. Bull markets often last longer than expected, but they eventually end.

Why the Forecast Looks Rosy

Several factors are supporting today’s strong market backdrop:

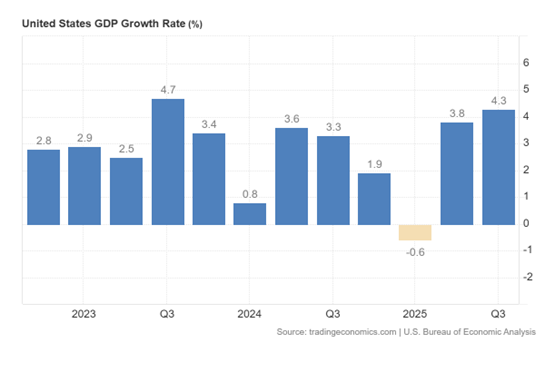

- Strong Economic Growth: Third-quarter GDP growth of 4.3% marked the fastest expansion in two years (see chart below)

Source: Trading Economics

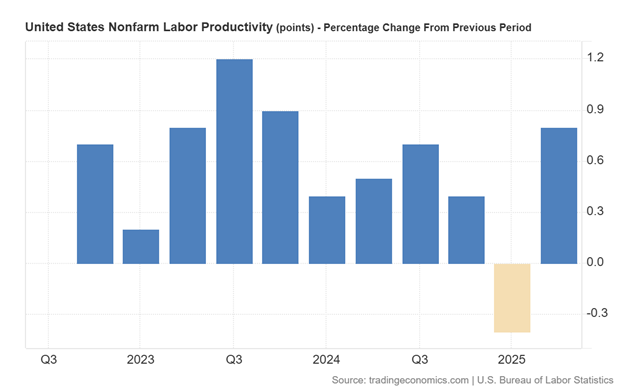

- AI-Driven Productivity: GDP growth has remained robust even as unemployment has risen from 4.0% earlier in the year to approximately 4.6% today. Growth outpacing employment is the definition of productivity, and the proliferation of artificial intelligence is accelerating this trend. Large companies such as Amazon.com (AMZN), Microsoft (MSFT), Alphabet-Google (GOOGL), and Meta Platforms (META) have reduced headcount significantly by tens of thousands in recent years while revenues and profits continue to surge (see also Mag 7 Takes Cash to the Bank).

Source: Trading Economics

- Taming Inflation: Crude oil prices have fallen roughly 20% over the last year, and Owner’s Equivalent Rent (which makes up about one-third of CPI inflation) has been steadily declining—both positive signals for inflation pressures ahead (see chart below).

Source: Calafia Beach Pundit

- Lapping Tariffs: Tariffs represented a one-time price increase. As we move into 2026, their inflationary impact should diminish as those increases roll off.

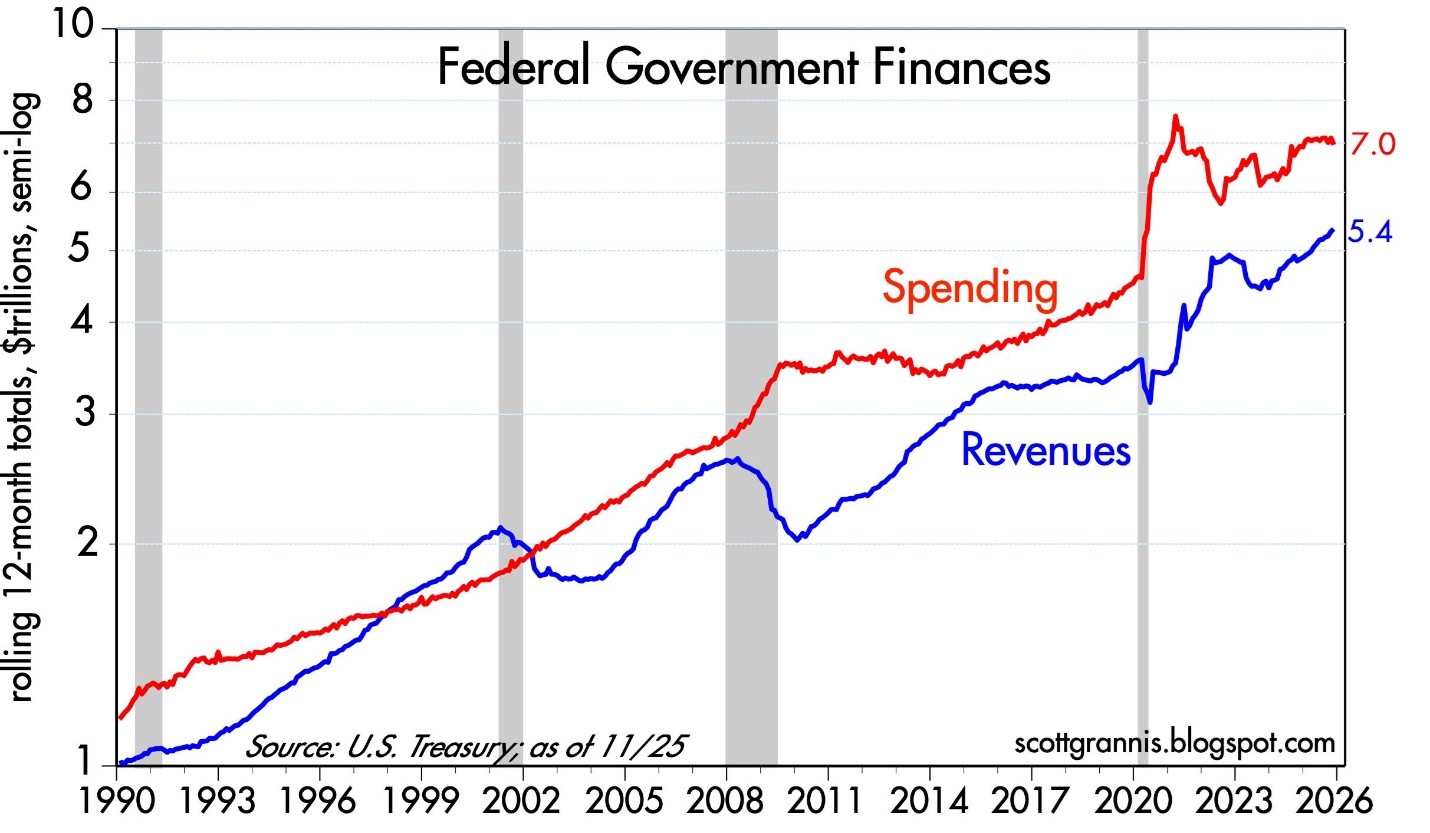

- Narrowing Budget Deficit: While debt and deficits remain headline risks, federal spending has been flat over the past year while revenues have increased roughly 10%, according to Scott Grannis (see chart below).

Source: Calafia Beach Pundit

- Tax Cuts & Higher Refunds Ahead: Many provisions of the One Big Beautiful Bill (OBBB) will be felt more fully in 2026, including 100% bonus depreciation for businesses, higher SALT deduction caps, increased standard deductions, no tax on tips or overtime, and a higher Child Tax Credit (CTC). Collectively, these could result in refunds up to $1,000 higher per individual.

Together, these factors could support continued market strength into 2026. But weather, road conditions, and markets can change quickly.

Reasons to Keep Your Foot Near the Brake Pedal

While the road looks smooth, several caution signs deserve attention:

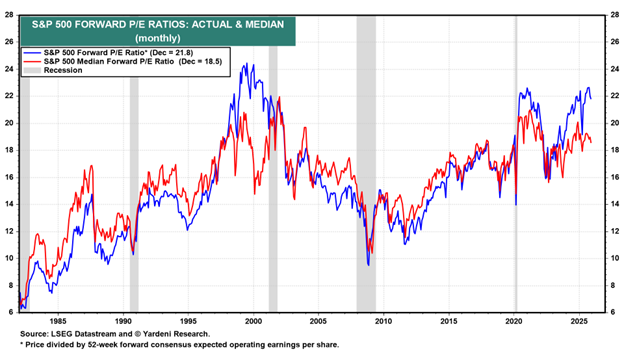

- Elevated Valuations: Forward price-to-earnings ratios (P/E) are at their highest levels since the late 1990s, outside of the brief post-COVID period. (see chart below).

Source: Yardeni Research

- Animal Spirits Are Back: Speculation has expanded well beyond traditional markets. Prediction platforms such as Kalshi, Polymarket, FanDuel, DraftKings, Robinhood, Coinbase, and others now allow bets on everything from political outcomes to economic data—further evidence of speculative behavior.

- Gold and Silver Speculation: Despite a relatively stable U.S. dollar over the past six months, gold rose +64% and silver catapulted +145% in 2025—moves difficult to justify by fundamentals alone (see chart below).

Source: MarketSurge

- Investor Complacency: The Volatility Index (VIX), often called the “fear gauge,” currently hovers near 15, well below its long-term average of 20. Historically, true fear doesn’t surface until readings exceed 25.

- Market Concentration: The “Magnificent 7” stocks represent roughly 1% of the companies in the S&P 500 but account for about 37% of the index’s weighting (see Mag 7 Takes Cash to the Bank)—a concentration reminiscent of the late 1990s. When leadership narrows, downturns can be sharper.

The Sidoxia View

At Sidoxia Capital Management, we have implemented all-weather, time-tested strategies through decades of both bull and bear markets. We believe diversification and disciplined risk management are essential—not fruitless prediction attempts. Rather than attempting to time short-term market moves, we focus on adapting portfolios to changing conditions and navigating inevitable financial potholes.

We don’t always get it right, but over the long run, this approach has allowed us to earn and retain the trust, loyalty, and confidence of our clients.

After three years of strong performance, it’s easy to assume clear roads and blue skies will continue indefinitely. But history teaches us that the most dangerous moments often occur when confidence is highest. This is not a call to abandon the journey—only a reminder to stay alert. When markets accelerate this quickly, discipline, diversification, and risk management matter more than ever.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (Jan. 2, 2026). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in MSFT, GOOGL, AMZN, META, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in ORCL or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

End of the World or Status Quo?

If you were the chief executive of a newspaper, television, or magazine company, what headline stories would you run to generate the most viewers and readers? Which subjects will you choose to make me impulsively grab a magazine in the grocery line, keep me glued to the television news, or suck me in to click-bait advertisements on the web? For example, what topics below would you select to grab the most attention?

· Hurricane or Sunshine?

· High Speed Car Chase or Cat Saved from Tree?

· Bloody Murder or Baby’s Birthday?

· Messy Divorce or Wedding Celebration?

· Impeachment or Bipartisan Legislation

· End of the World or Status Quo?

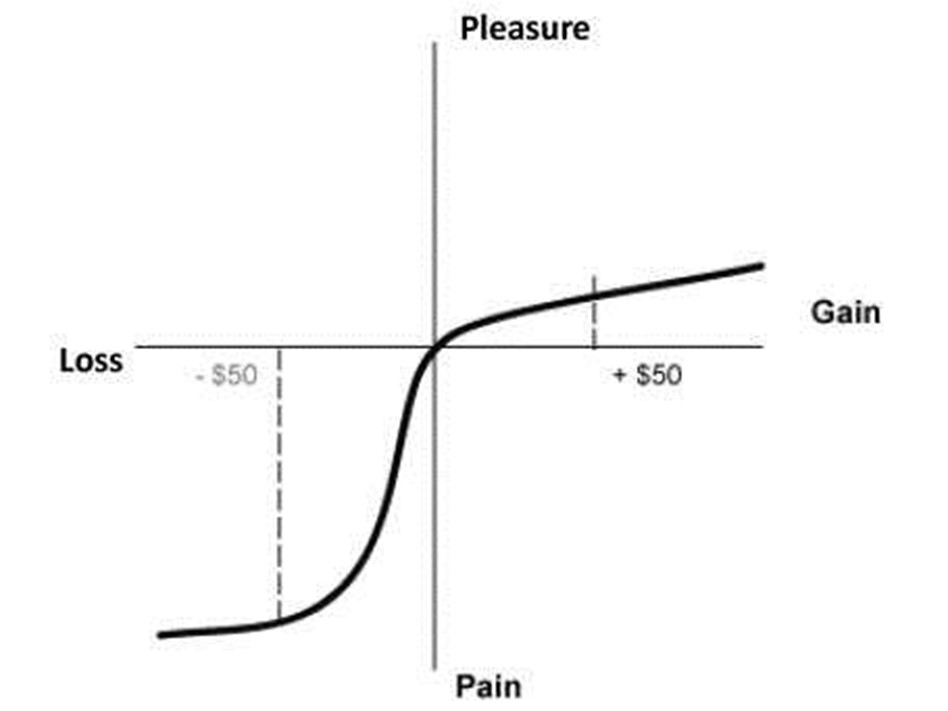

If you selected the first subject in each pair above, you would likely gain much more initial interest. In choosing a winning topic, the saying goes, “what bleeds, leads.” In other words, scary or controversial stories always grab more attention than feel-good or status quo narratives. And that is why the vast majority of media outlets are drawn to negativity, just as mosquitos are attracted to bug zappers. This phenomenon can be explained in part with the help of Nobel Prize winner Daniel Kahneman and his partner Amos Tversky, who conducted research showing the pain from losses is more than twice as painful as are the pleasures experienced from gains (see chart below).

The significant volatility seen in the stock market recently from the Russian war/invasion of Ukraine is further evidence of how this fear dynamic can create short-term panics.

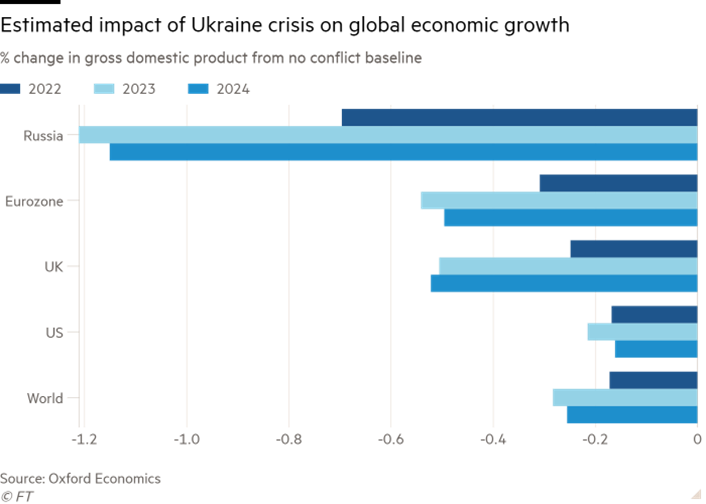

Although the stock market as measured by the S&P 500 index has gone gangbusters over the last three years, almost doubling in value (2019: +29%, 2020: +16%, 2021: +27%), the S&P 500 has hit an air pocket during the first couple months of 2022 (-8%), including down -3% in February. The year started with turbulence as investors became fearful of a Federal Reserve that is entering the beginning stages of interest rate hikes while cutting stimulative bond purchases. And then last month, the Russian-Ukrainian incursion made investors even more skittish. Like always, these geopolitical events tend to be short-lived once investors realize the impact turns out to be less meaningful than initially feared. As you can see below, the worst economic impact is forecasted to be felt by Russia (consensus on 2/24/22 of approximately a -1.0% hit to economic growth), more than twice as bad as the -0.2% to -0.4% knock to growth for the U.S., Europe, and the world (see chart below). The Russian hit will likely be worse after accelerated sanctions.

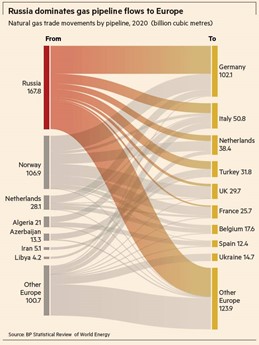

As it relates to Ukraine, many Americans don’t even know where the country is located on a map. Ukraine accounts for about only 0.14% of total global GDP (i.e., a rounding error and less than 1% of total global economic activity). Russia, although larger than Ukraine, is still a relative small-fry and represents only about 3% of total global economic activity. If you live in Europe during the winter, you might be a little more concerned about Vladimir Putin’s recent activities because a lot of Europe’s energy (natural gas) is supplied by Russia through Ukraine. For example, Germany receives about half of its natural gas from Russia (see chart below).

Russia, on the other hand, is larger than Ukraine, but the red country is still a relative small-fry representing only about 3% of total global economic activity. When it comes to energy production however, Russia is more than a rounding error because the country accounts for about 11% of global energy production (#3 country globally behind the United States and Saudi Arabia). By taking all these factors into account, we can confidently state that Russia and Ukraine have a very low probability of solely pulling the global economy into recession.

If history repeats itself, this conflict will turn out to be another garden variety decline in the stock market and an opportunity to buy at a discount. It’s virtually impossible to predict a short-term bottom in stock prices has been reached, but over the long-run, stock investors have been handsomely rewarded for not panicking and staying invested (see chart below).

At the end of the day, the daily headlines will continually attempt to sell the negative story that the world is coming to an end. If you have the fortitude and discipline to ignore the irrelevant noise, the status quo of normal volatility can create more exciting opportunities and better returns for long-term investors.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2022). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Recovering from the Coma

The patient, the U.S. economy, is sick and remains in a coma. Although the patient was never healthier six weeks ago, now the economy has fallen victim to a worldwide pandemic that has knocked the global economy on its back. On the surface, the physical impact of coronavirus on the health of the 330 million Americans seems relatively modest statistically (4,394 deaths vs. 45,000 estimated common flu deaths this season). However, in order to kill this insidious novel coronavirus, which has spread like wildfire across 200 countries, governments have been forced to induce the economy into a coma, by closing schools, halting sporting events, creating social distancing guidelines, instituting quarantines/lockdowns, and by shutting down large non-essential swaths of the economy (e.g., restaurants, retail, airlines, cruises, hotels, etc.). We have faced and survived other epidemics like SARS (2003-04), H1N1 (2009-10), MERS (2012), and Ebola (2014-16), but the pace of COVID-19 spreading has been extraordinarily rapid and has created dramatic resource drains on healthcare systems around the world (including New York with approximately 75,000 cases alone). The need for test kits, personal protective equipment, and ventilators, among other demands has hit the U.S. caregiving system especially hard.

Given the unique characteristics of this sweeping virus, U.S. investors were not immune from the economic impact. The swift unprecedented downdraft from all-time record highs has not been seen since the October 1987 crash. And although the major indexes experienced an illness this month (Dow Jones Industrial Average -13.7%; S&P 500 -12.5%; NASDAQ -10.1%), the nausea was limited in large part thanks to trillions of dollars in unparalleled government intervention announced in the form of monetary and fiscal stimulus.

Healing the Patient

While the proliferation of the viral outbreak has been painful in many ways from a human and financial perspective, the beneficial impact of the medicine provided to the economic patient by the Federal Reserve and federal government through the Coronavirus Aid, Relief, and Economic Security (CARES) act cannot be overstated. The measures taken will provide a temporary safety net for not only millions of businesses, but also millions of workers and investors. Although last month many investors felt like vomiting when they looked at their investment account balances, gratefully the period ended on an upbeat note with the Dow bouncing +20% from last week’s lows.

Fed Financial Fixes

Here is a partial summary of the extensive multi-trillion dollar emergency measures taken by the Federal Reserve to keep the financial markets and economy afloat:

- Cut interest rates on the benchmark Federal Funds target to 0% – 0.25% from 1% – 1.25%.

- Make $1 trillion available in 14-day loans it is offering every week.

- Make $1 trillion of overnight loans a day available.

- Purchase an unlimited amount of Treasury securities after initially committing to $500 billion.

- Purchase an unlimited amount of mortgage-backed securities after initially committing to at least $200 billion.

- Provide $300 billion of financing to employers, consumers, and businesses. The Department of the Treasury will provide $30 billion in equity to this financing via the Exchange Stabilization Fund (ESF).

- Establish two lending facilities to support credit to large employers – the Primary Market Corporate Credit Facility (PMCCF) for new bond and loan issuance and the Secondary Market Corporate Credit Facility (SMCCF) to provide liquidity for outstanding corporate bonds.

- Create the Term Asset-Backed Securities Loan Facility (TALF), to support the flow of credit to consumers and businesses, including student loans, auto loans, credit card loans, loans guaranteed by the Small Business Administration (SBA).

- Expand the Money Market Mutual Fund Liquidity Facility (MMLF) and the Commercial Paper Funding Facility (CPFF) to include a wider range of securities.

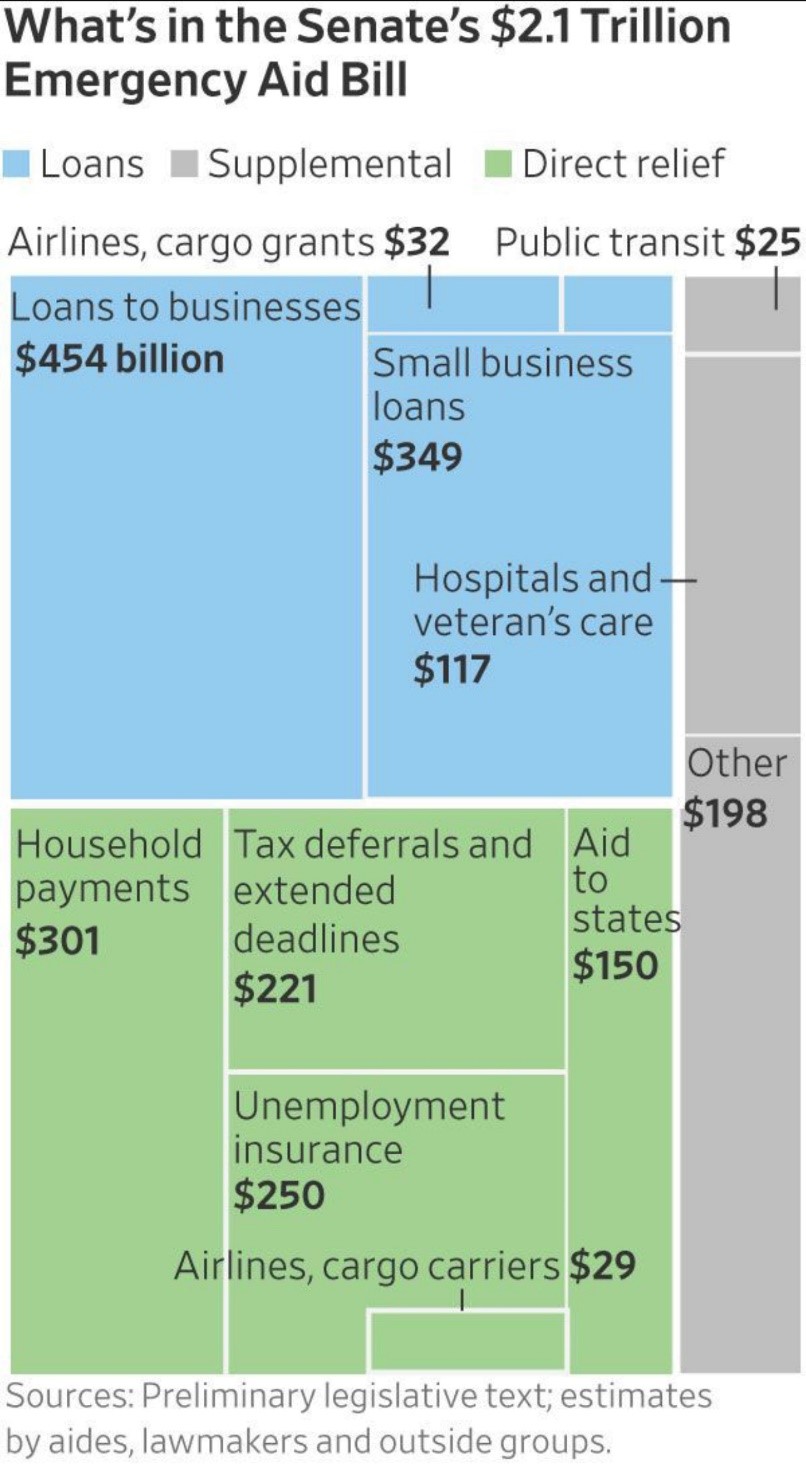

Corona CARE to Country

Here is a limited summary of the sprawling $2.1 trillion bipartisan stimulus legislation that was recently passed by Congress (see summary and table below):

- Direct Payments: Americans who pay taxes will receive a one-time direct deposit of up to $1,200, and married couples will receive $2,400, plus an additional $500 per child. The payments will be available for incomes up to $75,000 for individuals and $150,000 for married couples, and phase out completely at $99,000 and $198,000, respectively.

- Unemployment: The program provides $250 billion for an extended unemployment insurance program and expands eligibility and offers workers an additional $600 per week for four months, on top of what state programs pay. It also extends UI benefits through Dec. 31 for eligible workers. The deal also applies to the self-employed, independent contractors and gig economy workers.

- Payroll Taxes: The measure allows employers to delay the payment of their portion of 2020 payroll taxes until 2021 and 2022.

- Use of Retirement Funds: The bill waives the 10% early withdrawal penalty for distributions up to $100,000 for coronavirus-related purposes, retroactive to Jan. 1. Withdrawals are still taxed, but taxes are spread over three years, or the taxpayer has the three-year period to roll it back in.

- Small Business Relief: $350 billion is being earmarked to preventing layoffs and business closures while workers need to stay home during the outbreak. Companies with 500 employees or fewer that maintain their payroll during coronavirus can receive up to 8 weeks of financial assistance. If employers maintain payroll, the portion of the loans used for covered payroll costs, interest on mortgage obligations, rent, and utilities would be forgiven.

- Large Corporations: $500 billion will be allotted to provide loans, loan guarantees, and other investments, these will be overseen by a Treasury Department inspector general. These loans will not exceed five years and cannot be forgiven. Airlines will receive $50 billion (of the $500 billion) for passenger air carriers, and $8 billion for cargo air carriers.

- Hospitals and Health Care: The deal provides over $140 billion in appropriations to support the U.S. health system, $100 billion of which will be injected directly into hospitals. The rest will be dedicated to providing personal and protective equipment for health care workers, testing supplies, increased workforce and training, accelerated Medicare payments, and supporting the CDC, among other health investments.

- Coronavirus Testing: All testing and potential vaccines for COVID-19 will be covered at no cost to patients.

- States and Local Governments: State, local and tribal governments will receive $150 billion. $30 billion is set aside for states, and educational institutions. $45 billion is for disaster relief, and $25 billion for transit programs.

- Agriculture: The deal would increase the amount the Agriculture Department can spend on its bailout program from $30 billion to $50 billion.

Source: The Wall Street Journal

Patient Requires Patience

As we enter the new 30-day extension of social distancing guidelines until April 30th, there is good news and bad news for the patient as the economy recovers from its self-induced coma. On the good news front, their appears to be a light at the end of the tunnel with respect to the spread of the virus. Enough data has been collected from countries like China, S. Korea, Italy, and our own, such that statisticians appear to have a better handle on the trajectory of the virus.

More specifically, here are some positive developments:

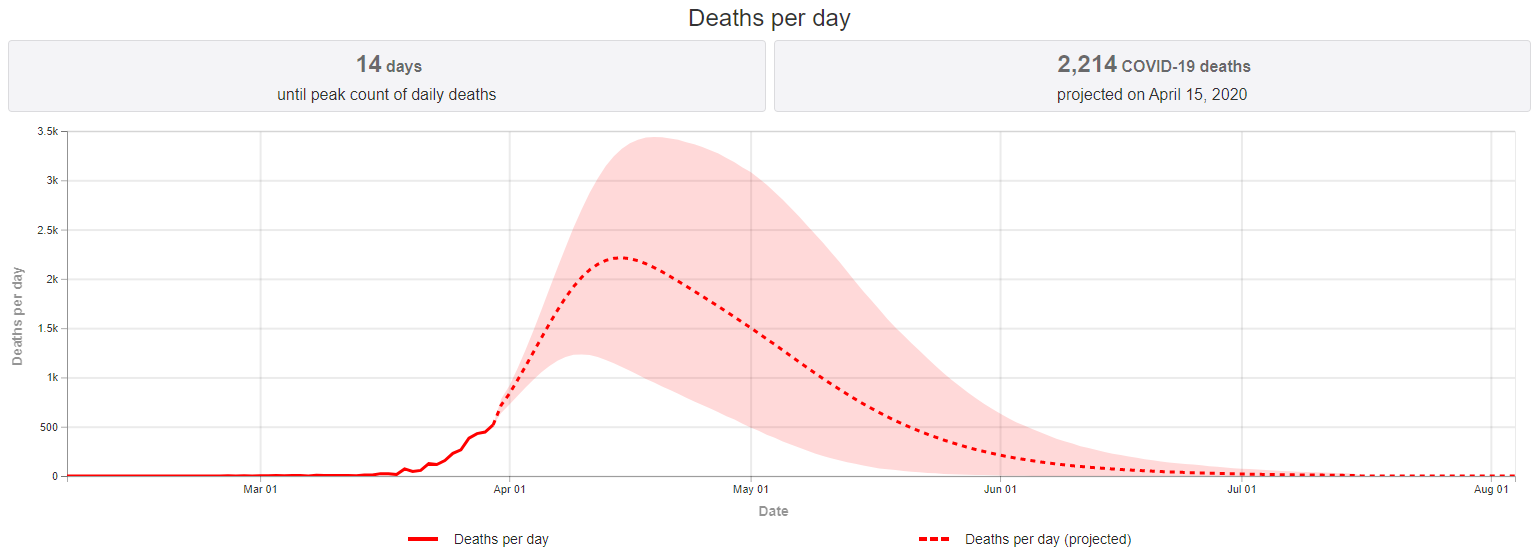

- Peak Seen on April 14th: According to the IMHE model that the White House is closely following, the number of COVID-19 deaths is projected to peak in two weeks.

Source: IHME

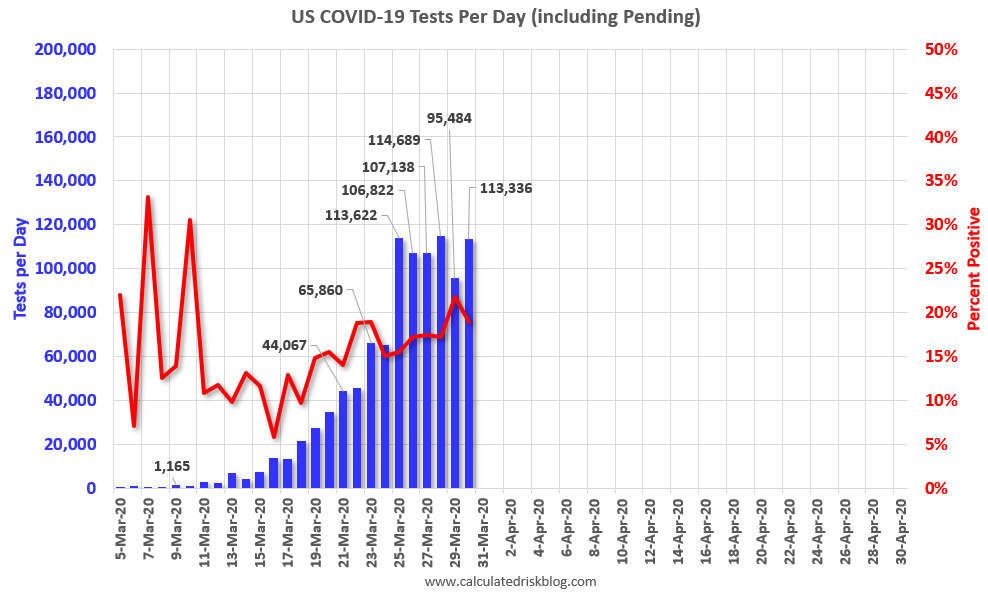

- Testing Ramping: The United States definitely got off to a slow start in the virus testing department, but as you can see from the chart below, COVID-19 tests are ramping significantly. Nevertheless, the number of tests still needs to increase dramatically until the percent of “positive” test results declines to a level of 5% or lower, based on data collected from South Korea. In another promising development, Abbott Laboratories (ABT) received emergency approval from the FDA for a rapid point-of-care test that produces results in just five minutes.

Source: Calculated Risk

- Closer to a COVID Cure: There are no Food and Drug Administration (FDA)-approved therapies or vaccines yet, but the FDA has granted emergency use authorization to anti-malarial drugs chloroquine phosphate and hydroxychloroquine sulfate to treat coronavirus patients. Patients are currently using these drugs in conjunction with the antibiotic azithromycin in hopes of achieving even better results. Remdesivir is a promising anti-viral treatment (also used in treating the Ebola virus) manufactured by Gilead Sciences Inc. (GILD), which is in Phase 3 clinical trial testing of the drug. If proven effective, broad distribution of remdesivir could be administered to COVID-19 patients in the not-too-distant future. Another company, Regeneron Pharmaceuticals (REGN), is working on clinical trials of its rheumatoid arthritis antibody drug Kevzara as a hopeful treatment. In addition, there are multiple companies, including Moderna Inc. (MRNA) and Johnson & Johnson (JNJ) that are making progress on coronavirus vaccines, that could have limited availability as soon as early-2021.

Darkest Before the Dawn

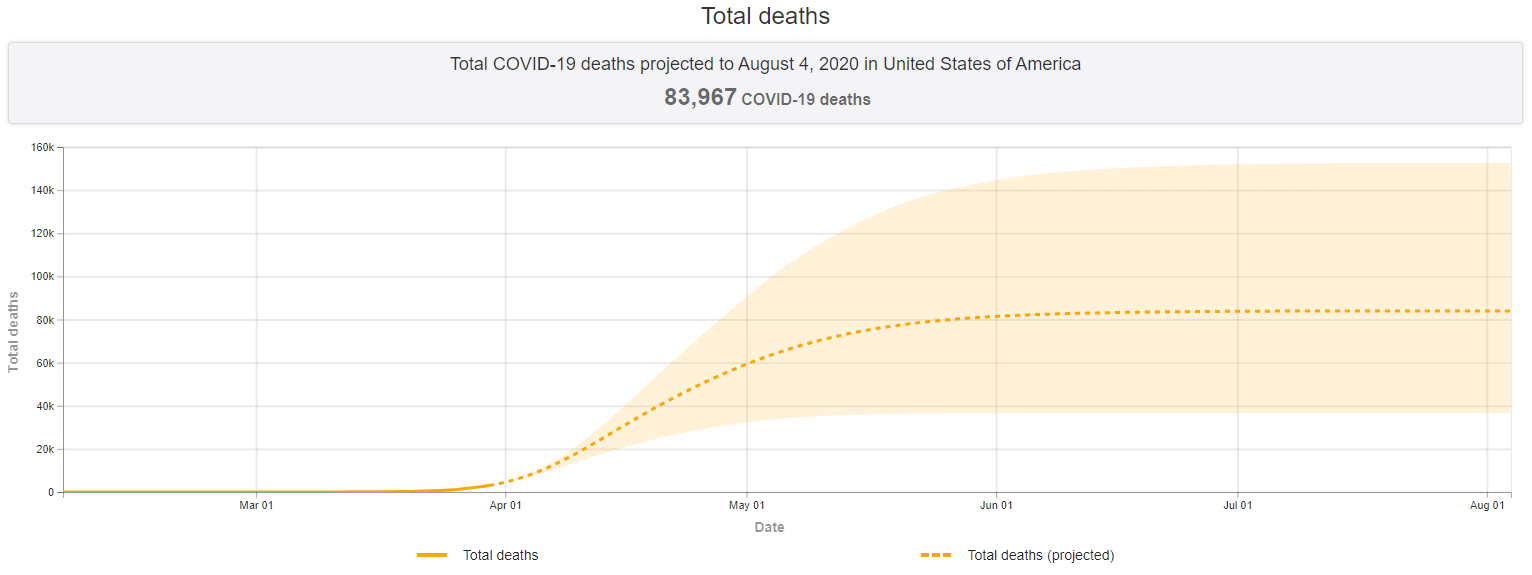

It is always darkest before the dawn, and the same principle applies to this coronavirus epidemic. Despite providing the patient’s medicine in the form of monetary and fiscal stimulus, time and patience is necessary for the prescription to take effect. As you can see from the chart below, the median total deaths projected is expected to rise to over 80,000 deaths by June 1st from roughly 4,000 today.

Source: IHME

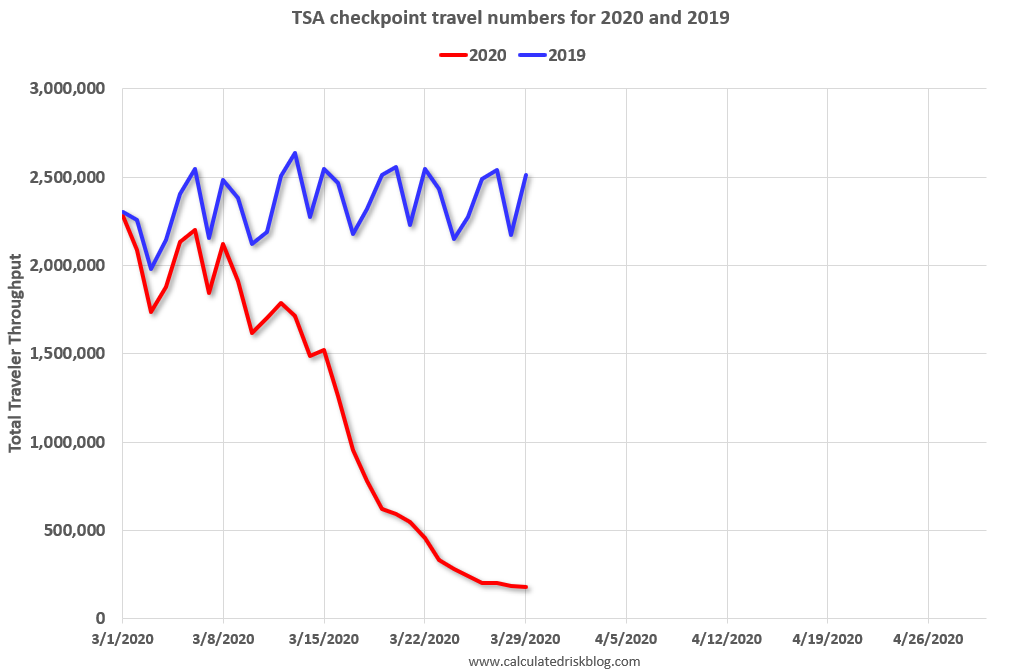

The physical toll will exceedingly become difficult over the next month, and the same can be said economically, especially for the hardest hit industries such as leisure, hospitality, and transportation. Just take a look at the -93% decline in airport travel versus a year ago (see chart below).

Source: Calculated Risk

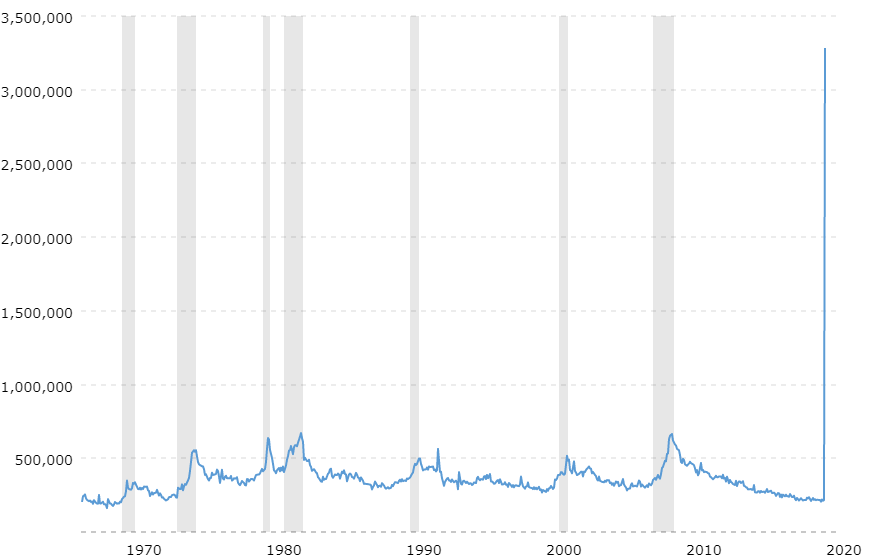

The closure of restaurants, retail stores, and hotels, coupled with a cratering of travel has resulted in a more than a 1,000% increase in Americans filing for unemployment payments (see chart below – gray shaded regions correspond to recessions), and the unemployment rate is expected to increase from a near record-low 3.5% unemployment to a staggering 10% – 30% unemployment rate.

Source: Macrotrends

The spread of the incredibly debilitating COVID-19 virus has placed the economic patient into a self-induced coma. The financial and physical pain felt by the epidemic will worsen in the coming weeks, but fortunately the monetary stimulus, fiscal emergency relief, and social distancing guidelines are pointing to a predictable recovery in the not-too-distant future. Financial markets have survived wars, assassinations, recessions, impeachments, banking crises, currency crises, housing collapses, and yes, even pandemics. Each and every time, we have emerged stronger than ever…and I’m confident we will achieve the same result once COVID-19 is defeated.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in GILD, MRNA, JNJ, and certain exchange traded funds (ETFS), but at the time of publishing had no direct position in ABT, REGN or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}