Posts tagged ‘ECB’

Greece: The Slow Motion, Multi-Year Train Wreck

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2015). Subscribe on the right side of the page for the complete text.

Watching Greece fall apart over the last five years has been like watching a slow motion train wreck. To many, this small country of 11 million people that borders the Mediterranean, Aegean, and Ionian Seas is known more for its Greek culture (including Zeus, Parthenon, Olympics) and its food (calamari, gyros, and Ouzo) than it is known for financial bailouts. Nevertheless, ever since the financial crisis of 2008-2009, observers have repeatedly predicted the debt-laden country will default on its €323 billion mountain of obligations (see chart below – approximately $350 billion in dollars) and subsequently exit the 19-member eurozone currency membership (a.k.a.,”Grexit”).

Source: MoneyMorning.com and CNN

Now that Greece has failed to repay less than 1% of its full €240 billion bailout obligation – the €1.5 billion payment due to the IMF (International Monetary Fund) by June 30th – the default train is coming closer to falling off the tracks. Whether Greece will ultimately crash itself out of the eurozone will be dependent on the outcome of this week’s surprise Greek referendum (general vote by citizens) mandated by Prime Minister Alexis Tsipras, the leader of Greece’s left-wing Syriza party. By voting “No” on further bailout austerity measures recommended by the European Union Commission, including deeper tax increases and pension cuts, the Greek people would effectively be choosing a Grexit over additional painful tax increases and deeper pension cuts.

Ouch!

And who can blame the Greeks for being a little grouchy? You might not be too happy either if you witnessed your country experience an economic decline of greater than 25% (see Greece Gross Domestic Product chart below); 25% overall unemployment (and 50% youth unemployment); government worker cuts of greater than 20%; and stifling taxes to boot. Sure, Greeks should still shoulder much of the blame. After all, they are the ones who piled on $100s of billions of debt and overspent on the pensions of a bloated public workforce, and ran unsustainable fiscal deficits.

Source: TradingEconomics.com

For any casual history observers, the current Greek financial crisis should come as no surprise, especially if you consider the Greeks have a longstanding habit of not paying their bills. Over the last two centuries or so, since the country became independent, the Greek government has spent about 90 years in default (almost 50% of the time). More specifically, the Greeks defaulted on external sovereign debt in 1826, 1843, 1860, 1894 and 1932.

The difference between now and past years can be explained by Greece now being a part of the European Union and the euro currency, which means the Greeks actually do have to pay their bills…if they want to remain a part of the common currency. During past defaults, the Greek central bank could easily devalue their currency (the drachma) and fire up the printing presses to create as much currency as needed to pay down debts. If the planned Greek referendum this week results in a “No” vote, there is a much higher probability that the Greek government will need to dust off those drachma printing presses.

“Perspective People”

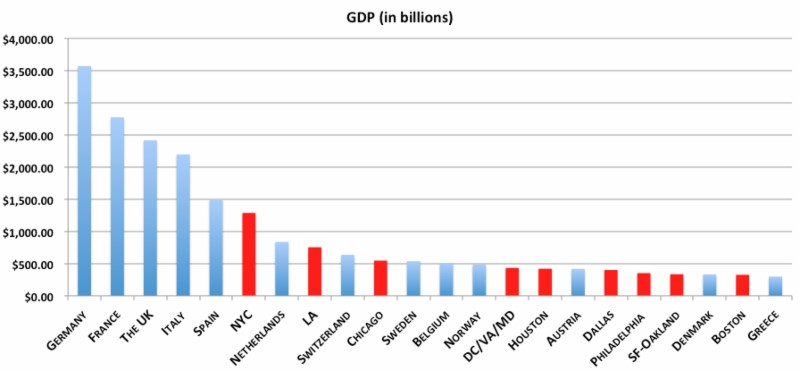

Protest, riots, defaults, changing governments, and new currencies make for entertaining television viewing, but these events probably don’t hold much significance as it relates to the long-term outlook of your investments and the financial markets. In the case of Greece, I believe it is safe to say the economic bark is much worse than the bite. For starters, Greece accounts for less than 2% of Europe’s overall economy, and about 0.3% of the global economy.

Since I live out on the West Coast, the chart below caught my fancy because it also places the current Greek situation into proper proportion. Take the city of L.A. (Los Angeles – red bar) for example…this single city alone accounts for almost 3x the size of Greece’s total economy (far right on chart – blue bar).

Give Me My Money!

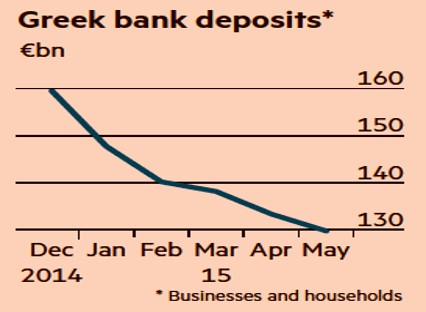

It hasn’t been a fun year for Greek banks. Depositors, who have been flocking to the banks, withdrew about $45 billion in cash from their accounts, over an eight month period (see chart below). Before the Greek government decided to mandatorily close the banks in recent days and implement capital controls limiting depositors to daily ATM withdrawals of only $66.

Source: The Financial Times

But once again, let’s put the situation into context. From an overall Greek banking sector perspective, the four largest Greek Banks (Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank) account for about 90% of all Greek banking assets. Combined, these banks currently have an equity market value of about $14 billion and assets on the balance sheets of $400 billion – these numbers are obviously in flux. For comparison purposes, Bank of America Corp. (BAC) alone has an equity market value of $179 billion and $2.1 trillion in assets.

Anxiety Remains High

Skeptical bears will occasionally acknowledge the miniscule-ness of Greece, but then quickly follow up with their conspiracy theory or domino effect hypothesis. In other words, the skeptics believe a contagion effect of an impending Grexit will ripple through larger economies, such as Italy and Spain, with crippling force. Thus far, as you can see from the chart below, Greece’s financial problems have been largely contained within its borders. In fact, weaker economies such as Spain, Portugal, Ireland, and Italy have fared much better – and actually improving in most cases. In recent days, 10-year yields on government bonds in countries like Portugal, Italy, and Spain have hovered around or below 3% – nowhere near the peak levels seen during 2008 – 2011.

Source: Business Insider

Other doubting Thomases compare Greece to situations like Lehman Brothers, Long Term Capital Management, and the subprime housing market, in which underestimated situations snowballed into much worse outcomes. As I explain in one of my newer articles (see Missing the Forest for the Trees), the difference between Greece and the other financial collapses is the duration of this situation. The Greek circumstance has been a 5-year long train wreck that has allowed everyone to prepare for a possible Grexit. Rather than agonize over every news headline, if you are committed to the practice of worrying, I would recommend you focus on an alternative disaster that cannot be found on the front page of all newspapers.

There is bound to be more volatility ahead for investors, and the referendum vote later this week could provide that volatility spark. Regardless of the news story du jour, any of your concerns should be occupied by other more important worrisome issues. So, unless you are an investor in a Greek bank or a gyro restaurant in Athens, you should focus your efforts on long-term financial goals and objectives. Ignoring the noisy news flow and constructing a diversified investment portfolio across a range of asset classes will allow you to avoid the harmful consequences of the slow motion, multi-year Greek train wreck.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and BAC, but at the time of publishing, SCM had no direct position in Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Chicken or Beef? Time for a Stock Diet?

The stock market has been gorging on gains over the last six years and the big question is are we ready for a crash diet? In other words, have we consumed too much, too fast? Since the lows of 2009 the S&P 500 index has more than tripled (or +209% without dividends).

In our daily food diets our proteins of choice are primarily chicken and beef. When it comes to finances, our investment choices are primarily stocks and bonds. There are many factors that can play into a meat-eaters purchase decision, including the all-important factor of price. When the price of beef spikes, guess what? Consumers rationally vote with their wallets and start substituting beef for relatively lower priced chicken options.

The same principle applies to stocks and bonds. And right now, the price of bonds in general have gone through the roof. In fact bond prices are so high, in Europe we are seeing more than $2 trillion in negative yielding sovereign bonds getting sucked up by investors.

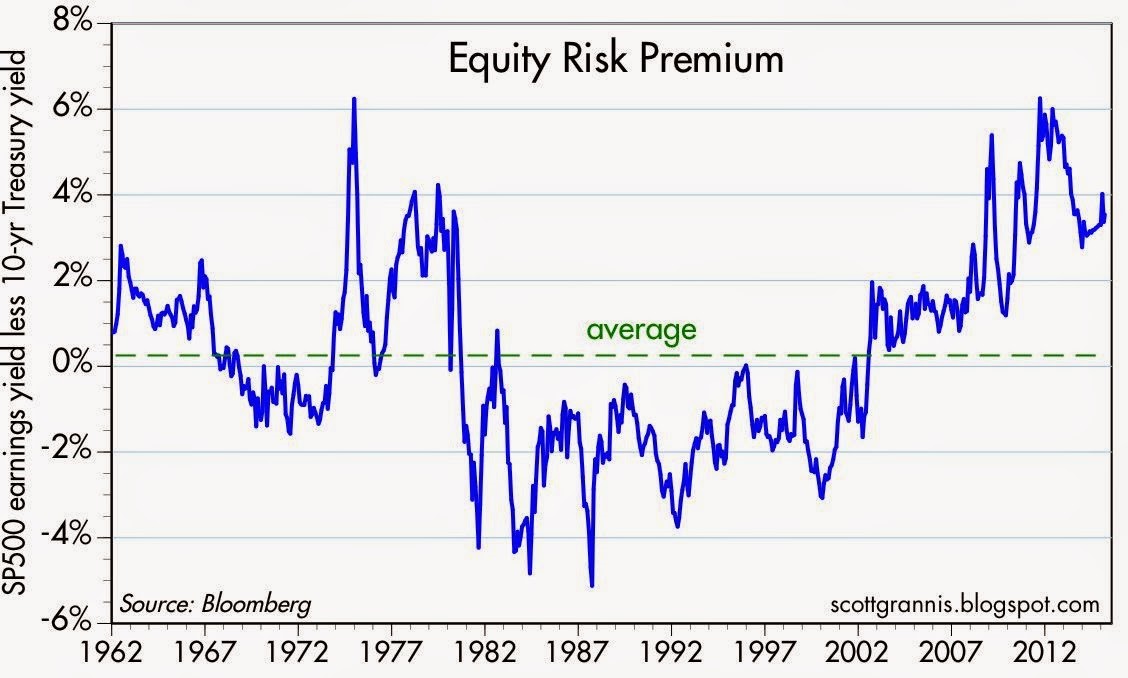

Another area where we see evidence of pricey bonds can be found in the value of current equity risk premiums. Scott Grannis of Calafia Beach Pundit posted a great 50-year history of this metric (chart below), which shows the premium paid to stockholders over bondholders is near the highest levels last seen during the Great Recession and the early 1980s. To clarify, the equity risk premium is defined as the roughly 5.5% yield currently earned on stocks (i.e., inverse of the approx. 18x P/E ratio) minus the 2.0% yield earned on 10-Year Treasury Notes.

Source: Scott Grannis

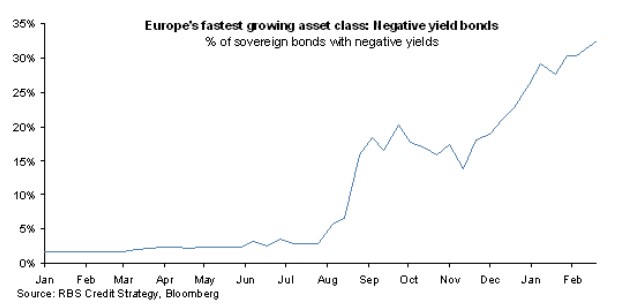

The equity risk premium even looks more favorable if you consider the negative interest rate European environment mentioned earlier. The 60 billion euros of monthly debt in ECB (European Central Bank) quantitative easing purchases has accelerated the percentage of negative yield bond issuance, as you can see from the chart below.

Source: FT Alphaville

Hibernating Bond Vigilantes

Dr. Ed Yardeni coined the famous phrase “bond vigilantes” to describe the group of hedge funds and institutional investors who act as the bond market sheriffs, ready to discipline any over leveraged debt-issuing entity by deliberately cratering prices via bond sales. For now, the bond vigilantes have in large part been hibernating. As long as the vigilantes remain asleep at the switch, stock investors will likely continue earning these outsized premiums.

How long will these fat equity premiums and gains stick around? A simple diet of sharp interest rate increases or P/E expansion would do the trick. An increase in the P/E ratio could come in one of two ways: 1) sustained stock price appreciation at a rate faster than earnings growth; or 2) a sharp earnings decline caused by a recessionary environment. On the bright side for the bulls, there are no imminent signs of interest rate spikes or recessions. If anything, dovish commentary coming from Fed Chairwoman Janet Yellen and the FOMC would indicate the economy remains in solid recovery mode. What’s more, a return to normalized monetary policy will likely involve a very gradual increase in interest rates – not a piercing rise as feared by many.

Regardless of whether it’s beef prices or bond prices spiking, rather than going on a crash diet, prudently allocating your money to the best relative value will serve your portfolio and stomach best over the long run.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

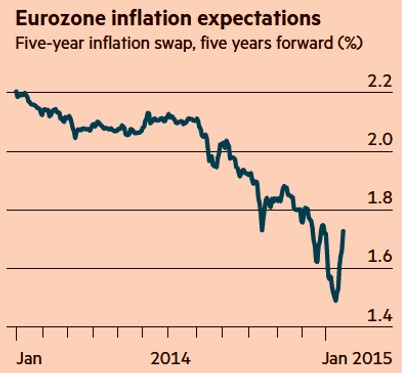

Draghi Provides Markets QE Beer Goggles

While the financial market party has been gaining momentum in the U.S., Europe has been busy attending an economic funeral. Mario Draghi, the European Central Bank President is trying to reverse the somber deflationary mood, and therefore has sent out $1.1 trillion euros worth of quantitative easing (QE) invitations to investors with the hope of getting the eurozone party started.

Draghi and the stubborn party-poopers sitting on the sidelines have continually been skeptical of the creative monetary punch-spiking policies initially implemented by U.S. Federal Reserve Chairman Ben Bernanke (and continued by his fellow dovish successor Janet Yellen). With the sluggish deflationary European pity party (see FT chart below) persisting for the last six years, investors are in dire need for a new tool to lighten up the dead party and Draghi has obliged with the solution…“QE beer goggles.” For those not familiar with the term “beer goggles,” these are the vision devices that people put on to make a party more enjoyable with the help of excessive consumption of beer, alcohol, or in this case, QE.

Source: The Financial Times

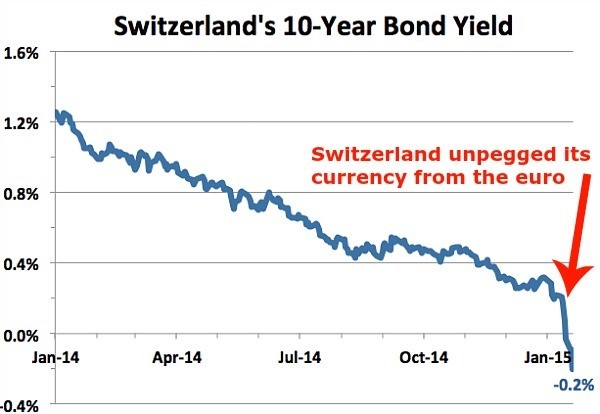

Although here in the U.S. “QE beer goggles” have been removed via QE expiration last year, nevertheless the party has endured for six consecutive years. Even an economy posting such figures as an 11-year high in GDP growth (+5.0%); declining unemployment (5.6% from a cycle peak of 10.0%); and stimulative effects from declining oil/commodity prices have not resulted in the cops coming to break up the party. It’s difficult for a U.S. investor to admit an accelerating economy; improving job additions; recovering housing market; with stronger consumer balance sheet would cause U.S. 10-Year Treasury Note yields to plummet from 3.04% at the beginning of 2014 to 1.82% today. But in reality, this is exactly what happened.

To confound views on traditional modern economics, we are seeing negative 10-year rates on Swiss Treasury Bonds (see chart below). In other words, investors are paying -1% to the Swiss government to park their money. A similar strategy could be replicated with $100 by simply burning a $1 bill and putting the remaining $99 under a mattress. Better yet, why not just pay me to hold your money, I will place your money under my guarded mattress and only charge you half price!

Does QE Work?

Debate will likely persist forever as it relates to the effectiveness of QE in the U.S. On the half glass empty side of the ledger, GDP growth has only averaged 2-3% during the recovery; the improvement in the jobs upturn is arguably the slowest since World War II; and real wages have declined significantly. On the half glass full side, however, the economy has improved substantially (e.g., GDP, unemployment, consumer balance sheets, housing, etc.), and stocks have more than doubled in value since the start of QE1 at the end of 2008. Is it possible that the series of QE policies added no value, or we could have had a stronger recovery without QE? Sure, anyone can make that case, but the fact remains, the QE training wheels have officially come off the economy and Armageddon has still yet to materialize.

I expect the same results from the implementation of QE in Europe. QE is by no means an elixir or panacea. I anticipate minimal direct and tangible economic benefits from Draghi’s $1+ trillion euro QE bazooka, however the psychological confidence building impacts and currency depreciating effects are likely to have a modest indirect value to the eurozone and global financial markets overall. The downside for these unsustainable ultra-low rates is potential excessive leverage from easy credit, asset bubbles, and long-term inflation. Certainly, there may be small pockets of these excesses, however the scars and regulations associated with the 2008-2009 financial crisis have delayed the “hangover” arrival of these risk possibilities on a broader basis. Therefore, until the party ends or the cops come to break up the fun, you may want to enjoy the gift provided by Mario Draghi to global investors…and strap on the “QE beer goggles.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including positions in certain exchange traded funds positions , but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

To Taper or Not to Taper…That is the Question?

It’s not Hamlet who is providing theatrical intrigue in the financial markets, but rather Federal Reserve Chairman Ben Bernanke. Watching Bernanke decide whether to taper or not to taper the $85 billion in monthly bond purchases (quantitative easing) is similar to viewing an emotionally volatile Shakespearean drama. The audience of investors is sitting at the edge of their seats waiting to see if incoming Fed Chief will be plagued with guilt like Lady Macbeth for her complicit money printing ways or will she score a heroic and triumphant victory for her hawkish stance on quantitative easing (QE). No need to purchase tickets at a theater box office near you, the performance is coming live to your living room as Yellen’s upcoming Senate confirmation hearings will be televised this upcoming week.

Bad News = Good News; Good News = Bad News?

In deciding whether to slowly kill QE, the Fed has been stricken with the usual stream of never-ending economic data (see current data from Barry Ritholtz). Most recently, investors have followed the script that says bad news is good news for stocks and good news is bad news. So-called pundits, strategists, and economists generally believe sluggish economic data will lead the Fed to further romance QE for a longer period, while robust data will force a poisonous death to QE via tapering.

Good News

Despite the recent, tragically-perceived government shutdown, here is the week’s positive news that may contribute to an accelerated QE stimulus tapering:

- Strong Jobs: The latest monthly employment report showed +204,000 jobs added in October, almost +100,000 more additions than economists expected. August and September job additions were also revised higher.

- GDP Surprise: 3rd quarter GDP registered in at +2.8% vs. expectations of 2%.

- IPO Dough: Twitter Inc (TWTR) achieved a lofty $25,000,000,000 initial public offering (IPO) value on its first day of trading.

- ECB Cuts Rates: The European Central Bank (ECB) lowered its key benchmark refinancing rate to a record low 0.25% level.

- Service Sector Surge: ISM non-manufacturing PMI data for October came in at 55.4 vs. 54.0 estimate.

Bad News

Here is the other side of the coin, which could assist in the delay of tapering:

- Mortgage Apps Decline: Last week the MBA mortgage application index fell -7%.

- Jobless # Revised Higher: Last week’s Initial jobless Claims were revised higher by 5,000 to 345,000.

- Investors Too Happy: The spread between Bulls & Bears is highest since April 2011 as measured by Investors Intelligence

Much Ado About Nothing

With the recent surge in the October jobs numbers, the tapering plot has thickened. But rather than a tragic death to the stock market, the inevitable taper and eventual tightening of the Fed Funds rate will likely be “Much Ado About Nothing.” How can that be?

As I have written in an article earlier this year (see 1994 Bond Repeat), the modest increase in 2013 yields (up +1.35% approximately) from the July 2012 lows pales in comparison to the +2.5% multi-period hike in the 1994 Federal Funds rate by then Fed Chairman Alan Greenspan. What’s more, inflation was a much greater risk in 1994 with GDP exceeding 4.0% and unemployment reaching a hot 5.5% level.

Given an overheated economy and job market in 1994, coupled with a hawkish Fed aggressively raising rates, the impact of these factors must have been disastrous for the stock market…right? WRONG. The S&P 500 actually finished the year essentially flat (~-1.5%) after experiencing some volatility earlier in the year, then subsequently stocks went on a tear to more than triple in value over the next five years.

To taper or not to taper may be the media question du jour, however the Fed’s ultimate decision regarding QE will most likely resemble a heroic Shakespearean finale or Much Ado About Nothing. Panicked portfolios may be in love with cash like Romeo & Juliet were with each other, but overreaction by investors to future tapering and rate hikes may result in poisonous or tragic returns.

Referenced article: 1994 Bond Repeat or 2013 Stock Defeat?

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in TWTR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page. Some Shakespeare references were sourced from Kevin D. Weaver.

2012 Party Train Missed Thanks to F.U.D.

Article is an excerpt from previously released Sidoxia Capital Management’s complementary January 2, 2013 newsletter. Subscribe on right side of page.

There was plenty of fear, uncertainty, and doubt (F.U.D.) in 2012, and the gridlock in Washington has been a contributing factor to investors’ angst. As the saying goes, the stock market climbs a “wall of worry” and that was certainly the case this year with the S&P 500 index rising +13.4% (over +15% including dividends), and the Nasdaq index soaring +15.9% before dividends. Short-term investors had ample worries to fret about throughout the year, including a European financial collapse, the presidential elections, fiscal cliff negotiations, and a Mayan doomsday (see this hilarious clip). Despite these fears dominating the daily airwaves and newspaper headlines, long-term investors holding an adequate equity asset allocation jumped on the non-stop 2012 party train.

While Americans were served a full plate of concerns this year, global investors benefited from European Central Bank intervention by Mario Draghi who promised to do “whatever it takes” to save the euro currency (the European dominated EAFE index rose +13.6% in 2012). Growth here in the U.S. slowed as cautious consumers and businesses horded cash, but a rebound in the domestic housing market provided support to the sluggish economic expansion (3rd quarter GDP growth was revised higher to +3.1% vs. 2011).

Now that the presidential elections are over and we achieved a partial fiscal cliff deal, the amount of F.U.D. going into 2013 will diminish, which should provide a tailwind to economic growth and the financial markets. The impending debt ceiling and deficit reduction talks may slow the train down, but if a sufficient resolution can be accomplished, the economic party train can continue chugging along.

Attention: Grab Your Ear Muffs

Economists and strategists will continue to sound smart and be completely wrong about their 2013 predictions (see Strategist Predictions & MacGyver), but that won’t stop average investors from neglecting their long-term investment plans. Investors have commonly overindulged in certain narrow asset classes like overpriced bonds and gold, which both underperformed equities in 2012. Diversification may sound like an overused finance cliché, but the principle is paramount if you are serious about reducing risk, beating inflation, and smoothing out incessant volatility.

2013 New Year’s Resolution: Avoid Personal Fiscal Cliff

With the New Year upon us, just because politicians have financial problems, it doesn’t mean you have to be fiscally irresponsible too. There is no better time than now to make a financial New Year’s resolution to avoid your own personal fiscal cliff. If you are too heavily parked in cash or over-exposed to low-yielding bonds subject to significant interest rate risk, then now is the time to re-evaluate your investment plan.

There is always something to worry about (see also Uncertainty: Love It?), but in order to prevent working into your 80s, a long-term investment plan needs to be implemented, regardless of economic headlines or market volatility. In other words, investors need to replace their short-term microscope for their long-term telescope. By committing to a disciplined fiscal New Year’s resolution, you can earn a ticket on the 2013 party train!

Monthly News Tidbits

The presidential elections dominated the news cycle in November, but there were a whole host of other tidbits occurring over the last thirty-one days. Here are some of the main storylines:

Congress Approves Mini Fiscal Cliff Deal: After months of debate, Congress painfully and reluctantly agreed upon an estimated $600 billion mini fiscal cliff deal that represents the largest tax increase in two decades. Contrary to a $4 trillion “Grand Bargain” deal, this bill amounts to a more modest reduction in the deficit over 10 years. The Senate passed the bill by a margin of 89-8 and the House of Representatives by a spread of 257-167. The fact that any deal got done is somewhat surprising since the gridlock has been especially rampant in the House. As proof of this assertion, one need only point to the chamber’s meager voting activity record – the House has passed the fewest bills in 60 years during its recent term.

Fiscal Cliff Bill Details: Despite the Senate’s convincing voting margin, large numbers of Congressional Democrats and Republicans were unhappy with the bill’s details. The President made good on his campaign promises by securing revenue-raising taxes from wealthy Americans. More specifically, the law contains provisions including a 39.6% rate on earners above $400,000; a 20% capital gains rate increase from 15%; new exemption/deduction limits; an estate tax increase to 40% from 35%; and a measure to help prevent near-term milk price spikes. There are plenty more details, but I will spare your eyeballs and brain from the painful minutiae. If you haven’t had enough partisan politics, no need to worry, you have the debt ceiling debate to look forward to in a few months.

Quantitative Easing Redux (QE4): Federal Reserve Chairman Ben Bernanke helped orchestrate additional monetary policy stimulus via a fourth round of quantitative easing (a.k.a., QE4). As part of this plan, the Fed will vastly expand its $2.8 trillion balance sheet in 2013 with additional monthly purchases of $45 billion of long-term Treasuries. By executing this invigorating QE4 bond buying program, the Fed pledges to keep interest rates in the cellar until the unemployment rate falls below 6.5% or inflation rises above 2.5%.

Same-Sex Marriage: The Supreme Court tackled a long-debated social issue and declared it would rule on the legality of a law denying benefits to same-sex couples in 2013.

New Female President: Additional hormones were added to the gender-skewed global pool of testosterone-filled leaders as South Korea elected its first female president, Park Geun-hye.

Global Bank Fined: Another greedy financial institution got caught with its hand in the cookie jar. UBS agreed to cough up a $1.5 billion penalty to the U.S., U.K., and Swiss authorities as part of an agreement to resolve its involvement in the manipulation of the London Interbank Offered Rate (LIBOR) – see also Wall Street Meets Greed Street.

Sandy Hook Distressing Disaster: The gun control debate was reignited when 20-year-old Adam Lanza gunned down 20 children and 7 adults (including his mother) at a Connecticut elementary school – Sandy Hook Elementary. Besides the examination of an assault weapons ban, the government needs to revisit the inadequate awareness and resources devoted to the serious issue of mental illness.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including fixed income ETFs, but at the time of publishing SCM had no direct position in EFA, UBS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Financial Olympics: Chasing Gold, Siver & Bronze

Article is an excerpt from previously released Sidoxia Capital Management’s complementary August 1, 2012 newsletter. Subscribe on right side of page.

As a record number of 204 nations compete at the XXX Olympic Games in London, and millions of couch-watchers root on their favorite athletes, a different simultaneous competition is occurring…the 2012 Financial Olympics. So far, both Olympics have provided memorable moments for all. While the 2012 London Olympic viewers watched James Bond and Queen Elizabeth II parachute into a stadium filled with 80,000 cheering fans, investors cheered the Dow Jones Industrial Average above the 13,000 level on the same day of the opening ceremony. We have already witnessed a wide range of emotions displayed by thousands of athletes chasing gold, silver, and bronze, and the same array of sentiments associated with glory and defeat have been observed in the 2012 Financial Olympics. There is still a way to go, but despite all the volatility, the stock market is still up a surprising +10% in 2012.

Here were some of the key Financial Olympic events last month:

Draghi Promises Gold for Euro: Some confident people promise gold medals while others promise the preservation of a currency – European Central Bank President (ECB) Mario Draghi personifies the latter. Draghi triggered the controversy with comments he made at the recent Global Investment Conference in London. In the hopes of restoring investor confidence Draghi emphatically proclaimed, “The ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.” To view this excerpt, click video link here.

U.S. Economy Wins Bronze: Whereas Europe has been disqualified from the Financial Olympics due to recessionary economic conditions (Markit predicts a -0.6% contraction in Q3 eurozone GDP), the U.S. posted respectable Q2 GDP results of +1.5%. This surely is an effort worthy of a bronze medal given the overall sluggish, global demand. Fears over a European financial crisis contagion; undecided U.S. Presidential election; and uncertain “fiscal cliff” (automatic tax hikes and spending cuts) are factors contributing to the modest growth. Nevertheless, the US of A has posted 12 consecutive quarters of economic growth (see chart below) and if some clarity creeps back into the picture, growth could reaccelerate.

Source (Calafia Beach Pundit)

No Podium for Spain: Spain’s recent economic achievements closely mirror those of the athletic team, which thus far has failed to secure a sporting medal of any color. Why no Spanish glory? Recently, the Bank of Spain announced the country’s economy was declining at a -1.6% annual rate. Shortly thereafter, Spain estimated its economy would contract by -0.5% in 2013 instead of expanding +0.2%, as previously expected. Adding insult to injury, Valencia (Spain’s most indebted region) said central government support would be needed to repay its debts. These factors, and others, have forced the Spanish government to adopt severe austerity measures to cut its budget deficit by $80 billion through 2015. Spanish banks have negotiated a multi-billion-euro bailout, but they will have to hand control over to European institutions as a concession. Considering these facts, combined with an unemployment rate near 25%, one can appreciate the dominant and pervading losing spirit.

Global Central Banks Inject Financial Steroids: The challenging and competitive global growth environment is not new news to central bankers around the world. As a result, finance leaders around the world are injecting financial steroids into their countries via monetary stimulus (mostly rate cuts and bond buying). Like steroids, these actions may have short-term invigorating effects, but these measures can also have longer-term negative consequences (i.e., inflation). Here are some of the latest country-specific examples (also see chart below):

- U.S. Federal Reserve Chairman Ben Bernanke has already shot a couple “Operation Twist” and “QE” (Quantitative Easing) bullets, but as global growth continues to slow, he has openly acknowledged his willingness to dig into his toolbox for additional measures under the right circumstances, including QE3.

- The PBOC (People’s Bank of China) surprised many observers by employing its second rate cut in less than a month. The PBOC lowered its one-year lending rate by 0.31% to 6%.

- The ECB (European Central Bank) lowered its key lending rate by 0.25% to an all-time low of 0.75% and also cut its overnight deposit rate (the equivalent of our Federal Funds rate) by 0.25% to 0%.

- Brazil’s central bank recently cut its benchmark Selic rate for the 8th time in a year to an all-time low of 8% from 12.5%.

- South Korea’s central bank lowered its key interest rates by 0.25% to 3%, its first such action in three years.

- The BOE (Bank of England) raised its quantitative easing goal by 50 billion pounds (~$78 billion).

Source (Calafia Beach Pundit)

Source (Calafia Beach Pundit)

Banks Disqualified from Libor Games: As a result of the Libor (London Interbank Offered Rate) rigging scandal, Barclays CEO Robert Diamond resigned from the bank and agreed to forfeit $31 million in bonus money. Libor is a measure of what banks pay to borrow from each other and, perhaps more importantly, it acts as a measuring stick for determining rates on mortgages and other financial contracts. In an attempt to boost the perceived financial strength of their financial condition, multiple banks artificially manipulated the calculation of the Libor rate. Ironically, this scandal likely helped consumers with lower mortgage and credit card rates.

Rates Running Backwards: Sports betting on teams and events is measured by point spreads and numerical odds. In the global debt markets, betting is measured by interest rates. So while losing, debt-laden countries like Greece and Spain have seen their interest rates explode upwards, winning, fiscally responsible countries (including Switzerland, Austria, Denmark, Netherlands, Germany, and Finland) have seen their bond yields turn NEGATIVE. That’s right, investors are earning a negative return. Rather than making a bet on higher yielding bonds, many investors are flocking to the perceived safety of these interest-losing bonds (see chart below). This game cannot last forever, especially for individual and institutional investors who require income to meet liquidity and return requirements.

Source (The Financial Times)

China Wins GDP Gold Medal but No World Record: China currently leads in both the Olympic Games gold medal count (China 13 vs. U.S. 9 through July 31st) and GDP competition. Given the fiscal and monetary stimulus measures the government has implemented, it appears their economy is bottoming. Despite the tremendous anxiety over China’s growth, China’s National Bureau of Statistics just announced a +7.6% Q2 GDP growth rate (see chart below), down from +8.1% in Q1. Although this is the slowest growth since the global financial crisis, Even though this was the slowest GDP growth rate in over three years, most countries would die for this level of growth. Adding evidence to the bottoming storyline, HSBC recently reported the preliminary Chinese PMI manufacturing index rose to 49.5 in July, up from 48.2 in June – the highest reading since early this year (February).

Source (Calafia Beach Pundit)

Higgs Wins God Particle Gold: Michael Phelps and Missy Franklin are not the only people to win gold medals in their fields. Peter Higgs and fellow scientists had 50-years of their physics research validated when the Large Hadron Collider discovered the long-sought Higgs boson (a.k.a., the “god particle”). The collider, located on the Franco-Swiss border, measured approximately 17 miles in length, took years to build, and cost about $8 billion to finish. Pundits are declaring the unearthing of Higgs boson as the greatest scientific discovery since the sequencing of the human genome. Higgs’s gold medal may just come in the form of a Nobel Prize in Physics.

Source (The Financial Times)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in Barclays or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Markets Race Out of 2012 Gate

Article includes excerpts from Sidoxia Capital Management’s 2/1/2012 newsletter. Subscribe on right side of page.

Equity markets largely remained caged in during 2011, but U.S. stocks came racing out of the gate at the beginning of 2012. The S&P 500 index rose +4.4% in January; the Dow Jones Industrials climbed +3.4%; and the NASDAQ index sprinted out to a +8.0% return. Broader concerns have not disappeared over a European financial meltdown, high U.S. unemployment, and large unsustainable debts and deficits, but several key factors are providing firmer footing for financial race horses in 2012:

• Record Corporate Profits: 2012 S&P operating profits were recently forecasted to reach a record level of $106, or +9% versus a year ago. Accelerating GDP (Gross Domestic Product Growth) to +2.8% in the fourth quarter also provided a tailwind to corporations.

• Mountains of Cash: Companies are sitting on record levels of cash. In late 2011, U.S. non-financial corporations were sitting on $1.73 trillion in cash, which was +50% higher as a percentage of assets relative to 2007 when the credit crunch began in earnest.

• Employment Trends Improving: It’s difficult to fall off the floor, but since the unemployment rate peaked at 10.2% in October 2009, the rate has slowly improved to 8.5% today. Data junkies need not fret – we have fresh new employment numbers to look at this Friday.

• Consumer Optimism on Rise: The University of Michigan’s consumer sentiment index showed optimism improved in January to the highest level in almost a year, increasing to 75.0 from 69.9 in December.

• Federal Reserve to the Rescue: Federal Reserve Chairman, Ben Bernanke, and the Fed recently announced the extension of their 0% interest rate policy, designed to assist economic expansion, through the end of 2014. In addition, Bernanke did not rule out further stimulative asset purchases (a.k.a., QE3 or quantitative easing) if necessary. If executed as planned, this dovish stance will extend for an unprecedented six year period (2008 -2014).

Europe on the Comeback Trail?

Source: Calafia Beach Pundit

Europe is by no means out of the woods and tracking the day to day volatility of the happenings overseas can be a difficult chore. One fairly easy way to track the European progress (or lack thereof) is by following the interest rate trends in the PIIGS countries (Portugal, Ireland, Italy, Greece, and Spain). Quite simply, higher interest rates generally mean more uncertainty and risk, while lower interest rates mean more confidence and certainty. The bad news is that Greece is still in the midst of a very complex restructuring of its debt, which means Greek interest rates have been exploding upwards and investors are bracing for significant losses on their sovereign debt investments. Portugal is not in as bad shape as Greece, but the trends have been moving in a negative direction. The good news, as you can see from the chart above (Calafia Beach Pundit), is that interest rates in Ireland, Italy and Spain have been constructively moving lower thanks to austerity measures, European Central Bank (ECB) actions, and coordination of eurozone policies to create more unity and fiscal accountability.

Political Horse Race

Source: Real Clear Politics via The Financial Times

The other horse race going on now is the battle for the Republican presidential nomination between former Massachusetts governor Mitt Romney and former House of Representatives Speaker Newt Gingrich. Some increased feistiness mixed with a little Super-Pac TV smear campaigns helped whip Romney’s horse to a decisive victory in Florida – Gingrich ended up losing by a whopping 14%. Unlike traditional horse races, we don’t know how long this Republican primary race will last, but chances are this thing should be wrapped up by “Super Tuesday” on March 6th when there will be 10 simultaneous primaries and caucuses. Romney may be the lead horse now, but we are likely to see a few more horses drop out before all is said and done.

Flies in the Ointment

As indicated previously, although 2012 has gotten off to a strong start, there are still some flies in the ointment:

• European Crisis Not Over: Many European countries are at or near recessionary levels. The U.S. may be insulated from some of the weakness, but is not completely immune from the European financial crisis. Weaker fourth quarter revenue growth was suffered by companies like Exxon Mobil Corp (XOM), Citigroup Inc. (C), JP Morgan Chase & Co (JPM), Microsoft Corp (MSFT), and IBM, in part because of European exposure.

• Slowing Profit Growth: Although at record levels, profit growth is slowing and peak profit margins are starting to feel the pressure. Only so much cost-cutting can be done before growth initiatives, such as hiring, must be implemented to boost profits.

• Election Uncertainty: As mentioned earlier, 2012 is a presidential election year, and policy uncertainty and political gridlock have the potential of further spooking investors. Much of these issues is not new news to the financial markets. Rather than reading stale, old headlines of the multi-year financial crisis, determining what happens next and ascertaining how much uncertainty is already factored into current asset prices is a much more constructive exercise.

Stocks on Sale for a Discount

Source: Calafia Beach Pundit

A lot of the previous concerns (flies) mentioned is not new news to investors and many of these worries are already factored into the cheap equity prices we are witnessing. If everything was all roses, stocks would not be selling for a significant discount to the long-term averages.

A key ratio measuring the priceyness of the stock market is the Price/Earnings (P/E) ratio. History has taught us the best long-term returns have been earned when purchases were made at lower P/E ratio levels. As you can see from the 60-year chart above (Calafia Beach Pundit), stocks can become cheaper (resulting in lower P/Es) for many years, similar to the challenging period experienced through the early 1980s and somewhat analogous to the lower P/E ratios we are presently witnessing (estimated 2012 P/E of approximately 12.4). However, the major difference between then and now is that the Federal Funds interest rate was about 20% back in the early-’80s, while the same rate is closer to 0% currently. Simple math and logic tell us that stocks and other asset-based earnings streams deserve higher prices in periods of low interest rates like today.

We are only one month through the 2012 financial market race, so it much too early to declare a Triple Crown victory, but we are off to a nice start. As I’ve said before, investing has arguably never been as difficult as it is today, but investing has also never been as important. Inflation, whether you are talking about food, energy, healthcare, leisure, or educational costs continue to grind higher. Burying your head in the sand or stuffing your money in low yielding assets may work for a wealthy few and feel good in the short-run, but for much of the masses the destructive inflation-eroding characteristics of purported “safe investments” will likely do more damage than good in the long-run. A low-cost diversified global portfolio of thoroughbred investments that balances income and growth with your risk tolerance and time horizon is a better way to maneuver yourself to the investment winner’s circle.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in XOM, MSFT, JPM, IBM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Draghi & ECB Pass Trash and Serve Brussels Sprouts

ECB (European Central Bank) President Mario Draghi made it clear with his most recent monetary banking announcements that he is perfectly willing to shovel the sovereign debt trash around the financial system, but he just doesn’t want the ECB to gobble up heaps of the smelly debt.

On the same day that Draghi lowered the key benchmark interest rate by -0.25% to 1.00%, he also reduced the lending credit rating threshold for acceptable banking collateral to “single-A” and offered banks endless three-year loans with . But wait…there’s more! In typical infomercial fashion, Draghi had an additional stimulative gift offering – he halved the reserve requirement ratios for European banks.

Although Draghi is handing out lots of hugs and kisses to the banks, including infinite amounts of three-year loans, he is also providing very little direct love to European debt-laden governments. In other words, Draghi isn’t ready to pull out the printing press bazooka to sop up mounds of trashy sovereign debt (i.e., Greece, Italy, and Spain). Draghi may be willing to make the ECB the lender of last resort for the banks, but he is not signaling the same lender of last resort commitment for careless governments.

Despite Draghi’s public aversion to bond buying (a.k.a. QE or quantitative easing), he indirectly is funding quantitative easing anyway. Rather than having the ECB accelerate the direct purchase of besieged sovereign debt, he indirectly is giving money to the banks to purchase the same struggling bonds. Sneaky, but clever…I like it.

Eat Your Brussels Sprouts!

Draghi in his new role as ECB President is clearly trying to be a responsible parent to the Euro leaders, but as a result, he could be placing himself in trouble with the law. I haven’t contacted my attorneys yet, however Mario Draghi is blatantly infringing on my patented “Brussels sprouts mandate” that I regularly use at the dinner table with my children. On any given night, by 6:30 p.m. my kids are practically frothing at the mouth for some unhealthy dessert delight. The problem with the situation is unfinished Brussels sprouts sitting on their plates, so with respected authority I command, “If you want dessert tonight, you better eat your Brussels sprouts!” Normally this is not a bad strategy because my plea usually results in an extra consumed sprout or two. Ultimately, given the softy that I am, all parties involved know that dessert will be served regardless of the number of sprouts consumed.

Draghi in his new role as ECB President is clearly trying to be a responsible parent to the Euro leaders, but as a result, he could be placing himself in trouble with the law. I haven’t contacted my attorneys yet, however Mario Draghi is blatantly infringing on my patented “Brussels sprouts mandate” that I regularly use at the dinner table with my children. On any given night, by 6:30 p.m. my kids are practically frothing at the mouth for some unhealthy dessert delight. The problem with the situation is unfinished Brussels sprouts sitting on their plates, so with respected authority I command, “If you want dessert tonight, you better eat your Brussels sprouts!” Normally this is not a bad strategy because my plea usually results in an extra consumed sprout or two. Ultimately, given the softy that I am, all parties involved know that dessert will be served regardless of the number of sprouts consumed.

Draghi, in dealing with the irresponsible fiscal actions of the sovereigns, is using the same precise “sprout mandate.” In a recent press conference, here’s how Draghi delivered his tough talk:

“All euro-area governments urgently need to do their utmost” for fiscal sustainability. “Policy makers need to correct excessive deficits and move to balanced budgets in the coming years. This will strengthen overall economic sentiment. To accompany fiscal consolidation, the governing council has called for bold and ambitious structural reforms.”

Just as it makes sense for me not to say, “Hey kids, don’t worry about eating your vegetables, save room for the ice cream sundae buffet,” it probably doesn’t make sense for Draghi to inform European leaders, “Hey kids, don’t worry about those massive debts and deficits, the ECB will give you plenty of money to buy up all that trashy sovereign debt of yours.”

Hypocritical Or Shrewd?

I applaud Signore Draghi for implementing his bold actions as lender of last resort for European Banks, but isn’t it a tad bit hypocritical? The ECB President talks seriously about Basel III capital requirements, yet he is easing rules on collateral and reserves. Why is it OK for the ECB to condone reckless behavior and introduce moral hazards for the banks (i.e., limitless ECB backstop), but not for irresponsible governments too? If I am a European bank with continuous access to ECB loans, why not roll the dice and risk shareholder capital in hopes of a big risky payoff? I’m sure Jon Corzine at MF Global (MFGLQ.PK) would appreciate similar financial backing. What’s more, how credible can Draghi be about his tough fiscal love and anti-quantitative easing stances when he is currently offering never-ending amounts of money to the banks and already buying collapsing sovereign bonds as we speak?

No matter the view you hold, the ECB is openly demonstrating it will not sit idle watching the banking system collapse under its own watch, much like the Federal Reserve and Ben Bernanke did not sit idle in 2008-2009. Perhaps Draghi isn’t being hypocritical, but is rather being shrewd? Although Draghi wants governments to eat their fiscal Brussels sprouts, let’s not kid ourselves. Just as Draghi is willing to pass the trash and appease the banking system, if the eurozone sovereign debt crisis continues worsening, don’t be surprised to see Draghi roll out his ice cream sundae buffet of aggressive bond buying. That will taste much better than Brussels sprouts.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MF Global (MFGLQ.PK), or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Dominoes, Deleveraging, and Justin Bieber

Despite significant 2011 estimated corporate profit growth (+17% S&P 500) and a sharp rebound in the markets since early October (+18% since the lows), investors remain scared of their own shadows. Even with trembling trillions in cash on the sidelines, the Dow Jones Industrial Average is up +5.0% for the year (+11% in 2010), and that excludes dividends. Not too shabby, if you think about the trillions melting away to inflation in CDs, savings accounts, and cash. With capital panicking into 10-year Treasuries, hovering near record lows of 2%, it should be no surprise to anyone that fears of a Greek domino toppling Italy, the eurozone, and the global economy have sapped confidence and retarded economic growth.

Deleveraging is a painful process, and U.S. consumers and corporations have experienced this first hand since the financial crisis of 2008 gained a full head of steam. Sure, housing has not recovered, and many domestic banks continue to chew threw a slew of foreclosures and underwater loan modifications. However, our European friends are now going through the same joyful process with their banks that we went through in 2008-2009. Certainly, when it comes to the government arena, the U.S. has only just begun to scratch the deleveraging surface. Fortunately, we will get a fresh update of how we’re doing in this department, come November 23rd, when the Congressional “Super Committee” will update us on $1.2 trillion+ in expected 10-year debt reductions.

Death by Dominoes?

Is now the time to stock your cave with a survival kit, gun, and gold? I’m going to go out on a limb and say we may see some more volatility surrounding the European PIIGS debt hangover (Portugal/Italy/Ireland/Greece/Spain) before normality returns, but Greece defaulting and/or exiting the euro does not mean the world is coming to an end. At the end of the day, despite legal ambiguity, the ECB (European Central Bank) will come to the rescue and steal a page from Ben Bernanke’s quantitative easing printing press playbook (see European Deadbeat Cousin).

Greece isn’t the first country to be attacked by bond vigilantes who push borrowing costs up or the first country to suffer an economic collapse. Memories are short, but it was not too long ago that a hedge fund on ice called Iceland experienced a massive economic collapse. It wasn’t pretty – Iceland’s three largest banks suffered $100 billion in losses (vs. a $13 billion GDP); Iceland’s stock market collapsed 95%; Iceland’s currency (krona) dropped 50% in a week. The country is already on the comeback trail. Currently, unemployment (@ 6.8%) in Iceland is significantly less than the U.S. (@ 9.0%), and Iceland’s economy is expanding +2.5%, with another +2.5% growth rate forecasted by the IMF (International Monetary Fund) in 2012.

Iceland used a formula of austerity and deleveraging, similar in some fashions to Ireland, which also has seen a dramatic -15% decrease in its sovereign debt borrowing costs (see chart below).

Source: Bloomberg.com

OK, sure, Iceland and Ireland are small potatoes (no pun intended), so how realistic is comparing these small countries’ problems to the massive $2.6 trillion in Italian sovereign debt that bearish investors expect to imminently implode? If these countries aren’t credibly large enough, then why not take a peek at Japan, which was the universe’s second largest economy in 1989. Since then, this South Pacific economic behemoth has experienced an unprecedented depression that has lasted longer than two decades, and seen the value of its stock market decline by -78% (from 38,916 to 8,514). Over that same timeframe, the U.S. economy has seen its economy grow from roughly $5.5 trillion to $15.2 trillion.

There’s no question in mind, if Greece exits the euro, financial markets will fall in the short-run, but if you believe the following…

1.) The world is NOT going to end.

2.) 2012 S&P profits are NOT declining to $65.

AND/OR

3.) Justin Bieber will NOT run and overtake Mitt Romney as the leading Republican candidate

…then I believe the financial markets are poised to move in a more constructive direction. Perhaps I am a bit too Pollyannaish, but as I decide if this is truly the case, I think I’ll go play a game of dominoes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Solving Europe and Your Deadbeat Cousin

The fall holidays are quickly approaching, and almost every family has at least one black-sheep member among the bunch. You know, the unemployed second cousin who shows up for Thanksgiving dinner intoxicated – who then proceeds to pull you aside after a full meal to ask you for some money because of an unlucky trip to Las Vegas. For simplicity purposes, let’s name our deadbeat cousin Joe.

Right now the European union (EU) is dealing with a similar situation, but rather than being forced to deal with money-begging cousin named Joe, the EU is being forced to confront the irresponsible debt-binging practices of its own relatives – the PIIGS (Portugal, Ireland, Italy, Greece, and Spain). The European troika (International Monetary Fund/IMF; European Union/EU; and European Central Bank/ECB), spearheaded by German and French persuasion, is contemplating everything from prescribing direct bank recapitalization, bailouts via the leveraging of the EFSF (European Financial Stability Facility), ECB bond purchases, debt guarantees, unlimited central bank loans, and more.

New stress tests are being reevaluated as we speak. Previous tests failed in gaining the necessary credibility because inadequate haircuts were applied to the values of PIIGS debt held by European banks. European Leaders are beginning to gain some religion as to the urgency and intensity of the financial crisis. Just today, Germany’s chancellor (Angela Merkel) and France’s President (Nicolas Sarkozy) announced that they will introduce a comprehensive package of measures to stabilize the eurozone by the end of this month, right before the summit of the G20 leading global economies in Cannes, France.

Pick Your Poison

Whatever the path used to mop up debt excesses, the options for solving the financial mess can be lumped together in the following categories:

1. Austerity: Plain, unadulterated spending cuts is one prescription being administerd in hopes of curing bloated European sovereign debt issues. Negatives: Slowing economic growth, slowing tax receipts, potentially widening deficits (reference Greece), and political reelection self interests call into question the feasibility of the austerity option. Positives: Austerity is a morally correct fiscal response, which has the potential of placing a country’s financial situation back on a sustainable path.

2. Bailouts: The troika is also talking about infusing the troubled banks with new capital. Negatives: This action could result in more debt placed on country balance sheets, a potentially lower credit rating, higher costs of borrowing, higher tax burden for blameless taxpayers, and often an impossible political path of success. Positives: Financial markets may respond constructively in the short-run, but providing an alcoholic more alcohol doesn’t solve long-term fiscal responsibility, and also introduces the problem of moral hazard.

3. Haircuts: Voluntary or involuntary haircuts to principal debt obligations may occur in conjunction with previously described bailout efforts, depending on the severity of debt levels. Negatives: There are many different sets of constituents and investors, which can make voluntary haircut/debt restructuring terms difficult to agree upon. If the haircuts are too severe, banking reserves across the EU will become decimated, which will only lead to more austerity, bailouts, and potential credit downgrades. Such actions could hamper or eliminated future access to capital, and the cost of access to future capital could be cost prohibitive for the borrowing countries that defaulted/restructured. Positives: Haircuts eliminate or lessen the need for other more painful austerity or restructuring measures, and force borrowers to become more fiscally responsible, not to mention, investors are forced to conduct more thorough due diligence.

4. Printing Press: Buying back debt with freshly printed euros hot off the press is another strategy. Negatives: Inflation is an invisible tax on everyone, including those constituents who are behaving in a fiscally responsible manner. Positives: Not only is this strategy more politically palatable because the inflation tax is spread across the whole union, but this path to debt reduction also does not require as painful and unpopular cuts in spending as experienced in other options.

The Costs

What is the cost for this massive European debt-binging rehabilitation? Estimates vary widely, but a JP Morgan analyst sized it up this way as explained in the The Financial Times:

“In a worst-case, severe recession scenario, €230bn in new capital is needed to meet Basel III requirements, assuming a 60 per cent debt writedown on Greece, 40 per cent on Ireland and Portugal and 20 per cent on Italy and Spain, and that banks withhold dividends.”

More bearish estimates with larger bond loss haircuts, stricter regulatory guidelines, and harsher austerity measures have generated recapitalization numbers north of €1 trillion euros. Regardless of the estimates, European governments, regulators, and central banks are likely to select a combination of the poisons listed above. There is no silver bullet solution, and any of the chosen paths come with their own unique set of consequences.

As time passes and the European crisis matures, I am confident that you will be hearing more about ECB involvement and the firing-up of the printing presses. Perhaps the ECB will fund and work jointly with the EFSF to soak up debt and/or capitalize weak banks. Alternatively, and more simply, the ECB is likely to follow the path of the U.S. and implement significant amounts of quantitative easing (i.e., provide liquidity to the financial system via sovereign debt purchases and guarantees).

Dealing with irresponsible and intoxicated deadbeat second cousins (or European countries) fishing for money is never a pleasurable experience. There are many ways to address the problem, but ignoring the issue will only make the situation worse. Fortunately, our European friends on the other side of the pond appear to be taking notice. As in the U.S., if government officials delay or ignore the immediate problems, the financial market cops (a.k.a., “bond vigilantes”) will force them into action. In the recent past, European officials have used a strategy of sober talking “tough love,” but signs that the ECB printing presses are now beginning to warm up are evident. Once the euros come flying off the presses to detoxify the debt binging banks, perhaps the ECB can print a few extra euros for my cousin Joe.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in JPM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}