Posts tagged ‘Ebola’

Ignoring Economics and Vital Signs

As stock prices sit near all-time record highs, and as we enter year nine of the current bull market, I remain amazed and amused at the brazen disregard for important basic economic concepts like supply & demand, interest rates, and rising profits.

If the stock market was a doctor’s patient, over the last decade, bloggers, pundits, talking heads, and pontificators have been ignoring the improving, healthy patient’s vital signs, while endlessly predicting the death of the resilient stock market.

However, let’s be clear – it has not been all hearts and flowers for stocks – there have been numerous -10%, -15%, and -20% corrections since the Financial Crisis nine years ago. Those corrections included the Flash Crash, debt downgrade, Arab Spring, sequestration, Taper Tantrum, Iranian Nuclear Threat, Ukrainian-Crimea annexation, Ebola, Paris/San Bernardino Terrorist Attacks, multiple European & Chinese slowdowns and more.

Despite the avalanche of headlines and volatility, we all know the net result of these events – a more than tripling of stock prices (+259%) from March 2009 to new all-time record highs. With the incessant stream of negative news, how could prices appreciate so dramatically?

Over the years, the explanations by outside observers have changed. First, the recovery was explained as a “dead cat bounce” or a short-term cyclical bull market within a long-term secular bear market. Then, when stock prices broke to new records, the focus shifted to Quantitative Easing (QE1, QE2, QE3, and Operation Twist). The QE narrative implied the bull advance was temporary due to the non-stop, artificial printing presses of the Fed. Now that the Fed has not only ended QE but reversed it (the Fed is actually contracting its balance sheet) and hiked interest rates (no longer cutting), outsiders are once again at a loss. Now, the bears are left clinging to the flawed CAPE metric I wrote about three years ago (see CAPE Smells Like BS), and using political headlines as a theory for record prices (i.e., record stock prices stem from inflated tax cut and infrastructure spending expectations).

It’s unfortunate for the bears that all the conspiracy theory headlines and F.U.D. (fear, uncertainty, and doubt) over the last 10 years have failed miserably as predictors for stock prices. The truth is that stock prices don’t care about headlines – stock prices care about economics. More specifically, stock prices care about profits, interest rates, and supply & demand.

Profits

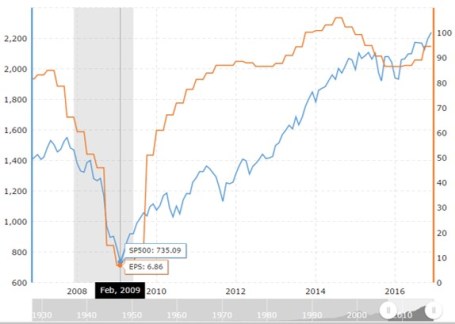

It’s quite simple. Stock prices have more than tripled since early 2009 because profits have more than tripled since 2009. As you can see from the Macrotrends chart below, 2009 – 2016 profits for the S&P 500 index rose from $6.86 to $94.54, or +1,287%. It’s no surprise either that stock prices stalled for 18 months from 2015 to mid-2016 when profits slowed. After profits returned to growth, stock price appreciation also resumed.

Source: Macrotrends

Interest Rates

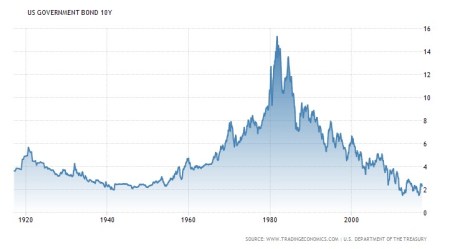

When you could earn a +16% on a guaranteed CD bank rate in the early 1980s, do you think stocks were a more or less attractive asset class? If you can sense the rhetorical nature of my question, then you can probably understand why stocks were about as attractive as rotten milk or moldy bread. Back then, stocks traded for about 8x’s earnings vs. the 18x-20x multiples today. The difference is, today interest rates are near generational lows (see chart below), and CDs pay near +0%, thereby making stocks much more attractive. If you think this type of talk is heresy, ignore me and listen to the greatest investor of all-time, Warren Buffett who recently stated:

“Measured against interest rates, stocks are actually on the cheap side.”

Source: Trading Economics

Supply & Demand

Another massively ignored area, as it relates to the health of stock prices, is the relationship of new stock supply entering the market (e.g., new dilutive shares via IPOs and follow-on offerings), versus stock exiting the market through corporate actions. While there has been some coverage placed on the corporate action of share buybacks – about a half trillion dollars of stock being sucked up like a vacuum cleaner by cash heavy companies like Apple Inc. (AAPL) – little attention has been paid to the trillions of dollars of stock vanishing from mergers and acquisition activities. Yes, Snap Inc. (SNAP) has garnered a disproportionate amount of attention for its $3 billion IPO (Initial Public Offering), this is a drop in the bucket compared to the exodus of stock from M&A activity. Consider the trivial amount of SNAP supply entering the market ($3 billion) vs. $100s of billions in major deals announced in 2016 – 2017:

- Time Warner Inc. merger offer by AT&T Inc. (T) for $85 billion

- Monsanto Co. merger offer by Bayer AG (BAYRY) for $66 billion

- Reynolds American Inc. merger offer by British American Tobacco (BTI) for $47 billion

- NXP Semiconductors merger offer by Qualcomm Inc. (QCOM) for $39 billion

- LinkedIn merger offer by Microsoft Corp. (MSFT) for $28 billion

- Jude Medical, Inc. merger offer by Abbott Laboratories (ABT) for $25 billion

- Mead Johnson Nutrition merger offer by Reckitt Benckiser Group for $18 billion

- Mobileye merger offer by Intel Corp. (INTC) for $15 billion

- Netsuite merger offer by Oracle Corp. (ORCL) for $9 billion

- Kate Spade & Co. merger offer by Coach Inc. (COH) for $2 billion

While these few handfuls of deals represent over $300 billion in disappearing stock, as long as corporate profits remain strong, interest rates low, and valuations reasonable, there will likely continue to be trillions of dollars in stocks being purchased by corporations. This continued vigorous M&A activity should provide further healthy support to stock prices.

Admittedly, there will come a time when profits will collapse, interest rates will spike, valuations will get stretched, sentiment will become euphoric, and/or supply of stock will flood the market (see Don’t be a Fool, Follow the Stool). When the balance of these factors turn negative, the risk profile for stock prices will obviously become less desirable. Until then, I will let the skeptics and bears ignore the healthy economic vital signs and call for the death of a healthy patient (stock market). In the meantime, I will continue focus on the basics of math and offer my economics textbook to the doubters.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own AAPL, ABT, INTC, MSFT, T, and certain exchange traded funds, but at the time of publishing SCM had no direct position in SNAP, TWX, MON, KATE, N, MBLY, MJN, STJ, LNKD, NXPI, BAYRY, BTI, QCOM, ORCL, COH, RAI, Reckitt Benckiser Group, any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Stock Market Tug-of-War

Image by © Royalty-Free/Corbis

Some things never change. There are several certainties in life, including death and taxes. And when it comes to investing, there are several other certainties: the never-ending existence of geopolitical concerns, and incessant worries over Fed policy.

Let’s face it, since the dawn of mankind, humans have been programmed to worry, whether it stemmed from avoiding a man-eating lion or foraging for food to survive (see Controlling the Investment Lizard Brain). Investors function in much the same way.

There is always a constant tug-of-war between bulls and bears, and if you are obsessed with following the relentless daily headlines about a Grexit (European Greek Exit) and an imminent Federal Reserve rate hike, you like many other investors will continue to experience sweaty palms, heart palpitations, and underperformance.

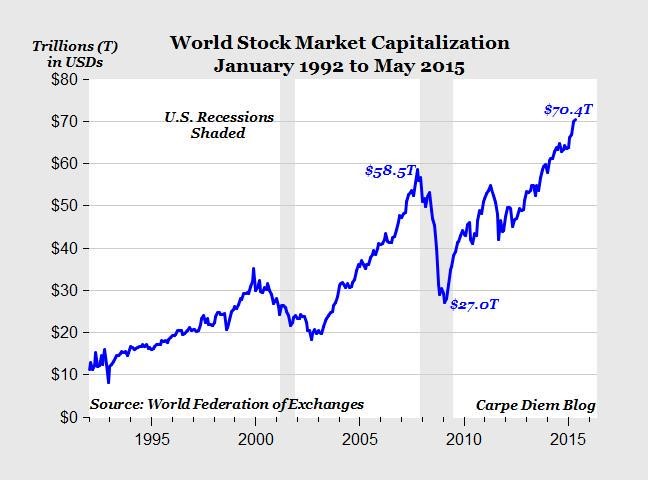

Despite the gloomy headlines, the bulls are currently winning the tug-of-war as measured by the 6-year boom in global stock prices, which has breached a record $70 trillion in value (see chart below).

Source: Mark J. Perry (Carpe Diem)

If you become hostage and react to the headlines about Greece, China, Fed policy, Ukraine, ISIS, Russia, Ebola, North Korea, QE Tapering, etc., not only are you ignoring the key positives fueling this bull market (see also Don’t Be a Fool, Follow the Stool) but you are also costing yourself a lot of money. While I have been watching the “sideliners” for years, they have missed a market driven by generationally low interest rates; improved employment picture (10% to 5%); tame inflation; steady improvement in housing market; fiscal deficit reductions; record corporate profits; record share buybacks and dividends; contrarian investor sentiment (leaving plenty of room for converts to join the party), and other fundamentally positive factors.

Yes, stocks will eventually go down by a significant amount – they always do. Stocks can temporarily go down based on the fear du jour (like the 10-20% declines in 2010, 2011, 2012, and 2014), but the nastier hits to stock markets always come from good old fashion cyclical recessions. As I’ve discussed before, there are no signs of a recession on the horizon, and the yield curve has been a great predictor of this trigger (see Dynamic Yield Curve in Digesting Stock Gains). Until then, the bears will be fighting an uphill battle.

Independent of recession timing, investing is a very challenging game, even for the most experienced professionals. The best long-term investors, including the likes of Warren Buffett and Peter Lynch, understand the never-ending geopolitical and Fed policy headlines are absolutely meaningless over the long run. However, media outlets, blogs, newspapers, and radio shows make money by peddling fear as economic and political concerns jump like a frog from one lily pad to the next. At Sidoxia we have a disciplined and systematic approach to creating diversified portfolios with our proprietary S.H.G.R. model (“sugar”) that screens for attractively valued investments. We believe this is the way to win the long-term tug-of-war.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

After 2014 Stock Party, Will Investors Have a 2015 Hangover?

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (January 2, 2015). Subscribe on the right side of the page for the complete text.

Investors in the U.S. stock market partied their way to a sixth consecutive year of gains during 2014 (S&P 500 +11.4%; Dow Jones Industrial Average +7.5%; and NASDAQ +13.4%). From early 2009, at the worst levels of the crisis, the S&P 500 has more than tripled – not too shabby. But similar to recent years, this year’s stock bubbly did not flow uninterrupted. Several times during the party, neighbors and other non-participants at the stock party complained about numerous concerns, including the Fed Tapering of bond purchases; the spread of the deadly Ebola virus; tensions in Ukraine; the rise of ISIS; continued economic weakness across the eurozone; the decline of “The Fragile Five” emerging markets (Brazil, India, Indonesia, Turkey and South Africa), and other headline grabbing stories to name just a few. In fact, the S&P 500 briefly fell -10% from its mid-September level to mid-October before a Santa Claus rally pushed the index higher by +4% in the last quarter of the year.

Even though the U.S. was partying hardy in 2014, it was not all hats and horns across all segments of the market. Given all the geopolitical trepidation and sluggish economic growth abroad, international markets as measured by the Total World Stock ETF (VT) gained a paltry +1.2% for the year. This dramatic underperformance was also seen in small capitalization stocks (Russell 2000 Index ETF – IWM), which only rose +3.7% last year, and the Total Bond Market (BND), which increased +2.9%.

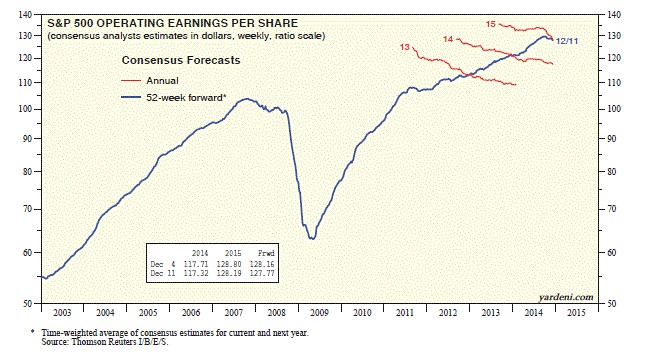

Despite these anxieties and the new Federal Reserve Chairwoman Janet Yellen removing the Quantitative Easing (QE) punchbowl in 2014, there were still plenty of festive factors that contributed to gains last year, which should prevent any hangover for stocks going into 2015. As I wrote in Don’t Be a Fool, corporate profits are the lifeblood for stock prices. Fortunately for investors, the news on this front remains positive (see chart below). As strategist Dr. Ed Yardeni pointed out a few weeks ago, profit growth is still expected to accelerate to +9.3% in 2015, despite the recent drag from plummeting oil prices on the energy sector.

Source: Dr. Ed’s Blog

While a -50% decline in oil prices may depress profits for some energy companies, the extra discretionary spending earned by consumers from $2.24 per gallon gasoline at the pump has been a cheery surprise. This consumer spending tailwind, coupled with the flow-through effect to businesses, should provide added stimulative benefit to the economy in 2015 too. Let’s not forget, this economic energy boost comes on the heels of the best economic growth experienced in the U.S. in over a decade. More specifically, the recently reported third quarter U.S. GDP (Gross Domestic Product) statistics showed growth accelerating to +5%, the highest rate seen since 2003.

Another point to remember about lower energy prices is how this phenomenon positively circulates into lower inflation and lower interest rate expectations. If energy prices remain low, this only provides additional flexibility to the Federal Reserve’s monetary policy decisions. With the absence of any substantive inflation data, Chairwoman Yellen can remain “patient” in hitting the interest rate brakes (i.e., raising the Federal Funds rate) in 2015.

Geographically, our financial markets continue to highlight our country’s standing as one of the best houses in a sluggish global growth neighborhood. Not only do we see this trend in our outperforming stock indexes, relative to other countries, but we also see this in the rising value of the U.S. dollar. It is true that American exports become less competitive internationally in a strong dollar environment, but from an investment standpoint, a rising dollar makes U.S. stock markets that much more attractive to foreign investors. To place this dynamic into better perspective, I would note the U.S. Dollar index rose by approximately +13% in 2014 against a broad basket of currencies (including the basket case Russian Rouble). With the increasing likelihood of eurozone Quantitative Easing to take place, in conjunction with loose monetary policies in large developed markets like Japan, there is a good chance the dollar will continue its appreciation in the upcoming year.

On the political front, despite the Republicans winning a clean sweep in the midterm elections, we should still continue to expect Washington gridlock, considering a Democrat president still holds the all-important veto power. But as I have written in the past (see Who Said Gridlock is Bad?), gridlock has resulted in our country sitting on a sounder financial footing (i.e., we have significantly lower deficits now), which in turn has contributed to the U.S. dollar’s strength. At the margin however, one can expect any legislation that does happen to get passed by the Republican majority led Congress will likely be advantageous for businesses and the stock market.

When Will the Party End?

What could cause the party to come to a screeching halt? While I can certainly point out some obvious potential negative scenarios (e.g., European financial mayhem, China economic speed bump, interest rate spike), history shows us it is usually unforeseen events (surprises) that cause significant downdrafts in stock market prices. The declines rarely come from factors you read in current newspaper headlines or hear on television.

Just like any party, this year is likely to include high points and low points in the financial markets – and of course some lull periods mixed in as well. However, with the economy improving and risk appetites increasing, we are bound to see more party poopers on the sidelines come join the celebration in 2015. It will be a while before the cops arrive and stop the party, so there should be plenty of time to prepare for any hypothetical hangover.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions, including positions in certain exchange traded funds positions (including BND), but at the time of publishing SCM had no direct position in VT, IWM or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Scrapes on the Sidewalk

Baron Rothschild, an 18th century British nobleman and member of the Rothschild banking family, is credited with the investment advice to “buy when there’s blood in the streets.” Well, with the Russell 2000 correcting about -14% and the S&P 500 -8% from their 2014 highs, you may not be witnessing drenched, bloody streets, but you could say there has been some “scrapes on the sidewalk.”

Although the Volatility Index (VIX – a.k.a., “Fear Gauge”) reached the highest level since 2011 last week (31.06), the S&P 500 index still hasn’t hit the proverbial “correction” level yet. Even with some blood being shed, the clock is still running since the last -10% correction experienced during the summer of 2011 when the Arab Spring sprung and fears of a Greek exit from the EU was blanketing the airwaves. If investors follow the effective 5-year investment playbook, this recent market dip, like previous ones, should be purchased. Following this “buy-the-dip” mentality since the lows experienced in 2011 would have resulted in stock advancing about +75% in three years.

If you have a more pessimistic view of the equity markets and you think Ebola and European economic weakness will lead to a U.S. recession, then history would indicate investors have suffered about 50% of the pain. Your ordinary, garden-variety recession has historically resulted in about a -20% hit to stock prices. However, if you’re in the camp that we’re headed into another debilitating “Great Recession” as we experienced in 2008-2009, then you should brace for more pain and grab some syringes of Novocaine.

If you’re seriously considering some of these downside scenarios, wouldn’t it make sense to analyze objective data to bolster evidence of an impending recession? If the U.S. truly was on the verge of recession, wouldn’t the following dynamics likely be in place?

- Two quarters of consecutive, negative GDP (Gross Domestic Property) data

- Inverted yield curve

- Rising unemployment and mass layoff announcements

- Declining corporate profits

- Hawkish Federal Reserve

The reality of the situation is the U.S. economy continues to expand; the yield curve remains relatively steep and positive; unemployment declined to 5.9% in the most recent month; corporate profits are at record levels and continue to grow; and the Fed has communicated no urgency to raise short-term interest rates in the near future. While the current headlines may not be so rosy, and the Ebola, eurozone, and Chinese markets may be giving you heartburn, nevertheless, the stock market has steadily climbed a wall of market worry over the last five years.

As the great Peter Lynch stated (see also Inside the Brain of an Investing Genius), “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” Stated differently, Value investor Seth Klarman noted, “We can predict 10 of the next two recessions,” which highlights pundits’ inabilities of accurately predicting the next downturn (see also 100-Year Flood ≠ 100-Day Flood). As Lynch also adds, rather than trying to time the market, it is better to “assume the market is going nowhere and invest accordingly.”

Now may not be the time to dive into stocks headfirst, but many stocks have fallen -10%, -20%, and -30%, so it behooves long-term investors to take advantage of the correction. It’s true that buying when there is “blood in the streets” is an optimal strategy, but facts show this is a difficult strategy to execute. Rather than get greedy, long-term investors may be better served by opportunistically buying when there are “scrapes on the sidewalk.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing with Crayons

At one level, investing can be extremely challenging if you consider the plethora of diverse and unpredictable factors such as monetary policy, fiscal policy, wars, banking crises, natural disasters, currency crises, geopolitical turmoil, Ebola, Scottish referendums, etc. On the other hand, investing (not trading or speculating) should be quite simple…like drawing stick figures with a crayon. However, simplicity does not mean laziness. Successful stock research requires rigorous due diligence without cutting corners. Once the heavy research lifting is completed, concise communication is always preferred.

In order to be succinct, investors need to understand the key drivers of stock performance. In the short run, investors may not be able to draw the directional path of stock prices, but over the long run, Peter Lynch described stock predictions best (see Inside the Investing Genius) when he stated:

“People may bet on hourly wiggles of the market but it’s the earnings that waggle the wiggle long term.”

In other words, if revenues, earnings, and most importantly cash flows go up over the long-term, then it is highly likely that stock prices will follow. Besides profits, interest rates and sentiment are other key contributing factors affecting the trajectory of future stock prices.

In high school and college, students often cram as much information into a paper with the goal of layering pages as high as possible. Typically, the heaviest papers got A’s and the lightest papers got C’s or D’s. However, as it relates to stock analysis, the opposite holds true – brevity reigns supreme.

American psychologist and philosopher William James noted, “The art of being wise is the art of knowing what to overlook.”

In our digital world of informational overload, knowing what to overlook is quite a challenge. I experienced this dynamic firsthand early on in my professional career when I was an investment analyst. When asked to research a new stock by my portfolio manager, often my inclination was to throw in the data kitchen sink into my report. Rather than boil down the report to three or four critical stock-driving factors, I defaulted to a plan of including every possible risk factor, competitor, and valuation metric. This strategy was designed primarily as a defense mechanism to hedge against a wide range of possible outcomes, whether those outcomes were probable or very unlikely. Often, stuffing irrelevant information into reports resulted in ineffectual, non-committal opinions, which could provide cosmetic wiggle room for me to rationalize any future upward or downward movement in the stock price.

Lynch understood as well as anyone that stock investing does not have to be complex rocket science:

“Everyone has the brainpower to follow the stock market. If you made it through fifth-grade math, you can do it.”

In fact, when Lynch worked with investment analysts, he ran a three-minute timer and forced the analysts to pitch stock ideas in basic terms before the timer expired.

If you went back further in time, legendary Value guru Benjamin Graham also understood brain surgery is not required to conduct successful equity analysis:

“People don’t need extraordinary insight or intelligence. What they need most is the character to adopt simple rules and stick to them.”

Similarly, Warren Buffett hammers home the idea that a gargantuan report or extravagant explanation isn’t required in equity research:

“You should be able to explain why you bought a stock in a paragraph.”

Hedge fund veteran manager Michael Steinhardt held the belief that a stock recommendation should be elegant in its simplicity as well. In his book No Bull – My Life In and Out of Markets he states that an analyst “should be able to tell me in two minutes, four things: 1) the idea; 2) the consensus view; 3) his variant perception; and 4) a trigger event.

All these previously mentioned exceptional investors highlight the basic truth of equity investing. A long, type-written report inundated with confusing charts and irrelevant data is counterproductive to the investment and portfolio management process. Outlining a stock investment thesis is much more powerful when succinctly written with a crayon.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions in certain exchange traded fund positions, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}