Posts tagged ‘diversification’

The Fallibility of Tangibility

Why do so many star athletes end up going bankrupt? Rather than building a low-cost, tax-efficient, diversified portfolio of stocks and bonds that could help generate significant income and compounded wealth over the long-term (yawn…boring), many investors succumb to the allure of over-exposing themselves to costly, illiquid, tangible assets, while assuming disproportionate risk.

After all, it’s much more exciting to brag about the purchase of a car wash, apartment building or luxury condo than it is to whip out a brokerage statement and show a friend a bond fund earning a respectable 4% yield.

Many real estate investors in my Southern California backyard (epicenter of the 2008-2009 Financial Crisis) have experienced both ruin and riches over the last few decades. The appeal and pitfalls associated with owning tangible assets like real estate are particularly exemplified with professional athletes (see also Hidden Train Wreck). Consider the fate suffered by these following individuals:

- Mike Tyson: Famous boxer Mike Tyson tore through $300 million on multiple homes, cars, jewels and pet tigers before filing for bankruptcy in 2003.

- Julius Erving: Hall of Fame NBA player Julius “Dr. J” Erving went financially belly-up in 2010 after his Celebrity Golf Club International was pushed into foreclosure. Dr. J. was also forced to auction off coveted NBA memorabilia (including championship uniforms, trophies, and rings) along with foreclosing on his personal $2 million, 6,600-square foot Utah home.

- Mark Brunell: Pro Bowl quarterback Mark Brunell was estimated to have earned over $50 million during his career. Due to failed real estate ventures and business loans, Brunell filed for bankruptcy in 2010.

- Evander Holyfield: Heavyweight boxing champion Evander Holyfield burned through a mountain of money estimated at $230 million, including a 235-acre Utah estate, which had 109 rooms and included at least one monthly electric bill of $17,000.

Caveat Emptor

Inclusion of real estate as part of a diversified portfolio makes all the sense in the world – this is exactly what we do for clients at Sidoxia. But unfortunately, many investors mistake the tangibility of real estate with “lower risk,” even though levered real estate is arguably more volatile than the stock market – evidenced by the volatility in publicly traded REIT share prices. For example, the Dow Jones SPDR REIT (RWR) declined by -78% from its 2007 high to its 2009 low versus the S&P 500 SPDR (SPY) drop of -57% over the comparable period. Private real estate investors are generally immune from the heart-pumping price volatility rampant in the public markets because they are not bombarded with daily, real-time, second-by-second pricing data over flashing red and green colored screens.

Without experiencing the emotional daily price swings, many real estate investors ignore the risks and costs associated with real estate, even when those risks often exceed those of traditional investments (e.g., stocks and bonds). Here are some of the important factors these real estate investors overlook:

Leverage: Many real estate investors don’t appreciate that the fact that 100% of a 10% investment (90% borrowed) can be wiped out completely (i.e., lose -100%), if the value of a property drops a mere -10%. Real estate owners found this lesson out the hard way during the last housing downturn and recession.

Illiquidity: Unlike a stock and bond, which merely takes a click of a mouse, buying/selling real estate can take weeks, if not months, to complete. If a seller needs access to liquidity, they may be forced to sell at unattractively low, fire-sale prices. Pricing transparency is opaque due to the variability and volume of transactions, although online services offered by Zillow Group Inc. (Z).

Costs: For real estate buyer, the list of costs can be long: appraisal fee, origination fee, pre-paid interest, pre-paid insurance, flood certification fee, tax servicing fee, credit report fee, bank processing fee, recording fee, notary fee, and title insurance. And once an investment property is officially purchased, there are costs such as property management fees, property taxes, association dues, landscaping fees and the opportunity costs of filling vacancies when there is tenant turnover. And this analysis neglects the hefty commission expenses, which generally run 5-6% and split between the buying and selling agent. Add all these costs up, and you can understand the dollars can become significant.

Concentration Risk: It’s perfectly fine to own a levered, cyclical asset in a broadly diversified portfolio for long-term investors, but owning $1.3 million of real estate in a $1.5 million total portfolio does not qualify as diversified. If a portfolio is real estate heavy, hopefully the real estate assets are at least diversified across geographies and real estate type (e.g., residential / commercial / multi-family / industrial / retail mall / mortgages / etc).

Stocks Abhorred, Gold & Real Estate Adored

With the downdraft in the stock market that started in late August, a recent survey conducted by CNBC showed how increased volatility has caused wealthy investors to sour on the stock market. More specifically, the All-America Survey, conducted by Hart-McInturff, polled 800 wealthy Americans at the beginning of October. Unsurprisingly, many investors automatically correlate temporary weakness in stocks to a lagging economy. In fact, 32% of respondents believed the U.S. economy would get worse, a 6% increase from the last poll in June, and the highest level of economic pessimism since the government shutdown in 2013 (as it turned out, this was a very good time to buy stocks). These gloom and doom views manifested themselves in skeptical views of stocks as well. Overall, 46% of the public felt it is a bad time to invest in stocks, representing a 12% gain from the last survey.

With investor appetites tainted for stocks, hunger for real state has risen. Actually, real estate was the top investment choice by a large margin, selected by 39% percent of the investors polled. Real estate has steadily gained in popularity since the depths of the recession in 2008. Jockeying for second place have been stocks and gold with the shiny metal edging out stocks by a score of 25% to 21%, respectively.

Successful long-term investors like Warren Buffett understand the best returns are earned by going against the grain. As Buffett said, “Be fearful when others are greedy and greedy when others are fearful,” and we know stock investors are fearful. Along those same lines, Bill Miller, the man who beat the S&P 500 index for 15 consecutive years (1991 – 2005), believes now is a perfect time to buy stocks. Investing in real estate is not a bad idea in the context of a diversified portfolio, but investors should not forget the fallibility of tangibility.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including SPY, but at the time of publishing, SCM had no direct position in Z, RWR, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

F.U.D. and Dividend Shock Absorbers

As the existential question remains open on whether Greece will remain a functioning entity within the eurozone, investor anxiety and manic behavior continues to be the norm. Rampant fear seems very counterintuitive for a stock market that has more than tripled in value from early 2009 with the S&P 500 index only sitting -3% below all-time record highs. Common sense would dictate that euphoric investor appetites have contributed to years of new record highs in the U.S. stock market, but that isn’t the case now. Rather, the enormous appreciation experienced in recent years can be better explained by the trillions of dollars directed towards buoyant share buybacks and mergers.

With a bull market still briskly running into its sixth year, where can we find the evidence for all this anxiety? Well, if you don’t believe all the nail biting concerns you hear from friends, family members, and co-workers about a Grexit (Greek exit from the euro), Chinese stock market bubble, Puerto Rico collapse, and/or impending Fed rate hike, then here are a few confirming data points.

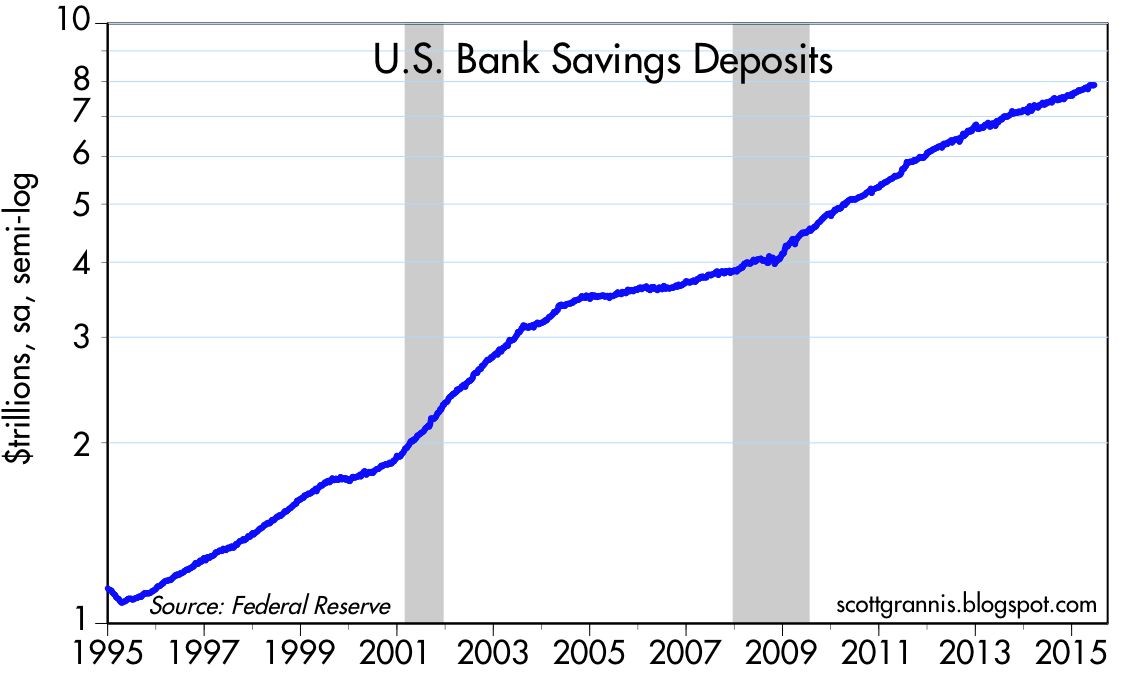

For starters, let’s take a look at the record $8 trillion of cash being stuffed under the mattress at near 0% rates in savings deposits (see chart below). The unbelievable 15% annual growth rate in cash hoarding since the turn of the century is even scarier once you consider the massive value destruction from the eroding impact of inflation and the colossal opportunity costs lost from gains and yields in alternative investments.

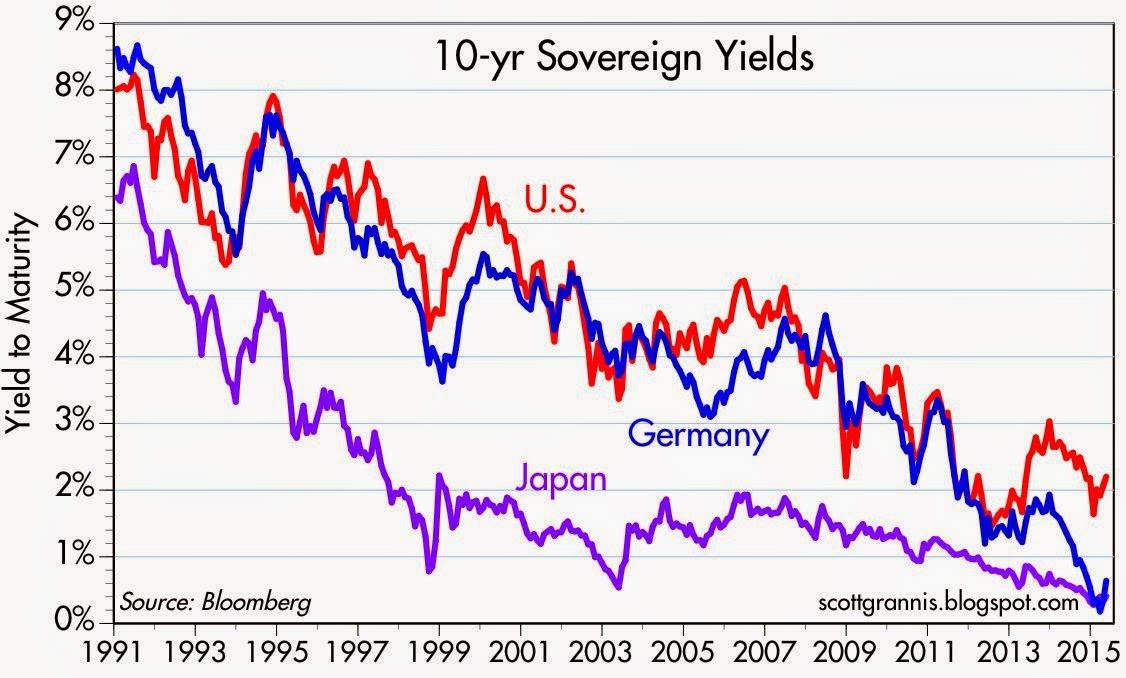

Next, you can witness the irrational risk averse behavior of investors piling into low (and negative) yielding bonds. Case in point are the 10-year yields in developing countries like Germany, Japan, and the U.S. (see chart below).

The 25-year downward trend in rates is a very scary development for yield-hungry investors. The picture doesn’t look much prettier once you realize the compensation for holding a 30-year bond (currently +3.2%) is only +0.8% more than holding the same Treasury bond for 10 years (now +2.4%). Yes, it is true that sluggish global growth and tame inflation is keeping a lid on interest rates, but these trends highlight once again that F.U.D. (fear, uncertainty, and doubt) has more to do with the perceived flight to safety and high bond prices (low bond yields).

In addition, the -$57 billion in outflows out of U.S. equity funds this year is further evidence that F.U.D. is out in full force. As I’ve noted on repeated occasions, when the tide turns on a sustained multi-year basis and investors dive head first into stocks, this will be proof that the bull market is long in the tooth and conservatism should be the default posture.

Dividend Shock Absorbers

There are always plenty of scary headlines that tempt investors to bail out of their investments. Today those alarming headlines span from Greece and China to Puerto Rico and the Federal Reserve. When the winds of fear, uncertainty, and doubt are fiercely swirling, it’s important to remember that any investment strategy should be constructed in a diversified manner that meshes with your time horizon and risk tolerance.

Consistent with maintaining a diversified portfolio, owning reliable dividend paying stocks is an important component of investment strategy, especially during volatile periods like we are experiencing currently. Sure, I still love to own high octane, non-dividend growth stocks in my personal and client portfolios, but owning stocks with a healthy stream of dividends serve as shock absorbers in bumpy markets with periodic surprise potholes.

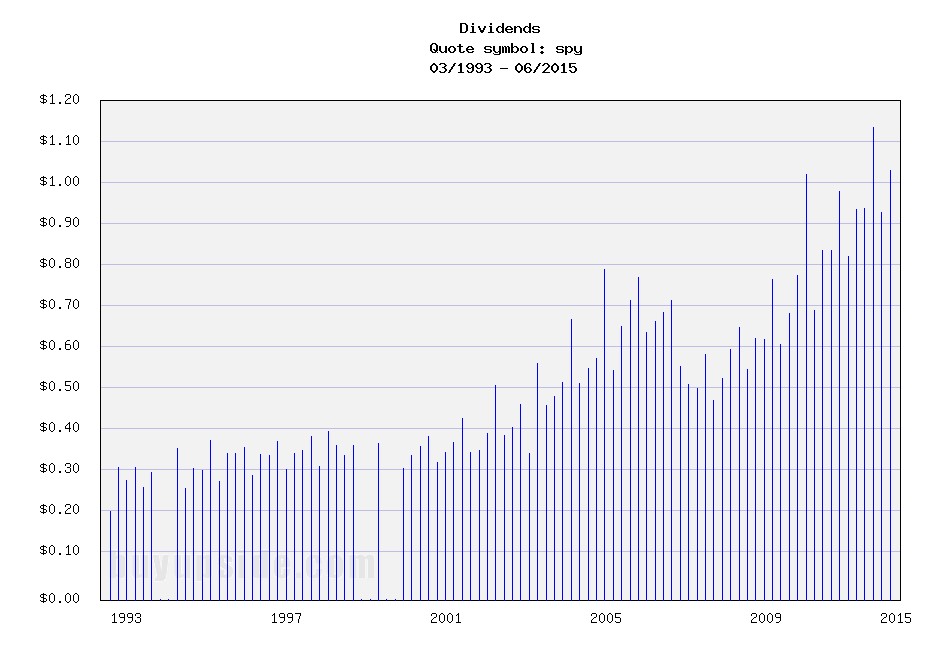

As I’ve note before, bond issuers don’t call up investors and raise periodic coupon payments out of the kindness of their hearts, but stock issuers can and do raise dividends (see chart below). Most people don’t realize it, but over the last 100 years, dividends have accounted for approximately 40% of stocks’ total return as measured by the S&P 500.

Source: BuyUpside.com

Markets will continue to move up and down on the news du jour, but dividends overall remain fairly steady. In the worst financial crisis in a generation, dividends dipped temporarily, but as I explain in a previous article (The Gift that Keeps on Giving), dividends have been on a fairly consistent 6% growth trajectory over the last two decades. With corporate dividend payout ratios well below long term historical averages of 50%, companies still have plenty of room to maintain (and grow) dividends – even if the economy and corporate profits slow.

Don’t succumb to all the F.U.D., and if you feel yourself beginning to fall into that trap, re-evaluate your portfolio to make sure your diversified portfolio has some shock absorbers in the form of dividend paying stocks. That way your portfolio can handle those unexpected financial potholes that repeatedly pop up.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and SPY, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Building Your All-Star NBA Portfolio

Image by © Royalty-Free/Corbis

You may or may not care, but the NBA (National Basketball Association) playoffs are in full swing. If you were an owner/manager of an NBA team, you probably wouldn’t pick me as a starting player on your roster – and if you did, we would need to sit down and talk. I played high school basketball (“played” is a loose term) in my youth, and even played in my early 40s against other over-aged veterans with knee braces, goggles, and headbands. Once my injuries began to pile up and my playing time was minimized by the spry, millennial team members, I knew it was time to retire and hang up my jockstrap.

The great thing about your investments is that you can create an All-Star NBA portfolio without the necessity of a salary market cap or billions of dollars like Mark Cuban. You can actually put the greatest professional players in the world (stocks/bonds) into your portfolio whether you invest $1,000 or $10,000,000. Sure, transactions costs can eat away at the smaller portfolios, but if investors are correctly managing their funds over years, and not months, then virtually everyone can create a cost-efficient elite team of stocks, bonds, and alternatives.

Now that we’ve established that anyone can create a championship caliber portfolio, the question then becomes, how does an owner go about selecting his/her team’s players? It may sound like a cliché, but diversification is paramount. Although centers Tim Duncan, Dwight Howard, Chris Bosh, Marc Gasol, and DeAndre Jordan may get a lot of rebounds for your team, it wouldn’t make sense to have those five starting centers on your team. The same principle applies to your investment portfolio.

Generally speaking, the best policy for investors is to establish exposure to a broad set of asset classes customized to your time horizon, risk tolerance, objectives, and constraints. In other words, it is prudent to have exposure to not only stocks and bonds, but other areas like real estate, commodities, alternatives, and emerging markets. Everybody has their own unique situation, and with interest rates and valuations continually changing, it makes sense that asset allocations across all individuals will be very diverse.

In basketball terms, the sizes and types of guards, forwards, and centers will be dependent on the objectives of the team’s owners/managers. For example, it is very logical to have Stephen Curry (see great video) as the starting guard for the fast-paced, highest scoring NBA team, Golden State Warriors but Curry would not be ideally suited for the slow, grind-em-up offense of the Utah Jazz (one of the lowest scoring teams in the NBA).

In order to build a consistent winning percentage for your portfolio, you need to have a systematic, disciplined process of choosing your all-star-team, which can’t just consist of picking the hottest player of the day. Not only could it be too expensive, the consequences of over-concentrating your portfolio with an expensive position can be painful….just ask Los Angeles Laker fans how they feel about overpaying for Kobe Bryant’s $23.5 million 2014-2015 salary. Investors who chased the overpriced tech sector in the late 1990s, with stock prices trading at over 100 times trailing 12-month earnings, understand how painful losses can be in the subsequent “bubble” burst.

Having a strong bench of players is crucial as well. This requires a research process that can prioritize opportunities based on quantitative and fundamental processes (at Sidoxia we use our SHGR model). Sometimes your starters get injured, fatigued, or bought out by a competitor. Interest rates, valuations, exchange rates, earnings growth rates and other economic factors are continually fluctuating, so having a bench of suitable investment ideas is critical for different financial environments.

Beating the market is a challenging endeavor, not only for individuals, but also for professionals. If you don’t believe me, then check out what Dalbar had to say about this subject in its annual report entitled, Quantitative Analysis of Investor Behavior:

Dalbar found that in 2014, the average investor in a stock mutual fund underperformed the S&P 500 by a margin of 8.19 percent. Fixed-income investors underperformed the Barclays Aggregate Bond Index by a margin of 4.81 percent.

Ouch! If you want to generate winning returns matching the likes of the 1,000-win club, which includes Gregg Popovich, Phil Jackson, and Pat Riley then you need to avoid some of the most common investor mistakes (see also 10 Ways to Destroy Your Portfolio). Chasing performance, ignoring diversification, emotionally reacting to news headlines, paying high fees, and over-trading are sure fire ways to get technical fouls and ejected from the investment game. Avoiding these mistakes and following a systematic, objective process will make you and your investment portfolio a successful all-star.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Why Buy at Record Highs? Ask the Fat Turkey

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (December 1, 2014). Subscribe on the right side of the page for the complete text.

I’ve fulfilled my American Thanksgiving duty by gorging myself on multiple helpings of turkey, mash potatoes, and pumpkin pie. Now that I have loosened my belt a few notches, I have had time to reflect on the generous servings of stock returns this year (S&P 500 index up +11.9%), on top of the whopping +104.6% gains from previous 5 years (2009-2013).

Conventional wisdom believes the Federal Reserve has artificially inflated the stock market. Given the perceived sky-high record stock prices, many investors are biting their nails in anticipation of an impending crash. The evidence behind the nagging investor skepticism can be found in the near-record low stock ownership statistics; dismal domestic equity fund purchases; and apathetic investor survey data (see Market Champagne Sits on Ice).

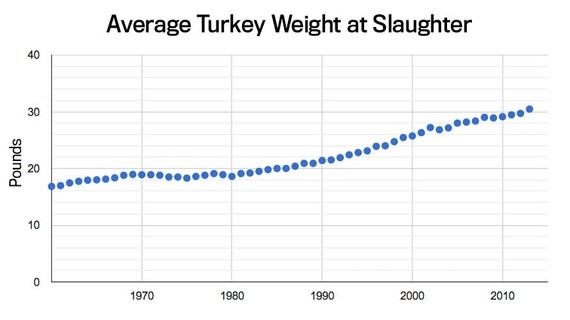

Turkey-lovers are in a great position to understand the predicted stock crash expected by many of the naysayers. As you can see from the chart below, the size of turkeys over the last 50+ years has reached a record weight – and therefore record prices per turkey:

Source: The Atlantic

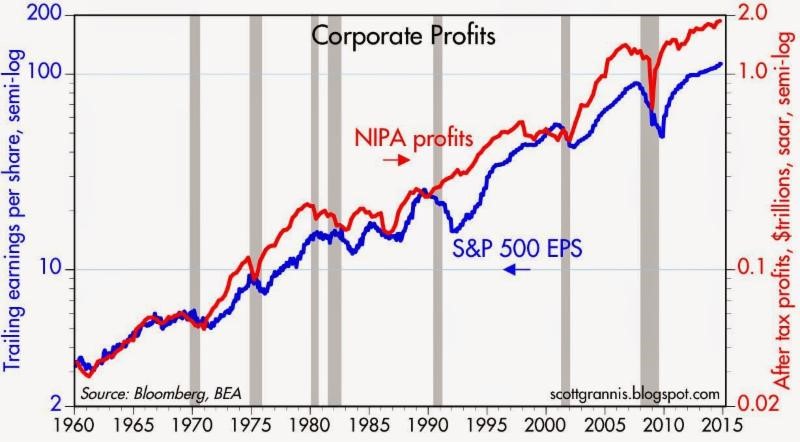

Does a record size in turkeys mean turkey meat prices are doomed for an imminent price collapse? Absolutely not. A key reason turkey prices have hit record levels is because Thanksgiving stomachs have been buying fatter and fatter turkeys every year. The same phenomenon is happening in the stock market. The reason stock prices have continued to move higher and higher is because profits have grown fatter and fatter every year (see chart below). Profits in corporate America have never been higher. CEOs are sitting on trillions of dollars of cash, and providing stock-investors with growing plump dividends (see also The Gift that Keeps on Giving), $100s of billions in shareholder friendly stock buybacks, while increasingly taking leftover profits to invest in growth initiatives (e.g., technology investments, international expansion, and job hiring).

Source: Calafia Beach Pundit

Despite record turkey prices, I will make the bold prediction that hungry Americans will continue to buy turkey. More important than the overall price paid per turkey, the statistic that consumers should be paying more attention to is the turkey price paid per pound. Based on that more relevant metric, the data on turkey prices is less conclusive. In fact, turkey prices are estimated to be -13% cheaper this year on a per pound basis compared to last year ($1.58/lb vs. $1.82/lb).

The equivalent price per pound metric in the stock market is called the Price-Earnings (P/E) ratio, which is the price paid by a stock investor per $1 of profits (or earnings). Today that P/E ratio sits at approximately 17.5x. As you can see from the chart below, the current P/E ratio is reasonably near historical averages experienced over the last 50+ years. While, all else equal, anyone would prefer paying a lower price per pound (or price per $1 in earnings), any objective person looking at the current P/E ratio would have difficulty concluding recent stock prices are in “bubble” territory.

However, investor doubters who have missed the record bull run in stock market prices over the last five years (+210% since early 2009) have clung to a distorted, overpriced measurement called the CAPE or Shiller P/E ratio. Readers of my Investing Caffeine blog or newsletters know why this metric is misleading and inaccurate (see also Shiller CAPE Peaches Smell).

Don’t Be an Ostrich

While prices of stocks arguably remain reasonably priced for many Baby Boomers and retirees, the conclusion should not be to gorge 100% of investment portfolios into stocks. Quite the contrary. Everyone’s situation is unique, and every investor should customize a globally diversified portfolio beyond just stocks, including areas like fixed income, real estate, alternative investments, and commodities. But the exposures don’t stop there, because in order to truly have the diversified shock absorbers in your portfolio necessary for a bumpy long-term ride, investors need exposure to other areas. Such areas should include international and emerging market geographies; a diverse set of styles (e.g., Value, Growth, Blue Chip dividend-payers); and a healthy ownership across small, medium, and large equities. The same principles apply to your bond portfolio. Steps need to be taken to control credit risk and interest rate risk in a globally diversified fashion, while also providing adequate income (yield) in an environment of generationally low interest rates.

While I’ve spent a decent amount of time talking about eating fat turkeys, don’t let your investment portfolio become stuffed. The year-end time period is always a good time, after recovering from a food coma, to proactively review your investments. While most non-vegetarians love eating turkey, don’t be an investment ostrich with your head in the sand – now is the time to take actions into your own hands and make sure your investments are properly allocated.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own a range of positions in certain exchange traded fund positions, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Pain of Diversification

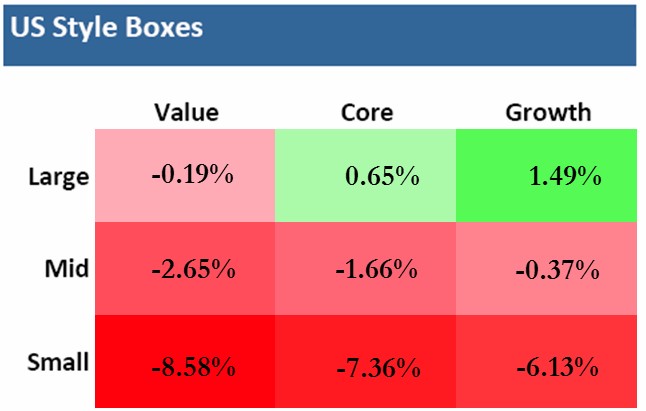

The oft-quoted tenet that diversification should be the cornerstone of any investment strategy has come under assault in the third quarter. As you can see from the chart below, investors could run, but they couldn’t hide. The Large Cap Growth category was the major exception, thanks in large part to Apple Inc.’s (AAPL) +8% appreciation. More specifically, seven out of the nine Russell Investments style boxes were in negative territory for the three month period. The benefits of diversification look even worse, if you consider other large asset classes and sectors such as the Gold/Gold Miners were down about -14% (GDX/GLD); Energy -9% (XLE); Europe-EAFE -6% (EFA); Utilities -5% (XLU); and Emerging Markets -4% (EEM).

*Results are for Q3 – 2014 (Source: Vanguard Group, Inc. & Russell Investments)

On the surface, everything looks peachy keen with all three major indices posting positive Q3 appreciation of +1.3% for the Dow, +0.6% for S&P 500, and +1.9% for the NASDAQ. It’s true that over the long-run diversification acts like shock absorbers for economic potholes and speed bumps, but in the short-run, all investors can hit a stretch of rough road in which shock absorbers may seem like they are missing. Over the long-run, you can’t live without diversification shocks because your financial car will eventually breakdown and the ride will become unbearable.

What has caused all this underlying underperformance over the last month and a half? The headlines and concerns change daily, but the -5% to -6% pullback in the market has catapulted the Volatility Index (VIX or “Fear Gauge”) by +85%. The surge can be attributed to any or all of the following: a slowing Chinese economy, stagnant eurozone, ISIS in Iraq, bombings in Syria, end of Quantitative Easing (QE), impending interest rate hikes, mid-term elections, Hong Kong protests, proposed tax inversion changes, security hacks, rising U.S. dollar, PIMCO’s Bill Gross departure, and a half dozen other concerns.

In general, pullbacks and corrections are healthy because shares get transferred out of weak hands into stronger hands. However, one risk associated with these 100 day floods (see also 100-Year Flood ≠ 100-Day Flood) is that a chain reaction of perceptions can eventually become reality. Or in other words, due to the ever-changing laundry list of concerns, confidence in the recovery can get shaken, which in turn impacts CEO’s confidence in spending, and ultimately trickles down to employees, consumers, and the broader economy. In that same vein, George Soros, the legendary arbitrageur and hedge fund manager, has famously written about his law of reflexivity (see also Reflexivity Tail Wags Dog). Reflexivity is based on the premise that financial markets continually trend towards disequilibrium, which is evidenced by repeated boom and bust cycles.

While, at Sidoxia, we’re still finding more equity opportunities amidst these volatile markets, what this environment shows us is conventional wisdom is rarely correct. Going into this year, the consensus view regarding interest rates was the economy is improving, and the tapering of QE would cause interest rates to go significantly higher. Instead, the yield on the 10-Year Treasury Note has gone down significantly from 3.0% to 2.3%. The performance contrast can be especially seen with small cap stocks being down-10% for the year and the overall Bond Market (BND) is up +3.1% (and closer to +5% if you include interest payments). Despite interest rates fluctuating near generational lows with paltry yields, the power of diversification has proved its value.

While there are multiple dynamics transpiring around the financial markets, the losses across most equity categories and asset classes during Q3 have been bloody. Nonetheless, investing across the broad bond market and certain large cap stock segments is evidence that diversification is a valuable time-tested principle. Times like these highlight the necessity of diversification gain to offset the current equity pain.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AAPL, BND, and certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in EEM, GDX, GLD, EFA, XLE, XLU, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Organizing Your Investment Basket

With the Easter bunny relaxing after a busy holiday, kids from all over are given the task of organizing the candy and money collected during their hunts. Investors are also constantly reminded that their portfolio eggs should not be solely placed in one basket either. Instead, investors are told to diversify their investments across a whole host of asset classes, geographies, styles, and sizes. In other words, this means investors should be spreading their money across commodity, real estate, international, emerging market, value, growth, small-cap, and large-cap investments. As Jason Zweig, journalist from a the Wall Street Journal points out, much of the diversification benefits can be achieved with relatively small change in the position count of a portfolio:

“As many studies have shown, at least 40% of the variability in returns can be reduced by moving from a single company to 20. Once a portfolio contains 20 or 30 stocks, adding more does little to damp the fluctuations in wealth over time.”

But wait. Going from one banking stock to 20 banking stocks is not going to provide you with the proper diversification you want or need. Rather, what is as important as investing across asset class, geography, style, and size, is to follow the individual stock strategies of guru Peter Lynch. In order to put his performance into perspective, Lynch’s Fidelity Magellan fund averaged +29% per year from 1977 – 1990 – almost doubling the return of the S&P 500 index for that period.

More specifically, to achieve these heroic returns, Lynch divided the stocks in his fund into the following categories:

Slow Growers: This group of stocks wasn’t Lynch’s favorite because these companies typically operate in mature industries with limited expansion opportunities. For these single-digit EPS growers, Lynch focused more on identifying high dividend-paying stocks that were trading at attractive valuations. In particular, he paid attention to a dividend-adjusted PEG ratio (Price-to-Earnings Growth). A utility company would be an example of a “Slow Grower.”

Stalwarts: These are large established companies that still have the ability to achieve +10% to +12% annual earnings growth regardless of the economic cycle. Lynch liked these stocks especially during recessions and downturns. Valuations are still very important for Stalwarts, and many of them pay dividends. An investor may not realize a “home run” with respect to returns, but a +30% to 50% return over a few years is not out of the question, if selected correctly. Former examples of “Stalwarts” include Coca Cola (KO) and Procter & Gamble (PG).

Fast Growers: This categorization applies to small aggressive firms averaging about +20% to +25% annual earnings growth. While “Fast Growers” offer the most price appreciation potential, these stocks also offer the most risk, especially once growth/momentum slows. If timed correctly, as Lynch adeptly achieved, these stocks can increase multi-fold in value. The great thing about these “Fast Growers” is they don’t have to reside in fast growth industries. Lynch actually preferred market share gainers in legacy industries.

Cyclicals: These companies tend to see their sales and profits rise and fall with the overall economic cycle. The hyper-sensitivity to economic fluctuations makes the timing on these stocks extremely tricky, leading to losses and tears – especially if you get in too late or get out too late. To emphasize his point, Lynch states, “Cyclicals are like blackjack: stay in the game too long and it’s bound to take all your profit.” The other mistake inexperienced investors make is mistaking a “Cyclical” company as a “Stalwart” at the peak of a cycle. Examples of cyclical industries include airline, auto, steel, travel, and chemical industries.

Turnarounds: Lynch calls these stocks, “No Growers,” and they primarily of consist of situations like bail-outs, spin-offs, and restructurings. Unlike cyclical stocks, “Turnarounds” are usually least sensitive to the overall market. Even though these stocks are beaten down or depressed, they are enormously risky. Chyrysler, during the 1980s, was an example of a favorable Lynch turnaround.

Asset Plays: Overlooked or underappreciated assets such as real estate, oil reserves, patented drugs, and/or cash on the balance sheet are all examples of “Asset Plays” that Lynch would consider. Patience is paramount with these types of investments because it may take considerable time for the market to recognize such concealed assets.

Worth noting is that not all stocks remain in the same Lynch category. Apple Inc. (AAPL) is an example of a “Fast Grower” that has migrated to “Stalwart” or “Slow Grower” status, therefore items such as valuation and capital deployment (dividends and share buyback) become more important.

Peter Lynch’s heroic track record speaks for itself. Traditional diversification methods of spreading your eggs across various asset class baskets is useful, but this approach can be enhanced by identifying worthy candidates across Lynch’s six specific stock categories. Hunting for these winners is something Lynch and the Easter bunny could both agree upon.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and AAPL, but at the time of publishing SCM had no direct position in KO, PG, Chrysler, Fidelity Magellan, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Political Art of Investment Commentators

There are approximately 2 billion people surfing the internet globally and over 150 million bloggers (source: blogpulse.com) spewing their thoughts out into cyberspace. Throw in economists, strategists, columnists, and the talking heads on television, and you can sleep comfortably knowing there will never be a shortage of opinions for investors to sift through. The real question regarding the infinite number of ideas floating around from the “market commentators” is how useful or harmful is all this information? These diverse points of view, like guns, can be useful or dangerous – depending on an investor’s experience and knowledge level. Deciphering the nuances and variances of investment opinions can be very challenging for an untrained investing eye or ear. While there are plenty of diamonds in the rough to be discovered in the investment advice buffet, there are also a plethora of landmines and booby traps that could explode investment portfolios – especially if these volatile opinions are not handled with care.

No Credentials Required

Unlike dentists, lawyers, accountants, or doctors, becoming a market commentator requires little more than a pulse. All a writer, squawker, or blogger really needs is an internet connection, a keyboard, and something interesting or provocative to talk about. Are any credentials required to blast toxic gibberish to the millions among the masses? Unfortunately there are no qualifications required…scary thought indeed.

In order to successfully navigate the choppy investment opinion waters, investors need to be self-aware enough to answer the following key questions:

• What is your investment time horizon?

• What is your risk tolerance? (see also Sleeping like a Baby)

With these answers in hand, you can now begin to evaluate the credibility and track record of the market commentators and match your personal time horizon and risk profile appropriately. Ideally, investors would seek out prudent long-term counsel, but in this instant gratification society we live in, immediate fear and greed sells advertisements and attracts viewers. Even if media producers and editors of all stripes believed focusing on multi-year time horizons is most beneficial for investors, some serious challenges arise. The brutal reality is that concentrating on the lackluster long-term does not generate a lot of advertisement revenue or traffic. The topics of dollar-cost averaging, asset allocation, diversification, and rebalancing are about as exciting as watching an infomercial marathon (OK, actually this is quite funny) or paint dry. More interesting than the sleepy, uninspiring topics of long-term value creation are stories about terrorist threats, DSK sex scandals, Bernie Madoff Ponzi schemes, currency crises, hacking misconduct, bailouts, tsunamis, earthquakes, hurricanes, 50-day moving averages…OK, you get the idea.

Focus on Long-Term and Do Not Succumb to Short-Termism

Regrettably, there is a massive disconnect between the nano-second time horizons of market commentators and the time horizons of most investors. Moreover, this short-termism dispersed instantaneously via Facebook, Google (GOOG), Twitter, and traditional media channels, has sadly infected the psyches and investment habits of ordinary investors. If you don’t believe me, then check out some of the John Bogle’s work, which shows how dramatically investors underperform the benchmark thanks to emotionally charged reactions (see Fees, Exploitation, and Confusion Hammer Investors).

Although myopic short-termism is not the solution, extending time horizons too long does no good for investors either. As economist John Maynard Keynes astutely noted, “In the long run we are all dead.” But surely bloggers and pundits alike could provide perspectives in multiple year timeframes, rather than in multiple hours. Investors would be served best by turning off the TV, PC, or cell phone, and using the resulting free time to read a good book about the virtues of patient investing from successful long-term investors. Stuffing cash under the mattress, parking it in a 0.5% CD, or panicking into sub-2% Treasuries probably is not going to get the job done for your whole portfolio when inflation, longer life expectancies, and the unsustainable trajectory of entitlements destroy the value of your hard-earned nest egg.

Investment Commentators Look into Politician Mirror

Heading into a heated election year with volatility reaching historic heights in the financial markets, both politicians and investment commentators have garnered a great deal of the media spotlight. With the recent heightened interest in the two fields, some common characteristics between politicians and investment commentators have surfaced. Here are some of the similarities:

- Politicians have a short-term incentives to get re-elected and not get fired, even if there is an inherent conflict with the long-term interest of their constituents; Investment commentators have a short-term incentives to follow the herd and not get fired, even if there is an inherent conflict with the long-term interest of their constituents;

- Many politicians have extreme views that conflict with peers because blandness does not get votes; Many investment commentators have extreme views that conflict with peers because blandness does not get votes;

- Many politicians lack practical experience that could benefit their followers, but the politicians have the gift of charisma to mask their inexperience; Many investment commentators lack practical experience that could benefit their followers, but the commentators have the gift of charisma to mask their inexperience;

Investing has never been so difficult, and also has never been so important, which behooves investors to carefully consider portfolio actions taken based on a very volatile and inconsistent opinions from a group of bloggers, economists, strategists, columnists, and various other media commentators. Investors are bombarded with an avalanche of ever-changing daily data, much of which is irrelevant and should be ignored by long-term investors. As you weigh the precious value of your political votes in the upcoming election season, I urge you to back the candidates that represent your long-term interests. With regard to the financial markets, I also urge you to back the investment commentators that support your long-term interests – the success of your financial future depends on it.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and GOOG, but at the time of publishing SCM had no direct position in Facebook, Twitter, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page

Sleeping like a Baby with Your Investment Dollars

Amidst the recent, historically high volatility in the financial markets, there have been a large percentage of investors who have been sleeping like a baby – a baby that stays up all night crying! For some, the dream-like doubling of equity returns achieved from the first half of 2009 through the first half of 2011 quickly turned into a nightmare over the last few weeks. We live in an inter-connected, globalized world where news travels instantaneously and fear spreads like a damn-bursting flood. Despite the positive returns earned in recent years, the wounds of 2008-2009 (and 2000 to a lesser extent) remain fresh in investors’ minds. Now, the hundred year flood is expected every minute. Every European debt negotiation, S&P downgrade, or word floating from Federal Reserve Chairman Ben Bernanke’s lips, is expected to trigger the next Lehman Brothers-esque event that will topple the global economy like a chain of dominoes.

Volatility Victims

The few hours of trading that followed the release of the Federal Reserve’s August policy statement is living proof of investors’ edginess. After initially falling approximately -400 points in a 30 minute period late in the day, the Dow Jones Industrial Average then climbed over +600 points in the final hour of trading, before experiencing another -400 point drop in the first hour of trading the next day. Many of the day traders and speculators playing with the explosively leveraged exchange traded funds (e.g., TNA, TZA, FAS, FAZ), suffered the consequences related to the panic selling and buying that comes with a VIX (Volatility Index) that climbed about +175% in 17 days. A VIX reading of 44 or higher has only been reached nine times in the last 25 years (source: Don Hays), and is normally associated with significant bounce-backs from these extreme levels of pessimism. Worth noting is the fact that the 2008-2009 period significantly deteriorated more before improving to a more normalized level.

Keys to a Good Night’s Sleep

The nature of the latest debt ceiling negotiations and associated Standard & Poor’s downgrade of the United States hurt investor psyches and did little to boost confidence in an already tepid economic recovery. Investors may have had some difficulty catching some shut-eye during the recent market turmoil, but here are some tips on how to sleep comfortably.

• Panic is Not a Strategy: Panic selling (and buying) is not a sustainable strategy, yet we saw both strategies in full force last week. Emotional decisions are never the right ones, because if they were, investing would be quite easy and everyone would live on their own personal island. Rather than panic-sell, investments should be looked at like goods in a grocery store – successful long-term investors train themselves to understand it is better to buy goods when they are on sale. As famed growth investor Peter Lynch said, “I’m always more depressed by an overpriced market in which many stocks are hitting new highs every day than by a beaten-down market in a recession.”

• Long-Term is Right-Term: Everybody would like to retire at a young age, and once retired, live like royalty. Admirable goals, but both require bookoo bucks. Unless you plan on inheriting a bunch of money, or working until you reach the grave, it behooves investors to pull that money out from under the mattress and invest it wisely. Let’s face it, entitlements are going to be reduced in the future, just as inflation for food, energy, medical, leisure and other critical expenses continue eroding the value of your savings. One reason active traders justify their knee-jerk actions and derogatory description of long-term investors is based on the stagnant performance of U.S. equity markets over the last decade. Nonetheless, the vast number of these speculators fail to recognize a more than tripling in average values in markets like Brazil, India, China, and Russia over similar timeframes. Investing is a global game. If you do not have a disciplined, systematic long-term investment strategy in place, you better pray you don’t lose your job before age 70 and be prepared to eat Mac & Cheese while working as a Wal-Mart (WMT) greeter in your 80s.

• Diversification: Speaking of sleep, the boring topic of diversification often puts investors to sleep, but in periods like these, the power of diversification becomes more evident than ever. Cash, metals, and certain fixed income instruments were among the investments that cushioned the investment blow during the 2008-2009 time period. Maintaining a balanced diversified portfolio across asset classes, styles, size, and geographies is crucial for investment survival. Rebalancing your portfolio periodically will ensure this goal is achieved without taking disproportionate sized risks.

• Tailored Plan Matching Risk Tolerance: An 85 year-old wouldn’t go mountain biking on a tricycle, and a 10 year-old shouldn’t drive a bus to his fifth grade class. Sadly, in volatile times like these, many investors figure out they have an investment portfolio mismatched with their goals and risk tolerance. The average investor loves to take risk in up-markets and shed risk in down-markets (risk in this case defined as equity exposure). Regrettably, this strategy is designed exactly backwards for long-term investors. Historically, actual risk, the probability of permanent losses, is much lower during downturns; however, the perceived risk by average investors is viewed much worse. Indeed, recessions have been the absolute best times to purchase risky assets, given our 11-for-11 successful track record of escaping post World War II downturns. Could this slowdown or downturn last longer than expected and lead to more losses? Absolutely, but if you are planning for 10, 20, or 30 years, in many cases that issue is completely irrelevant – especially if you are still adding funds to your investment portfolio (i.e., dollar-cost averaging). On the flip side, if an investor is retired and entirely dependent upon an investment portfolio for income, then much less attention should be placed on risky assets like equities.

If you are having trouble sleeping, then one of two things is wrong: 1.) You are taking on too much risk and should cut your equity exposure; and/or 2.) You do not understand the risk you are taking. Volatile times like these are great for reevaluating your situation to make sure you are properly positioned to meet your financial goals. Talking heads on TV will tell you this time is different, but the truth is we have been through worse times (see History Never Repeats, but Rhymes), and lived to tell the tale. All this volatility and gloom may create anxiety and cause insomnia, but if you want to quietly sleep through the noise like a content baby, make yourself a long-term financial bed that you can comfortably sleep in during good times and bad. Focusing on the despondent headline of the day, and building a portfolio lacking diversification will only lead to panic selling/buying and results that would keep a baby up all night crying.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including emerging market ETFs) and WMT, but at the time of publishing SCM had no direct position in TNA, TZA, FAS, FAZ, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

O’Neil Swings for the Fences

Approaches used in baseball strategy are just as varied as they are in investing. Some teams use a “small ball” approach to baseball, in which a premium is placed on methodically advancing runners around the bases with the help of bunts, bases on ball, stolen bases, sacrifice flies, and hit-and- run plays. Other teams stack their line-up with power-hitters, with the sole aim of achieving extra base hits and home runs.

Investing is no different than baseball. Some investors take a conservative, diversified value-approach and seek to earn small returns on a repeated basis. Others, like William J. O’Neil, look for the opportunities to knock an investment out of the park. O’Neil has no problem of concentrating a portfolio in four or five stocks. Warren Buffett talks about how Ted Williams patiently waited for fat pitches–O’Neil is very choosy too, when it comes to taking investment swings.

The Making of a Growth Guru

Born in Oklahoma and raised in Texas, William O’Neil has accomplished a lot over his 53-year professional career. After graduating from Southern Methodist University, O’Neil started his career as a stock broker in the late-1950s. Soon thereafter in 1963, at the ripe young age of 30, O’Neil purchased a seat on the New York Stock Exchange (NYX) and started his own company, William O’Neil + Co. Incorporated. Ambition has never been in short supply for O’Neil – following the creation of his firm, O’Neil the investment guru put on his computer science hat and went onto pioneer the field of computerized investment databases. He used his unique proprietary data as a foundation to unveil his next entrepreneurial baby, Investor’s Business Daily, in 1984.

O’Neil’s Secret Sauce

The secret sauce behind O’Neil’s system is called CAN SLIM®. O’Neil isn’t a huge believer in stock diversification, so he primarily focuses on the cream of the crop stocks in upward trending markets. Here are the components of CAN SLIM® that he searches for in winning stocks:

C Current Quarterly Earnings per Share

A Annual Earnings Increases

N New Products, New Management, New Highs

S Supply and Demand

L Leader or Laggard

I Institutional Sponsorship

M Market Direction

Rebel without a Conventional Cause

In hunting for the preeminent stocks in the market, the CAN SLIM® method uses a blend of fundamental and technical factors to weed out the best of the best. I may not agree with everything O’Neil says in his book, How to Make Money in Stocks, but what I love about the O’Neil doctrine is his maverick disregard of the accepted modern finance status quo. Here is a list of O’Neil’s non-conforming quotes:

- Valuation Doesn’t Matter: “The most successful stocks from 1880 to the present show that, contrary to most investors’ beliefs, P/E ratios were not a relevant factor in price movement and have very little to do with whether a stock should be bought or sold.” (see also The Fallacy of High P/Es)

- Diversification is Bad: “Broad diversification is plainly and simply a hedge for ignorance… The best results are usually achieved through concentration, by putting your eggs in a few baskets that you know well and watching them very carefully.”

- Buy High then Buy Higher: “[Buy more] only after the stock has risen from your purchase price, not after it has fallen below it.”

- Dollar-Cost Averaging a Mistake: “If you buy a stock at $40, then buy more at $30 and average out your cost at $35, you are following up your losers and throwing good money after bad. This amateur strategy can produce serious losses and weigh down your portfolio with a few big losers.”

- Technical Analysis Matters: “Learn to read charts and recognize proper bases and exact buy points. Use daily and weekly charts to materially improve your stock selection and timing.”

- Ignore TV & So-Called Experts: “Stop listening to and being influenced by friends, associates, and the continuous array of experts’ personal opinions on daily TV shows.”

- Stay Away from Dividends: “Most people should not buy common stocks for their dividends or income, yet many people do.”

Managing Momentum Risk

Although O’Neil’s CAN SLIM® investment strategy does not rely on a full-fledged, risky style of momentum investing (see Riding the Momentum Wave), O’Neil’s investment approach utilizes very structured rules designed to limit downside risk. Since true O’Neil disciples understand they are dealing with flammable and volatile hyper-growth companies, O’Neil always keeps a safety apparatus close by – I like to call it the 8% financial fire extinguisher rule. O’Neil simply states, “Investors should definitely set firm rules limiting the loss on the initial capital they have invested in each to an absolute maximum of 7% or 8%.” If a trade is not working, O’Neil wants you to quickly cut your losses. As the “M” in CAN SLIM® indicates, downward trending markets make long position gains very challenging to come by. Raising cash and cutting margin is the default strategy for O’Neil until the next bull cycle begins.

While some components of William O’Neil’s “cup and handle” teachings (see link)are considered heresy among various traditional financial textbooks, O’Neil’s lessons and CAN SLIM® method shared in How to Make Money in Stocks provide a wealth of practical information for all investors. If you want to add a power-hitting element to your investing game and hit a few balls out of the park, it behooves you to invest some time in better familiarizing yourself with the CAN SLIM® teachings of William O’Neil.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Wade Slome, President of Sidoxia Capital Management (SCM), worked at William O’Neil + Co. Incorporated in 1993-1996. SCM and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in NYX or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Another Year, Another Decade

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}