Posts tagged ‘demographics’

Investors Slowly Waking to Technology Tailwinds

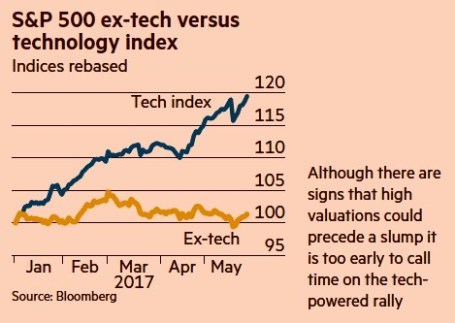

In recent years, investors have been overwhelmingly been distracted by geopolitical headlines and risk aversion caused by the worst financial crisis in a generation. In the background, the tailwinds of technological innovation have been silently gaining momentum. Although this topic is nothing new for Investing Caffeine followers, the outperformance of technology stocks has been pretty stunning in 2017 (see chart below), with the S&P 500 Technology sector rising almost +20% versus the Non-Tech sector eking out a little more than +1% return. Peered through the style lenses of Growth versus Value, technology’s contribution is also evident by the Russell 1000 Growth index’s 2017 outperformance over the Russell 1000 Value index by +11% (approximately +14% vs +3%, respectively).

Source: Bloomberg via The Financial Times

More specifically, what’s driving a significant portion of this outperformance? Robin Wigglesworth from The Financial Times highlighted a key contributing trend here:

“Facebook, Apple, Amazon and Netflix have all gained over 30 per cent this year, and Google is up 24 per cent. Their total market capitalisation now stands at $2.4 trillion. That makes them bigger than the French CAC 40 or Germany’s Dax, and nearly as large as the FTSE 100.”

Technology’s domination has been even more impressive since the cycle bottom of stock prices in 2009, if one contrasts the stark difference in the performance of the tech-heavy NASDAQ versus the more sector-balanced S&P 500. Over this timeframe, the NASDAQ has more than quadrupled in value and beaten the S&P 500 by more than +120%.

While the mass media likes to talk about technology bubbles, artificial money printing by global central banks, and imminent recessions, for years I have been highlighting the importance of the technology revolution and its beneficial impact on stock prices. Here are a few examples:

Technology Does Not Sleep in a Recession (2009)

Technology Revolution Raises Tide (2010)

NASDAQ and the R&D Tech Revolution (2014)

NASDAQ 5,000…Irrational Exuberance Déjà Vu? (2014)

The Traitorous 8 and Birth of Silicon Valley (2016)

As I have explained in many of my previous writings, the important factors of technology, globalization, and demographics have been the key driving forces behind the stock bull market and multi-decade decline in interest rates – not Quantitative Easing (QE) and/or rising debt levels.

Eventually, undoubtedly, euphoria and over-investment will lead to a cyclically-driven recession caused by excess capacity (supply exceeding demand). Regardless of the timing of future economic cycles, the continued multi-generational advance in new technological innovations will continue to drive economic growth, disinflation, improved standards of living, and higher stock prices. Until the animal spirits of the masses fully embrace this technological trend, Sidoxia and its clients will enjoy the tailwind of innovation as I continue to discover attractive investment opportunities.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own FB, AAPL, AMZN, GOOG/L, certain exchange traded funds, and short position in NFLX, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Flat Pancakes & Dividends

Over the last 18 months, stock prices have been flat as a pancake. Absent a few brief China and recessionary scares, the Dow Jones Industrial Average index has spent most of 2015 and 2016 trading between the relatively tight levels of 17,000 – 18,000. Record corporate profits and faster growth than other developed and developing markets have created a tug-of-war with countervailing factors. A strong dollar, reversal in monetary policy, geopolitical turmoil, and volatile commodity markets have produced a neutralizing struggle among corporate executives with deep financial pockets and short arms. In this environment, share buybacks, stable profit margins, and growing dividends have taken precedence over accelerated capital investments and expensive new-hires.

With flat stock prices and interest rates at unprecedented low levels, it’s during times like these that stock investors really appreciate the appetizing flavor of stable, growing dividends. To this day, I still find it almost impossible to fathom how investors are burning money by irrationally speculating in $7 trillion in negative interest rate bonds (see Retire at Age 90).

Historically there are very few periods in which stock dividend yields have exceeded bond yields (2.1% S&P yield vs. 1.8% 10-Year Treasury yield). As I showed in my Dividend Floodgates article, for roughly 50 years (1960 – 2010), the yield on the 10-Year Treasury Notes have exceeded the dividend yield on stocks (S&P 500) – that longstanding trend does not hold today.

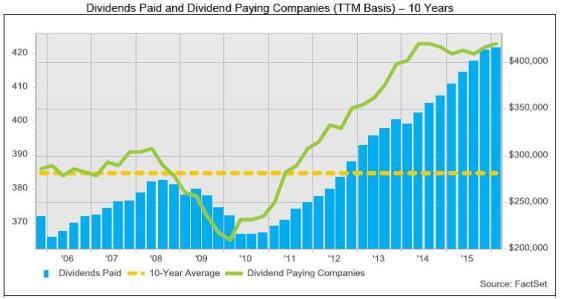

In the face of the competitive stock market, several trends are contributing to the upward trajectory in dividend payments (see chart below).

#1.) Corporate profits (ex-Energy) are growing and at/near record levels. Earnings are critical in providing fertile ground for dividend growth.

#2.) Demographics, plain and simple. As 76 million Baby Boomers transition into retirement, their income needs escalate. These shareholders whine and complain to corporate executives to share the spoils and increase dividends.

#3.) Low interest rates and disinflation are shrinking the available pool of income generating assets. As I pointed out above, when trillions of dollars are getting thrown into negative yielding investments, many investors are flocking to alternative income-generating assets…like dividend paying stocks.

Source: FactSet

The Power of Dividends (Case Studies)

Most people don’t realize it, but over the last 100 years, dividends have accounted for approximately 40% of stocks’ total return as measured by the S&P 500. In other words, using history as a guide, if you initially invested in a stock XYZ at $100 that appreciated in value to $160 (+60%) 10 years later, that stock on average would have supplied an incremental $40 in dividends (40%) over that period, creating a total return of 100%.

Rather than using a hypothetical example, here are a few stock specific illustrations that highlight the amazing power of compounding dividend growth rates. Here are two “Dividend Aristocrats” (stocks that have increased dividends for at least 25 consecutive years):

- PepsiCo Inc (PEP): PepsiCo has increased its dividend for an astonishing 44 consecutive years. Today, the dividend yield is 2.9% based on the current share price. But had you purchased the stock in June 1972 for $1.60 per share (split-adjusted), you would currently be earning a +188% dividend yield ($3.01 dividend / $1.60 purchase price), which doesn’t even account for the +6,460% increase in the share price ($104.96 per share today from $1.60 in 1972). Over that 44 year period, the split-adjusted dividend has increased from about $0.02 per share to an annualized $3.01 dividend per share today, which equates to a mind-blowing +16,153% increase. On top of the $103 price appreciation, assuming a conservative 5% dividend reinvestment rate, my estimates show investors would have received more than $60 in reinvested dividends, making the total return that much more gargantuan.

- Emerson Electric Co (EMR): Emerson Electric too has had an even more incredible streak of dividend increases, which has now extended for 59 consecutive years. Emerson currently yields a respectable 3.6% rate, but if you purchased the stock in June 1972 for $3.73 per share (split-adjusted), you would currently be earning a +51% dividend yield ($1.92 dividend / $3.73 purchase price), which doesn’t even consider the +1,423% increase in the share price ($53.31 per share today from $3.73 in 1972).

There is never a shortage of FUD (Fear, Uncertainty, and Doubt), which has kept stock prices flat as a pancake over the last couple of years, but market leading franchise companies with stable/increasing dividends do not disappear during challenging times. Record profits (ex-energy), demographics, and a scarcity of income-generating investment alternatives are all contributing factors to the increased appetite for dividends. If you want to sweeten those flat pancakes, do yourself a favor and pour some quality dividend syrup over your investment portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and PEP, but at the time of publishing had no direct position in EMR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Wealth Creation Using the Demi-Ashton Ratio

Ajay Kapur at Mirae Asset Securities is bullish on the global markets in the short-run (he sees the S&P 500 index reaching 1250 by March 2010), but even more optimistic in the long-run due to a demographic shift occurring in particular markets. According to this Chief Global Strategist, the more Demi Moores and less Ashton Kutchers we have populating the earth, the better our financial markets will perform.

Mr. Kapur’s Demi-Ashton argument is based on the belief that the higher the ratio of middle aged workers in their 40s (Demis) versus those in their 20s (Ashtons) will result in higher stock prices. Basically, those in their 40s generally have accumulated more wealth to invest and are very concerned about their impending retirement, while those in their 20s have little savings to invest and are more concerned about going to clubs and chasing the opposite sex. Seems to make logical sense.

Even though he is bullish in the domestic markets in the short-run, he sees the U.S., Canada, and Western Europe persisting through a secular bear market that began in 2000 and will last through 2015. Mr. Kapur is quick to point out these markets generally maxed-out when the Demi-Ashton ratios peaked in the 2000 timeframe. When these ratios were rising, for example as in Japan in the 1980s and the U.S. in the 1990s, the respective markets went on an upwards tear. Kapur sees emerging markets like Russia, Eastern Europe, and Latin America benefitting from the rising Demi-Ashton ratios in the coming years.

Whether his hypothesis proves correct or not, I admire the strategist’s bold call on the market direction. Typically economists and strategists herd together due to fear of being an outlier. As for Demi Moore and Ashton Kutcher, they should sleep fine with respect to their retirement plans, as long as they do not go on M.C. Hammer, Michael Jackson, or Mike Tyson spending binges.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

V-Shaped Recovery or Road to Japan Lost Decades?

The Lost Decades from the 1989 Peak

On the 6th day of March this year, the S&P 500 reached a devilish low of 666. Now the market has rebounded more than 50% over the last five months. So is this a new bull market throttled into gear, or is it just a dead-cat bounce on route to a lost two decades, like we saw in Japan?

Smart people like Nobel Prize winner and economist Paul Krugman make the argument that like Japan, the bigger risk for the U.S. is deflation (NY Times Op-Ed), not inflation.

Now I’m no Nobel Prize winner, but I will make a bold argument of why Professor Krugman is out to lunch and why we will not go in a Japanese death-like, deflationary spiral.

Let’s review why our situation is dissimilar from our South Pacific friends.

Major Differences:

- Japanese Demographics: The Japanese population keeps getting older (see UN chart), which will continue to pressure GDP growth. According to the National Institute of Population and Social Security Research, by 2055 the Japanese population will fall 30% to 90 million (equivalent to 1955 level). Over the same time frame, the number of elderly under age 65 is expected to halve. To minimize the effects of the contraction of the working population, it will be necessary both to increase labor productivity, loosen immigration laws, and to promote the employment of woman and people over 65. Japan’s population is expected to expected contraction in Japan’s labor force of almost 1% a year in 2009-13.

Source: The Financial Times/UN (Declining Workforce Per 65 Year Old)

- Bank of Japan Was Slow to React: Japan recognized the bubble occurring and as a result hiked its key lending discount rate from 1989 through May 1991. The move had the desired effect by curbing the danger of inflation and ultimately popped the Nikkei-225 bubble. Stock prices soon plummeted by 50% in 1990, and the economy and land prices began to deteriorate a year later. Belatedly, Japan’s central bank began a series of interest rate-cuts, lowering its discount rate by 500-basis points to 1% by 1995. But the Japanese economy never recovered, despite $1-trillion in fiscal stimulus programs.

- The Higher You Fly, the Farther You Fall: The relative size of the Japanese bubble was gargantuan in scale compared to what we experienced here in the United States. The Nikkei 225 Index traded at an eye popping Price-Earnings ratio of about 60x before the collapse. The Nikkei increased over 450% in the eight years leading up to the peak in 1989, from the low of about 6,850 in October 1982 to its peak of 38,957 in December 1989. Compare those extreme bubble-icious numbers with the S&P 500 index, which rose approximately a more meager 20% from the end of 1999 to the end of 2007 (U.S. peak) and was trading at more reasonable 18x’s P-E ratio.

Source: Dow Jones

- Debt Levels not Sustainable: Japan is the most heavily indebted nation in the OECD. Japan is moving towards that 200% Debt/GDP level rapidly and the last time Japanese debt went to 200% of GDP (during WWII), hyper-inflation ensued and forced many fixed income elderly into poverty. Although our debt levels have yet to reach the extremes seen by Japan, we need to recognize the inflationary pressure building. Japan’s debt bubble cannot indefinitely sustain these debt increases, leaving little option but to eventually inflate their way out of the problem.

- Banking System Prolongs Japanese Deflation: Despite the eight different stimulus plans implemented in the 1990s, Japan lacked the fortitude to implement the appropriate corrective measures in their banking system by writing off bad debts. An article from July 2003 Barron’s article put it best:

After the collapse of the property bubble, many families and businesses had debts that far exceeded their devalued assets. When a version of this happened in America in the savings-and-loan crisis, the resulting mess was cleaned up quickly. The government seized assets, sold them off, bankrupted ailing banks and businesses, sent a few crooks to jail and everything started fresh, so that deserving new businesses could get loans. The process is like a tooth extraction — painful but mercifully short. In Japan this process has barely begun. Dynamic new businesses cannot get loans, because banks use available credit to lend to bankrupt businesses, so they can pretend they are paying their debts and avoid the pain of write-offs. This is self-deception. The rotten tooth is still there. And the Japanese people know it.

The Future – Rise of the Rest: Fareed Zakaria, Newsweek editor wrote about the “Rise of the Rest” in an incredible article (See Sidoxia Website) describing the rising tide of globalization that is pulling up the rest of the world. The United States population represents only 5% of the global total, and as the technology revolution raises the standard of living for the other 95%, this trend will only accelerate the demand of scarce resources, which will create a constant inflationary headwind.

For those countries in decline, like Japan, demand destruction raises the risk of deflation, but historically the innovative foundation of capitalism has continually allowed the U.S. to grow its economic pie. Economic legislation by our Congress will help or hinder our efforts in dealing with these inflationary pressures. One way is to incentivize investment in innovation and productive technologies. Another is to expand our targeted immigration policies towards attracting college educated foreigners, thereby relieving aging demographics pressures (as seen in Japan). These are only a few examples, but regardless of political leanings, our country has survived through wars, assassinations, terrorist attacks, banking crises, currency crises, and yes recessions, to only end up in a stronger global position.

This crisis has been extremely painful, but so have the many others we have survived. I believe time will heal the wounds and we will eventually conquer this crisis. I’m confident that historians will look at the coming years in favorable light, not the lost decades of pain as experienced in Japan.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

{kind=link}