Posts tagged ‘Dell’

M&A Bankers Away as Elephant Hunters Play

With trillions in cash sitting in CEO and private equity wallets, investment bankers have been chasing mergers & acquisitions with a vengeance. Unfortunately for the bankers, investor skittishness has slowed merger activity in the boardroom. Rather than aggressively stalk corporate prey, bidders look more like deer in headlights. However, animal spirits are not completely dead. Some board members have seen the light and realize the value-destroying characteristics of idle cash in a near-zero interest rate environment, so they have decided to go elephant hunting. During a nine day period alone in the first quarter of 2013, a total of $87.7 billion in elephant deals were announced:

- HJ Heinz Company (HNZ – $27.4 billion) – February 14, 2013 – Bidder: Berkshire Hathaway (BRKA)/ 3G Capital Partners.

- Virgin Media Inc. (VMED – $21.9 billion) – February 6, 2013 – Bidder: Liberty Global Inc. (LBTYA).

- Dell Inc. (DELL – $21.8 billion) – February 5, 2013 – Bidder: Silver Lake Partners LP, Michael Dell, Carl Icahn.

- NBCUniversal Media LLC 49% Stake (GE- $17.6 billion) – February 12, 2013 – Bidder: Comcast Corp. (CMCSA).

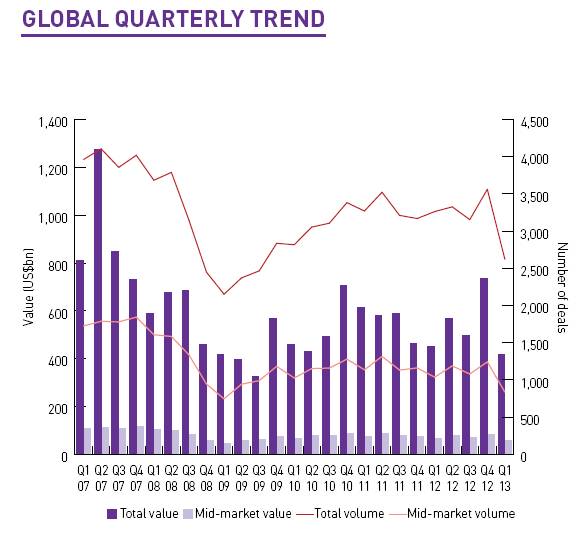

These elephant deals helped the overall M&A deal values in the United States increase by +34% in Q1 from a year ago to $167 billion (see Mergermarket report). Unfortunately, the picture doesn’t look so good on a global basis. The overall value for global M&A deals in Q1 registered $418 billion, down -7% from the first quarter of 2012. On a transaction basis, there were a total of 2,621 deals during the first three months of the year, down -20% from 3,262 deals in the comparable period last year.

Source: Mergermarket

With central banks across the globe pumping liquidity into the financial system and the U.S. stock market near record highs, one would think buyers would be writing big M&A checks as they wrote poems about rainbows, puppy dogs, and flowers. This is obviously not the case, so why such the sour mood?

The biggest scapegoat right now is Europe. While the U.S. economy appears to be slowly-but-surely plodding along on its economic recovery, Europe continues to dig a deeper recessionary hole. Austerity-driven fiscal policies are hindering growth, and concerns surrounding a Cypriot contagion continue to grab headlines. Although the U.S. dollar value of deals was up substantially in Q1, the number of transactions was down significantly to 703 deals from 925 in Q1-2012 (-24%). Besides buyer nervousness, unfriendly tax policy could have accelerated deals into 2012, and stole business from 2013.

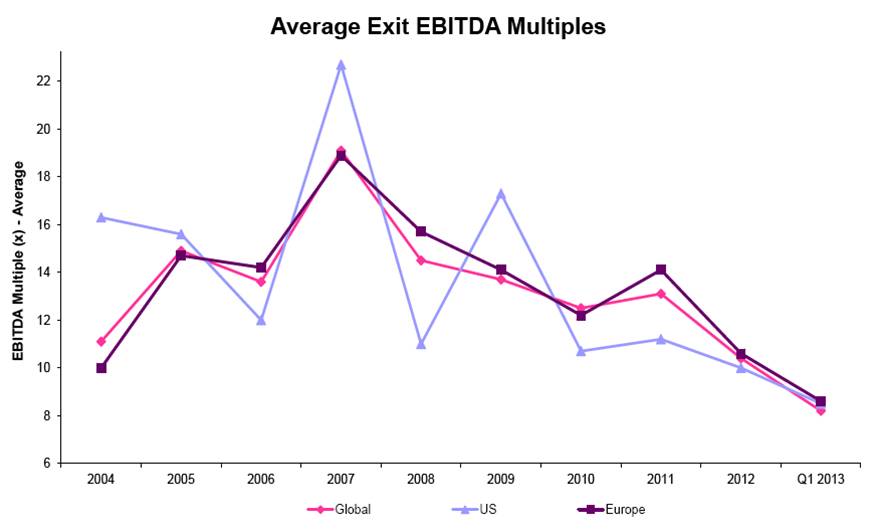

Besides lackluster global M&A volume, the record low EBITDA multiples on private equity exit prices is proof that skepticism on the sustainability of the economic recovery remains uninspired. With exit multiples at a meager level of 8.2x globally, many investors are holding onto their companies longer than they would like.

Source: Mergermarket

While merger activity has been a mixed bag, a bright spot in the M&A world has been the action in emerging markets. In 2012, the value of global transactions was essentially flat, yet emerging market deal values were up approximately +9% to $524 billion. This value exceeded the pre-crisis M&A activity level in 2007 by $73 billion, a feat not achieved in the other regions around the globe. Although emerging markets also pulled back in Q1, this region now account for 23% of total global M&A deal values.

Elephant buyout deals in the private equity space (skewed heavily by the Heinz & Dell deals) caused results to surge in this segment during the first quarter. Private equity related buyouts accounted for the highest share of global M&A activity (~21%) since 2007. However, like the overall U.S. M&A market, the number of Q1 transactions in the buyout space (372 transactions) declined to the lowest count in about four years.

Until skepticism turns into confidence, elephant deals will continue to distort results in the M&A sector (Echostar’s [DISH] play for Sprint [S] is further evidence). However, the existence of these giant transactions could be a leading indicator for more activity in the coming quarters. If bankers want to generate more fees, they may consider giving Warren Buffett a call. Here’s what he had to say after the announcement of the Heinz deal:

“I’m ready for another elephant. Please, if you see any walking by, just call me.”

Despite the weak overall M&A activity, the hunters are out there and they have plenty of ammunition (cash).

See also: Mergermarket Monthly M&A Insider Report (April 2013)

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and CMCSA, but at the time of publishing SCM had no direct position in HNZ, BRKA, VMED, LBTYA, DELL, GE, DISH, S or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Winner’s Curse: HP’s Storage Prize

Congratulations HP (HPQ)…you are the proud winner of 3Par Inc. (PAR), a relatively small enterprise storage hardware and software company, for the bargain price of 125x’s 2011 earnings! Never mind that you were late to the game in your winning $2.4 billion bid against Dell Inc. (DELL), or that you paid more than triple the price ($33 per share) that 3Par was trading just 21 days ago (< $10 per share). At least you have a storage trophy you can show all your friends and you don’t have to carry around all those heavy bills anymore.

Winner’s Curse

In bidding wars and auctions, the victor of the price battle runs the risk of earning the “Winner’s Curse.” The curse falls upon those that bid a price that exceeds an auctioned asset’s intrinsic value. How can this occur? Well for one reason, the bidder may not have complete information regarding the value of the asset. Secondly, there can be emotional factors, or ego, that play a role in the decision and price paid. Lastly, unique factors, such as strategic benefits or synergies may exist that allow one bidder to offer a higher price than other auction participants. For example, consider an exploration and production company (XYZ Drilling Co.) that is bidding for drilling lease rights in Prudhoe Bay, Alaska. If XYZ Drilling Co. has unique existing drilling operations in the same area as the auctioned assets, XYZ Drilling Co. may be in a better position of making a profitable bid relative to its peers.

HP vs. Dell – A Deeper Look

Let’s take a deeper dive into the HP bid of 3Par. While HP generates a lot of cash by selling printers, cartridges, and computers, the company doesn’t exactly have a bullet-proof balance sheet. Unlike let’s say Apple Inc. (AAPL), which has about $46 billion in cash on its balance sheet with no debt (see Steve Jobs: Gluttonous Hog), HP actually carries more debt than cash (about $20 billion in debt and $15 billion in cash). What’s more, HP has little tangible equity, once $42 billion in goodwill and intangible assets are subtracted from the total asset value of the company – leaving HP with an astronomically high ratio of 275x’s price to tangible book value. For most companies operating with a positive net cash position, making acquisitions accretive is not that difficult in this current environment – when cash is decaying away with a paltry 1% return. Unfortunately for HP, their accretive hurdle is higher than a cash-rich company. Their weighted average cost of capital is ratcheted significantly higher due to a net debt position (not net cash).

Here is the viewpoint on the deal from Ashok Kumar, senior technology analyst at Rodman & Renshaw LLC:

“It’s in excess of $3 million per employee. To put it in perspective, today 3Par has about 5 percent [market share] of the very high-end market and for these premiums to pay out, [HP] would have to expand their market share to about 25 percent or about $1.5 billion, which is 5x the projected growth rate. And all of that would come at the expense of incumbents [like] IBM, EMC, Hitachi.”

On the Bright Side

Although the price paid by Hewlett-Packard for 3Par is ridiculously too high, this deal alone is not going to break HP’s piggybank. HP is currently raking in about $8 billion in cash flow per year, so absent aggressive share buybacks or other large acquisitions, HP should be able to pay off the cost of the deal in a few quarters. Secondarily, HP does gain some synergies by integrating 3Par’s blocklevel data storage expertise into HP’s existing portfolio of other storage technologies ( i.e., StoreOnce and IBRIX). Thirdly, HP gains some strategic defensive benefits by keeping 3Par out of Dell’s hands, a potentially formidable competitor in the storage space, given the intensive overlap in customer bases between HP & Dell. Lastly, HP will no doubt be able to introduce and cross-sell 3Par products into Hewlett’s vastly larger customer distribution channels and reap the resulting rewards.

All in all, the 3Par acquisition by HP makes perfect strategic sense, however the price paid will turn out to be a much better deal for 3Par shareholders, rather than HP shareholders. HP ultimately shelled out a hefty price tag to become the victorious party in the 3Par bidding war, but rather than increasing shareholder value, HP ended up achieving the “Winner’s Curse.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in HPQ, PAR, DELL, IBM, EMC, Hitachi, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}