Posts tagged ‘deflator’

Recession Storm Fears Reign Supreme as Stocks Gain Steam

Commentators continue to shout the doom-and-gloom forecasts of a hard landing recession, but after an economic hurricane in 2022 there are some signs the financial clouds have begun to lift this year. The stock market has reflected this positive fundamental shift during January, as the S&P 500 catapulted +6.2%, NASDAQ +10.8%, and the Dow Jones Industrial Average +2.8%.

Last year, a major influencing cause to the -19% downdraft in the stock market (S&P 500) was due to the highest inflation readings experienced in four decades, compounded by a Federal Reserve hell-bent on slamming on the interest rate brakes. A big contributing factor to the surge in inflation was the spike in consumer spending fueled by trillions in government stimulus, coupled with widespread shortages in goods triggered by supply chain disruptions.

Fortunately, the headwinds of inflation now appear to be abating. Recently released inflation figures showed core inflation dropping from a peak of 9.1% last year to 3.5% in the fourth quarter (see chart below). Although the Fed will likely raise its interest rate target by 0.25% up to 4.75% this week, the downward reversal in inflation has raised the probabilities of the Federal Reserve “pausing” or “pivoting” on the direction of previous rate hikes. The odds of a halt or cut in rates will likely only increase if the descending trajectory of inflation persists and other upcoming economic data weaken further.

No Signs of Recession…Yet. Investors Waiting for Another Flood

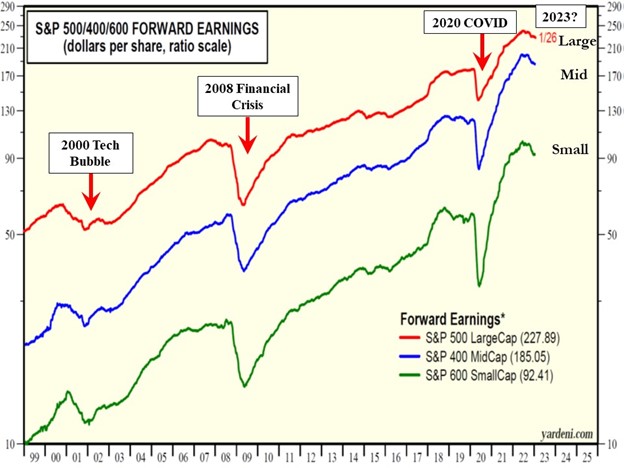

While the calls for a hard economic landing remain, healthy GDP growth (+2.9% in Q4), generationally low unemployment (3.5%), and relatively stable earnings (see chart below) all point to a stable economy with the ability to navigate a soft landing. China’s new reopening of the economy and Europe’s seeming ability of dodging a recession provide additional evidence for a soft landing scenario.

As you can see further from the 25-year earnings chart above, the drop in S&P 500 earnings in recent months has been fairly modest compared to previous downturns, and the forecast for 2023 earnings is currently estimating a modest gain on a year-over-year basis. Over the last 25 years, we have arguably experienced three 100-year floods (2000 Tech Bubble, 2008 Financial Crisis, and 2020 COVID pandemic), so investors have been bracing for another enormous financial hurricane.

Although the bursting of the 2000 Tech Bubble had an outsized impact on the technology sector, the effect on the overall economy was more muted, as you can observe from the shallow decline in the earnings. As the earnings show, during the Financial Crisis (2008) and COVID (2020), the crash in earnings was much more severe. Thus far in 2023, there has been no earnings plummet or sign of recession, and if financial conditions continue to soften, there is no reason we couldn’t undergo a more vanilla, garden-variety recession like we did in 1990 and 2000.

Stairs & Elevators

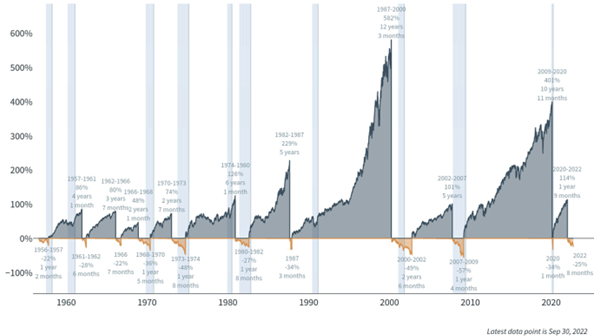

While the future always remains unclear, nobody knows for certain whether a recession will occur this year or if the 2022 bear market will endure into 2023. However, as you can notice below, history over the last 70 years shows the duration of bull markets (average of about 6 years) are much longer than bear markets (approximately 1 year). I like to compare bull markets to walking up stairs in a tall building, and bear markets to going down an elevator. The main difference is that the stock market elevator generally never goes to the bottom floor and the stairs keep growing to record heights over the long-run. Since World War II, Americans have experienced 13 economic recessions (see also Recession or Mental Depression?). Not only are investors batting 1,000% in successfully surviving these recessions, they have thrived. From 1956 until the present, the S&P 500 has vaulted approximately 80-fold.

Presently, economic skies might not all be clear, blue, and sunny, but the fact that inflation is dropping, our economy is still growing, labor markets remain healthy, China has reopened for business, and Europe hasn’t cratered all leave room for optimism. It may not be time to bust out the sunscreen quite yet, but the dark economic clouds of 2022 appear to be lifting slowly.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (Feb. 1, 2023). Subscribe Here to view all February articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

New Year, New Clean Slate

Stock and bond market returns in 2022 were disappointing, but we now get to start 2023 with a clean slate. Before we turned the page on another annual chapter, Santa Claus chose to finish last year by placing a lump of coal in investor stockings, as evidenced by the S&P 500 index decline of -5.9% during December.

Good News & Bad News

There is some good news and bad news as it relates to this year’s underwhelming stock market results (-19.4%). The bad news is last year turned out to be the 4th worst year in the stock market since World War II (1945) and also marked the worst year since 2008. Here’s a summary of the S&P 500’s worst years over the last eight decades:

2008: -38.5%

1974: -29.7%

2002: -23.4%

2022: -19.4%

Source: CNBC (Bob Pisani)

The good news is that the stock market is up 81% of the time in subsequent years following down years. The average increase in bounce-back years is +14%. In another study of down years, the analysis showed that after the stock market has fallen -20% or more, stock prices were higher on average by +15% one year later, +26% two years later, and +29% three years later. Nothing is guaranteed in life, but as Mark Twain famously stated, “History does not repeat itself, but it often rhymes.”

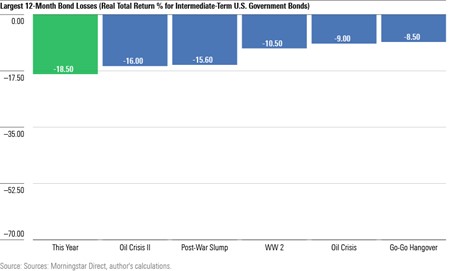

2022: The Year of No Shock Absorbers (Worst Bond Market Ever)

The stock market receives most of the media glory and reporting, however the bond market is the Rodney Dangerfield of asset classes, it “gets no respect.” Typically, during weak stock markets (i.e., “bear markets”), the bond or fixed income investments in a diversified portfolio act as shock absorbers to cushion the blow of volatile stock prices. More specifically, in a typical bear market, the economy generally slows down causing demand to decelerate, and interest rates to decline, which causes the values of bonds to increase. Therefore, as stock prices decline, the gains from bonds in your portfolio usually help offset stock losses. Unfortunately, this scenario didn’t happen in 2022, but rather investors experienced a double negative whammy. Not only did stocks experience one of its worst years in decades, the bond market also suffered what many pundits are describing as the “Worst Bond Market Ever” – see chart below.

Why in particular did bonds perform so poorly this year, when they commonly outperform in slow or recessionary economic conditions? For starters, interest rates spent most of 2022 increasing at the fastest pace in more than four decades (see chart below). An unanticipated rise in inflation was the main culprit, which was caused by spiking energy prices from Russia’s invasion of Ukraine; COVID-related supply chain disruptions; unprecedented fiscal stimulus (trillions of dollars in infrastructure spending and incentives); record monetary stimulus (QE – Quantitative Easing); and extended years of ZIRP (Zero Interest Rate Policy). For these reasons, and others, bonds collapsed in sympathy with deteriorating stock prices.

Room for Optimism in 2023

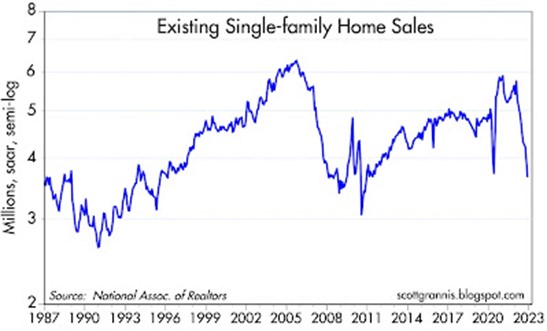

Last year was challenging, however, not all is lost. The Federal Reserve, inflation, interest rates, Ukraine, and cryptocurrency volatility (e.g., Bitcoin down -64% in 2022) dominated headlines this year, but many of these headwinds could abate or reverse in 2023. For example, there are numerous indicators pointing to peaking and/or declining inflation, which, if true, could create a tailwind for investors this year. Bolstering this argument are the current weakening trends we are witnessing in the housing market, which should ripple through the economy to cool inflation (see chart below).

And if it’s not declining home prices, lower energy prices have also filtered through the global economy to lower transportation and shipping costs (e.g., freight rates from China to West Coast are down -90%). What’s more, a stronger dollar has contributed to declining commodity prices as well.

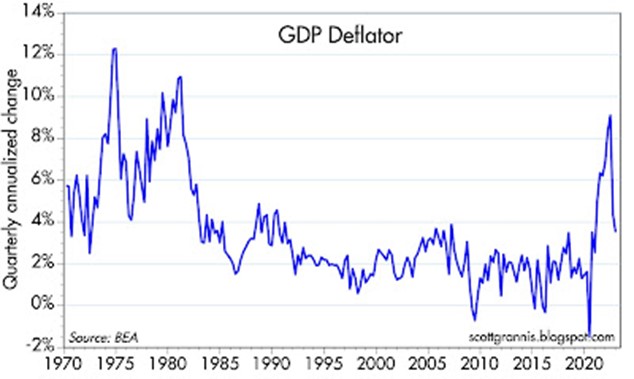

Although inflation still has a long way to go before reaching the Federal Reserve’s 2% target rate, broad inflation measures, such as the GDP Deflator, are showing a significant decrease in inflation (see chart below). By analyzing the various disinflationary tea leave markers, we can gain some confidence regarding future interest rates. Observing the fastest rate hike cycle by the Fed in decades informs us that we are likely closer to an end of rate hikes (i.e., pause or cut), rather than the beginning. If correct, tamer inflation means 2023 could prove to be a better environment for both stock and bond investors.

In summary, last year was painful across the board, but investors are starting this year with a clean slate and signs are pointing to a potential reversal in inflation and interest rate headwinds. With the change of the calendar, a messy 2022 could turn into a spick-and-span 2023.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (Jan. 3, 2023). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}