Posts tagged ‘deficit’

Bad Weather Coming: Hurricane or Drizzle?

It was a stormy month in the stock market, but the sun eventually came out and the Dow Jones Industrial Average rallied more than 2,300+ points before eking out a small gain (up +0.04%) and the S&P 500 index also posted an incremental increase (+0.005%). But there are clouds on the horizon. Although the economy is currently very strong (i.e., record corporate profits and a generationally low unemployment rate of 3.6% – see chart below), some forecasters are predicting a recession during 2023 as a result of the Federal Reserve pumping the brakes on the economy by increasing interest rates, in addition to elevated inflation, supply chain disruptions, COVID lockdowns in China, and a war between Russia and Ukraine.

UNEMPLOYMENT RATE (1997 – 2022)

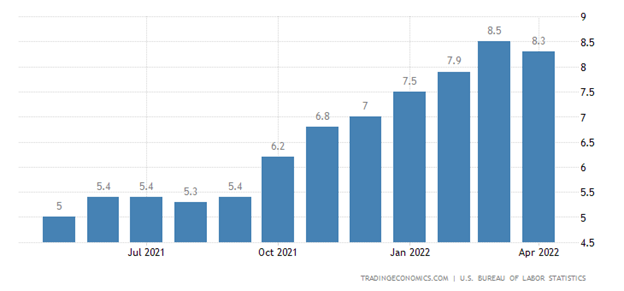

But like weather forecasters, economists are perpetually unreliable. While some doomsday-er economists are expecting a deeply destructive hurricane (deep recession), others are only seeing a mild drizzle (soft landing) developing. The truth is, nobody knows for certain at this point, but what we do know is that the correction in stock prices this year (-13% now and -20% two weeks ago) has already significantly discounted (factored in) a mild recession. In other words, even if a mild recession were to occur in the coming months or quarters, there may be very little reaction or negative consequences for investors. Similarly, if inflation begins to be peaking as it appears to be doing (see chart below), and the Fed can orchestrate a soft landing (i.e., raise interest rates and reduce balance sheet debt without crippling the economy), then substantial rewards could accrue to stock market investors. On the flip side, if the economy were to go into a deep recession, history would suggest this stormy forecast might result in another -10% to -15% of chilliness.

INFLATION RATE (%)

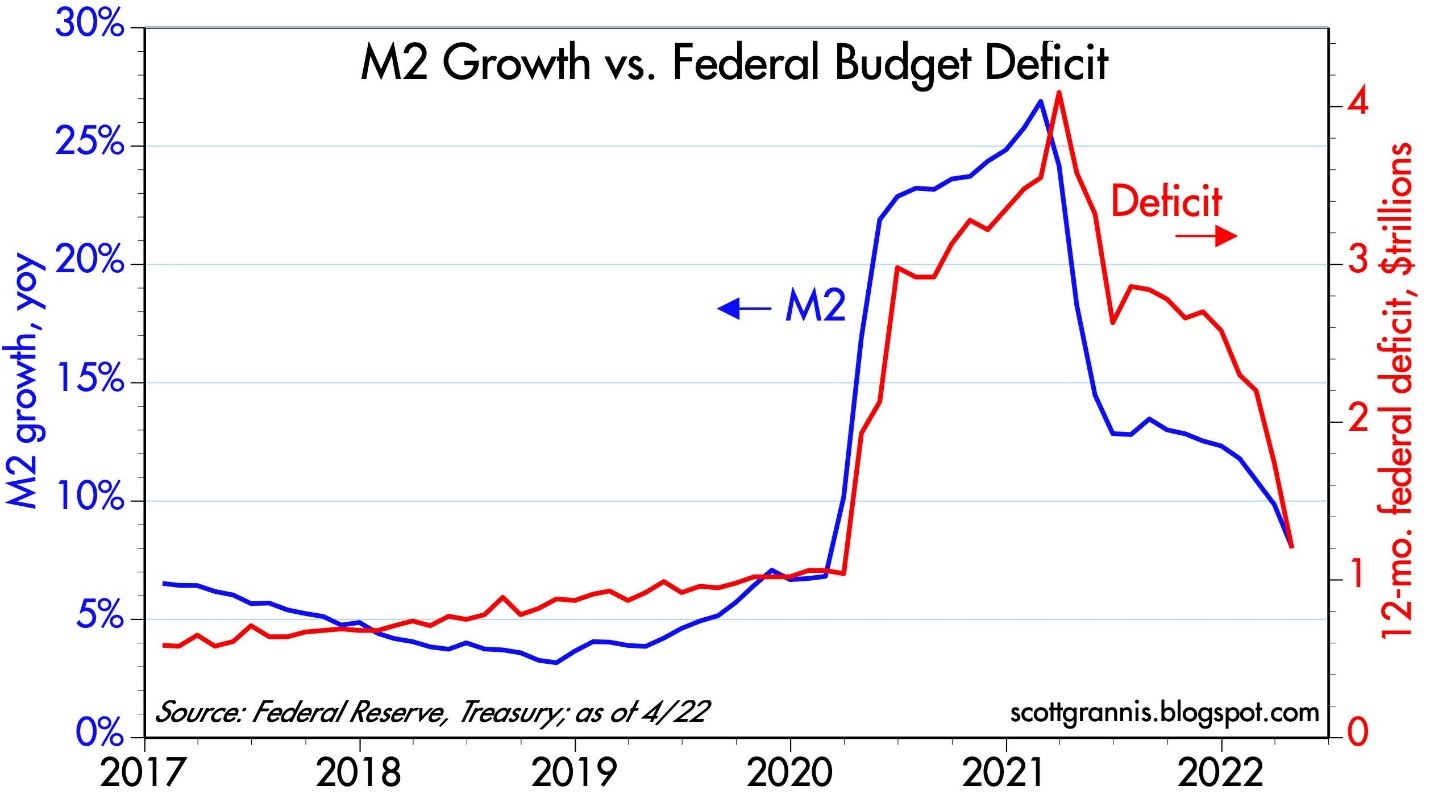

Due to trillions of dollars in increased stimulus spending and Federal Reserve Quantitative Easing (bond buying), we experienced an explosion in the government deficit and surge in money supply growth (i.e., the root cause for swelling inflation). Arguably, some or all of these accommodations were useful in surviving through the worst parts of the COVID pandemic, however, we are paying the price now in sky-high food costs, explosive gasoline prices, and expanding credit card bills. The good news is the deficit is plummeting (see chart below) due to a reduction in spending (due in part to no Build Back Better infrastructure spending legislation) and soaring income tax receipts from a strengthening economy and capital gains in the stock market.

MONEY SUPPLY GROWTH% (M2) VS. GOVERNMENT DEFICIT

For many investors, getting used to large multi-year gains has been very comfortable, but interpreting downward gyrations in the stock market can be very confusing and counterintuitive. In short, attempting to decipher the reasons behind the short-term zigs and zags of the market is a fool’s errand. Not many people predicted a +48% gain in the stock market during a global pandemic (2020-2021), just like not many people predicted a short-lived -20% reduction in the stock market during 2022 as we witnessed record-high corporate profits and unemployment rates hovering near generational lows (3.6%).

Stock market veterans understand that stock prices can go down when current economic news is sunny but future expectations are too high. Experienced investors also understand stock prices can go up when the current economic news may be getting too cloudy but future expectations are too low.

Apparently, the world’s greatest investor of all-time thinks that all this gloomy recession talk is creating lots of stock market bargains, which explains why Buffett has invested $51 billion of his cash at Berkshire Hathaway as the stock market has gotten a lot more inexpensive this year. So, while the economy will likely face a number of headwinds going into 2023, it doesn’t mean a hurricane is coming and you need to hide in a bunker. If you pull out your umbrella and rain gear, just like smart investors do during all previous challenging economic cycles, the drizzle from the storm clouds will eventually pass and blue skies shall reappear.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (June 1, 2022). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in BRK.B/A or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Consumer Confidence Flies as Stock Market Hits New Highs

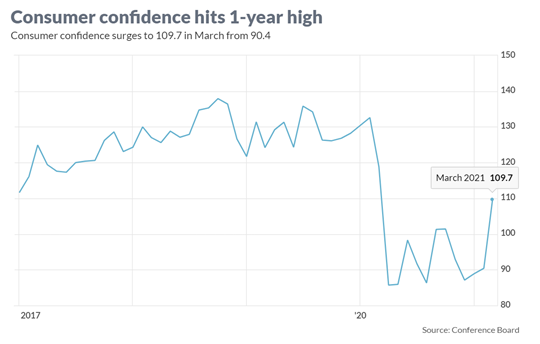

As the economy starts reopening from a global pandemic that is improving, consumers and businesses are beginning to see a light at the end of the tunnel. The surge in the recently reported Consumer Confidence figures to a new one-year high (see chart below) is evidence the recovery is well on its way. A stock market reaching new record highs is further evidence of the reopening recovery. More specifically, the Dow Jones Industrial Average catapulted 2,094 points higher (+6.2%) for the month to 32,981 and the S&P 500 index soared +4.2%. A rise in interest rate yields on the 10-Year Treasury Note to 1.7% from 1.4% last month placed pressure on technology growth stocks, which led to a more modest gain of +0.4% in the tech-heavy NASDAQ index during March.

Comeback from COVID

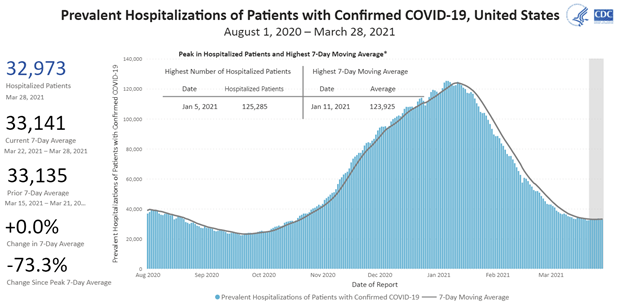

With a combination of 150 million vaccine doses administered and 30 million cumulative COVID cases, the U.S. population has creeped closer toward herd immunity protection against the virus and pushed down hospitalizations dramatically (see chart below).

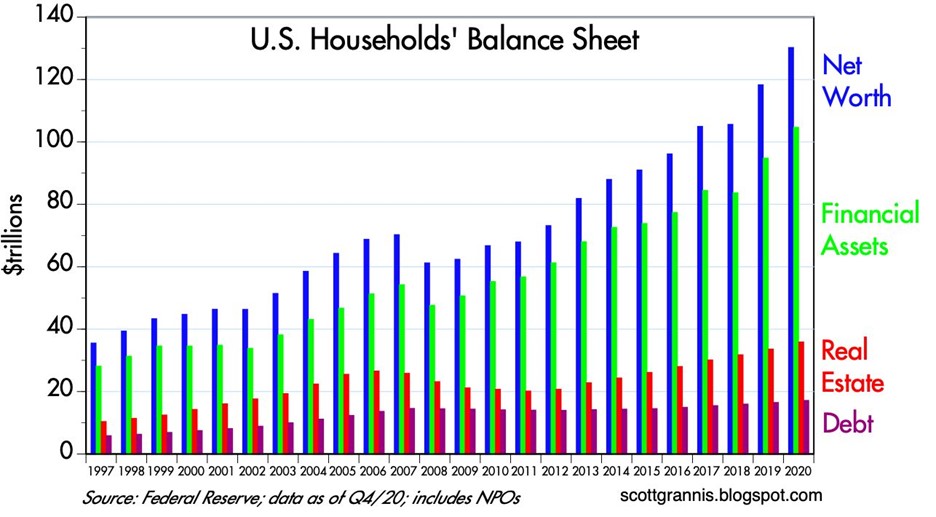

Also contributing to investor optimism have been the rising values of investments and real estate assets thanks to an improving economy and COVID case count. As you can see from the chart below, the net worth of American households has more than doubled from the 2008-2009 financial crisis to approximately $130 trillion dollars, which in turn has allowed consumers to responsibly control and manage their personal debt. Unfortunately, the U.S. government hasn’t been as successful in keeping debt levels in check.

Spending and Paying for Infrastructure Growth

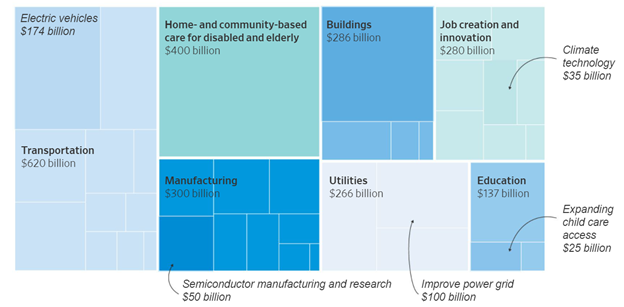

Besides focusing on positive COVID trends, investors have also centered their attention on the passage of a $1.9 trillion stimulus bill last month and a new proposed $2.3 trillion infrastructure bill that President Biden unveiled details on yesterday. At the heart of the multi-trillion dollar spending are the following components (see also graphic below):

- $621 billion modernize transportation infrastructure

- $400 billion to assist the aging and disabled

- $300 billion to boost the manufacturing industry

- $213 billion to build and retrofit affordable housing

- $100 billion to expand broadband access

With over $28 trillion in government debt, how will all this spending be funded? According to The Fiscal Times, there are four main tax categories to help in the funding:

Corporate Taxes: Raising the corporate tax rate to 28% from 21% is expected to raise $730 billion over 10 years

Foreign Corporate Subsidiary Tax: A new global minimum tax on foreign subsidiaries of American corporations is estimated to raise $550 billion

Capital Gains Tax on Wealthy: Increasing income tax rates on capital gains for wealthy individuals is forecasted to raise $370 billion

Income Tax on Wealthy: Lifting the top individual tax rate back to 39.6% for households earning more than $400,000 per year is seen to bring in $110 billion

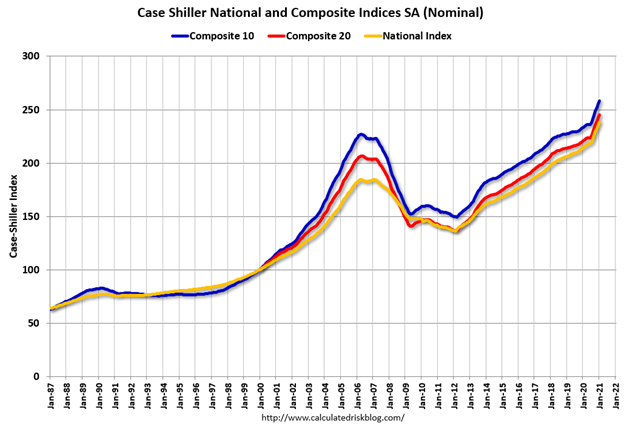

Besides the economy being supported by government spending, growth and appreciation in the housing market are contributing to GDP growth. The recently released housing data shows housing prices accelerating significantly above the peak levels last seen before the last financial crisis (see chart below).

Although the economy appears to be on solid footing and stock prices have marched higher to new record levels, there are still plenty of potential factors that could derail the current bull market advance. For starters, increased debt and deficit spending could lead to rising inflation and higher interest rates, which could potentially choke off economic growth. Bad things can always happen when large financial institutions take on too much leverage (i.e., debt) and speculate too much (see also Long-Term Capital Management: When Genius Failed). The lesson from the latest, crazy blow-up (Archegos Capital Management) reminds us of how individual financial companies can cause billions in losses and cause ripple-through effects to the whole financial system. And if that’s not enough to worry about, you have rampant speculation in SPACs (Special Purpose Acquisition Companies), Reddit meme stocks (e.g., GameStop Corp. – GME), cryptocurrencies, and NFTs (Non-Fungible Tokens).

Successful investing requires a mixture of art and science – not everything is clear and you can always find reasons to be concerned. At Sidoxia Capital Management, we continue to find attractive opportunities as we strive to navigate through areas of excess speculation. At the end of the day, we remain disciplined in following our fundamental strategy and process that integrates the four key legs of our financial stool: corporate profits, interest rates, valuations, and sentiment (see also Don’t Be a Fool, Follow the Stool). As long as the balance of these factors still signal strength, we will remain confident in our outlook just like consumers and investors are currently.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

U.S. – Best House in Bad Global Neighborhood

Article below represents a portion of free December 1, 2011 Sidoxia monthly newsletter (Subscribe on right-side of page)

There is no shortage of issues to worry about in our troubled global neighborhood, but then again, anybody older than 25 years old knows the world is always an uncertain place. Whether we are talking about wars (Vietnam, Cold War, Iraq); presidential calamities (Kennedy assassination, Nixon resignation/impeachment proceedings); international turmoil (dissolution of Soviet Union, 9/11 attacks, Arab Spring); investment bubbles (technology, real estate); or financial crises (S&L crisis, Long Term Capital, Lehman Brothers bankruptcy), investors always have a large menu of concerns from which they can order.

Despite the doom and gloom dominating the media airwaves, and the lackluster performance of equities experienced over the last decade, the Dow Jones Industrial Average and the S&P 500 index are both up more than 20-fold since the 1970s (those gains also exclude the positive impact of dividends).

Times Have Changed

Just a few decades ago, nobody would have talked or cared about small economies like Iceland, Dubai, and Greece. Today, technology has accelerated the forces of globalization, resulting in information travelling thousands of miles at the click of a mouse, often creating scary financial mountains out of meaningless molehills. As a result of these trends, news of Italian bond auctions, which normally would be glossed over on the evening news, instantaneously clogs our smart phones, computers, radios, and televisions. The implications of all these developments mean investing has become much more difficult, just as its importance has never been more crucial.

How has investing become more critical? For starters, interest rates are near 60-year lows and Treasury bond prices are at record highs, while inflation (food, energy, healthcare, leisure, etc.) is shrinking the value of people’s savings. Next, entitlement and pension reliability are decreasing by the minute – fiscal imbalances and unrealistic promises have contributed to a less certain retirement outlook. Layer on hyper-manic volatility of daily, multi-hundred point swings in the Dow Jones Industrial index and a less experienced investor quickly realizes investing can become an overwhelming game. Case in point is the VIX volatility index (a.k.a., the “Fear Gauge”), which has registered a whopping +57% increase in 2011.

December to Remember?

After an explosive +23% return in the S&P 500 index for 2009 (excluding dividends) and another +13% return in 2010, equity investors have taken a breather thus far in 2011 – the Dow Jones Industrial Average is up modestly (+4%) and the S&P 500 index is down fractionally (-1%). We still have the month of December to log, but in the short-run the European tail has definitely been wagging the rest of the global dog.

Although the United States knows a thing or two about lack of political leadership and coordination, herding the 17 eurozone countries to resolve the European debt financial crisis has proved even more challenging. As you can see below in the performance figures of the major global equity markets, the U.S. remains the best house in a bad neighborhood:

Our fiscal house undeniably needs some work (i.e., unsustainable deficits and bloated debt), but record corporate profits, record levels of cash, voracious consumer spending, improving employment data, and attractive valuations are all contributing to a domestic house that makes opportunities in our backyard look a lot more appealing to investors than prospects elsewhere in the global neighborhood.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and VGK, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Plumbers & Cops: Can the Debt Ceiling be Fixed?

The ceiling is leaking, but it’s unclear whether it will be repaired? Rather than fix the seeping fiscal problem, Democrats and Republicans have stared at the leaky ceiling and periodically applied debt ceiling patches every year or two by raising the limit. Nanosecond debt ceiling coverage has reached a nauseating level, but this issue has been escalating for many months. Last fall, politicians feared their long-term disregard of fiscally responsible policies could lead to a massive collapse in the financial ceiling protecting us, so the President called in the bipartisan plumbers of Alan Simpson & Erskine Bowles to fix the leak. The commission swiftly identified the problems and came up with a deep, thoughtful plan of action. Unfortunately, their recommendations were abruptly dismissed and Washington fell back into neglect mode, choosing instead to bicker like immature teenagers. The result: poisonous name calling and finger pointing that has placed Washington politicians one notch above Cuba’s Fidel Castro, Venezuela’s Hugo Chavez, and Iran’s Mahmoud Ahmadinejad on the list of the world’s most hated leaders. Strategist Ed Yardeni captured the disappointment of American voters when he mockingly states, “The clowns in Washington are making people cry rather than laugh.”

Although despair is in the air and the outlook is dour, our government can redeem itself with the simple passage of a debt ceiling increase, coupled with credible spending reduction legislation (and possibly “revenue enhancers” – you gotta love the tax euphimism).

The Elephant in the Room

Our country’s spending problems is nothing new, but the 2008-2009 financial crisis merely amplified and highlighted the severity of the problem. The evidence is indisputable – we are spending beyond our means:

Source: scottgrannis.blogspot.com

If the federal spending to GDP chart is not convincing enough, then review the following graph:

- Source: blog.yardeni.com – A graph a first grader could understand.

You don’t need to be a brain surgeon or rocket scientist to realize government expenditures are massively outpacing revenues (tax receipts). Expenditures need to be dramatically reduced, revenues increased, and/or a combination thereof. Applying for a new credit card with a limit to spend more isn’t going to work anymore – the lenders reviewing those upcoming credit applications will straightforwardly deny the applications or laugh at us as they gouge us with prohibitively high borrowing costs. The end result will be the evaporation of entitlement programs as we know them today (including Medicare and Social Security). For reference of exploding borrowing costs, please see Greek interest rate chart below. The mathematical equation for the Greek financial crisis (and potentially the U.S.) is amazingly straightforward…Loony Spending + Looney Politicians = Loony Interest Rates.

Source: Bloomberg.com via Wikipedia.com

To illustrate my point further, imagine the government owning a home with a mortgage payment tied to a 2.5% interest rate (a tremendously low, average borrowing cost for the U.S. today). Now visualize the U.S. going bankrupt, which would then force foreign and domestic lenders to double or triple the rates charged on the mortgage payment (in order to compensate the lenders for heightened U.S. default risk). Global investors, including the Chinese, are pointing a gun at our head, and if a political blind eye on spending continues, our foreign brethren who have provided us with extremely generous low priced loans will not be bashful about pulling the high borrowing cost trigger. The ballooning mortgage payments resulting from a default would then break an already unsustainably crippling budget, and the government would therefore be placed in a position of painfully slashing spending. Too extreme a shift towards austerity could spin a presently wobbling economy into chaos. That’s precisely the situation we face under a no-action Congressional default (i.e., no fix by August 2nd or shortly thereafter). To date, the Chinese have collected their payments from us with a nervous smile, but if the U.S. can’t make some fiscally responsible choices, our Asian Pacific pals will be back soon with a baseball bat to collect.

The Cops to the Rescue

Any parent knows disciplining teenagers doesn’t always work out as planned. With fiscally irresponsible spending habits and debt load piling up to the ceiling, politicians are stealing the prospects of a brighter future from upcoming generations. The good news is that if the politicians do not listen to the parental voter cries for fiscal sanity, the capital market cops will enforce justice for the criminal negligence and financial thievery going on in Washington. Ed Yardeni calls these capital market enforcers the “bond vigilantes.” If you want proof of lackadaisical and stubborn politicians responding expeditiously to capital market cops, please hearken back to September 2008 when Congress caved into the $700 billion TARP legislation, right after the Dow Jones Industrial average plummeted 777 points in a single day.

Who exactly are these cops? These cops come in the shape of hedge funds, sovereign wealth funds, pension funds, endowments, mutual funds, and other institutional investors that shift their dollars to the geographies where their money is treated best. If there is a perceived, heightened risk of the United States defaulting on promised debt payments, then global investors will simply take their dollar-denominated investments, sell them, and then convert them into currencies/investments of more conscientious countries like Australia or Switzerland.

Assisting the capital market cops in disciplining the unruly teenagers are the credit rating agencies. S&P (Standard and Poor’s) and Moody’s (MCO) have been watching the slow-motion train wreck develop and they are threatening to downgrade the U.S.’ AAA credit rating. Republicans and Democrats may not speak the same language, but the common word in both of their vocabularies is “reelection,” which at some point will effect a reaction due to voter and investor anxiety.

Nobody wants to see our nation’s pipes burst from excessive debt and spending, and if the political plumbers can repair the very obvious and fixable fiscal problems, we can move on to more important challenges. It’s best we fix our problems by ourselves…before the cops arrive and arrest the culprits for gross negligence.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MCO, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

End of the World Put on Ice

Our 3.5 billion year old planet has received a temporary reprieve, at least until the next Mayan Armageddon destroys the world in 2012. Sex, money, and doom sell and Arnold, Oprah, and the Rapture have not disappointed in generating their fair share of advertising revenue clicks.

With 2 billion people connected to the internet and 5 billion people attached to a cell phone, every sneeze, burp, and fart around the world makes daily headline news. The globalization cat is out of the bag, and this phenomenon will only accelerate in the years to come. In 1861 the Pony Express took ten days to deliver a message from New York to San Francisco, and today it takes a few seconds to deliver a message across the world over Twitter or Facebook.

The equity markets have more than doubled from the March 2009 lows and even previous, ardent bulls have turned cautious. Case in point, James Grant from the Interest Rate Observer who was “bullish on the prospects for unscripted strength in business activity” (see Metamorphosis of Bear into Bull) now sees the market as “rich” and asserts “nothing is actually cheap.” Grant rubs salt into the wounds by predicting inflation to spike to 10% (read more).

Layer on multiple wars, Middle East/North African turmoil, gasoline prices, high unemployment, mudslinging presidential election, uninspiring economic growth, and you have a large pessimistic poop pie to sink your teeth into. Bearish sentiment, as calculated by the AAII Sentiment Survey, is at a nine-month high and currently bears outweigh bulls by more than 50%.

The Fear Factor

I think Cullen Roche at Pragmatic Capitalism beautifully encapsulates the comforting blanket of fear that is permeating among the masses through his piece titled, “In Remembrance of Fear”:

“The bottom line is, stay scared. Do not let yourself feel confident, happy or wealthy. You are scared, poor and miserable. You should stay that way. You owe it to yourself. The media says so. And more importantly, there are old rich white men who need to sell books and if you’re not scared by them you’ll never buy their books. So, do yourself a favor. Buy their books and services and stay scared. You deserve it.”

Here is Cullen’s prescription for dealing with all the doom and gloom:

“Associate with people who are more scared than you. That way, you can all sit in bunkers and talk about the end of days and how screwed we all are. Think about how much better that will make you feel. Misery loves company. Do it.”

All is Not Lost

While inflation and gasoline price concerns weigh significantly on economic growth expectations, some companies are taking advantage of record low interest rates. Take for example, Google Inc.’s (GOOG) recent $3 billion bond offerings split evenly across three-year, five-year, and ten-year notes with an average interest rate of 2.3%. Although Google has languished relative to the market over the last year, the market blessed the internet giant with the next best thing to free money by pricing the deal like a AAA-rated credit. Cash-heavy companies have been able to issue low cost debt at a frantic pace for accretive EPS shareholder-friendly activities, such as acquisitions, share buybacks, and organic growth initiatives. Cash rich balance sheets have afforded companies the ability to offer shareholders a steady diet of dividend increases too.

While there is no question high oil prices have put a wet towel over consumer spending, the largest component of corporate check books is labor costs, which accounts for roughly two-thirds of corporate spending. With unemployment rate at 9.0%, this is one area with no inflation pressure as far as the eye can see. Money losing companies that go bankrupt lay-off employees, while profitable companies with stable input costs (labor) will hire more – and that’s exactly what we’re seeing today. Despite all the economic slowing and collapse anxiety, S&P 500 operating earnings, as of last week, are estimated to rise +17% in 2011. Healthy corporations coupled with a growing, deleveraged workforce will have to carry the burden of growth, as deficit and debt direction will ultimately act as a drag on economic growth in the immediate and intermediate future.

Fear and pessimism sell news, and technology is only accelerating the proliferation of this trend. The good news is that you have another 18 months until the next apocalypse on December 21, 2012 is expected to destroy the human race. Rather than attempting to time the market, I urge you to follow the advice of famed investor Peter Lynch who says, “Assume the market is going nowhere and invest accordingly.” For all the others addicted to “pessimism porn,” I’ll let you get back to constructing your bunker.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and GOOG, but at the time of publishing SCM had no direct position in Twitter, Facebook, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Foreign Frights & Debt Doubts

Excerpts from Sidoxia monthly newsletter (Subscribe on right side of page)

Over the last few years the globalized nature of the financial crisis has forced a diverse set of world leaders to deal with obscure international flare-ups in countries ranging from Iceland to Dubai, and Greece to Tunisia. The crisis du jour is the popular revolt in Egypt against 30-year president Hosni Mubarak and his autocratic, authoritarian government. The situation for the U.S. becomes a little sticky because Egypt, although creating a GDP (Gross Domestic Product) of less than the state of Illinois, is still the largest Arab country by population (approximately 82 million – even larger than Iran); a staunch ally with the U.S. in keeping peace with Israel; has contributed important intelligence to our country’s war on terror; and has been a responsible partner in controlling commerce through the all-important Suez Canal. The problem with Egypt and Mubarak’s regime is that the Egyptian economy is in relative shambles (they do not have oil reserves like their neighbors), unemployment is through the roof, and the government has been slow to push democratic advancements forward for the Egyptian people.

As emerging market “haves” increasingly join the ranks of the middle class, the people representing the “have-nots” of Yemen, Jordan, Algeria, Tunisia, Egypt, and others are thirsting for a cocktail of democracy and a higher standard of living, like some of their wealthier neighbors. These autocratic, authoritarian regimes can do their best to slow or delay the democratizations of their countries, but they cannot put the genie back in the bottle. Information is flowing faster than ever, and societies previously kept in the dark are now seeing the light of democracy.

Like any volatile government situation, there are threats and opportunities, depending on whether Mubarak stays in power, and if not, the nature of the new leadership. If an extremist government fills the leadership void, the U.S. may wish to rewind the clock and put the slow-moving reformist, Mubarak, back in power.

The short-term impact of the popular revolt may create additional volatility in the markets, but in the long-run, if the turmoil introduces more open, transparent, less corrupt, and democratic ideals to the new agenda, then the world will become a better place.

Bitter Debt Pill Tough to Swallow

There is never a shortage of issues to worry about, and from an economic standpoint, the suffocating amount of debt our country is dealing with is at the top of the concern list. The 2008-2009 financial crisis hole that we are still climbing our way out of is a friendly reminder of what happens to countries adopting irresponsible fiscal policies. The choking amount of debt the U.S. is swallowing remains a central issue for the current administration and will be a core topic to be debated through the 2012 Presidential election cycle.

How serious is the issue? The problem is serious enough the Congressional Budget Office (CBO) just raised its budget deficit forecast for fiscal 2011 to hit a record $1.5 trillion (9.8% of GDP), a level higher than $1.3 trillion in fiscal 2010. The blame for the new record can be largely attributed to the recent extension of the $858 billion in Bush tax-cuts and other benefits/breaks. Kicking the can down the road recently led Moody’s Investors Services of threatening the U.S. with a downgrade of its triple-A rated debt.

Source: The Peterson Institute

The President addressed some of our fiscal problems in his State of the Union Address recently (e.g., proposing a freeze on discretionary spending), but the rubber really hits the road when he comes out with his budget proposal later this month. How serious is he about reducing our hemorrhaging deficits? We’ll soon find out when the individual budget line-items are distributed for everyone to see. Shortly thereafter, around the end of March, the debt ceiling impasse will become a game of political “chicken.” Each side, Democrats and Republicans, will attempt to withdraw concessions from the other party, in exchange for a vote that will prevent a disastrous default of our government’s debt payments. Basically, our government is effectively looking to expand its credit card credit line, because our government credit limit is maxed out.

The situation isn’t hopeless if our politicians can show leadership by making difficult, unpopular fiscal decisions, but if America ignores our painful debt problems and does not take its bitter medicine, then prepare for an economy on the verge of keeling over.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Impoverished Global Babysitter

I don’t mind being a babysitter for the world, as long as I get paid for it. Unfortunately, not only are we paying to be the nation’s global defense babysitter, but we are also paying for the protection responsibility with unsustainable borrowings.

I don’t want to be a cold-hearted neighbor to our friends and allies, but it is all a matter of degree. Collecting a vacationing neighbor’s newspaper and mail, and watching for any potential suspicious activity is all part of being a conscientious, dependable neighbor, but where do you draw the line? As a good neighbor, should I also be responsible for paying for and installing a security system on their premises? Or how about getting my 16 year old nephew to spend the night at my neighbor’s because of some scary noises heard during the previous night?

For politicians to say we need to cut spending but defense spending is off the table is hypocritical. Bruce Bartlett, columnist at The Fiscal Time, had this to say on the subject:

“No one is saying the defense budget is the sole source of the deficit, but the fact is that it has risen from 3 percent of the gross domestic product in fiscal year 2001 to 4.7 percent this year. That additional 1.7 percent of GDP amounts to $250 billion in spending — almost 20 percent of this year’s budget deficit. And according to a recent Congressional Research Service report, the cost of wars in Iraq and Afghanistan alone accounted for 23 percent of the combined budget deficits between fiscal years 2003 and 2010.”

Even the government should have learned one of the prime lessons from the 2008-2009 financial crisis: tough times require the necessity to do more with less. Whether you are talking about a large corporation like $173 billion valued General Electric (GE), a small mom-and-pop coffee shop, or a middle-class family of four, the moral of the story is bad things eventually happen to individuals, corporations, and governments that live beyond their means. The crisis was exacerbated by excessive borrowing to achieve the higher standard of living and operations.

New Heightened Sensibility?

The initial deficit reduction proposals crafted by the bipartisan commission headed by Erskine Bowles and Alan Simpson should be lauded, regardless of how much Congress decides to dilute the $4 trillion in budget cuts over the next 10 years. The plan may not garner votes for politicians, but these types of necessary cuts will place our country on firmer ground and provide a more sustainable path to prosperity. More specifically, the plan would bring the federal budget deficit down to 2.2% of GDP (Gross Domestic Product) by 2015 and reduce the country’s debt to 60% of GDP by 2024.

Building Flying Rolls Royces

Bowles and Simpson appear to get it, but our bloated government doesn’t seem to understand. If I were running an unprofitable company with a lot of debt, would it be a good idea to develop a new flying Rolls Royce car fleet (with questionable utility) for my employees? Common fiscal sense would dictate the answer to be “NO.”

Regrettably our government has answered “yes” by building a ridiculously costly flying Rolls Royce fleet of its own under the name of Joint Strike Fighter (the F-35 program from Lockheed Martin Corp. [LMT]). This absurdly priced program – the costliest in our country’s history – is projected to cost up to $382 billion for 2,443 aircraft over the next two decades (Reuters). This translates into a whopping $156 million per aircraft. Cost overruns have already come in 40-90% higher than expected over the last nine years, and the price tag continues to rise. The state of the art jet program is touted as a Swiss army knife (flexibility to be used by all three branches of the military), but may actually turn out to be a butter knife due to the program’s questioned utility (see great PBS video here).

So like any company, individual, or government, there is something called prioritization. By cutting fat in less critical areas, a portion of those savings can be redeployed to INCREASE spending in the areas that matter. I won’t wade into the relative merits (or lack thereof) related to Afghanistan and Iraq expenditures or appropriate troop levels, but suffice it to say, I’m certain spending can be cut in many areas to make room for our country’s primary defense priorities.

I’m no defense expert but when faced to deal with a murky, inconspicuous issue of terrorism (cave dwelling insurgents and bomb-making sleeper cells), intelligence collection and international coordination make more sense than building $150 million flying Rolls Royces, which are better suited for fighting an obsolete cold war than finding terrorist needles in a global haystack.

Crotch Costs

Layer on the new TSA passenger flight costs associated with crotch fondling pat downs and the costs related to buying miniaturized shampoo and gel containers, one wonders if tax-payer money can be more efficiently spent. For what it’s worth, the FDA has approved the latest body scanning machines with no health concerns, so if an airport worker gets his/her jollies by ogling an overweight out of shape passenger like me, then so be it. The fact of the matter is that estimates show 99% of passengers choose the innocuous body scan, which displays a white, ghost-like naked computer image to the agent. For those worried about self image issues or privacy concerns, perhaps the airports can set up a meet-and-greet room option for passengers to become better acquainted with the agent before passing through the scanner.

Freeloaders Cutting Spend

Source: The Financial Times

Domestic defense spending cuts become especially touchy when discussed in concert with European spending reductions. Take for example German plans to slash $10.7 billion in defense spending by 2014 and British spending cuts of 10% to 20% (around $6 – $12 billion). Europeans are labeled by Americans as socialists because of their lengthy paid vacations, maternity leaves, and generous healthcare benefits. More power to them and I desire all those things for myself and my family too, but I just don’t want my taxes to pay for others’ benefits when our country cannot afford those same wonderful benefits for ourselves.

While our Defense Secretary, Robert Gates, has been talking a good game with respect to a $100 billion in savings cuts, these cuts should be put in the context of a $567 billion budget for 2011 and a $700 billion estimated 2015 budget. As it turns out, these $100 billion in cuts are not cuts at all – Gates is also talking out of the other side of his mouth by saying he wants to continue increasing overall defense spending.

Is the size of spending appropriate? According to SIPRI, an independent international research institute, the U.S. defense budget accounts for 54% of the world’s total military spending, when our population only represents less than 5% of the world’s total. If that is not a disproportionate subsidy to the rest of the world, then I do not know what one is? The real longer term threat is not Iran or North Korea, but rather China. I’ll go out on a limb and say we can probably hold our own for a while, considering China is still only spending about 15% of what we spend on defense.

As I stated earlier, it is more important than ever to do more with less. Corporations are clearly doing that now by cutting spending, while still able to create record profits. The government has to get on board with trimming fat in all areas of our government…including defense. Coordinating intelligence and combining resources across the globe is crucial if we want to get more bang for our buck, while still devoting adequate resources to fend off the real and immediate evil threats of terrorism. Babysitting is an important duty and responsibility, but as impoverished Americans we are not capable of providing that service to the whole world free of charge.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in GE, LMT, Rolls Royce, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Will the Fiscal Donkey Fly?

Source: TopPayingIdeas.com/blog

Will Barack Obama become a “one-termer” like somewhat recent Presidents, Democrat Jimmy Carter (1977-1981) and Republican George H.W. Bush #41 (1989-1993)? Or will Obama get the Democratic donkey off the ground like Bill Clinton managed to do after the 1994 mid-term election when Republican Newt Gingrich spearheaded the Contract with America, which led to a similar Republican majority in the House of Representatives. Clinton’s approval ratings were in the dumps at the time, comparable to voter’s current lackluster opinion of Obama and his spending spree (see also Profitless Healthcare).

Source: Gallup

Reagan Rebound

Similarly, Republican Ronald Reagan (1981-1989) was picking up the pieces with his lousy approval rating after the 1982 midterm election. Tax cuts, “trickle-down” supply side economics, and a tough stance on the Russian Cold War turned around the economy and his approval rating and catapulted him to reelection in a landslide victory. Reagan carried 49 states with the help of Reagan Democrats (one-quarter of registered Democrats voted for him).

Source: The Wall Street Journal

One should be clear though, popularity is not the only factor that plays into reelection success. George H. W. Bush had the highest average approval rating in five decades (60.9% approval), only superseded by John F. Kennedy (70.1% approval). The economy, international politics, and other external factors also play a large role in the reelection process.

Flying Donkey Time?

If President Obama wants to get the Democratic donkey off the ground and raise his current approval rating of 47% and remedy his self-admitted “shellacking” by the Republicans, then he will need to shift his hard-left political agenda more towards the middle, like Clinton did in 1994. If he leads on ideology alone, then the next two years will likely be a long tough slog for him and his Democratic colleagues.

In order to shift toward the center and gain more Independent voters, Obama will need to find common ground with Republicans and Tea-Partiers. Obama has already conceded in principle to extend the Bush tax cuts, but if he wants to gain more political capital, he will have to gain some ground in the area of fiscal responsibility. With the help of a strong economy, Clinton managed to run surpluses, but front and center today is a $1.3 trillion deficit and over $13 trillion in debt. The first step in building any credibility on the issue will come on December 1st when the president’s bi-partisan commission for deficit reduction will release its report.

It will be interesting which party will show leadership in making unpopular spending cuts, just as the 2012 re-election cycle just begins. The elephants in the room are the entitlements (Medicare and Social Security), and although less talked about, efficient cuts to defense spending should be put on the table. Sure, pork barrel spending, inefficient subsidies, tax loopholes, are gaps that need to be filled, but they alone are rounding errors given our country’s unsustainable current circumstances. Whether or not politicians (red or blue) will point out the unpopular elephants in the room will be interesting to watch.

Financial irresponsibility at the consumer and corporate level were major drivers behind the 2008-2009 financial crisis, and both individuals and businesses are responsibly adjusting their expense structures and balance sheets. Our government has to wake up to reality and adjust its expense structure and balance sheet too. Although foreign countries have reacted (i.e., European austerity), egotistical American politicians on both sides of the aisle haven’t quite woken up and smelled the coffee yet. Thank goodness for the democracy that we live in because citizens are pointing to the elephants in the room and demanding reckless spending and debt levels to come under control. If President Barack Obama doesn’t want to become another one-termer, he’ll have to move more to the center and get the finances of our country under control. If the stubborn donkey refuses to deal with reality and remains flightless, hopefully an elephant or ship-full of tea partiers can get this grass roots call for fiscal sanity off the ground.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Debt Control: Turn Off Costly Sprinklers When Raining

By living in Southern California, I am acutely aware of the water shortage issues we face in this region of the country. We all have our pet peeves, and one that eats at me repeatedly occurs when I drive by a neighbor’s house and notice they are blasting the sprinklers in the pouring rain. I get the same sensation when I read about out-of control government spending confronting our current and future generations in light of the massive debt loads we presently carry.

I, like most people, love free stuff, whether it comes in the form of tooth-pick skewered, teriyaki meatball samples at Costco Wholesale Corp. (COST), or free government education from our school systems. But in times of torrential downpours, at a minimum, we need to be a little more cost conscious of our surroundings and turn off the spending sprinklers.

Certainly, when it comes to government spending, there’s no getting around the entitlement elephant in the room, which accounts for the majority of our non-discretionary government spending (see D-E-B-T: New Four Letter Word article). Unfortunately, layering on new entitlements on top of already unsustainable promises is not aiding our cause. For example, showering our Americans with free drugs as part of Medicare Part D program, and paying for tens of millions into a fantasy-based universal healthcare package (purported to save money…good luck) only serves to fatten up the elephant squeezed into our room.

Reform is absolutely necessary and affordable healthcare should be made available to all, but it is important to cut spending first. Then, subsequently, we will be in a better position to serve the needy with the associated savings. Instead, what we chose appears to have been a jamming of a massive, complex, divisive bill through Congress.

Slome’s Spending Rules

In an effort to guide ourselves back onto a path of sensibility, I urge our government legislators to follow these basic rules as a first step:

Rule #1 – Don’t Pay Dead People: I know we have an innate maternal/paternal instinct to help out others, but perhaps our government could stop doling out taxpayer dollars to buried individuals underground or those people incarcerated in jail? Over the last three years the government sent $180 million in benefit checks to 20,000 corpses, and also delivered $230 million to 14,000 convicted felons (read more).

Rule #2 – Pay for Our Own First: Before we start spending money on others outside our borders, I propose we tend to our flock first. For starters, our immigration policies are a disaster. As I wrote earlier (read Our Nation’s Keys to Success), I am a big proponent of legal immigration for productive, higher-educated individuals – not elitist, just practical. If you don’t believe me, just count the jobs created by the braniac immigrant founders at the likes of Google Inc. (GOOG), Intel Corp. (INTC), and Yahoo! Inc. (YHOO). These are the people who will create jobs and out-battle scrappy, resourceful international competitors that want to steal our jobs and our economic leadership position in the world. What I don’t support is illegal immigration – paying for the healthcare and education of foreign criminals with our country’s maxed-out credit cards. This is the equivalent of someone breaking into my house, and me making their bed and feeding them breakfast…ridiculous. I do not support the immigration law passed in Arizona, but this unfortunate chain of events thankfully puts a spotlight on the issue.

Rule #2a. – Stop Being the Globe’s Free Police: If we are going to comb the caves of Tora Bora as part of funding two wars and chasing terrorists all over the world, then we not only should be spending our defense budget more efficiently (non-Cold War mentality), but also charging freeloaders for our services (directly or indirectly). We are spending a whopping 20 cents of each federal tax dollar on defense, so let’s spend it wisely and charge those outside our borders benefiting from our monetary and physical sacrifices. And, oh by the way, sending $400 million to the territory controlled by Hamas (read more) doesn’t sound like the brightest decision given our fiscal and human challenges at home. I sure hope there are some tangible, accountable benefits accruing to the right people when we have 25 million people here in the U.S. unemployed, underemployed, or discouraged from finding a job.

Rule #3: Put the Obese Elephant on a Diet – As I alluded to above, our government doesn’t need to serve our overweight, entitlement-fed elephant more chocolate, pizza, and ice cream in the form of more entitlements we are not capable of funding. Let’s cut our spending first before we buy off the voters with new spending.

There are obviously a wide ranging set of economic, political, and even religious perspectives on the best ways of managing our hefty debt and deficits. I do not pretend to have all the answers, but what I do know is it is not wise to blast the sprinklers when it is pouring rain outside.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and GOOG, but at the time of publishing SCM had no direct positions in COST, YHOO, INTC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Digging a Debt Hole

Little did I know when I signed up for a recent “distressed” debt summit (see previous article) that a federal official and state treasurer would be presenting as keynote speakers? After all, this conference was supposed to be catering to those professionals interested in high risk securities. Technically, California and the U.S. government are not classified as distressed yet, but nonetheless government heavy-hitters Matthew Rutherford (Deputy Assistant Secretary, Federal Finance at the U.S. Department of Treasury), and Bill Lockyer (Treasurer for the State of California) shared their perspectives on government debt and associated economic factors.

Why have government officials present at a distressed debt conference? After questioning a few organizers and attendees, I was relieved to discover the keynote speaker selections were made more as a function as a sign of challenging economic times, rather than to panic participants toward debt default expectations. As it turns out, the conference organizers packaged three separate conferences into one event – presumably for cost efficiencies (Distressed Investments Summit + Public Funds Summit + California Municipal Finance Conference).

The U.S. Treasury Balancing Act

Effectively operating as the country’s piggy bank, the Treasury has a very complex job of constantly filling the bank to meet our country’s expenditures. Deputy Assistant Secretary Matthew Rutherford launched the event by speaking to domestic debt levels and deficits along with some the global economic trends impacting the U.S.

- Task at Hand: Rutherford spoke to the Treasury’s three main goals as part of its debt management strategy, which includes: 1) Cash management (to pay the government bills); 2) Attempt to secure low cost financing; and 3) Promote efficient markets. With more than a few hundred auctions held each year, the Treasury manages an extremely difficult balancing act.

- Debt Limit Increased: The recent $1.9 trillion ballooning in the U.S. debt ceiling to $14.3 trillion gives the Treasury some flexibility in meeting the country’s near-term funding needs. The Treasury expects to raise another $1.5 trillion in debt in 2010 (from $1.3 trillion in ’09) to fund our government initiatives, but that number is expected to decline to $1.0 – $1.1 trillion in 2011.

- Funding Trillions at 0.16%: Thanks to abnormally low interest rates, an investor shift to short-term safety (liquidity), and a temporary rush to the dollar, the U.S. Treasury was able to finance their borrowing needs at a mere 16 basis points. Clearly, servicing the U.S.’ massive debt load at these extremely attractive rates is not sustainable forever, and the Treasury is doing its best to move out on the yield curve (extend auctions to lengthier maturities) to lock in lower rates and limit the government’s funding risk should short-term rates spike.

- Chinese Demand Not Waning: Contrary to recent TIC (Treasury International Capital) data that showed Japan jumping to the #1 spot of U.S. treasury holders, Rutherford firmly asserted that China remains at the top by a significant margin of $140 billion, if you adjust certain appropriate benchmarks. He believes foreign ownership at over 50% (June 2009) remains healthy and steady despite our country’s fiscal problems.

- TIPS Demand on the Rise: Appetite for Treasury Inflation Protection Securities is on the rise, therefore the Treasury has its eye on expanding its TIP offerings into longer maturities, just last week they handled their first 3-year TIPS auction.

There is no “CA” in Greece

State of California Treasurer Bill Lockyer did not sugarcoat California’s fiscal problems, but he was quick to defend some of the comparisons made between Greece and California. First of all, California’s budget deficit represents less than 1% of the state’s GDP (Gross Domestic Product) versus 13% for Greece. Greece’s accumulated debt stands at 109% of GDP – for California debt only represents 4% of the state’s GDP. What’s more, since 1800 Greece has arguably been in default more than not, where as California has never in its history defaulted on an obligation.

The current California picture isn’t pretty though. This year’s fiscal budget deficit is estimated at $6 billion, leaping to $12 billion next year, and soaring to $20 billion per year longer term.

Legislative political bickering is at the core of the problem due to the constitutional inflexibility of a 2/3 majority vote requirement to get state laws passed. The vast bulk of states require a simple majority vote (> than 50%) – California holds the unique super-majority honor with only Arkansas and Rhode Island. Beyond mitigating partisan bickering, Lockyer made it clear no real progress would be made in budget cuts until core expenditures like education, healthcare, and prisons are attacked.

On the subject of bloatedness, depending on how you define government spending per capita, California ranks #2 or #4 lowest out of all states. Economies of scale help in a state representing 13% of the U.S.’ GDP, but Lockyer acknowledged the state could just be less fat than the other inefficient states.

Lockyer also tried to defend the state’s 10.5% blended tax rate (versus the national median of 9.8%), saying the disparity is not as severe as characterized by the media. He even implied there could be a little room to creep that rate upwards.

Finishing on an upbeat note, Lockyer recognized the January state revenues came in above expectations, but did not concede victory until a multi-month trend is established.

After filtering through several days of meetings regarding debt, you quickly realize how the debt culture (see D-E-B-T article), thanks to cheap money, led to a glut across federal governments, state governments, corporations, and consumers. Hopefully we have learned our lesson, and we are ready to climb out of this self created hole…before we get buried alive with risky debt.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including CMF and TIP), but at time of publishing had no direct position on any security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}