Posts tagged ‘default’

Greece: The Slow Motion, Multi-Year Train Wreck

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2015). Subscribe on the right side of the page for the complete text.

Watching Greece fall apart over the last five years has been like watching a slow motion train wreck. To many, this small country of 11 million people that borders the Mediterranean, Aegean, and Ionian Seas is known more for its Greek culture (including Zeus, Parthenon, Olympics) and its food (calamari, gyros, and Ouzo) than it is known for financial bailouts. Nevertheless, ever since the financial crisis of 2008-2009, observers have repeatedly predicted the debt-laden country will default on its €323 billion mountain of obligations (see chart below – approximately $350 billion in dollars) and subsequently exit the 19-member eurozone currency membership (a.k.a.,”Grexit”).

Source: MoneyMorning.com and CNN

Now that Greece has failed to repay less than 1% of its full €240 billion bailout obligation – the €1.5 billion payment due to the IMF (International Monetary Fund) by June 30th – the default train is coming closer to falling off the tracks. Whether Greece will ultimately crash itself out of the eurozone will be dependent on the outcome of this week’s surprise Greek referendum (general vote by citizens) mandated by Prime Minister Alexis Tsipras, the leader of Greece’s left-wing Syriza party. By voting “No” on further bailout austerity measures recommended by the European Union Commission, including deeper tax increases and pension cuts, the Greek people would effectively be choosing a Grexit over additional painful tax increases and deeper pension cuts.

Ouch!

And who can blame the Greeks for being a little grouchy? You might not be too happy either if you witnessed your country experience an economic decline of greater than 25% (see Greece Gross Domestic Product chart below); 25% overall unemployment (and 50% youth unemployment); government worker cuts of greater than 20%; and stifling taxes to boot. Sure, Greeks should still shoulder much of the blame. After all, they are the ones who piled on $100s of billions of debt and overspent on the pensions of a bloated public workforce, and ran unsustainable fiscal deficits.

Source: TradingEconomics.com

For any casual history observers, the current Greek financial crisis should come as no surprise, especially if you consider the Greeks have a longstanding habit of not paying their bills. Over the last two centuries or so, since the country became independent, the Greek government has spent about 90 years in default (almost 50% of the time). More specifically, the Greeks defaulted on external sovereign debt in 1826, 1843, 1860, 1894 and 1932.

The difference between now and past years can be explained by Greece now being a part of the European Union and the euro currency, which means the Greeks actually do have to pay their bills…if they want to remain a part of the common currency. During past defaults, the Greek central bank could easily devalue their currency (the drachma) and fire up the printing presses to create as much currency as needed to pay down debts. If the planned Greek referendum this week results in a “No” vote, there is a much higher probability that the Greek government will need to dust off those drachma printing presses.

“Perspective People”

Protest, riots, defaults, changing governments, and new currencies make for entertaining television viewing, but these events probably don’t hold much significance as it relates to the long-term outlook of your investments and the financial markets. In the case of Greece, I believe it is safe to say the economic bark is much worse than the bite. For starters, Greece accounts for less than 2% of Europe’s overall economy, and about 0.3% of the global economy.

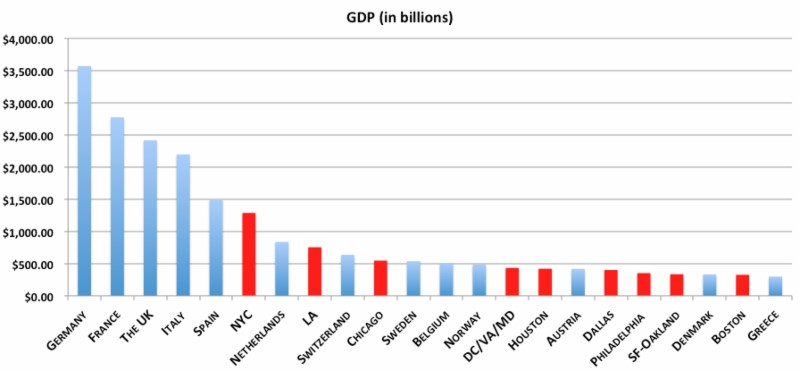

Since I live out on the West Coast, the chart below caught my fancy because it also places the current Greek situation into proper proportion. Take the city of L.A. (Los Angeles – red bar) for example…this single city alone accounts for almost 3x the size of Greece’s total economy (far right on chart – blue bar).

Give Me My Money!

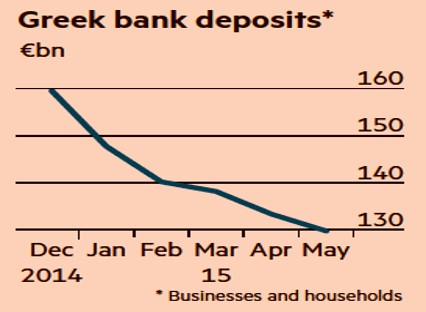

It hasn’t been a fun year for Greek banks. Depositors, who have been flocking to the banks, withdrew about $45 billion in cash from their accounts, over an eight month period (see chart below). Before the Greek government decided to mandatorily close the banks in recent days and implement capital controls limiting depositors to daily ATM withdrawals of only $66.

Source: The Financial Times

But once again, let’s put the situation into context. From an overall Greek banking sector perspective, the four largest Greek Banks (Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank) account for about 90% of all Greek banking assets. Combined, these banks currently have an equity market value of about $14 billion and assets on the balance sheets of $400 billion – these numbers are obviously in flux. For comparison purposes, Bank of America Corp. (BAC) alone has an equity market value of $179 billion and $2.1 trillion in assets.

Anxiety Remains High

Skeptical bears will occasionally acknowledge the miniscule-ness of Greece, but then quickly follow up with their conspiracy theory or domino effect hypothesis. In other words, the skeptics believe a contagion effect of an impending Grexit will ripple through larger economies, such as Italy and Spain, with crippling force. Thus far, as you can see from the chart below, Greece’s financial problems have been largely contained within its borders. In fact, weaker economies such as Spain, Portugal, Ireland, and Italy have fared much better – and actually improving in most cases. In recent days, 10-year yields on government bonds in countries like Portugal, Italy, and Spain have hovered around or below 3% – nowhere near the peak levels seen during 2008 – 2011.

Source: Business Insider

Other doubting Thomases compare Greece to situations like Lehman Brothers, Long Term Capital Management, and the subprime housing market, in which underestimated situations snowballed into much worse outcomes. As I explain in one of my newer articles (see Missing the Forest for the Trees), the difference between Greece and the other financial collapses is the duration of this situation. The Greek circumstance has been a 5-year long train wreck that has allowed everyone to prepare for a possible Grexit. Rather than agonize over every news headline, if you are committed to the practice of worrying, I would recommend you focus on an alternative disaster that cannot be found on the front page of all newspapers.

There is bound to be more volatility ahead for investors, and the referendum vote later this week could provide that volatility spark. Regardless of the news story du jour, any of your concerns should be occupied by other more important worrisome issues. So, unless you are an investor in a Greek bank or a gyro restaurant in Athens, you should focus your efforts on long-term financial goals and objectives. Ignoring the noisy news flow and constructing a diversified investment portfolio across a range of asset classes will allow you to avoid the harmful consequences of the slow motion, multi-year Greek train wreck.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and BAC, but at the time of publishing, SCM had no direct position in Bank of Greece, Piraeus Bank, Eurobank Ergasias, Alpha Bank or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on ICContact page.

Inflation and the Debt Default Paradox

With the federal government anchored down with over $14 trillion in debt and trillion dollar deficits as far as the eye can see, somehow people are shocked that Standard & Poor’s downgraded its outlook on U.S. government debt to “Negative” from “Stable.” This is about as surprising as learning that Fat Albert is overweight or that Charlie Sheen has a substance abuse problem.

Let’s use an example. Suppose I received a pay demotion and then I went on an irresponsible around-the-world spending rampage while racking up over $1,000,000.00 in credit card debt. Should I be surprised if my 850 FICO score would be reviewed for a possible downgrade, or if credit card lenders became slightly concerned about the possibility of collecting my debt? I guess I wouldn’t be flabbergasted by their anxiety.

Debt Default Paradox?

With the recent S&P rating adjustment, pundits over the airwaves (see CNBC video) make the case that the U.S. cannot default on its debt, because the U.S. is a sovereign nation that can indefinitely issue bonds in its own currency (i.e., print money likes it’s going out of style). There is some basis to this argument if you consider the last major developed country to default was the U.S. government in 1933 when it went off the gold standard.

On the other hand, non-sovereign nations issuing foreign currencies do not have the luxury of whipping out the printing presses to save the day. The Latin America debt defaults in the 1980s and Asian Financial crisis in the late 1990s are examples of foreign countries over-extending themselves with U.S. dollar-denominated debt, which subsequently led to collapsing currencies. The irresponsible fiscal policies eventually destroyed the debtors’ ability to issue bonds and ultimately repay their obligations (i.e., default).

Regardless of a country’s strength of currency or central bank, if reckless fiscal policies are instituted, governments will eventually be left to pick their own poison…default or hyperinflation. One can think of these options as a favorite dental procedure – a root canal or wisdom teeth pulled. Whether debtors get paid 50 cents on the dollar in the event of a default, or debtors receive 100 cents in hyper-inflated dollars (worth 50% less), the resulting pain feels the same – purchasing power has been dramatically reduced in either case (default or hyperinflation).

Of course, Ben Bernanke and the Federal Reserve Bank would like investors to believe a Goldilocks scenario is possible, which is the creation of enough liquidity to stimulate the economy while maintaining low interest rates and low inflation. At the end of the day, the inflation picture boils down to simple supply and demand for money. Fervent critics of the Fed and Bernanke would have you believe the money supply is exploding, and hyperinflation is just around the corner. It’s difficult to quarrel with the printing press arguments, given the size and scale of QE1 & QE2 (Quantitative Easing), but the fact of the matter is that money supply growth has not exploded because all the liquidity created and supplied into the banking system has been sitting idle in bank vaults – financial institutions simply are not lending. Eventually this phenomenon will change as the economy continues to recover; banks adequately build their capital ratios; the housing market sustainably recovers; and confidence regarding borrower creditworthiness improves.

Scott Grannis at the California Beach Pundit makes the point that money supply as measured by M2 has shown a steady 6% increase since 1995, with no serious side-effects from QE1/QE2 yet:

- Source: Calafia Beach Pundit

In fact, Grannis states that money supply growth (+6%) has actually grown less than nominal GDP over the period (+6.7%). Money supply growth relative to GDP growth (money demand) in the end is what really matters. Take for instance an economy producing 10 widgets for $10 dollars, would have a CPI (Consumer Price Index) of $1 per widget and a money supply of $10. If the widget GDP increased by 10% to 11 widgets (10 widgets X 1.1) and the Federal Reserve increased money supply by 10% to $11, then the CPI index would remain constant at $1 per widget ($11/11 widgets). This is obviously grossly oversimplified, but it makes my point.

Gold Bugs Banking on Inflation or Collapse

Gold prices have been on a tear over the last 10 years and current fiscal and monetary policies have “gold bugs” frothing at the mouth. These irresponsible policies will no doubt have an impact on gold demand and gold prices, but many gold investors fail to acknowledge a gold supply response. Take for example Freeport-McMoRan Copper & Gold Inc. (FCX), which just reported stellar quarterly sales and earnings growth today (up 31% and 57%, respectively). FCX more than doubled their capital expenditures to more than $500 million in the quarter, and they are planning to double their exploration spending in fiscal 2011. Is Freeport alone in their supply expansion plans? No, and like any commodity with exploding prices, eventually higher prices get greedy capitalists to create enough supply to put a lid on price appreciation. For prior bubbles you can reference the recent housing collapse or older burstings such as the Tulip Mania of the 1600s. One of the richest billionaires on the planet, Warren Buffett, also has a few thoughts on the prospects of gold.

The recent Standard & Poor’s outlook downgrade on U.S. government debt has caught a lot of press headlines. Fears about a technical default may be overblown, but if fiscal constraint cannot be agreed upon in Congress, the alternative path to hyperinflation will feel just as painful.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in FCX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Digging a Debt Hole

Little did I know when I signed up for a recent “distressed” debt summit (see previous article) that a federal official and state treasurer would be presenting as keynote speakers? After all, this conference was supposed to be catering to those professionals interested in high risk securities. Technically, California and the U.S. government are not classified as distressed yet, but nonetheless government heavy-hitters Matthew Rutherford (Deputy Assistant Secretary, Federal Finance at the U.S. Department of Treasury), and Bill Lockyer (Treasurer for the State of California) shared their perspectives on government debt and associated economic factors.

Why have government officials present at a distressed debt conference? After questioning a few organizers and attendees, I was relieved to discover the keynote speaker selections were made more as a function as a sign of challenging economic times, rather than to panic participants toward debt default expectations. As it turns out, the conference organizers packaged three separate conferences into one event – presumably for cost efficiencies (Distressed Investments Summit + Public Funds Summit + California Municipal Finance Conference).

The U.S. Treasury Balancing Act

Effectively operating as the country’s piggy bank, the Treasury has a very complex job of constantly filling the bank to meet our country’s expenditures. Deputy Assistant Secretary Matthew Rutherford launched the event by speaking to domestic debt levels and deficits along with some the global economic trends impacting the U.S.

- Task at Hand: Rutherford spoke to the Treasury’s three main goals as part of its debt management strategy, which includes: 1) Cash management (to pay the government bills); 2) Attempt to secure low cost financing; and 3) Promote efficient markets. With more than a few hundred auctions held each year, the Treasury manages an extremely difficult balancing act.

- Debt Limit Increased: The recent $1.9 trillion ballooning in the U.S. debt ceiling to $14.3 trillion gives the Treasury some flexibility in meeting the country’s near-term funding needs. The Treasury expects to raise another $1.5 trillion in debt in 2010 (from $1.3 trillion in ’09) to fund our government initiatives, but that number is expected to decline to $1.0 – $1.1 trillion in 2011.

- Funding Trillions at 0.16%: Thanks to abnormally low interest rates, an investor shift to short-term safety (liquidity), and a temporary rush to the dollar, the U.S. Treasury was able to finance their borrowing needs at a mere 16 basis points. Clearly, servicing the U.S.’ massive debt load at these extremely attractive rates is not sustainable forever, and the Treasury is doing its best to move out on the yield curve (extend auctions to lengthier maturities) to lock in lower rates and limit the government’s funding risk should short-term rates spike.

- Chinese Demand Not Waning: Contrary to recent TIC (Treasury International Capital) data that showed Japan jumping to the #1 spot of U.S. treasury holders, Rutherford firmly asserted that China remains at the top by a significant margin of $140 billion, if you adjust certain appropriate benchmarks. He believes foreign ownership at over 50% (June 2009) remains healthy and steady despite our country’s fiscal problems.

- TIPS Demand on the Rise: Appetite for Treasury Inflation Protection Securities is on the rise, therefore the Treasury has its eye on expanding its TIP offerings into longer maturities, just last week they handled their first 3-year TIPS auction.

There is no “CA” in Greece

State of California Treasurer Bill Lockyer did not sugarcoat California’s fiscal problems, but he was quick to defend some of the comparisons made between Greece and California. First of all, California’s budget deficit represents less than 1% of the state’s GDP (Gross Domestic Product) versus 13% for Greece. Greece’s accumulated debt stands at 109% of GDP – for California debt only represents 4% of the state’s GDP. What’s more, since 1800 Greece has arguably been in default more than not, where as California has never in its history defaulted on an obligation.

The current California picture isn’t pretty though. This year’s fiscal budget deficit is estimated at $6 billion, leaping to $12 billion next year, and soaring to $20 billion per year longer term.

Legislative political bickering is at the core of the problem due to the constitutional inflexibility of a 2/3 majority vote requirement to get state laws passed. The vast bulk of states require a simple majority vote (> than 50%) – California holds the unique super-majority honor with only Arkansas and Rhode Island. Beyond mitigating partisan bickering, Lockyer made it clear no real progress would be made in budget cuts until core expenditures like education, healthcare, and prisons are attacked.

On the subject of bloatedness, depending on how you define government spending per capita, California ranks #2 or #4 lowest out of all states. Economies of scale help in a state representing 13% of the U.S.’ GDP, but Lockyer acknowledged the state could just be less fat than the other inefficient states.

Lockyer also tried to defend the state’s 10.5% blended tax rate (versus the national median of 9.8%), saying the disparity is not as severe as characterized by the media. He even implied there could be a little room to creep that rate upwards.

Finishing on an upbeat note, Lockyer recognized the January state revenues came in above expectations, but did not concede victory until a multi-month trend is established.

After filtering through several days of meetings regarding debt, you quickly realize how the debt culture (see D-E-B-T article), thanks to cheap money, led to a glut across federal governments, state governments, corporations, and consumers. Hopefully we have learned our lesson, and we are ready to climb out of this self created hole…before we get buried alive with risky debt.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including CMF and TIP), but at time of publishing had no direct position on any security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}