Posts tagged ‘credit default swaps’

Mideast War an Investor Bore as Markets Soar

If I told you at the beginning of the year that the U.S. would bomb key nuclear sites in Iran, would you have guessed that Middle East stability would follow—and that global financial markets would soar to record highs? Personally, I wouldn’t have bet on that outcome. But that’s exactly what happened last month. While geopolitical dynamics remain fluid, markets shrugged off the chaos. The S&P 500 rallied +5.0%, the Dow Jones Industrial Average climbed +4.3%, and the NASDAQ catapulted +6.6%, powered largely by artificial intelligence stocks like NVIDIA Corp., which surged +16.9% for the month to a market value of $3.9 trillion (more on AI below). This is an important reminder that trading off of news headlines is a fool’s errand.

Economy Resilient Despite Tariffs and Geopolitical Turmoil

Source: Calafia Beach Pundit

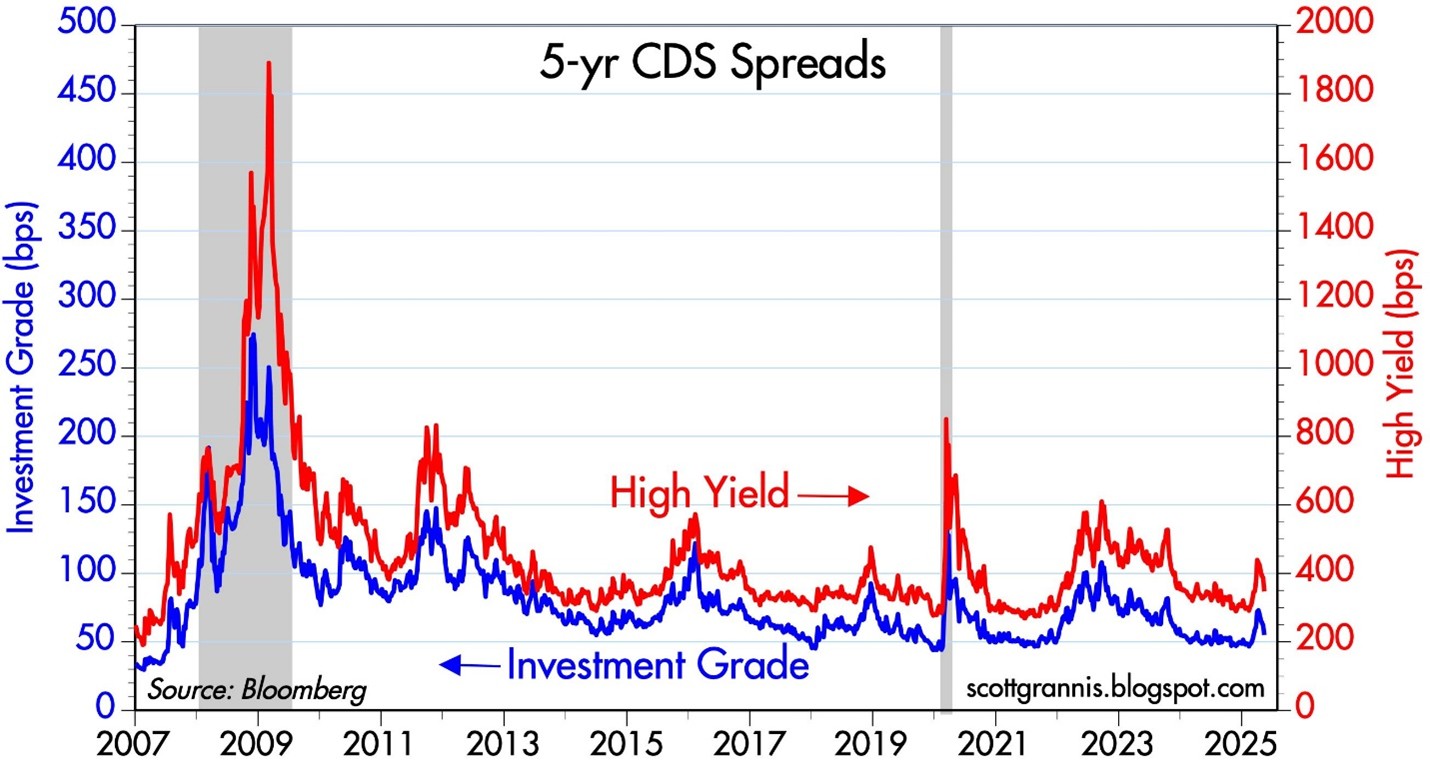

Credit Default Swaps (CDS) act as insurance contracts that protect investors against corporate debt defaults. During financial stress—like the 2008 crisis or the COVID crash in 2020—CDS prices surge as investors seek protection. Today, however, CDS prices are falling across both high-yield (junk bonds) and investment-grade (Blue Chip) debt. As seen in the chart above, the cost to insure corporate bonds has declined steadily over the past two years. This signals bond investors aren’t worried about a recession or a wave of defaults, despite tariff policy uncertainty, geopolitical risk, and modest GDP growth.

Inflation Tame as Tariffs Loom

President Trump has repeatedly criticized Fed Chair Jerome Powell for not cutting interest rates, calling him everything from a “dummy” to a “major loser” and a “stupid person” to a “numbskull”. While the name-calling is colorful, the economic pressure is real: U.S. GDP contracted -0.5% in Q1 2025. Powell, however, wants to see the full impact of upcoming tariffs before making a move. . A new tariff deadline looms on July 9th, and the market is anxiously awaiting clarity. But even if tariffs are implemented, many economists believe the inflationary impact will be temporary—what’s known as a one-time price shock.

Source: Calafia Beach Pundit

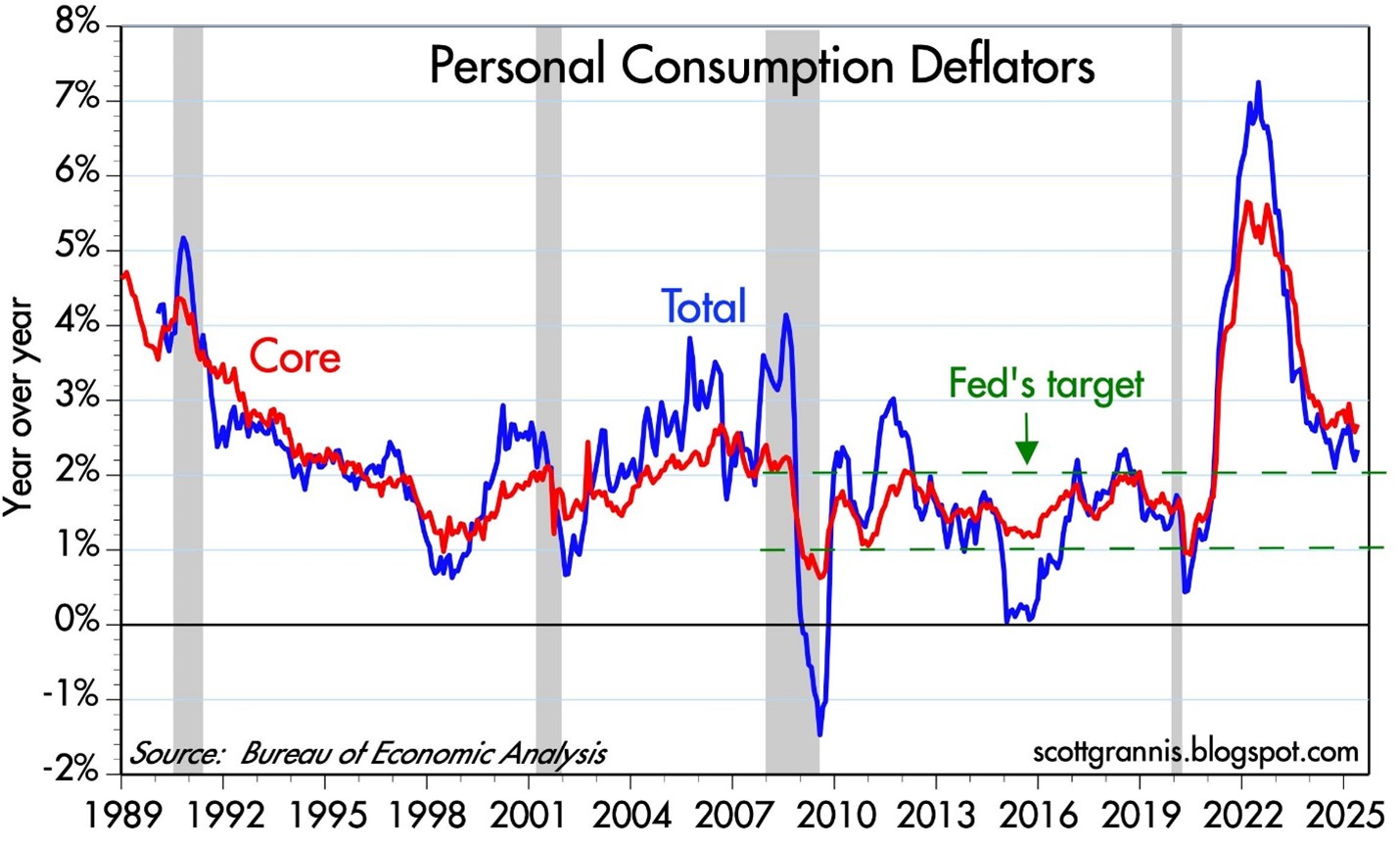

The Fed’s preferred inflation gauge—the Personal Consumption Expenditure (PCE) index—has been easing and is now near the 2% target (see chart above). With inflation cooling, Trump’s case for rate cuts gains credibility. Still, the Fed appears in no rush. It will take time to understand the lasting effects of the tariff rollout.

AI Wave Fueling Markets

For a generation, the semiconductor revolution has quietly powered innovation, guided by Moore’s Law—the principle that chip performance doubles roughly every two years (see my article The Traitorous 8). Sixty years after Gordon Moore wrote his seminal article, “Cramming More Components onto Integrated Circuits”, the power of software is catching up. NVIDIA’s Grace Blackwell GB200 chip contains an astronomical 208 billion transistors, supercharging AI software models like ChatGPT.

The AI revolution is fueling trillions in global investment and rapidly transforming industries – from data centers and self-driving cars to robotics and drug discovery. It’s important to realize that this AI arms race is not just occurring in the United States. AI investment spending extends way beyond Silicon Valley to countries like Saudi Arabia, Singapore, and China.

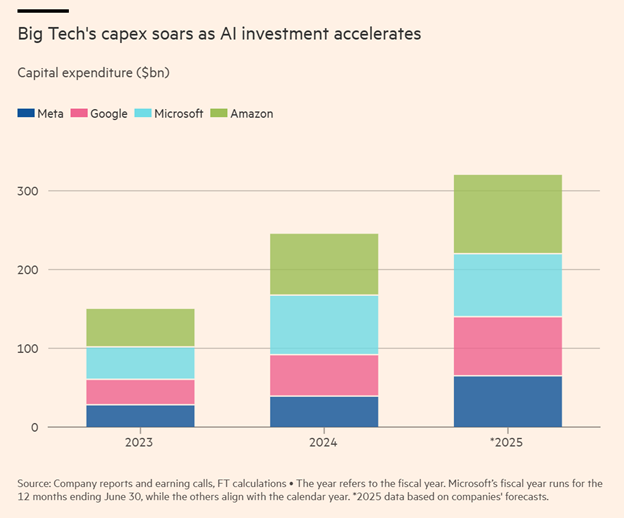

The AI boom is not a U.S.-only phenomenon. Countries like China, Saudi Arabia, and Singapore are pouring capital into AI, creating a global arms race in tech. In the U.S., the four biggest hyperscalers—Amazon, Microsoft, Google, and Meta—are projected to spend over $300 billion on capital expenditures in 2025 alone (see chart below).

To illustrate the scale: Amazon is forecasted to spend more than $100 billion in CapEx this year. For context, that’s 40% more than the company spent over the entire 2000–2020 period combined.

Source: The Financial Times

The Stargate Initiative: AI Infrastructure on a Galactic Scale

A prime example of the AI gold rush is the $500 billion Stargate initiative, with Phase 1 already underway in Abilene, Texas (see rendering below). The initial construction includes two buildings totaling 1,000,000 square feet. Ultimately, the full project will cove about 1,000 acres and be powered by an on-site natural gas facility generating 360 megawatts—enough to support 300,000 homes.

A huge portion of the project costs are dedicated to the budget for NVIDIA super chips. Oracle Corp. has committed $40 billion to purchase 400,000 of NVIDIA’s GB200 chips, making this project a centerpiece of the global AI infrastructure boom. Just this week, Oracle also announced a new $30 billion cloud deal, which will soak up a good chunk of the data center supply created by the database and enterprise software company.

Source: CoStar

The Big Picture: Volatility and Opportunity

There’s no shortage of risk—geopolitics, inflation, Fed uncertainty, tariffs. But the economy is showing surprising resilience. If tariff clarity improves, interest rate cuts materialize, and AI capital spending accelerates, a “boring” market could rapidly turn into a soaring one.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

The European Dog Ate My Homework

I never thought my daily routine would be dominated by checking European markets before our domestic open, but these days it is appearing like the European tail is wagging the global dog. Tracking Spanish bond yields from the Tesoro Publico and the Italia Borsa index is currently having a larger bearing on my portfolio than U.S. fundamentals. When explaining short term performance to others, I feel a little like an elementary school student making an excuse that my dog ate my homework.

Although the multi-year European saga has gone on for years, this too shall pass. What’s more, despite the bailouts of Portugal, Ireland, and Greece in recent years, the resilient U.S. economy has recorded 11 consecutive quarters of GDP (Gross Domestic Product) growth and added more than 4 million jobs, albeit at a less than desirable pace.

Could it get worse? Certainly. Will it get worse before it gets better? Probably. Is worsening European fundamentals and a potential Greek eurozone exit already factored into current stock prices? Possibly. The truth of the matter is that nobody knows the answers to these questions with certainty. At this point, the probability of an unknown or unexpected event in a different geography is more likely to be the cause of our economic downfall than a worsening European crisis. As sage investor and strategist Don Hays aptly points out, “When everyone is concerned about a problem, that problem is solved.” That may be overstating the truth a bit, but I do believe the issues absent from current headlines are the matters we should be most concerned about.

The European financial crisis may drag on for a while longer, but nothing lasts forever. Years from now, worries about the PIIGS countries (Portugal, Ireland, Italy, Greece, Spain) will switch to others, like the BRICs (Brazil, Russia, India, China) or other worry geography du jour. The issues of greatest damage in 2008-2009, like Bear Stearns, Lehman Brothers, AIG, CDS (credit default swaps), and subprime mortgages, didn’t dominate the headlines for years like the European crisis stories of today. As compared to Europe’s problems, these prior pains felt like Band Aids being quickly ripped off.

Correlation Conundrum

Eventually European worries will be put on the backburner, but until some other boogeyman dominates the daily headlines, our financial markets will continue to correlate tightly with European security prices. How does one fight these tight correlations? For starters, the correlations will not stay tight forever. If an investor can survive through the valley of strong security association, then the benefits will eventually accrue.

Although the benefits from diversification may disappear in the short-run, they should not be fully forgotten. Bonds, cash, and precious metals (i.e., gold) proved to be great portfolio diversifiers in 2008 and early 2009. Commodities, inflation protection, floating rate bonds, real estate, and alternative investments, are a few asset classes that will help diversify portfolios. Risk is defined in many circles as volatility (i.e., standard deviation) and combining disparate asset classes can lower volatility. But risk, defined as the potential of experiencing permanent losses, can also be controlled by focusing on valuation. By in large, large cap dividend paying stocks have struggled for more than a decade, despite equity dividend yields for the S&P 500 exceeding 10-year Treasury yields (the first time in more than 50 years). Investing in large companies with strong balance sheets and attractive growth prospects is another strategy of lowering portfolio risk.

Politics & Winston Churchill

Some factors however are out of shareholders hands, such as politics. As we know from last year’s debt ceiling melee and credit downgrade debacle, getting things done in Washington is very challenging. If you think achieving consensus in one country is difficult, imagine what it’s like in herding 17 countries? That’s the facts of life we are dealing with in the eurozone right now.

Although I am optimistic something will eventually get done, I consider myself a frustrated optimist. I am frustrated because of the gridlock, but optimistic because these problems are not rocket science. Rather these challenges are concepts my first grade child could understand:

• Expenses are running higher than revenues. You must cut expenses, increase revenues, or a combination thereof.

• Adding debt can support growth, but can lead to inflation. Cutting debt can hinder growth, but leads to a more sustainable fiscal state of wellbeing.

Relieving all the excess global leverage is a long, tortuous process. We saw firsthand here in the U.S. what happened to the U.S. real estate market and associated financial institutions when irresponsible debt consumption took place. Fortunately, corporations and consumers adjusted their all-you-can-eat debt buffet habits by going on a diet. As a matter of fact, corporations today are holding records amounts of cash and debt service loads for consumers has been reduced to levels not seen in decades (see chart below). Unlike governments, luckily CEOs and individuals do not need Congressional approval to adapt to a world of reality – they can simply adjust spending habits.

Source: Calafia Beach Pundit (Scott Grannis)

Governments, on the other hand, generally do need legislative approval to adjust spending habits. Regrettably, cutting the benefits of your constituents is not a real popular political strategy for accumulating votes or brownie points. If you don’t believe me, see what voters are doing to their leaders in Europe. Nicolas Sarkozy is the latest European leader to be booted from office due to austerity backlash and economic frustration. No less than nine European leaders have been cast aside since the financial crisis began.

The fate for U.S. politicians is less clear as we enter into a heated presidential election over the next six months. We do however know how the mid-term Congressional elections fared for the incumbents…not all sunshine and roses. Until elections are completed, we are resigned to the continued mind-numbing political gridlock, with no tangible resolutions to the trillion dollar deficits and gargantuan debt load. Obviously, most citizens would prefer a forward looking strategic plan from politicians (rather than a reactive one), but there are no signs that this will happen anytime soon…in either party.

Realistically though, tough decisions made by politicians only occur during crises, and if this slow-motion train wreck continues along this same path, then at least we have something to look forward to – forced resolution. We are seeing this firsthand in Greece. The “bond vigilantes” (see Plumbers & Cops) and responsible parents (i.e., Germany) have given Greece two options:

1.) Fix your financial problems and receive assistance; or

2.) Leave the EU (return to the Drachma currency) and figure your problems out yourself.

Panic has a way of forcing action, and we are approaching that “when push comes to shove” moment very quickly. I believe the Europeans are currently taking a note from our strategic playbook, which basically is the spaghetti approach – throw lots of things up on the wall and see what sticks. Or as Winston Churchill stated, “You can always count on Americans to do the right thing – after they’ve tried everything else.”

There is no question, the European sovereign debt issue is a complete mess, and there are no clear paths to a quick solution. Until voters force politicians into making tough unpopular decisions, or leaders come together with forward looking answers, the default position will be to keep kicking the fiscal can issues down the road. In the absence of political leadership, eventually the crisis will naturally force tough decisions to be made. Until then, I will go on explaining to others how the European dog ate my homework.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including commodities, inflation protection, floating rate bonds, real estate, dividend, and alternative investment ETFs), but at the time of publishing SCM had no direct position in AIG, JNJ, Bear Stearns, Lehman Brothers, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}