Posts tagged ‘corrections’

To Test or Retest?

In Shakespeare’s tragedy Hamlet, the main character Prince Hamlet raises the existential question to himself, “To be, or not to be, that is the question?” With the recent -13% correction in the S&P 500 index, and subsequent mini-rebound, a lot of investors have also been talking to themselves and asking the fundamental question, “To test or retest, that is the question?” The inability of Fed Chairwoman dove, Janet Yellen, to increase the Federal Funds interest rate target by 0.25% after nine years only increased short-term uncertainty.

For investors playing in the stock market, uncertainty and corrections are par for the course. Howard Getson at Capitalogix recently pointed out the following.

Since 1900, on average, we’ve experienced…

- -5% market corrections: 3 times/year.

- -10% market corrections: 1 time/ year.

- -20% market corrections: 1 time/3.5 years.

However, no market correction is the same. Sure it would be nice if, during every bull market, the pain from any -10% correction lasted a second – similar to ripping off a Band-Aid. Unfortunately, when you live through such rapid and violent corrections, as we just did, volatility tends to stick around for a while. And in many instances, any brief rebound in stock prices is met with another downdraft in prices that retests the recent lows in prices.

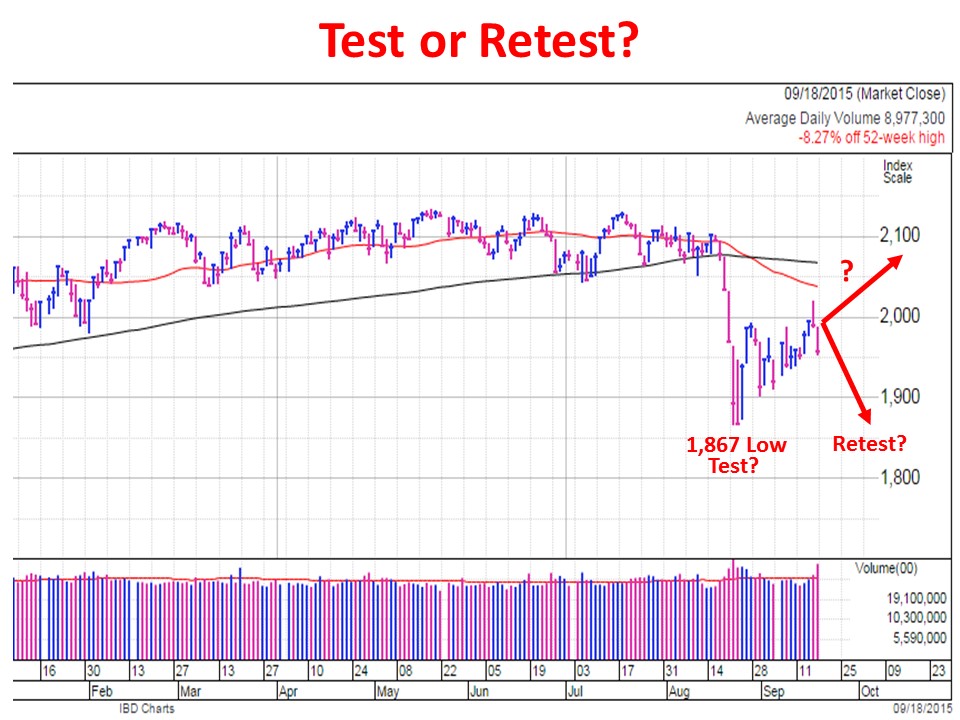

In the recent correction example, a retest of the lows would mean another -5% drop, on top of Friday’s -2% cut, to a level of 1,867 on the S&P 500 index. This is definitely a realistic probability (see chart below).

Chart Source: Investors.com (Powered by IBD)

Although corrections are quite common, violent corrections are less common. Scott St. Clair, an analyst at MarketSmith, a division of William O’Neil & Co., recently did a study examining the frequency of 10%+ corrections occurring in four days or less across the three major indices (Dow Jones Industrial, S&P 500, and NASDAQ). Before the latest -15% decline in the NASDAQ from August 19th to August 24th, St. Clair only identified drops of -10% or more (in four trading sessions) eight previous times since the Great Depression (six of the eight periods are listed below).

- DJIA May 1940 -26% in eight days

- DJIA May 1962 -16% in 10 days

- S&P 500 Aug 1998 -15% in five days

- S&P 500 July 2002 -25% in 13 days

- S&P 500 October 2008 -33% in 15 days.

- S&P 500 August 2011 -19% in 13 days

Following all these corrections, the market always rebounded, but what St. Clair showed was in many cases stock prices had to retest the previous lows before advancing again.

As Mark Twain said, “History doesn’t repeat itself but it often rhymes,” which explains why this study is a useful historical exercise to prepare investors for potential future downdrafts. With that said, for long-term investors, much of this utility is marginal at best and useless at worst.

If you can’t handle the volatility, you need a more diversified portfolio, or you need to park your money in a savings account or CD and watch it melt away to inflation.

In reviewing corrections, famed growth investor Peter Lynch said it best:

“I can’t recall ever once having seen the name of a market timer on Forbes’ annual list of the richest people in the world. If it were truly possible to predict corrections, you’d think somebody would have made billions by doing it.”

Whether the August 24th low was the only test of this correction, or investors retest it again, is a moot point. Ignoring irrelevant headlines and focusing your attention on a low-cost, tax-efficient, globally diversified investment portfolio is a better use of your time. That is a tenet for which Hamlet would certainly be willing to die.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) , but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Get Out of Stocks!*

Get out of stocks!* Why the asterisk mark (*)? The short answer is there is a certain population of people who are looking at alluring record equity prices, but are better off not touching stocks – I like to call these individuals the “sideliners”. The sideliners are a group of investors who may have owned stocks during the 2006-2008 timeframe, but due to the subsequent recession, capitulated out of stocks into gold, cash, and/or bonds.

The risk for the sideliners getting back into stocks now is straightforward. Sideliners have a history of being too emotional (see Controlling the Investment Lizard Brain), which leads to disastrous financial decisions. So, even if stocks outperform in the coming months and years, the sideliners will most likely be slow in getting back in, and wrongfully knee-jerk sell at the hint of an accelerated taper, rate-hike, or geopolitical sneeze. Rather than chase a stock market at all-time record highs, the sideliners would be better served by clipping coupons, saving, and/or finish that bunker digging project.

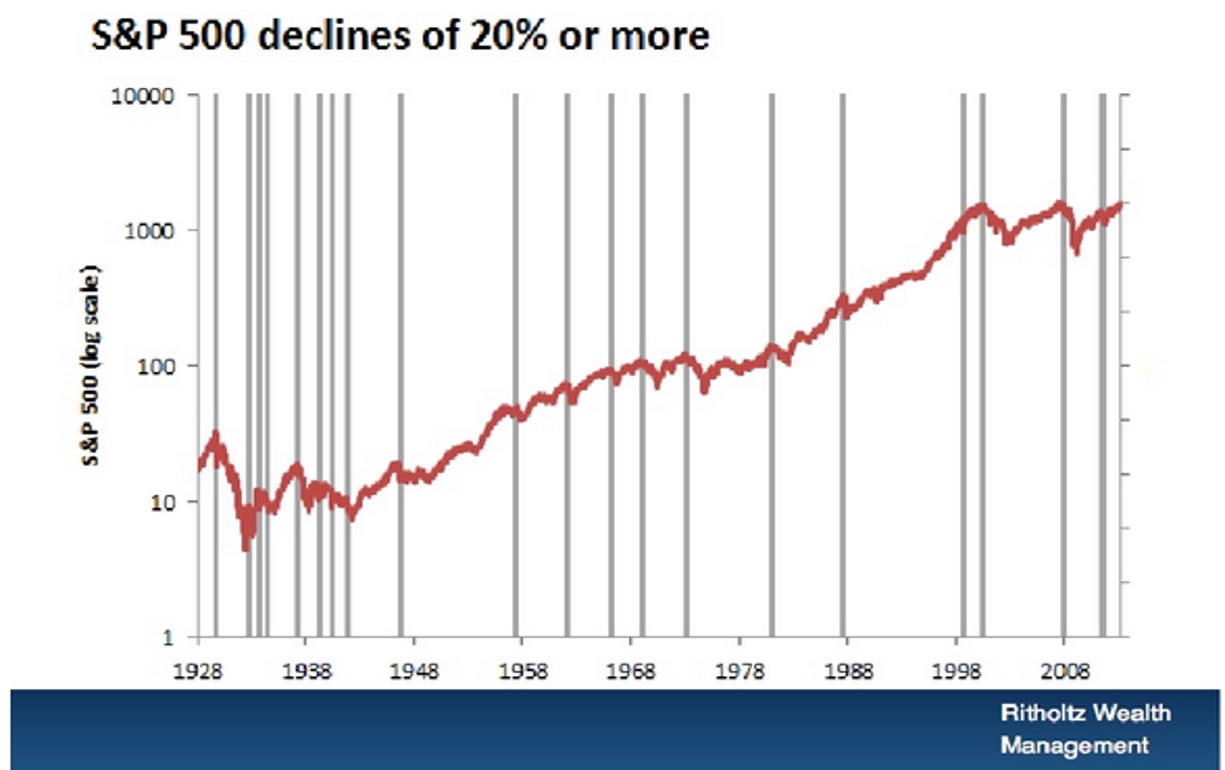

The fact is, if you can’t stomach a -20% decline in the stock market, you shouldn’t be investing in stocks. In a recent presentation, Barry Ritholtz, editor of The Big Picture and CIO of Ritholtz Wealth Management, beautifully displayed the 20 times over the last 85 years that the stocks have declined -20% or more (see chart below). This equates to a large decline every four or so years.

Strategist Dr. Ed Yardeni hammers home a similar point over a shorter duration (2008-2014) by also highlighting the inherent volatility of stocks (see chart below).

Stated differently, if you can’t handle the heat in the stock kitchen, it’s probably best to keep out.

It’s a Balancing Act

For the rest of us, the vast majority of investors, the question should not be whether to get out of stocks, it should revolve around what percentage of your portfolio allocation should remain in stocks. Despite record low yields and record high bond prices (see Bubblicious Bonds and Weak Competition, it is perfectly rational for a Baby-Boomer or retiree to periodically ring their stock-profit cash register, and reallocate more dollars toward bonds. Even if you forget about the 30%+ stock return achieved last year and the ~6% return this year, becoming more conservative in (or near) retirement with a larger bond allocation still makes sense. For some of our clients, buying and holding individual bonds until maturity reduces the risky outcome associated with a potential of interest rates spiking.

With all of that said, our current stance at Sidoxia doesn’t mean stocks don’t offer good value today (see Buy in May). For those readers who have followed Investing Caffeine for a while, they will understand I have been relatively sanguine about the prospects of equities for some time, even through a host of scary periods. Whether it was my attack of bears Peter Schiff, Nouriel Roubini, or John Mauldin in 2009-2010, or optimistic articles written during the summer crash of 2011 when the S&P 500 index declined -22% (see Stocks Get No Respect or Rubber Band Stretching), our positioning did not waver. However, as stock values have virtually tripled in value from the 2009 lows, more recently I have consistently stated the game has gotten a lot tougher with the low-hanging fruit having already been picked (earnings have recovered from the recession and P/E multiples have expanded). In other words, the trajectory of the last five years is unsustainable.

Fortunately for us, at Sidoxia we’re not hostage to the upward or downward direction of a narrow universe of large cap U.S. domestic stock market indices. We can scour the globe across geographies and capital structure. What does that mean? That means we are investing client assets (and my personal assets) into innovative companies covering various growth themes (robotics, alternative energy, mobile devices, nanotechnology, oil sands, electric cars, medical devices, e-commerce, 3-D printing, smart grid, obesity, globalization, and others) along with various other asset classes and capital structures, including real estate, MLPs, municipal bonds, commodities, emerging markets, high-yield, preferred securities, convertible bonds, private equity, floating rate bonds, and TIPs as well. Therefore, if various markets are imploding, we have the nimble ability to mitigate or avoid that volatility by identifying appropriate individual companies and alternative asset classes.

Irrespective of my shaky short-term forecasting abilities, I am confident people will continue to ask me my opinion about the direction of the stock market. My best advice remains to get out of stocks*…for the “sideliners”. However, the asterisk still signifies there are plenty of opportunities for attractive returns to be had for the rest of us investors, as long as you can stomach the inevitable volatility.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

{kind=link}