Posts tagged ‘correction’

End of the World or Status Quo?

If you were the chief executive of a newspaper, television, or magazine company, what headline stories would you run to generate the most viewers and readers? Which subjects will you choose to make me impulsively grab a magazine in the grocery line, keep me glued to the television news, or suck me in to click-bait advertisements on the web? For example, what topics below would you select to grab the most attention?

· Hurricane or Sunshine?

· High Speed Car Chase or Cat Saved from Tree?

· Bloody Murder or Baby’s Birthday?

· Messy Divorce or Wedding Celebration?

· Impeachment or Bipartisan Legislation

· End of the World or Status Quo?

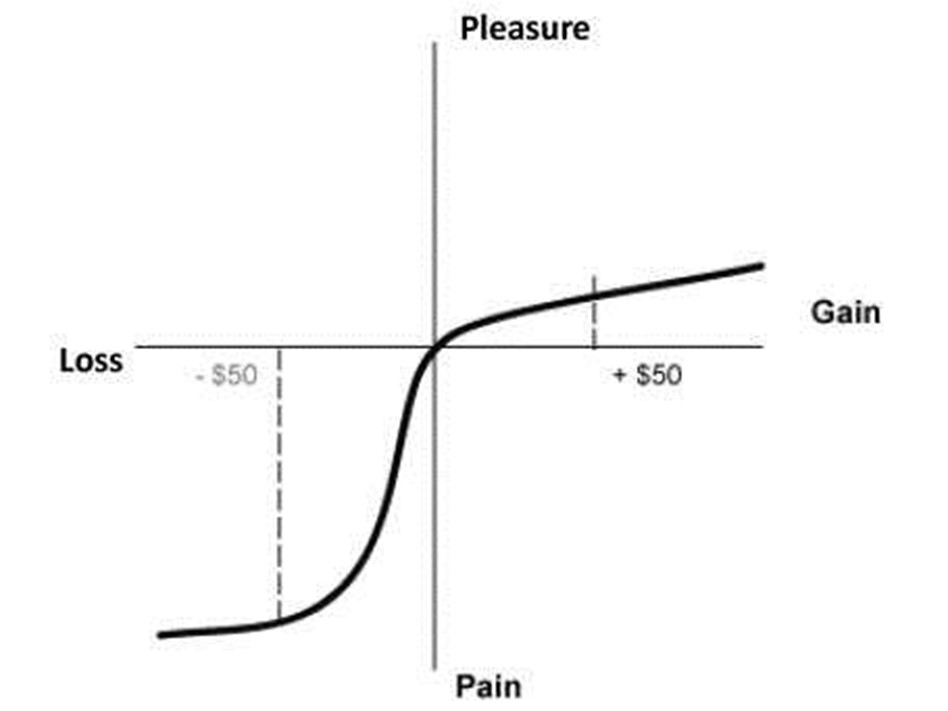

If you selected the first subject in each pair above, you would likely gain much more initial interest. In choosing a winning topic, the saying goes, “what bleeds, leads.” In other words, scary or controversial stories always grab more attention than feel-good or status quo narratives. And that is why the vast majority of media outlets are drawn to negativity, just as mosquitos are attracted to bug zappers. This phenomenon can be explained in part with the help of Nobel Prize winner Daniel Kahneman and his partner Amos Tversky, who conducted research showing the pain from losses is more than twice as painful as are the pleasures experienced from gains (see chart below).

The significant volatility seen in the stock market recently from the Russian war/invasion of Ukraine is further evidence of how this fear dynamic can create short-term panics.

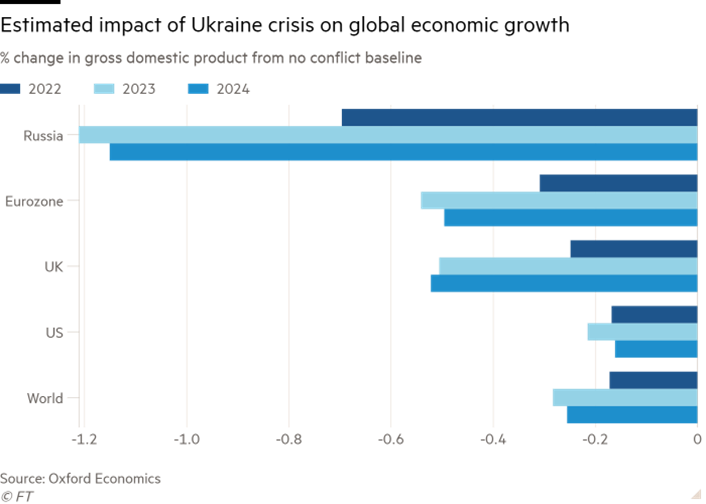

Although the stock market as measured by the S&P 500 index has gone gangbusters over the last three years, almost doubling in value (2019: +29%, 2020: +16%, 2021: +27%), the S&P 500 has hit an air pocket during the first couple months of 2022 (-8%), including down -3% in February. The year started with turbulence as investors became fearful of a Federal Reserve that is entering the beginning stages of interest rate hikes while cutting stimulative bond purchases. And then last month, the Russian-Ukrainian incursion made investors even more skittish. Like always, these geopolitical events tend to be short-lived once investors realize the impact turns out to be less meaningful than initially feared. As you can see below, the worst economic impact is forecasted to be felt by Russia (consensus on 2/24/22 of approximately a -1.0% hit to economic growth), more than twice as bad as the -0.2% to -0.4% knock to growth for the U.S., Europe, and the world (see chart below). The Russian hit will likely be worse after accelerated sanctions.

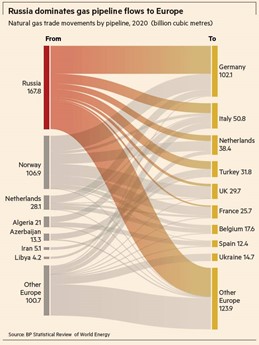

As it relates to Ukraine, many Americans don’t even know where the country is located on a map. Ukraine accounts for about only 0.14% of total global GDP (i.e., a rounding error and less than 1% of total global economic activity). Russia, although larger than Ukraine, is still a relative small-fry and represents only about 3% of total global economic activity. If you live in Europe during the winter, you might be a little more concerned about Vladimir Putin’s recent activities because a lot of Europe’s energy (natural gas) is supplied by Russia through Ukraine. For example, Germany receives about half of its natural gas from Russia (see chart below).

Russia, on the other hand, is larger than Ukraine, but the red country is still a relative small-fry representing only about 3% of total global economic activity. When it comes to energy production however, Russia is more than a rounding error because the country accounts for about 11% of global energy production (#3 country globally behind the United States and Saudi Arabia). By taking all these factors into account, we can confidently state that Russia and Ukraine have a very low probability of solely pulling the global economy into recession.

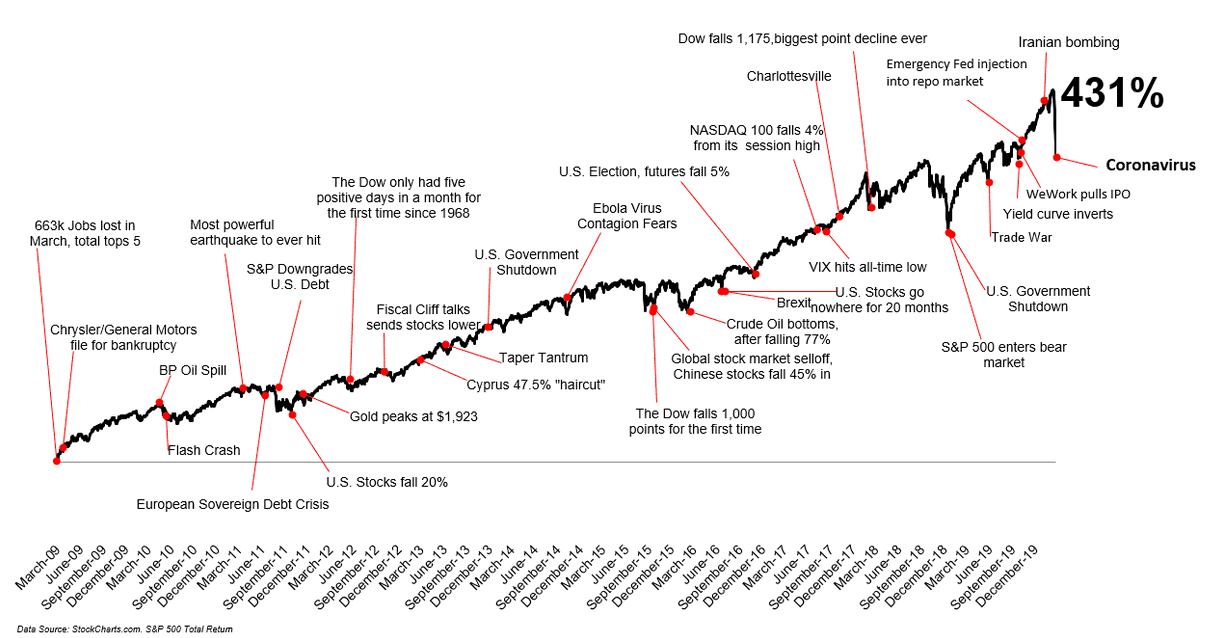

If history repeats itself, this conflict will turn out to be another garden variety decline in the stock market and an opportunity to buy at a discount. It’s virtually impossible to predict a short-term bottom in stock prices has been reached, but over the long-run, stock investors have been handsomely rewarded for not panicking and staying invested (see chart below).

At the end of the day, the daily headlines will continually attempt to sell the negative story that the world is coming to an end. If you have the fortitude and discipline to ignore the irrelevant noise, the status quo of normal volatility can create more exciting opportunities and better returns for long-term investors.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 1, 2022). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

This Too Shall Pass

Ever since December 31st last year when China alerted the WHO (World Health Organization) about several cases of unusual pneumonia in Wuhan, a port city of 11 million people in the central Hubei province, the dark coronavirus (Covid-19) clouds began to form. Last week, the storm came rumbling through with a vengeance.

I have been investing for close to 30 years, so facing these temporary bouts of thunder and lightning is nothing new for me. Although the pace of this week’s -3,583 point drop in the Dow Jones Industrial Average was particularly noteworthy, we experienced a more severe -5,000 point correction a little more than a year ago due to China trade war concerns and our Federal Reserve increasing interest rates. What happened after that year-end 2018 drop? Stock prices skyrocketed more than +7,800 points (+36%) to a new record high on February 12th, just a few weeks ago. Over the long-run, stock prices have always eventually moved up to new record highs, but this week reminds us that volatility is a normal occurrence.

This week also reminds us that the best decisions made in life generally are not emotionally panicked ones. The same principle applies to investing. So rather than knee-jerk react to the F.U.D. (Fear, Uncertainty, Doubt), let’s take a look at some of the current facts as it relates to coronavirus (Covid-19):

- The number of deaths this season in the U.S. from the common flu: 18,000. The number of deaths in the U.S. from coronavirus: 2 individuals (both in WA with underlying health conditions).

- The number of new coronavirus cases in China is declining. Confirmed infections have fallen from more than 2,000 per day to a few hundred. People are going back to work and companies like Starbucks are re-opening their China stores for business.

- Coronavirus is relatively benign compared to other contagious pathogens. Roughly 98% of infected individuals fully recover, and deaths are limited to people with weakened immune systems, who in many cases are suffering from other illnesses.

- Previous viral outbreaks, which were significantly more fatal, were all contained, e.g., SARS (2003-04), MERS (2012), and Ebola (2014-16). In each instance, the stock market initially fell, and then subsequently fully recovered.

- Although the coronavirus has accelerated in areas outside of China, there are dozens of different companies currently developing a vaccine. If a working vaccine is discovered, a rebound could occur as fast as the drop.

- Governments and central banks are not sitting on their hands. Coordinated efforts are being instituted to curtail the spread of the virus and also provide liquidity to financial markets.

The actual death toll from the coronavirus is relatively small compared to other pandemics, catastrophes (e.g., 9/11), and wars. However, the hangover effect from the fear, uncertainty, and panic that can manifest in the days, weeks, and months after global events can last for some time. I expect the same to occur in the coming weeks and months as the drip of continued coronavirus headlines blankets social media and the news.

I don’t want to sugar coat the economic impact from a potential pandemic because quarantining 60 million people in China, instituting global travel bans, and closing areas of gathering has and will continue to have a material economic impact. Although history would indicate otherwise, it is certainly possible the current situation could worsen and lead to a global recession. Even if that were the case, I believe we are more likely closer to a bottom, than we are to a top, especially given how low interest rates are now. More specifically, we just hit an all-time record low yield of 1.13% on the 10-Year Treasury. In other words, putting money in the bank isn’t going to earn you much.

In summary, the current situation experienced this week is nothing new – we’ve lived through similar situations many times (see chart above). The short-run headlines can get more painful, but in the meantime, you can wash your hands and bathe in Purell. This too shall pass.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (March 2, 2020). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFS), but at the time of publishing had no direct position in SBUX or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Scrapes on the Sidewalk

Baron Rothschild, an 18th century British nobleman and member of the Rothschild banking family, is credited with the investment advice to “buy when there’s blood in the streets.” Well, with the Russell 2000 correcting about -14% and the S&P 500 -8% from their 2014 highs, you may not be witnessing drenched, bloody streets, but you could say there has been some “scrapes on the sidewalk.”

Although the Volatility Index (VIX – a.k.a., “Fear Gauge”) reached the highest level since 2011 last week (31.06), the S&P 500 index still hasn’t hit the proverbial “correction” level yet. Even with some blood being shed, the clock is still running since the last -10% correction experienced during the summer of 2011 when the Arab Spring sprung and fears of a Greek exit from the EU was blanketing the airwaves. If investors follow the effective 5-year investment playbook, this recent market dip, like previous ones, should be purchased. Following this “buy-the-dip” mentality since the lows experienced in 2011 would have resulted in stock advancing about +75% in three years.

If you have a more pessimistic view of the equity markets and you think Ebola and European economic weakness will lead to a U.S. recession, then history would indicate investors have suffered about 50% of the pain. Your ordinary, garden-variety recession has historically resulted in about a -20% hit to stock prices. However, if you’re in the camp that we’re headed into another debilitating “Great Recession” as we experienced in 2008-2009, then you should brace for more pain and grab some syringes of Novocaine.

If you’re seriously considering some of these downside scenarios, wouldn’t it make sense to analyze objective data to bolster evidence of an impending recession? If the U.S. truly was on the verge of recession, wouldn’t the following dynamics likely be in place?

- Two quarters of consecutive, negative GDP (Gross Domestic Property) data

- Inverted yield curve

- Rising unemployment and mass layoff announcements

- Declining corporate profits

- Hawkish Federal Reserve

The reality of the situation is the U.S. economy continues to expand; the yield curve remains relatively steep and positive; unemployment declined to 5.9% in the most recent month; corporate profits are at record levels and continue to grow; and the Fed has communicated no urgency to raise short-term interest rates in the near future. While the current headlines may not be so rosy, and the Ebola, eurozone, and Chinese markets may be giving you heartburn, nevertheless, the stock market has steadily climbed a wall of market worry over the last five years.

As the great Peter Lynch stated (see also Inside the Brain of an Investing Genius), “Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in corrections themselves.” Stated differently, Value investor Seth Klarman noted, “We can predict 10 of the next two recessions,” which highlights pundits’ inabilities of accurately predicting the next downturn (see also 100-Year Flood ≠ 100-Day Flood). As Lynch also adds, rather than trying to time the market, it is better to “assume the market is going nowhere and invest accordingly.”

Now may not be the time to dive into stocks headfirst, but many stocks have fallen -10%, -20%, and -30%, so it behooves long-term investors to take advantage of the correction. It’s true that buying when there is “blood in the streets” is an optimal strategy, but facts show this is a difficult strategy to execute. Rather than get greedy, long-term investors may be better served by opportunistically buying when there are “scrapes on the sidewalk.”

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Aaaaaaaah: Turbulence or Nosedive?

We’ve all been there on that rocky plane ride…clammy hands, heart beating rapidly, teeth clenched, body frozen, while firmly bracing the armrests with both appendages. The sky outside is dark and the interior fuselage rattles incessantly until….whhhhhssssshhh. Another quick jerking moment of turbulence has once again sucked the air out of your lungs and the blood from your heart. The rational part of your brain tries to assure you that this is normal choppy weather and will shortly transition to calm blue skies. The irrational and emotional, part of our brains (see Lizard Brain) tells us the treacherous plane ride is on the cusp of plummeting into a nosedive with passengers’ last gasps saved for blood curdling screams before the inevitable fireball crash.

Well, we’re now beginning to experience some small turbulence in the financial markets, and at the center of the storm is a collapsing Argentinean peso and a perceived slowing in China. In the case of Argentina, there has been a century-long history of financial defaults and mismanagement (see great Scott Grannis overview). Currently, the Argentinean government has been painted into a corner due to the depletion of its foreign currency reserves and financial mismanagement, as evidenced by an inflation rate hitting a whopping 25% rate.

On the other hand, China has created its own set of worries in investors’ minds. The flash Markit/HSBC Purchasing Managers’ Index (PMI) dropped to a level of 49.6 in January from 50.50 in December, which has investors concerned of a market crash. Adding fuel to the fear fire, Chinese government officials and banks have been trying to reverse excesses encountered in the country’s risky shadow banking system. While the size of Argentina’s economy may not be a drop in the bucket, the ultimate direction of the Chinese economy, which is almost 20x’s the size of Argentina’s, should be much more important to global investors.

At the end of the day, most of these mini-panics or crises (turbulence) are healthy for the overall financial system, as they create discipline and will eventually change irresponsible government behaviors. While Argentinean and Chinese issues dominate today’s headlines, these matters are not a whole lot different than what we have read about Greece, Ireland, Italy, Spain, Portugal, Cyprus, Turkey, and other negligent countries. As I’ve stated before, money goes where it’s treated best, and the stock, bond, and currency vigilantes ensure that this is the case by selling the assets associated with deadbeat countries. Price declines eventually catch the attention of politicians (remember the TARP vote failure of 2008?).

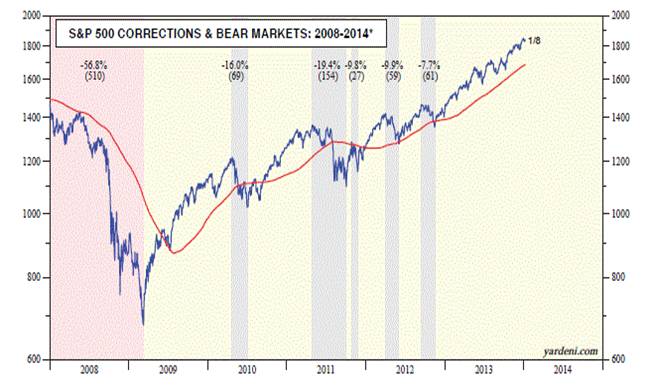

Is This the Beginning of the Crash?!

What goes up, must come down…right? That is the pervading sentiment I continually bump into when I speak to people on the street. Strategist Ed Yardeni did a great job of visually capturing the last six years of the stock market (below), which highlights the most recent bear market and subsequent major corrections. Noticeably absent in 2013 is any major decline. So, while many investors have been bracing for a major crash over the last five years, that scenario hasn’t happened yet. The S&P chart shows we appear to be due for a more painful blue (or red) period of decline in the not-too-distant future, but that is not necessarily the case. One would need only to thumb through the history books from 1990-1997 to see that investors lived through massive gains while avoiding any -10% correction – stocks skyrocketed +233% in 2,553 days. I’m not calling for that scenario, but I am just pointing out we don’t necessarily always live through -10% corrections annually.

Source: Dr. Ed’s Blog

Even though we’ve begun to experience some turbulence after flying high in 2013, one should not panic. You may be better off watching the end of the airline movie before putting your head in between your legs in preparation for a nosedive.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Earnings Coma: Digesting the Gains

Over the last five years, the stock market has been an all-you-can-eat buffet of gains for investors. It has been almost two years since the spring of 2012 when the Arab Spring and potential exit of Greece from the EU caused a -10% correction in the S&P 500 index (see Series of Unfortunate Events). Indigestion of this 10% variety is typically on the menu and ordered at least once per year. With stocks up about +50% over the last two years, performance has tasted sweet. But even binging on your favorite entrée or dessert will eventually lead to a food coma. At that bloated point, a digestion phase is required before another meal of gains can be consumed.

So far investors haven’t been compelled to expel their meals quite yet, but it’s clear to me the rate of appreciation is not sustainable over the long-term. Could the incredible returns continue in the short-run during 2014? Certainly. As I’ve written before, the masses remain skeptical of the recovery/rally and any definitive acceleration in economic growth could spark the powder-keg of skeptics to come join the party (see Here Comes the Dumb Money). If and when that happens, I will be gladly there to systematically ring the register of profits I’ve consumed, by locking in gains and reallocating to less loved areas (i.e., go on a stock diet).

Q4 Appetizers Here, Main Course Not Yet

The 4th quarter earnings appetizers have been served, evidenced by the 50-odd S&P 500 corporations that have reported their financial results, and thus far some Tums may be needed to relieve some heartburn. Although about half of those companies reporting have beat Wall Street estimates, 37% of the group have missed expectations, according to Thomson Reuters. It’s still early in the earnings season, but as of now, the ratio of companies beating Wall Street forecasts is below historical averages.

We can put a little meat on the earnings bone by highlighting the disappointing profit warnings and lackluster results from bellwether companies like United Parcel Service (UPS), Intel Corp (INTC), General Electric (GE), CSX Corp (CSX), and Royal Dutch Shell (RDSA), to name a few. Is it time to panic and run for the restroom (or exits)? Probably not. About 90% of the S&P 500 companies still need to give their Q4 profitability state of the union. What’s more, another reason to not throw in the white towel yet is the global economic environment looks significantly better in areas like Europe, China, and other emerging markets.

Worth remembering, the stock market is a discounting mechanism. The market pays much more attention to the future versus the past. So, even if the early earnings read doesn’t look so great now, the fact that the S&P 500 is down less than -1% off of its all-time, record highs may be an indication of better things ahead.

Recipe for a Pullback?

If earnings continue to drag on in a disappointing fashion, and political brinkmanship materializes surrounding the debt ceiling, it could easily be enough to spark some profit-taking in stocks. While Sidoxia is finding no shortage of opportunities, it has become apparent some speculative pockets of euphoria have developed. Areas like social media and biotech are ripe for corrections.

While the gains over the last few years have been tantalizing, investors must be reminded to not overindulge. Carefully selecting stocks to chew and digest is a better strategy than recklessly binging on everything in the buffet line. There are plenty of healthy areas of the market to choose from, so it’s important to be discriminating…or your portfolio could end up in a coma.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in UPS, INTC, GE, CSX, RDSA, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Stocks Take a Breather after Long Sprint

Like a sprinter running a long sprint, the stock market eventually needs to take a breather too, and that’s exactly what investors experienced this week as they witnessed the Dow Jones Industrial Average face its largest drop of 2013 (down -2.2%) – and also the largest weekly slump since 2012. Runners, like financial markets, sooner or later suffer fatigue, and that’s exactly what we’re seeing after a relatively unabated +27% upsurge over the last nine months. Does a -2% hit in one week feel pleasant? Certainly not, but before the next race, the markets need to catch their breath.

By now, investors should not be surprised that pitfalls and injuries are part of the investment racing game – something Olympian Mary Decker Slaney can attest to as a runner (see 1984 Olympic 3000m final against Zola Budd). As I have pointed out in previous articles (Most Hated Bull Market), the almost tripling in stock prices from the 2009 lows has not been a smooth, uninterrupted path-line, but rather investors have endured two corrections averaging -20% and two other drops approximating -10%. Instead of panicking by locking in damaging transaction costs, taxes, and losses, it is better to focus on earnings, cash flows, valuations, and the relative return available in alternative asset classes. With generationally low interest rates occurring over recent periods, the available subset of attractive investment opportunities has narrowed (see Confessions of a Bond Hater), leaving many investing racers to default to stocks.

Recent talk of potential Federal Reserve bond purchase “tapering” has led to a two-year low in bond prices and caused a mini spike in interest rates (10-year Treasury note currently yielding +2.83%). At the margin, this trend makes bonds more attractive (lower prices), but as you can see from the chart below, interest rates are still relatively close to historically low yields. For the time being, this still makes domestic equities an attractive asset class.

Source: Yahoo! Finance

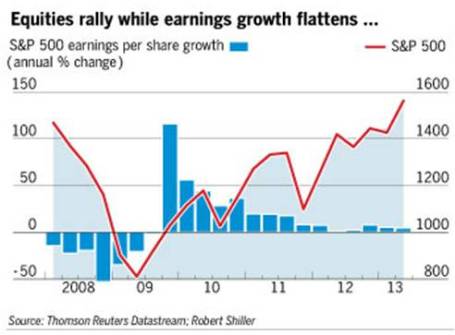

Price Follows Earnings

The simple but true axiom that stock prices follow earnings over the long-run is just as true today as it was a century ago. Interest rates and price-earnings ratios can also impact stock prices. To illustrate my argument, let’s talk baseball. Wind, rain, and muscle (interest rates, PE ratios, political risk, etc.) are factors impacting the direction of a thrown baseball (stock prices), but gravity is the key factor influencing the ultimate destination of the baseball. Long-term earnings growth is the equivalent factor to gravity when talking about stock prices.

To buttress my point that stock prices following long-term earnings, consider the fact that S&P 500 annualized operating earnings bottomed in 2009 at $39.61. Since that point, annualized earnings through the second quarter of 2013 (~94% of companies reported results) have reached $99.30, up +151%. S&P 500 stock prices bottomed at 666 in 2009, and today the index sits at 1655, +148%. OK, so earnings are up +151% and stock prices are up +148%. Coincidence? Perhaps not.

If we take a closer look at earnings, the deceleration of earnings growth is unmistakable (see Financial Times chart below), yet the S&P 500 index is still up +16% this year, excluding dividends. In reality, predicting multiple expansion or contraction is nearly impossible. For example, earnings in the S&P 500 grew an incredible +15% in 2011, yet stock prices were anemically flat for that year, showing no price appreciation (+0.0%). Since the end of 2011, earnings have risen a meager +3%, however stock prices have catapulted +32%. Is this multiple expansion sustainable? Given stock P/E ratios remain in a reasonable 15-16x range, according to forward and trailing earnings, there is some room for expansion, but the low hanging fruit has been picked and further double-digit price appreciation will require additional earnings growth.

Source: Financial Times

But stocks should not be solely looked through a domestic lens…there is another 95% of the world’s population slowly embracing capitalism and democracy to fuel future dynamic earnings growth. At Sidoxia (www.Sidoxia.com), we are finding plenty of opportunities outside our U.S. borders, including alternative asset classes.

The investment race continues, and taking breathers is part of the competition, especially after long sprints. Rather than panic, enjoy the respite.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Gravity Takes Hold in May

Warner Bros. picture of Wile E. Coyote’s failed apprehension of Roadrunner

Wile E. Coyote, the bumbling, roadrunner-loving carnivore from Warner Bros.’ Looney Tunes series spends a lot of time in the air chasing his fine feathered prey. Unfortunately for Mr. Coyote his genetic make-up and Acme purchases could not cure the ills caused by gravity (although user error was the downfall of Wile E’s effective Bat-Man flying outfit purchase). Just as gravity hampered the coyote’s short-term objectives, so too has gravity hampered the equity markets’ performance this May.

So far the adage of “Sell in May and walk away” has been the correct course of action. Just one day prior to the end of the month, the Dow Jones Industrial and S&P 500 indexes were on pace of recording the worst May decline in almost 50 years. If the -6.8% monthly decline in the S&P and the -7.8% drop in the S&P remains in place through the end of the month, these declines would mark the worst performance in a May month since 1962.

Should we be surprised by the pace and degree of the recent correction? Flash crash and Greece worries aside, any time a market increases +70-80% within a year, investors should not be caught off guard by a subsequent 10%+ correction. In fact corrections are a healthy byproduct of rapid advances. Repeated boom-bust cycles are not market characteristics most investors crave.

It was a volatile, choppy month of trading for the month as measured by the Volatility Index (VIX). The fear gauge more than doubled to a short-run peak of around 46, up from a monthly low close of about a reading of 20, before settling into the high 20s at last close. Digesting Greek sovereign debt issues, an impending Chinese real estate bubble bursting, budget deficits, government debt, and financial regulatory reform will determine if elevated volatility will persist. Improving macroeconomic indicators coupled with reasonable valuations appear to be factoring in a great deal of these concerns, however I would not be surprised if this schizophrenic trading will persist until we gain certainty on the midterm elections. As Wile E. Coyote has learned from his roadrunner chasing days, gravity can be painful – just as investors realized gravity in the equity markets can hurt too. All the more reason to cushion the blow to your portfolio through the use of diversification in your portfolio (read Seesawing Through Chaos article).

Happy long weekend!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in TWX, VXX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}