Posts tagged ‘Congress’

New Year’s Resolutions and Vaccine Distributions

Many people were ready to flush 2020 down the toilet after the novel coronavirus (COVID-19) global pandemic dominated the daily headlines, but panic eventually turned into optimism. With last year and a new year celebration now behind us, the annual tradition of creating a New Year’s resolution to better one’s life will be a challenge for many in 2021. Why? Well, from a financial perspective, the stock market, as measured by the S&P 500 index, finished the year at another mind-boggling, all-time record high (+16% for the year), making 2020 a tough act to follow.

One area of the stock market performed exceptionally well. With millions of employees, students, and bored Americans locked down for much of the year, demand for computers, mobile phones, and internet-connected televisions swelled. Due to a flood of sales into devices, gadgets, equipment, and software, technology stocks became huge beneficiaries in 2020. The performance of this sector can be gauged by the results of the tech-heavy NASDAQ index, which skyrocketed an astounding +44%.

Countering the Confusion

Given this unexpected surge in stock prices, many casual observers are asking how is it possible the Dow Jones Industrial Average capped off a year above the 30,000 level (best ever) after a year when 80 million people contracted COVID-19 and almost 2 million humans died from the virus?

This month, we will try to answer this confusing question. We shall explore the factors behind the unprecedented collapse early in the year and the subsequent recovery in stock prices surrounding this perplexing virus.

We’ve experienced a lot over the last year: death, destruction, an emotionally divisive presidential election, social distancing, face-coverings, Amazon deliveries, Netflix binging, DoorDash food deliveries, hand-sanitizer stocking, toilet-paper runs, and endless pants-less Zoom video sessions. After all this insanity, here are some reasons for why your and my investment accounts and 401(k) balances still managed to appreciate significantly last year:

- A COVID Cure: Although roughly only 4 million doses of the COVID-19 vaccine have been administered to date (after a 20 million goal), the government has contracted for the delivery of 400 million vaccine doses from Pfizer Inc. (PFE) and Moderna Inc. (MRNA) by summertime. With these two FDA (Food and Drug Administration) approvals alone, these doses should be enough to vaccinate all but about 60 million of the roughly 260 million adult Americans who are eligible to be inoculated. Even better, each of these cures appear to be over 90% effective. What’s more, in the not-too-distant future, additional relief is on its way in the form of further vaccine approvals by the likes of Johnson & Johnson (JNJ), Novavax Inc. (NVAX), AstraZeneca (AZN), and the Sanofi (SNY) / GlaxoSmithKline (GSK).

- Fed Firemen to the Rescue: As the COVID flames are blazing with record numbers of cases, hospitalizations, and deaths, the Federal Reserve firemen have come to an economic rescue by providing accommodative monetary policies. By effectively setting the benchmark Fed Funds Rate to 0% (see chart below), our central bank is not only stimulating loan activity for businesses, but also lowering the cost of mortgages and credit cards for consumers. In addition, the Fed has been providing support to financial markets and invigorating the economy through its asset purchases. More specifically, the Fed outlined its activities in its most recent December statement:

“The Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage-backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee’s maximum employment and price stability goals.“

- Economic Recovery is Well on its Way: In addition to the unmatched monetary policy stimulus from the Federal Reserve, we have also experienced an unparalleled $4 trillion in fiscal stimulus to trigger a sharp rebound in economic activity (see red line in chart below). There have been multiple rounds of PPP (Paycheck Protection Program) loans given to small businesses, millions of direct checks distributed to unemployed individuals, along with a host of other programs covering the healthcare, education, and infrastructure industries. As a result of these measures, coupled with the vaccines unleashing massive amounts of pent-up demand, pundits are forecasting above-trendline economic GDP growth in 2021 approximately 4% – 5% (e.g., Merrill Lynch +4.6%, Goldman Sachs +5.9%, and the Federal Reserve +3.7% to +5.0%).

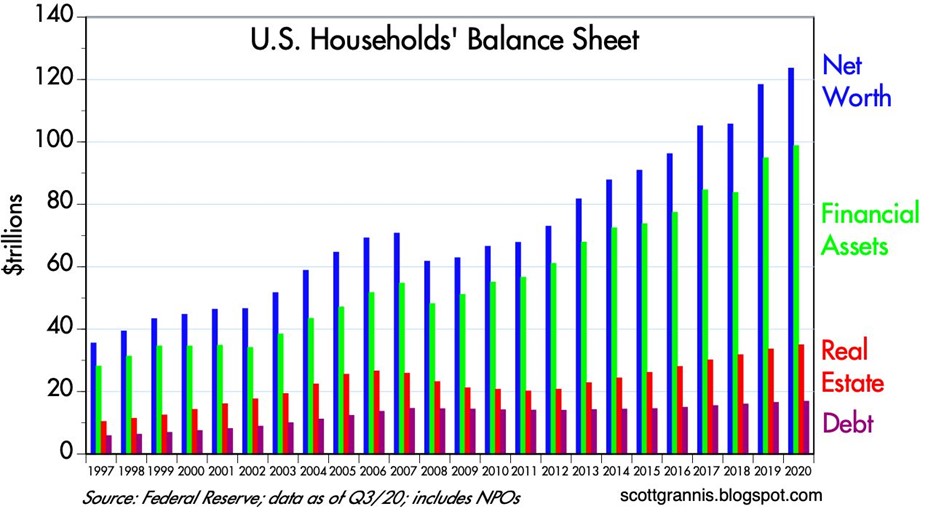

As part of the recovery, the banner year in stocks has also helped catapult consumer household balance sheets to over $120 trillion dollars, while simultaneously reducing debt (leverage) ratios (see chart below).

Flies in the Ointment

It’s worth noting that not all is well in COVID-land. Unemployment rates remain at elevated recessionary levels and industries such as travel, leisure, and restaurants persist in devastation by the pandemic. Politically, the hotly contested 2020 presidential election has largely been resolved, but a Georgia runoff vote this week for two Senate seats could swing full control of Congress to the Democrats. With the stock market at fresh new highs, a Democrat sweep in Georgia would likely be interpreted as a mandate for President-elect Biden to increase taxes for many people and businesses. Under this scenario, a temporary downdraft in the market should come as no surprise to any investor. However, any potential tax hikes on corporations and the wealthy should be accompanied with more infrastructure spending and fiscal spending, which could offset the drag of taxes to varying degrees.

Although Sidoxia Capital Management is still finding plenty of opportunities in the stock market while considering these record low interest rates (yield on 10-year Treasury Note of only 0.92%), areas of vulnerability still exist in recent high-flying, money-losing IPOs (Initial Public Offerings) such as Snowflake Inc. (SNOW), Airbnb Inc (ABNB), and DoorDash Inc (DASH).

Other cautionary areas of excess speculation include the hundreds of SPAC (Special Purpose Acquisition Company) deals totaling more than $70 billion in 2020, and the reemergence of Bitcoin froth (up greater than +300% this year). The recent rush into Bitcoin has been fierce, but industry veterans with memory greater than a gnat recall that Bitcoin plummeted more than -80% from its peak to trough in 2018. Suffice it to say, Bitcoin is not for the faint of heart and buyers should beware.While there was a lot of pain and suffering experienced by millions due to the COVID-19 global pandemic, there was a lot to be thankful for as well, including vaccines to cure the global pandemic. Even though we had another record year at Sidoxia Capital Management, there is always room for improvement. At Sidoxia our New Year’s resolution is always the same: Provide superior investment management and financial planning services, as we build sustaining, long-term relationships with our clients.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (January 4, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in AMZN, NFLX, MRNA, ZM, PFE, NVAX, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in DASH, JNJ, AZN, SNY, GSK, SNOW, ABNB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Trump: Bark Worse Than the Bite?

Unless you have been living in a cave this week, you are probably aware the country has elected a new president. Leading up to Election Day, the anxiety was palpable. A populist wave, much like the one experienced in the British Brexit vote earlier this year, resulted in economically disenfranchised voters coming out in full force to vote out the perceived establishment candidate, Hillary Clinton. Financial market pundits and media commentators predicted an immediate 11-13% decline in stock values if Donald Trump were to win. Could they have been more wrong? After a brief -5% decline in pre-trading Dow Jones Industrial Average future prices, the Dow subsequently skyrocketed more than 1,000 points higher to finish up +1.4% for the day (see chart below). For the week, the Dow amazingly rallied by +5.4%.

Source: Investing.com

As I have written on numerous occasions, politics have very little impact on the long-term direction of the financial markets. Yes, it is true that regulations and policies implemented by the president and Congress can influence specific industries or individual companies over the short-run. Hillary Clinton proved this assertion with her pharmaceutical industry tweet, which created a lasting hangover effect on the sector. But guess what? Regulations and politics have always changed throughout our country’s history, with various shifting policies impacting businesses asymmetrically – some positively and some negatively. The good news…in an ever-expanding global economy, accelerated through technology, capitalism forces businesses to adapt to political change.

Considering the amount of our nation’s political variation, what has been our country’s stock market and economic track record over the last 100 years under 17 different presidents (8 Democrats and 9 Republicans)? See chart below:

Source: Macrotrends

Not too shabby judging by the roughly 188x–fold increase in the Dow Jones Industrial Average (or > ~18,700%+ return) to a fresh all-time record high this week. While I am admittedly nervous about a full, Republican tri-power Trump administration (President/House/Senate), the reality is that Trump’s unconventional, unprecedented platform doesn’t fit squarely into the traditional Republican policy boxes. In fact, he has switched his party affiliation five times. President-elect Trump will therefore need to reach across the political aisle to Democrats, and work with Speaker of the House Paul Ryan to accomplish the platform agenda priorities he outlined during his presidential campaign.

While all this political election discussion has been stimulating and exhausting, fortunately, followers of my Investing Caffeine blog understand there are much more important factors than politics affecting the performance of the stock market and economy – namely corporate profits, interest rates, valuations, and sentiment (see Don’t Be a Fool, Follow the Stool).

As mentioned, the market’s returns are influenced by four key factors, but sentiment and stock market values are largely shaped by investor behavior. Trump has less control on investor behavior, but his policies can directly impact corporate profits and interest rates – two critical components of economic health. Part of the reason Trump won the election was due to campaign promises regarding many popular stimulative policies, including personal and corporate tax cuts; infrastructure spending; repatriation of foreign money; tax simplification and reform; Obamacare improvement; and immigration reform.

As it turns out, a good number of the issues relating to these policies happen to be bipartisan in nature. Given the Republican-controlled Congress, investors are perceiving these potential policy changes as positive for the market – at least for the first week of his presidential tenure.

For now, President-elect Trump has struck the proper conciliatory tone and made appropriate comments. In the coming days and weeks, investors are watching closely for tangible evidence and clues of his policy priorities, as he fills key political posts on his presidential team. Time will tell whether the early honeymoon will continue past Trump’s inauguration day, but currently, the consensus is his bark heard during Trump’s heated 18-month presidential campaign is worse than the actual bite of his election victory.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page

Politics & Your Money

Will you be able to retire, and what impact will the elections have on your financial future? Answering these questions can be a scary endeavor. And unless you have been living in a cave, you may have noticed we are in the middle of a heated U.S. presidential election campaign between Donald Trump and Hillary Clinton. Regardless of which side of the political fence you stand on, the prospects of your retirement are much more likely to be impacted by your personal actions than by the actions of Washington politicians.

Even if you despise politics and were living in a cave (with WiFi access), there’s a high probability you would be overloaded with detailed and dogmatic online editorials from overconfident Facebook friends. Besides offering self-assured predictions, these impassioned political pleas generally itemize the top 10 reasons your favorite candidate is a moron, and another 10 reasons why their candidate is the greatest.

Your friends’ opinions may have pure intentions, but unfortunately, rarely, if ever, do their thoughts alter your views. A reference from a recent Legal Watercooler article summed it up best:

“Political Facebook rants changed my mind…said nobody, ever.”

Nearly as ineffectual as political Facebook opinions on your politics is the ineffectual influence of presidential elections on your finances. For example, over the last four decades, stock prices have gone up and down during both Republican and Democrat presidential terms. The picture looks much the same, if you analyze the fiscal performance of conservatives and liberals since 1970 – debt burdens as a percentage of economic output have risen and fallen under both political parties. No matter who wins the presidency, many investors forget the ability of that individual to affect change is highly dependent upon the political balance of power in Congress. If Congress holds a split majority in the House and Senate, or the opposition party commands the entire Congress, then the winning presidential candidate will be largely neutered.

Rather than panic over a political loss or celebrate a candidate’s victory, here are some tangible actions to improve your finances:

- Organize. Typically individuals have investment and saving accounts scattered with no cohesive accounting or strategy. Get your financial house in order by gathering and organizing all your accounts.

- Budget. Spend less than you take in. Or in other words…save. You can achieve this goal in one of two ways – cut your spending, or increase your income.

- Create a Plan. When do you plan to retire? How much money do you need for retirement? What asset allocation and risk profile should you adopt to meet your financial goals?

If you have difficulty with any of these actions, then meet with an experienced financial professional to assist you.

Politics can trigger very emotional responses. However, realizing your actions have a much more direct impact on your finances than political Facebook rants and temporary elections will benefit you in achieving your long-term financial goals.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds and FB, but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Teflon Market

At the pace of all this head-scratching going on, our population is likely to turn completely bald. One thing is for certain, nothing has scratched this Teflon stock market. If you want to have fun with a friend, family member or co-worker, just ask them how they feel about politics and then ask them how stocks have done this year? You’re bound to get some entertaining responses. Despite a Congress that has a lower favorability rating than cockroaches, lice, root canals, and colonoscopies , the S&P 500 index is up a whopping +22% and the NASDAQ index + 30% this year, both records. The USA Today ran with the Teflon theme and had this to say:

“This year alone the stock market has survived the recent brush with a U.S. debt default. It has also survived a government shutdown. Tax hikes. Government spending cuts. The threat of war. Terror at the Boston Marathon. A spike in interest rates. Plunging Apple shares. Stock exchange glitches. Fears of a less-friendly Federal Reserve. And a narrow escape from going over the “fiscal cliff.” Nothing bad seems to stick.”

The reason nothing is sticking to this Teflon market is because the market is more sensitive to reality rather than perception. Here are some come current discrepancies between these two states:

Perception: The economy is on the verge of a recession. Reality: The economy has grown GDP for 15 of the last 16 quarters. The private sector has added about 7.5 million jobs and the unemployment rate has been cut by about three percentage points.

Perception: Corporations are struggling. Reality: Corporations are actually posting record profits; increasing dividends significantly; buying back stock; and registering record profit margins.

Perception: The Federal Reserve controls the economy. Reality: Federal Reserve Chairman Ben Bernanke has little to no influence on decisions made by companies like Google Inc (GOOG), Facebook Inc (FB), McDonald’s Corp (MCD), Tesla Motors Inc (TSLA), and Target Corporation (TGT) (see also The Greatest Thing Since Sliced Bread). Interest rates are actually higher than when QE1 (quantitative easing) was first implemented, yet growth persists.

These types of mental mistakes occur outside the realm of financial markets as well. For example, most people fail to correctly answer the question, “Which animal is responsible for the greatest number of human deaths in the U.S.?”

A.) Alligator; B.) Bear; C.) Deer; D.) Shark; and E.) Snake

The ANSWER: C) Deer.

Deer colliding into cars trigger seven times more deaths than alligators, bears, sharks, and snakes combined, according to Jason Zweig at the Wall Street Journal (see also Alligators & Airplane Crashes). Other mental disconnects include the belief that planes are more dangerous than cars. In fact, people are 65 times more likely to get killed in your own car versus a plane. Also, misconceptions exist that guns are more dangerous than smoking, or that tornadoes are more dangerous than asthma – both beliefs wrong.

Party Not Over Yet

Long-time followers and readers of Investing Caffeine know that I’ve been an active participant in this bull market that started in 2009, evidenced by my critical views of Armageddonists like Peter Schiff, John Mauldin, Nouriel Roubini, Meredith Whitney, and other doom & gloomers.

I fully recognize there’s no honor in being Pollyannaish or a perma-bull just for the sake of it. However, it’s also very clear that excessive fear exercised by many investors proved very painful as S&P 500 level 666 has exploded to 1,744. The extreme panic that reached a pinnacle in 2009 has now morphed into an insidious skepticism (see Sentiment Pendulum ). Investor emotions continually swing from fear to greed, and with the political shenanigans going on in Washington DC, the skeptical pendulum has a long way before reaching euphoric levels. Or stated differently, the pre-party is over (see my article from earlier this year, Those Who Missed the Pre-Party), but the DJ is still playing and the cops aren’t here to break up the party yet.

I agree that we’ve had a Teflon market for a handful of years. There have been a few minimal scratches and a few hand burns along the way, but for the most part, those investors who have stayed invested and ignored the endless manufactured crisis headlines have been rewarded handsomely. Investing in stocks will always cause some heartburn, but if you don’t want your long-term retirement to get grilled, seared, pan-fried, or flambéed, then you want to make sure you still have some stocks in your Teflon pan.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), AAPL and GOOG, but at the time of publishing, SCM had no direct position in FB, TGT, TSLA, MCD, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Lily Pad Jumping & Term Paper Cramming

Article is an excerpt from previously released Sidoxia Capital Management’s complementary December 3, 2012 newsletter. Subscribe on right side of page.

Over the last year, investors’ concerns have jumped around like a frog moving from one lily pad to the next. From the debt ceiling debate to the European financial crisis, and then from the presidential election to now the “fiscal cliff.” With the election behind us (Obama winning 332 electoral votes vs 206 for Romney; and Obama 50.8% of the popular vote vs 47.5% for Romney), the frog’s bulging eyes are squarely focused on the fiscal cliff. For the uninformed frogs that have been swimming underwater, the fiscal cliff is the roughly $600 billion in automatic tax hikes and spending cuts that are scheduled to be triggered by the end of this year, if Congress cannot come to some type of agreement (for more fiscal cliff information see videos here). The mathematical consequences are clear: Congress + No Deal = Recession.

While political brinksmanship and theater are nothing new, the explosive amount of data is something new. In our mobile world of 6 billion cell phones (more than the number of toothbrushes on our planet) and trillions of text messages sent annually, nobody can escape the avalanche of global data. Google (GOOG), Facebook (FB), Twitter, and millions of blogs (including this one) didn’t exist 15 years ago, therefore fiscal boogeymen like obscure Greek debt negotiations and Chinese PMI figures wouldn’t have scared pre-internet generations underneath their beds like today’s investors. The fact of the matter is our country has triumphed over plenty of significant issues (many of them scarier than today’s headlines), including wars, assassinations, currency crises, banking crises, double digit inflation, SARS, mad cow disease, flash crashes, Ponzi schemes, and a whole lot more.

Although today’s jumpy investors may worry about the lily pads of a double-dip recession in the US, a financial meltdown in Europe, and/or a hard landing in China, fiscal frogs will undoubtedly be worried about different lily pads (concerns) twelve months from now. This may not be an insightful observation for day traders, but for the other 99% of investors, taking a longer term view of the daily news cycle may prove beneficial.

Fiscal Cliff Term Paper Due on Friday December 21st

As a college student, chugging Jolt Cola, in combination with a couple dosages of NoDoz, was part of the routine procrastination process the day before a term paper was due. Apparently Congress has also earned a PhD in procrastination, judging by the last minute conclusion of the debt ceiling negotiations last summer. There are only a few more weeks until politicians break for the Christmas holiday break, therefore I am setting an Investing Caffeine mandated fiscal cliff due date of December 21st. Could Congress turn in its term paper early? Anything is possible, but unfortunately turning in the assignment early is highly unlikely, especially when politically bashing your opponent is perceived as a better re-election tactic compared to bipartisan negotiation.

A higher probability scenario involves Americans stuck listening to Nancy Pelosi, Harry Reid, John Boehner, and Mitch McConnell on a daily basis as these politicians finger-point and call the other side obstructionists. While I’m not alone in believing a deal will ultimately get done before Christmas, how credible and substantive the announcement will be depends on whether the politicians seriously face entitlement and tax reforms. Regardless, any deal announced by Investing Caffeine’s December 21st due date will likely be received well by the market, as long as a framework for entitlement and tax reform is laid out for 2013.

Frog News Bites

Source: Photobucket

GDP Revised Higher: Despite all the gloom and uncertainties, the barometer of the economy’s health (i.e., Real Gross Domestic Product), was revised higher to 2.7% growth for the third quarter (from 2.0%). Nominal growth, a related measurement that includes inflation, reached a five-year high of 5.55%. In the wake of Superstorm Sandy, which caused upwards of $50 billion in damage, fourth quarter GDP numbers are likely to be artificially depressed. The silver lining, however, is first quarter 2013 figures may get an economic boost from reconstruction efforts.

Source: Calafia Beach Pundit

Housing Recovery Continues: Buoyed by record low interest rates (30-yr fixed mortgages < 3.5%), housing sales and prices continue on an upward trajectory. New home sales came in at 368,000 in October, below expectations, but sales are still up around +20% from 2011 (Calculated Risk).

Source: Calculated Risk

Confidence Still Low but Climbing: The recently reported consumer confidence figures reached the highest level in more than four years, but as Scott Grannis highlights, this is nothing to write home about. These current confidence levels match where we were during the 1990-91 and 1980-82 recessions.

Source: Calafia Beach Pundit

Car Sales Picking Up: Fiscal cliff discussions haven’t discouraged consumers from buying cars. As you can see from the chart below, car and truck sales reached 14.3 million annualized units in October. November sales are expected to rise about +13% on a year-over-year basis, reaching approximately 15.3 million units.

Source: Calculated Risk

CIA Chief Fired in Sex Scandal: If you didn’t get enough of the Lindsay Lohan bar brawl dirt in New York, never fear, there was plenty of salacious details emanating from Washington DC this month. A complicated web of Florida socialites, a biographer, email chains, and a bare-chested FBI agent led to the firing of CIA director David Petraeus.

Source: The Financial Times

Death to Twinkies: After lining stomachs with golden cream-filled cakes for more than 80+ years, Hostess Brands was forced to halt production of Twinkies, Ding Dongs, and Ho Hos. Negotiations with union bakers crumbled, which led to Hostess Brands’ Chapter 7 bankruptcy and liquidation proceedings. My financial brain understands, but my sweet tooth is still grieving (see also Twinkie Investing).

Source: Photobucket

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct positions in FB, Twitter or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Plumbers & Cops: Can the Debt Ceiling be Fixed?

The ceiling is leaking, but it’s unclear whether it will be repaired? Rather than fix the seeping fiscal problem, Democrats and Republicans have stared at the leaky ceiling and periodically applied debt ceiling patches every year or two by raising the limit. Nanosecond debt ceiling coverage has reached a nauseating level, but this issue has been escalating for many months. Last fall, politicians feared their long-term disregard of fiscally responsible policies could lead to a massive collapse in the financial ceiling protecting us, so the President called in the bipartisan plumbers of Alan Simpson & Erskine Bowles to fix the leak. The commission swiftly identified the problems and came up with a deep, thoughtful plan of action. Unfortunately, their recommendations were abruptly dismissed and Washington fell back into neglect mode, choosing instead to bicker like immature teenagers. The result: poisonous name calling and finger pointing that has placed Washington politicians one notch above Cuba’s Fidel Castro, Venezuela’s Hugo Chavez, and Iran’s Mahmoud Ahmadinejad on the list of the world’s most hated leaders. Strategist Ed Yardeni captured the disappointment of American voters when he mockingly states, “The clowns in Washington are making people cry rather than laugh.”

Although despair is in the air and the outlook is dour, our government can redeem itself with the simple passage of a debt ceiling increase, coupled with credible spending reduction legislation (and possibly “revenue enhancers” – you gotta love the tax euphimism).

The Elephant in the Room

Our country’s spending problems is nothing new, but the 2008-2009 financial crisis merely amplified and highlighted the severity of the problem. The evidence is indisputable – we are spending beyond our means:

Source: scottgrannis.blogspot.com

If the federal spending to GDP chart is not convincing enough, then review the following graph:

- Source: blog.yardeni.com – A graph a first grader could understand.

You don’t need to be a brain surgeon or rocket scientist to realize government expenditures are massively outpacing revenues (tax receipts). Expenditures need to be dramatically reduced, revenues increased, and/or a combination thereof. Applying for a new credit card with a limit to spend more isn’t going to work anymore – the lenders reviewing those upcoming credit applications will straightforwardly deny the applications or laugh at us as they gouge us with prohibitively high borrowing costs. The end result will be the evaporation of entitlement programs as we know them today (including Medicare and Social Security). For reference of exploding borrowing costs, please see Greek interest rate chart below. The mathematical equation for the Greek financial crisis (and potentially the U.S.) is amazingly straightforward…Loony Spending + Looney Politicians = Loony Interest Rates.

Source: Bloomberg.com via Wikipedia.com

To illustrate my point further, imagine the government owning a home with a mortgage payment tied to a 2.5% interest rate (a tremendously low, average borrowing cost for the U.S. today). Now visualize the U.S. going bankrupt, which would then force foreign and domestic lenders to double or triple the rates charged on the mortgage payment (in order to compensate the lenders for heightened U.S. default risk). Global investors, including the Chinese, are pointing a gun at our head, and if a political blind eye on spending continues, our foreign brethren who have provided us with extremely generous low priced loans will not be bashful about pulling the high borrowing cost trigger. The ballooning mortgage payments resulting from a default would then break an already unsustainably crippling budget, and the government would therefore be placed in a position of painfully slashing spending. Too extreme a shift towards austerity could spin a presently wobbling economy into chaos. That’s precisely the situation we face under a no-action Congressional default (i.e., no fix by August 2nd or shortly thereafter). To date, the Chinese have collected their payments from us with a nervous smile, but if the U.S. can’t make some fiscally responsible choices, our Asian Pacific pals will be back soon with a baseball bat to collect.

The Cops to the Rescue

Any parent knows disciplining teenagers doesn’t always work out as planned. With fiscally irresponsible spending habits and debt load piling up to the ceiling, politicians are stealing the prospects of a brighter future from upcoming generations. The good news is that if the politicians do not listen to the parental voter cries for fiscal sanity, the capital market cops will enforce justice for the criminal negligence and financial thievery going on in Washington. Ed Yardeni calls these capital market enforcers the “bond vigilantes.” If you want proof of lackadaisical and stubborn politicians responding expeditiously to capital market cops, please hearken back to September 2008 when Congress caved into the $700 billion TARP legislation, right after the Dow Jones Industrial average plummeted 777 points in a single day.

Who exactly are these cops? These cops come in the shape of hedge funds, sovereign wealth funds, pension funds, endowments, mutual funds, and other institutional investors that shift their dollars to the geographies where their money is treated best. If there is a perceived, heightened risk of the United States defaulting on promised debt payments, then global investors will simply take their dollar-denominated investments, sell them, and then convert them into currencies/investments of more conscientious countries like Australia or Switzerland.

Assisting the capital market cops in disciplining the unruly teenagers are the credit rating agencies. S&P (Standard and Poor’s) and Moody’s (MCO) have been watching the slow-motion train wreck develop and they are threatening to downgrade the U.S.’ AAA credit rating. Republicans and Democrats may not speak the same language, but the common word in both of their vocabularies is “reelection,” which at some point will effect a reaction due to voter and investor anxiety.

Nobody wants to see our nation’s pipes burst from excessive debt and spending, and if the political plumbers can repair the very obvious and fixable fiscal problems, we can move on to more important challenges. It’s best we fix our problems by ourselves…before the cops arrive and arrest the culprits for gross negligence.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Performance data from Morningstar.com. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in MCO, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Do as I Say, Not as I Do

“Be smart…but don’t pay attention to me.”

Watching Goldman Sachs (GS) executives sweat it out under the hot lamps of Senator questioning makes for gripping television (see Goldman article), but as we all know the ethical standing of a significant number of politicians calls into question whether the pot should be calling the kettle black. Ever since I was a kid, I was told by seemingly responsible adults to “do as I say and not what I do.” I suppose the Goldman execs should follow the advice of Congress, but not their actions.

Based on a recent Wall Street Journal article that studied the investment activity of Congressional members (and spouses) during the financial crisis, the analysis discovered 13 of them were betting against the market. Just as Goldman and hedge fund manager John Paulson partnered to bet against the housing market via shorting synthetic CDOs (Collateralized Debt Obligations), Congressmen and their spouses were wagering against the market through the use of debt loaded (leveraged) exchange traded funds, which integrate derivatives.

Were any of the Congressional investment activities illegal? Likely not, but some question the ethical appearance of such behavior. The former head of the House Ethics Committee and past Representative Joel Hefley of Colorado believes such conduct “doesn’t look real great when the economy is tanking and people are blaming the government.” Facing similar challenges, the SEC’s (Security and Exchange Commission’s) squishy fraud charge complaint against Goldman Sachs is expected to encounter significant difficulty in proving the investment bank’s guilt.

Source: The Wall Street Journal (Yellow Dots = Shorting Exposure Trades)

Other politicians were critical of Wall Street too, despite apparent hypocritical behavior. For example, Representative Shelley Berkley of Nevada chided Wall Street for its reckless activities. “No casino on the planet behaves as irresponsibly and recklessly as Wall Street does. Wall Street ought to be ashamed, and take a lesson from the casino industry.” Nearly at the same time, Shelley’s husband Lawrence Lehrner placed 57 bearish trades.

I find it very amusing the same politicians shredding apart the Wall Street firms are in many cases the same politicians stretching the bounds of ethical behavior. Various politicians do a great job pontificating about the latest shortcomings of the financial industry, but fail to take some accountability for missing one of the greatest real estate booms of all-time. Where were the regulators and politicians when the debt bubble was bursting? Unfortunately, “reactive” is a much larger part of a politician’s lexicon than “proactive.” Responding to populist fervor is easier than leaning against consensus views, even if going against consensus makes more strategic sense.

For those having difficulty in deciphering the advice given by esteemed Congressmen, just remember to “do what they say, and not what they do.”

Read Full Wall Street Journal Article

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in GS, or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Nation’s CEOs Suffering Severely: Pay Down -0.08%

Hold on, let me pull out my violin to play some sympathetic consoling music for our nation’s Chief Executive Officers (CEOs). According to a Corporate Library survey of 2,700 publicly traded companies, CEO compensation declined -0.8% in 2008. I guess that 4th Ferrari and 3rd yacht will have to be put on hold. With some creative perseverance and a little elbow grease, I’m sure the class of underprivileged CEOs can still salvage a healthy package of stock options and restricted stock (to pad the paltry multi-million dollar salaries).

This is what Payscale.com had to say in a report from 2008:

“In 1970, CEO salary and bonus packages were typically about $700,000 – 25 times the average production worker salary; by 2000, CEO salaries had jumped to almost $2.2 million on average, 90 times the average salary of a worker, according to a 2004 study on CEO pay by Kevin J. Murphy and Jan Zabojnik. Toss in stock options and other benefits, and the salary of a CEO is nearly 500 times the average worker salary, the study says.”

Of course, Congress and the public are looking for scapegoats to blame for the global financial crisis. There is no better group to blame than highly compensated CEOs. As a result, we are seeing more “say on pay” proposals brought to shareholder votes, thereby removing power from the hands of self-appointed compensation committees and chummy board members. Currently, a Shareholder Bill of Rights Act is making its rounds through Congress that would establish an annual shareholder vote to approve executive compensation of executive management along with have a separate vote on “golden parachute” payments in the context of a company merger or acquisition.

The U.S. is not the only country to implement these types of shareholder rights. As David Ellis at CNN Money wrote, “In 2002, the United Kingdom embraced the practice, and it has subsequently been taken up in Australia and Sweden.” In the U.S. such proposals being considered are on a “non-binding” basis, which means that if “say on pay” is approved there will be no obligation for management to implement the changes – rather “shame” will be the strategic lever used by shareholders.

Everyone has been impacted in one shape or form by the financial crisis, so when you tuck-in your child or lay your head on the pillow tonight, rest assured our poor corporate CEOs are sharing in the pain…just remember, they only kept 99.2% of their pay last year.

Read More About Corporate Library Survey

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

{kind=link}