Posts tagged ‘compounding’

Dow Knocking on the Door of 40,000

The stock market rang the doorbell of the New Year with a bang during the 1st quarter. The S&P 500 index built on last year’s +24% gain with another +10% advance during the first three months of the year. And as a result of these increases, the Dow Jones Industrial Average index is knocking on the door of the 40,000 milestone – more specifically, the Dow closed the month at 39,807 (see chart below). To put his into context, when I was born more than 50 years ago, the Dow was valued at less than 1,000 – not a bad run. This is proof positive of what Einstein called the 8th Wonder of the World, “compounding”. At Sidoxia Capital Management, we view investing as a marathon, not a sprint. You cannot realize the benefits of compounding without having a long-term time horizon. The sooner you start saving and the more you save, the faster and larger your retirement nest egg will grow.

If you are one of the people who thinks the stock market is too high, then you should definitely ignore Warren Buffett, arguably the greatest investor of all-time. Buffett predicted the Dow will reach an astronomical level of one million (1,000,000) within the next 100 years. I’m not sure I will still be around to witness this momentous achievement, however, if history repeats itself, this targeted timeframe could prove conservative.

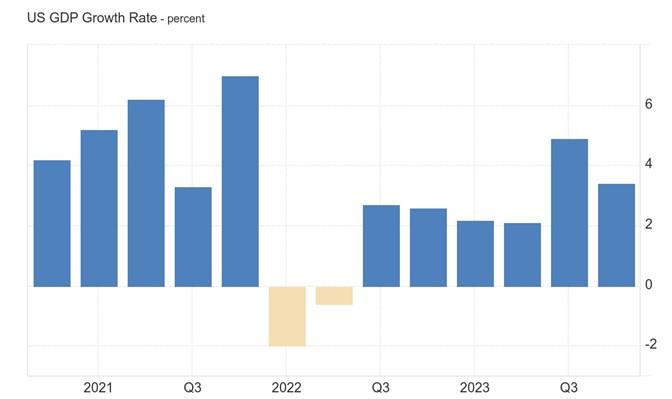

Despite the magnitude and duration of this bull market, there is still a lot of angst and anxiety over the upcoming election. Nevertheless, investors are choosing instead to focus on the strong fundamentals of the economy. Just this last week, we saw the broadest measurement of economic activity, GDP (Gross Domestic Product), get revised higher to +3.4% growth during the 4th quarter of 2023 (see chart below). On the jobs front, the unemployment picture remains healthy (3.9%), near a generational low.

Source: Trading Economics and Bureau of Economic Analysis

And when it comes to the all-important inflation data, the Federal Reserve’s preferred inflation measure, Core PCE index (Core Personal Consumption Expenditures), was also just released in-line with economists’ projections at 2.5% (see chart below), very near the Fed’s long-term 2.0% inflation target and well below the Core PCE’s recent peak near 6%.

Source: The Wall Street Journal and Commerce Department

This resilient economic data, when combined with the declining inflation figures, has resulted in the Federal Reserve sticking with its plan of cutting its Federal Funds interest rate target three times this year. If inflation reverses course or remains stubbornly high, then there is a higher likelihood that interest rate cuts will be delayed. On the flip side, if economic data slows significantly or the country goes into a recession, then the probability of sooner and/or more Fed interest-rate cuts will increase.

In other news, here are some of the other major financial headlines this month:

- Francis Scott Key Baltimore Bridge Collapse: Six people died when a large container ship crashed into the Francis Scott Key bridge in the Port of Baltimore. An estimated 50 million tons of goods valued at $80 billion flows through this port, making this one of the top 10 ports in the country. The auto and coal industry supply chains will be disproportionately affected, but the good news is much of these goods will be diverted to other larger ports (e.g., Port of New York and Port of New Jersey).

- DJT Debut: A lot of hype surrounded the trading debut of Trump Media & Technology Group, which began trading last week under the initials of our country’s former president, Donald J. Trump (Ticker: DJT). Despite only posting a few million in revenue and -$50 million in losses during the first nine months of 2023, the stock skyrocketed +65% in its first week of trading and attained a $9 billion valuation. Time will tell if Trump’s Truth Social media platform will gain traction and justify the stock’s price, or rather suffer the declining fate of other meme stocks like GameStop Corp. (GME) or AMC Entertainment Holdings (AMC).

- SBF Sentenced to 25 Years: The former CEO of cryptocurrency exchange company FTX, Sam Bankman-Fried (SBF), was sentenced to 25 years in prison due to his conviction on seven counts of fraud and what is believed to be $8 billion in stolen client funds. SBF didn’t help his own cause by perjuring himself, tampering with witnesses, and showing a lack of remorse, according to the judge.

We are only 25% of the way through the year, but the Dow is knocking on the 40,000-milestone door. The way things look now, investors are wiping their feet on the welcome doormat and ready to walk right in.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (April 1, 2024). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in individual stocks , certain exchange traded funds (ETFs), and notes including AMC 2026, but at the time of publishing had no direct position in DJT, GME, AMC or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Filet or Mac & Cheese? Investing for Retirement

The financial crisis of 2008-2009 placed a large swath of investors into paralysis based on a fear the United States and the rest of the world was on the verge of irreversible destruction. Regardless of what the newspaper headlines are reading and television pundits are spouting, individuals have to shrewdly plan for retirement no matter what the economy is doing. So then the question becomes, do you want to be eating macaroni & cheese in retirement, or does filet mignon or alternate five-star cuisine sound more appealing? I vote for the latter.

Despite what the government statistics are saying about the current state of benign inflation, you do not need to be a genius to see medical costs are exploding, energy charges have skyrocketed, and even more innocuous items such as movie ticket prices continue to rise. If that’s not a burden enough, depending on your age, there’s a legitimate concern the Social Security and Medicare safety nets may not be there for you in retirement. It is more important than ever to take control of your financial future by investing your money in a more efficient manner (see Fusion), focusing on long-term, low-cost, tax-efficient strategies. Whatever the direction of the financial markets (up, down, or sideways), if you don’t wisely invest your money, you will run the risk of working as a Wal-Mart (WMT) greeter into your 80s and relegated to eating mac & cheese (for lunch and dinner).

Broaden Your Horizons

The last decade has been tough for domestic equities. It’s true that not a lot of compounding of returns has occurred in the domestic equity markets over the last decade (see Lost Decade), but that weakness is not necessarily representative of the next decade’s performance or the past relative strength seen in areas like emerging markets, materials and certain fixed income markets. These alternatives, including cash, would have added significant diversification benefits to investor portfolios during previous years. Rather than focusing on what’s best for the investor, so much financial industry attention has been placed on high cost, high fee, high commission domestic stock funds or insurance-based products. Due to many inherent conflicts of interest, many individual investors have lost sight of other more attractive opportunities, like exchange traded funds, international strategies, and fixed-income investment vehicles.

Rule of 72

Depending on your risk profile, objectives and constraints, the “Rule of 72” implies your retirement portfolio should double from a $100,000 investment now to roughly $200,000 in seven years (to $400,000 in 14 years, $800,000 in 21 years, etc.), assuming your portfolio can earn a 10% annual return. Unfortunately, this snowballing effect of money growth does not work if you are paying out significant chunks of your returns to aggressive brokers and salespeople in the forms of high commissions, fees, and taxes (see a Penny Saved is Billions Earned). For example, if you are paying out total annual expenses of 2-3% to a broker, advisor, or investment manager, the doubling effect of the Rule of 72 will be stretched out to 9-10 years (rather than the above mentioned seven years). If you do not know what you are paying in fees and expenses (like the majority of people), then do yourself a favor and educate yourself about the fee structures and tax strategies utilized in your investments (see also Investor Confusion). If you haven’t started investing, or you are shoveling out a lot of money in fees, expenses, and taxes, then you should reconsider your current investment stretegy. Otherwise, you may just want to begin stockpiling a lot of macaroni & cheese in your retirement pantry.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and shares in WMT, but at the time of publishing SCM had no direct positions in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC “Contact” page for more information.

Compounding: A Penny Saved is Billions Earned

What is “compounding” and why is it so great? It sounds like such a fancy financial term. One can think of compounding as a snowball rolling down a hill – the longer the snowball rolls (or the higher up the mountain you begin), the more compounding will expand the size of your snowball. Expanding your investment portfolio through compounding should be your major goal.

Albert Einstein, arguably one of the most intelligent people to walk this planet, was asked to describe mankind’s greatest discovery. His answer: “compound interest.” He went so far as to call it one of the “Eight Wonders of the World.” The benefits of compounding can be demonstrated via famous explorer, Christopher Columbus.

We all know the story, “In 1492, Christopher Columbus sailed the ocean blue.” To emphasize the benefits of compounding, let us suppose that Christopher Columbus made an investment in the historic year of 1492. If Chris had placed a single penny in a 6% interest-bearing account and instructed someone to remove the interest every year and put it in a piggybank, the total value collected in that piggybank would eventually accumulate to more than 30 cents. A pretty nice multiplier-effect on one penny, but not too much absolute cold hard cash to write home about…agreed?

"It's magic, I can turn pennies into billions."

However, if the young explorer had placed the same paltry investment of one cent into the same interest-bearing account, but LEFT the remaining earned interest to compound (thereby earning interest upon the previously earned interest) the results would be drastically different.

What would you guess the compounded account would be worth in 2009?

$10,000? $100,000? $1 million? $10 million? $100 million?

“NO” is the correct answer to all these guesses.

The correct answer: $121,096,709,346.21! Your eyes do not deceive you. That one penny invested in 1492 would have grown to $121 billion dollars today. If you don’t believe me, pull out your calculator and multiply $.01 * 1.06%, and repeat 517 times. Surely, we will not live 517 years to collect on an investment of such long duration. However, with proper planning everyone has the ability to invest quite a bit more than one cent to significantly build future wealth.

As an advisor, the problems related to compounding I see investors commit most are two-fold:

1) Investors are constantly shifting money in and out of their accounts (usually at suboptimal points) due to apprehension and greed, thereby nullifying the benefits of compounding.

2) Because of overpowering fear relating to current economic conditions, investors are parking their money in low yielding CDs (Certificates of Deposit), savings accounts, checking accounts, money market accounts, or other low returning investment vehicles. This strategy is equivalent to pushing the aforementioned snowball over the sidewalk, rather than down a long, steep hill.

In order to reap the rewards of compounding and dramatically expand your investment portfolio, a systematic, disciplined approach to investing needs to be followed. A system that more likely than not has a 20 year horizon rather than 20 days. Now go start saving those pennies!

{kind=link}