Posts tagged ‘collapse’

Markets Surge Higher Despite Shutdown Anxiety Fire

Wars rage on in Ukraine and Gaza, political violence is on the rise at home, tariff-driven inflation remains debated, and anxiety over a looming government shutdown is intensifying. On the surface, this might sound like the perfect recipe for a market meltdown. But Wall Street seems unfazed. In fact, U.S. equities pushed to new record highs again this month, continuing the bull market’s relentless advance in the face of these concerns.

Here is a market performance snapshot for the month:

- S&P 500: +3.5% (+13.7% year-to-date)

- Dow Jones Industrial Average: +1.9% (+9.1% year-to-date)

- NASDAQ Composite: +5.6% (+17.3% year-to-date)

What’s fueling the optimism?

• A Strong Economy: The economy just produced a final +3.8% GDP growth for the 2nd quarter, and the Atlanta Federal Reserve is forecasting an even stronger economy for the 3rd quarter of +3.9% (see below).

• Robust Corporate Earnings: S&P 500 corporate profits surged by +11.8% in the 2nd quarter and consensus estimates call for 3rd quarter growth of +7.9%. Historically, CEOs tend to set conservative forecasts, therefore actual results often exceed low-bar expectations. Therefore, it’s very possible that Q3 earnings growth could achieve double-digit growth levels once again.

• A.I. Drive Still Alive: With trillions of dollars in A.I. spending plans already announced, hungry investors once again gobbled up A.I. tech stocks last month. For instance, Oracle Corp’s (ORCL) stock jumped +24% for the month in large part driven by a $317 billion increase in backlog orders during the company’s first fiscal quarter. Reportedly, the majority of the massive increase in orders came from one customer, OpenAI – the brains behind the A.I. juggernaut, ChatGPT. The rise in Oracle’s share price temporarily propelled CEO Larry Ellison past Tesla’s (TSLA) CEO Elon Musk as the world’s richest person, before markets began critically questioning whether OpenAI’s CEO (Sam Altman) can ultimately fund the hundreds of billions of dollars in Oracle commitments.

Source: Atlanta Federal Reserve

Shutdown Jitter History

Market anxiety has shifted from a hypothetical government shutdown nightmare to a scary reality, given the funding deadlines have already lapsed. Many investors are asking what this means for stocks. Fortunately, government shutdowns are nothing new. Our country has flourished over the last 50 years despite experiencing around two dozen shutdowns, many of which only lasted a few hours, a few days, or a few weeks. According to Kiplinger, since the 1970s, the stock market has averaged a +0.3% return during shutdown periods (see chart below).

Source: Kiplinger

In fact, the longest shutdown on record occurred most recently from December 2018 to January 2019 (35 days during President Trump’s first term) and resulted in a sharp +10% gain (see chart below).

Source: Kiplinger / YCharts

The partisan finger-pointing will continue, but history suggests that shutdowns are short-term noise with little bearing on long-term market direction. Long-term investors understand there is never a shortage of concerns during bad times (e.g., potential recessions, job losses, credit defaults, bankruptcies, etc.), or good times as well (e.g. fear of inflation, restrictive monetary policy, politics, etc.). Turning off the TV is often the best course of action (see also – Turn Off the TV).

What’s Next? Looking Ahead After more than 30 years of investing—including weathering the dot-com tech sense of purpose collapse in 2000—I’ve learned that markets always have a tendency of climbing a wall of worry, so it’s better to not react emotionally to daily news headlines. Rather, it’s better for investors to stay focused on those market leading, innovative companies and concentrate on those sectors experiencing long-term secular trends.

As we enter Q4 and head toward 2026, A.I. remains the defining theme. Since the launch of ChatGPT in November 2022, the S&P 500 has surged +24% in 2023, +23% in 2024, and +14% so far in 2025. Unfortunately, trees do not grow to the sky forever.

At Sidoxia Capital Management, we understand that valuations currently are stretched on a historic basis and that markets never move in a straight line. As a result, a correction at some point in stock prices should not come as a surprise to anyone. Nevertheless, whether you’re bullish on the productivity gains from large language models (LLMs) or skeptical of over-investment and hype, one thing is clear: A.I. is here to stay, and it doesn’t matter if you believe the government shutdown flames will grow into an inferno or fizzle out in smoke, which is usually the case.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (October 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in ORCL, TSLA, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Even Winning Teams Occasionally Lose

The stock market has been a winning team for years, generating outsized returns for investors. But so far this year, the winning streak appears to be coming to an end. For 2022, the S&P 500 index is down -21%, including -8% last month. However, since 2008, the stock market has generally been on a consistent tear racking up a record of 10 wins, 2 losses (2015 and 2018), and one tie (2011). In recent years, the U.S. stock market has been winning by a large margin (2019: +29%, 2020: +16%, 2021: +27%) and a significant contributor to the team’s win streak has been the Federal Reserve, or the designated hitter (DH).

Jerome Powell, the Fed Chair, has been a very effective clean-up hitter for the stock market, not only leading the stock market team to victories, but also appreciation in almost all global-risk asset classes. By keeping interest rates (the Federal Funds Rate target) essentially at 0% over the last few years, since the initial COVID pandemic outbreak, many investors are blaming Mr. Powell for elevated inflation rates. If that were truly the case, then we probably wouldn’t see the ubiquitous inflation globally, as we do now. Just as you would expect with any baseball team, any single player does not deserve all the credit for wins, nor should any single player receive all the blame for losses – the same principle applies to the Federal Reserve.

Regardless, the stock market’s best hitter is now injured. In addition to pushing interest rates higher, the Fed is hurting the team through its monetary policy of quantitative tightening or QT (i.e., selling bonds off the Fed’s balance sheet). Theoretically, QT should cause interest rates to move higher, all else equal, and thereby slow down growth in the economy, and help tame out-of-control inflation.

The stock market was also thrown a curve ball when Russia invaded Ukraine, which added gasoline to an already flaming inflation fire. Globally, consumers and businesses have witnessed exploding oil/gasoline prices, in addition to escalated food prices caused by a lack of grain and other commodity exports out of Ukraine.

Lastly, a wild pitch has been thrown at the U.S. stock market by China with its zero-COVID policy, which has essentially shut down the world’s 2nd largest economy and further delayed the full reopening of the global economic game. As a result of China’s hardline lockdown stance, global supply chain disruptions have intensified and import prices have mushroomed higher.

Although this all sounds like horrible news, in the game of investing, nobody wins all the time. As history teaches us, the stock market is generally up around 70% of the time. It just happens to be that we are in the middle of a 30% losing period.

Bad News Does Not Mean Bad Stock Market

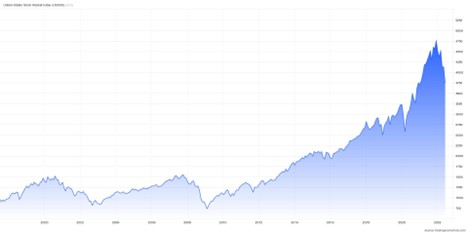

The majority of economists, strategists, and talking heads on television are forecasting a recession in our economy, either this year or next. This should come as no surprise to any experienced investor, as history teaches us that recessions occur on average about twice every decade. Long-term investors also understand that stock prices do not always just go up on good news and down on bad news. Stocks can go down on good news, and up on bad news. In fact, over the last 13 years, since the bottom of the 2008-2009 financial crisis, the stock market has increased about six-fold (even after this year’s -21% correction) in the face of some horrendously scary headlines (also see chart below):

· Ukraine-Russia

· COVID

· Elections / Capitol Insurrection

· Exit from Afghanistan

· Impeachment

· China Trade War & Tariffs

· Inverted Yield Curves

· N. Korea Missile Launches

· Brexit

· ISIS in Iraq

· Ebola

· Russia Takeover of Crimea

· Double Dip Recession Fears

· Eurozone Debt Crisis

S&P 500 Index (1997 – 2022)

Despite the recent headwinds in the stock market, not all the news is bad. Here are some tailwinds:

- PROFITS: Corporate profits remain at or near record levels.

- INFLATION: Inflation appears to be cooling as evidenced by declining commodity prices (TR Commodities CRB Index).

CRB Commodities Index (2022)

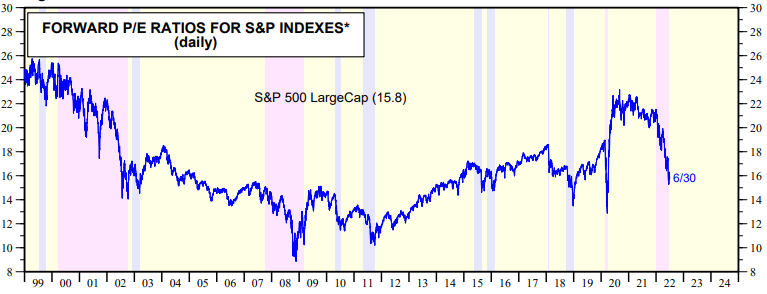

- PRICES: Valuations have come down significantly – Price/Earnings ratio of 15.9 (i.e., stock prices are on sale).

- SENTIMENT: Sentiment remains fearful – a contrarian buy indicator (an elevated VIX – Volatility Index can signal buying opportunities). As Warren Buffett says, “Be fearful when others are greedy, and greedy when others are fearful.”

VIX – Volatility Index (2021 – 2022)

Even though the U.S. stock market has been a long-term winner, investors have been betting against the winning team by selling stocks. As mentioned earlier, recessions, if we get one, are common and nothing new. The -21% correction in stock prices is already factoring in a mild recession, so we have already suffered near-maximum pain. Could prices go lower? Certainly. But should you quit a 26-mile marathon at mile 25 because the pain is too intense? In most instances, the answer should absolutely be “no” (see also No Pain, No Gain). Eventually, the Fed will stop raising interest rates, inflation will cool, the Russia-Ukraine war will be resolved, and solid growth will return. While many people are betting the stock market will lose this year, many long-term investors recognize betting on stock market success is a winning strategy over the long-run, especially when prices are on sale.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in BRKA/B or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Too Big to Fail (Review)

Some call Andrew Ross Sorkin’s new behind-the-scenes book about the financial crisis of 2008-2009 “Too Big to Read” due to its meaty page count at 624 pages (a tad more than my book). But actually, once you crack the first chapter of Too Big to Fail you become immediately sucked in. In creating the “fly on the wall” perspective covering the elite power brokers of Wall Street and Washington, Sorkin utilizes 500 hours of interviews with more than 200 individuals.

Through the detailed and vivid conversations, you get the keen sense of overwhelming desperation and self-preservation that overtakes the executives of the sinking financial system. Some of the chief participants failed, some were triumphant, and some were pathetically bailed out. History will ultimately be the arbiter of whether government and Wall Street averted, mitigated, postponed, or contributed to the financial collapse. Regardless, Sorkin brilliantly encapsulates this emotionally panicked period in our history that will never be erased from our memories.

Here are a few passages that capture the feeling and mood of the book:

Merger Musical Chairs

The terror-induced insanity of merger musical chairs is best depicted through the notepad of Timothy Geithner, then the president of the New York Federal Reserve Bank:

“On a pad that morning, Geithner started writing out various merger permutations: Morgan Stanley and Citigroup. Morgan Stanley and JP Morgan Chase. Morgan Stanley and Mitsubishi. Morgan Stanley and CIC. Morgan Stanley and Outside Investor. Goldman Sachs and Citigroup. Goldman Sachs and Wachovia. Goldman Sachs and Outside Investor. Fortress Goldman. Fortress Morgan Stanley. It was the ultimate Wall Street chessboard.”

AIG Bombshell

The book is also laced with financial nuggets to put the scope of the crisis in perspective. Here Sorkin examines the distressed call of assistance from AIG CEO, Bob Willumstad, to Timothy Geithner:

“A bombshell that Willumstad was confident would draw Geithner’s attention-was a report on AIG’s counterparty exposure around the world, which included ‘$2.7 trillion of notional derivative exposures, with 12,000 individual contracts.” About halfway down the page, in bold, was the detail that Willumstad hoped would strike Geithner as startling: “$1 trillion of exposures concentrated with 12 major financial institutions.’”

Bernanke’s Bumbled Spelling Bee

In setting the stage for the drama that unfolds, Sorkin also provides a background on the key players in the book. For example in describing Ben Bernanke you learn he was

“born in 1953 and grew up in Dillon South Carolina, a small town permeated by the stench of tobacco warehouses. As an eleven-year-old, he traveled to Washington to compete in the national spelling championship in 1965, falling in the second round, when he misspelled ‘Edelweiss.’”

TARP Tidbits

On how the precise $700 billion TARP (Troubled Asset Relief Program) figure was created, Sorkin describes the scattered thought process of the program designer Neel Kashkari:

“They knew they could count on Kashkari to perform some sort of mathematical voodoo to justify it: ‘There’s around $11 trillion of residential mortgages, there’s around $3 trillion of commercial mortgages, that leads to $14 trillion, roughly five percent of that is $700 billion.’ As he plucked numbers from thin air even Kashkari laughed at the absurdity of it all.”

Mercedes Moment

Mixed in with the facts and downbeat conversations are a series of humorous anecdotes and one-liners. Here is one exchange between Goldman Sachs CEO, Lloyd Blankfein, and his Chief of Staff Russell Horwitz:

“’I don’t think I can take another day of this,’ Horowitz said wearily. Blankfein laughed. ‘You’re getting out of a Mercedes to go to the New York Federal Reserve – you’re not getting out of a Higgins boat* on Omaha Beach! Keep things in perspective.’”

*Blankfein’s quote: A reference to the bloody D-Day battle.

Too Big to Fail is an incredible time capsule for the history books. Let’s hope we do not have to relive a period like this in our lifetimes. I wouldn’t mind reading another Andrew Ross Sorkin book…just not another one about a future financial crisis.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but did not have any direct positions in any stock mentioned in this article at time of publication (including GS, AIG, WFC, MS, and C). No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Pinning Down Roubini Requires a Lasso

Pinning down a Nouriel Roubini forecast is like lassoing a frenzied cow. They say a broken clock is right twice a day, and maybe the same principle applies to renowned economist, Professor Roubini (NYU)? Sure, credit should be given where credit is due. He nailed the forecast relating to the housing led financial bubble and subsequent financial collapse – even if the prediction was years early.

Here’s where I have a beef. Now that Roubini has become a celebrated rock star with frequent television interviews and speaking engagements, his touring views are becoming more fluid and slippery as time progresses. Sure it’s more comfortable to ride the fence and lean in whatever direction the weekly economic winds are blowing. I suppose if you throw out enough changing viewpoints, which adjust to evolving moods, you can never be wrong.

Let’s examine some of his views:

- Out of Context: Just last week, Mr. Roubini said the “worst is behind us,” but in order to retain his “Dr. Doom” celebrity status he felt compelled to issue a press release clarifying his statements. He noted his “views were taken out of context,” and added, “I have said on numerous occasions that the recession would last roughly 24 months.” That’s funny, because he just stated last year it would be 12-18 months (Click Here for Video).

- Sweating Out Rebound: Maybe the 41% bounce in the S&P 500 or the 49% jump in the NASDAQ from March 9th lows compelled Roubini to make the “worst is behind us” comments, but why then at the beginning of this year did he say, “We are still only in the early stages of this crisis. My predictions for the coming year, unfortunately, are even more dire: The bubbles, and there were many, have only begun to burst.” Hmmm…excuse me while I scratch my head.

- Alphabet Soup Recovery: Also frustrating are the John Kerry-esque waffling comments relating to whether this economic recovery will be a U, W, or L-shaped economic recovery. Last April he was in the U-camp: “My view is closer to a U-shaped recession as I expect that the economic contraction will last at least 12 months and possibly as long as 18 months through the middle of 2009.” Now, as early as last month Roubini is warning of a double dip or “W-shaped” recovery with the rising possibility of a “perfect storm” in 2010 (Click Here for Video). He sees the expiration of tax cuts, rising oil prices, inflating debt and interest rates leading to another downturn. So is it U or W, or will we hear more about an “L” shaped recovery? Maybe the worst is not behind us? I’m confused.

- Doomsday Earnings Yet to Arrive: Still early in the quarterly earnings reporting season but Roubini’s call for a downside in corporate earnings has yet to materialize. As a matter of fact, Zacks Investment Research reported last week that early second quarter upside surprises are beating downside surprises by a ratio of 7 to 1. So far not too “Doom-full.”

I’m no economist or recovery expert, but what I do know is that I’m having difficulty pinning down Professor Roubini’s ever-changing views. I suppose I will just mail CNBC, Bloomberg, or the bevy of other Roubini media groupies a lasso in hopes they will pin Mr. Roubini down.

Wade W. Slome, CFA, CFP®

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}