Posts tagged ‘cnbc’

Markets Soar and Investors Snore

This article is an excerpt from a previously released Sidoxia Capital Management complementary newsletter (August 1, 2013). Subscribe on the right side of the page for the complete text.

If you haven’t been paying close attention, or perhaps if you were taking a long nap, you may not have noticed that the stock market was up an astounding +5% in July (+78% if compounded annualized), pushing the S&P 500 index up +18% for the year to near all-time record highs. Wait a second…how can that be when that bald and grey-bearded man at the Federal Reserve has hinted at bond purchase “tapering” (see also Fed Fatigue)? What’s more, I thought the moronic politicians were clueless about our debt and deficit-laden economy, jobless recovery, imploding eurozone, Chinese real estate bubble, and impending explosion of inflation – all of which are expected to sink our grandchildren’s grandchildren into a standard of living not seen since the Great Depression. Okay, well a dash of hyperbole and sarcasm never hurt anybody.

This incessant stream of doom-and-gloom pouring over our TVs, newspapers, and internet devices has numbed Americans’ psyches. To prove my point, the next time you are talking to somebody at the water cooler, church, soccer game, or happy hour, gauge how excited your co-worker, friend, or acquaintance gets when you bring up the subject of the stock market. If my suspicions are correct, they are more likely to yawn or pass out from boredom than to scream in excitement or do cartwheels.

You don’t believe me? Reality dictates the wounds from the 2008-2009 financial crisis are still healing. Panic and fear may have disappeared, but skepticism remains in full gear, even though stocks have more than doubled in price in recent years. Here is some data to support my case there are more stock detractors than defenders:

Record Savings Deposits

|

| Source: Calafia Beach Pundit |

Although there are no signs of an impending recession, defensive cash hoarded in savings deposits has almost increased by $3 trillion since the end of the financial crisis.

Blah Consumer Confidence

|

| Source: Calafia Beach Pundit |

As you can see from the chart above, Consumer Confidence has bounced around quite a bit over the last 30+ years, but there is no sign that consumer sentiment has turned euphoric.

15-Year Low Stock Market Participation

|

|

Source: Gallup Poll

|

There has been a trickling of funds into stocks in 2013, yet participation in the stock market is at a 15-year low. Investors remain nervous.

Lack of Equity Fund Buying

|

| Source: ICI & Calafia Beach Pundit |

After a short lived tax-driven purchase spike in January, the buying trend quickly turned negative in the ensuing months. Modest inflows resumed into equity funds during the first few weeks of July (source: ICI), but the meager stock fund investments represent < 95% of 2012 positive bond flows ($15 billion < $304 billion, respectively). Moreover, these modest stock inflows pale in comparison to the hundreds of billions in investor withdrawals since 2008. See also Fund Flows Paradox – Investing Caffeine.

Decline in CNBC Viewership

In spite of the stock market more than doubling in value from the lows of 2009, CNBC viewer ratings are the weakest in about 20 years (source: Value Walk). Stock investing apparently isn’t very exciting when prices go up.

The Hater’s Index:

And if that is not enough, you can take a field trip to the hater’s comment section of my most recent written Seeking Alpha article, The Most Hated Bull Market Ever. Apparently the stock market more than doubling creates some hostile feelings.

JOLLY & JOVIAL MEMO

Keeping the previous objective and subjective data points in mind, it’s clear to me the doom-and-gloom memo has been adequately distributed to the masses. Less clear, however, is the dissemination success of the jolly-and-jovial memo. I think Ron Bailey, an author and science journalist at Reason.com (VIDEO), said it best, “News is always bad news. Good news is simply not news…that is our [human] bias.” If you turn on your local TV news, I think you may agree with Ron. Nevertheless, there are actually plenty of happier news items to report, so here are some positive bullet points to my economic and stock market memo:

16th Consecutive Positive GDP Quarter*

|

| Source: Quartz.com |

The broadest measure of economic activity, GDP (Gross Domestic Product), was reported yesterday and came in better than expected in Q2 (+1.7%) for the 16th straight positive reported quarter (*Q1-2011 was just revised to fractionally negative). Obviously, the economists and dooms-dayers who repeatedly called for a double-dip recession were wrong.

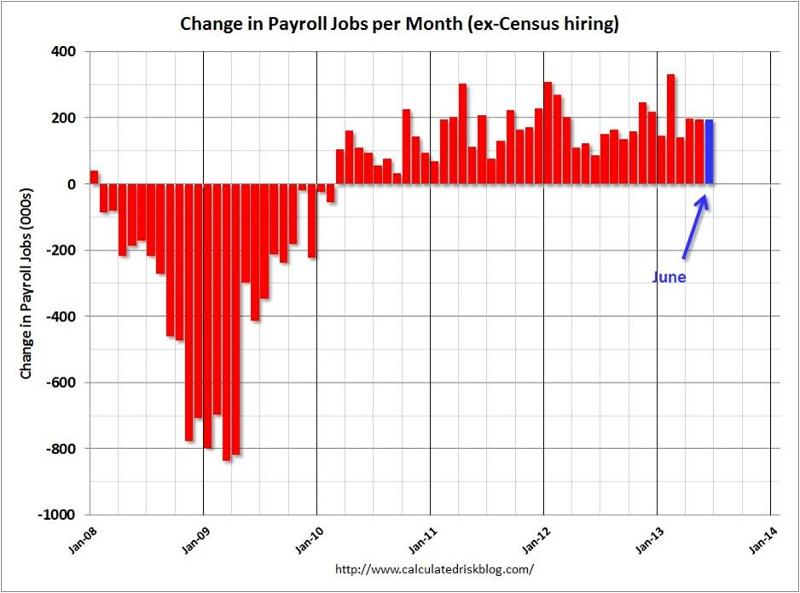

40 Consecutive Months & 7 Million Jobs

Source: Calculated Risk

The economic recovery has been painfully slow, but nevertheless, the U.S. has experienced 40 consecutive months of private sector job additions, representing +7.2 million jobs created. With about -9 million jobs lost during the most recent recession, there is still plenty of room for improvement. We will find out if the positive job creation streak will continue this Friday when the July total non-farm payroll report is released.

Housing on the Mend

|

| Source: Calafia Beach Pundit |

New home sales are up significantly from the lows; housing starts have risen about 40% over the last two years; and Case Shiller home prices rose by +12.2% in the latest reported numbers. The housing market foundation is firming.

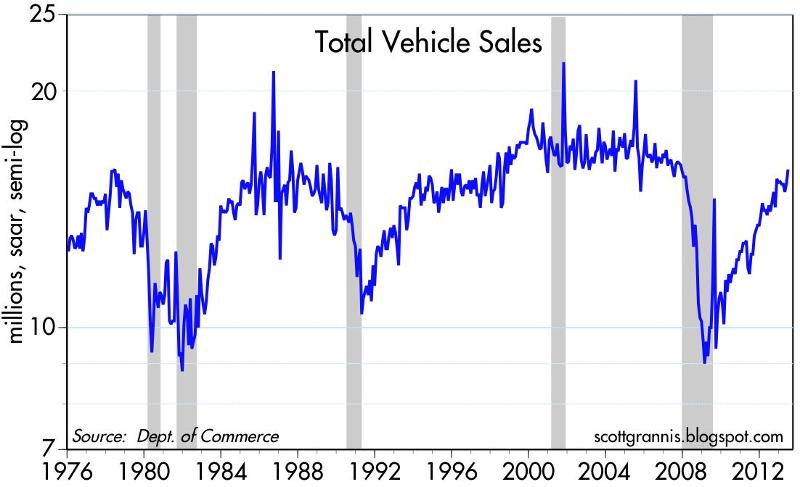

Auto Sales Rebound

|

| Source: Calafia Beach Pundit |

Auto sales remain on a tear, reaching an annualized level of 15.9 million vehicles, the highest since November 2007, and up +12% from June 2012. Car sales have almost reached pre-recessionary levels.

Record Corporate Profits

|

| Source: Dr. Ed’s Blog |

Optimistic forecasts have been ratcheted down, nonetheless corporate profits continue to grind to all-time record highs. As you can see, operating earnings have more than doubled since 2003. Given reasonable historical valuations in stocks, as measured by the P/E (Price Earnings) ratio, persistent profit growth should augur well for stock prices.

Bad Banks Bounce Back

Europe on the Comeback Trail

|

| Source: Calafia Beach Pundit |

There are signs of improvement in the Eurozone after years of recession. Talks of a European Armageddon have recently abated, in part because of Markit manufacturing manager purchasing statistics that are signaling expansion for the first time in two years.

Overall, corporations are achieving record profits and sitting on mountains of cash. The economy is continuing on a broad, steady recovery, however investors remain skeptical. Domestic stocks are at historic levels, but buying stocks solely because they are going up is never the right reason to invest. Alternatively, bunkering away excessive cash in useless, inflation depreciating assets is not the best strategy either. If nervousness and/or anxiety are driving your investment strategy, then perhaps now is the time to create a long-term plan to secure your financial future. However, if your goal is to soak up the endless doom-and-gloom and watch your money melt away to inflation, then perhaps you are better off just taking another nap.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Jobs and the DMV Economy

If you have ever gone to get your driver’s license at the Department of Motor Vehicles (DMV)…you may still be waiting in line? It’s a painful but often a mandatory process, and in many ways the experience feels a lot like the economic recovery we currently have been living through over the last four years. Steady progress is being made, but in general, people hardly notice the economy moving forward.

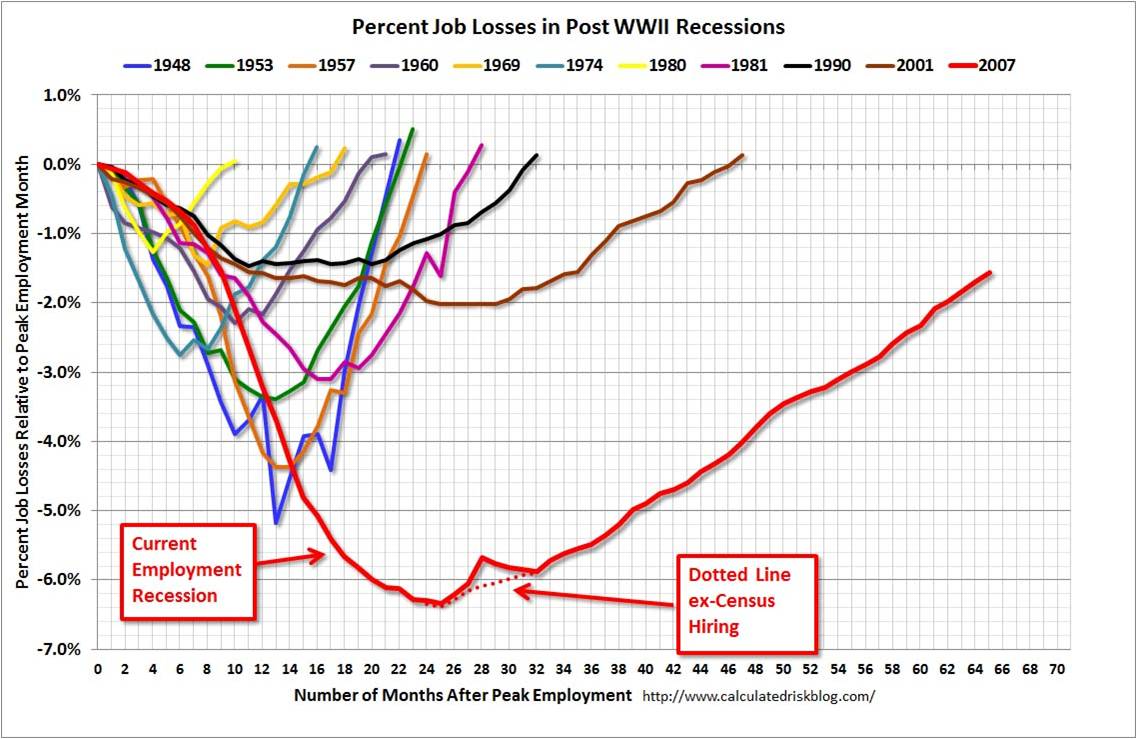

My geographic neighbor and blogger here in Orange County, California (Bill McBride – Calculated Risk) has some excellent visuals that compare our sluggish DMV economy with previous economic cycles dating back to 1948:

Source: Calculated Risk

As you can see from the chart above, the current economic recovery (red-line), as measured by job losses, is the slowest comeback in more than a half-century. Basically, over a two year period, the U.S. lost about nine million jobs, and during the following three years the economy regained approximately seven million of those jobs – still digging out of the hole. Last Friday’s June jobs report was welcomed, as it showed net jobs of +195,000 were added during the month, and importantly the previous two months were revised higher by another +70,000 jobs. These data points combined with last month’s Fed’s QE3 tapering comments by Ben Bernanke help explain why the continued rout in 10 year Treasury rates has continued in recent weeks, propelling the benchmark rate to 2.71% – almost double the 1.39% rate hit last year amidst continued European financial market concerns.

As with most recessions or crashes, the bursting of the bubble (i.e., damage) occurs much faster than the inflation (i.e., recovery), and McBride’s time series clearly shows this fact:

Source: Calculated Risk

While pessimists point to the anemic pace of the current recovery, the glass half-full people (myself included) appreciate that the sluggish rebound is likely to last longer than prior recoveries. There are two other key dynamics underlying the reported employment figures:

- Continued Contraction in Government Workers: Excessive government debt and deficits have led to continued job losses – state and local job losses appear to be stabilizing but federal cuts are ongoing.

- Decline in the Labor Force Participation Rate: Discouraged workers and aging Baby Boomer demographics have artificially lowered the short-term unemployment figures because fewer people are looking for work. If economic expansion accelerates, the participation contraction trend is likely to reverse.

Skepticism Reigns Supreme

Regardless of the jobs picture and multi-year expansion, investors and business managers alike remain skeptical about the sustainability of the economic recovery. Anecdotally I encounter this sentiment every day, but there are other data points that bolster my assertion. Despite the stock market more than doubling in value from the lows of 2009, CNBC viewer ratings are the weakest in about 20 years (see Value Walk) and investments in the stock market are the lowest in 15 years (see Gallup poll chart below):

Source: Gallup

Why such skepticism? Academic research in behavioral finance highlights innate flaws in human decision-making processes. For example, humans on average weigh losses twice as much as gains as economist and Nobel prizewinner Daniel Kahneman explains in his book Thinking Fast and Slow (see Investing Caffeine article: Decision Making on Freeways and in Parking Lots). Stated differently, the losses from 2008-2009 are still too fresh in the minds of Americans. Until the losses are forgotten, and/or the regret of missing gains becomes too strong, many investors and managers will fearfully remain on the sideline.

The speed of our economic recovery is as excruciatingly agonizing, and so is waiting in line at the DMV. The act of waiting can be horrific, but obtaining a driver’s license is required for driving and investing is necessary for retirement. If you don’t want to go to investing jail, then you better get in the investing line now before job growth accelerates, because you don’t want to be sent to the back of the line where you will have to wait longer.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Herbalife Strife: Icahn & Ackman Duke It Out

I have seen a lot of things in my two decades in the investment industry, but seeing a verbal cage fight between a senile 76 year-old corporate raider and a white-haired, 46 year-old Harvard grad makes for surprisingly entertaining viewing. The investment heavyweights I am referring to are the elder Carl Icahn, Chairman of Icahn Enterprises, and junior Bill Ackman, CEO of Pershing Square Capital Management. If getting a few billionaires yelling at each other on live TV is not enough to interest you, then how about adding some tongue-laced f-bombs coupled with blow-by-blow screaming from background traders?

What’s the source of the venomous, spitting hatred between these stock market tycoons? In short, it can be boiled down to a decade old lawsuit (profitable for both I might add), and a disagreement over the short position of a controversial stock, Herbalife (HLF). Regarding the legal spat, in 2003 the SEC was investigating Ackman while his Gotham Partners hedge fund was collapsing, so Ackman asked Icahn to buy shares of Hallwood Realty in hopes of salvaging his fund. Eventually, Icahn bought shares, but a difference in opinion over the transaction led to a lawsuit that Icahn lost, thereby forcing him to pay Ackman $9 million.

Icahn also had a beef with Ackman’s handling of Herbalife: Parading in front of hundreds of investors to self-indulgently create a bear raid on an unsuspecting company is poor form in Icahn’s view, and Carl wanted to make sure Ackman was aware of this investing faux pas.

Normally, investing reporting over cable television is rather mundane, unless you consider entertainers like Jim Cramer yelling “booyah” amusing (see also my article on Mr. Booyah)? On the other hand, if you enjoy billionaires embracing the spirit of the Jerry Springer Show by screaming purple-faced profanities, then you should check out the CNBC cage fight here in its entirety:

If you lack time in your busy schedule to soak in the full bloody battle, then here is a synopsis of my favorite highlights:

Icahn on Ackman the “Crybaby”: “I really sort of have had it with this guy Ackman….I get a call from this Ackman guy. I’m telling you, he’s like the crybaby in the schoolyard. I went to a tough school in Queens. They used to beat up the little Jewish boys. He was like a little Jewish boy crying that the world was taking advantage of him.”

Ackman Referring to Icahn as a “Bully” and Himself as “Roadkill on the Hedge Fund Highway”: “Why did he [Icahn] threaten to sue me? He was a bully. Okay? I was not in a good place in my business career. I was under investigation by Spitzer, winding down my fund. There was negative press about Gotham Partners. I was short MBIA (MBI). They were aggressively attacking me and Carl Icahn thought this guy [Ackman] is roadkill on the hedge fund highway… This is not an honest guy [Icahn] who keeps his word. This is a guy who takes advantage of little people.”

Agitated Icahn Tearing a New One for Scott Wapner (CNBC Commentator): “I didn’t get on to be bullied by you [Wapner]… I’m going to talk about what I want to talk about. Okay? If you want to take that position, I will never go on CNBC. You can say what the hell you want. I’m going to talk about what Ackman just said about me, not about Herbalife. I’ll talk about Herbalife when I want to, not when you ask me. I’m never going on a show with you again, that’s for damn sure. Let’s start with what I want to say. Ackman is a liar.”

Icahn on Another Ackman Rampage: “I will tell you something. As far as I’m concerned, he wanted to have dinner with me and I laughed. I couldn’t figure out if he was the most sanctimonious guy or the most arrogant… the guy takes inordinate risk…I don’t have an investment with Ackman. I wouldn’t have one if you paid me, if Ackman paid me to do it… I made a huge mistake getting involved with him…After he won [the lawsuit], he planted some article in the New York Times pounding his chest telling the world how great he was. You know, as far as I’m concerned the guy is a major loser.”

New CNBC Revenue Stream?

There hasn’t been this much fireworks since Professor Jeremy Siegel took Bill Gross to task on the Pimco Boss’s assessment that the “cult of equity is dying” last July. In retrospect, that minor tiff was child’s play relative to the Icahn vs. Ackman battle. With CNBC viewership down from pre-crisis levels, the network may strongly consider instituting a new pay-per-view revenue stream dedicated to battles between opposing investment enemies. I will even offer up my services to verbally smack down some of the enemies I’ve written about previously. If my phones don’t ring, then I can always offer up my American Investment Idol concept in which I can play Simon Cowell.

This may or may not be the last round of the Carl Icahn and Bill Ackman fight, but the ultimate bragging rights may depend on the ultimate outcome of Ackman’s Herbalife short. If Icahn makes a tender offer for Herbalife, I will anxiously wait for CNBC’s Scott Wapner to invite Carl back on the show. I can hardly wait…

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in HLF, MBI, NYT, Hallwood Realty, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Cramer Pulls Apple from Romney Tree

Republican Presidential primary candidate Mitt Romney has taken a lot of heat for his lack of conviction on various issues, whether they be on immigration, universal healthcare, or abortion. Jim Cramer, former hedge fund manager and host of TV show Mad Money, has also been known to do a bit of his own John Kerry-esque waffling. One of Cramer’s most recent high profile flip-flops is highflying Apple Inc. (AAPL). If Mitt Romney had his own stock show in his free time like Jim Cramer, there’s a high probability that Romney and Cramer could both agree that they were “for Apple, before they were against it, and now for it again.”

Some might think that picking on Jim Cramer is like clubbing a defenseless seal; wrestling a first grader; or stealing candy from a baby. Suffice it to say, I am not the first person to point out the dangers, inconsistencies, and irresponsible behavior associated with Jim Cramer’s recommendations. Here are some of the highest profile critiques of Jim Cramer in recent years past:

I. Daily Show Destruction

Vodpod videos no longer available.

Daily Show Skewering PART II Daily Show Skewering PART III

II. The Barron’s Bashing

This 2007 Barron’s article not only dissected all of Jim Cramer’s picks over a multi-year period and outlined how much money was lost relative to the major stock market indices, but also a subsequent Barron’s article highlighted research showing a strategy that could yield 25% per month by betting against Cramer’s picks.

This 2007 Barron’s article not only dissected all of Jim Cramer’s picks over a multi-year period and outlined how much money was lost relative to the major stock market indices, but also a subsequent Barron’s article highlighted research showing a strategy that could yield 25% per month by betting against Cramer’s picks.

III. New York Times Expose

Last year, this article highlighted the good, bad, and ugly, but the sentiment noted by famed Yale University endowment fund manager David Swensen echoes the sentiment of many investment professionals:

“Cramer induces his viewers to do things that are bad for them. He’s smart enough to know what he’s doing. ‘Mad Money’ delivers a very dangerous message — that individual investors can beat the market with momentum-driven, high-octane trading strategies. There are individuals who do beat the market, but their number is vanishingly small. Cramer is a master manipulator. He has absolutely no accountability. This is serious business; people’s retirements are at stake.”

Spoiled Apple Turns Sweet Again

Apple stock has historically been a favorite of Jim Cramer. Because why? Well, like many short-term traders, it’s a stock that has been going up! A few short months ago, however, Apple’s stock stopped going up, and was actually going down. Jim Cramer’s long love affair with Apple was on the rocks – this is what he had to say about Apple on November 9th (AAPL price – $395.28):

“Times Have Changed for Apple. I’m hearing about weak tablet sales, about iPhone 4S sales not up to snuff, along with worries about holiday sales for iPods.” In the past Jim would brush these worries aside, but in the past, the visionary Steve Jobs was still breathing. “These days though, every nuance, every little bit of worry about Apple, as we heard today from a brokerage firm talking about lighter tablet sales seaps into my ears, and I actually listen, and I agonize over it – I don’t want to…But I can’t dismiss these minute Apple data points as irrelevant any more. These days it would just be too glib…Apple is no longer a given. We are not going to re-recommend endlessly right here. We are waiting. I think actually better prices are coming. No reason to pull the trigger [buy]. No reason until then [lower prices].”

Oh my, what a difference 90 days makes! Has Steve Jobs been resurrected from the dead? Last I checked, the answer is no. Anxiety of whether new CEO Tim Cook was about to drive Apple off a cliff to obsolescence, like Research in Motion Ltd. (RIMM), has apparently been put on hold. Previous deep-rooted concerns about iPad and iPhone 4S sales from Jim Cramer’s in-depth analysis turned out to be completely off base. As a matter of fact, two months after Cramer went on his anti-Apple rant, the company reported blowout quarterly results of record proportions. Not only did earnings results explode +116% from a year ago (+37% higher than Wall Street forecasts), but iPad unit sales grew by +111% (15.4 million iPads) and iPhone unit sales grew +128% (37.0 million iPhones). To make matters worse, during Cramer’s temporary Apple break-up, he told his followers to buy Google Inc. (GOOG) instead of Apple. Oops…since that short time ago, Apple has only outperformed Google by a massive +28% or so.

Well, no reason to fret now because any worries about a dead Steve jobs, collapsing iPad/iPhone sales, and a RIMM-like train wreck have been quickly forgotten by Cramer over the last few months. Apple gloom has turned to champagne cheers. Here’s what Jim has to say now:

“This stock (Apple) has gripped the imagination like no other I’ve seen in my career. A stock going to $500 in a straight line.”

When Wall Street analysts recently weren’t bullish enough for Cramer (despite 50 “Buy” ratings, 3 “Hold” ratings, 2 “Sell” ratings), he had this to say:

“I want to grab them by the throat and say, ‘Will you give me a break?’ Apple sells at 10 times earnings; the average stock sells at 15 times earnings; Apple is a lot better than the average stock. Don’t you understand this stock is galloping to where it has to go, simply to catch up with the rest of the market? Don’t you see that happening? Don’t you understand that apple has to go higher?!

If these whipsaw stock recommendation reversals are not fast enough for you, no need to worry. Apparently flip-flopping on the overall market only takes 24 hours. Last week, Cramer could hardly control his excitement during his show’s opening, given another up-day in the market. To bolster his bullish case, Cramer proceeded to chastise Wall Street analysts for being so negative. With one rotation of the Earth, the following day, Cramer turned negative and nervous once again as the Dow Jones Industrials index fell 0.69%. Who knows what Cramer’s ever-changing mood will be next, but I can give you a hint – if you look at the daily direction of the Dow, your mood guessing batting average will be higher than Ty Cobb’s career average.

Selective Consumption at the Investment Supermarket

Despite all the criticisms, one should not shed a tear for this multi-mega-millionaire, Harvard grad, and Goldman Sachs Group Inc. alum (GS). Mad Money is highly entertaining for short-term traders, and in upward trending momentum markets, Cramer followers might do OK. Unfortunately, the lucrative, straight-upward market that Cramer made his fortunes in during the 1990s hasn’t been in existence over the last 12 years. For the untrained, investing masses who are looking to preserve and grow their retirement nest eggs, the schizophrenic recommendations that Jim Cramer provides can prove extremely damaging. We have seen this destructive dynamic especially at key inflection points in the market, whether it was at the 2000 peak of the market when his 10-stock “Winners of the New World” portfolio that collapsed by over -90%, or in late 2008/early 2009, near the market bottom, when Cramer told all investors to sell stocks unless you can wait five years.

Jim Cramer is not an evil person and he his very entertaining and sharp individual. I fully admit that I occasionally watch Mad Money for a chuckle and to also gain perspective of the speculative sentiment in the market. Although I would like to see better programming on the network, CNBC is not to be fully blamed. CNBC is like a supermarket that sells both healthy and unhealthy goods. While long-time Investing Caffeine readers know, I have been known to take numerous cavalier economists and strategists to task, many of my investing philosophies and strategies have been built off of long-time, successful investors that CNBC has interviewed or profiled. CNCB guests whom I have written about include, Warren Buffett, Ron Baron, Bill Gross, Ken Heebner, Wilbur Ross, Joel Greenblatt, Laszlo Birinyi, Jimmy Rogers, and others.

While Jim Cramer can be consumed in small doses by professionals and short-term traders, average investors should tread lightly. Investors will be better served by reading the labels of television commentators’ advice, and instead listen to those advisors or managers that have a time horizon consistent with your long-term financial goals.

Jim Cramer has been picked apart by many, but his screaming “Booyahs!,” singing “hallelujah” choirs, and flying bulls, make for compelling television. Although Jim Cramer and I are on the same page as Apple currently (I’ve owned for a long time), I have yet to come to a definitive decision on the 2012 presidential elections. If Cramer changes his view on Apple again in the coming days and weeks, I hope he invites his friend Mitt Romney on as a guest. That way I can kill two birds with one stone, and if one flip-flopper is entertaining to watch, having two should certainly be twice as amusing.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, AAPL, and GOOG but at the time of publishing SCM had no direct position in RIMM, GS, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Buying Bathing Suits in Winter

Buying fire insurance when your neighbor’s house is on fire or flood insurance as your car floats down your driveway can be a very expensive proposition. Stuffing money under the mattress in money market accounts, savings accounts, CDs, and low-yielding bonds can be a very expensive proposition too, as inflation eats away at the value and the auspice of higher interest rates looms. However, buying things when they are out of favor, like bathing suits in the winter, is an opportunistic way of cashing in on bargains when others are uninterested.

Speaking of uninterested, CNBC recently conducted a survey regarding the attractiveness of stock investing, and according to the participants, there has never been a worst time to invest (as long as the survey has been conducted). Despite consumers planning to spend +22% more on gifts this year, the national mood has not been worse since the financial crisis began in earnest during 2008. Specifically, as it pertains to stocks, 53% of Americans believe it is a bad time to invest in the stock market (SEE VIDEO BELOW).

Vodpod videos no longer available.

CLICK TO TO ENLARGE

Not a very happy picture. The study filtered through 4,600,000,000 expressions posted by 63 million unique Twitter social media users and graphically displayed people’s happiness (or lack thereof).

Endless Number of Concerns

There is no shortage of concerns, whether one worries about the collapse of Europe, declining home values, or an uncertain employment picture. But is now the time to give up and follow the scared herd? The best time to follow the herd is never. As the old saying goes, “the herd is led to the slaughterhouse.” Investing is game like chess where one has to anticipate and be forward looking multiple moves in advance – not reacting to every shift and move of your competitor.

Certainly, investing in stocks may not be appropriate for those investors needing access to liquid funds over the next year or two. Also, retirees needing steady income may not be in a position to handle the volatility of equities. However, for many millions of investors who are planning for the next 5, 10, or 20+ years, what happens over the next few months or next few years in Italy, Greece, or Spain is likely to be meaningless. As far as our economy goes, the U.S. averages about two recessions a decade, and has done quite well over the long-run despite that fact – thank you very much. Investors need to understand that investing is a marathon, and not a sprint.

December may not be the best time to head the beach in your swim trunks, bikini, or thong, but winter is now upon us and incredible deals abound (see deals for women & men). It may also be windy outside with frigid conditions in the water for stock investors too, but with winter beginning this week, the amount of bargains for long-term investors continue to heat up no matter how chilly the sentiment remains.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in Twitter, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Insider Trading Interview with Sidoxia Capital Management

I am recovering from one too many servings of turkey and pumpkin pie, so perhaps you can enjoy an interview I conducted with CNBC’s Erin Burnett on the subject of insider trading earlier this week (Minute 2:00).

Once I awake from the food-induced coma, I promise to return with a more typical article on Investing Caffeine’s site.

I hope everyone had a wonderful holiday…

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

“De-Risking” – It’s All Greek to Me

Source: Photobucket

In the classic comedy Animal House John Belushi (who played the character Bluto) gave new meaning to the Greek toga party (who cares if the Romans actually invented the garment?). Belushi also added some flare to Sam Cooke’s timeless song, Wonderful World:

“Don’t know much about history

Don’t know much biology

Don’t know much about the science book

Don’t know much about the French I took.”

Another line should have been added: “Don’t know much about Wall Street jargon.”

“Derisking” – New Wall Street Word Du Jour

Wading through and keeping up with the ever expanding dictionary of Wall Street lingo and acronyms can be a difficult task – much like deciphering the Greek writings of Plato, the famous ancient philosopher.

A recent term repeated constantly by CNBC commentators and hedge fund managers at the annual SALT (SkyBridge Alternatives) conference in Las Vegas, Nevada deserves some more attention…“derisking.” Elegant, simple, chic, and yes, pure B.S. Why not use “mis-risking,” “un-risking,” “dis-risking?” I suppose when charging people 2 and 20 (a 2% management fee plus 20% of profits above a hurdle), one must try to make the most prosaic terms and expressions sound mysterious and dazzling.

Asking one hedge fund manager after another, CNBC commentator David Faber continually asked managers at the May conference what investing strategies were being employed. Faber asked Marc Lasry, CEO and Co-Founder of Avenue Capital Group, the following:

“I have spoken to number of other large hedge fund managers this morning. Derisking, that’s what they are all talking about Marc. So, given that, are you derisking at all?”

Translation: “The market is going down, so are you following all the other lemmings and becoming more conservative because of the panicked-induced headlines we’re shoveling 24/7?”

Glenn Dubin, Co-Founder and CEO of Highbridge Capital Management, a hedge fund company owned by JP Morgan (JPM) got in the “derisking” mood too: “At this point…we are seeing massive de-risking.”

At the time of the SALT conference, European economic concerns were top of mind for all the fast-money traders, as fears of a credit contagion spreading from Greece to larger countries like Italy and Spain felt more palpable to many. Some nine weeks later, the European bank stress tests have been completed, some overseas economic indicators have come in better than anticipated (i.e., U.K. GDP, German business confidence, exports), and some European markets are up about +10% from the “derisking” phase. So, I wonder what those same hedge funds and traders are doing now?

Perhaps they are “rerisking?” I just made that one up out of thin air, but if I hear “rerisking” on CNBC or see it in the Wall Street Journal, I demand a credit in the Merriam-Webster dictionary, or a citation in Wikipedia at a minimum.

The “derisking” wave did not stop at the SALT conference, but remains alive and well today. In fact, a conference has been created in its honor: The 3rd Annual De-Risking Strategies Summit for Pension Funds, Foundations, and Endowments on October 25 – 27, 2010 in New York.

Obviously, this is just one of many terms, acronyms, and euphemisms that the Wall Street machine is constantly churning out. If “derisking” doesn’t float your boat, then why not try on a “swaption” and “straddle” or “contango” and “crawling peg?”

If the never-ending list of Wall Street jargon is weighing you down and a financial professional is speaking Greek to you with confusing financial terminology, then do yourself a favor and slap that person into silence. More often than not, these financial concepts can be explained to a fifth grader (or Bluto). Unfortunately, a convoluted combination of jargon and acronyms is often used in an attempt to impress the listener. The result is usually confusion and a blank stare.

If you are frustrated with learning the language of Wall Street, you are not alone. I recommend you “derisk” your education by adding Greek 101 to your coursework. If you are going to be confused, you might as well do it with a gyro and some Ouzo in hand.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in JPM or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Sukuk: Islamic Loophole for Dubai Debt Debacle

Islamic followers can be capitalists too. Although oil prices (currently around $77 per barrel) have fallen from the peak near $150 per barrel in 2008, oil rich nations have gotten creative in how they raise debt-like financing. Critical to fueling the speculative expansion in some oil rich areas has been the growth in sukuk bonds, which have been created as a function of an exploited loophole embedded in Islamic finance principles.

U.S. Does Not Have Monopoly on Debt Driven Greed

The pricked debt bubble that spanned a range of entities, from Icelandic banks to Donald Trump’s empire (read more), has now spread to Dubai commercial real estate. At the center of the storm is Dubai World, a quasi-government owned conglomerate of Dubai, which is in the process of negotiating a $26 billion debt restructuring with the government and sukuk bondholders. The overleveraged Dubai market ($80 billion in total debt) is home to the tallest building in the world, largest man-made islands, and a ski-resort based in the desert – all projects built with the help of debt in the face of collapsing real estate prices. Critical to Dubai World’s debt restructuring is a $3.5 billion sukuk bond issued by its commercial real estate subsidiary Nakheel Development (“Nakheel”). So what exactly is a sukuk (plural of sakk)?

Investopedia lists the following definition for sukuk:

“An Islamic financial certificate, similar to a bond in Western finance, that complies with Sharia, Islamic religious law. Because the traditional Western interest paying bond structure is not permissible, the issuer of a sukuk sells an investor group the certificate, who then rents it back to the issuer for a predetermined rental fee. The issuer also makes a contractual promise to buy back the bonds at a future date at par value.”

Sukuk “No-No”s

The generation of money on top of money – interest payments or what’s called “Riba” – is strictly forbidden by Shari’ah law. As a result, issuers must issue and repurchase sukuk at par (original value), not at a discount or a premium. Shari’ah law encompasses more than Islamic law, it also covers the amorphous spiritual and moral obligations demanded from the religious practitioners. In order to ensure compliance with Islamic principles, many financial institutions and funds typically have a Shari’ah Board monitoring the details of the sukuk. Shari’ah law is very consistent with the teachings in the Quran (the Western version of the Bible). Mixing finance and religion may seem strange on the surface, but I guess if we use world history as a proxy, we shouldn’t be surprised that money and Muhammad somehow find a way to coexist.

Click Here to View CNBC Interview on Sukuk Bonds

Sukuk Structure & Market

The core Islamic finance principles underpinning the sukuk market have been around for more than 1,500 years, but the actual sukuk market was actually introduced in Malaysia around 1990. Since then, the market has been on a continual uptrend. What makes this $1 trillion Islamic debt market (HSBC estimate) even fuzzier is the scores of sukuk structures (See Ijara Sukuk chart below – very similar to a sale-leaseback arrangement), and the diverse geographic issuer/investor base. For example, greater than 60% of Nakheel’s investors are based outside the Middle East (a large portion in Malaysia). Making matters as clear as mud, each geographic region and structure has its own interpretation of legal rights and Shari’ah law. Layer on issues such as derivatives, bankruptcy rights, and penalty fees and you end up with only more complexity. What’s more, many of these sukuk bonds involve Special Purpose Vehicles (SPVs) – made famous by the off-balance sheet variety used by Enron Corp. – in order to get around the Islamic issuance loopholes.

Source: Moody's Investor Service

Sukuk Liquidity

The illiquidity of sukuk market hasn’t made resolving the Dubai debt restructuring any easier. The sukuk market doesn’t come close to matching the liquidity of traditional corporate and sovereign debt markets. Little trading is done in secondary markets because most investors in sukuk bonds follow a buy and hold strategy. The lion’s share of trading in this immature market gets completed through inter-institution, over-the-counter transactions. A recent $500 million sukuk deal issued by General Electric (GE) last month has only raised awareness for the financing structure (pre-Nakheel restructuring). As oil rich states strive to diversify their economic bases, I would expect more deals to get done, in spite of the recent Dubai mess. How severe the recent Dubai sukuk black eye will be depends on how Nakheel, the United Arab Emirates (UAE), Abu Dhabi, bondholders, and other constituents restructure the pending sukuk obligations by the December 14th deadline.

The recent debt restructuring talks in Dubai highlight the complexity of this relatively new Islamic financing structure. With very few sukuk bankruptcy cases in existence, the structures remain largely untested and uncertain. How the Dubai debt debacle ultimately gets resolved will have a significant impact on this nascent, but rapidly growing market. Until the sukuk restructuring is settled, Dubai may just need to put the construction of that next man-made island on hold.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Information and data from Moody’s Investor Service (Shari’ah and Sukuk: A Moody’s Primer 5/31/2006), CNBC interview 12/2/09, Financial Times 12/1/09, and other articles. Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct positions in GE. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Meredith Whitney’s Cloudy Crystal Ball

Meredith Whitney, prominent banking analyst at her self-named advisory group, should have worn a bib to protect her from the adoring drool supplied by Maria Bartiromo in a recent CNBC interview. Ms. Whitney has quickly become a banking rock star during this “Great Recession” period. She was right at a critical juncture, and as a result she was thrust into the limelight. Much like Abby Joseph Cohen, the perma-bull Goldman Sachs strategist who gained notoriety in the late 1990s, Whitney (the perma-banking bear) will continue having difficulty living up to the lofty expectations demanded of her.

Despite the accolades, Whitney’s crystal ball has gotten cloudy in 2009. I suppose accuracy is not very important, judging by her bottom-half 2007 ranking (year of her major Citigroup call) in recommendation performance and 48%-ile ranking in the first half of 2008. Analysts, much like reporters, can avoid looking dumb by reporting the news du jour and by following the herd. Whitney has followed this formula with her continuous bearishness on the financial sector, excluding a brief but late upgrade of Goldman Sachs in July. Not only was her analysis tardy (Goldman’s stock tripled from the 2009 bottom), but her call has also underperformed the S&P 500 index since the upgrade.

Incoherent Inconsistencies

Like a bobbing and weaving wrestler (her husband John Layfield is a retired staged professional wrestler from the WWE), Whitney tries to concoct a completely mind-boggling narrative to explain her forecasts this year in the CNBC interview with Maria Bartiromo:

11/18/09 (XLF Price $14.60): “For the year, I have been at least ‘cover your shorts, go long.’ I haven’t been this bearish in a year.” (See Maria Bartiromo Interview)

Hmm, really? Are you kidding me? Wait a second…is this the same “go long” Meredith Whitney that expressed the following?

3/17/09: (XLF: 8.55 then, 14.60 now +71% ex-dividends): “These big banks are sitting on loans that were underwritten with bad math, and the stocks are going to go down…these stocks are uninvestable.”

(Fast forward to minute 8:20 for quote above)

2/4/09 (XLF: 8.97 then, 14.60 now +63% ex-dividends): “Investors should not even consider owning banks on an equity basis” (Click here and fast forward to minute 8:10 for quote).

The schizophrenic accounting of her postures are all the more confusing given her stance that the sector was “fairly valued” in October, according to the CNBC Bartiromo interview.

Don’t get me wrong, she made an incredible bearish call on Citigroup in the fall of 2007 and was expecting blood in the streets until a massive rebound in 2009 surprised her. Investors need to be wary of prognosticators that get thrust into the limelight (see Peter Schiff article) for a single prediction. The law of large numbers virtually guarantees a new breed of extreme forecasters will be rotated into the spotlight any time there is a major shift in the market direction. I choose to follow the footsteps of Warren Buffett and stay away from the game of market timing and market forecasts. I believe James Grant from the Interest Rate Observer states it best:

“The very best investors don’t even try to forecast the future. Rather, they seize such opportunities as the present affords them.”

Meredith Whitney may be a bright banking analyst and perhaps she’ll ultimately be proven right regarding the downward banking stock price trajectories, but like all bold forecasters she must live by the crystal ball, and die by the crystal ball.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and its clients own certain exchange traded funds (including VFH), but currently have no direct positions in C, GS, or XLF. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Ross Warns of Commercial Shoe Drop

The next shoe to drop in commercial real estate has been highly telegraphed for some time now. Wilbur Ross, restructuring specialist and founder of WL Ross & Co, has a long track record of success and he weighs in with his views regarding the impending crash in commercial real estate through several recent interviews.

What exactly is Mr. Ross worried about? He sees a correlation of what happened in the residential mortgage markets to what we are now beginning to see in the commercial real estate markets:

Fast forward to minute 4:20 to hear real estate commentary

Click Hear to See CNBC Interview with Wilbur Ross

“I have felt for quite some time that the same reckless lending that characterized the subprime mortgage business in residential was also characterizing what had gone on in commercial real estate in the mid-2000s. You had properties being bought at a 3% cash-on-cash yield. You had properties being financed at on such an aggressive basis that the lenders had to give them an advance – several years worth of interest – because there wasn’t enough cash coming from the properties even to pay the interest. And the theory was that rent rolls would go up, occupancy would go up, and eventually the property would grow its way into paying interest. Well now that clock is ticking – rents haven’t gone up, they’ve gone down; occupancy hasn’t gone up, it has gone down; and capitalization rates that people require from properties have gone up. So everything is going in the wrong direction, and I think we are going to see quite a lot of tragedies in that sector. “

Although Mr. Ross unequivocally sees a “huge crash in commercial real estate,” he puts his pessimistic views on impending destruction into perspective (read more about pessimism). The size of the commercial real estate market is quite a bit smaller than residential:

“The total of commercial mortgages is only about $3.5 trillion versus $11 trillion for residential mortgages.”

The commercial crash is already happening and forecasts for commercial property are expected to drop to the lowest levels in nearly two decades, according to according to property research firm Real Capital Analytics Inc. The sign of the times is evident by the recent Chapter 11 bankruptcy filing by Capmark Financial Group Inc., a company that originated about $60 billion in commercial real estate loans in 2006 and 2007 (Bloomberg). Anecdotally, at a professional event I just attended in southern California, I bumped into a real estate broker who informed me on the state of the market. The property across the street from the event location had a 50% vacancy rate and a glut of hedge funds were bidding on the building for 50% of its replacement value…ouch!

Reis Inc., a property research firm also notes:

“U.S. office vacancies hit a five-year high of almost 17 percent in the third quarter, while shopping center vacancies climbed to their highest since 1992.”

And from a fiscal response and taxpayer liability standpoint Ross is less worried because he thinks Washington, for the most part, will be watching the train wreck from the sidelines, with a bag of popcorn in hand:

“I don’t think the federal government’s going to do much to help the commercial building side because individual homeowners vote but buildings don’t vote.”

As Wilbur Ross has definitively communicated, he’s confident the commercial real estate mortgage market will cause the next surprising shoe to drop. Fortunately though, he feels the crash will be manageable. With all these shoes dropping, maybe I can find a new pair of shoes to wear?

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}