Posts tagged ‘central banks’

The New Abnormal: Living with Negative Rates

Pimco, the $1.5 trillion fixed-income manager located a stone’s throw distance from my office in Newport Beach, famously (or infamously) coined the phrase, “New Normal”. As former Pimco CEO (Mohamed El-Erian) described years ago, around the time of the Great Recession, the New Normal “reflects a growing realization that some of the recent abrupt changes to markets, households, institutions, and government policies are unlikely to be reversed in the next few years. Global growth will be subdued for a while and unemployment high.”

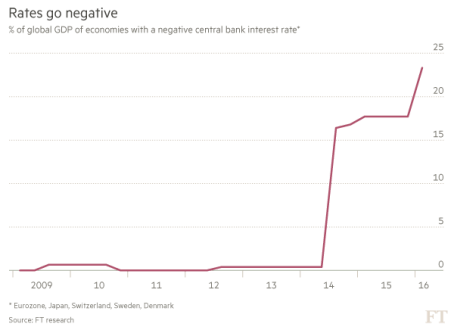

As it turns out, El-Erian was completely wrong in some respects and shrewdly prescient in others. For instance, although the job recovery has been one of the slowest in a generation, 14.5 million private sector jobs have been added since 2010, and the unemployment rate has been more than halved from 10% in early 2009, to below 5% today. However, the pace of global growth has been relatively weak since the 2008-2009 financial crisis, which has forced central banks all over the world to lower interest rates in hope of stimulating growth. Monetary policies around the globe have been cut so much that almost 25% of global GDP is tied to countries with negative interest rates (see chart below).

Source: Financial Times

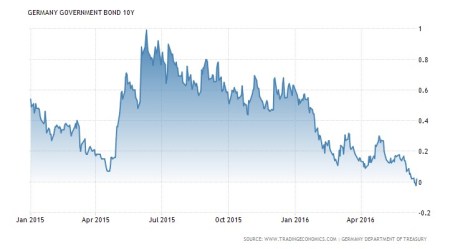

The European central banks started the sub-zero trend in 2014, and the Bank of Japan recently joined the central banks of Denmark, Sweden and Switzerland in negative territory. The negative short-term rate virus has spread further to long-term bonds as well, as evidenced by the 10-Year German Bund (sovereign bond) yield, which crossed into negative territory last week (see chart below).

Source: TradingEconomics.com

The New Abnormal

The unprecedented post-crisis move to a 0% Fed Funds rate target, along with the implementation of Quantitative Easing (QE) by former Federal Reserve Chairman Ben Bernanke, was already pushing the envelope of “normal” stimulative monetary policy. Nevertheless, central banks pushing rates to a negative threshold takes the whole stimulus discussion to another level because investors are guaranteed to lose money if they hold these bonds until maturity.

As we enter this new submerged rate phase, this activity can only be described as abnormal…not normal. Preserving money at a 0% level and losing value to inflation (i.e., essentially stuffing money under the proverbial mattress) is a bitter enough pill to swallow. Paying somebody to lend them money gives “insanity” a good name.

The stimulative objectives of negative interest policies established by central bankers may be purely intentioned, however there can be plenty of unintentional consequences. For starters, negative rates can produce too much of a good thing, in the form of excess borrowing or leverage. In addition, retirees and savers across a broad spectrum of ages are getting crushed by the paltry rates, and bank profit margins (net interest margins) are getting squeezed to boot.

Another unintended consequence of negative rate policies could be a polar opposite outcome to the envisioned stimulative design. Scott Mather, a co-portfolio manager of the $86 billion PIMCO Total Return Fund (PTTRX) is making the case that these policies could be creating more economic contractionary effects than invigorating expansion. More specifically, Mather notes, “It seems that financial markets increasingly view these experimental moves as desperate and consequently damaging to financial and economic stability.”

Eventually, the cheap money deliberately created by central banks will result in a glut of risk-taking and defaults. However, despite all the cries from hawks protesting money printing policies, cautious bank lending behavior coupled with regulatory handcuffs have yet to create widespread debt bubbles. Certainly, oceans of cheap money can create pockets of problems, as I have identified and discussed in the private equity market (see also Dying Unicorns), but supply and demand rule the day at some point.

In the end, as I have repeatedly documented, money goes where it is treated best. Realizing guaranteed losses while trapped in negative rate bonds is no way to treat your investment portfolio over the long-run. In the short-run, the safety and stability of short duration bonds may sound appealing, but ultimately rational and efficient behavior prevails. Why settle for 0% or negative rates when yields of 2%, 4%, and 6% can be found in plenty of other responsible investment alternatives?

Arguably, in this post financial crisis world we live in, we have transitioned from the New Normal to a New Abnormal environment of negative rates. Pundits and prognosticators will continue spewing fear-filled cautionary advice, but experienced, long-term investors will continue taking advantage of these risk averse markets by investing in a quality, diversified portfolio of superior yielding investments. For now, there are plenty of opportunities to choose from, until the next phase of this economic cycle… when the New Abnormal transitions to the New Normalized.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds , but at the time of publishing had no direct position in PTTRX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Michael Jordan and Market Statistics

Basketball is in the air as the NBA playoffs are once again upon us. While growing up in high school, Michael Jordan was my basketball idol, and he dominated the sport globally at the highest level. I was a huge fanatic. Besides continually admiring my MJ poster-covered walls, I even customized my own limited edition Air Jordan basketball shoes by applying high school colors to them with model paint – I would not recommend this fashion experiment to others.

Eventually the laws of age, physics, and gravity took over, as Jordan slowly deteriorated physically into retirement. On an infinitesimally smaller level, I also experienced a similar effect during my 30s when playing in an old man’s recreational basketball league. Day-by-day, month-by-month, and year-by-year, I too got older and slower (tough to believe that’s possible) as I watched all the 20-somethings run circles around me – not to mention my playing time was slashed dramatically. Needless to say, I too was forced into retirement like Michael Jordan, but nobody retired my number, and I still have not been inducted into the Hall of Fame.

“Air Wade” Before Retirement: No Photoshop in 1988, just an optical illusion created by an 8-foot rim.

Financial markets are subject to similar laws of science (economics) too. The stock market and the economy get old and tired just like athletes, as evidenced by the cyclical nature of bear markets and recessions. Statistics are a beautiful thing when it comes to sports. Over the long run, numbers don’t lie about the performance of an athlete, just like statistics over the long run don’t lie about the financial markets. When points per game, shooting percentage, rebounds, assists, minutes played, and other measurements are all consistently moving south, then it’s safe to say fundamentals are weakening.

I’ve stated it many times in the past, and I’ll state it again, these are the most important factors to consider when contemplating the level and direction of the stock market (see also Don’t Be a Fool, Follow the Stool).

- Profits

- Interest Rates

- Valuations

- Sentiment

While the absolute levels of these indicators are important, the trend or direction of each factor is also very relevant. Let’s review these factors a little more closely.

- Profits: Profits and cash flows, generally speaking, are the lifeblood behind any investment and currently corporate profits are near record levels. When it comes to the S&P 500, the index is currently expected to generate a 2016 profit of $117.47. Considering a recent price closing of 2,092 on the index, this translates into a price-earnings ratio (P/E) of approximately 17.8x or a 5.6% earnings yield. This earnings yield can be compared to the 1.9% yield earned on the 10-Year Treasury Note, which is even lower than the 2.1% dividend yield on the S&P 500 (a rare historical occurrence). If history repeats itself, the 5.6% earnings yield on stocks should double to more than 10% over the next decade, however the yield on 10-year Treasuries stays flat at 1.9% over the next 10 years. The strong dollar and the implosion of the energy sector has put a lid on corporate profits over the last year, but emerging signs are beginning to show these trends reversing. Stabilizing profits near record levels should be a positive contributor to stocks, all else equal.

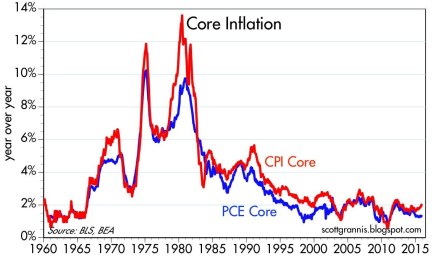

- Interest Rates: Pundits have been pointing to central banks as the sole reason for low/negative interest rates globally (see chart below). NEWS FLASH: Central banks have been increasing and decreasing interest rates for decades, but that hasn’t stopped the nearly unabated 36-year decline in interest rates and inflation (see chart below). As I described in previous articles (see Why 0% Rates?), technology, globalization, and the rise of emerging markets is having a much larger impact on interest rates/inflation than monetary policies. If central banks are so powerful, then why after eight years of loose global monetary policies hasn’t inflation accelerated yet? Regardless, all else equal, these historically low interest rates are horrible for savers, but wonderful for equity investors and borrowers.

Source: Calafia Beach Pundit

- Valuations: The price you pay for an investment is one of the, if not the, most important factors to consider. I touched upon valuations earlier when discussing profits, and based on history, there is plenty of evidence to support the position that valuations are near historic averages. Shiller CAPE bears have been erroneously screaming bloody murder over the last seven years as prices have tripled (see Shiller CAPE smells like BS). A more balanced consideration of valuation takes into account the record low interest rates/inflation (see The Rule of 20).

- Sentiment: There are an endless number of indicators measuring investor optimism vs. pessimism. Generally, most experienced investors understand these statistics operate as valuable contrarian indicators. In other words, as Warren Buffett says, it is best to “buy fear, and sell greed.” While I like to track anecdotal indicators of sentiment like magazine covers, I am a firm believer that actions speak louder than words. If you consider the post-crisis panic of dollars flowing into low yielding bonds – greater than $1 trillion more than stocks (see Chicken vs. Beef ) you will understand the fear and skepticism remaining in investors minds. The time to flee stocks is when everyone falls in love with them.

Readers of Michael Lewis’s book Moneyball understand the importance statistics can play in winning sports. Michael Jordan may not have been a statistician like Billy Beane, because he spent his professional career setting statistical records, not analyzing them. Unfortunately, my basketball career never led me to the NBA or Hall of Fame, but I still hope to continue winning in the financial markets by objectively following the all-important factors of profits, interest rates, valuations, and sentiment.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Bond-Choking Central Banks Expand Investment Menu

Central banks around the globe are choking on low-yielding bonds, and as result are now expanding their investment menu beyond Treasuries into equities. Expansionary monetary policies purchasing short-term, low-rate bonds means that central banks have been gobbling up securities on their balance sheets that are earning next to nothing. To counteract the bond-induced indigestion of the central banks, many of them are considering increasing their equity purchasing strategies. How can you blame them? With the 10-year U.S. Treasury notes yielding 1.66%; 10-year German bonds eking out 1.21%; and 10-year Japanese Government Bonds (JGBs) paying a paltry 0.59%, it’s no wonder central banks are looking for better alternatives.

More specifically, the Bank of Japan (BOJ) is planning to pump $1.4 trillion into its economy over the next two years to encourage some inflation through open-ended asset purchases. Earlier this month, the BOJ said it has a goal of more than doubling equity related exchange traded funds (ETFs) by the end of 2014. According to Business Insider, the BOJ is currently holding $14.1 billion in equity ETFs with an objective to reach $35.3 billion in 2014.

I can only imagine how stock market bears feel about this developing trend when they have already blamed central banks’ quantitative easing initiatives as the artificial support mechanism for stock prices (see also The Central Bank Dog Ate my Homework).

While expanded equity purchases could break the backs of bond bulls and stock naysayers, some smart people agree that this strategy makes sense. Take Jim O’Neill, the chairman of Goldman Sachs Asset Management, who is retiring next week. Here’s what he has to say about expanded central bank stock purchases:

“Frankly, it makes a huge amount of sense in a world of floating exchange rates and such incredible opportunity, why should central banks keep so much money in very short term, liquid things when they’re not going to ever need it? To help their future returns for their citizens, why would they not invest in equity?”

How big is this shift towards equities? The Royal Bank of Scotland conducted a survey of 60 central banks that have about $6.7 trillion in reserves. There were 13% of the central banks already invested in equities, and almost 25% of them said they are or will be invested in equities within the next five years.

While I may agree that stocks generally are a more attractive asset class than bubblicious bonds right now, I may draw the line once the Fed starts buying houses, gasoline, and groceries for all Americans. Until then, dividend yields remain higher than Treasury yields, and the earnings yields (earnings/price) on stocks will remain more attractive than bond yields. Once stocks gain more in price and/or bonds sell off significantly, it will be a more appropriate time to reassess the investment opportunity set. A further stock rise or bond selloff are both possible scenarios, but until then, central banks will continue to look to place its money where it is treated best.

The central bank menu has been largely limited to low-yielding, overpriced government bonds, but the appetite for new menu items has heightened. Stocks may be an enticing new option for central banks, but let’s hope they delay buying houses, gasoline, and groceries.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Rogers: Fed Following in Path of Dodo

Jimmy Rogers, the bow-tie boss of Rogers Holdings and past co-founder of the successful Quantum Fund with George Soros, is no stranger to making outrageous predictions. His latest prophetic assessment is the Federal Reserve Bank is on the path of the Dodo bird to extinction:

“Don’t worry – the Fed is going to abolish itself. Between Bernanke and Greenspan, they’ve made so many mistakes that within the next few years the Fed will disappear.”

Given the shock and awe that transpired from the Lehman Brothers collapse, I can only wonder how investors might react to this scenario….hmmm. If this doozy of an outlandish call catches you off guard, please don’t be surprised – Rogers is not shy about sharing additional ones (Read other IC article on Rogers). For example, just six months ago Rogers said the Dow Jones could collapse to 5,000 (currently around 10,472) or skyrocket to 30,000, but “of course it would be in worthless money.” Oddly, the printing presses that Rogers keeps talking about have actually produced deflation (-0.2%) in the most recently reported numbers, not the same 79,600,000,000% inflation from Zimbabwe (Cato Institute), he expects.

I suppose Rogers will either point to a data conspiracy, or use the “just you wait” rebuttal. I eagerly await, with bated breath, the ultimate outcome.

Is U.S. Fed Alone?

If the U.S. Federal Reserve system is indeed about to disappear after over nine decades of operations, does that mean Rogers advocates shutting all of the other 166 global reserve banks listed by the Bank for International Settlement? Should the 3 ½ century old Swedish Riksbank (origin in 1668) and the Bank of England (1694) central banks also be terminated? Or does the U.S. Federal Reserve Bank have a monopoly on incompetence and/or corruption?

Sidoxia’s Report Card on Fed

I must admit, I believe we would likely be in a much better situation than we are today if the Federal Reserve board let Adam Smith’s “invisible hand” self adjust short-term interest rates. Rather, we drank from the spiked punch bowls filled with low interest rates for extended periods of time. The Federal Reserve gets too much attention/credit for the impact of its decisions. There is a much larger pool of global investors that are buying/selling Treasury securities daily, across a wide range of maturities along the yield curve. I think these market participants have a much larger impact on prices paid for new capital, relative to the central bank’s decision of cutting or raising the Federal funds rate a ¼ point.

Although I believe the Fed gets too much attention for its monetary policies, I think Bernanke and the Fed get too little credit for the global Armageddon they helped avoid. I agree with Warren Buffett that Bernanke acted “very promptly, very decisively, very big” in helping us avert a second depression while we were on the “brink of going into the abyss.”

Beyond the monetary policy of fractional rate setting, the Fed also has essential other functions:

- Supervise and regulate banking institutions.

- Maintain stability of the financial system and control systemic risk of financial markets.

- Act as a liaison with depository institutions, the U.S. government, and foreign institutions.

- Play a major role in operating the country’s payments system.

I will go out on a limb and say these functions play an important role, and the Fed has a good chance of being around for the 2012 London Olympic Games (despite Jimmy Rogers’ prediction).

Sidoxia’s Report Card on Rogers

As I have pointed out in the past, I do not necessarily disagree (directionally) with the main points of his arguments:

- Is inflation a risk? Yes.

- Will printing excessive money lower the value of our dollar? Yes.

- Is auditing the Federal Reserve Bank a bad idea? No.

My beef with Rogers is merely in the magnitude, bravado, and overconfidence with which he makes these outrageous forecasts. Furthermore, the U.S. actions do not happen in a vacuum. Although everything is not cheery at home, many other international rivals are in worse shape than we are.

From a media ratings and entertainment standpoint, Rogers does not disappoint. His amusing and outlandish predictions will keep the public coming back for more. Since according to Rogers, Bernanke will have no job at the Fed in a few years, I look forward to their joint appearance on CNBC. Perhaps they could discuss collaboration on a new book – Extinction: Lessons Learned from the Fed and Dodo Bird.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (VFH) at the time of publishing, but had no direct ownership in BRKA/B. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}