Posts tagged ‘CDS’

Mideast War an Investor Bore as Markets Soar

If I told you at the beginning of the year that the U.S. would bomb key nuclear sites in Iran, would you have guessed that Middle East stability would follow—and that global financial markets would soar to record highs? Personally, I wouldn’t have bet on that outcome. But that’s exactly what happened last month. While geopolitical dynamics remain fluid, markets shrugged off the chaos. The S&P 500 rallied +5.0%, the Dow Jones Industrial Average climbed +4.3%, and the NASDAQ catapulted +6.6%, powered largely by artificial intelligence stocks like NVIDIA Corp., which surged +16.9% for the month to a market value of $3.9 trillion (more on AI below). This is an important reminder that trading off of news headlines is a fool’s errand.

Economy Resilient Despite Tariffs and Geopolitical Turmoil

Source: Calafia Beach Pundit

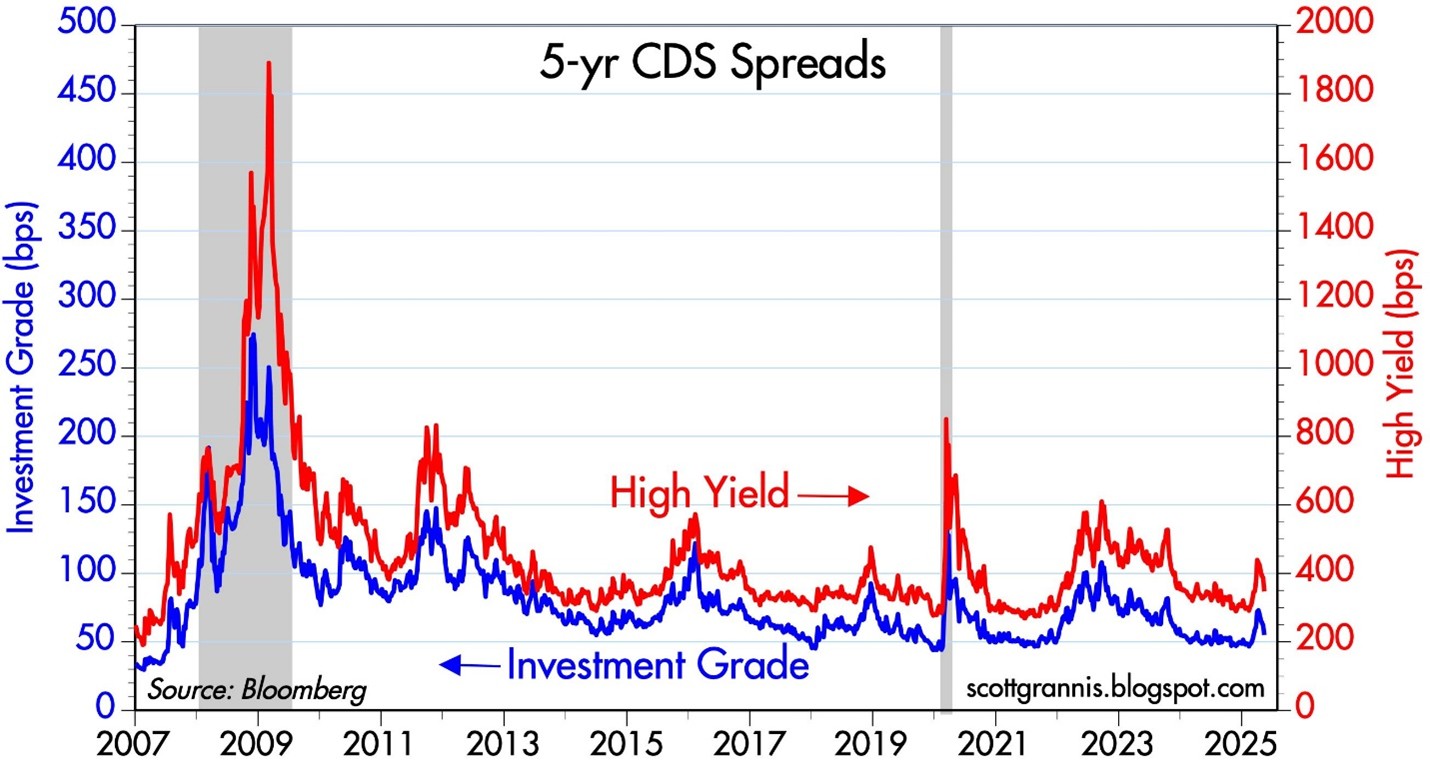

Credit Default Swaps (CDS) act as insurance contracts that protect investors against corporate debt defaults. During financial stress—like the 2008 crisis or the COVID crash in 2020—CDS prices surge as investors seek protection. Today, however, CDS prices are falling across both high-yield (junk bonds) and investment-grade (Blue Chip) debt. As seen in the chart above, the cost to insure corporate bonds has declined steadily over the past two years. This signals bond investors aren’t worried about a recession or a wave of defaults, despite tariff policy uncertainty, geopolitical risk, and modest GDP growth.

Inflation Tame as Tariffs Loom

President Trump has repeatedly criticized Fed Chair Jerome Powell for not cutting interest rates, calling him everything from a “dummy” to a “major loser” and a “stupid person” to a “numbskull”. While the name-calling is colorful, the economic pressure is real: U.S. GDP contracted -0.5% in Q1 2025. Powell, however, wants to see the full impact of upcoming tariffs before making a move. . A new tariff deadline looms on July 9th, and the market is anxiously awaiting clarity. But even if tariffs are implemented, many economists believe the inflationary impact will be temporary—what’s known as a one-time price shock.

Source: Calafia Beach Pundit

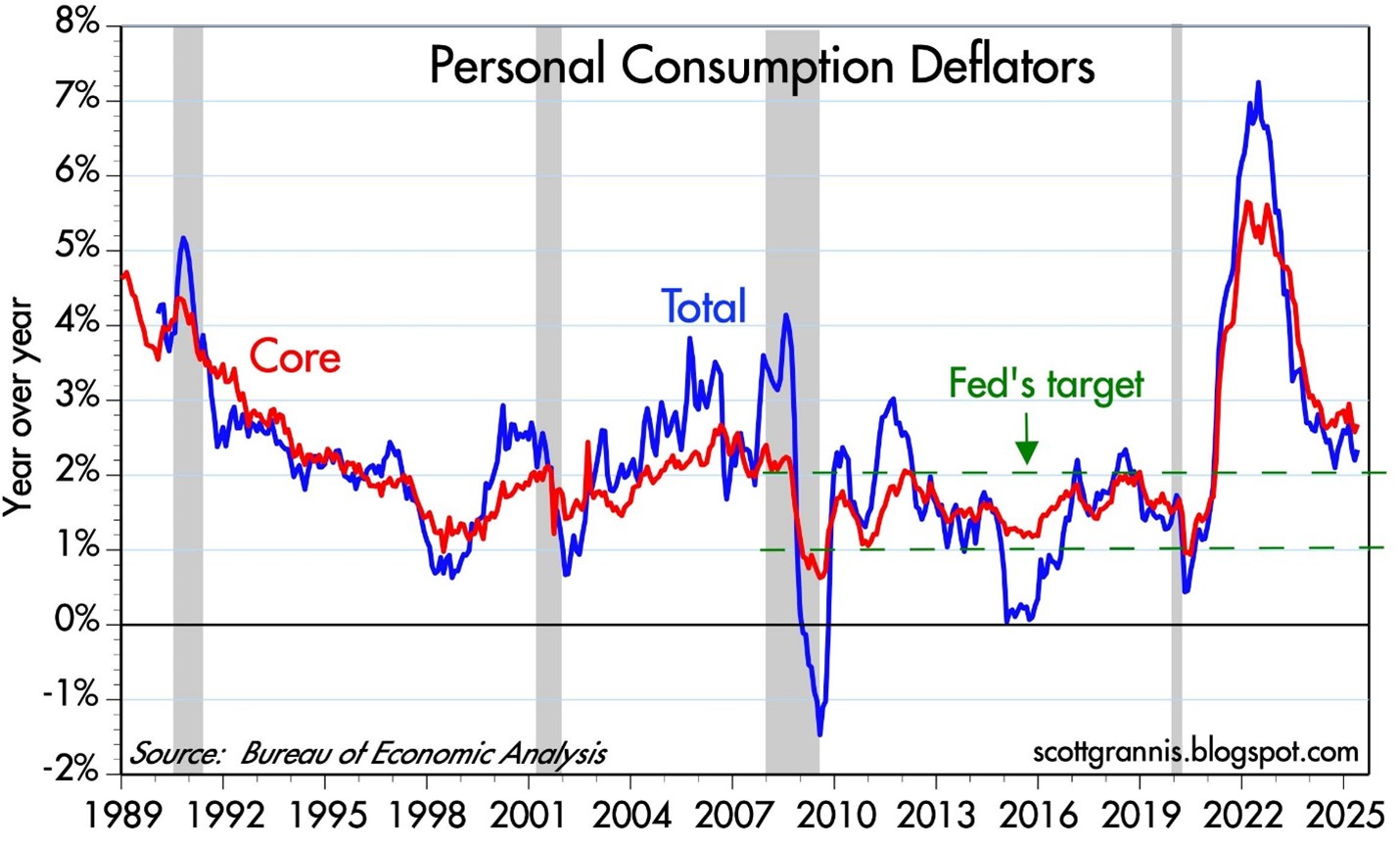

The Fed’s preferred inflation gauge—the Personal Consumption Expenditure (PCE) index—has been easing and is now near the 2% target (see chart above). With inflation cooling, Trump’s case for rate cuts gains credibility. Still, the Fed appears in no rush. It will take time to understand the lasting effects of the tariff rollout.

AI Wave Fueling Markets

For a generation, the semiconductor revolution has quietly powered innovation, guided by Moore’s Law—the principle that chip performance doubles roughly every two years (see my article The Traitorous 8). Sixty years after Gordon Moore wrote his seminal article, “Cramming More Components onto Integrated Circuits”, the power of software is catching up. NVIDIA’s Grace Blackwell GB200 chip contains an astronomical 208 billion transistors, supercharging AI software models like ChatGPT.

The AI revolution is fueling trillions in global investment and rapidly transforming industries – from data centers and self-driving cars to robotics and drug discovery. It’s important to realize that this AI arms race is not just occurring in the United States. AI investment spending extends way beyond Silicon Valley to countries like Saudi Arabia, Singapore, and China.

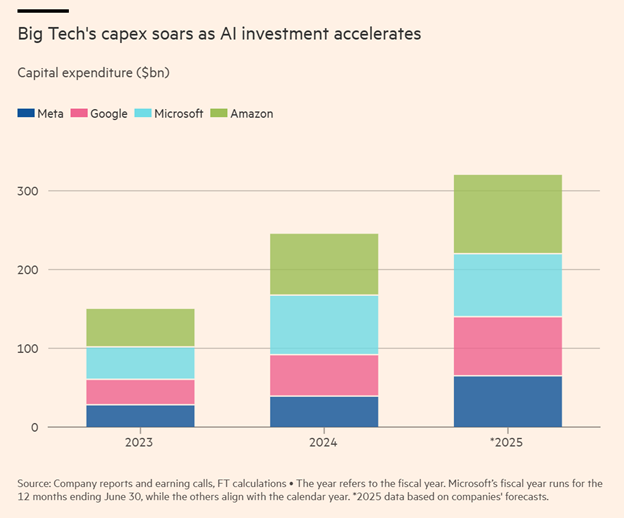

The AI boom is not a U.S.-only phenomenon. Countries like China, Saudi Arabia, and Singapore are pouring capital into AI, creating a global arms race in tech. In the U.S., the four biggest hyperscalers—Amazon, Microsoft, Google, and Meta—are projected to spend over $300 billion on capital expenditures in 2025 alone (see chart below).

To illustrate the scale: Amazon is forecasted to spend more than $100 billion in CapEx this year. For context, that’s 40% more than the company spent over the entire 2000–2020 period combined.

Source: The Financial Times

The Stargate Initiative: AI Infrastructure on a Galactic Scale

A prime example of the AI gold rush is the $500 billion Stargate initiative, with Phase 1 already underway in Abilene, Texas (see rendering below). The initial construction includes two buildings totaling 1,000,000 square feet. Ultimately, the full project will cove about 1,000 acres and be powered by an on-site natural gas facility generating 360 megawatts—enough to support 300,000 homes.

A huge portion of the project costs are dedicated to the budget for NVIDIA super chips. Oracle Corp. has committed $40 billion to purchase 400,000 of NVIDIA’s GB200 chips, making this project a centerpiece of the global AI infrastructure boom. Just this week, Oracle also announced a new $30 billion cloud deal, which will soak up a good chunk of the data center supply created by the database and enterprise software company.

Source: CoStar

The Big Picture: Volatility and Opportunity

There’s no shortage of risk—geopolitics, inflation, Fed uncertainty, tariffs. But the economy is showing surprising resilience. If tariff clarity improves, interest rate cuts materialize, and AI capital spending accelerates, a “boring” market could rapidly turn into a soaring one.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

The Thrill of the Chase

Men (and arguably women to a lesser extent) enjoy the process of hunting for a mate. Chasing the seemingly unattainable event aligns with man’s innate competitive nature. But the quest for the inaccessible is not solely limited to dating. When it comes to other aspirational categories, humans also want what they cannot have because they revel in a challenge. Whether it’s a desirable job, car, romantic partner, or even an investment, people bask in the pursuit.

For many investment daters and trading speculators, 2008-2009 was a period of massive rejection. Rather than embracing the losses as a new opportunity, many wallowed in cash, CDs, bonds, and/or gold. This strategy felt OK until the massive 5-year bull market went on a persistent, upward tear beginning in 2009. Now, as the relentless bull market has continued to set new all-time record highs, the negative sentiment cycle has slowly shifted in the other direction. Back in 2009, many investors regretted owning stocks and as a result locked in losses by selling at depressed prices. Now, the regret of owning stocks has shifted to remorse for not owning stocks. Missing a +23% annual return for five years, while getting stuck with a paltry 0.25% return in a savings account or 3-4% annual return achieved in bonds, can harm the psyche and make savers bitter.

Greed hasn’t fully set in like we witnessed in the late period of the 1990s tech boom, but nevertheless, some of the previous overly cautious “sideliners” feel compelled to now get into the stock game (see Get Out of Stocks!*) or increase their equity allocation. Like a desperate, testosterone-amped teen chasing a prom date, some speculators are chasing stocks, regardless of the price paid. As I’ve noted before, the overall valuation of the stock market seems quite reasonable (see PE ratio chart in Risk Aversion Declining – S. Grannis), despite selective pockets of froth popping up in areas like biotech stocks, internet companies, and junk bonds.

Even if chasing is a bad general investment practice, in the short-run, chasing stocks (or increasing equity allocations) may work because overall prices of stocks remain about half the price they were at the 2000 bubble peak (see Siegel Bubblicious article). How can stocks be -50% off when stock prices today (S&P 500) are more than +25% higher today than the peak in 2000? Plain and simply, it’s the record earnings (see It’s the Earnings Stupid). In the latest Sidoxia newsletter we highlighted the all-time record corporate profits, which are conveniently excluded from most stock market discussions in the blogosphere and other media outlets.

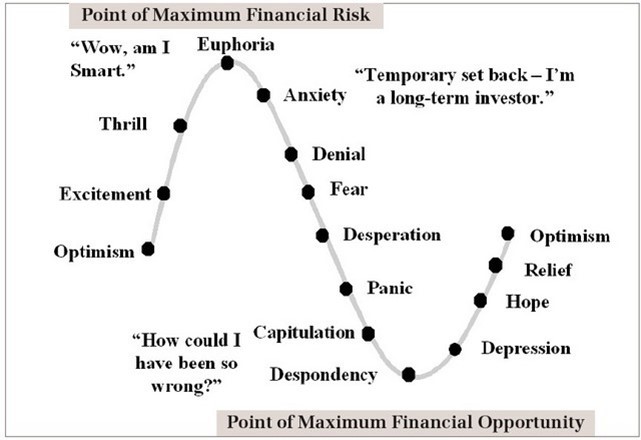

The Investor’s Emotional Roller Coaster (Perceived Risk vs Actual Risk)

The “Thrill of the Chase” is but a single emotion on the roller coaster sentiment spectrum (see Barry Ritholtz chart in Sentiment Cycle of Fear and Greed). The problem with the above chart is many investors confuse actual risk from perceived risk. Many investors perceive the “euphoric” stage of an economic cycle (top of the chart) as low-risk, when in actuality this point reflects peak risk. One can look back to the late 1990s and early 2000 when technology shares were priced at more than 100x years in earnings and every hairdresser, cabdriver and relative were plunging their life savings into stocks. The good news from my vantage point is we are a ways from that euphoric state (asset fund flows and consumer confidence are but a few data points to support this assertion).

The key to reversing the sentiment roller coaster is to follow the thought process of investment greats who learned to avoid euphoria in up markets:

“I’m always more depressed by an overpriced market in which many stocks are hitting new highs every day than by a beaten-down market in a recession.” -Peter Lynch

“Be fearful when others are greedy, and be greedy when others are fearful.” –Warren Buffett

While the “Thrill of the Chase” can seem exciting and a rational strategy at the time, successful long-term investors are better served by remaining objective, unemotional, and numbers-driven. If you don’t have the time, interest, or emotional fortitude to be disciplined, then find an experienced investment manager or advisor to assist you. That will make your emotional roller coaster ride even more thrilling.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Skiing Portfolios Down Bunny Slopes

Oh Nelly, take it easy…don’t get too crazy on that bunny slope. With fall officially kicking off and the crisp smell of leaves in the air, the new season also marks the beginning of the ski season. In many respects, investing is a lot like skiing. Unfortunately, many investors are financially skiing their investment portfolios down a bunny slope by stuffing their money in low yielding CDs, money market accounts, and Treasury securities. The bunny slope certainly feels safe and secure, but many investors are actually doing more long-term harm than good and could be potentially jeopardizing their retirements.

Let’s take a gander at the cautious returns offered up from the financial bunny slope products:

Source: Bankrate.com

That CD earning 1.21% should cover a fraction of your medical insurance premium hike, or if you accumulate the interest from your money market account for a few years, perhaps it will cover the family seeing a new 3-D movie. If you also extend the maturity on that CD a little, maybe it can cover an order of chicken fingers at Applebees (APPB)?!

We all know, for much of the non-retiree population, the probability that entitlement programs like Social Security and Medicare will be wiped out or severely cut is very high. Not to mention, life expectancies for non-retirees are increasing dramatically – some life insurance actuarial tables are registering well above 100 years old. These trends indicate the criticalness of investing efficiently for a large swath of the population, especially non-retirees.

Let’s Face It, One Size Does Not Fit All

Bodie Miller & Grandpa

As I have pointed out in the past, when it comes to investing (or skiing), one size does not fit all (see article). Just as it does not make sense to have Bode Miller (32 year old Olympic gold medalist) ski down a beginner’s bunny slope, it also does not make sense to take a 75-year old grandpa helicopter skiing off a cornice. The same principles apply to investment portfolios. The risk one takes should be commensurate with an individual’s age, objectives, and constraints.

Often the average investor is unaware of the risks they are taking because of the counterintuitive nature of the financial market dangers. In the late 1990s, technology stocks felt safe (risk was high). In the mid-2000s, real estate felt like a sure bet (risk was high), and in 2010, Treasury bonds and gold are currently being touted as sure bets and safe havens (read Bubblicious Bonds and Shiny Metal Shopping). You guess how the next story ends?

Unquestionably, coasting down the bunny slopes with CDs, money market accounts, and Treasuries is prudent strategy if you are a retiree holding a massive nest egg able to meet all your expenses. However, if you are younger non-retiree and do not want to retire on mac & cheese or work at Wal-Mart as a greeter into your 80s, then I suggest you venture away from the bunny slope and select a more suitable intermediate path to financial success.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and WMT, but at the time of publishing SCM had no direct position in APPB, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

The Big Short: The Silent Ticking Bomb

A bomb was ticking for many years before the collapse of Bear Stearns in March of 2008, but unfortunately for most financial market participants, there were very few investors aware of the looming catastrophe. In The Big Short: Inside the Doomsday Machine, author Michael Lewis manages to craft a detailed account of the financial crisis by weaving in the exceptional personal stories of a handful of courageous capitalists. These financial sleuths manage not only to discover the explosive and toxic assets buried on the balance sheets of Wall Street giants, but also to realize massive profits for their successful detective skills.

Lewis was not dabbling in virgin territory when he decided to release yet another book on the financial crisis of 2008-2009. Nonetheless, even after slogging through Andrew Ross Sorkin’s Too Big to Fail and Gregory Zuckerman’s The Greatest Trade Ever (see my reviews on Too Big to Fail and The Greatest Trade Ever), I still felt obligated to add Michael Lewis’s The Big Short to my bookshelf (OK…my e-reader device). After all, he was the creator of Liar’s Poker, The New New Thing, Moneyball, and The Blind Side, among other books in his distinguished collection.

Genesis of the Bomb Creations

Like bomb sniffing dogs, the main characters that Lewis describes in The Big Short (Michael Burry/Scion Capital; Steve Eisman/Oppenheimer and Co. & FrontPoint Partners; Gregg Lippman/Deutsche Bank (DB); and Jamie Mai & Charlie Ledley/Cornwall Capital) demonstrate an uncanny ability to smell the inevitable destruction, and more importantly have the conviction to put their professional careers and financial wellbeing at risk by making a gutsy contrarian call on the demise of the subprime mortgage market.

How much dough did the characters in the book make? Jamie Mai and Charlie Ledley (Cornwall Capital) exemplify the payoff for those brave, and shrewd enough to short the housing market (luck never hurts either). Lewis highlights the Cornwall crew here:

“Cornwall Capital, started four and a half years earlier with $110,000, had just netted from a million-dollar bet, more than $80 million.”

Lewis goes on to describe the volatile period as “if bombs of differing sizes had been placed in virtually every major Western financial institution.” The size of U.S. subprime bombs (losses) exploding was estimated at around $1 trillion by the IMF (International Monetary Fund). When it comes to some of the large publicly traded financial institutions, these money bombs manifested themselves in the form of about $50 billion in mortgage-related losses at Merrill Lynch (BAC), $60 billion at Citigroup (C), $9 billion at Morgan Stanley (MS), along with many others.

The subprime market, in and of itself, is actually not that large in the whole scheme of things. Definitions vary, but some described the market at around 7-8 million subprime mortgages outstanding during the peak of the market, which is a small fraction of the overall U.S. mortgage industry. The relatively small subprime market became a gargantuan problem when millions of lucrative subprime side-bets were created through investment banks and unregulated financial behemoths like AIG. The spirits of greed added fuel to the fire as the construction of credit default swap market and synthetic mortgage-backed CDOs (Collateralized Debt Obligations) were unleashed.

Triggering the Bomb

Multiple constituents, including the rating agencies (S&P [MHP], Moodys [MCO], Fitch) and banks, used faulty assumptions regarding the housing market. Since the subprime market was a somewhat new invention the mathematical models did not know how to properly incorporate declining (and/or moderating) national home prices, since national price declines were not consistent with historical housing data. These models were premised on the notion of Florida subprime price movements not being correlated (moving in opposite directions) with California subprime price movements. This thought process allowed S&P to provide roughly 80% of CDO issues with the top AAA-rating, despite a large percentage of these issues eventually going belly-up.

Lewis punctuated the faulty correlation reasoning underlying these subprime assumptions that dictated the banks’ reckless actions:

“The correlation among triple-B-rated subprime bonds was not 30 percent; it was 100 percent. When one collapsed, they all collapsed, because they were all driven by the same broader economic forces. In the end, it made little sense for a CDO to fall from 100 to 95 to 77 to 70 and down to 7. The subprime bonds beneath them were either all bad or all good. The CDOs were worth either zero or 100.”

Steve Eisman adds his perspective about subprime modeling:

“Just throw the model in the garbage can. The models are all backward looking.”

Ignorance, greed, and other assumptions, such as the credibility of VAR (Value-at-Risk) metrics, accelerated the slope of the financial crisis decline.

Eisman had some choice words about many banking executives’ lack of knowledge, including his gem about Ken Lewis (former CEO of Bank of America):

“I had an epiphany. I said to myself, ‘Oh my God he’s dumb!’ A lightbulb went off. The guy running one of the biggest banks in the world is dumb!”

Or Eisman’s short fuse regarding the rating agency’s refusal to demand critical information from the investment banks due to fear of market share loss:

“Who’s in charge here? You’re the grown up. You’re the cop! Tell them to f**king give it to you!!!…S&P was worried if they demanded the data from Wall Street, Wall Street would just go to Moody’s for their ratings.”

A blatant conflict of interest exists between the issuer and rating agency, which needs to be rectified if credibility will ever return to the rating system. At a minimum, all fixed income investors should wake up and smell the coffee by doing more of their own homework, and relying less on the rubber stamp rating of others. The credit default swap market played a role in the subprime bubble bursting too. Without regulation, it becomes difficult to explain how AIG’s tiny FP (Financial Products) division could generate $300 million in profits annually, or at one point, 15% of AIG’s overall corporate profits.

My Take

The Big Short may simply be recycled financial crisis fodder regurgitated by countless observers, but regardless, there are plenty of redeeming moments in the book. Getting into the book took longer than I expected, given the pedigree and track record of Lewis. Nonetheless, after grinding slowly through about 2/3 of the book, I couldn’t put the thing down in the latter phases.

Lewis chose to take a micro view of the subprime mortgage market, with the personal stories, rather than a macro view. In the first 95% of the book, there is hardly a mention of Bear Stearns (JPM) Lehman Brothers, Citigroup, Goldman Sachs (GS), Fannie Mae (FNM), Freddie Mac (FRE), etc. Nevertheless, at the very end of the book, in the epilogue, Lewis attempts to put a hurried bow around the causes of and solutions to the financial crisis.

There is plenty of room to spread the blame, but Lewis singles out John Gutfreund’s (former Salomon Brothers) decision to take Solly public as a key pivotal point in the moral decline of the banking industry. For more than two decades since the publishing of Liar’s Poker, Lewis’s view on the overall industry remains skeptical:

“The incentives on Wall Street were all wrong; they’re still all wrong.”

His doubts may still remain about the health in the banking industry, and regardless of his forecasting prowess, Michael Lewis will continue sniffing out bombs and writing compelling books on a diverse set of subjects.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AIG subsidiary debt, but at the time of publishing SCM had no direct positions in BAC, JPM, FRE, FNM, DB, MS, GS, C, MCO, MHP, Fitch, any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

California Checking Under the Derivatives Hood

[tweetmeme source=”WadeSlome” only_single=false https://investingcaffeine.com/2010/04/11/california-checking-under-the-derivatives-hood/%5D

Bill Lockyer, California’s State Treasurer, is in charge of driving “The Golden State’s” budget, but as he maneuvers the finances, he is hearing some strange knocks and pings as it relates to the pricing of Credit Default Swaps (CDS) on California debt obligations. CDSs, like virtually all derivatives, can either be used to speculate or hedge (see also, Einhorn CDS and Financial Engineering articles), so the existence of strange noises does not necessarily indicate foul play or problems that cannot be fixed.

Checking Under the Banks’ Hoods

At the heart of the CDS markets lie the major investment banks, so that is where Lockyer is looking under the hood and requesting information on the role the banks are playing in the municipal bond CDS market. Specifically, Lockyer has sent letters requesting information from Bank of America – Merrill Lynch (BAC), Barclays, Citigroup (C), Goldman Sachs (GS), JP Morgan (JPM),and Morgan Stanley (MS). California pays the banks millions of dollars every year to market bonds on behalf of the state. The I-banks operate in some way like a car dealership – the state produces the cars (bonds) and the banks buy the bonds and resell them to buyers/investors.

The financial transaction doesn’t necessarily stop there, because the banks can further pad their profits by selling and making markets in credit default swaps. After the state issues bonds, speculators can then pay the banks to place bets on whether the cars (bonds) fail (default), or investors can also buy insurance from the banks in the form of swaps. As you can probably surmise, there is the potential for conflicts of interest between the state and the banks, which partly explains why Lockyer is conducting his due diligence.

California…the Next Greece or Kazakhstan?

As the housing market came crashing down, credit default swaps were at the center of financial institution collapses and the billions made by John Paulson (see also the Gutsiest Trade Ever). More recently, CDSs were cited as negative contributors to the Greek financial crisis. Lockyer tries to deflect California comparisons with Greece by stating the European country’s budget deficit is 13 times larger than California’s (as % of GDP) and the foreign country’s accumulated debt is 25 times larger on GDP basis as well (read California’s Debt Hole story).

Beyond making sure the profit rules of the game are not stacked against California, Lockyer wants to understand what he perceives as a mispricing in the default risk of California debt obligations. He is worried that the state’s borrowing costs on future bond issues could be artificially escalated because he says the credit default swaps “wrongly brand our bonds as a greater risk than those issued by such nations as Kazakhstan, Croatia, Bulgaria and Thailand.”

Clarity on these issues is important because the state is exploring the expansion into taxable municipal bonds. The government has been subsidizing taxable munis, termed Build America Bonds (BABs), to stimulate the economy and bring down borrowing costs for municipalities. According to Thomson Reuters, BABS accounted for approximately 26% of overall muni bond issuance ($25.8 billion) in the first quarter.

If California were a car, I’m not sure how much cash they would get for their clunker ($16 billion budget deficit), but I tip my hat to State Treasurer Lockyer for holding the investment banks’ feet to the fire. All investors and financial product consumers stand to benefit by looking under the hood of their financial institution and asking tough questions.

Read Full Financial Times Article on California CDS Market

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

*DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct positions in BAC, C, GS, JPM, and MS or any security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

John Paulson and the “Gutsiest” Trade Ever

Although the pain and suffering of the 2008-09 financial crisis has been well documented and new books are continually coming out in droves, less covered are the winners who made a bonanza by predicting the collapse of the real estate and credit markets. Prizewinning Wall Street Journal reporter Gregory Zuckerman decided to record the fortunes made by hedge fund manager John Paulson in his book The Greatest Trade Ever (The Behind-the-Scenes story of How John Paulson Defied Wall Street and Made Financial History).

Paulson’s Cartoonish Cut

Zuckerman puts Paulson’s massive gains into perspective:

“Paulson’s winnings were so enormous they seemed unreal, even cartoonish. His firm, Paulson & Co., made $15 billion in 2007, a figure that topped the gross domestic products of Bolivia, Honduras, and Paraguay…Paulson’s personal cut was nearly $4 billion…more than the earnings of J.K. Rowling, Oprah Winfrey, and Tiger Woods put together.”

As impressive as those gains were, Paulson added another $5 billion into his firm’s coffers and $2 billion into his personal wallet over 2008 and early 2009.

There are many ways to skin a cat, and there are countless strategies used by the thousands of hedge fund managers looking to hit the jackpot like Paulson. John Paulson primarily made his multi-billion fortune thanks to his CDS positions (Credit Default Swaps), the same product that led to massive multi-billion bailouts and government support for various financial institutions.

Bigger Gamble than Perception

One surprising aspect I discovered from reading the book was the uncertainty surrounding Paulson’s negative real estate trade. Here’s how Zuckerman described the conviction level of John Paulson and Paolo Pelligrini (colleague) as it related to their CDS positions on subprime CDO (Collateralized Debt Obligation) debt:

“In truth, Paulson and Pellegrini still were unsure if their growing trade would ever pan out. They thought the CDOs and other risky mortgage debt would become worthless, Paulson says. ‘But we still didn’t know.’”

Often the trades that cause you to sweat the most tend to be the most profitable, and in this case, apparently the same principle held.

Disingenuous Dramatic License

Before Paulson made his billions, Zuckerman uses a little dramatic license in the book to characterize Paulson as a small fry manager, “Paulson now managed $1.5 billion, a figure that sounded like a lot to friends outside the business. But the firm was dwarfed by its many rivals.” Zuckerman goes on to call Paulson’s hedge fund “small potatoes.” I don’t have the industry statistics at my fingertips, but I’ll go out on a limb and make an educated guess that a $1.5 billion hedge fund has significantly more assets than the vast majority of hedge fund peers. Under the 2 and 20 model, I’m guessing the management fee alone of $30 million could cover Paulson’s food and shelter expenses. Before he struck the payload, the book also references the $100 million of his personal wealth he invested with the firm. I think John Paulson was doing just fine before he executed the “greatest trade.”

What Drove the Greatest Trade

Hind sight is always 20/20, but looking back, there was ample evidence of the real estate bubble forming. Fortunately for Paulson, he got the timing generally right too. Here are some of the factors leading to the great trade:

- CDO Leverage in Subprime: By the end of 2006, the subprime loan market was relatively large at around $1.2 trillion (representing around 10% of the overall mortgage market). But thanks to the introduction of CDOs, there were more than $5 trillion of risky investments created from all the risky subprime loans.

- Liars & Ninjas: “Liar Loans” loans based on stated income (using the honor system) and “ninja loans” (no income, no job, no assets) gained popularity and prevalence, which just led to more defaults and foreclosures in the mid-2000s.

- No Down Payments: What’s more, by 2005, 24% of all mortgages were completed with no down payment, up from approximately 3% in 2001. The percentage of first-time home buyers with no down payment was even higher at 43%.

Overall, I give kudos to Gregory Zuckerman, who spent more than 50 hours with John Paulson, for bringing something so abstract and homogenous (a skeptical real estate trade) to life. Zuckerman does a superb job of adding spice to the Paulson story by introducing other narratives and characters, even if the story lines don’t blend together perfectly. After reading The Greatest Trade Ever I came away with a new found respect for Paulson’s multi-billion dollar gutsy trade. Now, Paulson has reloaded his gun and is targeting the U.S. dollar. If Paulson’s short dollar and long gold position works out, I’ll keep an eye out for his next book…The Greatest Trad-er Ever.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including VNQ), but at time of publishing had no direct positions in companies mentioned. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Financial Engineering: Butter Knife or Cleaver?

Recently, former Federal Reserve Board Chairman Paul Volcker blasted the banking industry for innefectual derivative producs (i.e., credit default swaps [CDS] and collateralized debt obligations [CDOs]) and a lack of true innovation outside of the ATM machine, which was introduced some 40 years ago. In my opinion, the opposing views pitting the cowboy Wall Street bankers versus conservative policy hawks parallels the relative utility question of a butter knife versus a cleaver. Like knives, derivatives come in all shapes and sizes. Most Americans responsibly butter their toast and cut their steaks, nonetheless if put in the wrong hands, knives can lead to minor cuts, lost fingers, or even severed arteries.

That reckless behavior was clearly evident in the unregulated CDS market, which AIG alone, through its Financial Products unit in the U.K., grew its exposure to a mind boggling level of $2.7 trillion in notional value, according to Andrew Ross Sorkin’s book Too Big to Fail. The subprime market was a big driver for irresponsible CDO creation too. In The Greatest Trade Ever, Gregory Zuckerman highlights the ballooning nature of the $1.2 trillion subprime loan market (about 10% of the overall 2006 mortgage market) , which exploded to $5 trillion in value thanks to the help of CDOs.

Derivatives History

However, many derivative products like options, futures, and swaps have served a usefull purpose for decades, if not centuries. As I chronicled in the Investing Caffeine David Einhorn piece, derivative trading goes as far back as Greek and Roman times when derivative-like contracts were used for crop insurance and shipping purposes. In the U.S., options derivatives became legitimized under the Investment Act of 1934 before subsequently being introduced on the Chicago Board Options Exchange in 1973. Since then, the investment banks and other financial players have created other standardized derivative products like futures, and interest rate swaps.

Volcker Expands on Financial Engineering Innovation

In his comments, former Chairman Volcker specifically targets CDSs and CDOs. Volcker does not mince words when it comes to sharing his feelings about derivatives innovation:

“I hear about these wonderful innovations in the financial markets, and they sure as hell need a lot of innovation. I can tell you of two—credit-default swaps and collateralized debt obligations—which took us right to the brink of disaster…I wish that somebody would give me some shred of neutral evidence about the relationship between financial innovation recently and the growth of the economy, just one shred of information.”

When Volcker was challenged about his skeptical position on banking innovation, he retorted:

“All I know is that the economy was rising very nicely in the 1950s and 1960s without all of these innovations. Indeed, it was quite good in the 1980s without credit-default swaps and without securitization and without CDOs.”

Cutting through Financial Engineering

The witch-hunt is on for a financial crisis scapegoat, and financial engineering is at the center of the pursuit. Certainly regulation, standardized derivative contracts, trading exchanges, and increased capital requirements should all be factors integrated into new regulation. Curbs can even be put in place to minimize leveraged speculation. But the baby should not be thrown out with the bathwater. CDSs, CDOs, securitization and other derivative products serve a healthy and useful purpose towards the aim of creating more efficient financial markets – especially when it comes to hedging. For the majority of our daily requirements, I advocate putting away the dangerous cleaver, and sticking with the dependable butter knife. On special occasions, like birthday steak dinners, I’ll make sure to invite someone responsible, like Paul Volcker, to cut my meat with a steak knife.

Read Full WSJ Article with Paul Volcker Q&A

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct position in any company mentioned in this article, including AIG. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Making Safer Asbestos: Einhorn on CDS

David Einhorn, founding hedge fund manager of Greenlight Capital, exploited Credit Default Swaps (CDS) derivative contracts to their fullest in the midst of the financial crisis and now he says any effort to keep them in existence is like making “safer asbestos.” Hypocritical?

As toxic debt devices that profit from credit default triggers, CDSs have created “large correlated and asymmetrical risks,” which have “scared authorities into spending hundreds of billions of taxpayer money to prevent speculators who made bad bets from having to pay,” according to Einhorn.

The abolishment of the CDS market would have no impact on me (I have never traded a CDS in my life), but in principle Einhorn has no leg to stand on. Just because these unregulated insurance contracts were not properly disclosed or collateralized by American International Group, Inc. (AIG) does not mean a transparent, properly collateralized, central clearing exchange could not be created to efficiently meet the needs of counterparties.

Derivatives Description

Conceptually, a CDS is no different than a derivatives option contract. Take for example a put contract. Like a CDS, a put contract can be purchased as insurance (hedging against price declines on a current holding) or it can be purchased for speculative purposes (profit from future potential price declines if there is no underlying ownership position). All derivatives are structured for hedging or speculation, whether you are talking about options, futures, swaps, or other exotic forms of derivatives (i.e., swaptions). CDSs are no different.

Einhorn is not the first person to disingenuously speak about derivatives. The “do as I say, not as I do” principle holds true for Warren Buffett too. Buffett blasted derivatives as “weapons of mass destruction,” yet he has made billions of dollars (read about Buffett on derivatives) in premiums from writing (selling) multi-year options on various indexes.

Derivatives History

Derivative trading goes as far back as Roman and Greek history when similar contracts were used for crop insurance and shipping purposes. After the Great Depression, the Investment Act of 1934 legitimized options under the watchful eye of the Securities and Exchange Commission (SEC). Subsequently, the Chicago Board Options Exchange (CBOE) began trading listed options in 1973. Since then, the investment banks and other financial players have created derivative products making up many different flavors.

The Solution

How does Einhorn feel about central clearing exchanges?

“The reform proposal to create a CDS clearing house does nothing more than maintain private profits and socialised risk by moving the counterparty risk from the private sector to a newly created too big to fail entity.”

Oh really? If the utility of hedging contracts has been documented for hundreds of years, then why wouldn’t we create a standardized, transparent, adequately capitalized central clearing house for these tools? Whether Einhorn is asking for the eradication of all derivatives, I cannot be sure. If his extermination comments apply equally to all derivatives, then I guess we’ll just have to shutter entities like the CBOE, which handled 1.19 billion options contracts last year alone. If eliminating speculation was the focal point of Einhorn’s argument, then perhaps regulators could simply raise the reserve requirements for those merely gambling on price declines or default triggers.

In the end, if what Einhorn recommended came to fruition, he would only be throwing the baby out with the bathwater. CDSs, and other derivatives, serve a healthy and useful purpose towards the aim of creating more efficient financial markets. I agree that the AIG flavor of CDSs were like lethal asbestos, so let’s see if we can now replace it with some safer insulation protection.

Read Financial Times Editorial on David Einhorn

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) or its clients owns certain exchange traded funds, but currently has no direct position in AIG, or BRKA/BRKB. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Compensation: Pitchforks or Penalties

Currently there is witch hunt under way to get rid of excessive compensation levels, especially in the financial and banking industries. Members of Congress and their constituents are looking to reign in the exorbitant paychecks distributed to the fat-cat executives at the likes of Goldman Sachs, Bank of America and the rest of the banking field. According to The Financial Times, Goldman has set aside $16.7 billion so far this year for compensation and benefits and pay is on track to meet or exceed the $661,000 employee average in 2007. The public is effectively calling these executive bankers “cheaters” because they are receiving benefits they don’t deserve. The backlash resembles the finger-pointing we see directed at the wealthy steroid abusers in football or cork-bat swingers in baseball. Americans seem OK with big payouts as long as they are achieved in a fair manner. No one quibbles with the billions made by Bill Gates or Warren Buffett, but when you speak of other wealth cheaters like Jeff Skilling (Enron), Bernie Ebbers (WorldCom), or Dennis Kozlowski (Tyco), then the public cringes. The reaction to corporate crooks is similar to the response provoked by steroid use allegations tied to Major League Baseball players (i.e., Barry Bonds and Roger Clemens).

Less clear are the cases in which cheaters take advantage of a system run by regulators (referees) who are looking the other way or have inadequate rules/procedures in place to monitor the players. Take for example the outrage over $165 million in bonuses paid to the controversial AIG employees of the Financial Products division. Should AIG employees suffer due to lax rules and oversight by regulators? There has been no implication of illegal behavior conducted by AIG, so why should employees be punished via bonus recaptures? The rules in place allowed AIG to issue these lucrative Credit Default Swap (CDS) products (read more about CDS) with inadequate capital requirements and controls, so AIG was not shy in exploiting this lack of oversight. Rule stretchers and breakers are found in all professions. For example, Lester Hayes, famed All-Pro cornerback from the Oakland Raiders, used excessive “Stickum” (hand glue) to give himself an advantage in covering his opponents. If professionals legally operate within the rules provided, then punishments and witch hunts should be ceased.

Regulators, or league officials in sports, need to establish rules and police the players. Retroactively changing the rules after the game is over is not the proper thing to do. What the industry referees need is not pitchforks, but rather some yellow flags and a pair of clear glasses to oversee fair play.

Cash Givers Should Make the Rules

What should regulators and the government do when it comes to compensation? Simply let the “cash givers” make the rules. In the case of companies trading in the global financial markets, the shareholders should drive the rules and regulations of compensation. “Say on pay” seems reasonable to me and has already gained more traction in the U.K. On the other hand, if shareholders don’t want to vote on pay and feel more comfortable in voting for independent board members on a compensation committee, then that’s fine by me as well. If worse comes to worse, shareholders can always sell shares in those companies that they feel institute excessive compensation plans. At the end of the day, investors are primarily looking for companies whose goal it is to maximize earnings and cash flows – if compensation plans in place operate against this goal, then shareholders should have a say.

When it comes to government controlled entities like AIG or Citigroup, the cash givers (i.e., the government) should claim their pound of flesh. For instance, Kenneth Feinberg, the Treasury official in charge of setting compensation at bailed-out companies, decided to cut compensation across the board at American International Group, Citigroup, Bank of America, General Motors, GMAC , Chrysler, and Chrysler Financial for top executives by more than 90% and overall pay by approximately 50%.

Put Away the Pitch Forks

In my view, too much emphasis is being put on executive pay. Capital eventually migrates to the areas where it is treated best, so for companies that are taking on excessive risk and using excessive compensation will find it difficult to raise capital and grow profits, thereby leading to lower share prices – all else equal. Government’s job is to partner with private regulators to foster an environment of transparency and adequate risk controls, so investors and shareholders can allocate their capital to the true innovators and high-profit potential companies. Too big to fail companies, like AIG with hundreds of subsidiaries operating in over 100 countries, should not be able to hide under the veil of complexity. Even in hairy, convoluted multi-nationals like AIG, half a trillion CDS exposure risks need to be adequately monitored and disclosed for investors. That why regulators need to take a page from other perfectly functioning derivatives markets like options and futures and get adequate capital requirements and transparency instituted on exchanges. I’m confident that market officials will penalize the wrongdoers so we can safely put away the pitch forks and pull out more transparent glasses to oversee the industry with.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management and its clients do not have a direct position in Goldman Sachs (GS), AIG, Berkshire Hathaway, BRKA/B, Citigroup (C), Enron, General Motors, GMAC , Chrysler, WorldCom, or Tyco International (TYC) shares at the time this article was originally posted. Sidoxia Capital Management and its clients do have a direct position in Bank of America (BAC). No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Cash Strapped Bond Issuers Should Follow Willie Sutton

![940614_83408820[1]](https://investingcaffeine.com/wp-content/uploads/2009/07/940614_834088201.jpg "940614_83408820[1]")

When infamous bank robber Willie Sutton was asked why he robs banks, he coyly responded, “Because that’s where the money is.” Willie Sutton was one of the more prominent bank robbers in American history. During his long career he had robbed close to 100 banks from the late 1920s to 1952. He was known as “Slick Willie” or “The Actor.” As a master of disguise the FBI files show that Sutton masqueraded himself as a mailman, policeman, telegraph messenger, maintenance man and a host of other personas. The Credit Default Swap market has also been disguised in mystery and opaqueness.

With many cash strapped bond issuers looking for ways to negotiate more favorable credit terms during these tough economic times, one strategy has been to approach holders of the CDS instruments. However, CDS holders have no reason to negotiate with corporate bond issuers (for pennies on the dollar) when they stand to collect a full dollar from their bank (due to terms in the CDS contracts). Cash starved corporations rather should listen to Willie Sutton and go straight to the money source – the banks that issued the CDS to the investors. As bankruptcies increase, and bank failures rise, the trio of bond holders, bond issuers, and CDS issuers (banks) will become closer friends (and/or enemies).

Research Reloaded delved more into this issue by discussing the tactics used by media companies, Gannett and McClatchy (Read Article Here). Lots of wrinkles need to be ironed out in the CDS market, measured in the tens of trillions in notional value, but part of the solution involves the bond issuer and investor going straight to the money source (the bank issuer of the CDS). Willie would be proud.

Wade W. Slome, CFA, CFP® www.Sidoxia.com

{kind=link}

{kind=link}