Posts tagged ‘carry trade’

1994 Bond Repeat or 2013 Stock Defeat?

Interest rates are moving higher, bond prices are collapsing, and fear regarding a stock market plunge is palpable. Sound like a recent news headline or is this a description of a 1994 financial market story? For those with a foggy, double-decade-old memory, here is a summary of the 1994 economic environment:

- The economy registered its 34th month of expansion and the stock market was on a record 40-month advance

- The Federal Reserve embarked on its multi-hike, rate-tightening monetary policy

- The 10-year Treasury note exhibited an almost 2.5% jump in yields

- Inflation was low with a threat of rising inflation lurking in the background

- An upward sloping yield curve encouraged speculative bond carry-trade activity (borrow short, invest long)

- Globalization and technology sped up the pace of price volatility

Many of these listed items resemble factors experienced today, but bond losses in 1994 were much larger than the losses of 2013 – at least so far. At the time, Fortune magazine called the 1994 bond collapse the worst bond market loss in history, with losses estimated at upwards of $1.5 trillion. The rout started with what might have appeared as a harmless 0.25% increase in the Federal Funds rate (the rate that banks lend to each other) from 3% to 3.25% in February 1994. By the time 1994 came to a close, acting Federal Reserve Chairman Alan Greenspan had jacked up this main monetary tool by 2.5%.

Rising rates may have acted as the flame for bond losses, but extensive use of derivatives and leverage acted as the gasoline. For example, over-extended Eurobond positions bought on margin by famed hedge fund manager Michael Steinhardt of Steinhardt Partners lead to losses of about-30% (or approximately $1.5 billion). Renowned partner of Omega Partners, Leon Cooperman, took a similar beating. Cooperman’s $3 billion fund cratered -24% during the first half of 1994. Insurance company bond portfolios were hit hard too, as collective losses for the industry exceeded $20 billion, or more than the claims paid for Hurricane Andrew’s damage. Let’s not forget the largest casualty of this era – the public collapse of Orange County, California. Poor derivatives trades led to $1.7 billion in losses and ultimately forced the county into bankruptcy.

There are plenty of other examples, but suffice it to say, the pain felt by other bond investors was widespread as a massive number of margin calls caused a snowball of bond liquidations. The speed of the decline was intensified as bond holders began selling short and using derivatives to hedge their portfolios, accelerating price declines.

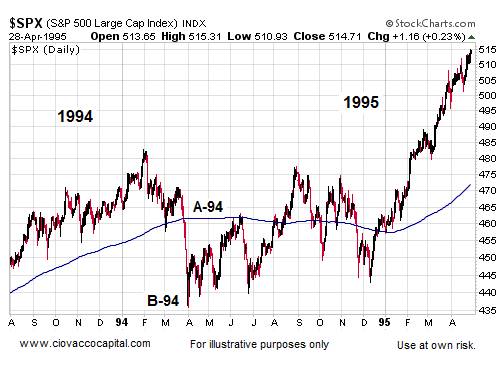

Just as the accommodative interest rate punch bowl was eventually removed by Greenspan, so too is Ben Bernanke (current Fed Chairman) threatening to do today. Even if Bernanke unleashes a cold-turkey tapering of the $85 billion per month in bond-purchases, massive losses in bond values won’t necessarily mean catastrophe for stock values. For evidence, one needs to look no further than this 1994-1995 chart of the stock market:

Source: Ciovaccocapital.com

Volatility for stocks definitely increased in 1994 with the S&P 500 index correcting about -10% early in the year. But as you can see, by the end of the year the market was off to the races, tripling in value over the next five years. Volatility has been the norm for the current bull market rally as well. Despite the more than doubling in stock prices since early 2009, we have experienced two -20% corrections and one -10% pullback.

What’s more, the onset of potential tapering is completely consistent with core economic principles. Capitalism is built on free trading markets, not artificial intervention. Extraordinary times required extraordinary measures, but the probabilities of a massive financial Armageddon have been severely diminished. As a result, the unprecedented scale of quantitative easing (QE) will eventually become more harmful than beneficial. The moral of the story is that volatility is always a normal occurrence in the equity markets, therefore any significant stock pullback associated with potential bond tapering (or fed fund rate hikes) shouldn’t be viewed as the end of the world, nor should a temporary weakening in stock prices be viewed as the end to the bull market in stocks.

Why have stocks historically provided higher returns than bonds? The short answer is that stocks are riskier than bonds. The price for these higher long-term returns is volatility, and if investors can’t handle volatility, then they shouldn’t be investing in stocks.

If you are an investor that thinks they can time the market, you wouldn’t be wasting your time reading this article. Rather, you’d be spending time on your personal island while drinking coconut drinks with umbrellas (see Market Timing Treadmill).

Although there are some distinct similarities between the economic backdrop of 1994 and 2013, there are quite a few differences also. For starters, the economy was growing at a much healthier clip then (+4.1% GDP growth), which stoked inflationary fears in the mind of Greenspan. Moreover, unemployment was quite low (5.5% by year-end vs. 7.6% today) and the Fed did not communicate forward looking Fed policy back then.

It’s unclear if the recent 50 basis point ascent in 10-year Treasury rates was just an appetizer for what’s to come, but simple mathematics indicate there is really only one direction left for interest rates to go…higher. If history repeats itself, it will likely be bond investors choking on higher rates (not stock investors). For the sake of optimistic bond speculators, I hope Ben Bernanke knows the Heimlich maneuver. Studying history may help bond bulls avoid indigestion.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

FX, the Carry Trade, and Arbitrage Vigilantes

What do you think of the Euro? How about the Japanese yen? Are you expecting the Thai baht to depreciate in value versus the Brazilian real? Speculators, central banks, corporations, governments, financial institutions, and other constituencies ask similar types of questions every day. The largely over-the-counter global foreign exchange markets (no central exchange) are ubiquitous, measuring in the trillions – the BIS (Bank for International Settlements) computed the value of traditional foreign exchange markets at $3.2 trillion in April 2007. Thanks to globalization, these numbers are poised to expand even further. Like other futures markets (think oil, gold, or pork bellies), traders can speculate on the direction of one currency versus another. Alternatively, investors and businesses around the world can use currency futures to hedge (protect) or facilitate international trade.

Without getting lost in the minutiae of foreign exchange currency trading, I think it’s helpful to step back and realize regardless of strategy, currency, interest rate, inflation, peg-ratio, deficits, sovereign debt, or other factor, money will eventually migrate to where it is treated best in the long-run. When it comes to currencies, it’s my fundamental belief that economies control their currency destinies based on the collective monetary, fiscal, and political decisions made by each country. If those decisions are determined imprudent by financial market participants, countries open themselves up to speculators and investors exploiting those decisions for profits.

Currency Trading Ice Cream Style

As mentioned previously, currency trading is predominantly conducted over-the-counter, outside an exchange, but there are almost more trading flavors than ice cream choices at Baskin-Robbins. For instance, one can trade currencies by using futures, options, swaps, exchange traded funds (ETFs), or trading on the spot or forward contract markets. Each flavor has its own unique trading aspects, including the all-important amount of leverage employed.

The Carry Trade

Similar to other investment strategies (for example real estate), if profit can be made by betting on the direction of currencies, then why not enhance those returns by adding leverage (debt). A simple example of a carry trade can illustrate how debt is capable of boosting returns. Suppose hedge fund XYZ wants to borrow (sell U.S. dollars) at 0.25% and buy the Swedish krona currency so they can invest that currency in 5.00% Swedish government bonds. Presumably, the hedge fund will eventually realize the spread of +4.75% (5.00% – 0.25%) and with 10x leverage (borrowings) the amplified return could reach +47.5%, assuming the relationship between the U.S. dollar and krona does not change (a significant assumption).

Positive absolute returns can draw large pools of capital and can amplify volatility when a specific trade is unwound. For example, in recent years, the carry trade from borrowing Japanese yen and investing in the Icelandic krona eventually led to a sharp unwinding in the krona currency positions when the Icelandic economy collapsed in 2008. High currency values make exports less competitive and more expensive, thereby dampening GDP (Gross Domestic Product) growth. On the flip side, higher currency values make imported goods and services that much more affordable – a positive factor for consumers. Adding complexity to foreign exchange markets are the countries, like China, that artificially inflate or depress currencies by “pegging” their currency value to a foreign currency (like the U.S. dollar).

Soros & Arbitrage Vigilantes

Hedge funds, proprietary trading desks, speculators and other foreign exchange participants continually comb the globe for dislocations and discrepancies to take advantage of. Traders are constantly on the look out for arbitraging opportunities (simultaneously selling the weakest and buying the strongest). Famous Quantum hedge fund manager, George Soros, took advantage of weak U.K. economy in 1992 when he spent $10 billion in bet against the British pound (see other Soros article). The Bank of England fought hard to defend the value of the pound in an attempt to maintain a pegged value against a basket of European currencies, but in the end, because of the weak financial condition of the British economy, Soros came out victorious with an estimated $1 billion in profits from his bold bet.

I’m not sure whether the debate over speculator involvement in currency collapses can be resolved? What I do know is the healthier economies making prudent monetary, fiscal, and political decisions will be more resilient in protecting themselves from arbitrage vigilantes.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at time of publishing had no direct position on any security referenced. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}