Posts tagged ‘CAPEX’

The Multi-Trillion AI Tsunami Sweeping the Market

Not only has Artificial Intelligence (AI) dominated headlines, but a multi-trillion-dollar investment tsunami is creating a rising tide that has lifted many AI-related stocks to market leadership. Since the seismic launch of OpenAI’s ChatGPT in November 2022, investors have rushed to participate in what may be one of the largest technology investment cycles in history.

At my firm, Sidoxia Capital Management, we have been positioned in the AI rush for several years—well before ChatGPT became a household name. Close followers of my work know I have been tracking the AI revolution for years (see my previous analysis on my Investing Caffeine blog.

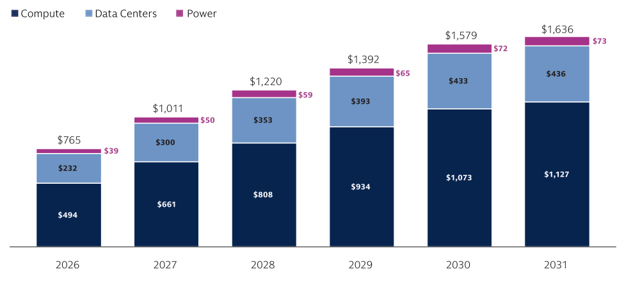

Goldman Sachs recently published an in-depth report highlighting the various AI scenarios and assumptions underlying an estimated $4 trillion to $8 trillion spending boom on compute (AI chips), data center infrastructure, and power investments over the next five years. As shown in the chart below, Goldman’s baseline capital expenditures scenario models a staggering $7.6 trillion in spending from 2026 to 2031. While variables like the lifespan of NVIDIA GPUs can shift annual AI spending estimates by hundreds of billions of dollars, the numbers remain enormous under virtually any scenario.

Source: Goldman Sachs

Market Momentum: Another Record-Breaking Month

For the month, the major indexes once-again vaulted to new record highs, driven by the AI capital expenditure cycle and a record level of profits:

· S&P 500: +5.2% (+10.7% year-to-date)

· NASDAQ: +8.4% (+16.1% year-to-date)

· Dow Jones Industrial Average: +2.8% (+6.2% year-to-date)

As I highlighted in last month’s post, it isn’t just speculative spending driving stock prices higher; it is an active AI productivity revolution that is causing corporate earnings to roar. This is especially true within the large-cap technology sector, which serves as the primary engine behind the S&P 500’s record-breaking performance.

It may seem counter-intuitive, but even as stock prices have reached record heights, valuations have actually become cheaper (sitting at a 20.9 forward P/E) compared to the peak price-to-earnings ratios seen in 2025. How is this possible? Quite simply, the denominator of the P/E ratio (earnings) has been growing at a faster clip than the numerator (stock prices), compressing the overall valuation multiple – see chart below.

Source: Yardeni.com

The Quest for Efficiency

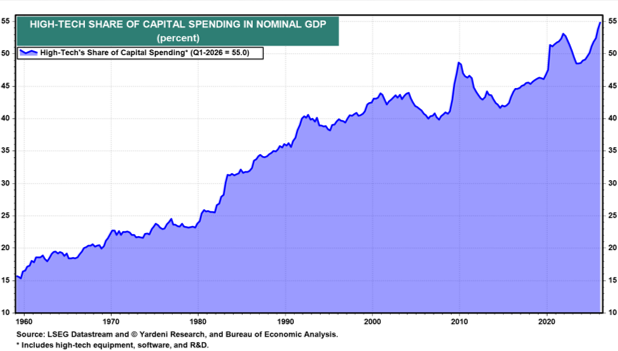

Ultimately, the objective of every publicly traded company is straightforward: increase profits and cash flow. For most businesses, labor remains the largest operating expense. One of the most effective ways to reduce labor costs and improve efficiency is through technology investment. The chart below highlights the growing role technology plays within the economy as companies increasingly invest in automation, software, cloud computing, and AI. These investments often improve productivity, expand margins, and enhance long-term profitability.

Source: Yardeni.com

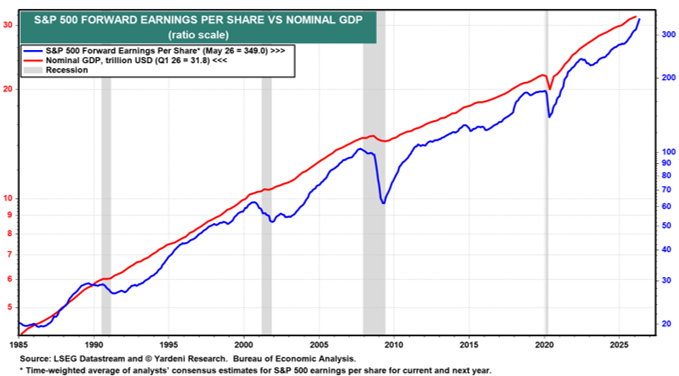

As this disruptive AI revolution permeates all sectors of the economy, we are witnessing the early stages of a productivity renaissance. Even as unemployment rates slowly creep higher (reaching 4.3% from a 2023 low of 3.4%), corporate profit growth is accelerating while nominal GDP continues to chug along at a steady rate (see chart below).

Source: Yardeni.com

The Infrastructure Winners

Underlying this economic growth are the individual companies building the foundation of the AI boom. Just five months into the year, a select group of infrastructure and semiconductor hardware companies have posted astronomical returns in 2026*:

Underlying the growth in profits and the economy are the individual companies driving the AI infrastructure boom. Even though we are only five months through the year, here is a small list of companies benefiting from and contributing to the rocketing growth in 2026 (YTD % Gains)*:

· Sandisk Corp. (SNDK) +604%

· Micron Technology Inc. (MU) +240%

· Dell Technologies Inc. (DELL) +234%

· Intel Corp. (INTC) +211%

· Western Digital Corp. (WDC) +208%

· Sterling Infrastructure Inc. (STRL) +181%

· Powell Industries Inc. (POWL) +168%

· Comfort Systems USA Inc. (FIX) +96%

· Vertiv Holdings Co. (VRT) +95%

*Sidoxia Capital Management and/or its clients hold positions in some of these companies (see Complete Strategy Performance and Disclosure at the bottom of this article or Click Here).

A major tailwind supporting these companies is the roughly $700 billion of capital expenditures expected in 2026 from hyperscale technology leaders such as Alphabet, Microsoft, Meta Platforms, and Amazon. These firms continue to aggressively invest in AI infrastructure to maintain competitive advantages and satisfy surging demand for AI-powered services – see AI Tech Spending article.

The Importance of Diversification (Even in a Hot Market)

At Sidoxia, our concentrated equity portfolios have significantly outperformed the S&P 500 index in 2026, as well as on a 1-year, 3-year, and 5-year basis. However, our winning exposure in AI infrastructure stocks has been partially offset by underperformance in the cryptocurrency, healthcare, and software/SaaS sectors. This includes drags from holdings like Exzeo Group, Inc. (XZO, -43% YTD), Salesforce Inc. (CRM, -28%), and Roper Technologies Inc. (ROP, -27%).

Ultimately, this underscores the necessity of a balanced portfolio: the positive contributions from our top-performing names heavily outweighed the negative drag from the laggards, allowing our concentrated strategy to come out ahead.

No Signs of Slowing, But Watch the Horizon

Euphoria surrounding the AI spending wave shows no signs of abating in the near term. The highly anticipated upcoming Initial Public Offerings (IPOs) from private giants like SpaceX (SPCX), Anthropic, and OpenAI will likely add fuel to investor excitement. This naturally begs the question: are we inflating another technology bubble?

Trees don’t grow to the sky forever, and the same fundamental law applies to investing—eventually, the parabolic gains will slow or reverse.

The AI tsunami is currently in full force, and while it has created massive wealth today, historical market cycles remind us that unmanaged momentum can eventually cause financial damage to unprepared investors. Right now, there is no shortage of demand for AI services and infrastructure, keeping the market tide exceptionally high. Sidoxia and its clients have benefited tremendously from this secular trend, but we remain highly vigilant and active in managing risk for when the tide inevitably turns.

Stay tuned, and ensure your portfolio is properly structured to navigate the waves ahead.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

Important Performance Disclosure: The specific positions discussed above were extracted based on the top and bottom performers from our overall Concentrated Equity Strategy portfolios. To see how these selections fit into our broader historical track record, please review our

Full Strategy Performance Sheet & Required Legal Disclosures (PDF)

Sidoxia Capital Management (SCM) and some of its clients hold positions in GS, STRL, POWL, FIX, VRT, XZO, CRM, ROP, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. Past performance is no guarantee of future results. Selections referenced in this article represent the top and bottom material contributors and do not reflect all positions bought or sold during this period.

ADDITIONAL DISCLOSURE: No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Each investor’s situation is unique so please work with a professional financial adviser, tax accountant or legal representative, as applicable, to develop an individualized plan or address any questions you may have. Investing involves risk including the possibility of loss of one’s investment.

A.I. Field of Dreams

In the 1989 Academy Award–nominated film Field of Dreams, the lead character Ray Kinsella (played by Kevin Costner) hears a mysterious voice whisper, “If you build it, he will come.” Acting on blind faith, Ray builds a baseball diamond in the middle of his Iowa cornfield, risking financial ruin. Against all logic, the field draws a flood of visitors.

Today, a similar “field of dreams” is being built—not with corn, but with data centers. Instead of baseball players, it is artificial intelligence (AI) models, applications, and users who are coming.

The Market’s AI Momentum

The AI boom has already reshaped markets with all three benchmarks hitting record highs. Last month, the S&P 500 climbed +1.9%, while the NASDAQ rose +1.6% and Dow Jones Industrial Average surged +3.2%. Year to date, the indexes are up +10%, +11%, and +7%, respectively.

Behind this surge lies an unprecedented wave of AI infrastructure investment. Hyperscalers—Amazon.com (AMZN), Microsoft Corp. (MSFT), Google-Alphabet (GOOGL), Meta Platforms (META), and others—are pouring hundreds of billions into AI, much of it flowing directly to NVIDIA Corp. (NVDA), the undisputed leader in GPUs (Graphic Processing Units) powering the world’s AI engines. How large is the spending? NVIDIA CEO Jensen Huang estimates $3 trillion to $4 trillion will be spent this decade to fuel the AI revolution.

Source: Visual Capitalist

The Scale of AI’s Buildout

To put this into perspective:

- Amazon is projected to spend over $100 billion in 2025 alone, more than its cumulative capital expenditures from 2000–2020 combined.

Meta is constructing its $10 billion+ Hyperion data center in Louisiana—a sprawling 4 million sq. ft. complex across 2,250 acres, powered by a $4 billion natural gas plant. The footprint is so gargantuan it could cover much of Manhattan (see graphic below).

- xAI’s Colossus, a 750,000 sq. ft. data center in Memphis, Tennessee was completed in just 122 days—equivalent to building 418 homes in half the time it normally takes to construct one house (see slide below).

Source: BOND (Global Technology Investment Firm)

This breakneck pace of spending underscores the urgency and competitive pressure driving the global AI arms race.

The Origin of the AI Floodgates Opening

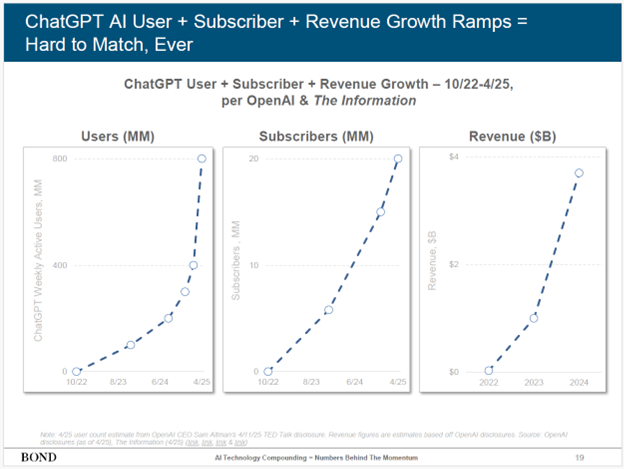

The spark was lit on November 30, 2022, when OpenAI released its LLM (large language model) called ChatGPT. Within two months, it amassed 100 million users.

Today, ChatGPT’s metrics have blasted much higher (see slide below):

- 800 million weekly active users

- 20 million paid subscribers

- $3.7 billion in revenue (as of April 2025)

Source: BOND (Global Technology Investment Firm)

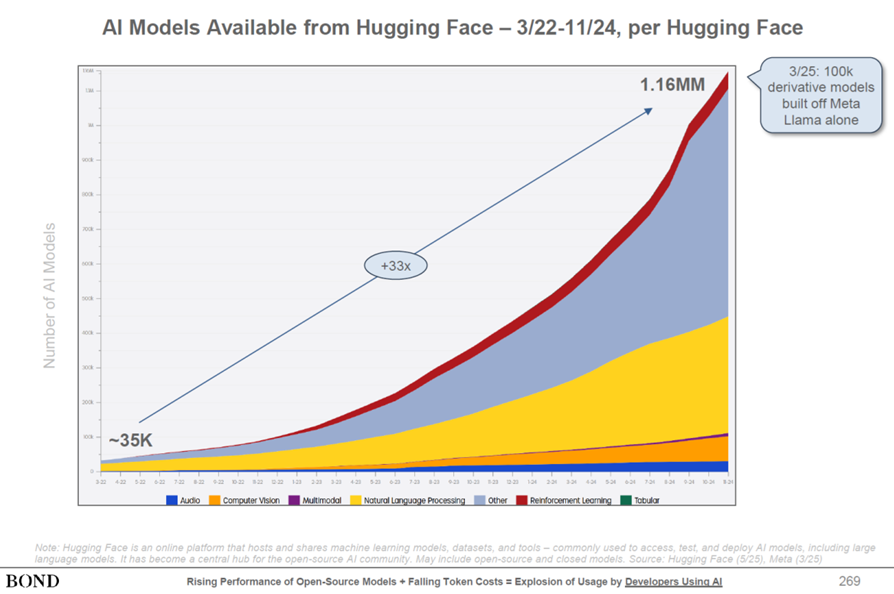

But OpenAI is far from alone. Google (Gemini), xAI (Grok), Anthropic (Claude), Meta (LLaMA), Amazon (Titan), Perplexity, and DeepSeek are all competing with their own LLMs. In total, over 1 million machine learning models now exist (see slide below) — each requiring costly compute power and pricey data centers.

Source: BOND (Global Technology Investment Firm)

Bubble or Productivity Breakthrough?

With trillions flowing into AI, a natural question arises: Is this a bubble?

Even OpenAI CEO Sam Altman admits we’re in an AI bubble :

“When bubbles happen, smart people get overexcited about a kernel of truth…Someone is going to lose a phenomenal amount of money… and a lot of people are going to make a phenomenal amount of money.”

Both realities can be true:

- Yes, hyperscalers are spending like “drunken sailors.”

- Yes, AI demand and productivity benefits are real and growing exponentially.

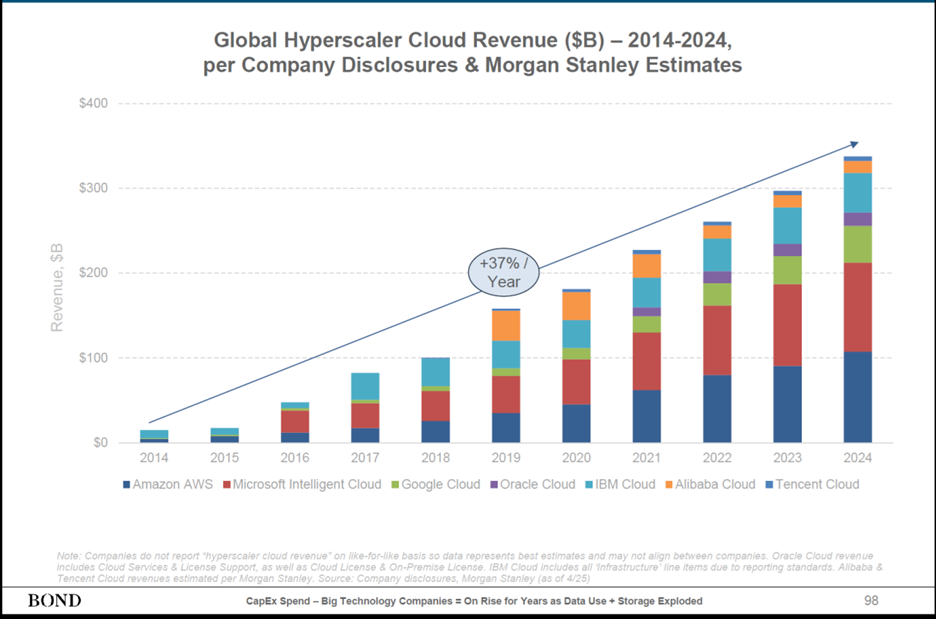

Consider the trajectory of global cloud revenues: from nearly $0 a decade ago to $300 billion today—a +37% CAGR (see chart below).

Source: BOND (Global Technology Investment Firm)

And the primary reason for cloud growth can be attributed to AI productivity benefits. A recent SAP survey found that workers using AI save nearly one hour per day on average. That’s transformative for companies: higher productivity without needing proportional hiring.

AI Use Cases Expanding Aggressively

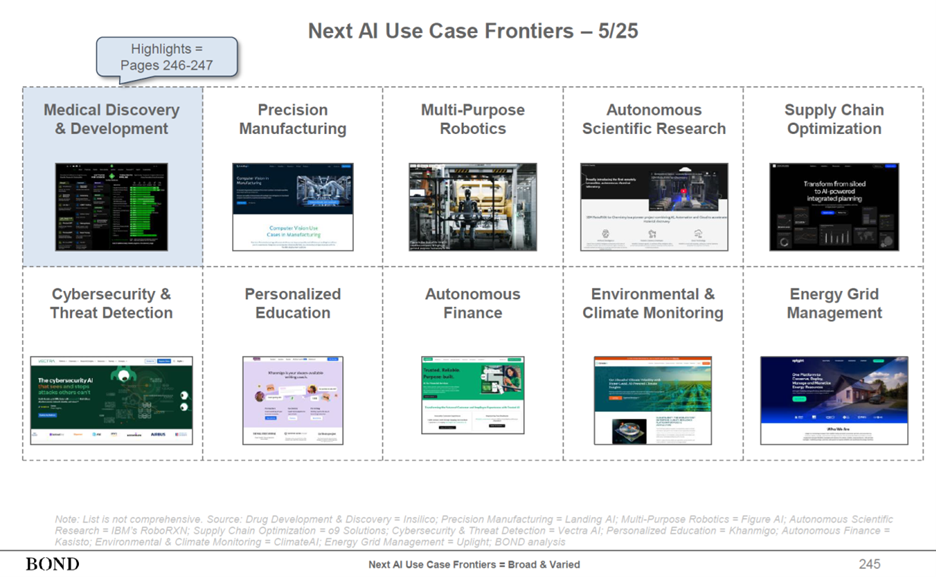

AI’s applications now span nearly every sector (see slide below):

- Technology – software engineering, code generation

- Customer Service & Marketing – customer support and call centers

- Transportation – autonomous vehicles and logistics

- Healthcare – drug discovery and development

- Supply Chains – precision manufacturing and optimization

- Automation – multi-purpose robotics

- Cybersecurity – threat detection and prevention

- Education – personalized lessons and curriculums

- Energy – grid optimization and demand forecasting

Source: BOND (Global Technology Investment Firm)

The New Field of Dreams

Throughout history, every great leap—printing press, steam engine, electricity, internet—has required massive upfront investment before the payoff arrived. AI is following the same path. Today, we are in the midst of building a new AI Field of Dreams. However, now, the data centers are the new baseball fields. And as with Ray Kinsella’s diamond, the masses are indeed coming.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in GOOGL, META, AMZN, MSFT, NVDA, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in SAP or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Mideast War an Investor Bore as Markets Soar

If I told you at the beginning of the year that the U.S. would bomb key nuclear sites in Iran, would you have guessed that Middle East stability would follow—and that global financial markets would soar to record highs? Personally, I wouldn’t have bet on that outcome. But that’s exactly what happened last month. While geopolitical dynamics remain fluid, markets shrugged off the chaos. The S&P 500 rallied +5.0%, the Dow Jones Industrial Average climbed +4.3%, and the NASDAQ catapulted +6.6%, powered largely by artificial intelligence stocks like NVIDIA Corp., which surged +16.9% for the month to a market value of $3.9 trillion (more on AI below). This is an important reminder that trading off of news headlines is a fool’s errand.

Economy Resilient Despite Tariffs and Geopolitical Turmoil

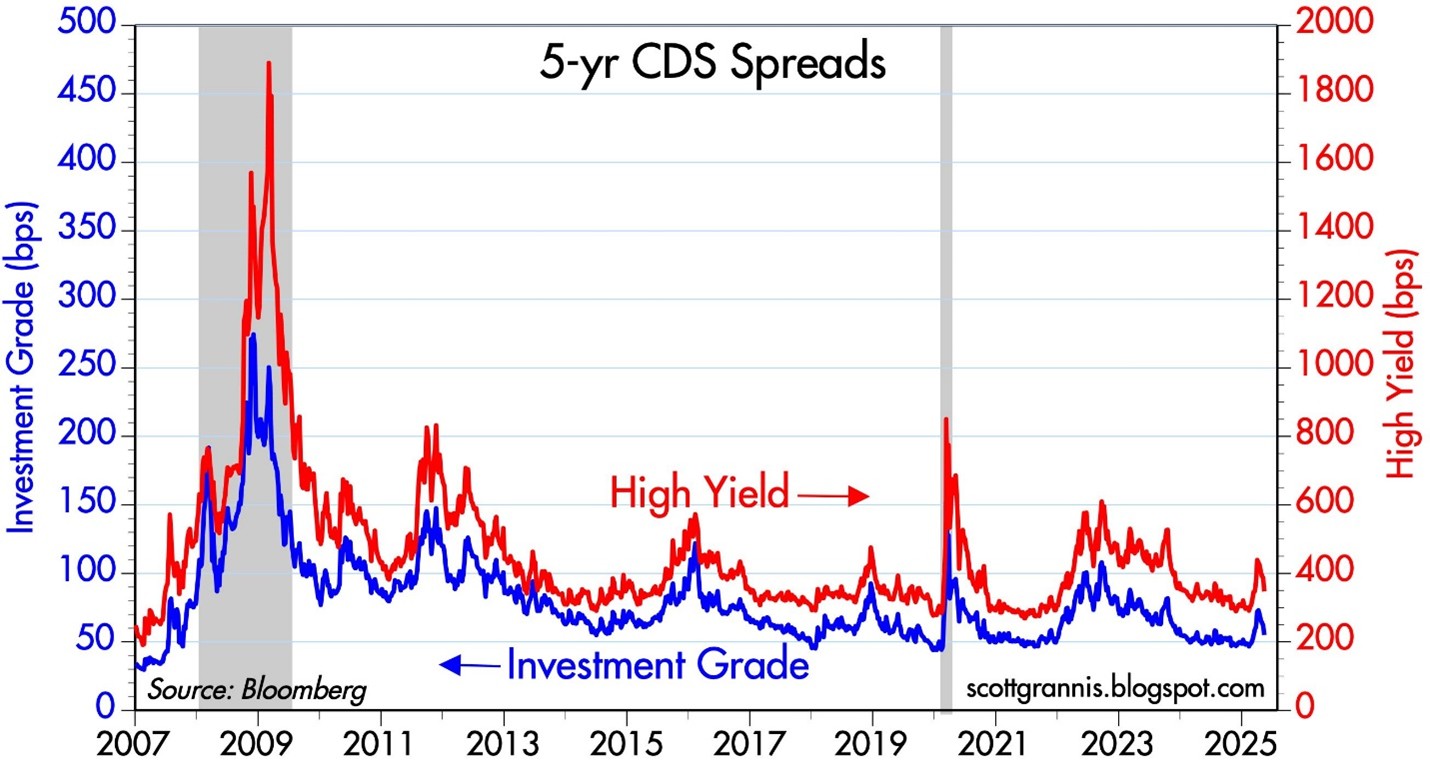

Source: Calafia Beach Pundit

Credit Default Swaps (CDS) act as insurance contracts that protect investors against corporate debt defaults. During financial stress—like the 2008 crisis or the COVID crash in 2020—CDS prices surge as investors seek protection. Today, however, CDS prices are falling across both high-yield (junk bonds) and investment-grade (Blue Chip) debt. As seen in the chart above, the cost to insure corporate bonds has declined steadily over the past two years. This signals bond investors aren’t worried about a recession or a wave of defaults, despite tariff policy uncertainty, geopolitical risk, and modest GDP growth.

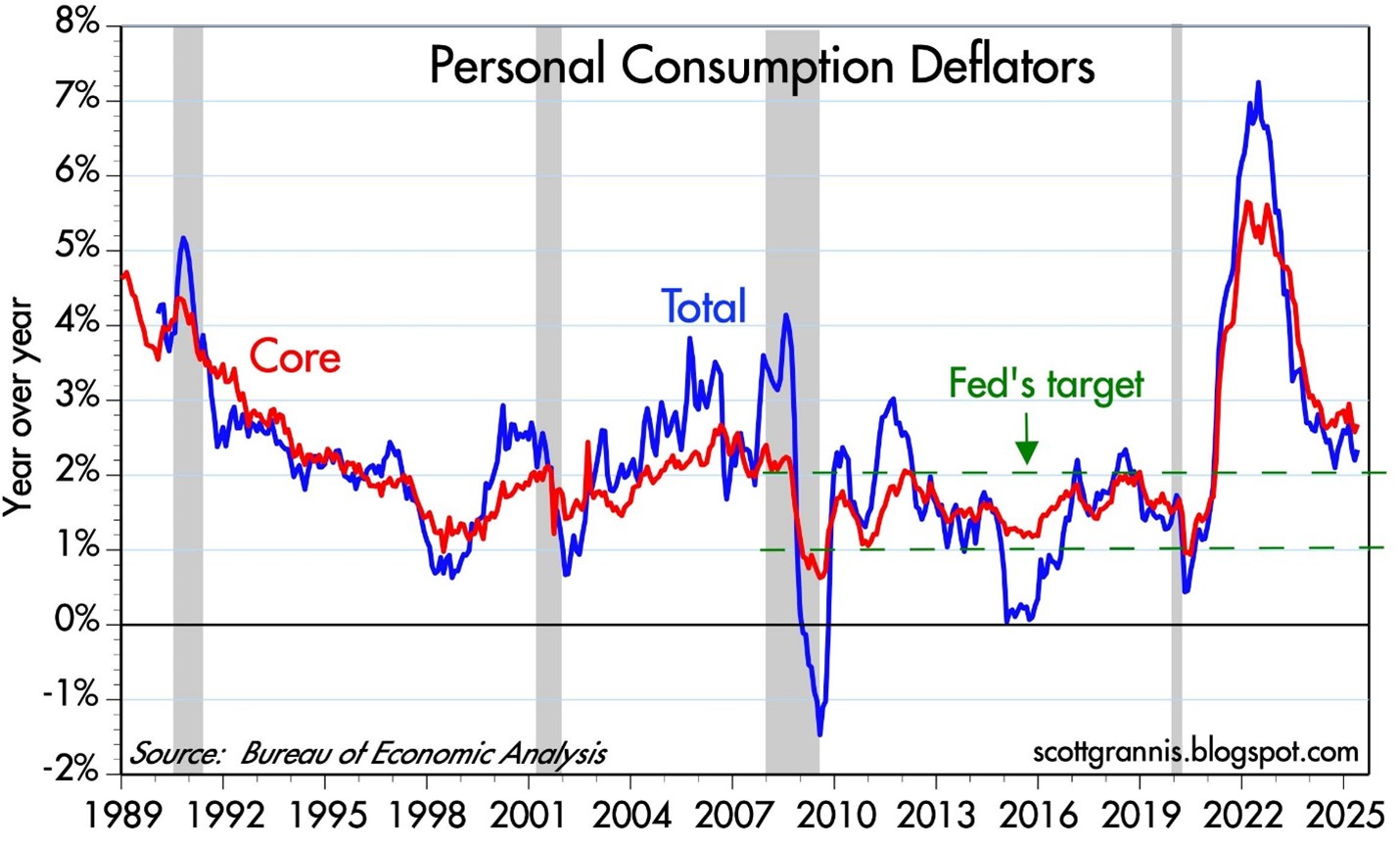

Inflation Tame as Tariffs Loom

President Trump has repeatedly criticized Fed Chair Jerome Powell for not cutting interest rates, calling him everything from a “dummy” to a “major loser” and a “stupid person” to a “numbskull”. While the name-calling is colorful, the economic pressure is real: U.S. GDP contracted -0.5% in Q1 2025. Powell, however, wants to see the full impact of upcoming tariffs before making a move. . A new tariff deadline looms on July 9th, and the market is anxiously awaiting clarity. But even if tariffs are implemented, many economists believe the inflationary impact will be temporary—what’s known as a one-time price shock.

Source: Calafia Beach Pundit

The Fed’s preferred inflation gauge—the Personal Consumption Expenditure (PCE) index—has been easing and is now near the 2% target (see chart above). With inflation cooling, Trump’s case for rate cuts gains credibility. Still, the Fed appears in no rush. It will take time to understand the lasting effects of the tariff rollout.

AI Wave Fueling Markets

For a generation, the semiconductor revolution has quietly powered innovation, guided by Moore’s Law—the principle that chip performance doubles roughly every two years (see my article The Traitorous 8). Sixty years after Gordon Moore wrote his seminal article, “Cramming More Components onto Integrated Circuits”, the power of software is catching up. NVIDIA’s Grace Blackwell GB200 chip contains an astronomical 208 billion transistors, supercharging AI software models like ChatGPT.

The AI revolution is fueling trillions in global investment and rapidly transforming industries – from data centers and self-driving cars to robotics and drug discovery. It’s important to realize that this AI arms race is not just occurring in the United States. AI investment spending extends way beyond Silicon Valley to countries like Saudi Arabia, Singapore, and China.

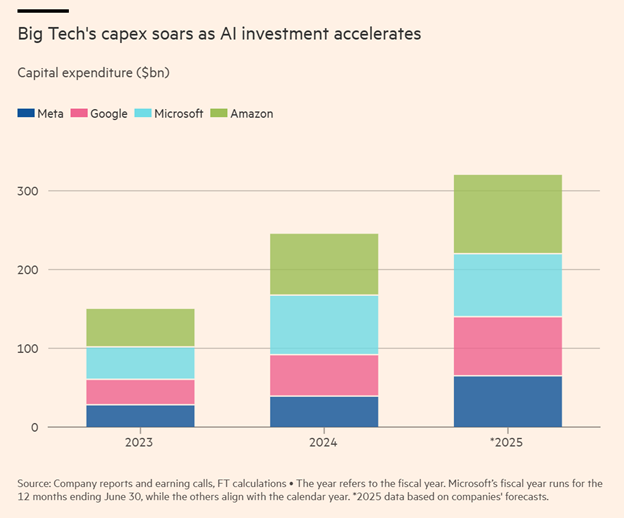

The AI boom is not a U.S.-only phenomenon. Countries like China, Saudi Arabia, and Singapore are pouring capital into AI, creating a global arms race in tech. In the U.S., the four biggest hyperscalers—Amazon, Microsoft, Google, and Meta—are projected to spend over $300 billion on capital expenditures in 2025 alone (see chart below).

To illustrate the scale: Amazon is forecasted to spend more than $100 billion in CapEx this year. For context, that’s 40% more than the company spent over the entire 2000–2020 period combined.

Source: The Financial Times

The Stargate Initiative: AI Infrastructure on a Galactic Scale

A prime example of the AI gold rush is the $500 billion Stargate initiative, with Phase 1 already underway in Abilene, Texas (see rendering below). The initial construction includes two buildings totaling 1,000,000 square feet. Ultimately, the full project will cove about 1,000 acres and be powered by an on-site natural gas facility generating 360 megawatts—enough to support 300,000 homes.

A huge portion of the project costs are dedicated to the budget for NVIDIA super chips. Oracle Corp. has committed $40 billion to purchase 400,000 of NVIDIA’s GB200 chips, making this project a centerpiece of the global AI infrastructure boom. Just this week, Oracle also announced a new $30 billion cloud deal, which will soak up a good chunk of the data center supply created by the database and enterprise software company.

Source: CoStar

The Big Picture: Volatility and Opportunity

There’s no shortage of risk—geopolitics, inflation, Fed uncertainty, tariffs. But the economy is showing surprising resilience. If tariff clarity improves, interest rate cuts materialize, and AI capital spending accelerates, a “boring” market could rapidly turn into a soaring one.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (July 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

Fink & Capitalism: Need 4 Kitchens in Your House?

Do you need four kitchens in your house? Apparently financial industry titan Larry Fink does. If Mr. Fink were a designer for millionaire homeowners, he would advise them to use their millions to build more kitchens in their house (reinvest) rather than distribute those monies to family members (dividends) or use that money to pay back an equity loan from mom and dad for the down payment (share buybacks). Essentially that is exactly what is happening in the stock market. Companies that are generating record profits and margins (millionaires) are increasingly choosing to pay out larger percentages of profits to stockholders (family members) in the form of rising dividends and share buybacks. Contrary to Mr. Fink’s belief, corporate America is actually doing plenty with room additions, landscaping, and roof replacements – I will describe more later.

As a consequence of corporate America’s increasingly shareholder friendly practices of returning cash, Fink believes this trend will stifle innovation and long-term growth in American companies. Here’s a snapshot of the supposed dividend/buyback problem Mr. Fink describes:

Source: Financial Times

Fink Mails Letter from Soapbox

For those of you who do not know who Larry Fink is, he is the successful Chairman and CEO of BlackRock Inc. (BLK), an investment manager which oversees about $4.65 trillion in investment assets. Mr. Fink ignited this recent financial controversy when he jumped on his soapbox by mailing letters to 500 CEOs lecturing them on the importance of long-term investing. What is Mr. Fink’s beef? Fink’s issues revolve around his belief that CEOs and corporations are too short-term oriented.

In his letter, Mr. Fink had this to say:

“This pressure [to meet short-term financial goals] originates from a number of sources—the proliferation of activist shareholders seeking immediate returns, the ever-increasing velocity of capital, a media landscape defined by the 24/7 news cycle and a shrinking attention span, and public policy that fails to encourage truly long-term investment.”

He goes on to bolster his argument with the following:

“More and more corporate leaders have responded with actions that can deliver immediate returns to shareholders, such as buybacks or dividend increases, while underinvesting in innovation, skilled workforces or essential capital expenditures necessary to sustain long-term growth.”

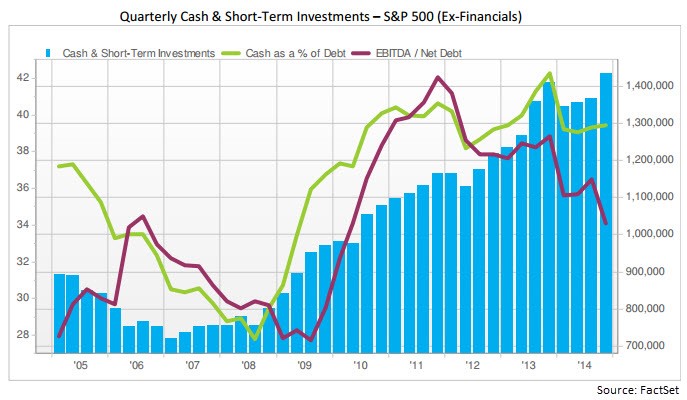

What Mr. Fink does not say in his letter is that large, multinational S&P 500 corporations driving this six-year bull run are sitting on a record hoard of cash, exceeding $1.4 trillion (see chart below). In this light, it should come as no surprise that CEOs are forking over more cash to investors in the forms of dividends and share repurchases.

What’s more, despite Fink’s assertion that share buybacks and dividends are killing innovation, he also fails to mention in his letter that 2014 capital expenditures of $730 billion are also at a record level. That’s right, CAPEX has not been cut to the bone as he implies, but rather risen to all-time highs.

It’s true that generationally low (and declining) interest rates have accelerated the pace of dividends/repurchases, however dividend payout ratios (the percentage of profits distributed to shareholders) of about 32% remain firmly below the long-term payout ratio of approximately 54% (see chart below) – see also Dividend Floodgates Widen. I find it difficult to fault many companies doing something with the gargantuan piles of inflation-losing cash anchoring their balance sheets. Don’t cash-rich companies have a fiduciary duty to borrow reasonable amounts of near-0% debt today (see Bunny Rabbit Market) in exchange for share buybacks currently providing returns of about 5.5% (inverse of 18x P/E ratio) and likely yielding 7%+ returns five years from now?

Source: Financial Times

The “Short-Term” Poster Child – Apple

There is no arguing that excessive debt eventually can catch up to a company. Our multi-year expanding economy is eventually due for another recession in the coming years, and there will be hell to pay for irresponsible, overleveraged companies. With that said, let’s take a look at the poster child of “short-termism” according to Mr. Fink …Apple Inc. (AAPL).

Of the roughly $500 billion in buybacks spent by S&P 500 companies in 2014, Apple accounted for approximately $45 billion of that figure. On top of that, CEO Tim Cook and his board generously decided to return another $11 billion to shareholders in the form of dividends. Has this “short-term” return of capital stifled innovation from the company that has launched iPhone version 6, iPad, Apple Watch, Apple Pay, and is investing into exciting areas like Apple Television, Apple Car, and who knows what else?

To put these Apple numbers into perspective, consider that last year Apple spent over $6 billion on research and development (R&D); $10 billion on capital expenditures; and hired over 12,000 new full-time employees. This doesn’t exactly sound like the death of innovation to me. Even after doling out roughly -$28 billion in expenditures and -$56 billion in dividends/share repurchases, Apple was amazingly able to keep their net cash position flat at an eye-popping +$141 billion!

Mr. Fink abhors “activist shareholders seeking immediate returns” but rather than deriding them perhaps he should send the greedy, capitalist Carl Icahn a personal thank you letter. Since Icahn’s vocal plea for a large Apple share buyback, the shares have skyrocketed about +85%, catapulting BlackRock’s ownership value in Apple to over $19 billion.

With respect to these increasing outlays, Mr. Fink also notes:

“Returning excessive amounts of capital to investors—who will enjoy comparatively meager benefits from it in this environment—sends a discouraging message.”

This would be true if investors took the dividends and stuffed them under their mattress, but an important message Mr. Fink neglects to address as it relates to dividends and share buybacks is demographics. There are 76 million Baby Boomers born between 1946 – 1964 and a Boomer is turning age 65 every 8 seconds. With many bonds trading at near 0% yields (even negative yields) it is no wonder many income starving retirees are demanding many of these cash-rich corporations to share more of the growing spoils via rising dividends.

Capitalism Works

After looking at a few centuries of our country’s history, one of the main lessons we can learn is that capitalism works – especially over the long-run. With about 200 countries across the globe, there is a reason the U.S. is #1…we’re good at capitalism. As our economy has matured over the decades, it is true our priorities and challenges have changed. It is also true that other countries may be narrowing the gap with the U.S., due to certain advantages (e.g., demographics, lower entitlements, easier regulations, etc), but the U.S. will continue to evolve.

In many respects, capitalism is very much like Darwinism – corporations either adapt with the competition…or they die. I repeatedly hear from pessimists that the U.S. is in a secular state of decline, but if that’s the case, how come the U.S. continues to dominate and innovate in major industries like biotechnology, mobile technology, networking, internet, aviation, energy, media, and transportation? Quite simply, we are the best and most experienced practitioners of capitalism.

Certainly, capitalism will continue to cultivate cyclical periods of excess investment/leverage and insufficient regulation. But guess what? Investors, including the public, eventually lose their shirts and behaviors/regulations adjust. At least for a little while, until the next period of excess takes hold. If Apple, and other balance sheet healthy companies allocate capital irresponsibly, capital will flow towards more aggressive and innovative companies. BlackBerry Limited (BBRY) knows a little bit about the consequences of cutthroat competition and suboptimal capital allocation.

While I emphatically share Mr. Fink’s focus on long-term investing values (including his self-serving tax reform ideas), I vigorously disagree with his attacks on shareholder friendly actions and his characterization of rising dividends/buybacks as short-term in nature. In fact, increasing dividends and share buybacks can very much coexist as a long-term investment and capital allocation strategy.

The question of proper capital allocation should have more to do with the age of a company. It only makes sense that younger companies on average should reinvest more of their profits into growth and innovation. On the other hand, more mature S&P 500-like companies will be in a better position to distribute higher percentages of profits to shareholders – especially as cash levels continue to rise to record levels and leverage remains in check.

BlackRock’s Larry Fink may continue to urge CEOs to reinvest their growing cash hoards into superfluous corporate kitchens, but Sidoxia and other prudent capitalist investors will continue to exhort CEOs to opportunistically take advantage of near-free borrowing rates and responsibly share the accretive gains with shareholders. That’s a message Mr. Fink should include in a letter to CEOs – he can use BlackRock’s lofty, above-average dividend to cover the cost of postage.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including AAPL and iShares ETFs, but at the time of publishing, SCM had no direct position in BLK, BBRY or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Short Arms, Deep Pockets

")

Companies have deep pockets flush with cash, but are plagued with short arms, unwilling to reach into their wallets to make substantive new hires. I have talked about “unemployment hypochondria” in the past but is this cautious behavior rational?

The short answer is yes, and it is very typical in light of the similar “jobless recoveries” we experienced in 1991 and 2001. After suffering the worst financial crisis in a generation, employers’ wounds are still not completely healed and the frightening memories of 2008-2009 are still fresh in their minds.

Linchpin Labor

The globalization cat is out of the bag, and technology is only accelerating the commoditization of labor. When labor can be purchased for $1 per hour in China or $.50 per hour in India , and in many instances no strategic benefit lost, then why are so many people surprised about the hemorrhaging of $25 per hour manufacturing jobs to cheaper locales? Agriculture and related industries used to account for more than 90% of our economy about 150 years ago – today agriculture makes up about 2% of our economic output. Even though this dominating sector withered away on a relative basis, the United States became the global powerhouse innovator of the 20th century.

Innovative companies understand that true value is created by those workers who make themselves indispensable – or what Seth Godin calls “Linchpins.” Apple Inc. (AAPL) understands these trends. If you don’t believe me, just flip over an iPhone and read where it clearly states, “Designed by Apple in California. Assembled in China.” (see BELOW).

We are falling further behind our global brethren in math and science, and our immigration policy is all backwards (Keys to Success). Education, creativity, ingenuity, and entrepreneurial spirit are the main ingredients necessary to climb the labor food chain. For those workers that make themselves linchpins, their services will be in demand during good times and bad times.

Jobs = Heavy Hiking Boots

Like scared hikers jettisoning heavy hiking boots to escape a pursuing grizzly bear, business owners will eventually need to purchase a new pair of boots, if they want to hike the mountain to face the next challenge. Right now, businesses are content waiting it out, more worried about the potential of a bear jumping out to devour them.

Although businesses may not be plunging into hiring a substantial number of new workers, positive leading indicators are becoming more apparent. Beyond the obvious improvement in the explicit job numbers (e.g., nine consecutive months of private job creation), other factors such as increased temporary workers, accelerating job listings, and increased capital expenditures are the precursors to sustained job hiring.

Quarterly Capital Carrots

Capital expenditures generally lead to more immediate productivity improvements and do not have a complete negative and immediate impact on the sacred EPS (earnings per share) and income statement metrics. On the other hand, hiring a new employee has an instant depressing effect on expenses, thereby dragging down the beloved EPS figure. What’s more, new employees do not typically become productive or sales generative for months. If you consider the heavy explicit wages coupled with implicit training costs, until the coast is clear and confidence overcomes fear, businesses are not going to dip their hands into their cash-filled pockets to hire workers willy-nilly.

As previously mentioned, improved business confidence is being signaled by increased capital spending. Just over the last week, investors have witnessed significantly expanded capital expenditures across a broad array of industries. Here are a few random samplings:

September 2010 – Quarterly Capital Expenditures

Q3 – 2010 Q3 – 2009 YOY%

Apple Inc. (AAPL) $760 mil vs. $459 mil +66%

Halliburton Company (HAL) $557 mil vs. $440 mil +27%

Coca Cola Company (KO) $442 mil vs. $419 mil +5%

Dominos Pizza Inc. (DPZ) $5.2 mil vs. $4.1 mil +26%

Intel Corp. (INTC) $1.4 bill vs $944 mil +44%

Although the pace of the recovery is losing steam, companies’ health persists to strengthen, as evidenced in part by the +45% growth in 2010 S&P 500 profits, swelling record cash piles, and increasing corporate confidence (rising capital expenditures). Despite these positive leading indicators, business owners are reluctant to dip their short arms into their deep cash-filled pockets to hire new employees. Given our experience over the last few decades this corporate behavior is perfectly consistent with recent jobless recoveries. Until its clear the economic bear is hibernating, businesses will continue building their cash warchests. Everyone will be happier once we are done running from bears, and instead chasing bulls.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, but at the time of publishing SCM had no direct position in HAL, KO, DPZ, INTC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Taking Facebook and Twitter Public

Facebook CEO Mark Zuckerberg

Valuing high growth companies is similar to answering a typical open-ended question posed to me during business school interviews: “Wade, how many ping pong balls can you fit in an empty 747 airplane?” Obviously, the estimation process is not an exact science, but rather an artistic exercise in which various techniques and strategies may be implemented to form a more educated guess. The same estimation principles apply to the tricky challenge of valuing high growth companies like Facebook and Twitter.

Cash is King

Where does one start? Conceptually, one method used to determine a company’s value is by taking the present value of all future cash flows. For growth companies, earnings and cash flows can vary dramatically and small changes in assumptions (i.e., revenue growth rates, profit margins, discount rates, taxes, etc.) can lead to drastically different valuations. As I have mentioned in the past, cash flow analysis is a great way to value companies across a broad array of industries – excluding financial companies (see previous article on cash flow investing).

Mature companies operating in stable industries may be piling up cash because of limited revenue growth opportunities. Such companies may choose to pay out dividends, buyback stock, or possibly make acquisitions of target competitors. However, for hyper-growth companies earlier in their business life-cycles, (e.g., Facebook and Twitter), discretionary cash flow may be directly reinvested back into the company, and/or allocated towards numerous growth projects. If these growth companies are not generating a lot of excess free cash flow (cash flow from operations minus capital expenditures), then how does one value such companies? Typically, under a traditional DCF (discounted cash flow model), modest early year cash flows are forecasted until more substantial cash flows are generated in the future, at which point all cash flows are discounted back to today. This process is philosophically pure, but very imprecise and subject to the manipulation and bias of many inputs.

To combat the multi-year wiggle room of a subjective DCF, I choose to calculate what I call “adjusted free cash flow” (cash flow from operations minus depreciation and amortization). The adjusted free cash flow approach provides a perspective on how much cash a growth company theoretically can generate if it decides to not pursue incremental growth projects in excess of maintenance capital expenditures. In other words, I use depreciation and amortization as a proxy for maintenance CAPEX. I believe cash flow figures are much more reliable in valuing growth companies because such cash-based metrics are less subject to manipulation compared to traditional measures like earnings per share (EPS) and net income from the income statement.

Rationalizing Ratios

Other valuation methods to consider for growth companies*:

- PE Ratio: The price-earnings ratio indicates how expensive a stock is by comparing its share price to the company’s earnings.

- PEG Ratio (PE-to-Growth): This metric compares the PE ratio to the earnings growth rate percentage. As a rule of thumb, PEG ratios less than one are considered attractive to some investors, regardless of the absolute PE level.

- Price-to-Sales: This ratio is less precise in my mind because companies can’t pay investors dividends, buy back stock, or make acquisitions with “sales” – discretionary capital comes from earnings and cash flows.

- Price-to-Book: Compares the market capitalization (price) of the company with the book value (or equity) component on the balance sheet.

- EV/EBITDA: Enterprise value (EV) is the total value of the market capitalization plus the value of the debt, divided by EBITDA (Earnings Before Interest Taxes Depreciation and Amortization). Some investors use EBITDA as an income-based surrogate of cash flow.

- FCF Yield: One of my personal favorites – you can think of this percentage as an inverted PE ratio that substitutes free cash flow for earnings. Rather than a yield on a bond, this ratio effectively provides investors with a discretionary cash yield on a stock.

*All The ratios above should be reviewed both on an absolute basis and relative basis in conjunction with comparable companies in an industry. Faster growing industries, in general, should carry higher ratio metrics.

Taking Facebook and Twitter Public

Before we can even take a stab at some of these growth company valuations, we need to look at the historical financial statements (income statement, balance sheet, and cash flow statement). In the case of Facebook and Twitter, since these companies are private, there are no publically available financial statements to peruse. Private investors are generally left in the dark, limited to public news related to what other early investors have paid for ownership stakes. For example, in July, a Russian internet company paid $100 million for a stake in Facebook, implying a $6.5 billion valuation for the total company. Twitter recently obtained a $100 million investment from T. Rowe Price and Insight Venture Partners thereby valuing the total company at $1 billion.

Valuing growth companies is quite different than assessing traditional value companies. Because of the earnings and cash flow volatility in growth companies, the short-term financial results can be distorted. I choose to find market leading franchises that can sustain above average growth for longer periods of time (i.e., companies with “long runways”). For a minority of companies that can grow earnings and cash flows sustainably at above-average rates, I will take advantage of the perception surrounding current short-term “expensive” metrics, because eventually growth will convert valuation perception to “cheap.” Google Inc. (GOOG) is a perfect example – what many investors thought was ridiculously expensive, at the $85 per share Initial Public Offering (IPO) price, ended up skyrocketing to over $700 per share and continues to trade near a very respectable level of $500 per share.

The IPO market is heating up and A123 Systems Inc (AONE) is a fresh example. Often these companies are volatile growth companies that require a deep dive into the financial statements. There is no silver bullet, so different valuation metrics and techniques need to be reviewed in order to come up with more reasonable valuation estimates. Valuation measuring is no cakewalk, but I’ll take this challenge over estimating the number of ping pong balls I can fit in an airplane, any day. Valuing growth companies just requires an understanding of how the essential earnings and cash flow metrics integrate with the fundamental dynamics surrounding a particular company and industry. Now that you have graduated with a degree in Growth Company Valuation 101, you are ready to open your boutique investment bank and advise Facebook and Twitter on their IPO price (the fees can be lucrative if you are not under TARP regulations).

DISCLOSURE: Sidoxia Capital Management and client accounts do not have direct long positions AONE, however some Sidoxia client accounts do hold GOOG securities at the time this article was published. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}