Posts tagged ‘buy and hold’

Market Drops as GameStop Pops

The stock market started with a bang this year with the S&P 500 index at first climbing +3% in January before ending with a whimper and a monthly decline of -1%. This performance followed a strong finish to a wild 2020 presidential election year (the S&P 500 rose +16%). There has been plenty of focus on the coronavirus health crisis and vaccine distribution (100 million doses in 100 days), along with debates over a $1.9 trillion proposed relief package by newly elected President Joe Biden, but there has been another story stealing attention in the financial market headlines…GameStop.

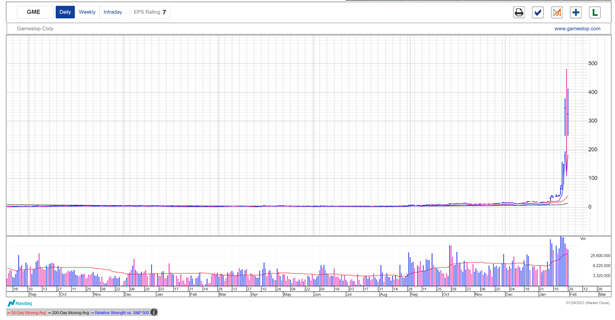

If a global pandemic and a populist attack on the Capitol were not enough for investors, the Reddit (WallStreetBets) and Robinhood revolution coordinated a mass attack on privileged hedge funds and short sellers by squeezing out-of-favor stocks like GameStop (Ticker: GME) to stratospheric levels (up +1,625% to $325/share in January alone) causing an estimated $20 billion of losses for many wealthy elites. To put the meteoric rise into perspective, before GameStop shares reached $325, the stock was valued below $20/share last month and has climbed more than 100x-fold from a low $2.57/share nine months ago (see chart below).

What Exactly Happened?

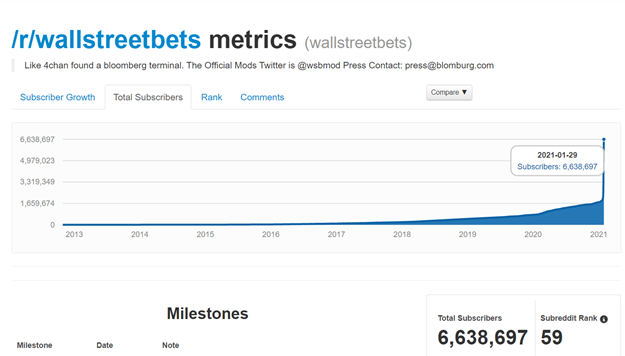

Well, millions of users on the social media platform Reddit banded together on a forum called “wallstreetbets” (see graphic below). WallStreetBets was established in 2012 and had approximately 1 million subscribers at the beginning of 2021 – today it has more than 7 million subscribers. Millions of these anti-establishment WallStreetBets followers effectively colluded together to inflate the share price of GameStop by ganging up on the many short sellers who were betting that GameStop share price would drop. In other words, Reddit-Robinhood buyer gains led to short seller losses. One hedge fund in particular, Melvin Capital, lost billions of dollars on its GameStop short bet and saw its fund performance decline by a whopping -53% in one month…ouch!

The Reddit WallStreetBets forum may have served as the match in this wildfire, but in order to trigger an inferno, a brokerage account is needed. A trading platform allows individual traders on Reddit to level the playing field against the hedge fund professionals and short sellers. The fuel for the GameStop detonation was Robinhood, a fintech (Financial Technology) brokerage firm founded in Silicon Valley in 2013 by two Stanford University graduates. The mission of the company is to “democratize finance for all.” But let’s not forget what Thomas Jefferson noted, “A democracy is nothing more than mob rule, where fifty-one percent of the people may take away the rights of the other forty-nine.” The Reddit-Robinhood mob certainly proved this point.

Although Robinhood was initially seen as a saint in the free trading revolution, eventually many of the brokerage company’s disciples became disenfranchised. Many users subsequently turned on the company and considered Robinhood a villain that was rigging the system when CEO Vlad Tenev halted the ability of its 13+ million users to buy GameStop shares.

Many traders came to the conclusion that Robinhood was working to save the perceived hedge fund bad guys by the firm temporarily terminating user purchases in GameStop stock. Mr. Tenev blamed regulatory capital requirements as a reason for disallowing Robinhood-ers to buy GameStop last week, which was a major contributing factor to why the stock price plummeted by -44% on January 28th. The following day, Robinhood partially reversed its stance and subsequently allowed minimal daily purchases of one share.

How Does Short Selling Work?

In the stock market, you can make gains by buying shares that go up in price, or you can make profits by short selling shares that go down in price. If you buy a stock, the most money you could lose is -100% of your original investment. For example, if you invest $1,000 into GameStop stock by buying 50 shares at $20 each, if the stock price goes to $0, the most the investor/trader could lose is 100% of their $1,000 original investment.

On the flip side, if you short a stock, the potential losses are limitless. For example, if you (or a hedge fund manager) shorts $1,000 of GameStop stock by selling 50 shares short at $20 each, if the stock price goes to $60, the short seller just loss -200% of their original investment [($20/shr – $60/shr) X 50 shares] = -$2,000. If GameStop goes to $100, the short seller loses -400%, and if GameStop price goes to $220, the short seller loses -1,000%. As you can see, the higher the price goes, there are infinite potential losses of the investor, trader, or hedge fund manager.

If a stock price continues to move higher, the only way for a short seller to stop the bleeding (i.e., close their short position or “bet”) is to buy shares. As a reminder, a buyer of stock closes their position by selling shares after they originally buy shares. A short seller closes their position by buying shares after they initially sell shares short. So again, if GameStop share price continues to move higher, the only way for GameStop short sellers to stop their losses is to buy more GameStop shares. This is the equivalent of pouring gasoline on a blazing fire because as millions of Reddit/Robinhood-ers are pushing GameStop’s share price higher almost every day, short selling hedge fund managers are left scrambling for the exits and forced to close their positions at even higher prices (i.e., larger losses).

What Does This All Mean?

Whether you are talking about speculation in Bitcoin, the rise of SPACs (Special Purpose Acquisition Companies), the increase in the number of IPOs (Initial Public Offerings), or the Reddit-Robinhood Revolution, risk appetite has been on the rise and long-term investors should proceed very cautiously. Just as many have experienced on trips to Las Vegas, big winnings can quickly turn to huge losses. Although it’s certainly fun to watch the individual Davids take down the hedge fund/short selling Goliaths, if the Reddit-Robinhood community gets too aggressive in its speculation, history shows us they will end up being the ones swimming in their tears or stoned to death.

If you need assistance navigating through all these land mines, please give us a call at Sidoxia Capital Management (949-258-4322) for a complimentary portfolio review.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (February 1, 2021). Subscribe on the right side of the page for the complete text.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in GME, AMC, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Re-Questioning the Death of Buy & Hold Investing

Article originally posted September 17, 2010: At the time this original article was written, the Dow Jones Industrial Average was hovering around 11,500. Last week, the Dow closed at 20,624. Sure there have been plenty of ups and downs since 2010, but as I suggested seven years ago, perhaps “buy and hold” still is not dead today?

In the midst of the so-called “Lost Decade,” pundits continue to talk about the death of “buy and hold” (B&H) investing. I guess it probably makes sense to define B&H first before discussing it, but like most amorphous financial concepts, there is no clear cut definition. According to some strict B&H interpreters, B&H means buy and hold forever (i.e., buy today and carry to your grave). For other more forgiving Wall Street lexicon analysts, B&H could mean a multi-year timeframe. However, with the advent of high frequency trading (HFT) and supercomputers, the speed of trading has only accelerated further to milliseconds, microseconds, and even nanoseconds. Pretty soon B&H will be considered buying a stock and holding it for a day! Average mutual fund turnover (holding periods) has already declined from about 6 years in the 1950s to about 11 months in the 2000s according to John Bogle.

Technology and the lower costs associated with trading advancements arre obviously a key driver to shortened investment horizons, but even after these developments, professionals success in beating the market is less clear. Passive gurus Burton Malkiel and John Bogle have consistently asserted that 75% or more of professional money managers underperform benchmarks and passive investment vehicles (e.g., index funds and exchange traded funds).

This is not the first time that B&H has been held for dead. For example, BusinessWeek ran an article in August 1979 entitled The Death of Equities (see Magazine Cover article), which aimed to eradicate any stock market believers off the face of the planet. Sure enough, just a few years later, the market went on to advance on one of the greatest, if not the greatest, multi-decade bull market run in history. People repudiated themselves from B&H back then, and while B&H was in vogue during the 1980s and 1990s it is back to becoming the whipping boy today.

Excuse Me, But What About Bonds?

With all this talk about the demise of B&H and the rise of the HFT machines, I can’t help but wonder why B&H is dead in equities but alive and screaming in the bond market? Am I not mistaken, but has this not been the largest (or darn near largest) thirty-year bull market in bonds? The Federal Funds Rate has gone from 20% in 1981 to 0% thirty years later. Not a bad period to buy and hold, but I’m going to go out on a limb and say the Fed Funds won’t go from 0% to a negative -20% over the next thirty years.

Better Looking Corpse

There’s no denying the fact that equities have been a lousy place to be for the last ten years, and I have no clue what stocks will do for the next twelve months, but what I do know is that stocks offer a completely different value proposition today. At the beginning of the 2000, the market P/E (Price Earnings) valued earnings at a 29x multiple with the 10-year Treasury Note trading with a yield of about 6%. Today, the market trades at 13.5 x’s 2010 earnings estimates (12x’s 2011) and the 10-Year is trading at a level less than half the 2000 rate (2.75% today). Maybe stocks go nowhere for a while, but it’s difficult to dispute now that equities are at least much more attractive (less ugly) than the prices ten years ago. If B&H is dead, at least the corpse is looking a little better now.

As is usually the case, most generalizations are too simplistic in making a point. So in fully reviewing B&H, perhaps it’s not a bad idea of clarifying the two core beliefs underpinning the diehard buy and holders:

1) Buying and holding stocks is only wise if you are buying and holding good stocks.

2) Buying and holding stocks is not wise if you are buying and holding bad stocks.

Even in the face of a disastrous market environment, here are a few stocks that have met B&H rule #1:

Maybe buy and hold is not dead after all? Certainly, there have been plenty of stinking losing stocks to offset these winners. Regardless of the environment, if proper homework is completed, there is plenty of room to profitably resurrect stocks that are left for a buy and hold death by the so-called pundits.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: At the time the article was originally written, Sidoxia Capital Management (SCM) and some of its clients owned certain exchange traded funds and AAPL, AMZN, ARMH, and NFLX, but at the time of publishing SCM had no direct position in GGP, APKT, KRO, AKAM, FFIV, OPEN, RVBD, BIDU, PCLN, CRM, FLS, GMCR, HANS, BYI, SWN (*2,901% is correct %), CTSH, CMI, ISRG, ESRX, or any other security referenced in this article. As of 2/19/17 – Sidoxia owned AAPL, AMZN, and was short NFLX. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

10 Ways to Destroy Your Portfolio

![]()

With the increased frequency of heightened volatility, investing has never been as challenging as it is today. However, the importance of investing has never been more crucial either, due to rising life expectancies, corrosive effects of inflation, and the uncertainty surrounding the sustainability of government programs like Social Security, Medicare, and pensions.

If you are not wasting enough money from our structurally flawed and loosely regulated investment industry that is inundated with conflicts of interest, here are 10 additional ways to destroy your investment portfolio:

#1. Watch and React to Sensationalist News Stories: Typically, strategists and pundits do a wonderful job of parroting the consensus du jour. With the advent of the internet, and 24/7 news cycles, it is difficult to not get caught up in the daily vicissitudes. However, the accuracy of the so-called media experts is no better than weather forecasters’ accuracy in predicting the weather three Saturdays from now at 10:23 a.m. Investors would be better served by listening to and learning from successful, seasoned veterans (see Investing Caffeine Profiles).

#2. Invest for the Short-Term and Attempt Market Timing: Investing is a marathon, and not a sprint, yet countless investors have the arrogance to believe they can time the market. A few get lucky and time the proper entry point, but the same investors often fail to time the appropriate exit point. The process works similarly in reverse, which hammers home the idea that you can be 200% wrong when you are constantly switching your portfolio positions.

#3. Blindly Invest Without Knowing Fees: Like a dripping faucet, fees, transaction costs, taxes, and other charges may not be noticeable in the short-run, but combined, these portfolio expenses can be devastating in the long-run. Whether you or your broker/advisor knowingly or unknowingly is churning your account, the practice should be immediately halted. Passive investment products and strategies like ETFs (Exchange Traded Funds), index funds, and low turnover (long time horizon / tax-efficient) investing strategies are the way to go for investors.

#4. Use Technical Analysis as a Primary Strategy: Warren Buffett openly recognizes the problem with technical analysis as evidenced by his statement, “I realized technical analysis didn’t work when I turned the charts upside down and didn’t get a different answer.” Legendary fund manager Peter Lynch adds, “Charts are great for predicting the past.” Most indicators are about as helpful as astrology, but in rare instances some facets can serve as a useful device (like a Lob Wedge in golf).

#5. Panic-Sell out of Fear & Panic-Buy out of Greed: Emotions can devastate portfolio returns when investors’ trading activity follows the herd in good times and bad. As the old saying goes, “The herd is lead to the slaughterhouse.” Gary Helms rightly identifies the role that overconfidence plays when ininvesting when he states,”If you have a great thought and write it down, it will look stupid 10 hours later.” The best investment returns are earned by traveling down the less followed path. Or as Rob Arnott describes, “In investing, what is comfortable is rarely profitable.” Get a broad range of opinions and continually test your investment thesis to make sure peer pressure is not driving key investment decisions.

#6. Ignore Valuation and Yield: Valuation is like good pitching in baseball…very important. Valuation may not cause all of your investments to win, but this factor should be an integral part of your investment process. Successful investors think about valuation similarly to skilled sports handicappers. Steven Crist summed it up beautifully when he said, “There are no ‘good’ or ‘bad’ horses, just correctly or incorrectly priced ones.” The same principle applies to investments. Dividends and yields should not be overlooked – these elements are an essential part of an investor’s long-run total return.

#7. Buy and Forget: “Buy-and-hold” is good for stocks that go up in price, and bad for stocks that go flat or decline in value. Wow, how deeply profound. As I have written in the past, there are always reasons of why you should not invest for the long-term and instead sell your position, such as: 1) new competition; 2) cost pressures; 3) slowing growth; 4) management change; 5) excessive valuation; 6) change in industry regulation; 7) slowing economy; 8 ) loss of market share; 9) product obsolescence; 10) etc, etc, etc. You get the idea.

#8. Over-Concentrate Your Portfolio: If you own a top-heavy portfolio with large weightings, sleeping at night can be challenging, and also force average investors to make bad decisions at the wrong times (i.e., buy high and sell low). While over-concentration can be risky, over-diversification can eat away at performance as well – owning a 100 different mutual funds is costly and inefficient.

#9. Stuff Money Under Your Mattress: With interest rates at the lowest levels in a generation, stuffing money under the mattress in the form of CDs (Certificates of Deposit), money market accounts, and low-yielding Treasuries that are earning next to nothing is counter-productive for many investors. Compounding this problem is inflation, a silent killer that will quietly disintegrate your hard earned investment portfolio. In other words, a penny saved inefficiently will lead to a penny depreciating rapidly.

#10. Forget Your Mistakes: Investing is difficult enough without naively repeating the same mistakes. As Albert Einstein said, “Insanity is doing the same thing, over and over again, but expecting different results.” Mistakes will be made and it behooves investors to document them and learn from them. Brushing your mistakes under the carpet may make you temporarily feel better emotionally, but will not help your financial returns.

As the year approaches a close, do yourself a favor and evaluate whether you are committing any of these damaging habits. Investing is tough enough already, without adding further ways of destroying your portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Playing the Field with Your Investments

For some, casually dating can be fun and exciting. The same goes for trading and speculating – the freedom to make free- wheeling, non-committal purchases can be exhilarating. Unfortunately the costs (fiscally and emotionally) of short-term dating/investing often outweigh the benefits.

Fortunately, in the investment world, you can get to know an investment pretty well through fundamental research that is widely available (e.g., 10Ks, 10Qs, press releases, analyst days, quarterly conference calls, management interviews, trade rags, research reports). Unlike dating, researching stocks can be very cheap, and you do not need to worry about being rejected.

Dating is important early in adulthood because we make many mistakes choosing whom we date, but in the process we learn from our misjudgments and discover the important qualities we value in relationships. The same goes for stocks. Nothing beats experience, and in my long investment career, I can honestly say I’ve dated/traded a lot of pigs and gained valuable lessons that have improved my investing capabilities. Now, however, I don’t just casually date my investments – I factor in a rigorous, disciplined process that requires a serious commitment. I no longer enter positions lightly.

One of my investment heroes, Peter Lynch, appropriately stated, “In stocks as in romance, ease of divorce is not a sound basis for commitment. If you’ve chosen wisely to begin with, you won’t want a divorce.”

Charles Ellis shared these thoughts on relationships with mutual funds:

“If you invest in mutual funds and make mutual funds investment changes in less than 10 years…you’re really just ‘dating.’ Investing in mutual funds should be marital – for richer, for poorer, and so on; mutual fund decisions should be entered into soberly and advisedly and for the truly long term.”

No relationship comes without wild swings, and stocks are no different. If you want to survive the volatile ups and downs of a relationship (or stock ownership), you better do your homework before blindly jumping into bed. The consequences can be punishing.

Buy and Hold is Dead…Unless Stocks Go Up

If you are serious about your investments, I believe you must be mentally willing to commit to a relationship with your stock, not for a day, not for a week, or not for a month, but rather for years. Now, I know this is blasphemy in the age when “buy-and-hold” investing is considered dead, but I refute that basic premise whole-heartedly…with a few caveats.

Sure, buy-and-hold is a stupid strategy when stocks do nothing for a decade – like they have done in the 2000s, but buying and holding was an absolutely brilliant strategy in the 1980s and 1990s. Moreover, even in the miserable 2000s, there have been many buy-and-hold investments that have made owners a fortune (see Questioning Buy & Hold ). So, the moral of the story for me is “buy-and-hold” is good for stocks that go up in price, and bad for stocks that go flat or down in price. Wow, how deeply profound!

To measure my personal commitment to an investment prospect, a bachelorette investment I am courting must pass another test…a test from another one of my investment idols, Phil Fisher, called the three-year rule. This is what the late Mr. Fisher had to say about this topic:

“While I realized thoroughly that if I were to make the kinds of profits that are made possible by [my] process … it was vital that I have some sort of quantitative check… With this in mind, I established what I called my three-year rule.” Fisher adds, “I have repeated again and again to my clients that when I purchase something for them, not to judge the results in a matter of a month or a year, but allow me a three year period.”

Certainly, there will be situations where an investment thesis is wrong, valuation explodes, or there are superior investment opportunities that will trigger a sale before the three-year minimum expires. Nonetheless, I follow Fisher’s rule in principle in hopes of setting the bar high enough to only let the best ideas into both my client and personal portfolios.

As I have written in the past, there are always reasons of why you should not invest for the long-term and instead sell your position, such as: 1) new competition; 2) cost pressures; 3) slowing growth; 4) management change; 5) valuation; 6) change in industry regulation; 7) slowing economy; 8 ) loss of market share; 9) product obsolescence; 10) etc, etc, etc. You get the idea.

Don Hays summed it up best: “Long term is not a popular time-horizon for today’s hedge fund short-term mentality. Every wiggle is interpreted as a new secular trend.”

Peter Lynch shares similar sympathies when it comes to noise in the marketplace:

“Whatever method you use to pick stocks or stock mutual funds, your ultimate success or failure will depend on your ability to ignore the worries of the world long enough to allow your investments to succeed.”

Every once in a while there is validity to some of the concerns, but more often than not, the scare campaigns are merely Chicken Little calling for the world to come to an end.

Patience is a Virtue

In the instant gratification society we live in, patience is difficult to come by, and for many people ignoring the constant chatter of fear is challenging. Pundits spend every waking hour trying to explain each blip in the market, but in the short-run, prices often move up or down irrespective of the daily headlines. Explaining this randomness, Peter Lynch said the following:

“Often, there is no correlation between the success of a company’s operations and the success of its stock over a few months or even a few years. In the long term, there is a 100% correlation between the success of a company and the success of its stock. It pays to be patient, and to own successful companies.”

Long-term investing, like long-term relationships, is not a new concept. Investment time horizons have been shortening for decades, so talking about the long-term is generally considered heresy. Rather than casually date a stock position, perhaps you should commit to a long-term relationship and divorce your field-playing habits. Now that sounds like a sweet kiss of success.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Playing the Field with Your Investments

For some, casually dating can be fun and exciting. The same goes for trading and speculating – the freedom to make free- wheeling, non-committal purchases can be exhilarating. Unfortunately the costs (fiscally and emotionally) of short-term dating/investing often outweigh the benefits.

Fortunately, in the investment world, you can get to know an investment pretty well through fundamental research that is widely available (e.g., 10Ks, 10Qs, press releases, analyst days, quarterly conference calls, management interviews, trade rags, research reports). Unlike dating, researching stocks can be very cheap, and you do not need to worry about being rejected.

Dating is important early in adulthood because we make many mistakes choosing whom we date, but in the process we learn from our misjudgments and discover the important qualities we value in relationships. The same goes for stocks. Nothing beats experience, and in my long investment career, I can honestly say I’ve dated/traded a lot of pigs and gained valuable lessons that have improved my investing capabilities. Now, however, I don’t just casually date my investments – I factor in a rigorous, disciplined process that requires a serious commitment. I no longer enter positions lightly.

One of my investment heroes, Peter Lynch, appropriately stated, “In stocks as in romance, ease of divorce is not a sound basis for commitment. If you’ve chosen wisely to begin with, you won’t want a divorce.”

Charles Ellis shared these thoughts on relationships with mutual funds:

“If you invest in mutual funds and make mutual funds investment changes in less than 10 years…you’re really just ‘dating.’ Investing in mutual funds should be marital – for richer, for poorer, and so on; mutual fund decisions should be entered into soberly and advisedly and for the truly long term.”

No relationship comes without wild swings, and stocks are no different. If you want to survive the volatile ups and downs of a relationship (or stock ownership), you better do your homework before blindly jumping into bed. The consequences can be punishing.

Buy and Hold is Dead…Unless Stocks Go Up

If you are serious about your investments, I believe you must be mentally willing to commit to a relationship with your stock, not for a day, not for a week, or not for a month, but rather for years. Now, I know this is blasphemy in the age when “buy-and-hold” investing is considered dead, but I refute that basic premise whole-heartedly…with a few caveats.

Sure, buy-and-hold is a stupid strategy when stocks do nothing for a decade – like they have done in the 2000s, but buying and holding was an absolutely brilliant strategy in the 1980s and 1990s. Moreover, even in the miserable 2000s, there have been many buy-and-hold investments that have made owners a fortune (see Questioning Buy & Hold ). So, the moral of the story for me is “buy-and-hold” is good for stocks that go up in price, and bad for stocks that go flat or down in price. Wow, how deeply profound!

To measure my personal commitment to an investment prospect, a bachelorette investment I am courting must pass another test…a test from another one of my investment idols, Phil Fisher, called the three-year rule. This is what the late Mr. Fisher had to say about this topic:

“While I realized thoroughly that if I were to make the kinds of profits that are made possible by [my] process … it was vital that I have some sort of quantitative check… With this in mind, I established what I called my three-year rule.” Fisher adds, “I have repeated again and again to my clients that when I purchase something for them, not to judge the results in a matter of a month or a year, but allow me a three year period.”

Certainly, there will be situations where an investment thesis is wrong, valuation explodes, or there are superior investment opportunities that will trigger a sale before the three-year minimum expires. Nonetheless, I follow Fisher’s rule in principle in hopes of setting the bar high enough to only let the best ideas into both my client and personal portfolios.

As I have written in the past, there are always reasons of why you should not invest for the long-term and instead sell your position, such as: 1) new competition; 2) cost pressures; 3) slowing growth; 4) management change; 5) valuation; 6) change in industry regulation; 7) slowing economy; 8 ) loss of market share; 9) product obsolescence; 10) etc, etc, etc. You get the idea.

Don Hays summed it up best: “Long term is not a popular time-horizon for today’s hedge fund short-term mentality. Every wiggle is interpreted as a new secular trend.”

Peter Lynch shares similar sympathies when it comes to noise in the marketplace:

“Whatever method you use to pick stocks or stock mutual funds, your ultimate success or failure will depend on your ability to ignore the worries of the world long enough to allow your investments to succeed.”

Every once in a while there is validity to some of the concerns, but more often than not, the scare campaigns are merely Chicken Little calling for the world to come to an end.

Patience is a Virtue

In the instant gratification society we live in, patience is difficult to come by, and for many people ignoring the constant chatter of fear is challenging. Pundits spend every waking hour trying to explain each blip in the market, but in the short-run, prices often move up or down irrespective of the daily headlines. Explaining this randomness, Peter Lynch said the following:

“Often, there is no correlation between the success of a company’s operations and the success of its stock over a few months or even a few years. In the long term, there is a 100% correlation between the success of a company and the success of its stock. It pays to be patient, and to own successful companies.”

Long-term investing, like long-term relationships, is not a new concept. Investment time horizons have been shortening for decades, so talking about the long-term is generally considered heresy. Rather than casually date a stock position, perhaps you should commit to a long-term relationship and divorce your field-playing habits. Now that sounds like a sweet kiss of success.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Questioning the Death of Buy & Hold Investing

In the midst of the so-called “Lost Decade,” pundits continue to talk about the death of “buy and hold” (B&H) investing. I guess it probably makes sense to define B&H first before discussing it, but like most amorphous financial concepts, there is no clear cut definition. According to some strict B&H interpreters, B&H means buy and hold forever (i.e., buy today and carry to your grave). For other more forgiving Wall Street lexicon analysts, B&H could mean a multi-year timeframe. However, with the advent of high frequency trading (HFT) and supercomputers, the speed of trading has only accelerated further to milliseconds, microseconds, and even nanoseconds. Pretty soon B&H will be considered buying a stock and holding it for a day! Average mutual fund turnover (holding periods) has already declined from about 6 years in the 1950s to about 11 months in the 2000s according to John Bogle.

Technology and the lower costs associated with trading advancements is obviously a key driver to shortened investment horizons, but even after these developments, professionals success in beating the market is less clear. Passive gurus Burton Malkiel and John Bogle have consistently asserted that 75% or more of professional money managers underperform benchmarks and passive investment vehicles (e.g., index funds and exchange traded funds).

This is not the first time that B&H has been held for dead. For example, BusinessWeek ran an article in August 1979 entitled The Death of Equities (see Magazine Cover article), which aimed to eradicate any stock market believers off the face of the planet. Sure enough, just a few years later, the market went on to advance on one of the greatest, if not the greatest, multi-decade bull market run in history. People repudiated themselves from B&H back then, and while B&H was in vogue during the 1980s and 1990s it is back to becoming the whipping boy today.

Excuse Me, But What About Bonds?

With all this talk about the demise of B&H and the rise of the HFT machines, I can’t help but wonder why B&H is dead in equities but alive and screaming in the bond market? Am I not mistaken, but has this not been the largest (or darn near largest) thirty year bull market in bonds? The Federal Funds Rate has gone from 20% in 1981 to 0% thirty years later. Not a bad period to buy and hold, but I’m going to go out on a limb and say the Fed Funds won’t go from 0% to a negative -20% over the next thirty years.

Better Looking Corpse

There’s no denying the fact that equities have been a lousy place to be for the last ten years, and I have no clue what stocks will do for the next twelve months, but what I do know is that stocks offer a completely different value proposition today. At the beginning of the 2000, the market P/E (Price Earnings) valued earnings at a 29x multiple with the 10-year Treasury Note trading with a yield of about 6%. Today, the market trades at 13.5 x’s 2010 earnings estimates (12x’s 2011) and the 10-Year is trading at a level less than half the 2000 rate (2.75% today). Maybe stocks go nowhere for a while, but it’s difficult to dispute now that equities are at least much more attractive (less ugly) than the prices ten years ago. If B&H is dead, at least the corpse is looking a little better now.

As is usually the case, most generalizations are too simplistic in making a point. So in fully reviewing B&H, perhaps it’s not a bad idea of clarifying the two core beliefs underpinning the diehard buy and holders:

1) Buying and holding stocks is only wise if you are buying and holding good stocks.

2) Buying and holding stocks is not wise if you are buying and holding bad stocks.

Even in the face of a disastrous market environment, here are a few stocks that have met B&H rule #1:

Maybe buy and hold is not dead after all? Certainly there have been plenty of stinking losing stocks to offset these winners. Regardless of the environment, if proper homework is completed, there is plenty of room to profitably resurrect stocks that are left for a buy and hold death by the so-called pundits.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and AAPL, AMZN, ARMH, and NFLX, but at the time of publishing SCM had no direct position in GGP, APKT, KRO, AKAM, FFIV, OPEN, RVBD, BIDU, PCLN, CRM, FLS, GMCR, HANS, BYI, SWN (*2,901% is correct %), CTSH, CMI, ISRG, ESRX, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Lessons Learned from Financial Crisis Management 101

For many investors the financial crisis over the last 24 months was an expensive education. Rather than have to enroll and take the courses all over again, I am hopeful we can put that past education to good use. Here are some valuable lessons I learned from my two year degree in Financial Crisis Management 101.

Investors Don’t Get Paid For Emotions: In investing, emotional decisions generally lead to suboptimal  decisions. Over the financial crisis, despite the market rebound last year, many investors fell prey to fear. This queasiness (see Queasy Investors article) resulted in money being stuffed under the mattress – earning subpar yields – and asset allocations dramatically shifting towards bonds. Not surprisingly, the Barclays Aggregate Bond Index fell -1% in 2009 as the herd piled in. On the flip side, those willing to brave the equity markets were rewarded with a +23% gain in the S&P500 index. Certainly this bond-equity picture looked different in 2008, but unfortunately many mainstream portfolios lacked adequate bond exposure then. As famed Fidelity Magellan fund manager Peter Lynch points out, fretting about your portfolio can work against you: “Your ultimate success or failure will depend on your ability to ignore the worries of the world long enough to allow your investments to succeed.”

decisions. Over the financial crisis, despite the market rebound last year, many investors fell prey to fear. This queasiness (see Queasy Investors article) resulted in money being stuffed under the mattress – earning subpar yields – and asset allocations dramatically shifting towards bonds. Not surprisingly, the Barclays Aggregate Bond Index fell -1% in 2009 as the herd piled in. On the flip side, those willing to brave the equity markets were rewarded with a +23% gain in the S&P500 index. Certainly this bond-equity picture looked different in 2008, but unfortunately many mainstream portfolios lacked adequate bond exposure then. As famed Fidelity Magellan fund manager Peter Lynch points out, fretting about your portfolio can work against you: “Your ultimate success or failure will depend on your ability to ignore the worries of the world long enough to allow your investments to succeed.”

Martin Luther King Jr. put anxious emotions into perspective by expressing, “Normal fear protects us; abnormal fear paralyses us.” Prudent conservatism makes sense, but panicked alarm can lead you astray. Behavioral economists Daniel Kahneman and Amos Tversky punctuated this idea by showing the impact that “loss” has on peoples’ psyches. Through their research, Kahneman and Tversky demonstrated the pain of loss is more than twice as painful as the pleasure from gain. Euphoria, whether for homes or for other forms of credit-induced spending, is not a desirable emotion when investing either – just ask any house-flipping Florida or California resident looking for work. The moral of the story: plan for a rainy day and don’t succumb to the elation of the herd. Create a disciplined systematic approach that relies less on your gut. Emotional decisions, as we’ve seen over the last few years, generally do not fare well.

Quality Doesn’t Die in a Crisis: Good companies with solid growth prospects don’t disappear in a bear market. On  the contrary, they typically are in much better position to invest, step on the throats of their competitors, and steal market share. Many of the quality companies left for dead last year have risen from the ashes. Leveraged financials and debt laden companies were hit the hardest, and bounced nicely last year, but the market leaders are the companies that endure through bull and bear markets.

the contrary, they typically are in much better position to invest, step on the throats of their competitors, and steal market share. Many of the quality companies left for dead last year have risen from the ashes. Leveraged financials and debt laden companies were hit the hardest, and bounced nicely last year, but the market leaders are the companies that endure through bull and bear markets.

Buy and Hold is Not Dead: Catching fish  can be difficult if one constantly dips their line in and out of the water. Academic research falls pretty bluntly on the shoulders of “day traders,” and I’m still searching for a Warren Buffett equivalent to show up on Oprah or Charlie Rose espousing the virtues of speculation – oh wait, maybe Jim Cramer qualifies?

can be difficult if one constantly dips their line in and out of the water. Academic research falls pretty bluntly on the shoulders of “day traders,” and I’m still searching for a Warren Buffett equivalent to show up on Oprah or Charlie Rose espousing the virtues of speculation – oh wait, maybe Jim Cramer qualifies?

Long-term investors are a rare but dying breed – just look at the average fund manager’s holding period, which has dropped from about five years in the 1960s to less than one year today. The 1980s and 1990s weren’t too bad for buy and holders (about a +1,400% increase), but the strategy has subsequently gone in hibernation for a decade. Warren Buffett may be pushing a bit too far when he says, “Our favorite holding period is forever,” but directionally this posture may actually work well over the next ten years. Patience can pay off – even if you arrive late to the game. For example, if you bought Wal-Mart shares (WMT) after it rose 10-fold during its first 10 years, you still could have achieved a 60x return over the next 30 years. I, myself, believe there is a happy medium between high frequency trading (see HFT article) and “forever” investing. Regardless of your time horizon, I agree with late Sir John Templeton who said, “The only way to avoid mistakes is not to invest – which is the biggest mistake of all.”

Cyclical is Not Secular: Party crashers may be optimistic about the prospects of a gathering, but if they arrive too  late to the event, there may be no more food or wine left. The same principle applies to investment themes, as well-known value manager Bill Miller states, “Latecomers are usually persuaded that the cyclical has become the secular.” Over the last few years, the secular arguments of “real estate prices will never go down nationally,” and the belief that emerging markets like China would “decouple” from the U.S. market in 2008, simple were proved wrong. Time will tell if the gold-bugs will be right regarding their call for continued secular increases, or if the spike is a crescendo on a return to more normalized levels. On the whole, I much rather prefer to arrive at a big party prematurely, rather than showing up late sifting through the crumbs and scraping the bottom of the punch bowl.

late to the event, there may be no more food or wine left. The same principle applies to investment themes, as well-known value manager Bill Miller states, “Latecomers are usually persuaded that the cyclical has become the secular.” Over the last few years, the secular arguments of “real estate prices will never go down nationally,” and the belief that emerging markets like China would “decouple” from the U.S. market in 2008, simple were proved wrong. Time will tell if the gold-bugs will be right regarding their call for continued secular increases, or if the spike is a crescendo on a return to more normalized levels. On the whole, I much rather prefer to arrive at a big party prematurely, rather than showing up late sifting through the crumbs and scraping the bottom of the punch bowl.

Turn Off the TV: Fanning the flames of our daily emotions are media outlets. Thanks to globalization, the internet,  and the 24/7 news cycle, we are bombarded with some type of daily fear factor to worry about. Typically, an eloquent strategist or economist pontificates on the direction of the market. In many instances these talking heads don’t even manage client money or are not held accountable for their predictions (see Peter Schiff article). I like Barron’s Michael Santoli’s description of these story-telling market mavens, “A strategist’s first job is to have a plausible, defensible case to shop around client conference rooms globally. Being right is gravy.” Although intellectually stimulating, I advise you to limit your consumption and delivery of strategist commentary to cocktail parties and don’t let their advice sway your portfolio decisions. You’ll be much better served by listening to veteran investors who have successfully navigated choppy market cycles. Famed growth investor William O’Neil shrewdly chimes in on the subject too, “Since the market tends to go in the opposite direction of what the majority of people think, I would say 95% of all these people you hear on TV shows are giving you their personal opinion. And personal opinions are almost always worthless … facts and markets are far more reliable.”

and the 24/7 news cycle, we are bombarded with some type of daily fear factor to worry about. Typically, an eloquent strategist or economist pontificates on the direction of the market. In many instances these talking heads don’t even manage client money or are not held accountable for their predictions (see Peter Schiff article). I like Barron’s Michael Santoli’s description of these story-telling market mavens, “A strategist’s first job is to have a plausible, defensible case to shop around client conference rooms globally. Being right is gravy.” Although intellectually stimulating, I advise you to limit your consumption and delivery of strategist commentary to cocktail parties and don’t let their advice sway your portfolio decisions. You’ll be much better served by listening to veteran investors who have successfully navigated choppy market cycles. Famed growth investor William O’Neil shrewdly chimes in on the subject too, “Since the market tends to go in the opposite direction of what the majority of people think, I would say 95% of all these people you hear on TV shows are giving you their personal opinion. And personal opinions are almost always worthless … facts and markets are far more reliable.”

Bad Loans are Made in Good Times: Markus Brunnermeier, a Princeton economist known for studying financial bubbles, declared this observation regarding loans. Hindsight is 20-20, but it’s no wonder that boat loads of no-doc, no down-payment, teaser rate subprime loans and overleveraged risky private equity loans were being made when unemployment was at 5% — not today’s 10% rate. Now with the loan spigots shut, the tables have been turned. Relatively few loans are now being made, but with a massively steep yield curve, surviving financial institutions are in a golden age for bringing on new wildly lucrative assets onto their balance sheets. Sure, the industry is still saddled with toxic legacy assets, but the negative impact should begin fading in coming quarters if the economy can continue building a firmer foundation.

Diversification Matters: Contrary to current thinking, which believes diversification didn’t help investors through  the crisis, owning certain asset classes like treasuries, certain commodities, and cash did help in 2008. Certainly, the correlations between many asset classes converged in the heat of the panic, but I’m convinced the benefits of diversification provide beneficial shock absorbers for most investment portfolios. Princeton professor and economist Burton Gordon Malkiel sums it up succinctly, “Diversity reduces adversity.”

the crisis, owning certain asset classes like treasuries, certain commodities, and cash did help in 2008. Certainly, the correlations between many asset classes converged in the heat of the panic, but I’m convinced the benefits of diversification provide beneficial shock absorbers for most investment portfolios. Princeton professor and economist Burton Gordon Malkiel sums it up succinctly, “Diversity reduces adversity.”

The Herd is Often Led to the Slaughterhouse: The technology and housing bubble implosions serve as gentle  reminders of the slaughterhouse fate for those who follow the herd. Avoiding consensus thinking is virtually a requirement of long-term outperformance. As Sir John Templeton stated, “It’s impossible to produce superior performance unless you do something different from the majority.” John Paulson can also attest to this fact. If aggressively shorting the housing market and loading up on CDS insurance was the consensus, his firm would not have made $20 billion over 2007 and 2008.

reminders of the slaughterhouse fate for those who follow the herd. Avoiding consensus thinking is virtually a requirement of long-term outperformance. As Sir John Templeton stated, “It’s impossible to produce superior performance unless you do something different from the majority.” John Paulson can also attest to this fact. If aggressively shorting the housing market and loading up on CDS insurance was the consensus, his firm would not have made $20 billion over 2007 and 2008.

These are obviously not all the lessons to be learned from the financial crisis, and by following a philosophy of continual learning, future mistakes should provide additional insights to help guard against losses and capitalize on potential opportunities. Having freshly graduated from Financial Crisis Management 101, I hope to immediately implement this education to land on the financial market’s Dean’s List.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds (including fixed income ETFs and FXI). Also at time of publishing SCM and some of its clients had a direct long position in WMT, but no position in BEN or BRKA/B. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}