Posts tagged ‘business’

A Sleepy Stock that Can Wake Up Your Portfolio

In over 35 years of investing, I have rarely encountered a company in such a unique – and frustrating – position as Harmony Biosciences (“Harmony” – HRMY). As a shareholder through my firm, Sidoxia Capital Management, I approach this analysis with a dual lens: as an investor seeing immense value, and as a fiduciary who expects corporate leadership to act in the best interest of its owners.

While Harmony’s executive team has executed brilliantly on its clinical mission, they are currently failing their fiduciary duty regarding capital allocation. Here is why Harmony is a “Diamond in the Rough” that needs a wake-up call.

Harmony Biosciences Overview – A Rare Disease Powerhouse

Harmony is a neuroscience-focused company targeting rare and underserved conditions such as narcolepsy, Prader-Willi Syndrome, and certain rare epilepsies—areas where treatment options are limited or nonexistent.

Today, the vast majority of revenue is driven by narcolepsy, a neurological disorder that disrupts sleep-wake cycles and leads to excessive daytime sleepiness and sudden sleep attacks. While approximately 135,000–200,000 Americans are diagnosed, the true number is likely higher due to underdiagnosis and misdiagnosis.

Harmony’s flagship drug, WAKIX (pitolisant), is on track to surpass $1 billion in annual revenue in 2026, achieving blockbuster status. Importantly, WAKIX is the only FDA-approved narcolepsy treatment that is not a controlled substance as defined by the U.S. Drug Enforcement Administration (DEA), providing a meaningful competitive advantage over alternative therapies.

Significant Growth Beyond WAKIX

Harmony’s long-term opportunity extends well beyond narcolepsy. The company is leveraging the pharmaceutical compound behind its franchise drug WAKIX (pitolisant) to expand and diversify its revenue base into additional CNS (Central Nervous System) indications, with five ongoing Phase 3 registrational programs (see below):

- Pitolisant HD (High Dose) – Idiopathic Hypersomnia (IH) – potential $1.5 billion – $2.0 billion market with possible FDA submission for approval in 2027.

- Pitolisant HD (High Dose) – Narcolepsy – potential to accelerate the growth of $1 billion WAKIX franchise (2026 estimate) by offering enhanced efficacy for fatigue. FDA submission for approval of Pitolisant HD could come in 2027.

- Pitolisant – Prader-Willi Syndrome (PWS) – There are an estimated 15,000–20,000 people in the U.S. with PWS. Over half of these targeted patients suffer from EDS, which is effectively treated with Pitolisant. PWS has a potential of reaching $300 million – $500 million in revenue and receiving FDA submission for approval during the 2nd half of 2026.

- EPX-100 (Clemizole HCl) – Dravet Syndrome (epilepsy with onset at infancy) – expands Harmony into a potential $800 million global market by 2030 with possible FDA submission for approval in the 1st half of 2027.

- EPX-100 (Clemizole HCl) – Lennox-Gastaut Syndrome (LGS) (epilepsy with multiple seizure types) – opens the company to a potential $1 billion market globally.

Collectively, this pipeline has the potential to generate billions in incremental revenue.

A Diamond in the Rough

There are many ways to value a stock, but one common approach is to compare a company’s price-to-earnings ratio (P/E) to that of the S&P 500. Generally, stocks trading below the market’s average P/E are considered cheap, while those above it are viewed as more expensive.

Harmony shares currently trade at approximately 8x trailing twelve-month earnings and 7x its 2026 earnings forecast. By comparison, this represents roughly a -70% discount to the average S&P 500 stock. Based on these metrics, Harmony appears dramatically undervalued—assuming the company’s fundamentals remain intact.

Of course, valuation must be considered alongside growth and execution. On that front, management continues to emphasize strong underlying performance.

And the results support that claim. In less than three years, CEO Dr. Jeffrey Dayno has grown revenue by approximately 74%, from roughly $500 million in April 2023 to over $860 million today, with expectations to exceed $1 billion in annual sales by the end of the year.

But wait, there’s more. The balance sheet tells a similarly compelling story. Over that same period, Harmony’s net cash position (gross cash minus debt) has increased from approximately $201 million to $719 million, even after completing two acquisitions totaling about $69 million (Zynerba and Epygenix). During this time, quarterly revenue growth has averaged roughly +23%, while cash has more than tripled, despite the acquisitions.

What’s more, Harmony’s cash profitability is equally impressive. In 2025, Harmony generated a 40% free cash flow margin, meaning $0.40 of every $1 of revenue converted into free cash flow. That level of efficiency would rank among the top two percent of companies in the S&P 500, placing Harmony alongside some of the most profitable behemoths in the market, including NVIDIA Corp.

Which brings us to the key question: If the stock is this inexpensive and the fundamentals are this strong, why isn’t the company aggressively repurchasing its own shares hand-over-fist? To date, management has not provided a clear or credible answer to this question.

What is the Downside to Harmony?

All this fundamental strength and financial momentum sounds like great news for shareholders—but where’s the risk and bad news? Regrettably, despite strong execution under CEO Dr. Jeffrey Dayno over the past three years, the stock is down approximately -14% (from ~$32 to ~$28 per share).

If everything is going so well, why have investors been so spooked recently? The primary concern centers on potential generic competition for WAKIX, the company’s key drug. To Harmony’s credit, it has already settled litigation with six of seven generic challengers, but one holdout—AET Pharma—has taken the case to trial. Some Wall Street analysts and investors believe the judge may rule in favor of AET, which contributed to a sharp decline in the stock last month.

If Harmony loses, WAKIX’s patent protection—currently expected to extend through 2030—could be materially weakened, potentially allowing generic competition to enter the market as early as late 2026 or early 2027, depending on the timing of the ruling and subsequent developments.

Fear not, says management. They remain confident in their defense strategy. As CEO Dr. Dayno stated, “Pitolisant GR will extend the WAKIX franchise and our leadership in narcolepsy as a line extension of WAKIX with its broad clinical utility. We are on track for NDA submission in Q2 this year with a target PDUFA date in Q1 2027.”

Management believes this next-generation formulation, Pitolisant GR, could significantly mitigate—or even eliminate—the impact of generic competition. Unlike WAKIX, which faces potential patent challenges, Pitolisant GR is expected to have patent protection through 2044.

If the timeline holds, the company expects a substantial portion of WAKIX patients to transition to GR, reducing the impact of any generic entrants. Additionally, even in a worst-case scenario where AET prevails, the financial risk associated with launching an “at-risk” generic—particularly if Harmony were to win on appeal—could be significant enough to deter entry and easily push AET towards a settlement with Harmony.

Am I Missing Something?

When a stock trades at such an egregiously low valuation, I inevitably ask myself, “Am I missing something?” If management is sitting on its hands doing nothing, perhaps Harmony’s fundamental outlook is worse than they are leading investors to believe. If management is unwilling to deploy even a portion of its inefficient, over-bloated cash hoard toward share repurchases – especially with the stock arguably at its cheapest level in history – why should investors commit their hard-earned capital to what could be a sinking ship?

Is it possible that management lacks confidence in the Pitolisant GR NDA data, or that the Q2 NDA timeline could slip? If so, and if AET prevails in court, Harmony’s entire $1 billion franchise revenue base could be at risk.

Management has dismissed these concerns and continues to insist that everything is on track. If that’s truly the case, then – with a clear line of sight into the company’s prospects – Harmony should be aggressively buying back its stock if the outlook is as strong and rosy as they claim.

Actions Speak Louder than Words

According to management, Harmony’s fundamentals remain robust. Not only does Harmony have five late-stage, phase three indications in the pipeline, it also claims to have a near bullet-proof generic competition protection strategy. Yet, with the stock down around -33% from its 52-week high, it is difficult to justify why management is not forcefully repurchasing shares at prices that are currently highly accretive to EPS.

I have raised this issue with senior management multiple times, but unfortunately my concerns have fallen on deaf ears. I’m hardly alone – other investors have voiced similar frustrations but inaction remains the default stance of management. The company’s response to this elephant in the room remains perplexing.

On the most recent fourth quarter conference call with investors, CFO Sandip Kapadia stated, “Business development is a high priority, and our intention is to deploy capital to expand our pipeline and commercial portfolio.” CEO Dr. Jeffrey Dayno echoed this sentiment, emphasizing a “commitment to generate even greater value through the pursuit of smart business development opportunities.”

It’s great that Harmony “intends” to deploy capital and “pursue” opportunities, but the fact remains, Harmony effectively has not devoted a penny over the last two years to capital deployment, and the company has spent next-to-nothing on capital deployment since the company’s IPO (Initial Public Offering) in August 2020.

Meanwhile, the company’s massive net cash balance – currently $719 million – is rapidly expanding by more than $100 million+ per quarter and is on track to swell to $1 billion this year. By the end of 2026, cash could represent as much as two-thirds of Harmony’s total market value, particularly if the share price remains depressed or declines further.

Walking and Chewing Gum

Can Harmony walk and chew gum at the same time? In other words, can the company allocate a portion of its gigantic cash balance toward a monumentally accretive share repurchase program while simultaneously pursuing business development (M&A – Mergers & Acquisitions) opportunities? The short answer is yes.

In fact, Harmony did exactly that in 2023 and 2024 – deploying nearly half of its cash toward share buybacks while ALSO completing two acquisitions that contributed to its expanding pipeline of promising new indications.

Management argues it’s currently evaluating a broad list of acquisition targets. However, one could reasonably contend that Harmony will be hard-pressed to find opportunities more attractive than its own stock. The bar is exceptionally high: identifying highly profitable companies with similarly robust pipelines, that are also trading at a steep discount and offering comparable growth characteristics.

By comparison, Harmony’s own shares appear to trade at roughly a -70% discount to the market, with approximately 50% of its market capitalization in cash, while delivering ~20% top-line growth, and securing a deep pipeline of five Phase 3 programs. Under these conditions, it seems like Harmony buying back their own stock is a no-brainer.

Where Is the Board and Why Are They Not Acting?

This is a question I’m asking, and I hope the board will answer the capital allocation question more thoughtfully. Ideally, the response will come in the form of a material share repurchase (i.e., action).

For those curious, I have identified the distinguished group of Harmony board members, and I intend to pursue an explanation relating to the board’s inaction. Here are Harmony’s current board members:

- Jeffrey S. Aronin (Executive Chairman) – Founder and CEO of Paragon Biosciences.

- Jeffrey M. Dayno, MD (President, CEO & Director) – Former CMO of Harmony; Board-certified neurologist.

- Peter Anastasiou (Independent Director) – CEO of Capsida Biotherapeutics; former Lundbeck executive.

- Antonio Gracias (Independent Director) – Founder/CEO of Valor Equity Partners and Director at Tesla.

- Mark Graf (Independent Director) – Former CFO of Discover Financial Services.

- Ron Philip (Independent Director) – CEO of Orbital Therapeutics and former CEO of Spark Therapeutics.

- Juan Sabater (Independent Director) – Partner at Valor Equity Partners and former Goldman Sachs MD.

- Gary Sender (Independent Director) – Former CFO of Nabriva Therapeutics and Shire PLC.

- Linda Szyper (Independent Director) – Former COO of McCann Health; pharmaceutical sales veteran.

- Andreas Wicki, PhD (Independent Director) – CEO of HBM Healthcare Investments.

I’m not sure whether the board is asleep at the switch, but it has a clear fiduciary duty to allocate capital efficiently and maximize shareholder value. Allowing the balance sheet to become excessively bloated while taking no meaningful action falls short of that responsibility. The company needs to act.

As Harmony’s share price remains stagnant and under pressure, management and the board continue to irresponsibly let cash accumulate. Net cash now represents approximately 45% of the company’s market capitalization. If Harmony were in the S&P 500, this would place it among the top 1% of companies by cash as a percentage of market value – all while trading at roughly a -70% discount to the broader market.

We remain long-term shareholders, but there are only two plausible explanations. Either management is correct, and this represents a generational buying opportunity—or the company knows something investors do not, which may explain the lack of action and the continued buildup of cash.

Bottom line: assuming a successful defense against generic competition and a conservative rollout of the pipeline—including Pitolisant GR and Pitolisant HD—$7 in EPS by 2030 at a 22x multiple implies a $154 price target, or roughly +450% upside from today’s ~$28 share price.

Harmony may be a sleepy stock today, but it has all the ingredients to wake up your portfolio. While management and the board have been slow to act and have yet to fully meet their fiduciary responsibility on capital allocation, I remain optimistic that they will ultimately do the right thing. By deploying capital more effectively – most notably through a meaningful share repurchase at today’s historically attractive valuation – Harmony has the opportunity to awaken significant shareholder value and live up to its full potential.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in HRMY, NVDA, TSLA, GS, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in DFS, HBMN, HLUYY, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

A.I. Field of Dreams

In the 1989 Academy Award–nominated film Field of Dreams, the lead character Ray Kinsella (played by Kevin Costner) hears a mysterious voice whisper, “If you build it, he will come.” Acting on blind faith, Ray builds a baseball diamond in the middle of his Iowa cornfield, risking financial ruin. Against all logic, the field draws a flood of visitors.

Today, a similar “field of dreams” is being built—not with corn, but with data centers. Instead of baseball players, it is artificial intelligence (AI) models, applications, and users who are coming.

The Market’s AI Momentum

The AI boom has already reshaped markets with all three benchmarks hitting record highs. Last month, the S&P 500 climbed +1.9%, while the NASDAQ rose +1.6% and Dow Jones Industrial Average surged +3.2%. Year to date, the indexes are up +10%, +11%, and +7%, respectively.

Behind this surge lies an unprecedented wave of AI infrastructure investment. Hyperscalers—Amazon.com (AMZN), Microsoft Corp. (MSFT), Google-Alphabet (GOOGL), Meta Platforms (META), and others—are pouring hundreds of billions into AI, much of it flowing directly to NVIDIA Corp. (NVDA), the undisputed leader in GPUs (Graphic Processing Units) powering the world’s AI engines. How large is the spending? NVIDIA CEO Jensen Huang estimates $3 trillion to $4 trillion will be spent this decade to fuel the AI revolution.

Source: Visual Capitalist

The Scale of AI’s Buildout

To put this into perspective:

- Amazon is projected to spend over $100 billion in 2025 alone, more than its cumulative capital expenditures from 2000–2020 combined.

Meta is constructing its $10 billion+ Hyperion data center in Louisiana—a sprawling 4 million sq. ft. complex across 2,250 acres, powered by a $4 billion natural gas plant. The footprint is so gargantuan it could cover much of Manhattan (see graphic below).

- xAI’s Colossus, a 750,000 sq. ft. data center in Memphis, Tennessee was completed in just 122 days—equivalent to building 418 homes in half the time it normally takes to construct one house (see slide below).

Source: BOND (Global Technology Investment Firm)

This breakneck pace of spending underscores the urgency and competitive pressure driving the global AI arms race.

The Origin of the AI Floodgates Opening

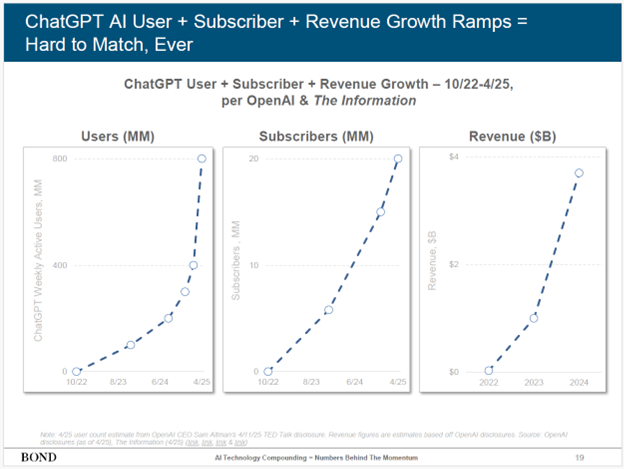

The spark was lit on November 30, 2022, when OpenAI released its LLM (large language model) called ChatGPT. Within two months, it amassed 100 million users.

Today, ChatGPT’s metrics have blasted much higher (see slide below):

- 800 million weekly active users

- 20 million paid subscribers

- $3.7 billion in revenue (as of April 2025)

Source: BOND (Global Technology Investment Firm)

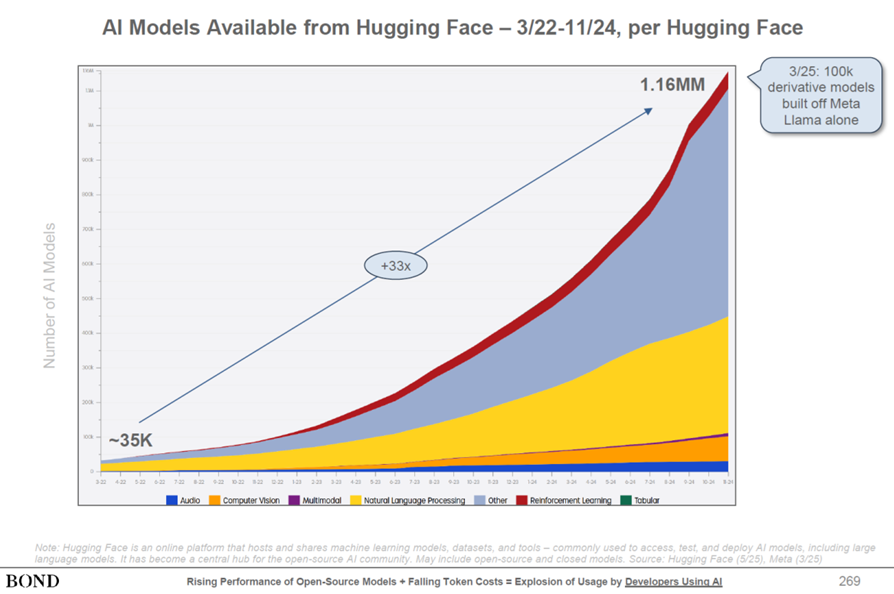

But OpenAI is far from alone. Google (Gemini), xAI (Grok), Anthropic (Claude), Meta (LLaMA), Amazon (Titan), Perplexity, and DeepSeek are all competing with their own LLMs. In total, over 1 million machine learning models now exist (see slide below) — each requiring costly compute power and pricey data centers.

Source: BOND (Global Technology Investment Firm)

Bubble or Productivity Breakthrough?

With trillions flowing into AI, a natural question arises: Is this a bubble?

Even OpenAI CEO Sam Altman admits we’re in an AI bubble :

“When bubbles happen, smart people get overexcited about a kernel of truth…Someone is going to lose a phenomenal amount of money… and a lot of people are going to make a phenomenal amount of money.”

Both realities can be true:

- Yes, hyperscalers are spending like “drunken sailors.”

- Yes, AI demand and productivity benefits are real and growing exponentially.

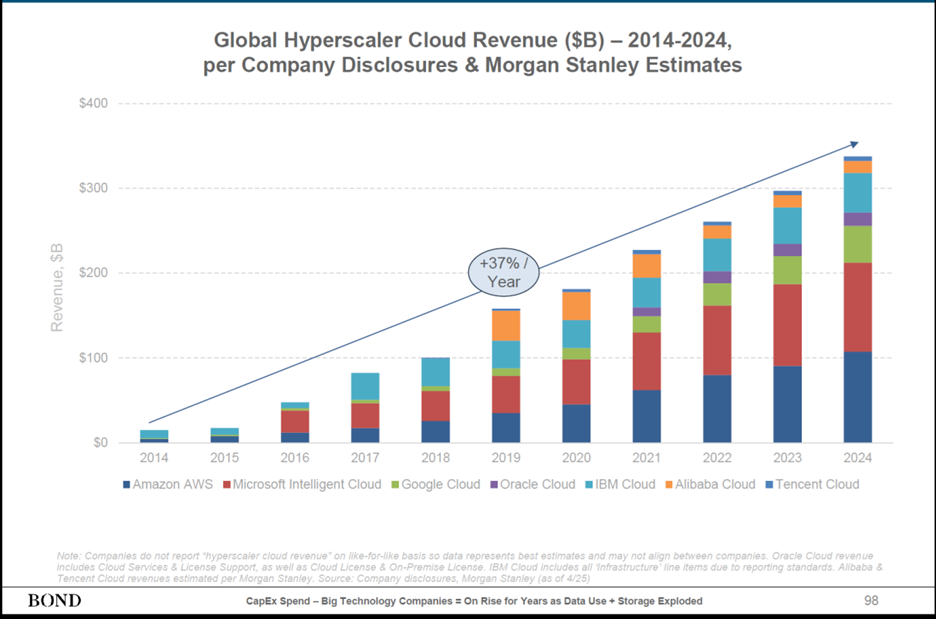

Consider the trajectory of global cloud revenues: from nearly $0 a decade ago to $300 billion today—a +37% CAGR (see chart below).

Source: BOND (Global Technology Investment Firm)

And the primary reason for cloud growth can be attributed to AI productivity benefits. A recent SAP survey found that workers using AI save nearly one hour per day on average. That’s transformative for companies: higher productivity without needing proportional hiring.

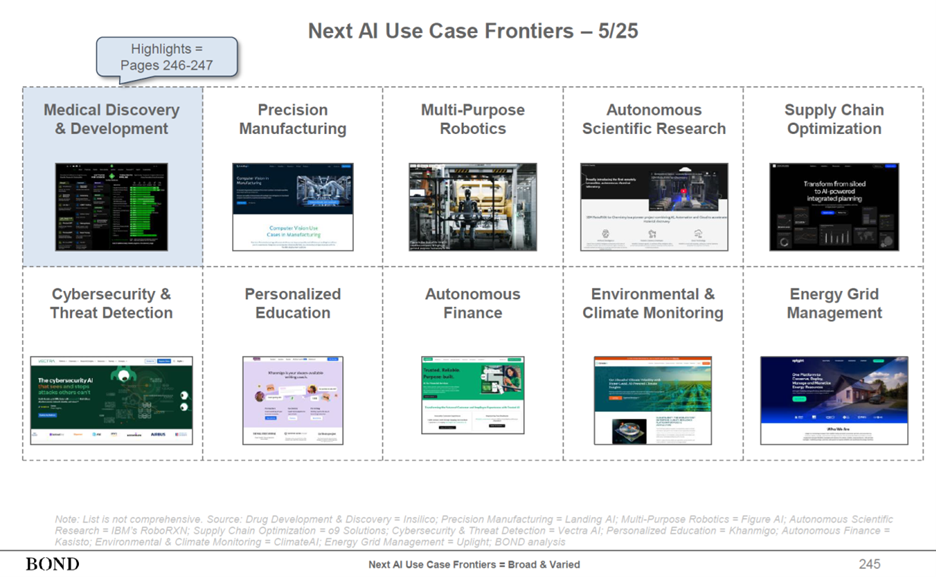

AI Use Cases Expanding Aggressively

AI’s applications now span nearly every sector (see slide below):

- Technology – software engineering, code generation

- Customer Service & Marketing – customer support and call centers

- Transportation – autonomous vehicles and logistics

- Healthcare – drug discovery and development

- Supply Chains – precision manufacturing and optimization

- Automation – multi-purpose robotics

- Cybersecurity – threat detection and prevention

- Education – personalized lessons and curriculums

- Energy – grid optimization and demand forecasting

Source: BOND (Global Technology Investment Firm)

The New Field of Dreams

Throughout history, every great leap—printing press, steam engine, electricity, internet—has required massive upfront investment before the payoff arrived. AI is following the same path. Today, we are in the midst of building a new AI Field of Dreams. However, now, the data centers are the new baseball fields. And as with Ray Kinsella’s diamond, the masses are indeed coming.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

This article is an excerpt from a previously released Sidoxia Capital Management complimentary newsletter (August 1, 2025). Subscribe Here to view all monthly articles.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in GOOGL, META, AMZN, MSFT, NVDA, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in SAP or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Investing in Pigs and Kidneys: Building a $100 Billion Empire and Revolutionizing Organ Transplants

How does one create a $100 billion empire while pioneering an endless supply of transplantable organs that could save millions of lives? The first step is launching a multi-billion-dollar satellite company (SiriusXM – SIRI). The next step? Founding a biotechnology company with nothing more than a high school-level biology education — all in a desperate attempt to save the life of your seven-year-old daughter from a rare heart disease that claims lives within three to five years.

This is the extraordinary path of Martine Rothblatt, CEO and visionary of United Therapeutics Corp. (UTHR), who began this journey 35 years ago.

Transforming Industries: From SiriusXM to Organ Transplants

Few individuals have singlehandedly transformed entire industries. One name that comes to mind is Steve Jobs – who revolutionized consumer electronics and laid the foundation for Apple Inc.’s (AAPL) meteoric rise to a multi-trillion dollar company before he passed away. While Rothblatt and United Therapeutics may not yet be household names, she is undeniably reshaping the healthcare industry and steering it toward a future of unprecedented, life-extending medical advancements.

How can these ambitious, world-changing goals be achieved? A whole aisle of books could be written about Rothblatt’s impressive lifetime accomplishments, but the unique investment opportunity for investors cannot be fully understood without appreciating the person that created United Therapeutics 29 years ago in 1996.

Rothblatt has accomplished more than most humans could in multiple lifetimes – here is a partial sampling of her achievements:

- Earned a Bachelor of Arts, a Juris Doctor (JD), and Master of Business Administration (MBA) degrees from the University of California, Los Angeles (UCLA).

- Finished her PhD at The London School of Medicine (Barts)

- Practiced law at the Covington & Burling law firm representing the television broadcasting industry before the Federal Communications Commission (FCC).

- Hired by NASA to seek approval from the FCC for NASA systems used to track and relay satellite data.

- Created the multi-billion-dollar satellite radio company SiriusXM in 1990 with the inspiration of physicist Gerard O’Neill, the same Princeton professor who motivated Amazon CEO, Jeff Bezos to create Blue Origin.

- Invented the Terasem Movement, an organization with the mission of human life extension that uses cognitive and artificial intelligence software. Terasem’s technology has created a lifelike robot (BINA48), which is modeled after her spouse, Bina Rothblatt.

- Pioneered EV (electric) helicopter transportation through the company’s Unither Bioelectronics division with the purpose of cutting energy consumption and speeding up organ delivery times.

The United Therapeutics Story

In 1996, while leading SiriusXM, Rothblatt faced every parent’s worst nightmare. Doctors diagnosed her seven-year-old daughter, Jenesis, with Pulmonary Arterial Hypertension (PAH) — a rare, devastating disease with no known cure. Determined to save her daughter, Rothblatt initially funded research grants totaling over a million dollars to a narrow group of five doctors studying the disease. When the scientists failed to find a cure, she took matters into her own hands.

With no formal medical background, she quit SiriusXM, immersed herself in biology, and founded United Therapeutics. Against all odds, armed with her mantra that “persistence leads to omnipotence,” Rothblatt’s relentless pursuit paid off when she discovered a cure. Today, decades later, Jenesis is 42 years old and thriving as a high-profile manager at United Therapeutics.

Addressing the Organ Shortage Crisis

United Therapeutics’ advancements in PAH treatment have allowed patients like Jenesis to live long, productive lives. However, many eventually require organ transplants – the company is already assisting hundreds of patients with lifesaving human lung transplants. Despite some progress, the current organ shortage crisis is staggering:

- Over 100,000 people are on the national transplant waiting list.

- More than 92,000 of them need a kidney due to kidney failure or End-Stage Renal Disease (ESRD).

To address the organ shortage, United Therapeutics recently made history last month when the FDA approved the first-ever clinical trial for its UKidney xenotransplantation procedure for kidney failure patients.

The severity of the organ shortage problem is clear-cut if you examine the numbers. In addition to the 92,000 patients on the kidney transplant waitlist mentioned above, there are approximately 500,000 additional ESRD dialysis patients not on the national transplant list. Roughly 10% of these ESRD patients die each year due to dialysis-related complications.

If you combine the wait list population with the dialysis patient population you get to a total of around 600,000 people total. Regrettably, the vast majority of these patients do not receive an organ. In fact, only 27,759 kidney transplants were performed in the U.S. last year. In other words, despite the enormous demand for transplantable organs, less than 5% of the addressable market have actually benefited from a new kidney.

The Future of Organ Transplants: Profitable Pig Potential

How can this massive undersupply of transplants be fixed? One word…pigs. With a very scarce supply of human donors, pigs may hold the key to solving the organ shortage. United Therapeutics has pioneered genetically engineered pig organs (xenotransplantation) by modifying 10 key genes to prevent immune system rejection. As part of the xenotransplantation trial, United Therapeutics has built multiple DPF (designated pathogen free) facilities that house the pigs carrying the gene-modified kidneys.

All of this may sound like science fiction, but the dream of xenotransplantation has already become reality. Just last November, a genetically engineered pig kidney was transplanted into a patient (Towana Looney) under a compassionate use basis granted by the FDA. With its new clinical trial now underway, United Therapeutics is planning to transplant up to 50 patients with modified pig kidneys in the coming months.

And UKidney is just the beginning. United Therapeutics has a deep organ transplant pipeline that extends beyond kidneys into livers, hearts, and lungs (see graphic below). The company is also working on the “holy grail” of transplants – 3D printed organs using the cells of organ recipients to build the tissue structure, which dramatically reduces or eliminates the risk of organ rejection.

If UKidney is successful, United Therapeutics and Martine Rothblatt will be one step closer to realizing the company’s vision of manufacturing an endless supply of transplantable organs.

Source: United Therapeutics

Investment Opportunity of a Lifetime?

Nothing in life is certain, and there are risks to making any investment, but betting against Martine Rothblatt over the years has been a major losing proposition. From an investment standpoint, the core PAH drug business is trading at an immense discount, and investors are essentially valuing the organ transplant business at $0.

Despite its groundbreaking advancements and tremendous profit growth, United Therapeutics has huge stock price appreciation potential. Here’s why:

Stock is Dirt Cheap: At $317 per share, the stock currently trades at roughly a 50% discount to the trailing S&P 500 Price-Earnings ratio (PE) – 13x P/E vs. 26x index P/E. In other words, the shares should be trading north of $600 (double the price), if United Therapeutics was afforded an “average” company P/E multiple. But United Therapeutics clearly is not an average company.

Over the last two years, the company has grown revenues +48% from $1.9 billion to $2.9 billion and seen earnings explode +64% higher from $15.00 per share to $24.64. The stock becomes even cheaper on a forward P/E multiple (11x P/E) if the company can meet 2025 Wall Street expectations of 15% growth in its EPS to $28.23. Its superior products, execution, and competitive moats should afford the company a significant premium, not a drastic discount. Short-term investors are missing the boat by ignoring the gargantuan market potential for the company.

Is it possible for a $15 billion company to reach a $100 billion market value? This is not difficult to imagine if the company can bring its innovative and revolutionary pipeline products to market and take its current revenue base of almost $3 billion to $16 billion (see graphic below). The company certainly will not reach $16 billion in revenues tomorrow, but if you applied an average market multiple to those projections, and the company were able to maintain its current profit margin profile, a $3,000 per share stock price would be well within reason, equating to a market value well above $100 billion.

Source: United Therapeutics

Many Irons (Catalysts) in the Fire: United Therapeutics is no one-trick pony. Besides the company’s organ transplant plans, and their core commercial PAH and PH-ILD franchise, which includes, Remodulin, Orenitram, and Adcirca, United Therapeutics has many more irons in the fire that can be catalysts for stock price appreciation over the next 12 – 24 months (see graphic below).

Here is a more detailed description of the drivers:

- New Markets for Core Drugs: Any biotech or pharmaceutical company is in the business of searching for new markets to sell its products. United Therapeutics has found that in both the IPF (Idiopathic Pulmonary Fibrosis) and PPF (Progressive Pulmonary Fibrosis) markets, which are two different forms of chronic lung disease that are characterized by the gradual scarring and thickening of the lung tissue, which is called fibrosis. These patients can be administered with modified formulations of its existing Tyvaso molecule. The revenue potential is huge if the efficacy data comes in as planned because the pools of patients suffering from these horrible, progressive lung diseases could more than double the size of the present addressable market. Data from the company’s TETON 1 (IPF), TETON 2 (IPF), and TETON PPF studies will be released over the next few years, starting as early as next quarter.

- Improved Drug Formulation: United Therapeutics is also waiting for groundbreaking data from a drug called Ralinepag, the first once-per-day prostacyclin pill that is an improvement over its existing drugs of Remodulin, Tyvaso, and Orenitram. The company is releasing the Ralinepag data from its ADVANCE OUTCOMES study next year, and if the data proves to be positive, this could represent another multi-billion dollar opportunity for the company and investors.

- Other Near-Term Catalysts: Although perhaps representing a less meaningful potential from a long-term revenue standpoint, the company’s Centralized Lung Evaluation System (CLES) program is awaiting an FDA decision this year – CLES is designed to expand the supply of donor lungs. Last, but not least, data from United Therapeutics’ microliverELAP study represents another sizeable revenue opportunity for liver transplants.

Source: United Therapeutics

Fly in the Ointment: Failing Capital Allocation Grade

United Therapeutics deserves an A+ grade for developing the critical, world-class therapeutics that serve the PAH and PH-ILD market and the massive potential pipeline in xenotransplantation and alternative organ platforms. However, the company receives a failing grade for the implementation of its capital allocation strategy. United Therapeutics holds an excessively bloated cash surplus on its balance sheet, which has exploded higher from $1.0 billion in 2015 to $4.7 billion in 2024.

Sadly, the problem is only getting worse, as the company is on pace to add more than $1 billion more to the cash balance this year, and in subsequent years. This is woefully inefficient and becoming an alarmingly growing percentage (approximately 30% currently) of the company’s market value. To put this issue into perspective, investors should consider the company has enough cash on its balance sheet to effectively fund two decades of capital expenditure requirements. Profitable companies in United Therapeutics’ hand-selected proxy peer group hold a much more responsible amount of cash, representing about 4% of their market values.

If you had $100k of annual spending requirements, would you negligently place $2 million dollars in a low-single-digit yielding checking account or multi-year CD at your bank, when you could responsibly earn a 10% or higher return by paying down credit card debt? This is what United Therapeutics is doing. The company is essentially burning shareholder money by letting cash sit idly on its balance sheet earning a pittance when it could be earning significantly more. Why invest in government Treasuries when you could invest in your own company, compounding at rates greater than 10%?

The solution is clear. Implement a meaningful share repurchase program that is immediately EPS-accretive with the company’s bloated mountain of cash and bring down to responsible levels that are consistent with profitable growth peers. And rather than limiting your share repurchase to a one-time accelerated stock repurchase (ASR) program, expand the buyback to be more open ended on top of immediate purchases. This strategy provides the company with the flexibility to opportunistically purchase shares at a discount when the share price is depressed – like now, when shares are down -24% over the last five months.

Unfortunately, my message appears to be falling on deaf ears. I was hoping to gain clarity through communications with the company along with a letter sent to management and the board of directors. In my letter, I attempted to remind management of the importance of upholding its rigorous corporate governance standards and exercise its fiduciary duty when it comes to the company’s allocation strategy. However, regrettably, up to this point, there has been no indication to the market or me that there is any urgency to take advantage of the massively discounted United Therapeutics share price that exists today.

READ RECENT LETTER SENT TO MANAGEMENT & BOARD OF DIRECTORS BY CLICKING HERE

Investors Should Not Miss the Forest for the Trees

Although the company receives a failing capital allocation grade from my perspective, investors should not miss the forest from the trees. United Therapeutics’ share price is currently trading at a gigantic discount, yet it boasts unparalleled profitability and a groundbreaking organ transplant pipeline.

This lack of appreciation for the shares is surprising given how wildly profitable the company is and its tremendous long-term track record of success. But the company is not sitting on its hands – United Therapeutics has ambitious plans to expand its current annual revenue base by more than five-fold from $3 billion to $16 billion due to full cupboard of pipeline products.

With Martine Rothblatt at the helm—a visionary with a track record rivaling Steve Jobs—the company is poised to revolutionize healthcare. The world is a better place due to Martine Rothblatt, and your portfolio will be a better place with an investment in United Therapeutics.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in UTHR, AAPL, and certain exchange traded funds (ETFs), but at the time of publishing had no direct position in SIRI or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on the IC Contact page.

{kind=link}