Posts tagged ‘Brazil’

E.M.s Want Cake & Eat It Too

Since the end of 2010, the emerging markets (E.M.) have gotten absolutely obliterated (MSCI Emerging Markets index –25%) compared to a meteoric rise in U.S. stocks (S&P 500 index +60%) over the same period.

Source: Financial Times

Slowing global growth, especially with resource-hungry China going on a crash diet, has caused commodity-exporting emerging markets like Brazil to suffer economic starvation. Rising inflation, expanding debt, decelerating Chinese growth, collapsing commodity prices, and political corruption allegations are all factors pressuring the Brazilian economy. Weak emerging market economies like Brazil are contributing to global GDP forecast reductions. As you can see from the chart below, global GDP growth rates have been steadily declining since 2010, and the IMF recently lowered their 2015 forecast from +3.5% down to 3.1%.

Source: Financial Times

Beginning in late 2008, when Ben Bernanke first announced his QE 1 (Quantitative Easing) money printing binge, the U.S. dollar remained relatively weak against other global currencies for years. The weak dollar provided a nice tailwind to U.S. exporters (i.e., American manufactured goods were more cost competitive for foreign buyers).

Multinationals loved the export lift, but emerging international politicians and investors cried foul. They complained the U.S. was starting a “currency war” by artificially deflating the value of the U.S. dollar, thereby making international markets less competitive. At the time, the thought process was the emerging markets (e.g., China, Russia, Brazil et.al.) would be disproportionately impacted because their economies are export-driven. In a 2010 article from the Guardian (World Gripped by International Currency War) Brazilian finance minister Guido Mantega explicitly stated, “We’re in the midst of an international currency war, a general weakening of currency. This threatens us because it takes away our competitiveness.”

This “currency war” griping stayed in place until the end of 2013 when the Fed announced its plans to begin “tapering” bond buying (i.e., pull away the financial punch bowl). We all know what has happened since then…the U.S. dollar has spiked by about +20% and the Brazilian real has depreciated by a whopping -37%. This is good news for emerging markets like Brazil, right? Wrong!

A few years ago, emerging market investors were initially worried about the depressing effects of a strong currency on exports, but now that emerging market currencies have depreciated, fears have shifted. Now, investors are concerned whether E.M. countries can pay off foreign borrowed debt denominated in pricey U.S. dollars (paid with vastly weaker E.M. currencies). Moreover, with foreign governments holding dramatically lower valued currency, investors are worried about the ability of these E.M. countries to raise additional capital or refinance existing debt. SocGen’s head of emerging market strategy, Guy Stear, summed it up by noting, “Prevailing risks of a deterioration of the external financing environment and disruptive capital flow and asset price shifts that increase volatility in the respective bond and currency markets, make a rapid rebound in EM growth over the next months unlikely.”

So which one is it…do E.M. investors want a weak currency to power exports, or a strong currency to pay down debt and raise additional capital? Unfortunately, investors can’t have their cake and eat it too – you can’t have a depreciating and appreciating currency at the same time.

While anxiety has shifted from strong emerging market currencies to the issues associated with weak currencies, India is one E.M that has reaped the rewards from a declining rupee (-20% since 2013). In other words, India is benefiting from a stronger trade balance via a boost in exports and reduction in imports – interestingly, the U.S. has experienced the exact opposite. Regardless, eventually, other emerging markets will benefit from these same positive trends as India – that will finally be a tasty slice of cake.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including EWZ, but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Nail Not in Emerging Market Coffin Yet

I wouldn’t say the nail is in the emerging market coffin quite yet. During the financial crisis, the EMSCI Emerging Market Index (EEM) was left for dead (down -50% in 2008) before resurrection in 2009 and 2010 (up +74% and +16%, respectively). For the last two years however, the EMSCI index has underperformed the S&P 500 Index massively by more than -30%. Included in this international index are holdings from China, Russia, India, Brazil, South Korea, and South Africa, among others.

The question now becomes, can the emerging markets resurrect themselves from the dead again? Recent signs are flashing “yes”. Over the last three months, the emerging markets have outperformed the S&P 500 by more than +8%, but these stocks still have a lot of ground to make up before reaching the peak levels of 2007. Last year’s slowing growth in China and a European recession, coupled with talks of the Federal Reserve’s “tapering” of monetary stimulus, didn’t provide the EMSCI index any help over the last few years.

With all the distracting drama currently taking place in Washington D.C., it’s a relief to see some other indications of improvement. For starters, China’s most recent PMI manufacturing index results showed continued improvement, reaching a level of 51.1 – up from August and signaling a reversal from contraction earlier this year (levels above 50 point to expansion). Chinese government leaders are continuing their migration from an externally export-driven economy to an internally consumer-driven economy. Despite the shift, China is still targeting a respectable +7.5% GDP economic growth target, albeit a slower level than achieved in the past.

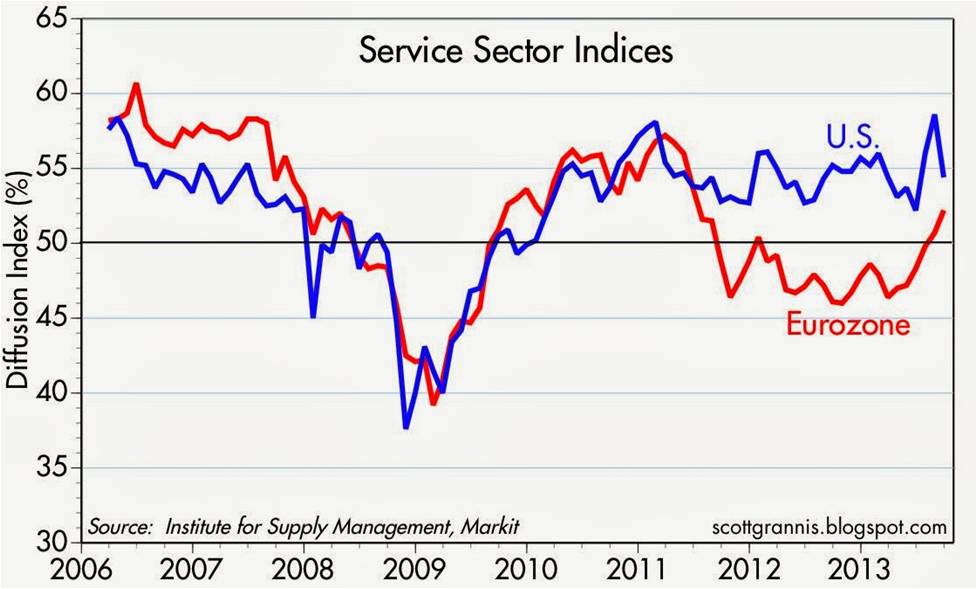

Adding to emerging market optimism is Europe’s apparent economic turnaround (or stabilization). As you can see from the chart below, the European Institute for Supply Management (ISM) service sector index has lately shown marked improvement. If the European and Chinese markets can sustain these recovering trends, these factors bode well for emerging market financial returns.

Source: Calafia Beach Pundit

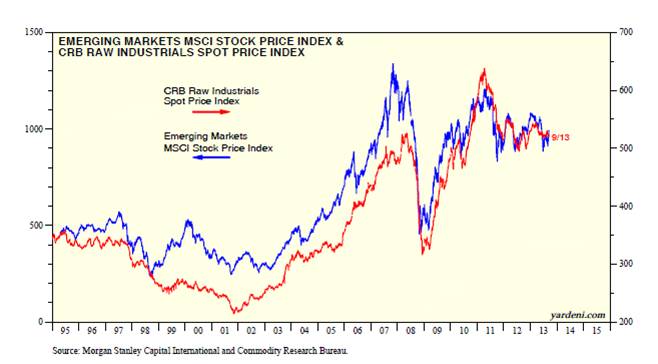

While it is clear these developments are helping the rebound in emerging market indices, it is also clear the supply-demand relationship in commodities will coincide with the next big up or down move in developing markets. Ed Yardeni, strategist and editor of Dr. Ed’s Blog, recently wrote a piece showing the tight correlation between emerging market stock prices and commodity prices (CRB Index). His conclusions come as no surprise to me given these resource-rich markets and their dependence on Chinese demand along with commodity needs from other developed countries. Expanding populations and rising standards of living in emerging market countries have and will likely continue to position these countries well for long-term commodity price appreciation. The development of new, higher-value service and manufacturing sectors should also lead to sustainably improved growth in these emerging markets relative to developed economies.

Source: Dr. Ed’s Blog

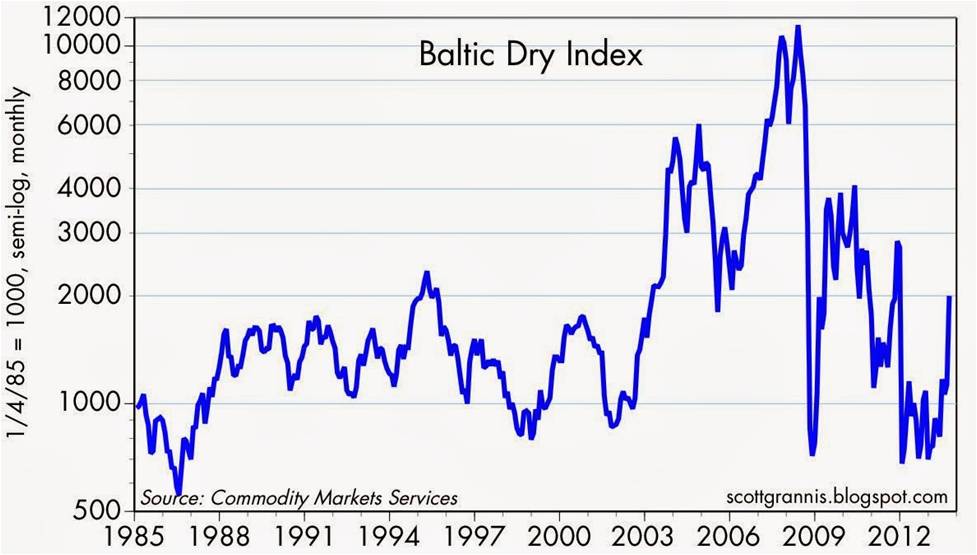

Adding fuel to the improving emerging market case is the advancement in the Baltic Dry Index (see chart below). The recent upward trajectory of the index is an indication that the price for moving major raw materials like coal, iron ore, and grains by sea is rising. This statistical movement is encouraging, but as you can see it is also very volatile.

Source: Calafia Beach Pundit

While the emerging markets are quite unpredictable and have been out-of-favor over the last few years, a truly diversified portfolio needs a healthy dosage of this international exposure. You better check a pulse before you put a nail in the coffin – the emerging markets are not dead yet.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including emerging market ETFs, but at the time of publishing, SCM had no direct position in EEM, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

U.S. Small-Caps Become Global Big Dog

With the emerging market currencies and financial markets under attack; Japan’s Nikkei index collapsing in the last three weeks; and the Federal Reserve hinting about its disciplinarian tapering of $85 billion in monthly QE3 bond purchases, one would expect higher beta small cap stocks to get hammered in this type of environment.

Before benchmarking results in the U.S., let’s take a closer look at some of the international carnage occurring from this year’s index value highs:

- Japan: -19% (Nikkei 225 index)

- Brazil: -22% (IBOVESPA index)

- Hong Kong: -12% (Hang Seng index)

- Russia: -19% (MICEX/RTS indexes)

Not a pretty picture. Given this international turmoil and the approximately -60% disintegration in U.S. small-cap stock prices during the 2007-2009 financial crisis, surely these economically sensitive stocks must be getting pummeled in this environment? Well…not necessarily.

Putting the previously mentioned scary aspects aside, let’s not forget the higher taxes, Sequestration, and ObamaCare, which some are screaming will push us off a ledge into recession. Despite these headwinds, U.S. small-caps have become the top dog in global equity markets. Since the March 2009 lows, the S&P 600 SmallCap index has more than tripled in value ( about +204%, excluding dividends), handily beating the S&P 500 index, which has advanced a respectable +144% over a similar timeframe. Even during the recent micro three-week pullback/digestion phase, small cap stocks have retreated -2.8% from all-time record highs (S&P 600 index). Presumably higher dividend, stable, globally-diversified, large-cap stocks would hold up better than their miniature small-cap brethren, but that simply has not been the case. The S&P 500 index has underperformed the S&P 600 by about -80 basis points during this limited period.

How can this be the case when currencies and markets around the world are under assault? Attempting to explain short-term moves in any market environment is a hazardous endeavor, but that has never slowed me down in trying. I believe these are some of the contributing factors:

1) No Recession. There is no imminent recession coming to the U.S. As the saying goes, we hear about 10 separate recessions before actually experiencing an actual recession. The employment picture continues to slowly improve, and the housing market is providing a slight tailwind to offset some the previously mentioned negatives. If you want to fill that half-full glass higher, you could even read the small-cap price action as a leading indicator for a pending acceleration in a U.S. cyclical recovery.

2) Less International. The United States is a better house in a shaky global neighborhood (see previous Investing Caffeine article), and although small cap companies are expanding abroad, their exposure to international markets is less than their large-cap relatives. Global investors are looking for a haven, and U.S. small cap companies are providing that service now.

3) Inflation Fears. Anxiety over inflation never seems to die, and with the recent +60 basis point rise in 10-year Treasury yields, these fears appear to have only intensified. Small-cap stocks cycle in and out of favor just like any other investment category, so if you dig into your memory banks, or pull out a history book, you will realize that small-cap stocks significantly outperformed large-caps during the inflationary period of the 1970s – while the major indexes effectively went nowhere over that decade. Small-cap outperformance may simply be a function of investors getting in front of this potential inflationary trend.

Following the major indexes like the Dow Jones Industrials index and reading the lead news headlines are entertaining activities. However, if you want to become a big dog in the investing world and not get dog-piled upon, then digging into the underlying trends and market leadership dynamics of the market indexes is an important exercise.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) including emerging market ETFs, IJR, and EWZ, but at the time of publishing, SCM had no direct position in Hong Kong ETFs, Japanese ETFs, Russian ETFs, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

How Sweet it Is: Sugar Prices Near 30-Year High

The Cap'n Hangin' with the Crunch Berry Beast

The cost of a sugar coma has gone up, making my Cap’n Crunch with Crunch Berries craving a pricier endeavor. It’s seems like almost yesterday when I was crouched over my sugar cereal on a Saturday morning watching cartoons – hey wait, maybe that was last weekend? Regardless of the timeframe, prices for sugar have not been this high since Coke and Pepsi used sugar, rather than corn syrup, in their 1970s formulations and Cuba was the world’s largest sugar producer.

What’s the reason for the +67% price rise in sugar this year*? There are several reasons:

1) Disappointing Crops: India is the largest consumer of sugar at 23.5 million tons and a very significant producer of the sweetener. Due to deficient rainfall in the northeast and southern regions in India (caused in part by El Niño conditions), the country is estimated to need more than double the imports of the good this year. Disappointing crops in Brazil have also contributed to the tightening global supply. India and Brazil account for about 40% of global sugar supplies.

2) Forward Buying / Hedging: The supply-demand dynamics of the sugar market have caused certain high sugar-consuming countries, like Egypt and Mexico, to buy large stockpiling purchases – further pushing up prices. Beyond consumer and speculators, global food and beverage companies from the likes of Kraft, General Mills and ConAgra Foods have been purchasing futures to hedge the risk of additional price hikes.

3) Oil Increase Buoys Ethanol: Oil’s +59% price increase this year to about $70 per barrel has provided additional price support through increased demand for sugar-based ethanol.

Weather, oil demand, and sentiment may change thereby easing the cost burden of higher priced sugar goods, but irrespective of sugar prices you can rest assured my Cap’n Crunch with Crunch Berries addiction will remain resilient.

*Source: The Financial Times (8-7-09).

Read Financial Times Article on Sugar Here

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

{kind=link}