Posts tagged ‘biases’

Sitting on the Sidelines: Fear & Selective Memory

Fear is a motivating (or demotivating) emotion that can force individuals into suboptimal actions. The two main crashes of the 2000s (technology & housing bubbles) coupled with the mini-crises (e.g., flash crash, European crisis, debt ceiling, sequestration, fiscal cliff, etc.) have scared millions of investors and trillions of dollars to sit on the sidelines. Financial paralysis may be great in the short-run for bruised psyches and egos, but for the passive onlookers, the damage to retirement accounts can be crippling.

Selective memory is a great coping mechanism for those investors sitting on the sidelines as well. Purposely forgetting your wallet at a group dinner may be beneficial in the near-term, but repeated incidents will result in lost friends over the long-run. Similarly, most gamblers frequenting casinos tend to pound their chests when bragging about their wins, however they tend to conveniently forget about all the losses. These same reality avoidance principles apply to investing.

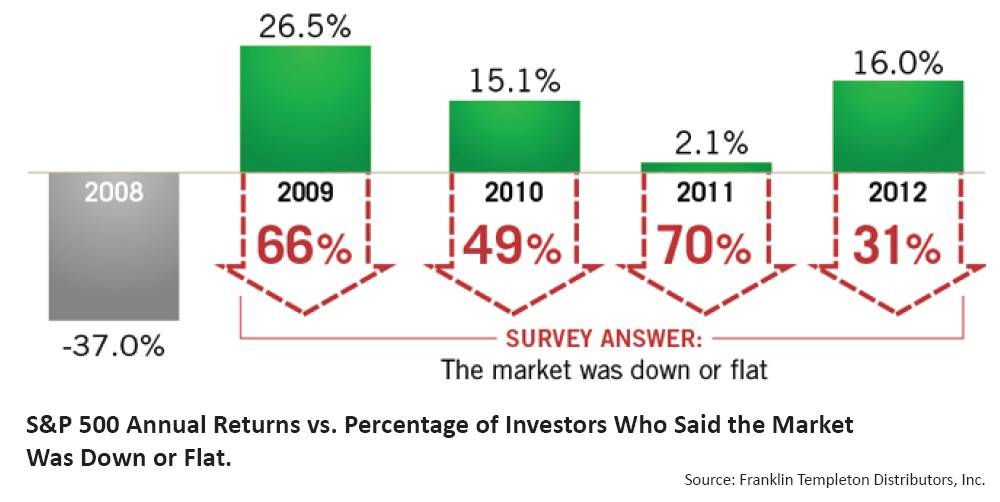

A recent piece written by CEO Bill Koehler at Tower Wealth Managers, entitled The Fear Bubble highlights a survey conducted by Franklin Templeton. In the study, investors were asked how the stock market performed in 2009-2012. As you can see from the chart below, perception is the polar opposite of reality (actual gains far exceeded perceived losses):

Source: Franklin Templeton via Tower Wealth Managers

With so many investors sitting on the sidelines in cash or concentrated in low-yielding bonds and gold, I suppose the results shouldn’t be too surprising. Once again, selective memory serves as a wonderful tool to bury the regrets of missing out on a financial market recovery of a lifetime.

Humans also have a predisposition to seek out people who share similar views, even though accumulating different viewpoints ultimately leads to better decisions. Morgan Housel at The Motley Fool just wrote an article, Putting a Gap Between You and Stupid, explaining how individuals should seek out others who can help protect them from harmful biases. A scientific study referenced in the article showed how the functioning of biased brains literally shuts down:

“During the 2004 presidential election, psychologist Drew Westen of Emory University and his colleagues studied the brains of 15 “committed” Democrats and 15 “committed” Republicans with an MRI scanner. Each group was shown a collection of contradictory statements made by George W. Bush and John Kerry. Not surprisingly, the partisans were quick to call out contradictions made by the opposing party, and made up all kinds of justifications to rationalize quotes made by their own side’s candidate. But here’s what’s scary: The participants weren’t just being stubborn. Westen found that areas of their brains that control reasoning and logic virtually shut down when confronted with a conflicting view of their preferred candidate.”

Rather than letting emotions rule the day, the proper approach is to stick to unbiased numbers like valuations, yields, fees, and volatility. If you continually make mistakes; you aren’t disciplined enough; or you don’t like investing; then find a trusted advisor who uses an objective financial approach. Opportunistically taking advantage of volatility, instead of knee-jerk reactions is the preferred approach. For those people sitting on the sidelines and using selective memory, you may feel better now, but you will eventually have to get in the game, if you don’t want to lose the retirement account game.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing, SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is the information to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Experts vs. Dart-Throwing Chimps

Daniel Kahneman, a professor of psychology at Princeton University, knows a few things about human behavior and decision making, and he has a Nobel Prize in Economics to prove it. We live in a complex world and our brains will often try to compensate by using shortcuts (or what Kahneman calls “heuristics” and “biases”), in hopes of simplifying complicated situations and problems.

When our brains become lazy, or we are not informed in a certain area, people tend to also listen to so-called experts or pundits to clarify uncertainties. In the process of their work, Kahneman and other researchers have discovered something – experts should be listened to as much as monkeys. Frequent readers of Investing Caffeine understand my shared skepticism of the talking heads parading around on TV (read first entry of 10 Ways to Destroy Your Portfolio)

Here is how Kahneman describes the reliability of professional forecasts and predictions in his recently published bestseller, Thinking, Fast and Slow:

“People who spend their time, and earn their living, studying a particular topic produce poorer predictions than dart-throwing monkeys who would have distributed their choices evenly over the options.”

Most people fall prey to this illusion of predictability created by experts, or this idea that more knowledge equates to better predictions and forecasts. One of the factors perpetuating this myth is the rearview mirror. In other words, human’s ability to concoct a credible story of past events creates a false confidence in peoples’ ability to accurately predict the future.

Here’s how Kahneman describes the phenomenon:

“The idea that the future is unpredictable is undermined every day by the ease with which the past is explained…Our tendency to construct and believe coherent narratives of the past makes it difficult for us to accept the limits of our forecasting ability. Everything makes sense in hindsight, a fact financial pundits exploit every evening as they offer convincing accounts of the day’s events. And we cannot suppress the powerful intuition that what makes sense in hindsight today was predictable yesterday. The illusion that we understand the past fosters overconfidence in our ability to predict the future.”

Even when experts are wrong about their predictions, they tend to not accept accountability. Rather than take responsibility for a bad prediction, Philip Tetlock says the errors are often attributed to “bad timing” or an “unforeseeable event.” Philip Tetlock, a psychologist at the University of Pennsylvania did a landmark twenty-year study, which was published in his book Expert Political Judgment: How Good Is It? How Can We Know? (read excellent review in The New Yorker). In the study Tetlock interviewed 284 economic and political professionals and collected more than 80,000 predictions from them. The results? The experts did worse than blind guessing.

Based on the extensive training and knowledge of these experts, many of them develop a false sense of confidence in their predictions. Or as Tetlock explains it, “They [experts] are just human in the end. They are dazzled by their own brilliance and hate to be wrong. Experts are led astray not by what they believe, but by how they think.”

Brain Blunders and Stock Picking

The buyer of a stock thinks the price will go up and the seller of a stock thinks the price will go down. Both participants engage in the transaction because they believe the current stock price is wrong. The financial services industry is built largely on this phenomenon that Kahneman calls an “illusion of skill,” or ability to exploit inefficient market pricing. Relentless advertisements and marketing pitches continually make the case that professionals can outperform the markets, but this is what Kahneman found:

“Although professionals are able to extract a considerable amount of wealth from amateurs, few stock pickers, if any, have the skill needed to beat the market consistently, year after year. Professional investors, including fund managers, fail a basic test of skill: persistent achievement…Skill in evaluating the business prospects of a firm is not sufficient for successful stock trading, where the key question is whether the information about the firm is already incorporated in the price of its stock. Traders apparently lack the skill to answer this crucial question, but they appear ignorant of their ignorance.”

For the few managers that actually do outperform, Kahneman assigns luck to the outcome, not skill:

“For a large majority of fund managers, the selection of stocks is more like rolling dice than like playing poker. Typically at least two out of three mutual funds underperform the overall market in any given year…The successful funds in any given year are mostly lucky; they have a good roll of the dice.”

The picture for individual investors isn’t any prettier. Evidence from Terry Odeam, a finance professor at UC Berkeley, who studied 100,000 individual brokerage account statements and about 163,000 trades over a seven-year period, was not encouraging. He discovered that stocks sold actually did +3.2% better than the replacement stocks purchased. And this detrimental impact on performance excludes the significant expenses related to trading.

In response to Odean’s work, Kahneman states:

“It is clear that for the large majority of individual investors, taking a shower and doing nothing would have been a better policy than implementing the ideas that came to their minds….Many individual investors lose consistently by trading, an achievement that a dart-throwing chimp could not match.”

In a future Odean paper titled, “Trading is Hazardous to your Wealth,” Odean and his colleague Brad Barber also proved that “less is more.” The results showed the most active traders had the weakest performance, and those traders who traded the least had the best returns. Interestingly, women were shown to have better investment results than men.

Regardless of whether someone is listening to an expert, fund manager, or individual investor, what Daniel Kahneman has discovered in his long, illustrious career is that humans consistently make errors. If you are wise, you will heed Kahneman’s advice by stealing the expert’s darts and handing them over to the chimp.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

{kind=link}