Posts tagged ‘baby boomers’

Flat Pancakes & Dividends

Over the last 18 months, stock prices have been flat as a pancake. Absent a few brief China and recessionary scares, the Dow Jones Industrial Average index has spent most of 2015 and 2016 trading between the relatively tight levels of 17,000 – 18,000. Record corporate profits and faster growth than other developed and developing markets have created a tug-of-war with countervailing factors. A strong dollar, reversal in monetary policy, geopolitical turmoil, and volatile commodity markets have produced a neutralizing struggle among corporate executives with deep financial pockets and short arms. In this environment, share buybacks, stable profit margins, and growing dividends have taken precedence over accelerated capital investments and expensive new-hires.

With flat stock prices and interest rates at unprecedented low levels, it’s during times like these that stock investors really appreciate the appetizing flavor of stable, growing dividends. To this day, I still find it almost impossible to fathom how investors are burning money by irrationally speculating in $7 trillion in negative interest rate bonds (see Retire at Age 90).

Historically there are very few periods in which stock dividend yields have exceeded bond yields (2.1% S&P yield vs. 1.8% 10-Year Treasury yield). As I showed in my Dividend Floodgates article, for roughly 50 years (1960 – 2010), the yield on the 10-Year Treasury Notes have exceeded the dividend yield on stocks (S&P 500) – that longstanding trend does not hold today.

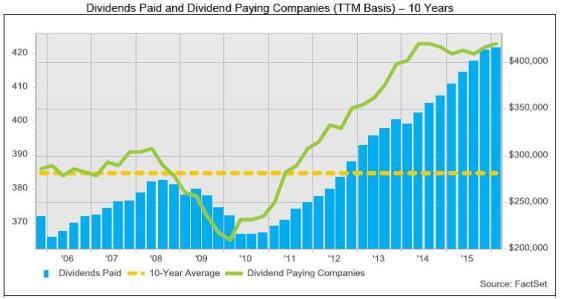

In the face of the competitive stock market, several trends are contributing to the upward trajectory in dividend payments (see chart below).

#1.) Corporate profits (ex-Energy) are growing and at/near record levels. Earnings are critical in providing fertile ground for dividend growth.

#2.) Demographics, plain and simple. As 76 million Baby Boomers transition into retirement, their income needs escalate. These shareholders whine and complain to corporate executives to share the spoils and increase dividends.

#3.) Low interest rates and disinflation are shrinking the available pool of income generating assets. As I pointed out above, when trillions of dollars are getting thrown into negative yielding investments, many investors are flocking to alternative income-generating assets…like dividend paying stocks.

Source: FactSet

The Power of Dividends (Case Studies)

Most people don’t realize it, but over the last 100 years, dividends have accounted for approximately 40% of stocks’ total return as measured by the S&P 500. In other words, using history as a guide, if you initially invested in a stock XYZ at $100 that appreciated in value to $160 (+60%) 10 years later, that stock on average would have supplied an incremental $40 in dividends (40%) over that period, creating a total return of 100%.

Rather than using a hypothetical example, here are a few stock specific illustrations that highlight the amazing power of compounding dividend growth rates. Here are two “Dividend Aristocrats” (stocks that have increased dividends for at least 25 consecutive years):

- PepsiCo Inc (PEP): PepsiCo has increased its dividend for an astonishing 44 consecutive years. Today, the dividend yield is 2.9% based on the current share price. But had you purchased the stock in June 1972 for $1.60 per share (split-adjusted), you would currently be earning a +188% dividend yield ($3.01 dividend / $1.60 purchase price), which doesn’t even account for the +6,460% increase in the share price ($104.96 per share today from $1.60 in 1972). Over that 44 year period, the split-adjusted dividend has increased from about $0.02 per share to an annualized $3.01 dividend per share today, which equates to a mind-blowing +16,153% increase. On top of the $103 price appreciation, assuming a conservative 5% dividend reinvestment rate, my estimates show investors would have received more than $60 in reinvested dividends, making the total return that much more gargantuan.

- Emerson Electric Co (EMR): Emerson Electric too has had an even more incredible streak of dividend increases, which has now extended for 59 consecutive years. Emerson currently yields a respectable 3.6% rate, but if you purchased the stock in June 1972 for $3.73 per share (split-adjusted), you would currently be earning a +51% dividend yield ($1.92 dividend / $3.73 purchase price), which doesn’t even consider the +1,423% increase in the share price ($53.31 per share today from $3.73 in 1972).

There is never a shortage of FUD (Fear, Uncertainty, and Doubt), which has kept stock prices flat as a pancake over the last couple of years, but market leading franchise companies with stable/increasing dividends do not disappear during challenging times. Record profits (ex-energy), demographics, and a scarcity of income-generating investment alternatives are all contributing factors to the increased appetite for dividends. If you want to sweeten those flat pancakes, do yourself a favor and pour some quality dividend syrup over your investment portfolio.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs) and PEP, but at the time of publishing had no direct position in EMR or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Ration or Tax: Eating Cake Not an Option

We live in an instant gratification society that would like everything for free ( like my pal Bill Maher), which explains why we want to have our healthcare cake and eat it too. I think George Will said it best when discussing universal healthcare coverage, “If you think health care is expensive now, just wait until it is free.” Look, I love free stuff too, like the rest of us, whether it’s free sausage sample at Costco (COST) or a breath mint at the Olive Garden (DRI). But regrettably, exploding deficits come at a price.

With midterm elections coming up, the issue of healthcare is once again front and center. The majority party feels like a checkbook is a solution to healthcare prosperity. Can you really look me in the eyes and say covering additional 32 million uninsured Americans is going to save us money. The government hasn’t exactly built a ton of credibility with the disastrous train-wreck we call Medicare, which is already carrying 45 million covered passengers.

The minority party hasn’t done a lot better with the layering of the 2006 unsustainable Medicare Part D drug plan. Conservatives are campaigning on “repeal and replace” and that is great, but where are the cuts?

There are only two solutions to our current healthcare problem: ration or tax (read Plucking Feathers of Taxpaying Geese). Is healthcare a right or privilege? I don’t know, but if we want to cover current obligations, or add 32 – 50 million more uninsured, then we will be required to cut expenses (ration) to pay for increased benefits and/or increase taxes to cover additional benefits. I would love to cover all Americans, along with the starving children in Africa too, but unfortunately we are limited by our resources. Writing checks with borrowed money will only last for so long.

How severe are the exploding healthcare costs, which are covering the graying of the 76 million baby boomers? Here’s how Forbes describes the unsustainable Medicare obligations:

The Medicare Trustees tell us that Medicare’s expected future obligations exceeded premiums and dedicated taxes by $89 trillion (measured in current dollars). No, that’s not a misprint. To put that number in perspective, Medicare’s liability is about 5 1/2 times the size of Social Security’s ($18 trillion) and about six times the size of the entire U.S. economy.

Not a pretty picture. These estimates look pretty far in the future, but even more bare bone figures arrive at a still frightening $33 trillion. Take a look at healthcare spending forecasts as a percentage of GDP – even the lowest estimates are depressing:

Source: National Center for Policy Analysis via Forbes

In our increasingly flat globalized world, competition between countries is becoming even more intense. We are in a marathon race for improved standards of living, and all these debts and deficits are dragging us down like an anchor tied to our legs. Even without considering other massive entitlements like Social Security, healthcare alone has the potential of grinding our economy to a halt. Politicians are great at promising more benefits and tax cuts in exchange for your votes, but true leadership requires delivering the sour medicine necessary for future prosperity. Before we eat the healthcare cake, let’s raise the money to buy the cake first.

Read more about the Medicare Explosion on Forbes

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, but at the time of publishing SCM had no direct position in COST, DRI, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

From Pooches to Profits

Oh, I’m sure you’ve seen them – those nauseating people that willingly accept facial tongue baths from their pets and dress them up in ridiculous costumes. Hey, wait a second… I guess I’m one of those annoying people too. My wife and I were just debating which Halloween attire we should get for our dog…Cound Dogula or Barkenstein? But we are not the only fanatics humanizing our pets, as Petsmart (PETM) recently outlined in their recent analyst day. Sixty-two percent of U.S. households own a pet and if you just add up all the cats and dogs, the total reaches 171 million pets.

This is no small business – according to PETM, the industry exceeded $43 billion in 2008, spanning a whole variety of products and services, including food, veterinary care, supplies, and grooming/boarding services. PETM is collecting its growing share of the market at 14%, and I expect this share to increase over time.

What’s fueling the growth of the sector? For one, demographics is a contributor. As many Baby Boomers have become “empty-nesters” (kids move on) over time, they tend to fill that void with a pet. In addition, many working marriages have pushed having kids to the back-burner and choose to substitute a furry baby as a surrogate.

These trends have translated into vibrant growth for PETM over the years. The company has over 1,150 stores and 738 Banfield veterinary partnership locations, not to mention a significant rise in hotels. No, these are not the Four Seasons, but rather pet hotels that you can board Fido in when you take that family vacation to Hawaii or where guilt-ridden families can drop your friend off for doggy Day camp. These 156 pet hotels, which are included as part of PETM’s “Services,” continue to gain traction as they plan to open 20 new locations per year. Currently, services represents 11% of PETM’s sales (up from 8.8% in 2006), growing faster than overall sales with a significantly higher profit margins than the corporate average.

Source: Petsmart 2009 Analyst Day

Not everything is peachy keen as the company acknowledges the negative impact of unemployment, lower discretionary consumer spending and higher savings rate. As a result, PETM’s high margin “Hardgoods” category has gotten clobbered lately – even with more stable sales in non-discretionary categories like “Food.” Despite the economic developments, the company is not sitting on its hands. Not only are they focusing on driving sales through store pet adoptions (approaching four million on a cumulative basis), but the company is also reaping the rewards of its Pet Perks customer database to optimize sales performance. Petsmart has even taken a page out of Costco’s (COST) book with its focus on private label brands.

Beyond sales growth initiatives, the company has also been tightening their spending belt. For example, PETM is reducing capital expenditures from 6.4% of sales ($294 million) in 2007 to an estimated 2.2% ($120 million) this year. In addition, PETM is working on process improvements, space optimization, labor scheduling, and other cost-cutting initiatives.

The fruits of these labors are creating results. Just last week at their analyst meeting, PETM raised their 2009 earnings per share forecast to a range of $1.43 – $1.51 (from previous estimate of $1.37 – $1.45). Based on 2010 Wall Street estimate of $1.54, PETM’s stock currently trades at a reasonable 16.5x P/E multiple. On a free cash flow basis, the multiple on the estimated $226 million this year is even more attractive (see my article on cash flow investing).

Halloween is just around the corner, so maybe beyond picking up a doggie cardigan for the crisp fall weather, maybe you should consider some PETM shares too.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management and its client accounts have no direct position in COST shares at the time this article was originally posted. Slome Sidoxia Fund does have a long position in PETM shares at the time this article was originally posted. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Healthcare Reform: The Brutal Reality of Aging Demographics

The global population is aging and that is a bad trend for healthcare costs.

There’s no question healthcare reform is required. The Economist’s cover story, This is Going to Hurt, addresses this problem head-on:

“Even though one dollar in every six generated by the world’s richest economy is spent on health—almost twice the average for rich countries—infant mortality, life expectancy and survival-rates for heart attacks are all worse than the OECD average. Meanwhile, because health insurance is so expensive, nearly 50m Americans, an obscene number in such a rich place, have none; those that are insured pay through the nose for their cover, and often find it bankruptingly inadequate if they get seriously ill or injured.”

The real question is not whether we have a problem, but rather how are we going to approach it? Estimates of the current healthcare congressional plans put estimates for reform between $1.2 trillion and $1.6 trillion over 10 years. I tend to side with George Will when discussions center on costs, “If you think health care is expensive now, just wait until it is free.”

One of the reasons healthcare costs are exploding is because of our aging demographics. The 76 million “Baby Boomers” are entering their golden years, and as a result are consuming more healthcare products and services. Because our system is so convoluted and opaque, true healthcare competition cannot flourish. Rather, patients expect a cheap “all-you-can-eat” smorgasbord of services without consideration of cost. Unfortunately, the aging trend of our global population (especially in the developed countries like the U.S.) has put our economy on track for a disastrous train-wreck.

The Economist’s article, A Slow Burning Fuse, crystallizes the aging trend into proper perspective by providing some interesting statistics. At the beginning of the last century, in 1900, the average life expectance at birth was approximately 30. Today, the average life expectancy has more than doubled to 67 years (and 78 years in richer developed countries).

Read Full Economist Article, A Slow Burning Fuse

A second major cause of aging societies is the decline in number of children families are having. During the early 1970s, women on average were having 4.3 children each. Now the average is about 2.6 children (and 1.6 children in developed countries). What these statistics mean is that the taxable younger workforce is shrinking (growing slower), therefore unable to adequately feed the swelling appetites of the aging, healthcare-hungry global populations.

My solution would focus on the following:

Technology: Yes, chopping down trees, wasting years of our lives filling out and storing library-esque piles of medical forms is so 20th Century.

Consolidation of Insurers: And do we need dozens of different insurers on different billing platforms? Reducing inefficient and undercapitalized competitors down to a common technological digital record and billing platform makes common sense to me. Although I love competition, if I look at things like cell phones, cable, or even local grocery stores, there is a law of diminishing return whereby inefficiencies eventually outweigh benefits of competition.

Fewer Late Life Benefits: Nearly 30 percent of Medicare spending pays for care in the final year of patients’ lives, according to George Will. Does it really make sense to pay such a high proportion of costs for the last 1-2% of our lives? Other countries, including European ones, deny certain costly services for elderly patients. Does spending over $50,000 on certain cancer treatments for a few extra months of life seem equitable? If elderly ill patients are in the financial position to pay, then that’s great. Otherwise, at some point, the ethical question has to be faced – what is an extra month of human life worth?

Not really a rosy subject, but an important one. I’m confident we can solve these problems, if addressed immediately, or else future generations will be saddled with a more disastrous problem to heal.

Wade W. Slome, CFA, CFP® www.Sidoxia.com

{kind=link}