Posts tagged ‘Asset Allocation’

Invest or Die

Seventy-six million Baby Boomers are earning near 0% (or negative rates) and aren’t getting any younger in the process, which is forcing them and others to decide…invest or die. The risk of outliving your savings is becoming a larger reality these days. Demographics and economics are dictating that our aging population is living longer and earning less due to generationally low interest rates.

Richard Fisher, the former Dallas Federal Reserve president, understands these looming dynamics. Fisher has identified how low-interest rates are increasing investor discontent by pushing consumers to save more in order to meet retirement needs. The unintended consequence from low rates, he said, is “you’re going to have to save a hell of a lot more before you consume.”

Besides saving, the other option investors have is to lower your standard of living. For example, you could continually eat mac & cheese and sleep in a tent – that is indeed one way you could save money. However, your kids and/or desired lifestyle may make this way of life unpalatable for all. Rather, the proper approach to achieving a comfortable standard of living requires you to invest more efficiently and prudently.

What a lot of individuals fail to understand is that accepting too much risk can be just as dangerous as being too conservative, over the long run. Case in point, depositing your savings into a CD at current interest rates (near 0%) is the equivalent of burning your cash, as any income produced is overwhelmed by the deleterious effects of inflation. It would take more than a lifetime of CD interest income to equal equity returns earned over the last seven years. Since early 2009, stocks have more than tripled in value.

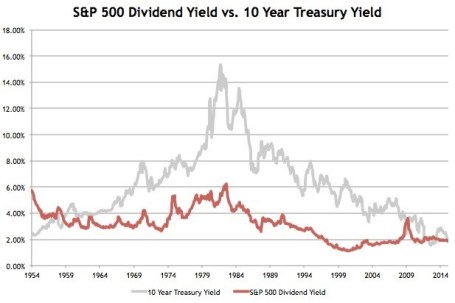

Given the prevailing economic and demographic trends, investors are slowly realizing the attractive income-producing nature of stocks relative to bonds. It has been a rare occurrence, but stocks, as measured by the S&P 500, continue to yield more than 10-Year Treasury Notes (2.0% vs. 1.6%, respectively) – see chart below. The picture for bonds looks even worse in many international markets, where $13 trillion in bonds are yielding negative interest rates. Unlike bonds, which generally pay fixed coupon payments for years at a time, stocks overall have historically increased their dividend payouts by approximately 6% annually.

Source: Avondale Asset Management

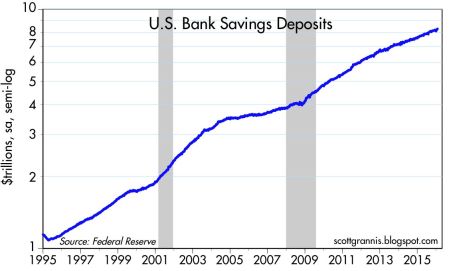

With a scarcity of attractive investment alternatives available, investors will eventually be forced to adopt higher levels of equity risk, like it or not. However, this dynamic has yet to happen. Currently, actions are speaking louder than words, and as you can see, risk aversion reigns supreme with Americans tucking over $8 trillion dollars under their mattress (see chart below), in the form of savings accounts, earning next to nothing and jeopardizing retirements.

Source: Calafia Beach Pundit

Even if you fall into the camp that believes rates are artificially low by central bank printing presses, that doesn’t mean every company is recklessly leveraging their balance sheets up to the hilt. Many companies are still scared silly from the financial crisis and conservatively managing every penny of expense, like a stingy retiree living on a fixed income. Thanks to this reluctance to spend and hire aggressively, profit margins are at/near record highs. This financial stewardship has freed up corporations’ ability to pay higher dividends and implement discretionary stock buybacks as means to return capital to shareholders.

With the dovish Fed judiciously raising interest rates – only one rate hike of 0.25% over a decade (2006 – 2016) – there are no signs this ultra-low interest rate environment is going to turn aggressively higher anytime soon. Until economic growth, inflation, and interest rates return with a vengeance, and the persistent investor risk aversion abates, it behooves all the cash hoarders to….invest or die!

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold positions in certain exchange traded funds (ETFs), but at the time of publishing had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Thrill of the Chase

Men (and arguably women to a lesser extent) enjoy the process of hunting for a mate. Chasing the seemingly unattainable event aligns with man’s innate competitive nature. But the quest for the inaccessible is not solely limited to dating. When it comes to other aspirational categories, humans also want what they cannot have because they revel in a challenge. Whether it’s a desirable job, car, romantic partner, or even an investment, people bask in the pursuit.

For many investment daters and trading speculators, 2008-2009 was a period of massive rejection. Rather than embracing the losses as a new opportunity, many wallowed in cash, CDs, bonds, and/or gold. This strategy felt OK until the massive 5-year bull market went on a persistent, upward tear beginning in 2009. Now, as the relentless bull market has continued to set new all-time record highs, the negative sentiment cycle has slowly shifted in the other direction. Back in 2009, many investors regretted owning stocks and as a result locked in losses by selling at depressed prices. Now, the regret of owning stocks has shifted to remorse for not owning stocks. Missing a +23% annual return for five years, while getting stuck with a paltry 0.25% return in a savings account or 3-4% annual return achieved in bonds, can harm the psyche and make savers bitter.

Greed hasn’t fully set in like we witnessed in the late period of the 1990s tech boom, but nevertheless, some of the previous overly cautious “sideliners” feel compelled to now get into the stock game (see Get Out of Stocks!*) or increase their equity allocation. Like a desperate, testosterone-amped teen chasing a prom date, some speculators are chasing stocks, regardless of the price paid. As I’ve noted before, the overall valuation of the stock market seems quite reasonable (see PE ratio chart in Risk Aversion Declining – S. Grannis), despite selective pockets of froth popping up in areas like biotech stocks, internet companies, and junk bonds.

Even if chasing is a bad general investment practice, in the short-run, chasing stocks (or increasing equity allocations) may work because overall prices of stocks remain about half the price they were at the 2000 bubble peak (see Siegel Bubblicious article). How can stocks be -50% off when stock prices today (S&P 500) are more than +25% higher today than the peak in 2000? Plain and simply, it’s the record earnings (see It’s the Earnings Stupid). In the latest Sidoxia newsletter we highlighted the all-time record corporate profits, which are conveniently excluded from most stock market discussions in the blogosphere and other media outlets.

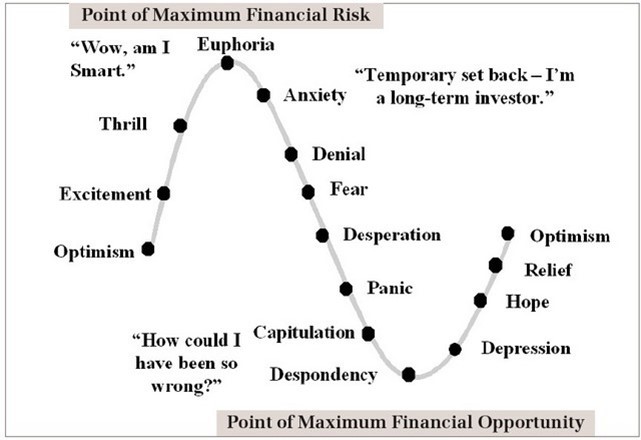

The Investor’s Emotional Roller Coaster (Perceived Risk vs Actual Risk)

The “Thrill of the Chase” is but a single emotion on the roller coaster sentiment spectrum (see Barry Ritholtz chart in Sentiment Cycle of Fear and Greed). The problem with the above chart is many investors confuse actual risk from perceived risk. Many investors perceive the “euphoric” stage of an economic cycle (top of the chart) as low-risk, when in actuality this point reflects peak risk. One can look back to the late 1990s and early 2000 when technology shares were priced at more than 100x years in earnings and every hairdresser, cabdriver and relative were plunging their life savings into stocks. The good news from my vantage point is we are a ways from that euphoric state (asset fund flows and consumer confidence are but a few data points to support this assertion).

The key to reversing the sentiment roller coaster is to follow the thought process of investment greats who learned to avoid euphoria in up markets:

“I’m always more depressed by an overpriced market in which many stocks are hitting new highs every day than by a beaten-down market in a recession.” -Peter Lynch

“Be fearful when others are greedy, and be greedy when others are fearful.” –Warren Buffett

While the “Thrill of the Chase” can seem exciting and a rational strategy at the time, successful long-term investors are better served by remaining objective, unemotional, and numbers-driven. If you don’t have the time, interest, or emotional fortitude to be disciplined, then find an experienced investment manager or advisor to assist you. That will make your emotional roller coaster ride even more thrilling.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

Searching for the Market Boogeyman

With the stock market reaching all-time record highs (S&P 500: 1900), you would think there would be a lot of cheers, high-fiving, and back slapping. Instead, investors are ignoring the sunny, blue skies and taking off their rose-colored glasses. Rather than securely sleeping like a baby (or relaxing during a three-day weekend) with their investment accounts, people are biting their fingernails with clenched teeth, while searching for a market boogeyman in their closets or under their beds.

If you don’t believe me, all you have to do is pick up the paper, turn on the TV, or walk over to the office water cooler. An avalanche of scary headlines that are spooking investors include geopolitical concerns in Ukraine & Thailand, slowing housing statistics, bearish hedge fund managers (i.e., Tepper Einhorn, Cooperman), declining interest rates, and collapsing internet stocks. In other words, investors are looking for things to worry about, despite record corporate profits and stock prices. Peter Lynch, the manager of the Magellan Fund that posted +2,700% in gains from 1977-1990, put short-term stock price volatility into perspective:

“You shouldn’t worry about it. You should worry what are stocks going to be 10 years from now, 20 years from now, 30 years from now.”

Rather than focusing on immediate stock market volatility and other factors out of your control, why not prioritize your time on things you can control. What investors can control is their asset allocation and spending levels (budget), subject to their personal time horizons and risk tolerances. Circumstances always change, but if people spent half the time on investing that they devoted to planning holiday vacations, purchasing a car, or choosing a school for their child, then retirement would be a lot less stressful. After realizing 99% of all the short-term news is nonsensical noise, the next important realization is stocks are volatile securities, which frequently go down -10 to -20%. As much as amateurs and professionals say or think they can profitably predict these corrections, they very rarely can. If your stomach can’t handle the roller-coaster swings, then you shouldn’t be investing in the stock market.

Bear-markets generally coincide with recessions, and since World War II, Americans experience about two economic contractions every decade. And as I pointed out earlier in A Series of Unfortunate Events, even during the current massive bull market, a recession has not been required to suffer significant short-term losses (e.g., Flash Crash, Greece, Arab Spring, Obamacare, Cyprus, etc.). Seasoned veterans understand these volatile periods provide incredible investment opportunities. As Warren Buffett states, “Be fearful when others are greedy, and be greedy when others are fearful.” Fear and panic may be behind us, but skepticism is still firmly in place. Buying during current skepticism is still not a bad thing, as long as greed hasn’t permeated the masses, which remains the case today.

Overly emotional people that make investment decisions with their gut do more damage to their savings accounts than conservative, emotional investors who understand their emotional shortcomings. On the other hand, the problem with investing too conservatively, for those that have longer-term time horizons (10+ years), is multi-pronged. For starters, overly conservative investments made while interest rate levels hover near historical lows lead to inflationary pressures gobbling up savings accounts. Secondly, the low total returns associated with excessively conservative investments will result in a later retirement (e.g., part-time Wal-Mart greeter in your 80s), or lower quality standard of living (e.g., macaroni & cheese dinners vs. filet mignon).

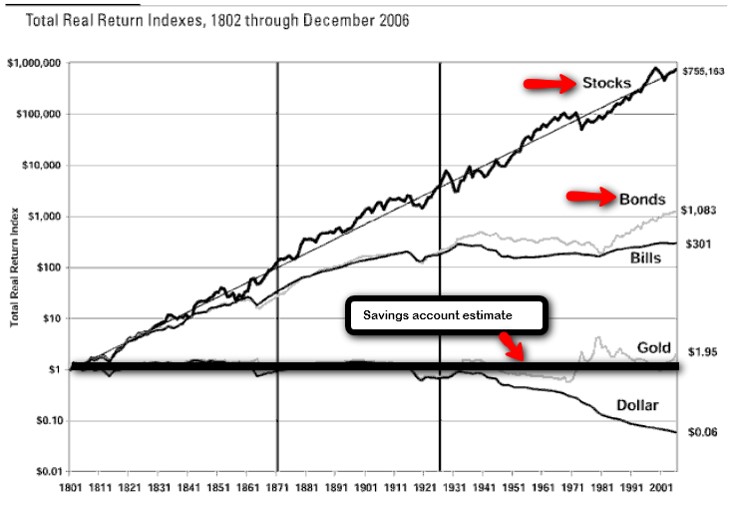

Most people say they understand the trade-offs of risk and return. Over the long-run, low-risk investments result in lower returns than high risk investments (i.e., bonds vs. stocks). If you look at the following chart and ask anyone what their preferred path would be over the long-run, almost everyone would select the steep, upward-sloping equity return line.

Source: Betterment.com / Stocks for the Long Run

Yet, stock ownership and attitudes towards stocks remain at relatively low and skeptical levels (see Gallup survey in Markets Soar and Investors Snore). It’s true that attitudes are changing at a glacial pace and bond outflows accelerated in 2013, but more recently stock inflows remain sporadic and scared money is returning to bonds. Even though it has been over five years, the emotional scars from 2008-2009 apparently still need some time to heal.

Investing in stocks can be very scary and hazardous to your health. For those millions of investors who realize they do not hold the emotional fortitude to withstand the ups and downs, leave the worrying responsibilities to the experienced advisors and investment managers like me. That way you can focus on your job and retirement, while the pros can remain responsible for hunting and slaying the boogeyman.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients hold long positions in certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC Contact page.

The Political Art of Investment Commentators

There are approximately 2 billion people surfing the internet globally and over 150 million bloggers (source: blogpulse.com) spewing their thoughts out into cyberspace. Throw in economists, strategists, columnists, and the talking heads on television, and you can sleep comfortably knowing there will never be a shortage of opinions for investors to sift through. The real question regarding the infinite number of ideas floating around from the “market commentators” is how useful or harmful is all this information? These diverse points of view, like guns, can be useful or dangerous – depending on an investor’s experience and knowledge level. Deciphering the nuances and variances of investment opinions can be very challenging for an untrained investing eye or ear. While there are plenty of diamonds in the rough to be discovered in the investment advice buffet, there are also a plethora of landmines and booby traps that could explode investment portfolios – especially if these volatile opinions are not handled with care.

No Credentials Required

Unlike dentists, lawyers, accountants, or doctors, becoming a market commentator requires little more than a pulse. All a writer, squawker, or blogger really needs is an internet connection, a keyboard, and something interesting or provocative to talk about. Are any credentials required to blast toxic gibberish to the millions among the masses? Unfortunately there are no qualifications required…scary thought indeed.

In order to successfully navigate the choppy investment opinion waters, investors need to be self-aware enough to answer the following key questions:

• What is your investment time horizon?

• What is your risk tolerance? (see also Sleeping like a Baby)

With these answers in hand, you can now begin to evaluate the credibility and track record of the market commentators and match your personal time horizon and risk profile appropriately. Ideally, investors would seek out prudent long-term counsel, but in this instant gratification society we live in, immediate fear and greed sells advertisements and attracts viewers. Even if media producers and editors of all stripes believed focusing on multi-year time horizons is most beneficial for investors, some serious challenges arise. The brutal reality is that concentrating on the lackluster long-term does not generate a lot of advertisement revenue or traffic. The topics of dollar-cost averaging, asset allocation, diversification, and rebalancing are about as exciting as watching an infomercial marathon (OK, actually this is quite funny) or paint dry. More interesting than the sleepy, uninspiring topics of long-term value creation are stories about terrorist threats, DSK sex scandals, Bernie Madoff Ponzi schemes, currency crises, hacking misconduct, bailouts, tsunamis, earthquakes, hurricanes, 50-day moving averages…OK, you get the idea.

Focus on Long-Term and Do Not Succumb to Short-Termism

Regrettably, there is a massive disconnect between the nano-second time horizons of market commentators and the time horizons of most investors. Moreover, this short-termism dispersed instantaneously via Facebook, Google (GOOG), Twitter, and traditional media channels, has sadly infected the psyches and investment habits of ordinary investors. If you don’t believe me, then check out some of the John Bogle’s work, which shows how dramatically investors underperform the benchmark thanks to emotionally charged reactions (see Fees, Exploitation, and Confusion Hammer Investors).

Although myopic short-termism is not the solution, extending time horizons too long does no good for investors either. As economist John Maynard Keynes astutely noted, “In the long run we are all dead.” But surely bloggers and pundits alike could provide perspectives in multiple year timeframes, rather than in multiple hours. Investors would be served best by turning off the TV, PC, or cell phone, and using the resulting free time to read a good book about the virtues of patient investing from successful long-term investors. Stuffing cash under the mattress, parking it in a 0.5% CD, or panicking into sub-2% Treasuries probably is not going to get the job done for your whole portfolio when inflation, longer life expectancies, and the unsustainable trajectory of entitlements destroy the value of your hard-earned nest egg.

Investment Commentators Look into Politician Mirror

Heading into a heated election year with volatility reaching historic heights in the financial markets, both politicians and investment commentators have garnered a great deal of the media spotlight. With the recent heightened interest in the two fields, some common characteristics between politicians and investment commentators have surfaced. Here are some of the similarities:

- Politicians have a short-term incentives to get re-elected and not get fired, even if there is an inherent conflict with the long-term interest of their constituents; Investment commentators have a short-term incentives to follow the herd and not get fired, even if there is an inherent conflict with the long-term interest of their constituents;

- Many politicians have extreme views that conflict with peers because blandness does not get votes; Many investment commentators have extreme views that conflict with peers because blandness does not get votes;

- Many politicians lack practical experience that could benefit their followers, but the politicians have the gift of charisma to mask their inexperience; Many investment commentators lack practical experience that could benefit their followers, but the commentators have the gift of charisma to mask their inexperience;

Investing has never been so difficult, and also has never been so important, which behooves investors to carefully consider portfolio actions taken based on a very volatile and inconsistent opinions from a group of bloggers, economists, strategists, columnists, and various other media commentators. Investors are bombarded with an avalanche of ever-changing daily data, much of which is irrelevant and should be ignored by long-term investors. As you weigh the precious value of your political votes in the upcoming election season, I urge you to back the candidates that represent your long-term interests. With regard to the financial markets, I also urge you to back the investment commentators that support your long-term interests – the success of your financial future depends on it.

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds, and GOOG, but at the time of publishing SCM had no direct position in Facebook, Twitter, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page

The Curious Case of Gen Y and Benjamin Button

If a current Gen Y-er aged backwards like Benjamin Button, he would feel right at home when it comes to investing, because acute conservatism and risk aversion have struck older and younger generations alike. The Curious Case of Benjamin Button is a story that follows the critical peaks and valleys of a boy born in his eighties, who immediately begins to reverse the aging process. Investors of all ages have suffered their peaks and valleys over the last decade, and these experiences have impacted investing attitudes and perceptions heavily during the prime earning years. For retirees, it’s virtually impossible for extreme events like the Great Depression, World War II, Vietnam, Kennedy’s assassination, and Nixon’s impeachment to NOT have had an influence on individuals’ investing behavior.

Investing Consequences on Younger Investors

If a younger Mr. Button were still alive today, there is no doubt the disheartening events experienced in his 80s would only become reinforced by the bleak occurrences in 2008-2009. His reverse aging would not only have allowed him to witness the collapse of Lehman Brothers, but also behold the demise and bailout of other gargantuan financial institutions. Today, if Benjamin wasn’t busy watching the MTV Video Music Awards, he would most likely be diligently managing his bullet-proof portfolio of cash, CDs (Certificates of Deposit), Treasury bills, and maybe some tax-free municipals if he was feeling a little spunky.

The cautious stance of youthful savers was confirmed in a recent study conducted by Merrill Lynch Global Wealth Management. The report demonstrates how the recent financial crisis has had a severe dampening impact on the risk appetites of 18-34 year old “Millennials.” So dramatic an effect was the recession, the nervous conservatism experienced by the 30-somethings was only rivaled by fear from 65 year olds. In fact, the 56% of young investors, who were more cautious today than a year ago, was the highest percentage registered by any age group.

Here’s what Christopher Geczy adjunct associate professor of finance at University of Pennsylvania’s Wharton School had to say about younger Millennials:

“We’re coming off a series of financial crises that hit this young generation at points in their lives where external events shape strong opinions…Many of them have witnessed a decline in the wealth of their families and seen their parents delay retirement or even return to the workforce.”

Beyond witnessing the challenges faced by their parents, the Millennials are encountering their own obstacles – such as joblessness. For those workers under age 35, the unemployment rate in August stood at more than 13% – significantly higher than the 9.6% national rate.

Note to Youths: Stocks for the Long Haul

In the typical life cycle of investing, investors flaunt a higher risk tolerance in their younger years and exhibit more risk aversion as they approach or enter retirement. Historically, this makes perfect sense because workers earlier in their careers have plenty of time to ride out the fluctuations associated with owning equities. Jeremy Siegel, professor at the Wharton University Professor, says stocks significantly outperform bonds by 6% per year over longer timeframes (see Siegel Digs in Heels).

For Gen Y-ers the larger risk is being too conservative, not too aggressive. Barry Nalebuff, a strategy professor at Yale’s School of Management agrees:

“The biggest risk for this generation is that they’ll live too long. With medical breakthroughs, the reality is that many of them will live beyond 100…The only way they have enough assets to last them is to invest in stocks. If they don’t, a lot of people will have to keep working way past when they want to because they won’t have enough money saved up.”

Even for those downbeat on the domestic equity markets – rightfully so with no price gains achieved over the last decade – younger investors should not lose sight of the tremendous equity opportunities available internationally (see the Blowing the Perfect Investment Game).

For many people, reverse aging may be fun for a while, but for Benjamin Button, living through the Great Depression and multiple wars as an adult would likely dampen the mood and increase risk aversion dramatically. Millennials have persevered through difficult times too. Generation Y has survived two recessionary bubbles caused by excessive technology spending and consumer credit binging, both over a short timeframe. Becoming too conservative for these investors will feel comfortable in the short-run if uncertainty continues to prevail. But investing now with adequate, diversified equity exposure is the prudent course of action. Even a wrinkly Benjamin Button could agree, wisely investing in some equities during your earlier career sure beats working as a Wal-Mart (WMT) greeter into your 80s.

Read the full Money-CNN and Newsweek articles on the subject

Wade W. Slome, CFA, CFP®

Plan. Invest. Prosper.

DISCLOSURE: Sidoxia Capital Management (SCM) and some of its clients own certain exchange traded funds and WMT, but at the time of publishing SCM had no direct position in BAC/Merrill, Lehman, or any other security referenced in this article. No information accessed through the Investing Caffeine (IC) website constitutes investment, financial, legal, tax or other advice nor is to be relied on in making an investment or other decision. Please read disclosure language on IC “Contact” page.

Building Your Financial Future – Mistakes Made in Investment Planning

Building Your Dream Future Requires a Plan

Building your retirement and financial future can be likened with the challenge of designing and building your dream home. The tools and strategies selected will determine the ultimate cost and outcome of the project.

I constantly get asked by investors, “Wade, is this the bottom – is now the right time to get in the markets?” First of all, if I precisely knew the answer, I would buy my own island and drink coconut-umbrella drinks all day. And secondarily, despite the desire for a simple, get-rich quick answer, the true solution often is more complex (surprise!). If building your financial future is like designing your dream home, then serious questions need to be explored before your wealth building journey begins:

1) Do I have enough money, and if not, how much money do I need to develop my financial future?

2) Can I build it myself, or do I need the help of professionals?

3) Do I have contingency plans in place, should my circumstances change?

4) What tools and supplies do I need to effectively bring my plans to life?

Most investors I run into have no investment plan in place, do not know the costs (fees) of the tools and strategies they are using, and if they are using an advisor (broker) they typically are in the dark with respect to the strategy implemented.

For the “Do-It-Yourselfers”, the largest problem I am witnessing right now is excessive conservatism. Certainly, for those who have already built their financial future, it does not make sense to take on unnecessary risk. However, for most, this is a losing strategy in a world laden with inflation and ever-growing entitlements like Medicare and Social Security. There’s clearly a difference between stuffing money under the mattress (short-term Treasuries, CDs, Money Market, etc.) and prudent conservatism. This is a credo I preach to my clients.

In many cases this conservative stance merely compounds a previous misstep. Many investors undertook excessive risk prior to the current financial crisis – for example piling 100% of investment portfolios into five emerging market commodity stocks.

What these examples prove is that the average investor is too emotional (buys too much near peaks, and capitulates near bottoms), while paying too much in fees. If you don’t believe me, then my conclusions are perfectly encapsulated in John Bogle’s (Vanguard) 1984-2002 study. The analysis shows the average investor dramatically underperforming both the professionally managed mutual fund (approximately by 7% annually) and the passive (“Do Nothing”) strategy by a whopping 10% per year.

Building your financial future, like building your dream home, requires objective and intensive planning. With the proper tools, strategies and advice, you can succeed in building your dream future, which may even include a coconut-umbrella drink.

Your Investment Car Needs Shocks

Smooth Out the Bumpy Ride

Investing can make for a bumpy ride. What can investors do to smooth out the rough financial journey? The simple answer: diversification. If you consider your investment portfolio as a car, then the process of diversification acts like shock absorbers. Those shocks make for a more comfortable ride while preventing potential disasters – like accidentally driving your investments off a cliff.

People generally understand the concept behind, “not putting all your eggs in one basket.” However, once introduced to financial theory terms such as correlation, covariance, and the efficient frontier, people’s eyes begin to glaze over…and rightfully so!

So what are some of the key points one should understand regarding diversification:

- Lunch CAN Be Free! There are very few free lunches in life, but with “diversification” you can indeed get something for nothing. For example, let’s assume you are approached with two investments, ski hats and sun visors, and each investment is expected to deliver a 5% annual return. Furthermore, let’s suppose that zero ski hats are sold in Spring and Summer (and zero sun visors in Fall and Winter). If you merely own one investment, that investment will be more risky (volatile) than a combo portfolio for half the year. Although any combination of two investments will create a 5% return, by diversifying (owning both investments), you can smooth out the ride. There’s your free lunch – the same return achieved for less risk (volatility)!

- Gravity Holds True For Investments Too! Nothing goes up forever, so do not concentrate your portfolio in sectors that have wildly outperformed other sectors/asset classes for long periods of time. Lessons learned over the last 10 years in the areas of technology and real estate highlight the dangers of over-exposure to any one sector in the economy.

- Vary Your Investment Diet! In the Oscar-nominated documentary Super Size Me, Morgan Spurlock decides to eat McDonald’s fast-food for breakfast, lunch, and dinner for thirty days. As a result, his cholesterol levels sky-rocket, he gains over 24 pounds, and his liver function deteriorates significantly. When it comes to your investment portfolio, you should balance it across a wide range of healthy options, including domestic and international stocks and bonds; large and small capitalization stocks; growth and value styles; cash and low-risk liquid investments; and alternative asset classes, such as real estate, commodities, and private investments.

The benefits of diversification will fluctuate under different economic climates. During our recent financial crisis, especially in late 2008, the correlation ratio (the degree that different asset classes move together) unfortunately was very high. However, those investors who were exposed to areas such as Treasury securities, gold, cash, and bonds generally fared better than those who did not. Subsequently, in the early part of 2009, the benefits of diversification shined through as outperformance in emerging markets, technology, consumer discretionary and growth stocks balanced the weakness suffered in banking, transportation, healthcare, bond and value segments.

Diversification helps on the rough roads of investing, so make sure to check those shocks!

{kind=link}

{kind=link}